4G/5G Cellular Router Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

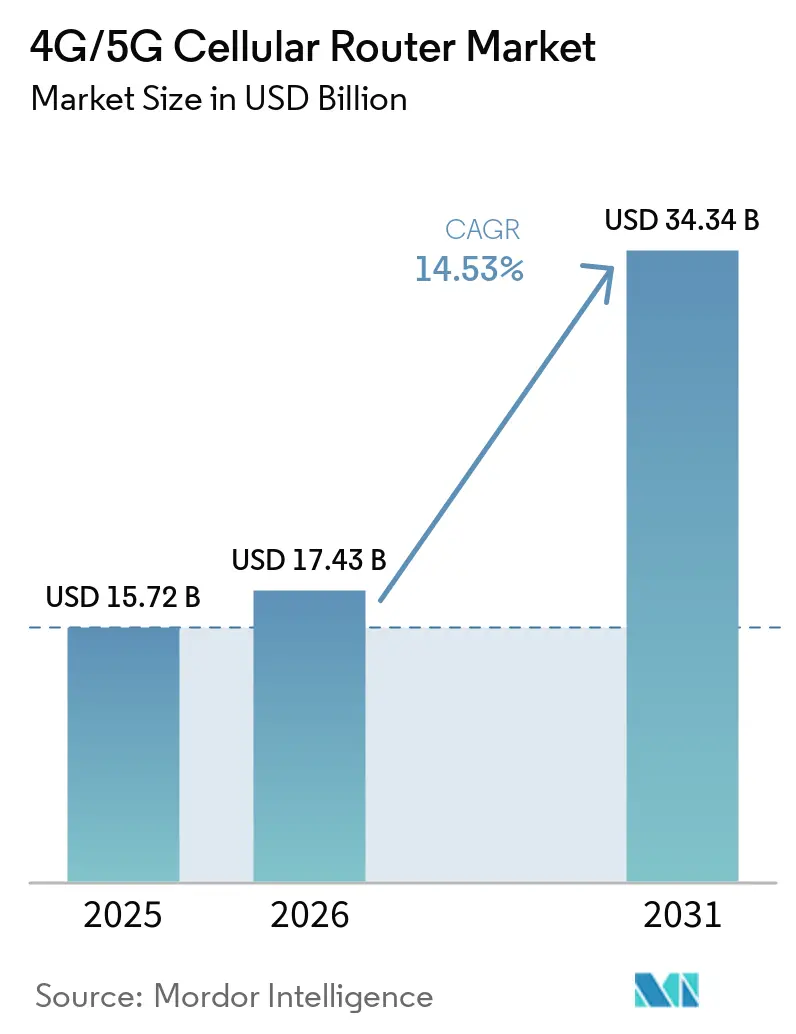

| Market Size (2026) | USD 17.43 Billion |

| Market Size (2031) | USD 34.34 Billion |

| Growth Rate (2026 - 2031) | 14.53% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

4G/5G Cellular Router Market Analysis by Mordor Intelligence

The 4G/5G cellular router market size is expected to grow from USD 15.72 billion in 2025 to USD 17.43 billion in 2026 and is forecast to reach USD 34.34 billion by 2031 at a 14.53% CAGR over 2026-2031. Robust investment in private wireless networks, edge-compute architectures, and fixed wireless access installations is redefining enterprise connectivity. Manufacturers that operate autonomous guided vehicles and time-sensitive quality-vision systems are bypassing legacy Wi-Fi and campus LANs, choosing 5G standalone cores paired with rugged routers that embed IEEE 802.1Qbv traffic scheduling. National broadband programs from India’s BharatNet to Brazil’s population-coverage mandate now specify cellular backhaul where trenching fiber exceeds USD 100 per meter. Meanwhile, operators in harmonized C-band markets are scaling fixed wireless access at gross margins above 60 percent, accelerating demand for customer-premises equipment and outdoor rugged units. Taken together, these shifts explain why the 4G/5G cellular router market is moving from cost-focused deployments toward performance-centric designs that support traffic shaping, dual-SIM resilience, and containerized edge workloads.

Key Report Takeaways

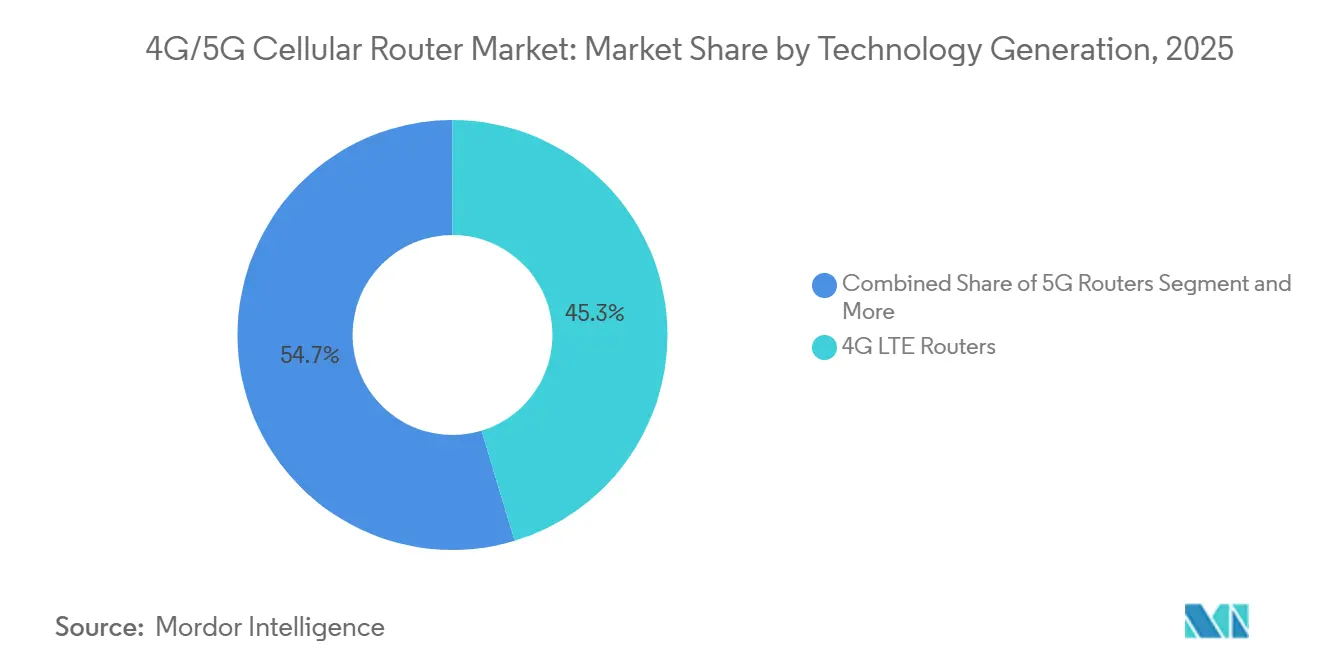

- By technology generation, 4G LTE routers commanded 45.32% of 4G/5G cellular router market share in 2025, while 5G routers are advancing at an 18.44% CAGR through 2031.

- By end-user industry, manufacturing led with 32.84% revenue share in 2025, whereas public safety and emergency services are forecast to expand at a 16.21% CAGR to 2031.

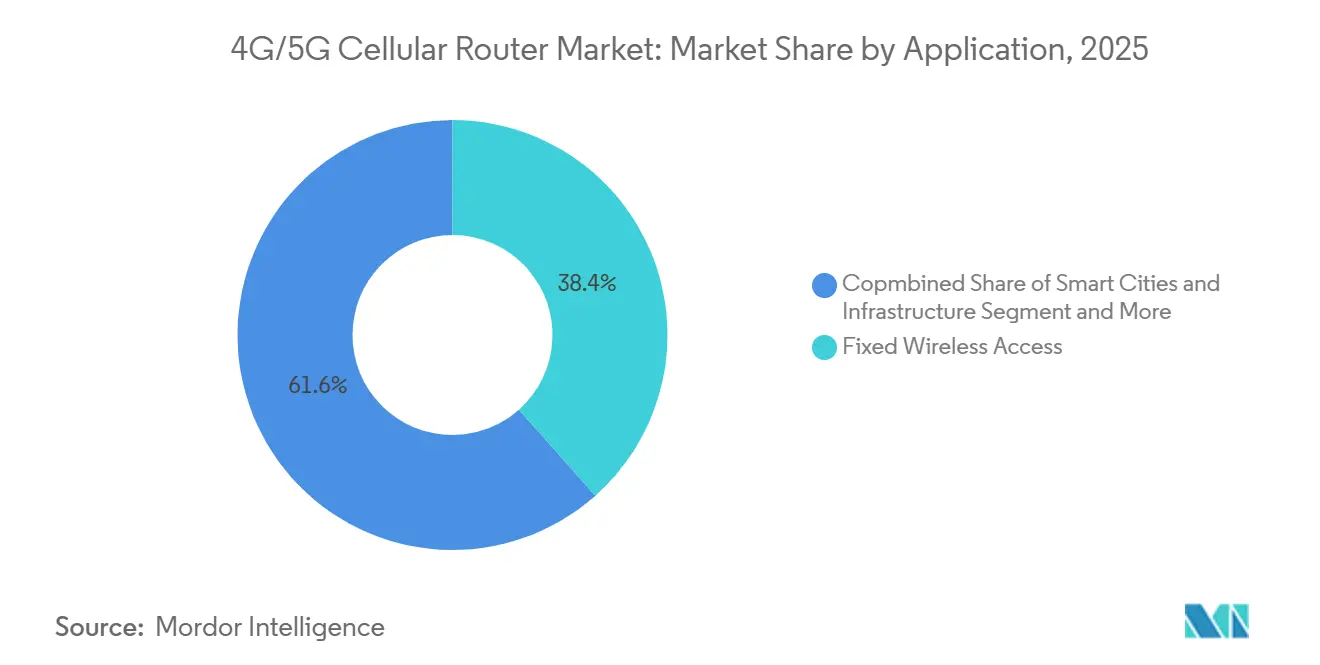

- By application, fixed wireless access accounted for 38.43% of the 4G/5G cellular router market in 2025, and smart cities and infrastructure are growing at a 16.92% CAGR over 2026-2031.

- By form factor, indoor CPE devices captured 41.63% of the 4G/5G cellular router market in 2025, and edge-compute routers are projected to grow at an 18.71% CAGR between 2026 and 2031.

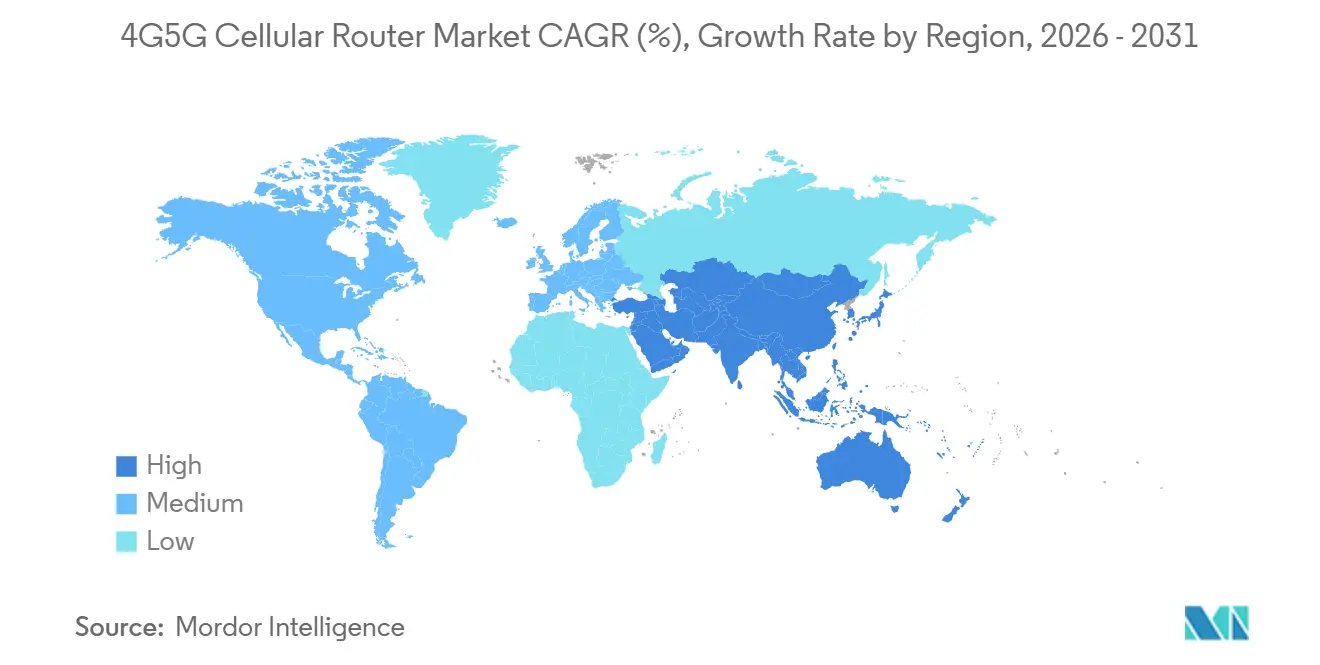

- By geography, North America captured 34.89% of the 4G/5G cellular router market in 2025, while Asia-Pacific is forecast to grow at a 17.84% CAGR through 2031,

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 4G/5G Cellular Router Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring Private 5G Network Deployments in Manufacturing | +3.8% | Global, early concentration in Germany, United States, Japan, South Korea | Medium term (2-4 years) |

| Rising Demand for Fixed Wireless Access in Rural Broadband | +3.2% | North America, Europe, India, Brazil, Sub-Saharan Africa | Short term (≤ 2 years) |

| Edge-Compute Enabled Routers for Predictive Maintenance | +2.6% | Global, led by automotive and process industries in Germany, United States, China | Medium term (2-4 years) |

| Dual-SIM Fail-over Becoming Mandatory for Business Continuity | +1.9% | Global, especially financial services and healthcare in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Government Incentives for Domestic Router Production | +1.5% | United States, European Union, India, China | Long term (≥ 4 years) |

| AI-Based Traffic Optimization Enhancing Router Value Proposition | +1.3% | Global, early adoption in smart cities and industrial automation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Soaring Private 5G Network Deployments in Manufacturing

Manufacturers are deploying private 5G networks to achieve deterministic latency for robotic assembly lines, automated guided vehicles, and augmented reality work instructions. Industrial-grade routers supporting network slicing and IEEE 802.1AS time synchronization now anchor these deployments, ensuring round-trip latency below 10 milliseconds. Jaguar Land Rover’s Halewood plant connected more than 200 devices over a private 5G network, validating time-sensitive networking for real-time quality inspection. NTT DATA and Celanese implemented multi-site private 5G deployments, prioritizing edge compute routers capable of running anomaly-detection models locally to reduce reliance on backhaul. Cargill plans to equip 50 food processing plants with private 5G by 2027, using dual SIM routers with LTE fallback for redundancy. Standards evolution, such as IEC 61158, now incorporates time-sensitive networking over 5G, accelerating integration of sub-microsecond clock synchronization in routers.[1]Ericsson, “Ericsson and Jaguar Land Rover Deploy Private 5G at Halewood Plant,” ericsson.com

Rising Demand for Fixed Wireless Access in Rural Broadband

Fixed wireless access has emerged as the lowest-cost path to universal broadband when fiber construction costs exceed USD 100 per meter. U.S. operators AT&T and Verizon served a combined 8 million fixed wireless access subscribers by early 2026, delivering a median throughput of 200 to 300 Mbps through mid-band spectrum aggregation. India’s BharatNet connected more than 214,000 gram panchayats, yet relies on 5G routers to bridge the final 500 to 1,000 meters in sparsely populated villages. Brazil has mandated 80% population coverage by the end of 2026, compelling carriers to deploy outdoor rugged routers that withstand tropical humidity and temperatures. Zain KSA’s introduction of an eSIM-capable Nokia FastMile router illustrates how remote provisioning reduces operational costs in hard-to-reach areas.[2]AT&T, “Fixed Wireless Access Subscriber Statistics,” att.com

Edge-Compute Enabled Routers for Predictive Maintenance

Industrial operators are consolidating gateways, programmable logic controllers, and cellular modems into single-edge compute routers that run containerized analytics. Teltonika’s RUT and TRB families integrate quad-core ARM processors and 4 GB RAM, enabling vibration analysis workloads via Docker on the device. Nokia’s Industrial Edge combines 5G routers with Kubernetes orchestration, enabling predictive models to execute within 10 milliseconds of sensor acquisition. Robustel’s R5020 series supports TensorFlow Lite and ONNX runtimes, allowing factories to deploy local inference without consuming WAN bandwidth. The ITU’s Y.4235 specification formalizes edge-processing functions for power-grid IoT devices, accelerating adoption across utilities.[3]Teltonika Networks, “Edge-Compute Router Families and Product Launches,” teltonika-networks.com

Dual-SIM Fail-over Becoming Mandatory for Business Continuity

High-profile network outages have led enterprises to reassess single-carrier architectures due to revenue risk exposure. A 2024 incident disrupted more than 15,000 retail point of sale terminals for six hours, accelerating the adoption of dual SIM router configurations across the finance and healthcare sectors. Cradlepoint’s NetCloud automatically switches carriers when packet loss or latency thresholds are exceeded. Digi International’s TX64 5G Rail router distributes traffic across two operators while maintaining EN 50155 compliance for railway environments. Release 17 of 3GPP further supports this shift by enabling simultaneous slices for mission-critical and best-effort traffic across separate carriers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Investment and Total Cost of Ownership | -2.1% | Global, acute in SMEs across emerging markets | Short term (≤ 2 years) |

| Fragmented Spectrum Regulations Across Regions | -1.7% | Global, pronounced in United States, Europe, Asia-Pacific | Medium term (2-4 years) |

| Cyber-Security and Data-Privacy Concerns | -1.2% | Global, heightened in European Union and United States | Medium term (2-4 years) |

| Skilled Workforce Shortage for 5G Networking | -0.9% | Global, severe in North America, Western Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Investment and Total Cost of Ownership

Enterprise-grade 5G routers with edge-compute modules can cost over USD 2,000 each, a barrier for small and medium enterprises operating on capital-expenditure budgets below USD 50,000. A mid-sized logistics fleet needs 50 routers, costing up to USD 150,000 in hardware and USD 30,000 annually for cloud-management subscriptions. Dual-carrier SIM plans add USD 40-60 per device each month, swelling operational expenses. Router-as-a-service models that amortize hardware over multi-year contracts exist, yet penetration remains below 20 percent outside North America and Western Europe.[4]European Commission, “EU Chips Act and 5G Spectrum Allocations,” ec.europa.eu

Fragmented Spectrum Regulations Across Regions

Inconsistent spectrum regulations force vendors to design region specific SKUs, extending product development cycles by 6 to 12 months and increasing R and D costs. The FCC’s Citizens Broadband Radio Service allows shared access in the 3.55 to 3.7 GHz band, but ongoing reallocation proposals create uncertainty. Europe remains fragmented, with Germany allocating 3.4 to 3.7 GHz for industrial use while France reserves 2.57 to 2.62 GHz for vertical applications, requiring separate compliance frameworks. China’s n41, n78, and n79 bands are clearly defined, but export controls complicate participation for Western vendors. This lack of harmonization increases router development costs by approximately 18 to 22%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Generation: 5G Uptake Accelerates While 4G Remains Entrenched

4G LTE held a 45.32% share of the 4G/5G cellular router market in 2025, reflecting its strong price-performance balance for fixed wireless access, fleet management, and point-of-sale applications. Multi-mode devices that fall back to LTE remain essential in regions like India and Brazil, where rural 5G coverage is inconsistent. Sierra Wireless’s RV55 Industrial LTE-M model, introduced at a bill-of-materials cost under USD 100, highlights the continuing relevance of 4G for ultra-low-power deployments.

5G routers are projected to grow at an 18.44% CAGR through 2031 as enterprises adopt network slicing and ultra-reliable low-latency communication. Cradlepoint’s X35 5G-Advanced unit aggregates six component carriers to exceed 5 Gbps, making 5G viable for uncompressed machine-vision streams. The Release 18 specification for reduced-capability devices will further compress silicon costs, extending 5G economics into cost-sensitive verticals. As a result, the 4G/5G cellular router market tied to 5G deployments is set to expand most rapidly in manufacturing and public safety segments.

By End-User Industry: Public Safety Momentum Builds

Manufacturing accounted for 32.84% of the 4G/5G cellular router market in 2025, led by automotive and chemical sites that require deterministic latency for robotics. Ericsson’s installation at Jaguar Land Rover validated 5G routers for closed-loop quality control on body shops. Energy and utilities are deploying routers that translate DNP3 and IEC 61850 traffic, improving substation visibility without requiring dedicated MPLS.

Public safety and emergency services are advancing at a 16.21% CAGR through 2031, supported by FirstNet mandates requiring mission-critical devices to support priority and preemption signaling. Nextivity’s SHIELD MegaFi 2 Certified router highlights demand for Band 14 capable hardware, while Semtech’s XR80 and XR90 add network slicing to separate body-camera video from situational-awareness telemetry. Together, these investments illustrate how the 4G/5G cellular router market is diversifying beyond manufacturing into life-critical applications.

By Application: Smart Cities Overtake Fixed Wireless Growth

Fixed wireless access accounted for 38.43% of the 4G/5G cellular router market in 2025, delivering rural and semi-urban broadband at roughly one-third the cost of fiber trenching. Outdoor rugged CPEs with IP67 enclosures dominate this use case in Brazil’s semi-urban belts. Smart-city and infrastructure deployments are on track for a 16.92% CAGR, with China integrating routers into traffic-signal controllers across 330 cities to enable real-time congestion mitigation, reducing average travel times by 12%.

Industrial automation and SCADA projects also rely on edge-compute routers to host MQTT brokers locally, trimming cloud fees by up to 40 percent. Fleet and mobile connectivity segments rely on EN 50155-certified hardware, such as Digi’s TX64 5G Rail, to ensure uptime in high-vibration environments. Remote monitoring and surveillance further leverage solar-powered routers that deliver Power over Ethernet to cameras at construction sites without grid access, expanding connectivity into challenging locations.

By Form Factor: Edge-Compute Units Lead Innovation

Indoor CPE routers accounted for 41.63% of the 4G/5G cellular router market size in 2025, anchoring home broadband and small-office deployments. Edge-compute routers are projected to grow fastest at a 18.71% CAGR as industrial customers consolidate gateway, PLC, and modem functions into a single appliance. Teltonika’s RUTM50 model, which ships with Docker pre-installed, enables factories to execute thermal-imaging inference directly on-device, underscoring the shift toward localized intelligence.

Outdoor rugged routers are gaining traction in utilities and smart-city lighting, featuring IP67-rated casings and operating temperatures from -40 °C to +75 °C. Mobile routers serve vehicle fleets and emergency response, favoring ignition-sensing power management to prevent battery drain. Embedded modules in M.2 or mini-PCIe form factors allow kiosk and ATM manufacturers to add cellular connectivity without requalifying entire enclosures, broadening the 4G/5G cellular router market beyond standalone hardware.

Geography Analysis

North America captured 34.89% of the 4G/5G cellular router market in 2025, driven by AT&T and Verizon surpassing 8 million fixed wireless subscribers and FirstNet enforcing Band 14 support in public-safety routers. Edge-compute adoption is rising in Michigan’s automotive plants, while Canadian utilities deploy 5G routers for substation telemetry. The market is shifting from subscriber acquisition to upselling premium tiers that bundle security analytics and cloud management.\

Asia-Pacific is forecast to grow at a 17.84% CAGR through 2031, propelled by China’s 4.958 million 5G base stations operational by March 2026 and its commercial launch of 5G-Advanced in 330 cities. India’s BharatNet Phase 3 awarded Tejas Networks up to 60,000 TJ1400 routers, highlighting cellular backhaul for last-mile connectivity. Japan and South Korea prioritize private 5G networks in automotive and electronics plants, accelerating the adoption of ruggedized edge-compute routers with TSN profiles.

Europe leverages EU Chips Act incentives to localize semiconductor supply and router production, with EUR 80 billion (USD 94 billion) in plant approvals by 2025. Germany’s 3.4-3.7 GHz auction stimulates multi-vendor private 5G ecosystems, while France’s discrete 2.6 GHz vertical band forces custom SKUs. South America pursues rural connectivity, with Brazil’s 80% coverage target by end-2026 driving the adoption of pole-mounted rugged routers. The Middle East invests in smart-city mega-projects, with Saudi Arabia’s stc extending 5G coverage to 75 cities and ADNOC valuing its private 5G network at USD 1.5 billion. Africa remains nascent but rapidly adopts fixed wireless access, led by South Africa, Nigeria, and Kenya, where trenching costs and terrain favor cellular deployments.

Competitive Landscape

The 4G/5G cellular router market shows moderate fragmentation, with leading vendors holding a significant but not dominant share, leaving space for regional manufacturers and vertical specialists. Cradlepoint, Sierra Wireless, and Digi International increasingly monetize software through cloud-native consoles that enable zero-touch provisioning and AI-based traffic optimization. Chinese challengers such as Teltonika, InHand Networks, and Robustel undercut hardware pricing by up to 35%, targeting agriculture and small retail with aggressive volume discounts.

Edge-compute integration is the key differentiator in 2026. Vendors embed x86 or ARM cores with 4-16 GB RAM to run inference locally, reducing the total cost of ownership by up to 40%. Partnerships with hyperscalers are strategic: Cradlepoint anchors AWS IoT Core, Sierra Wireless embeds Microsoft Azure IoT Hub, and Digi aligns with Google Cloud IoT for remote firmware updates. Patent activity centers on AI-driven traffic steering and dynamic network slicing to assure latency and bandwidth for mission-critical flows.

Regulatory compliance is emerging as a pricing lever. The NIST IR 8425A baseline, published in 2024, and forthcoming FIPS 140-3 cryptographic validation allow certified vendors to command premiums in public-sector bids. The ITU’s X.1818 security standard reinforces secure boot and encrypted firmware updates, raising design complexity but elevating trust marks. White-space opportunities also exist in hybrid LTE-M and NB-IoT routers offering 10-year battery life at sub-USD 50 bill of materials, an underserved niche valuable for utility metering and agricultural sensors.

4G/5G Cellular Router Industry Leaders

Cradlepoint, Inc.

Sierra Wireless, Inc.

Digi International Inc.

Teltonika Networks UAB

Peplink International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Cradlepoint introduced the X35 5G-Advanced router, supporting six-carrier aggregation and 5 Gbps peak downlink for enterprise fixed wireless access and industrial automation.

- June 2025: Peplink released the MAX Transit 5G Cat-20 router featuring dual-SIM failover and SpeedFusion bandwidth bonding for uninterrupted fleet connectivity.

- June 2025: Peplink released the MAX Transit 5G Cat-20 router featuring dual-SIM failover and SpeedFusion bandwidth bonding for uninterrupted fleet connectivity.

- May 2025: Sierra Wireless unveiled the AirLink XR90 rugged router, IP67 rated and FirstNet certified for public-safety deployments.

Global 4G/5G Cellular Router Market Report Scope

The 4G/5G cellular router market comprises networking devices that provide wireless wide-area connectivity via cellular networks as primary or backup links for enterprises, industrial systems, and consumer applications. These routers integrate SIM-based communication, edge processing, and secure routing to enable fixed wireless access, IoT, and mission-critical operations. The market spans indoor, outdoor, and embedded form factors across sectors such as manufacturing, transportation, utilities, retail, and public safety, driven by demand for reliable, low-latency, and scalable connectivity solutions.

The 4G/5G Cellular Router Market Report is Segmented by Technology Generation (4G LTE Routers, 5G Routers, and Multi-Mode 4G/5G Routers), End-User Industry (Manufacturing, Energy and Utilities, Transportation and Logistics, Retail and Payments, and Public Safety and Emergency Services), Application (Fixed Wireless Access, Industrial Automation and SCADA, Fleet and Mobile Connectivity, Smart Cities and Infrastructure, and Remote Monitoring and Surveillance), Form Factor (Indoor CPE Routers, Outdoor Rugged Routers, Mobile Routers, Embedded/Module Routers, and Edge-Compute Routers), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 4G LTE Routers |

| 5G Routers |

| Multi-Mode (4G/5G) Routers |

| Manufacturing |

| Energy and Utilities |

| Transportation and Logistics |

| Retail and Payments |

| Public Safety and Emergency Services |

| Fixed Wireless Access |

| Industrial Automation and SCADA |

| Fleet and Mobile Connectivity |

| Smart Cities and Infrastructure |

| Remote Monitoring and Surveillance |

| Indoor CPE Routers |

| Outdoor Rugged Routers |

| Mobile Routers |

| Embedded / Module Routers |

| Edge-Compute Routers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Technology Generation | 4G LTE Routers | |

| 5G Routers | ||

| Multi-Mode (4G/5G) Routers | ||

| By End-User Industry | Manufacturing | |

| Energy and Utilities | ||

| Transportation and Logistics | ||

| Retail and Payments | ||

| Public Safety and Emergency Services | ||

| By Application | Fixed Wireless Access | |

| Industrial Automation and SCADA | ||

| Fleet and Mobile Connectivity | ||

| Smart Cities and Infrastructure | ||

| Remote Monitoring and Surveillance | ||

| By Form Factor | Indoor CPE Routers | |

| Outdoor Rugged Routers | ||

| Mobile Routers | ||

| Embedded / Module Routers | ||

| Edge-Compute Routers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the 4G/5G cellular router market by 2031?

The 4G/5G cellular router market is forecast to reach USD 34.34 billion by 2031, expanding at a 14.53% CAGR over 2026-2031 (Mordor Intelligence).

Which end-user vertical is growing fastest for 4G/5G routers?

Public safety and emergency services lead growth with a 16.21% CAGR, propelled by FirstNet and equivalent mandates that require routers with priority and preemption features (Mordor Intelligence).

How significant is Asia-Pacific to future 4G/5G cellular router demand?

Asia-Pacific is expected to post a 17.84% CAGR through 2031, driven by extensive 5G rollouts in China and India that elevate demand for carrier-aggregation capable routers (Mordor Intelligence).

What differentiates edge-compute routers from conventional CPE?

Edge-compute routers embed multi-core processors and RAM to execute containerized analytics locally, reducing backhaul costs by up to 40 percent while meeting sub-10 ms latency targets.

How are spectrum regulations affecting router design?

Fragmented regional allocations force vendors to produce different hardware SKUs, inflating R&D costs by roughly 20 percent and extending certification cycles by up to twelve months.

Why are dual-SIM routers becoming standard in enterprise deployments?

Outages on single carriers have exposed revenue risks; dual-SIM routers with automatic failover now provide 99.99% uptime guarantees that are critical for finance, healthcare, and retail operations.

Page last updated on: