Residential Routers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.58 Billion |

| Market Size (2031) | USD 22.62 Billion |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

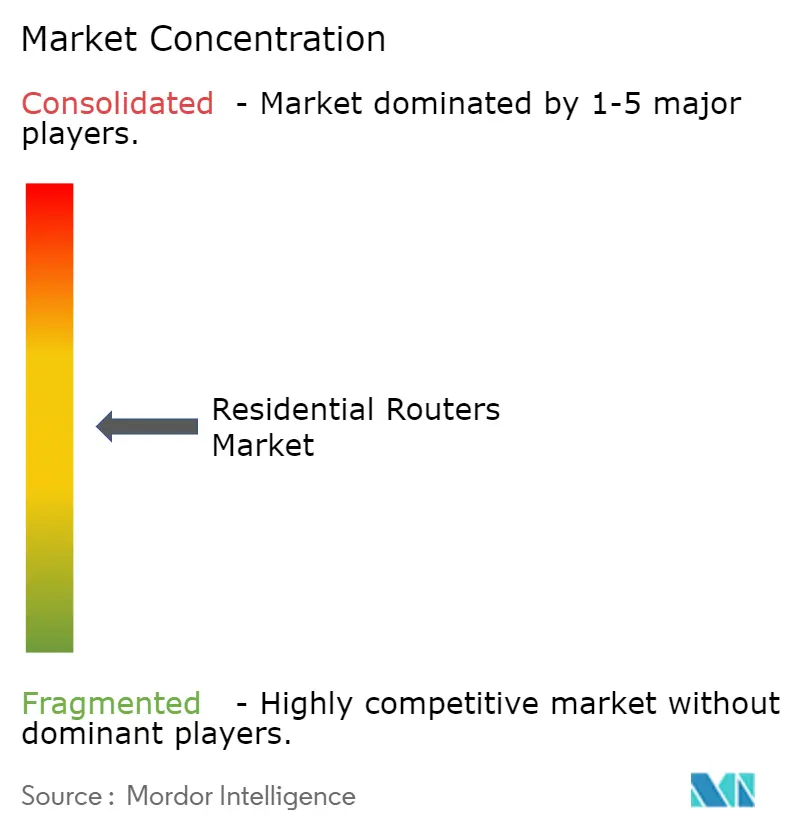

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Residential Routers Market Analysis by Mordor Intelligence

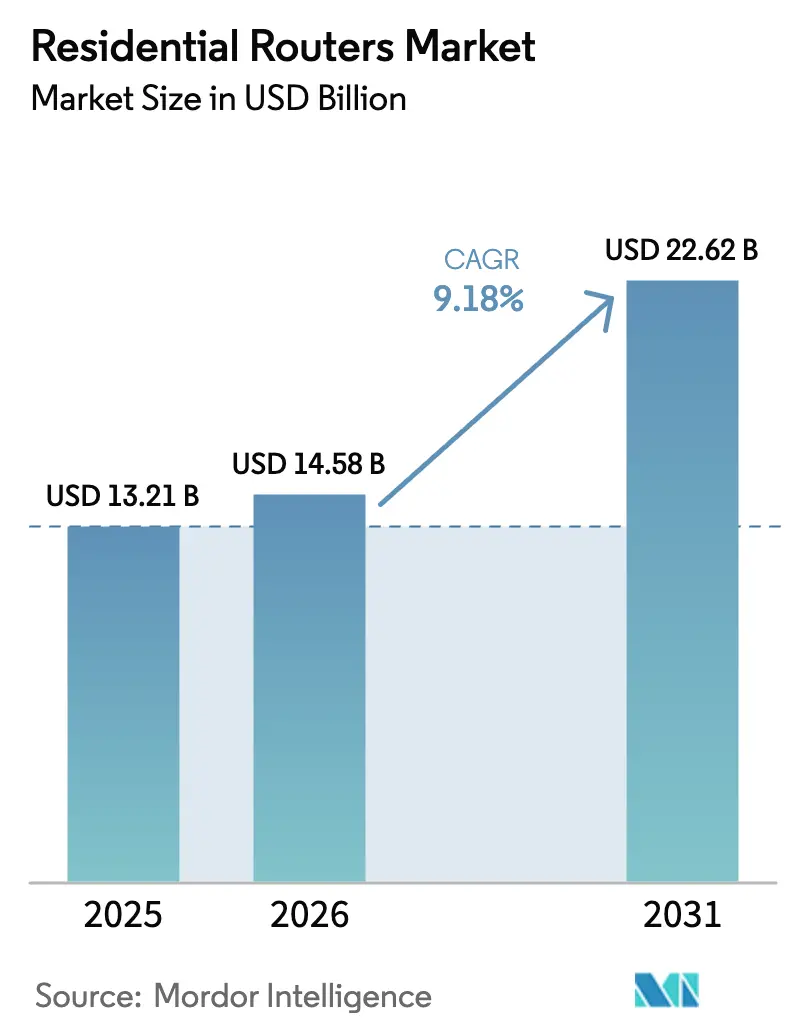

The residential routers market size was valued at USD 13.21 billion in 2025, USD 14.58 billion in 2026, and is projected to attain USD 22.62 billion by 2031, translating into a 9.18% CAGR during the 2026-2031 period. Growing household demand for multi-gig connectivity, ISP fiber roll-outs that bundle Wi-Fi 7 gateways, and the steady replacement of Wi-Fi 5 hardware underpin this upward trajectory. Wireless connectivity continues to absorb spending because tri-band routers help alleviate congestion caused by remote work, multi-stream entertainment, and smart-home devices. ISPs monetize the shift by embedding AI-driven optimization and cybersecurity services in subscription bundles, a model that redirects value from retail shelf space to managed Wi-Fi fees. Competitive advantage is increasingly hinging on chipset allocation agreements and cloud-based network-management platforms, rather than cosmetic hardware upgrades. Energy-efficiency mandates in the European Union and North America further accelerate refresh cycles by setting power-consumption ceilings that legacy routers cannot meet.

Key Report Takeaways

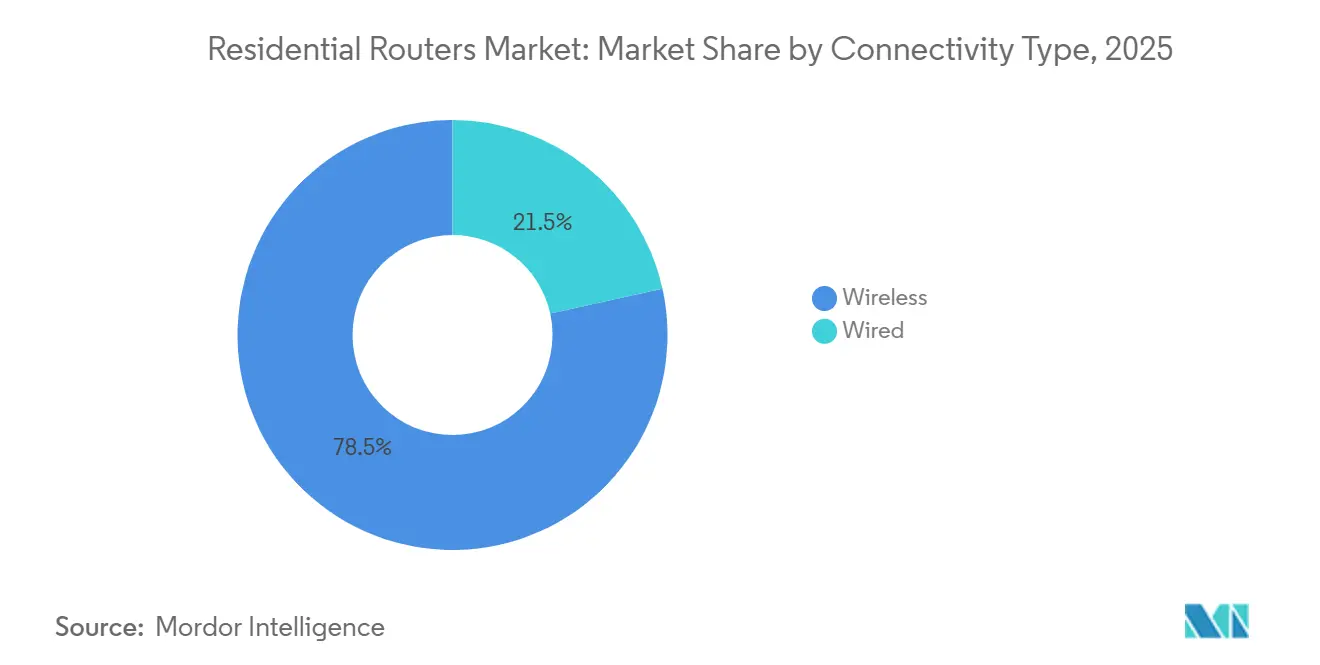

- By connectivity type, wireless commanded 78.46% residential routers market share in 2025, while the same segment is forecast to grow at a 10.17% CAGR through 2031.

- By Wi-Fi standard generation, Wi-Fi 6 and 6E led with 47.82% share in 2025; Wi-Fi 7 is projected to expand at a 10.88% CAGR through 2031.

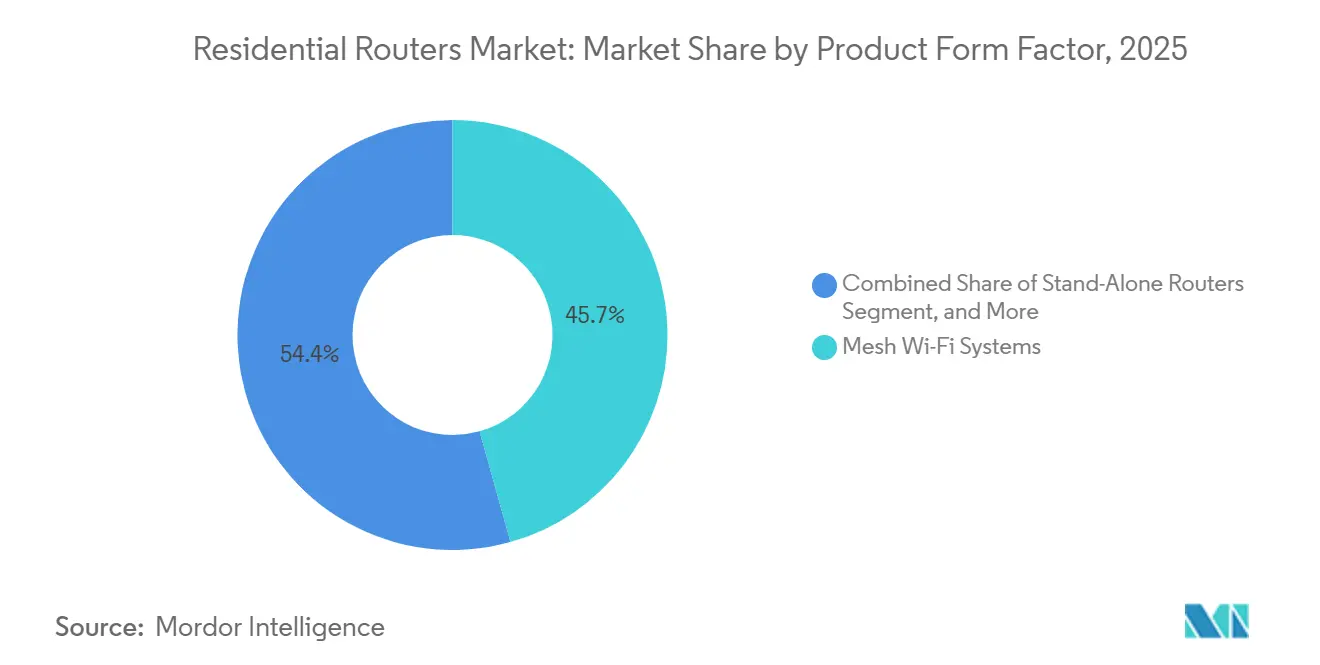

- By product form factor, mesh Wi-Fi systems accounted for 45.65% of the residential routers market size in 2025 and are advancing at a 9.46% CAGR through 2031.

- By distribution channel, ISP-bundled and leased gateways held 61.37% of 2025 revenue; the channel is expected to post a 9.79% CAGR through 2031.

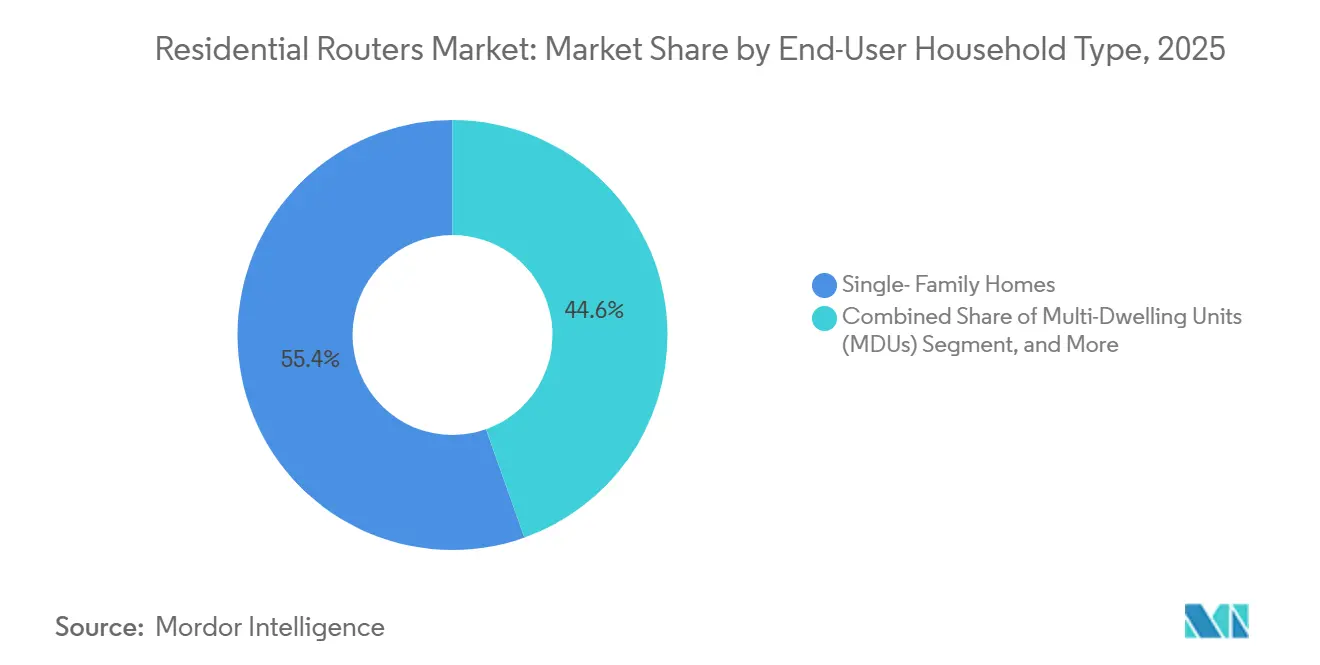

- By end-user household type, single-family homes captured 55.43% share in 2025, while multi-dwelling units are growing the fastest at a 10.02% CAGR through 2031.

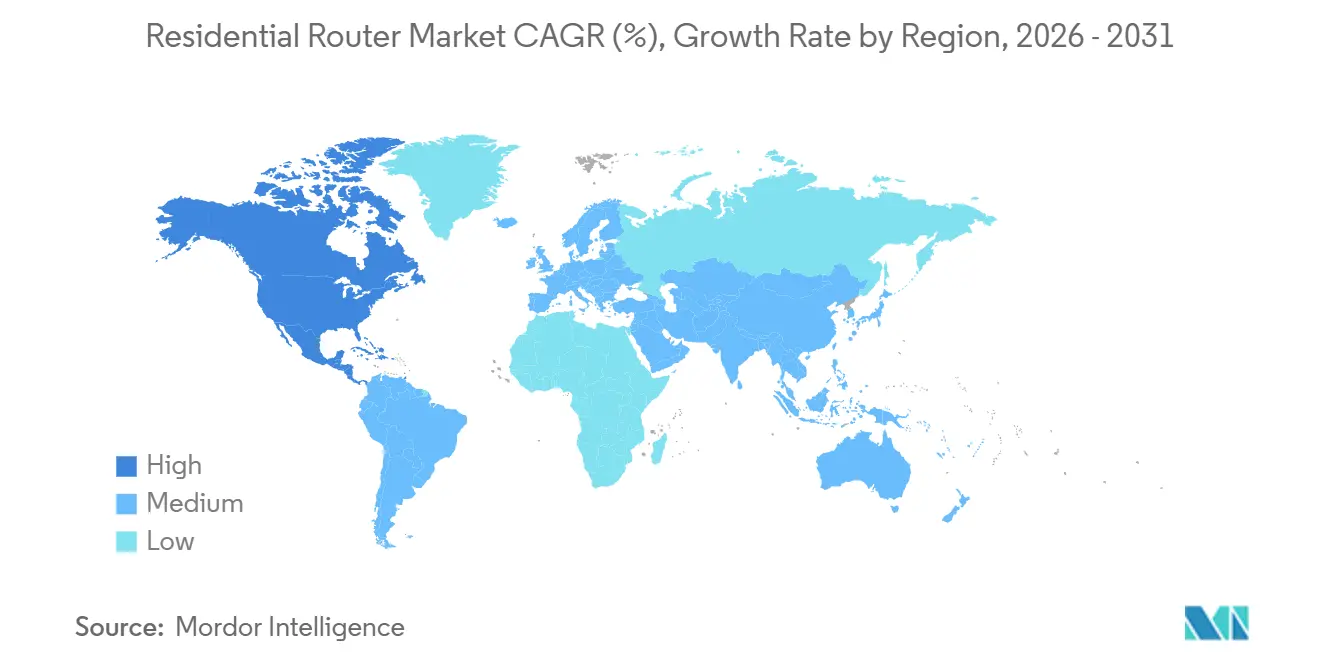

- By geography, North America led with 41.58% share in 2025, whereas Asia-Pacific is projected to grow at a 10.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Residential Routers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of smart-home and IoT devices | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Surging global IP traffic and high-speed broadband uptake | +2.4% | Global, led by Asia-Pacific fiber deployments | Long term (≥ 4 years) |

| Migration to Wi-Fi 6/6E/7 standards fueling replacement cycles | +1.8% | North America and Europe early adopters, Asia-Pacific volume growth | Short term (≤ 2 years) |

| ISP fiber roll-outs bundling Wi-Fi 7 gateways at scale | +1.6% | North America and Europe mature markets, Asia-Pacific emerging | Medium term (2-4 years) |

| AI-driven managed-Wi-Fi subscriptions boosting premium router demand | +0.9% | North America and Europe, gradual Asia-Pacific uptake | Long term (≥ 4 years) |

| Energy-efficiency mandates prompting low-power router upgrades | +0.4% | Europe and North America regulatory compliance zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Smart-Home and IoT Devices

Connected-device density climbed to 17 units per household in North America and 12 in Europe by 2025. This saturation forces legacy routers, originally designed for fewer than 10 concurrent links, into obsolescence. Households facing latency during simultaneous 4K streaming, smart-thermostat polling, and security-camera uploads now view tri-band or mesh systems as utilities rather than luxuries. ISPs exploit the pain point by bundling Wi-Fi 6E and Wi-Fi 7 gateways with new fiber installations, locking subscribers into managed Wi-Fi ecosystems at USD 10-15 per month. Matter interoperability has become baseline, compelling manufacturers to embed Thread border-router functionality that fragments competition between platform-centric entrants and traditional hardware brands.

Surging Global IP Traffic and High-Speed Broadband Uptake

Global IP traffic reached 4.8 zettabytes in 2024 and will exceed 7.5 zettabytes by 2028. Fiber penetration surpassed 52% in China and 48% in South Korea during 2025, creating pull for routers with 2.5 Gbps or 10 Gbps WAN ports. North American cable operators responded by integrating Wi-Fi 7 radios into DOCSIS 4.0 gateways, shifting profit pools from hardware to recurring managed-service fees. In India, BharatNet extended backbone capacity to 250,000 villages, but the absence of firmware-update infrastructure in sub-USD 25 routers leaves rural users exposed to botnets. These dynamics polarize the residential routers market between ISP-controlled gateways and premium enthusiast gear.

Migration to Wi-Fi 6/6E/7 Standards Fueling Replacement Cycles

Wi-Fi 7 routers entered volume shipment in late 2024 as Qualcomm, Broadcom, and MediaTek ramped 802.11be chipsets.[1]Qualcomm Newsroom. “Chipmakers Ramp 802.11be Silicon Production.” qualcomm.com/news ISPs accelerate adoption by offering no-cost gateway swaps to long-term subscribers, bypassing consumer price sensitivity and embedding Wi-Fi 7 two years ahead of client-device saturation. Regulatory approval for 6 GHz spectrum varies, the United States and Europe authorized usage in 2020 and 2021, while India waited until 2024, fragmenting inventory strategies. The lag creates a two-speed resident router market where ISP-bundled upgrades outpace retail sales, concentrating revenue with vertically integrated suppliers.

ISP Fiber Roll-Outs Bundling Wi-Fi 7 Gateways at Scale

Tier-1 ISPs such as AT&T, Spectrum, and BeFibre standardized on Wi-Fi 7 gateways for gigabit customers in 2025. By procuring chipsets in bulk, operators undercut retail pricing by USD 50-100 and secure allocation priority during shortages. Remote firmware updates and cloud diagnostics slash on-site service calls by 30%, allowing operators to recoup subsidies within 18 months. Stand-alone router vendors counter by targeting gamers and open-source enthusiasts, but that niche represents less than 15% of annual unit volume.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cybersecurity and privacy risks | -1.2% | Global, acute in North America and Europe due to regulatory scrutiny | Short term (≤ 2 years) |

| Price sensitivity in emerging markets | -0.8% | Asia-Pacific (India, Southeast Asia), Africa, South America | Medium term (2-4 years) |

| User skill gaps causing feature under-utilization, delaying upgrades | -0.5% | Global, more pronounced in emerging markets and aging demographics | Long term (≥ 4 years) |

| Chipset supply-chain volatility creating product shortages and price spikes | -0.6% | Global, with acute impact on Tier-2 and Tier-3 OEMs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Cybersecurity and Privacy Risks

Routers represented 75% of successful IoT botnet compromises in 2024. The EU Cyber Resilience Act now mandates five-year security-update commitments, adding USD 3-5 to bill of materials and squeezing low-margin brands.[2]European Commission Digital Strategy. “EU Cyber Resilience Act Sets Security-Update Rules.” digital-strategy.ec.europa.eu In the United States, a voluntary FCC cybersecurity label remains underused because most consumers cannot interpret technical badges. Privacy advocacy intensified after revelations that some ISP gateways harvest browsing metadata for ad targeting, pressuring operators to adopt opt-in frameworks. As households wait for regulatory clarity, upgrade cycles slow and OEMs divert budgets from feature innovation to compliance.

Price Sensitivity in Emerging Markets

In India, 68% of router purchases in 2025 were below USD 30, a range dominated by unbranded Wi-Fi 4 devices that lack WPA3 encryption. Import tariffs between 15% and 25% in sub-Saharan Africa inflate retail prices and keep fixed-line adoption urban-centric. Brazilian router prices climbed 15%-25% because of logistics and currency volatility. OEMs respond with stripped-down SKUs, but these cost-downs erode brand perception and cannibalize higher-margin lines, limiting revenue expansion even as unit shipments rise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connectivity Type: Wireless Dominance Anchored by Multi-Device Households

Wireless routers held 78.46% residential routers market share in 2025 and are set to grow at a 10.17% CAGR, reflecting their ability to manage simultaneous streams and remote-work loads. Households that host three or more concurrent video sessions favor tri-band units over wired alternatives that require costly structured cabling. ISPs accelerate wireless adoption by bundling mesh-capable gateways that erase dead zones, moving the residential routers market toward subscription models. The wired segment persists in latency-sensitive niches such as high-frequency trading, yet its contraction will continue as Wi-Fi 7 delivers near-wired performance.

Mesh ecosystems and AI-assisted roaming now define the wireless value proposition. The EU Radio Equipment Directive’s standardization on USB-C chargers lowers e-waste objections and shortens router replacement deliberations. Markets like Germany and Japan, which integrate Ethernet jacks in every room, still end sessions on Wi-Fi endpoints for flexibility. The residential routers market will therefore remain decisively wireless as IoT density rises.

By Wi-Fi Standard Generation: Wi-Fi 7 Ascent Driven by ISP Pre-Deployment

Wi-Fi 6 and 6E accounted for 47.82% of shipments in 2025, yet Wi-Fi 7 is poised for the fastest growth at 10.88% CAGR. Multi-link operation aggregates 2.4 GHz, 5 GHz, and 6 GHz bands to deliver deterministic latency for cloud gaming and augmented reality. ISPs distribute 802.11be gateways during service activation, cutting the adoption lag that historically separates new standards from mass uptake. China’s restriction of 6 GHz to indoor use forces dual-SKU strategies, but volume pricing will normalize by 2027.

Enthusiast-grade Wi-Fi 7 routers priced above USD 400 serve as brand halo products and constitute less than 8% of unit volume. As client devices arrive, the performance gulf will motivate replacements of Wi-Fi 5 units, further propelling the residential routers market size.

By Product Form Factor: Mesh Systems Capitalize on Whole-Home Coverage

Mesh systems captured 45.65% of 2025 revenue and will sustain a 9.46% CAGR through 2031 as multi-story homes and thick-wall construction challenge single-unit coverage. Plug-and-play satellite nodes appeal to non-technical users looking for seamless roaming. ISPs upsell mesh extenders at USD 50–80, a profitable addition that also cuts support calls. Stand-alone routers survive in small apartments but face gross margins below 15%, driving vendors to pivot toward subscription services.

Modem-router gateways dominate ISP deployments because integrated designs trim power and simplify customer education. 5G fixed-wireless gateways bridge last-mile gaps in rural settings, though latency variability confines them to cost-sensitive users. As fiber expands, the residential routers market will coalesce around mesh and gateway hybrids that simplify home networking.

By Distribution Channel: ISP Bundling Reshapes Margin Pools

ISP-bundled and leased gateways generated 61.37% of 2025 revenue and will rise at a 9.79% CAGR. Zero-upfront-cost propositions convert routers into annuity streams through USD 10–15 monthly managed-Wi-Fi fees. Retail in-store sales shrank to 18% as big-box chains reduced SKU counts by 30%. Online direct-to-consumer brands like eero leverage firmware cadence and customer education to offset the absence of physical shelf space.

The leased-router model also accelerates hardware refresh every three to four years, advancing the residential routers market toward recurrent revenue. Power users who insist on open-source firmware continue to buy premium SKUs, yet they represent less than 12% of annual volume.

By End-User Household Type: MDUs Emerge as Fastest-Growing Segment

Single-family homes accounted for 55.43% of 2025 demand, but multi-dwelling units are expanding the fastest at a 10.02% CAGR. Property developers now view gigabit Wi-Fi amenities as table stakes, with vacancy penalties of 15-20% for laggards. Bulk service agreements hand procurement to building owners, embedding managed-Wi-Fi fees into rent and elevating mesh and centralized gateway installs.

MDUs require distributed antenna systems to overcome concrete attenuation, lifting per-unit hardware costs by USD 80–120. Small Office/ Home Office (SOHO) users, 12% of demand, pay premiums for dual-WAN failover and VPN throughput. As residential construction plateaus, MDUs will account for an outsized share of incremental residential routers market size growth.

Geography Analysis

North America generated 41.58% of residential router revenue in 2025, propelled by ISP bundling that embeds Wi-Fi 7 gateways into fiber and cable tiers. Comcast’s xFi platform serves 32 million households and monetizes AI-driven optimization at USD 14 per month. AT&T and Verizon adopted similar tactics, cutting truck-roll costs by 28% through remote diagnostics. Average selling prices remain high at USD 140-200 for mesh systems. Regulatory moves such as the FCC cybersecurity label add compliance overhead without visibly shifting consumer choices.

Asia-Pacific is forecast to deliver the fastest regional expansion at a 10.62% CAGR through 2031. China’s 580 million fiber households require multi-gig routers, while India’s BharatNet backbone highlights security gaps in low-cost hardware. ASEAN nations remain price sensitive, with 72% of routers priced below USD 35. Japan and South Korea lead Wi-Fi 7 adoption as operators bundle 10 Gbps services.

Europe held 22% of global revenue in 2025, shaped by the EU Cyber Resilience Act and Ecodesign mandates that favor brands with established certification pipelines. BeFibre and EE priced AI-powered Wi-Fi 7 tiers at USD 15 per month, trimming churn by 18%. Germany’s structured wiring norms slow mesh proliferation, yet fiber penetration reached 48% in 2025, creating latent demand for multi-gig routers. South America, the Middle East, and Africa combined for 18% of revenue, constrained by import tariffs and currency volatility.[3]African Development Bank. “Tariff Barriers in Networking Equipment.” afdb.org

Competitive Landscape

The residential routers market is moderately concentrated. The top five vendors, including Netgear, TP-Link, ASUS, D-Link, and Xiaomi, held about 48% of 2025 revenue. ISP-branded gateways from Cisco, CommScope, and Nokia dominate bundled channels, shading retail exposure. Vendors that secure multi-year chipset contracts with Qualcomm and Broadcom gain first-mover status in Wi-Fi 7 deployments, an advantage for vertically integrated players such as Huawei. White-space persists in MDU bulk deals where price ceilings hover below USD 60 per unit.

Technology differentiation increasingly revolves around cloud-based network optimization rather than hardware specifications. Qualcomm's Networking Pro Series chipsets enable real-time device prioritization and predictive channel switching, features that ISPs embed into tiered service plans priced at USD 10 to USD 18 per month.

Patent filings in 2024 and 2025 concentrated on multi-link operation (MLO) algorithms and AI-driven interference mitigation, signaling a shift toward software-defined networking architectures that commoditize hardware and elevate platform lock-in as the primary competitive moat. Smaller contenders such as Ubiquiti and Synology target enthusiast segments with open-source firmware compatibility and prosumer NAS integration, but these niches represent less than 10 percent of unit volume and face margin pressure as ISP-bundled alternatives incorporate similar features at zero upfront cost

Residential Routers Industry Leaders

D-Link Corporation

TP-Link Technologies Co. Ltd

NETGEAR Inc.

Belkin International, Inc. (Linksys)

ASUSTeK Computer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: TP-Link launched the BE19000 quad-band Wi-Fi 7 router targeting gamers at USD 599.

- November 2025: NETGEAR partnered with Plume to embed AI-driven optimization in Orbi mesh systems, trimming ISP support calls by 25% .

- October 2025: AT&T expanded All-Fi Pro to 15 million households, bundling Nokia Wi-Fi 7 gateways at USD 15 per month.

- September 2025: Xiaomi introduced the Redmi Router AX6000 in India at INR 3,999 (USD 48) to capture value-segment upgrades.

- August 2025: Comcast deployed 2 million xFi Wi-Fi 7 gateways for Gigabit Pro subscribers, integrating Broadcom BCM6726 silicon.

Global Residential Routers Market Report Scope

A router is a gateway that passes data between one or more local area networks. It is a device that provides Wi-Fi and is typically connected to a modem. For the study scope, a router that is installed in homes to share a single internet connection to multiple devices is considered a residential router. These internet-connected devices in the home form a local area network (LAN).

The Residential Routers Market Report is Segmented by Connectivity Type (Wired, and Wireless), Wi-Fi Standard Generation (Wi-Fi 4, Wi-Fi 5, Wi-Fi 6/6E, and Wi-Fi 7), Product Form Factor (Stand-alone Routers, Mesh Wi-Fi Systems, Modem-Router Gateways, and 5G/FWA Home Gateways), Distribution Channel (Retail, Online/E-commerce, ISP Bundled/Leased, and Direct-to-Consumer Brands), End-User Household Type (Single-Family Homes, Multi-Dwelling Units, and Small Office/ Home Office SOHO), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Wired |

| Wireless |

| Wi-Fi 4 (802.11n) |

| Wi-Fi 5 (802.11ac) |

| Wi-Fi 6 / 6E (802.11ax) |

| Wi-Fi 7 (802.11be) |

| Stand-alone Routers |

| Mesh Wi-Fi Systems |

| Modem- Router Gateways (IADs) |

| 5G/ FWA Home Gateways |

| Retail (In-store) |

| Online/ E-commerce |

| ISP Bundled/ Leased |

| Direct-to-Consumer Brands |

| Single- Family Homes |

| Multi- Dwelling Units (MDUs) |

| Small Office/ Home Office (SOHO) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Connectivity Type | Wired | |

| Wireless | ||

| By WiFi Standard Generation | Wi-Fi 4 (802.11n) | |

| Wi-Fi 5 (802.11ac) | ||

| Wi-Fi 6 / 6E (802.11ax) | ||

| Wi-Fi 7 (802.11be) | ||

| By Product Form Factor | Stand-alone Routers | |

| Mesh Wi-Fi Systems | ||

| Modem- Router Gateways (IADs) | ||

| 5G/ FWA Home Gateways | ||

| By Distribution Channel | Retail (In-store) | |

| Online/ E-commerce | ||

| ISP Bundled/ Leased | ||

| Direct-to-Consumer Brands | ||

| By End-User Household Type | Single- Family Homes | |

| Multi- Dwelling Units (MDUs) | ||

| Small Office/ Home Office (SOHO) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What growth rate is projected for the residential router market between 2026 and 2031?

The residential router market is forecast to grow at a 9.18% CAGR from 2026 to 2031.

Which connectivity type leads current demand?

Wireless routers dominate, holding 78.46% share in 2025 and expanding with a 10.17% CAGR.

How are ISPs influencing router replacement cycles?

ISPs bundle Wi-Fi 7 gateways with fiber packages and charge USD 10–15 monthly for managed Wi-Fi, shortening refresh intervals to 3–4 years.

Why are mesh systems growing faster than stand-alone routers?

Mesh nodes solve coverage gaps in multi-story homes, leading to a 9.46% CAGR compared with stagnating single-unit sales.

Which region is expected to post the fastest growth?

Asia-Pacific is projected to grow at a 10.62% CAGR through 2031, driven by China’s fiber mandates and India’s rural broadband push.

What is the main cybersecurity concern for residential routers?

Routers account for 75% of successful IoT botnet breaches, prompting new security-update regulations in the European Union and the United States.

Page last updated on: