Body Fluid Collection And Diagnostics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 9.98 Billion |

| Market Size (2030) | USD 14.34 Billion |

| Growth Rate (2025 - 2030) | 7.52% CAGR |

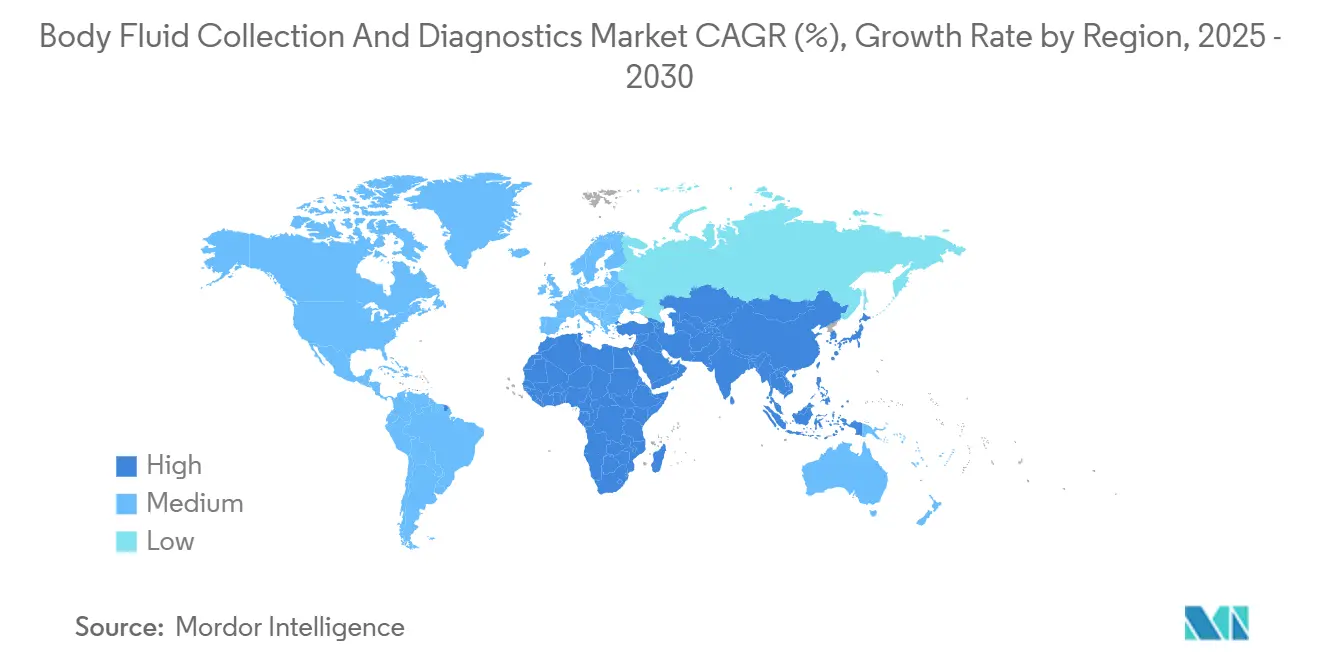

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

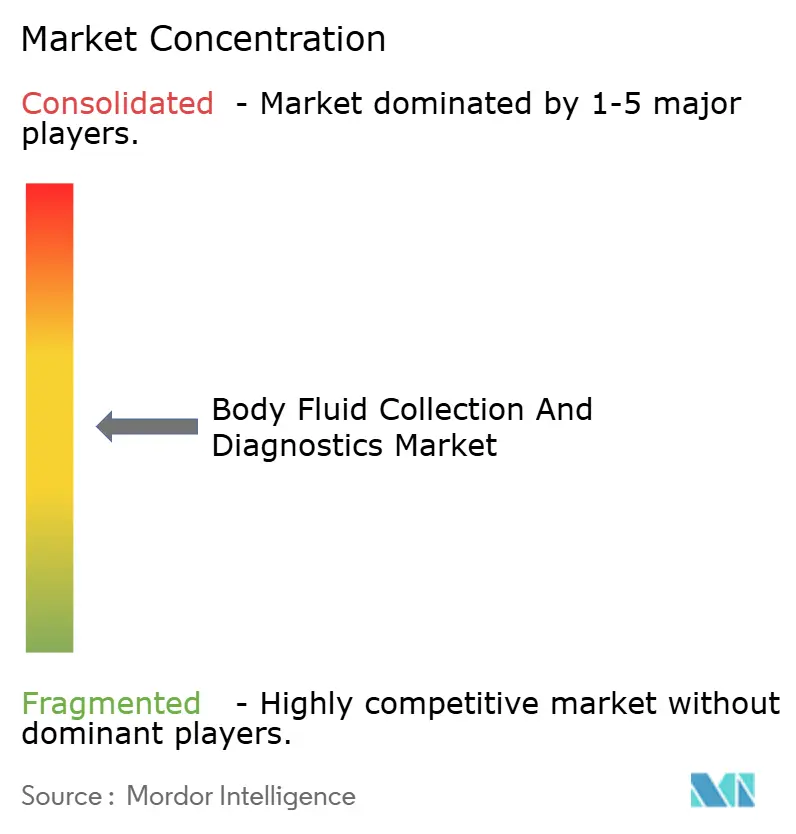

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Body Fluid Collection And Diagnostics Market Analysis by Mordor Intelligence

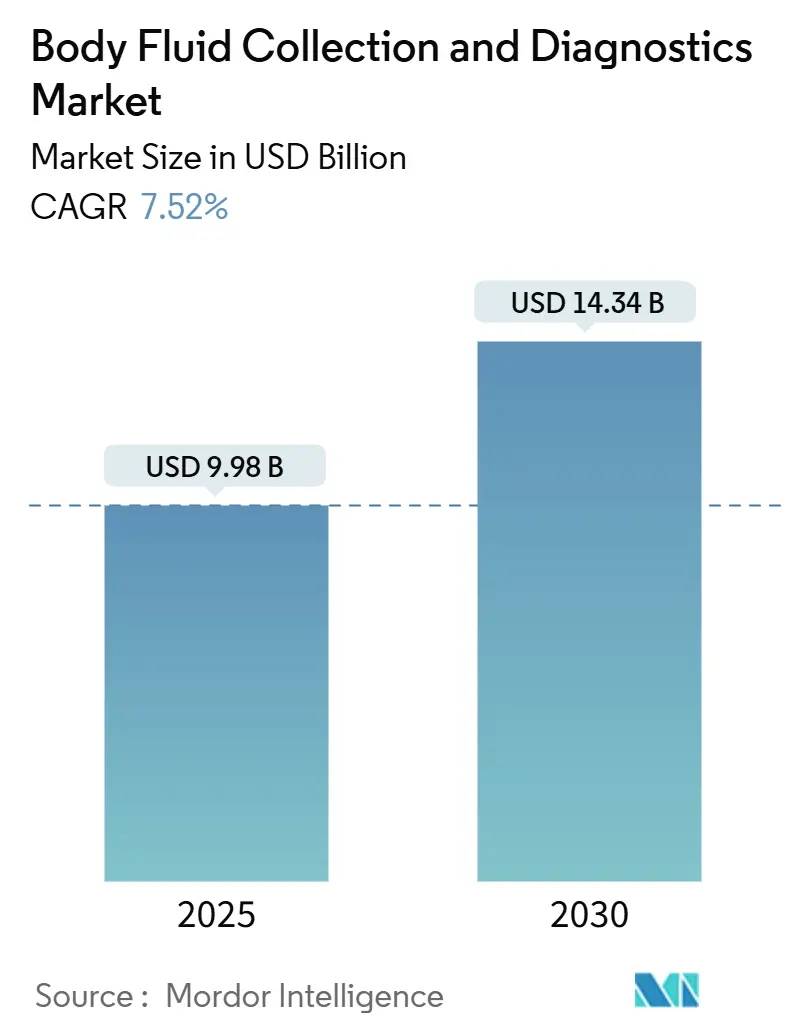

The body fluid collection and diagnostics market size stands at USD 9.98 billion in 2025 and is forecast to reach USD 14.34 billion by 2030, registering a 7.52% CAGR over the period. This trajectory mirrors the shift from centralized laboratories to digitally linked, patient-centric testing models that shorten result times and reduce care costs . Regulatory modernization—most notably the FDA’s 2024 laboratory-developed-test rule—adds predictable oversight that spurs device approvals while protecting public health.[1]U.S. Food and Drug Administration, “Medical Devices: Laboratory Developed Tests,” federalregister.govDemand is further amplified by chronic-disease monitoring needs, post-pandemic infectious-disease preparedness, and the rapid diffusion of wearable biosensors that enable continuous fluid analysis. Competitive strategies now revolve around integrating artificial intelligence with point-of-care platforms, securing polymer supply for advanced collection systems, and partnering with telehealth providers to embed home-based testing into mainstream care pathways.

Key Report Takeaways

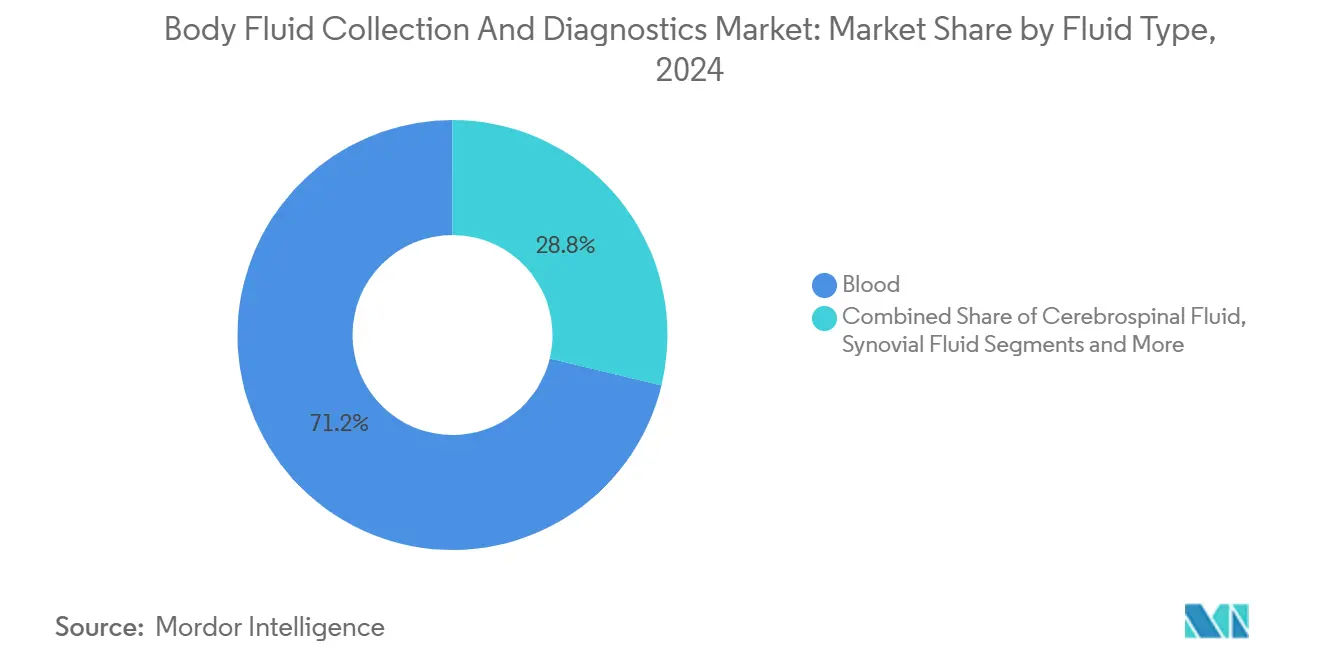

- By fluid type, blood retained 71.22% share of the body fluid collection and diagnostics market size in 2024; saliva/oral fluid diagnostics are projected to expand at an 11.85% CAGR through 2030.

- By product type, collection devices captured 34.45% revenue in 2024, whereas diagnostic consumables are forecast to post a 10.32% CAGR to 2030.

- By diagnostic technology, immunoassay platforms commanded 28.73% of the body fluid collection and diagnostics market size in 2024; wearable and continuous-monitoring sensors exhibit the fastest 10.68% CAGR outlook.

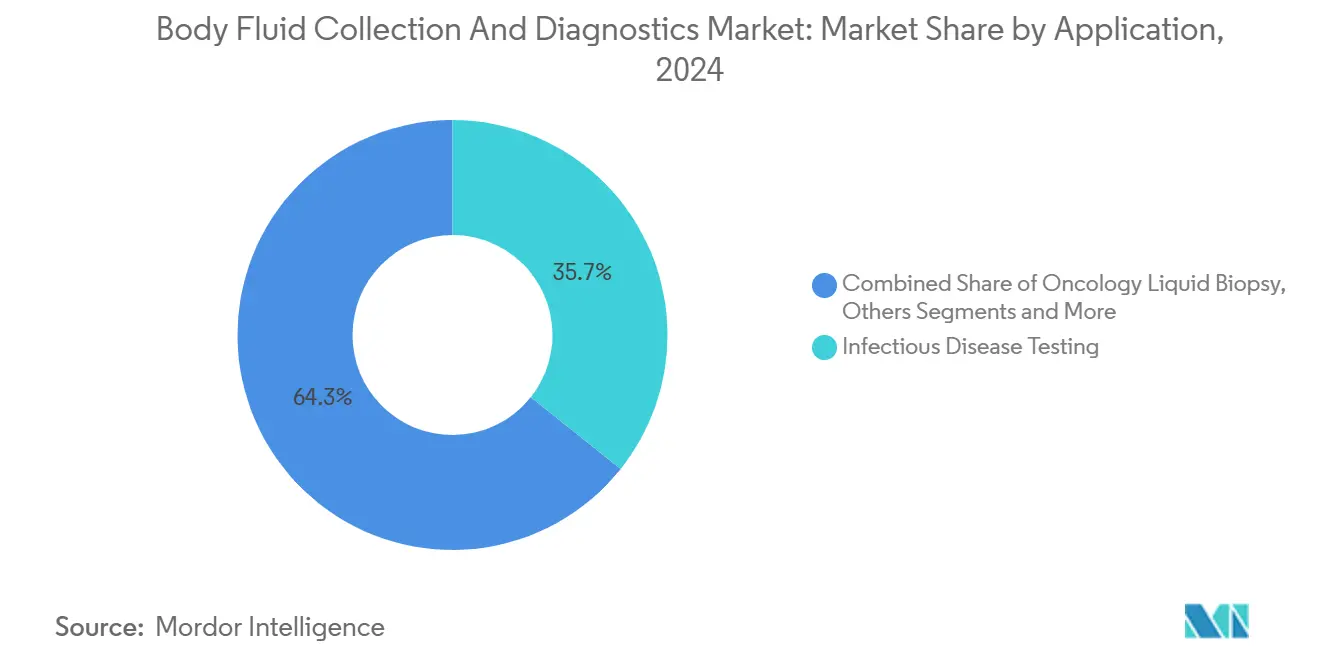

- By application, infectious-disease testing led with 35.71% of the body fluid collection and diagnostics market share in 2024, while oncology liquid biopsy is on track for an 11.44% CAGR to 2030.

- By end user, hospitals held 41.22% of the body fluid collection and diagnostics market share in 2024, yet homecare and remote collection services are advancing at a 9.84% CAGR through 2030.

- By geography, North America contributed 37.53% revenue in 2024, while Asia-Pacific is anticipated to expand at a 9.12% CAGR during the forecast window.

Global Body Fluid Collection And Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic Disease Prevalence Necessitating Routine Fluid-Based Testing | +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Point-Of-Care & Minimally-Invasive Collection Adoption Surge | +1.5% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Government Infectious-Disease Screening Mandates & Funding Uptick | +1.2% | Global, with emphasis on APAC and emerging markets | Short term (≤ 2 years) |

| At-Home Self-Collection Kits Integrated With Digital Logistics | +1.0% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Reimbursement Expansion For Liquid-Biopsy Multi-Omics Assays | +0.8% | North America & EU primarily | Long term (≥ 4 years) |

| Wearable Microfluidic Sensors Enabling Continuous Fluid Monitoring | +0.9% | Global, with tech-forward markets leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic-Disease Prevalence Necessitating Routine Fluid-Based Testing

Escalating diabetes, cardiovascular, and multimorbidity burdens are turning once-episodic diagnostics into routine monitoring tools. Continuous glucose monitoring systems now link directly with automated insulin delivery—exemplified by Abbott’s collaboration with Medtronic—which allows therapeutic adjustments based on real-time biofluid readings. Wearable sweat and interstitial-fluid sensors add cardiovascular biomarker surveillance, and payers in the United States and Europe increasingly reimburse such long-term monitoring because it trims downstream treatment costs. As populations age, health systems pivot toward multi-biomarker panels that can be run on a single blood, urine, or saliva sample, reinforcing the relevance of the body fluid collection and diagnostics market.

Point-of-Care & Minimally Invasive Collection Adoption Surge

The FDA’s first point-of-care hepatitis C RNA clearance in 2024 reaffirmed that rapid results delivered during a single visit can transform clinical pathways.[2]U.S. Food and Drug Administration, “FDA Permits Marketing of First Point-of-Care Hepatitis C RNA Test,” fda.gov BD’s MiniDraw fingertip system achieves venous-grade accuracy without traditional phlebotomy, opening emergency-department and retail-clinic opportunities. AI-enabled readers interpret multi-analyte cartridges in minutes, shaving hours from historical turnaround. Hospitals redeploy personnel toward higher acuity tasks as decentralized testing scales, cementing point-of-care as a cornerstone of the body fluid collection and diagnostics market.

Government Infectious-Disease Screening Mandates & Funding Uptick

Post-COVID policy reforms have locked in sustained public financing for portable PCR and antigen platforms. The WHO’s mpox emergency announcement in 2024 triggered immediate demand for Cepheid’s multiplex cartridges, which can be deployed in airports and primary-care clinics. Asia-Pacific governments embed rapid-testing capacity into digital-health rollouts backed by the Asian Development Bank, ensuring early detection infrastructure persists beyond crises.[3]Asian Development Bank, “Digital Development Facility for Asia and the Pacific,” adb.org

At-Home Self-Collection Kits Integrated With Digital Logistics

Emergency authorizations for monkeypox home-collection PCR tests signaled regulatory comfort with consumer-handled specimens. Blockchain-based chain-of-custody platforms now track each kit, and telehealth portals deliver results alongside physician consults, expanding the body fluid collection and diagnostics market into rural and under-served communities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pre-Analytical Errors & Contamination Raising Repeat-Test Costs | -0.9% | Global, with higher impact in resource-limited settings | Short term (≤ 2 years) |

| High Capital Cost Of Advanced Molecular Systems In LMICs | -1.2% | Low and middle-income countries primarily | Medium term (2-4 years) |

| Data-Privacy Rules Curbing Secondary Use Of Residual Specimens | -0.7% | EU & North America, expanding globally | Long term (≥ 4 years) |

| Specialty-Polymer Supply Bottlenecks For Novel Collection Devices | -0.8% | Global, with concentration in manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pre-Analytical Errors & Contamination Raising Repeat-Test Costs

Up to 70% of laboratory mistakes originate before analysis begins, forcing retests, delaying care, and inflating overall expenditures. Molecular panels are especially sensitive, as trace contaminants can inhibit amplification. Automation, barcode tracking, and standardized procedures help, but training gaps in low-resource settings sustain the risk.

High Capital Cost Of Advanced Molecular Systems In LMICs

State-of-the-art sequencers and liquid-biopsy analyzers cost upward of USD 500,000, far outstripping annual diagnostic budgets in many developing economies. Even when grants fund initial purchases, consumables, calibration, and skilled labor remain hurdles. Pooled-facility models and portable mid-throughput devices are emerging, yet validation to gold-standard performance levels prolongs timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fluid Type: Saliva Emerges as Innovation Catalyst

In 2024, blood samples generated 71.22% of revenue within the body fluid collection and diagnostics market. The dominance stems from extensive biomarker libraries, mature collection practice, and broad reimbursement. Yet saliva diagnostics, supported by 100% breast-cancer detection accuracy in a University of Florida handheld system, is forecast for an 11.85% CAGR, the quickest among all fluids. National Institutes of Dental and Craniofacial Research grants exceeding USD 3 million accelerate saliva biomarker discovery, underscoring saliva’s role in reshaping the body fluid collection and diagnostics market size.

Continued reliance on urine for drug screening and metabolic tests keeps that fluid’s trajectory steady, while cerebrospinal-fluid panels for neurodegenerative markers gain relevance. Synovial fluid testing benefits from refined viscosity instrumentation that pinpoints joint infections swiftly. Researchers increasingly pursue multi-fluid algorithms that fuse saliva, sweat, and capillary blood to deliver panoramic health snapshots, underscoring the expanding frontier of the body fluid collection and diagnostics market.

By Product Type: Consumables Drive Innovation Velocity

Collection devices retained the largest 34.45% share in 2024, with BD Vacutainer celebrating 75 years of sustained enhancements. However, diagnostic consumables—including single-use microfluidic cartridges and rapid test strips—will post the highest 10.32% CAGR, reflecting point-of-care and at-home testing momentum. These disposable formats mitigate contamination, simplify workflows, and shorten result times, expanding the body fluid collection and diagnostics market size across primary-care and pharmacy outlets.

Needles and syringes continue migrating to safety-engineered designs, while instrument manufacturers embed cloud connectivity for remote maintenance. Hybrid devices now merge collection and readout in one sealed unit, minimizing pre-analytical errors and creating value-added differentiation that influences purchasing choices among labs and clinics.

By Diagnostic Technology: Wearables Reshape Monitoring Paradigms

Immunoassays accounted for 28.73% revenue in 2024, buoyed by established menu breadth. Molecular diagnostics extend reach via next-generation sequencing and highly multiplexed liquid biopsies. Nevertheless, wearable and continuous-monitoring sensors will mark the fastest 10.68% CAGR. Harvard’s anti-biofouling coating lengthens implant life, while KAIST’s three-minute multiplex reader enhances sensitivity 38-fold, demonstrating how the body fluid collection and diagnostics market is migrating from episodic draws to ongoing surveillance.

Rapid-test formats benefit from AI-powered interpretation; the TIMESAVER algorithm pushes accuracy to 97.6% and slashes assay time to two minutes. Cross-technology convergence packs flow-cytometry optics onto microfluidic chips, further blurring boundaries among platforms.

By Application: Liquid Biopsy Accelerates Precision Medicine

Infectious disease platforms held 35.71% revenue in 2024, reflecting institutionalized pandemic vigilance. Oncology liquid biopsy will surge at 11.44% CAGR, fueled by Guardant360's multi-modal assay suite and Labcorp’s 521-gene Plasma Complete launch. For oncologists, real-time circulating tumor-DNA profiling curtails invasive biopsies and enables dynamic therapy matching, strengthening the body fluid collection and diagnostics industry outlook.

Metabolic testing moves beyond HbA1c toward continuous metrics, and cardiovascular panels now package GFAP and D-dimer into portable stroke triage kits. Prenatal screening shifts to noninvasive maternal blood assays, enhancing safety and comfort. Each domain taps overlapping microfluidic and AI infrastructures, enhancing vendors' economies of scope.

By End User: Homecare Transforms Service Delivery

Hospitals delivered 41.22% sales in 2024 as centralized reference centers, yet growth tilts toward home care and remote-collection services, forecast at 9.84% CAGR. Consumers, accustomed to COVID-19 self-tests, adopt mail-in genomic panels and finger-prick metabolic trackers. Telehealth providers bundle diagnostics with virtual consults, widening the body fluid collection and diagnostics market.

Independent laboratories scale specialized workflows by acquiring AI-pathology firms—Quest Diagnostics’ PathAI deal illustrates the trend. Clinics and physician offices embrace cartridge-based analyzers for same-visit decisions, while research centers validate multi-omics panels that seed next-cycle commercial offerings.

Geography Analysis

North America generated 37.53% of 2024 revenue, supported by reimbursement clarity and early adoption of liquid-biopsy and AI-augmented platforms. Joint eSTAR submissions between the FDA and Health Canada reduce filing duplication, so innovators reach the broader market faster. Value-based-care incentives push providers to deploy rapid testing that curbs inpatient stays, further entrenching the body fluid collection and diagnostics market.

Asia-Pacific is set for a 9.12% CAGR, driven by large-scale digital health investments and universal health coverage expansion in economies such as India, Indonesia, and Vietnam. The Asian Development Bank’s Digital Development Facility finances AI pilots in public hospitals, while Australia’s National Digital Health Strategy prioritizes genomics integration—together, they are enlarging the body fluid collection and diagnostics market across the region.

Europe advances under the Medical Device Regulation and the In Vitro Diagnostic Regulation, which demand transparent clinical-evidence dossiers but reward compliant manufacturers with continent-wide market access. The European Liquid Biopsy Society’s 2024 summit unified 93 institutions on assay standardization, smoothing oncology test uptake. Middle East and Africa roll out mobile labs to remote communities, and South America’s public-private partnerships accelerate point-of-care deployment—collectively widening the global footprint of the body fluid collection and diagnostics market.

Competitive Landscape

The market remains moderately fragmented. BD, Abbott, and Roche integrate vertically—pairing collection devices with analytics and AI interpretation engines. Roche’s tie-up with LumiraDx boosts near-patient immunoassay throughput in under 12 minutes. Becton Dickinson validated MiniDraw, shrinking venous workflows to a fingertip.

M&A activity intensifies: bioMérieux bought SpinChip Diagnostics to secure 10-minute cartridge immunoassays. Quest Diagnostics acquired PathAI Diagnostics, underscoring digital pathology’s strategic value. Meanwhile, startups exploit niche biomarkers or specialty polymers to leapfrog incumbents, though supply-chain hurdles and regulatory complexity can slow scale-up.

Strategic partnerships between diagnostics firms and cloud-data companies aim to harness predictive analytics; Danaher’s tie-in with Innovaccer exemplifies convergence between lab science and patient-record platforms. Wearable-sensor entrants backed by med-tech giants (for example, Medtronic’s alliance with Philips on patient monitoring) further blur industry borders, widening competitive stakes.

Body Fluid Collection And Diagnostics Industry Leaders

BD

F. Hoffmann-La Roche AG

Abbott Laboratories

Danaher

Thermo Fisher Scientific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Guardant Health introduced nearly a dozen smart liquid-biopsy applications for Guardant360, enabling molecular profiling, cancer subtyping, and HLA genotyping from a single blood draw.

- March 2025: Becton Dickinson reported studies confirming MiniDraw capillary collection accuracy is equivalent to that of venous sampling.

- February 2025: Labcorp launched Plasma Complete liquid biopsy with 521-gene coverage and 0.1% variant sensitivity.

- January 2025: Danaher formed a strategic investment partnership with Innovaccer to merge AI diagnostics with unified patient records.

Global Body Fluid Collection And Diagnostics Market Report Scope

| Blood |

| Urine |

| Saliva / Oral Fluid |

| Cerebrospinal Fluid |

| Synovial Fluid |

| Others |

| Collection Devices | Needles & Syringes |

| Vacutainer Tubes | |

| Lancets & Capillary Sets | |

| Catheters & Drainage Sets | |

| Swabs / Absorptive Media | |

| Diagnostic Consumables | Reagents & Assay Kits |

| Microfluidic Cartridges | |

| Rapid Test Strips | |

| Instruments | IVD Laboratory Analyzers |

| Point-of-Care Readers | |

| Ancillary Accessories | Tube Holders & Stoppers |

| Transfer & Transport Devices |

| Immunoassay |

| Molecular Diagnostics (PCR/NGS) |

| Clinical Chemistry & Hematology |

| Flow Cytometry & Microfluidics |

| Rapid / Lateral-Flow Tests |

| Wearable & Continuous-Monitoring Sensors |

| Infectious Disease Testing |

| Oncology Liquid Biopsy |

| Diabetes & Metabolic Screening |

| Cardiovascular Diagnostics |

| Nephrology & Renal Function |

| Prenatal & Reproductive Health |

| Others |

| Hospitals |

| Independent Diagnostic Laboratories |

| Blood Banks & Biobanks |

| Clinics & Physician Offices |

| Homecare & Remote Collection |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Fluid Type | Blood | |

| Urine | ||

| Saliva / Oral Fluid | ||

| Cerebrospinal Fluid | ||

| Synovial Fluid | ||

| Others | ||

| By Product Type | Collection Devices | Needles & Syringes |

| Vacutainer Tubes | ||

| Lancets & Capillary Sets | ||

| Catheters & Drainage Sets | ||

| Swabs / Absorptive Media | ||

| Diagnostic Consumables | Reagents & Assay Kits | |

| Microfluidic Cartridges | ||

| Rapid Test Strips | ||

| Instruments | IVD Laboratory Analyzers | |

| Point-of-Care Readers | ||

| Ancillary Accessories | Tube Holders & Stoppers | |

| Transfer & Transport Devices | ||

| By Diagnostic Technology | Immunoassay | |

| Molecular Diagnostics (PCR/NGS) | ||

| Clinical Chemistry & Hematology | ||

| Flow Cytometry & Microfluidics | ||

| Rapid / Lateral-Flow Tests | ||

| Wearable & Continuous-Monitoring Sensors | ||

| By Application | Infectious Disease Testing | |

| Oncology Liquid Biopsy | ||

| Diabetes & Metabolic Screening | ||

| Cardiovascular Diagnostics | ||

| Nephrology & Renal Function | ||

| Prenatal & Reproductive Health | ||

| Others | ||

| By End User | Hospitals | |

| Independent Diagnostic Laboratories | ||

| Blood Banks & Biobanks | ||

| Clinics & Physician Offices | ||

| Homecare & Remote Collection | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the body fluid collection and diagnostics market in 2025?

The body fluid collection and diagnostics market size is valued at USD 9.98 billion in 2025.

What CAGR is expected for body fluid collection and diagnostics between 2025 and 2030?

The market is projected to grow at a 7.52% CAGR over the forecast period.

Which application shows the fastest growth through 2030?

Oncology liquid biopsy leads with an 11.44% CAGR as precision oncology becomes standard practice.

Which geographic region is expected to expand most rapidly?

Asia-Pacific is forecast to post a 9.12% CAGR thanks to digital-health investments and broader insurance coverage.

Why are diagnostic consumables gaining share?

Single-use cartridges and rapid strips match decentralized-testing trends, driving a 10.32% CAGR for consumables.

What factor most restrains adoption in developing economies?

The high capital cost of advanced molecular platforms—often exceeding USD 500,000—limits uptake in many low- and middle-income countries.

Page last updated on: