Core Router Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.32 Billion |

| Market Size (2031) | USD 13.02 Billion |

| Growth Rate (2026 - 2031) | 6.91% CAGR |

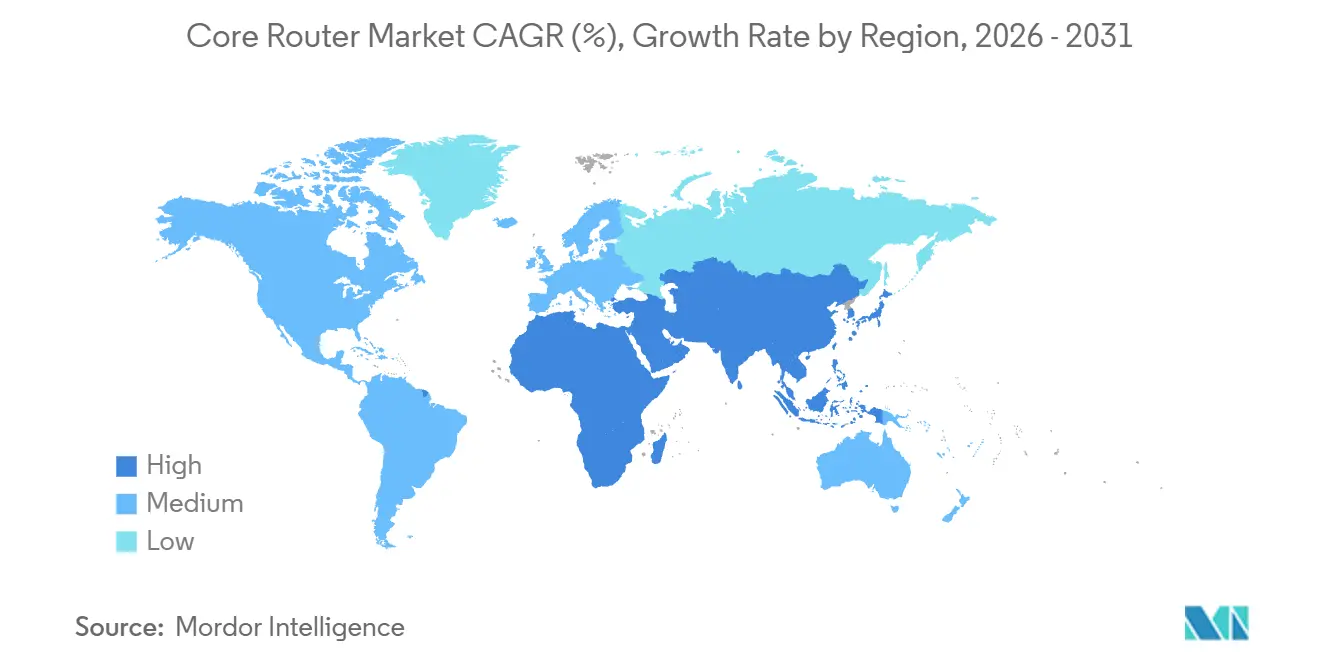

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Core Router Market Analysis by Mordor Intelligence

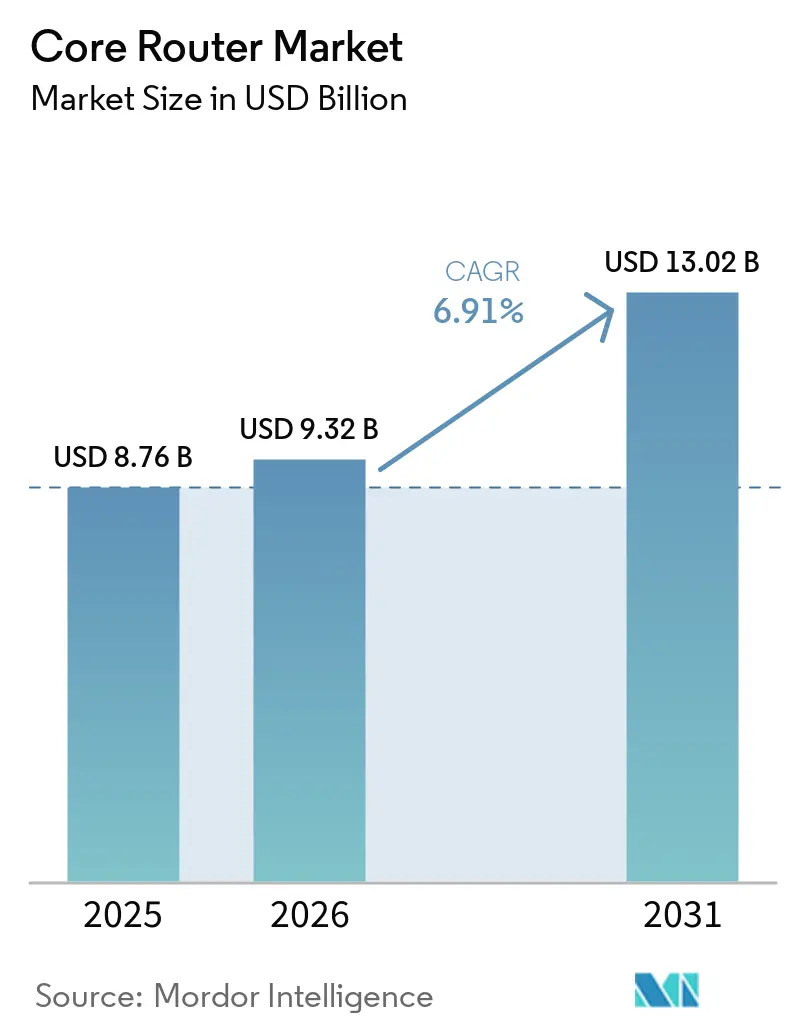

The core router market size reached USD 8.76 billion in 2025 and is expected to reach USD 9.32 billion in 2026 and USD 13.02 billion by 2031, growing at a CAGR of 6.91% from 2026 to 2031. Operators continue to replace legacy circuit-switched infrastructure with cloud-native packet cores, lifting demand for high-throughput, AI-aware routing platforms. Modular chassis systems still dominate, yet the accelerating shift toward white-box disaggregation is altering vendor economics and compressing hardware margins. Hyperscalers are standardizing on 800 Gbps Ethernet fabrics, and their record-high capital budgets are pulling the core router market toward ultra-high-density, lossless designs. Supply-chain tension in leading-edge ASICs remains the main short-term brake, but sustained cloud investment offsets delayed enterprise refresh cycles.

Key Report Takeaways

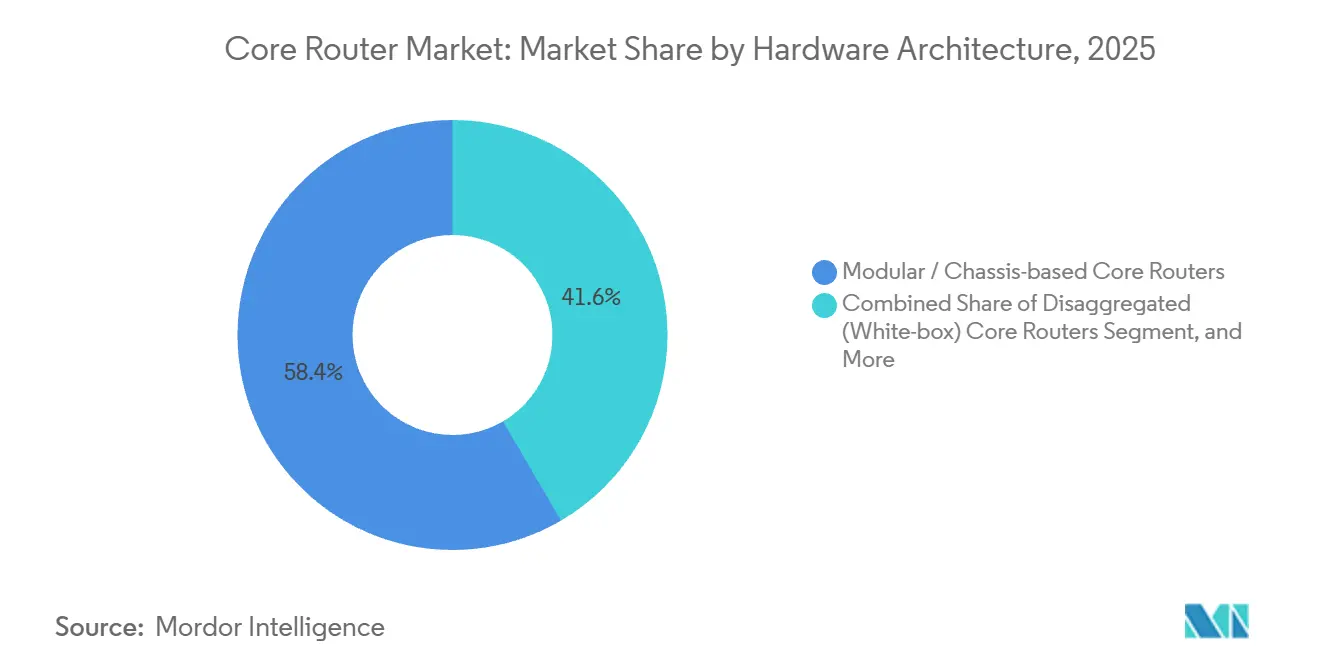

- By hardware architecture, modular chassis platforms led with 58.42% of the core router market share in 2025, while disaggregated white-box systems are projected to expand at an 8.94% CAGR through 2031.

- By throughput class, ultra-high platforms above 100 Gbps captured 62.18% of the core router market revenue share in 2025 and are forecast to grow at a 7.82% CAGR through 2031.

- By interface density, high-density systems with 256+ ports held a 54.27% share of the core router market in 2025, and this tier is advancing at a 7.36% CAGR across the forecast window.

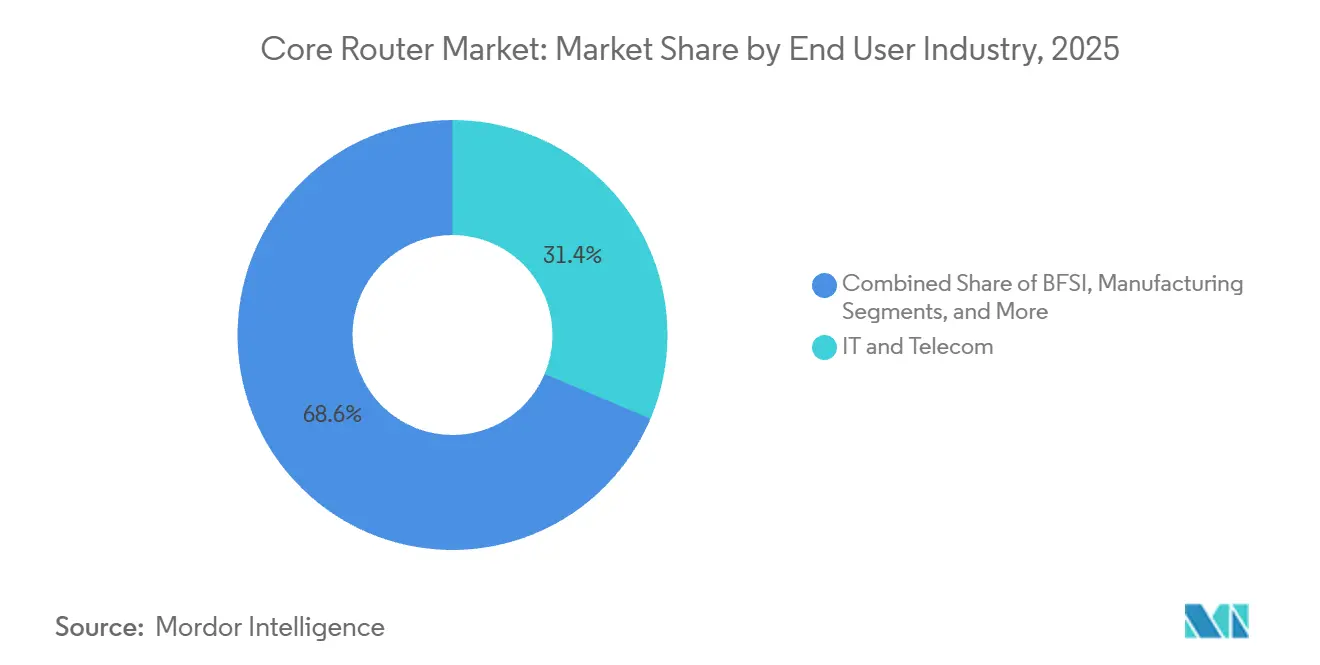

- By end-user industry, IT and telecom operators accounted for 31.36% of core router deployments in 2025 and are advancing at a 6.98% CAGR through 2031.

- By geography, North America led spending with a 36.22% share of the core router market in 2025, while Asia-Pacific is the fastest-growing region, with a 7.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Core Router Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising 5G Backbone Deployments | +1.80% | Global, early activity in Japan, South Korea, India | Medium term (2-4 years) |

| Hyperscale Data Center Expansion | +2.10% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Surge in AI-Driven Traffic Engineering | +1.50% | North America, Europe, Asia-Pacific core markets | Medium term (2-4 years) |

| Cloud Service Provider CAPEX Upswing | +1.20% | Global | Short term (≤ 2 years) |

| Adoption of Disaggregated Routing Architectures | +0.90% | North America, Europe, selective Asia-Pacific operators | Long term (≥ 4 years) |

| Sustainability-Focused Hardware Refresh Programs | +0.60% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising 5G Backbone Deployments

Operators are migrating from 4G packet cores to standalone 5G architectures that demand higher throughput, microservice granularity, and network slicing. SoftBank’s commercial SRv6 mobile user plane went live in December 2025, proving sub-10 ms latency on Jericho2 ASICs running ArcOS. KDDI followed with a nationwide Samsung 5G SA core that delivers geo-redundant failover for gaming and robotics workloads. Ericsson’s March 2026 deal with SoftBank adds dual-mode 5G core functions and subscriber data consolidation, increasing packet-processing loads on backbone routers.[1]Ericsson News, “Ericsson to Expand and Modernize SoftBank Core Network,” ericsson.com Containerized network functions amplify east-west traffic inside data centers, accelerating slot upgrades on spine routers. The cascading impact keeps 5G transport among the most material growth levers for the core router market.

Hyperscale Data Center Expansion

Alphabet budgeted USD 175 billion-USD 185 billion for 2026 infrastructure, and combined hyperscaler outlays top USD 690 billion, underwriting hundreds of new availability zones. Arista’s R4 chassis offers 576 ports of 800 Gbps and HyperPort 3.2 Tbps interfaces that trimmed AI job time by 44% in lab tests.[2]Arista Networks, “Arista R4 Product Family,” arista.com Huawei’s CloudEngine XH9230-128DQ-LC fixed switch pushes 51.2 Tbps using full liquid cooling, doubling rack utilization. These platforms lower power per bit, meeting stringent PUE targets while sustaining GPU cluster growth. As workloads centralize into mega-campuses, high-density core routers become critical aggregation points, propelling the core router market toward terabit fabrics.

Surge in AI-Driven Traffic Engineering

Machine learning optimizes path selection, anticipating congestion and re-routing flows in real time. Cisco’s Intent-Powered Fabric, anchored by Silicon One P200 and G300 ASICs, uses streaming telemetry to reroute before packet drops occur. Juniper’s Routing Director applied reinforcement learning in SoftBank field trials, cutting manual interventions and improving repair time. Microsoft Research showed AI-guided SRv6 trimming tail latency by 30% across its WAN. By extracting 15-20% more capacity from existing fiber, operators defer new builds, freeing budget for strategic chassis refreshes. The ROI advantage keeps AI analytics a growing catalyst for the core router market.

Cloud Service Provider CAPEX Upswing

Hyperscalers monetize incremental bandwidth through usage-based models, making backbone upgrades a repeatable line item in the budget. Telefónica España chose Nokia SR and IXR gear for 17 edge data centers to support AI inference at metro proximity. Rakuten Mobile’s multi-vendor 5G SA architecture runs Cisco, Nokia, and F5 functions on white-box servers, raising throughput pressure on aggregation routers. These use cases illustrate why cloud CAPEX is less cyclical than enterprise budgets, ensuring the core router market continues to compound even when other IT segments pause spending.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Expenditure | -1.3% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Supply-Chain Volatility in High-Speed ASICs | -1.1% | Global | Short term (≤ 2 years) |

| Skills Gap in Programmable Networking | -0.5% | Global, pronounced in Asia-Pacific and Africa | Medium term (2-4 years) |

| Long Depreciation Cycles Limiting Refresh Rates | -0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure

Chassis with 800 Gbps interfaces list above USD 1 million, and optics, redundant PSUs, and support contracts amplify lifetime cost. Regional carriers delay upgrades until regulatory mandates or service degradation override budget caution. Indian payments networks cut total cost by 40% after shifting to SONiC white-box routers, and Rakuten Mobile halved CAPEX with disaggregated hardware, yet smaller operators lack the engineering staff to integrate multivendor stacks.[3]Open Networking Foundation, “SONiC Deployment Case Studies,” opennetworking.org Consequently, many mid-tier providers still order integrated systems, muting unit volume growth across the core router market.

Supply-Chain Volatility in High-Speed ASICs

AI GPUs and router ASICs share the same bleeding-edge process nodes, and TSMC has allocated 60% of 2026 N3 capacity to AI chips, projected to reach 86% in 2027. PCB substrate lead times stretched from 6 weeks to 6 months, while coherent-optics laser shortages are delaying 800 Gbps module deliveries. Scarcity grants chip vendors pricing power, compressing router OEM margins and forcing staged deployments aligned with component availability. The bottlenecks slow shipment velocity, tightening near-term expansion in the core router market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hardware Architecture: Disaggregation Challenges Modular Dominance

Modular chassis platforms captured 58.42% of the core router market share in 2025 through field-replaceable line cards, redundant control planes, and mature failover software. The core router market size for these chassis benefited from decades-long refresh cycles among incumbent telcos that value proven availability benchmarks. Their embedded telemetry and carrier-grade clocking simplify compliance in regulated environments. However, cost-per-bit metrics favor merchant-silicon white-box devices.

Disaggregated routers are expanding at an 8.94% CAGR as AT&T’s backbone now moves more than 80% of its 840 PB daily load on DriveNets software running across generic ASICs. Comcast and KDDI are replicating this model, and SONiC has become the de facto operating system for hyperscaler-style deployments. Although initial systems integration remains complex, successful reference builds are reducing perceived risk. As hyperscalers open-source toolchains, service providers gain confidence, sustaining momentum for disaggregation within the core router market.

By Throughput Class: Ultra-High Tier Sets the Pace

Ultra-high-throughput routers exceeding 100 Gbps commanded 62.18% of market revenue in 2025 and will grow at a 7.82% CAGR through 2031, driven by AI cluster back-end networks, DCI links, and 5G user-plane gateways. Cisco’s Silicon One G300 enables 25.6 Tbps fabrics, letting operators collapse three-tier topologies into two layers for latency-critical workloads. Juniper's PTX12000 modular router, deployed by KPN in the Netherlands for 800 Gbps coherent transport, uses Nokia's FP5 photonic processor to achieve a 75% per-bit power reduction compared with prior generations, directly addressing sustainability mandates from European regulators.

High-throughput platforms above 10 Gbps but below 100 Gbps continue to serve enterprise campus cores and regional aggregation points, yet their share is eroding as operators consolidate traffic onto fewer, higher-capacity devices to reduce operational complexity and footprint. Mid-range platforms in the 10-100 Gbps span still serve campus cores, yet their share erodes as operators consolidate onto fewer ultra-high-capacity nodes. Low tiers linger in industrial IoT or rural backhaul. With QSFP-DD800 optics in volume and liquid-cooled 1.6 Tbps modules on the roadmap, the ultra-high segment will continue guiding technology direction and grabbing wallet share inside the core router market.

By End User Industry: Telcos Remain the Revenue Anchor

IT and telecom operators accounted for 31.36% of core router deployments in 2025 and will sustain 6.98% growth through 2031 as they modernize backbone networks to support 5G standalone, cloud-native packet cores, and AI-driven traffic engineering. Wind Tre’s seven-year modernization contract with Ericsson consolidates Italian data centers from 18 to 12, embeds dual-mode 5G core functions, and increases demand for terabit routers. Private-cloud banking and trading platforms buy high-assurance chassis, but volumes are modest compared with telcos.

Manufacturing, healthcare, and public sectors deploy edge routers for IoT and imaging, typically at lower throughput grades that have a limited effect on the aggregate core router market size. Government research networks procure encrypted systems that meet sovereign manufacturing requirements, sustaining a niche for trusted supply-chain vendors. Despite vertical diversification, telcos will stay the primary demand pillar through 2031.

By Interface Density Class: Port Counts Drive Consolidation

High-density routers exceeding 256 ports captured 54.27% of market share in 2025 and will expand at 7.36% CAGR as operators consolidate point-of-presence sites and adopt pluggable 800 Gbps optics to reduce footprint and power consumption. Huawei's CloudEngine XH16800 modular series, unveiled at MWC Barcelona 2026, scales to 768 ports of 800 Gbps Ethernet in a single chassis and integrates the Xinghe AI Fabric 2.0 architecture, which uses Network Packet Load Balancing and Network Stream Load Balancing to optimize GPU cluster traffic and reduce job completion time.[4]Huawei, “Xinghe AI Fabric 2.0 Solution,” huawei.com

Arista’s 7800R4 offers 36-port line cards, curbing cabling complexity and freeing rack space. Medium tiers (64-256 ports) address regional hubs, yet operators increasingly over-provision port count to delay the next chassis purchase. Low-density devices remain relevant at the customer edge but contribute little to overall revenue. With XPO liquid-cooled pluggable optics delivering 12.8 Tbps per module, operators can fit 204.8 Tbps in a single OCP rack unit, strengthening the high-density pull on the core router market.

Geography Analysis

North America generated 36.22% of 2025 spending as hyperscaler capital programs and Open RAN pilots absorbed vast port volumes. Alphabet, Microsoft, Amazon, and Meta together earmarked nearly USD 690 billion for 2026 infrastructure builds, funneling orders to high-bandwidth chassis with 800 Gbps interfaces. AT&T’s nationwide DriveNets rollout shows the region’s early adoption of disaggregated software stacks. Rural carriers, such as GCI in Alaska, outsource dual-mode 5G core operations to Ericsson, accelerating deployments despite harsh climates.

Asia-Pacific is the fastest-growing territory at a 7.88% CAGR. SoftBank’s SRv6 launch illustrates Japan’s appetite for advanced routing protocols. KDDI’s DriveNets partnership underscores broader acceptance of open architectures.[5]Calcalist Tech, “KDDI and DriveNets Sign Strategic Deal,” calcalistech.com India’s HFCL contract with Vodafone Idea expands 10 Gbps nodes to 100 Gbps without chassis swaps, highlighting cost-sensitive innovation. Chinese hyperscalers are erecting AI mega-clusters that demand lossless Ethernet fabrics, while South Korean telcos deploy 5G SA slicing for autonomous vehicles.

Europe advances steadily as energy-efficiency legislation, 5G SA upgrades, and edge data center rollouts unfold. Wind Tre’s network consolidation and Nokia’s exclusive deal with Telefónica España exemplify the move toward ultra-low-latency regional facilities. The Middle East invests in fiber backhaul to meet smart-city targets, and Africa’s modernization agreements, such as Ethio-Ericsson’s March 2026 project, extend 4G/5G coverage to underserved populations. Latin America widens 5G coverage in Brazil and Argentina, albeit under tighter macro constraints, leaving North America and Asia-Pacific as the twin engines of volume for the core router market.

Competitive Landscape

The core router market is moderately concentrated. Cisco, Juniper, Huawei, and Nokia retain incumbent positions thanks to integrated hardware and software, extensive support contracts, and certified lifecycles. DriveNets crossed USD 1 billion in 2025 bookings and turned cash-flow positive, validating a software-only model that scales across merchant-silicon white boxes. Arista’s R4 family marries 800 Gbps density with 3.2 Tbps HyperPorts, targeting AI back-end fabrics that prize deterministic latency.

Incumbents counter by embedding AI-driven operations, bundling security, and offering managed services. Ericsson’s Core Build and Operate agreement in Alaska hands daily administration to the vendor, giving the operator cost predictability. Huawei’s Xinghe AI Fabric 2.0 reduces service recovery time from 90 minutes to 15 minutes via automated rerouting, positioning the company for AI-era data center wins. The MANRS equipment vendor program, founded by Arista, Cisco, Huawei, Juniper, and Nokia, standardizes anti-hijack features, raising the cybersecurity watermark and creating a compliance hurdle for newcomers.

Open-source NOS projects lower entry barriers, attracting ODM hardware suppliers and cloud-native software specialists. Edgecore and Quanta build white-box chassis around Broadcom and Marvell ASICs, while RtBrick offers carrier-grade BNG and full-stack routing on disaggregated gear. Skills shortages in P4 and eBPF telemetry slow mass adoption, but vendors are rolling out certification tracks and reference designs. As telcos gravitate toward consumption-based pricing and operational outsourcing, service differentiation will hinge increasingly on automation depth rather than raw port speed, reshaping competitive dynamics inside the core router market.

Core Router Industry Leaders

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

Nokia Corporation

ZTE Corporation

Arista Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Ericsson signed a multi-year framework with SoftBank to modernize Japan’s core network, adding cloud-native dual-mode 5G core and integrated automation.

- March 2026: Arista announced the XPO agreement for liquid-cooled 12.8 Tbps pluggable optics, quadrupling rack-unit density for AI fabrics.

- March 2026: Wind Tre selected Ericsson for a seven-year modernization that consolidates data centers and deploys dual-mode 5G core with Release 17 features.

- February 2026: Nokia became Telefónica España’s exclusive networking partner for 17 edge data centers, supplying 7220 IXR and 7750 SR platforms.

Global Core Router Market Report Scope

The core router market refers to the revenue generated from high-capacity routing systems deployed at the backbone of telecom networks, internet infrastructure, and large-scale data centers to manage and transport massive volumes of data traffic across long distances. Core routers are designed to operate at the highest levels of network hierarchy, handling high-throughput, low-latency data transmission between aggregation layers, data centers, and global internet exchange points.

The Core Router Market Report is Segmented by Hardware Architecture (Fixed Core Routers, Modular/Chassis-based Core Routers, and Disaggregated (White-box) Core Routers), Throughput Class (Low Throughput, Mid Throughput, High Throughput, and Ultra-High), End User Industry (BFSI, IT and Telecom, Manufacturing, Government and Public Sector, Healthcare and Lifesciences, Retail and E-commerce, Education, and Other End User Industries), Interface Density Class (Low Density, Medium Density, and High Density), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Fixed Core Routers |

| Modular / Chassis-based Core Routers |

| Disaggregated (White-box) Core Routers |

| Low Throughput (<1 Gbps) |

| Mid Throughput (1-10 Gbps) |

| High Throughput (10-100 Gbps) |

| Ultra-High (>100 Gbps) |

| BFSI |

| IT and Telecom |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Education |

| Other End User Industries |

| Low Density (<64 ports) |

| Medium Density (64–256 ports) |

| High Density (>256 ports) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Hardware Architecture | Fixed Core Routers | |

| Modular / Chassis-based Core Routers | ||

| Disaggregated (White-box) Core Routers | ||

| By Throughput Class | Low Throughput (<1 Gbps) | |

| Mid Throughput (1-10 Gbps) | ||

| High Throughput (10-100 Gbps) | ||

| Ultra-High (>100 Gbps) | ||

| By End User Industry | BFSI | |

| IT and Telecom | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Healthcare and Lifesciences | ||

| Retail and E-commerce | ||

| Education | ||

| Other End User Industries | ||

| By Interface Density Class | Low Density (<64 ports) | |

| Medium Density (64–256 ports) | ||

| High Density (>256 ports) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the core router market in 2026?

The core router market size is estimated at USD 9.32 billion in 2026, on track to reach USD 13.02 billion by 2031, according to Mordor Intelligence.

Which hardware architecture leads global deployments?

Modular chassis systems led with 58.42% of 2025 revenue, although disaggregated white-box platforms are the fastest-growing at an 8.94% CAGR to 2031.

Which region is growing fastest through 2031?

Asia-Pacific shows the highest growth, projected at a 7.88% CAGR as Japan, India, and South Korea upgrade 5G backbones and build AI-ready data centers.

What throughput class captures most spending?

Ultra-high routers above 100 Gbps held 62.18% of 2025 revenue and are expanding at a 7.82% CAGR due to AI clusters and hyperscale DCI requirements.

How is 5G affecting core router upgrades?

Standalone 5G cores require higher throughput and network slicing, driving telcos to replace legacy MPLS gear with AI-enabled, 800 Gbps-capable routers.

Page last updated on: