Medical Gases And Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.29 Billion |

| Market Size (2031) | USD 27.03 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

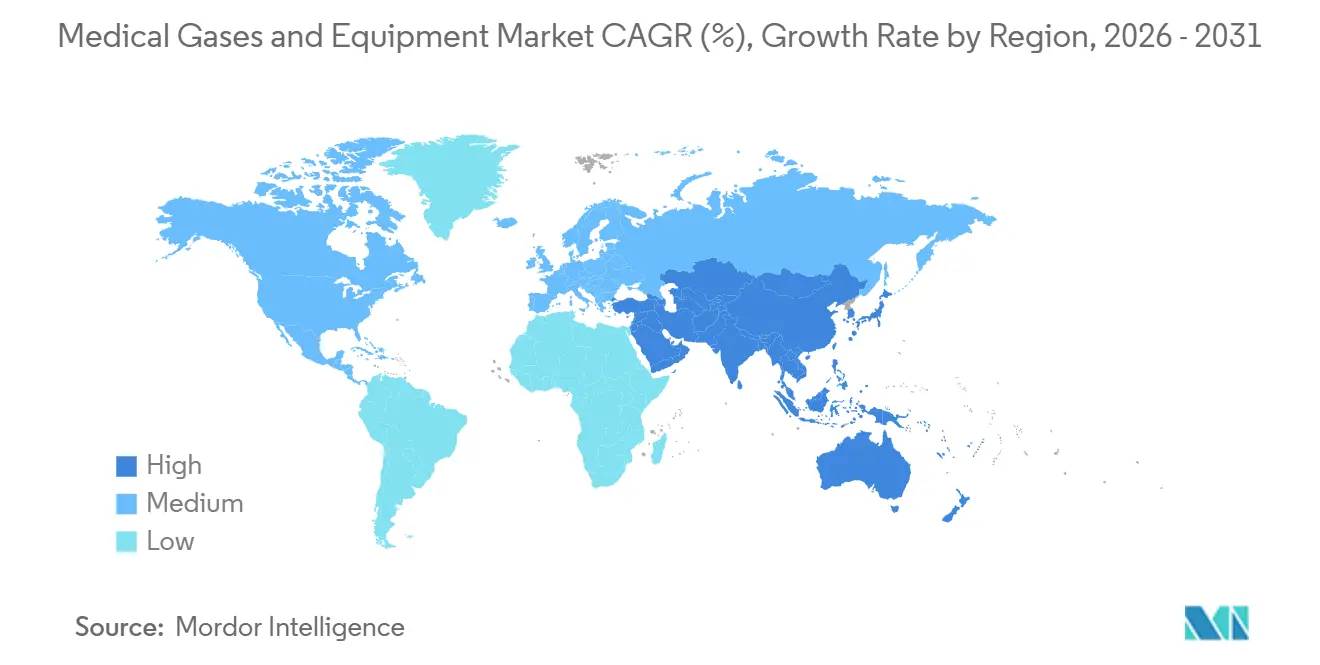

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Gases And Equipment Market Analysis by Mordor Intelligence

The Medical Gases And Equipment Market size is projected to be USD 18.12 billion in 2025, USD 19.29 billion in 2026, and reach USD 27.03 billion by 2031, growing at a CAGR of 6.98% from 2026 to 2031.

Growing reliance on home-based long-term oxygen therapy, hospitals switching from cylinders to on-site PSA plants, and rapid miniaturization of portable concentrators are reshaping demand across every major region. COPD prevalence reached 569.2 million cases in 2025, yet falling mortality is creating a larger cohort that needs multi-year oxygen support. U.S. reimbursement rules bundle oxygen devices into ASC payments, compressing supplier margins and pushing device makers to integrate vertically. Simultaneously, helium scarcity is catalyzing investment in closed-loop MRI cooling and helium-free magnets, pulling specialty gases and equipment into new technology cycles.

Key Report Takeaways

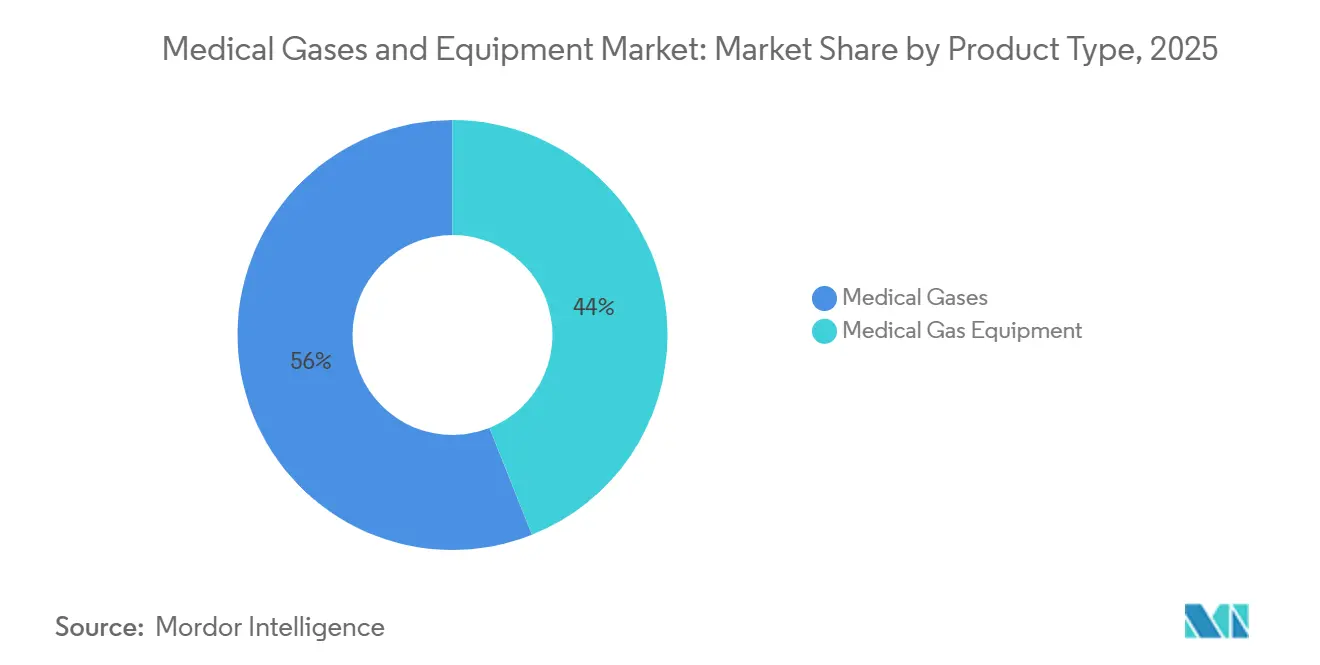

- By product type, medical gases led with 56.02% of the medical gases and equipment market share in 2025, while equipment trailed but remains essential as PSA adoption scales up in hospitals.

- By gas type, oxygen dominated the medical gases and equipment market with a 34.27% share in 2025; the helium & others subsegment is advancing at a 10.73% CAGR through 2031.

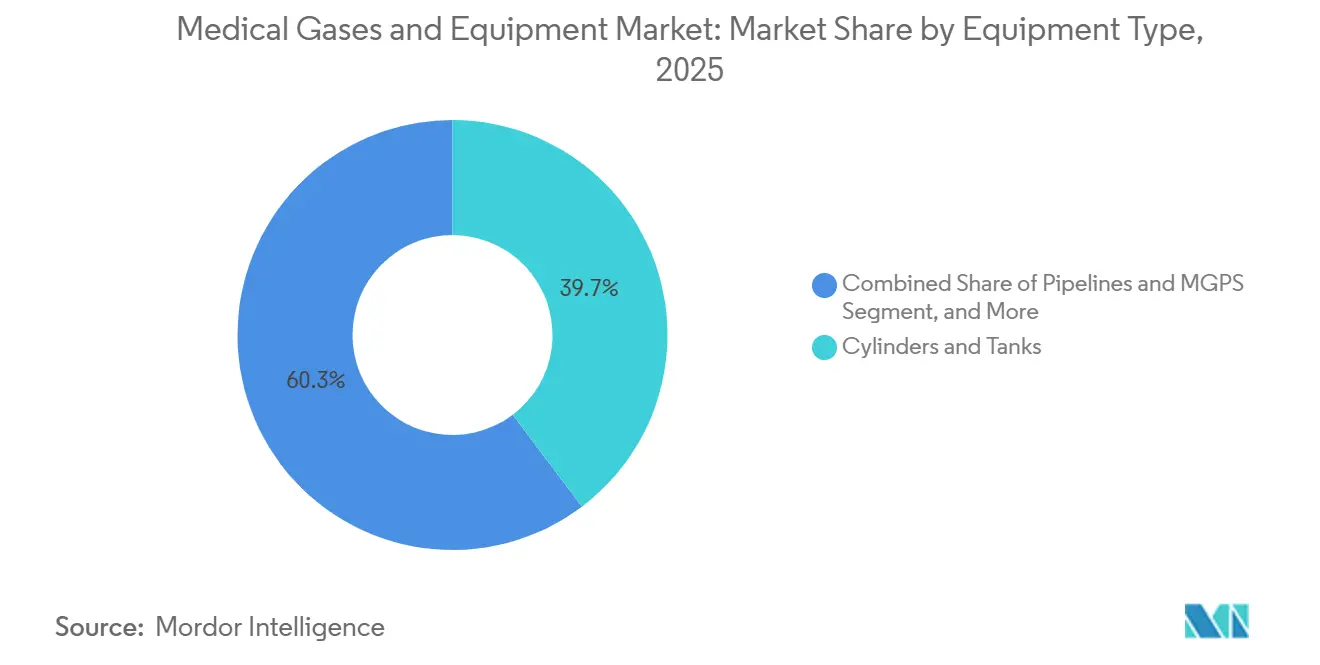

- By equipment type, cylinders and tanks accounted for 39.72% in 2025; however, vacuum and compressor systems are forecast to post a 9.12% CAGR through 2031.

- By application, therapeutic uses accounted for 47.78% of demand in 2025; diagnostic & imaging is the fastest-growing application, with a 9.38% CAGR through 2031.

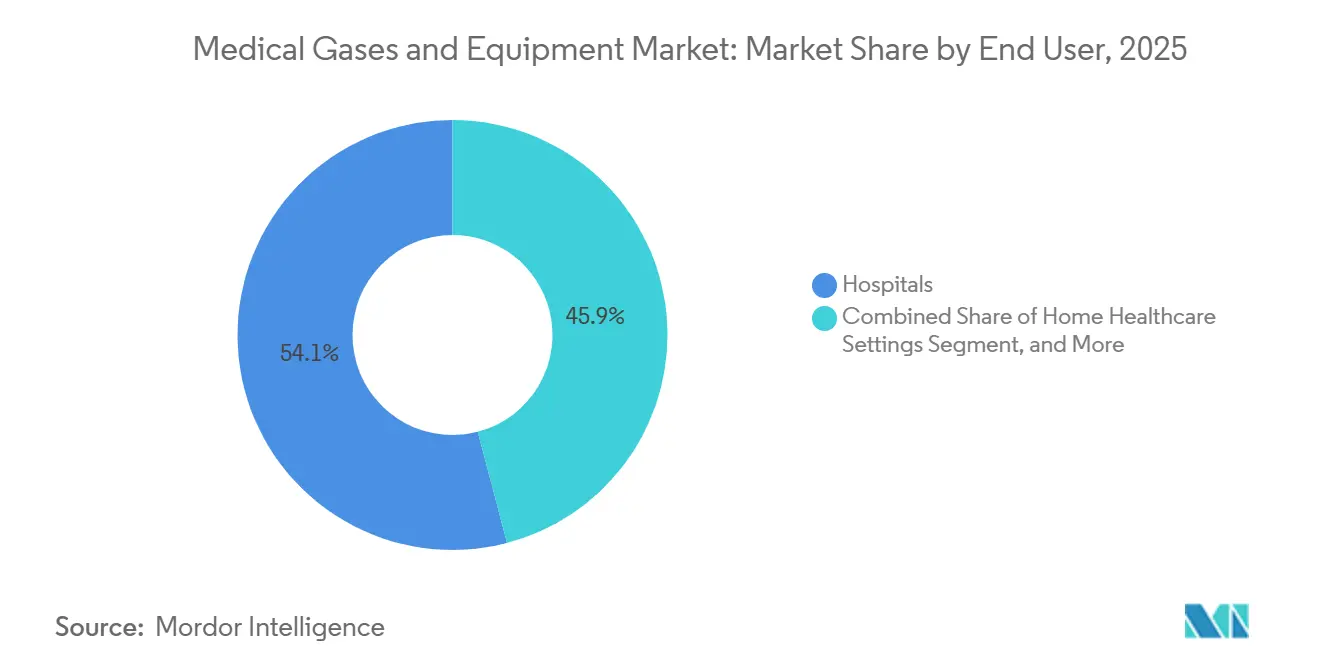

- By end user, hospitals accounted for 54.08% of revenue share in 2025, while home healthcare settings are projected to expand at an 8.42% CAGR during 2026-2031.

- By geography, North America accounted for 41.78% of the value in 2025; Asia-Pacific is the fastest-growing region, with a 11.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Gases And Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Rise in Chronic Respiratory Diseases | +1.8% | Global, acute in South Asia and Sub-Saharan Africa | Medium term (2-4 years) |

| Aging Population Boosting Long-Term Oxygen Therapy | +1.5% | North America, Europe, Japan | Long term (≥ 4 years) |

| Expansion of Surgical & Diagnostic Procedures | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Home-Healthcare Shift Driving Portable Equipment Demand | +1.4% | North America, Western Europe | Short term (≤ 2 years) |

| On-Site PSA Plants Adoption in Emerging Hospitals | +0.9% | Asia-Pacific, Middle East & Africa, South America | Long term (≥ 4 years) |

| Miniaturization of Portable Concentrators & Sensors | +0.7% | Global, earliest uptake in North America and Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Rise in Chronic Respiratory Diseases

Global COPD and asthma cases climbed to 569.2 million in 2025, yet age-standardized COPD mortality declined 30% between 2000 and 2019[1]World Health Organization, “Chronic Obstructive Pulmonary Disease,” who.int . Longer survival is driving millions of dollars into continuous home oxygen therapy, especially in regions with limited refill infrastructure. Europe logged 81.7 million respiratory cases in 2024, with COPD representing 32 million. South Asian and African patients experience an earlier onset due to indoor biomass smoke exposure, pushing governments to subsidize stationary and portable concentrators.

Aging Population Boosting Long-Term Oxygen Therapy

People aged 65 years and older accounted for 10% of the world's population in 2024 and will reach 16% by 2050[2]United Nations, “World Population Aging,” un.org . A 2024 meta-analysis showed that using oxygen for more than 15 hours daily extends hypoxemic COPD survival by 3.5 years. Japan expanded coverage for nocturnal oxygen therapy in 2025, adding roughly 120,000 eligible patients. Lightweight 2-kilogram devices with 8-hour batteries improve adherence among frail seniors and underpin growth in the medical gases and equipment market.

Expansion of Surgical & Diagnostic Procedures

U.S. robotic-assisted surgeries grew 8.3% year-over-year in 2025, and each procedure consumes 50-100 liters of medical-grade CO₂ and ancillary anesthetic gases. Ambulatory surgical centers performed 28 million cases in 2025 after new CMS coverage additions. MRI scans still rely on liquid helium, but helium-free magnets from Siemens Healthineers slash per-scan helium use by 95%.

Home-Healthcare Shift Driving Portable Equipment Demand

Bundled ASC payments push hospitals to discharge patients with portable concentrators, stimulating a 34% rise in tele-monitored home oxygen users in 2025. The FDA cleared 47 sub-2-kilogram concentrators in 2025, and reimbursement rose 3.2% under the 2026 DME fee schedule. Telemedicine platforms cut emergency visits by 18%, validating the economic case for remote monitoring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Purity & Safety Regulations | –0.6% | Global, tighter in EU and North America | Medium term (2-4 years) |

| Global Helium Shortage Affecting Specialty Gases | –0.9% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| High Cap-Ex for Pipeline & Manifold Installations | –0.5% | Asia-Pacific, Middle East & Africa | Long term (≥ 4 years) |

| Tariff-Driven Supply-Chain Volatility | –0.4% | North America, spillover to Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Purity & Safety Regulations

USP and Ph.Eur. require 99.5% oxygen purity and moisture below 67 ppm, forcing hospitals to install inline analyzers that cost USD 15,000-25,000 each. Quarterly pipeline testing adds USD 8,000-12,000 in annual overhead for a 200-bed facility. Divergent rules between China’s NMPA and overseas markets add up to USD 80,000 per product line and six-month delays, slowing new device launches.

Global Helium Shortage Affecting Specialty Gases

BLM reserve depletion doubled spot prices to USD 15 per cubic meter in 2025. MRI refill costs now reach USD 18,000 per magnet. France issued allocation rules that prioritize NICU cases, constraining adult access[3]Agence Nationale de Sécurité du Médicament, “Helium Allocation Guidelines,” ansm.sante.fr. New supply from Qatar and Russia may ease shortages post-2027, but geopolitical risks keep Western buyers exposed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Medical Gases Sustain Revenue Momentum

Medical gases generated 56.02% of the medical gases and equipment market revenue in 2025, and this segment is forecast to grow at 7.87% annually through 2031. Persistent COPD therapy, wider helium demand in imaging, and PSA cost advantages keep consumption recurring even as reimbursement tightens. In contrast, equipment sales lag because pipelines, manifolds, and monitors last 15-20 years and are increasingly bundled into procedural payments. Nonetheless, IoT-enabled manifolds are extending service revenue and anchoring buyers to premium brands, a dynamic that supports overall expansion of the medical gases and equipment market.

Specialty gases such as nitrous oxide, carbon dioxide, and medical air command premium prices due to purity controls. Nitrous oxide must reach 99% purity, whereas medical air compressors must achieve –40 °C dew points. Suppliers are embedding predictive maintenance sensors that cut downtime 25% and push hospitals toward multiyear service contracts. Those advances sustain margins even as competitive bidding intensifies.

By Gas Type: Helium Scarcity Alters Investment Patterns

Oxygen led with 34.27% of 2025 revenue, but helium & others will outpace all gases at 10.73% CAGR as MRI operators retrofit recovery systems and shift to conduction-cooled magnets. The medical gases and equipment market size for helium recovery and helium-free MRI is forecast to reach USD 1.8 billion by 2030. Nitrous oxide usage tracks the 6.2% rise in global surgical volumes, while carbon dioxide mirrors laparoscopic adoption at 7.8% growth in 2025. Converters moving to energy-efficient oxygen concentrators in home care reduce liquid oxygen consumption but create a backfill of demand for high-purity oxygen in neonatal and hyperbaric applications.

By Equipment Type: Vacuum & Compressor Systems Capture Growth

Cylinders & tanks still account for 39.72% of equipment value, yet vacuum and compressor systems are set to grow 9.12% annually as robotic procedures stretch suction requirements. NFPA 99 requires redundant pumps capable of –300 to –500 mmHg, prompting hospitals to upgrade legacy single-pump installations. Meanwhile, copper pipeline retrofits to ISO 7396-1 standards spur orders for alarm panels and zone valves, but long life cycles mean replacement waves occur only every two decades, affecting the cadence of equipment revenue inside the medical gases and equipment market.

By Application: Imaging Outpaces Therapy in Growth

Therapy remains the largest application at 47.78% of 2025 demand, yet diagnostic & imaging is the fastest mover with a 9.38% CAGR through 2031. U.S. MRI volumes rose to 42 million scans in 2025, lifting helium demand unless operators shift to helium-free magnets. Pharmaceutical manufacturing consumes increasing volumes of nitrogen for inerting and oxygen for fermentation as FDA continuous-process guidelines gain traction, reinforcing multigas supply contracts.

By End User: Home Healthcare Climbs on Reimbursement Clarity

Hospitals continue to dominate with 54.08% share, but home healthcare’s 8.42% CAGR underscores a payer drive to cut inpatient costs. Medicare now reimburses USD 156 monthly for the first quarter of portable concentrator use, improving economics for DME providers. Tele-monitoring lowers unplanned hospitalizations 18%, offering clear value propositions that accelerate patient uptake and bolster the long-run outlook for the medical gases and equipment market.

Geography Analysis

North America accounted for 41.78% of 2025 revenue, supported by USD 2.1 billion in Medicare and Medicaid outlays for home oxygen equipment. FDA 510(k) clearances for sub-2-kilogram concentrators hit 47 in 2025, highlighting a robust innovation cadence. Section 301 tariffs, ranging from 7.5% to 25%, are prompting U.S. assemblers to source valves from Mexico, although longer lead times test just-in-time models. Canadian provinces are piloting remote oxygen monitoring, with Ontario reporting a 22% reduction in emergency visits in a 2025 trial.

Europe’s demand benefits from strict ISO 7396-1 compliance requirements and the EMA’s 2025 Annex 1 revision, which mandates real-time oxygen monitoring. Germany, the U.K., France, Italy, and Spain together create more than 60% of regional volume. The U.K.’s HTM 02-01 guidance obliges annual pipeline integrity tests costing up to USD 13,000 per hospital. Carbon Border Adjustment levies, effective 2026, will add EUR 4-7 per imported cylinder, nudging buyers toward lighter composite models.

Asia-Pacific is the fastest-growing region, albeit from a lower base, at a 11.57% CAGR through 2031. China’s plan to add 500,000 beds by 2027 and mandate PSA plants in 40% of new hospitals channels vast capex into local generation. India’s Ayushman Bharat program expanded insurance coverage to 550 million citizens by late 2025, boosting oxygen demand in tier-2 cities. Japan’s aging society is fueling a surge in nocturnal oxygen therapy, and South Korea raised portable concentrator reimbursement by 8% in 2025.

Middle East & Africa and South America remain smaller but are investing in resilience. Saudi Arabia is spending USD 12 billion to boost hospital capacity by 25% and requires ISO-compliant PSA systems in new builds. In 2025, South Africa purchased 1,200 concentrators for rural clinics. Brazil’s SUS added home oxygen coverage for 180,000 COPD patients, yet reimbursement trails private insurers by 35%, limiting equipment uptake.

Competitive Landscape

The medical gases and equipment market shows moderate consolidation. Air Liquide, Linde, and Air Products supply more than half of global bulk gases by locking hospitals into 10- to 15-year contracts backed by ISO 13485 quality systems. In contrast, equipment supply is fragmented: regional pipeline fabricators, niche concentrator brands, and valve manufacturers compete for market share through customization and rapid service. Inogen and CAIRE captured 18% of the U.S. home oxygen channel in 2025 by selling direct and offering telehealth support. Siemens Healthineers and GE HealthCare each disclosed 20+ helium-recovery patents in 2025, a defensive hedge against supply shortages. Predictive analytics differentiates equipment: BeaconMedaes’ SmartCare flags valve failures 45 days in advance, cutting downtime by 28%. Tariff shocks are accelerating the reshoring of valve machining to Mexico under USMCA rules.

Medical Gases And Equipment Industry Leaders

Linde plc

Air Liquide S.A.

Atlas Copco AB

Amico Corporation

Messer SE & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: BeaconMedaes Pipeline Solutions launched three new systems to enhance safety: the MPR Pressure Reducing Set, MER Emergency Reserve Manifold, and LBV Line Ball Valve Assemblies.

- February 2025: Linde announced record wins for small on-site solutions in 2024, signing 59 long-term agreements to build and operate 64 nitrogen and oxygen plants, driven by electronics manufacturing growth and decarbonization initiatives.

- January 2025: Messer announced plans to invest over USD 70 million in air separation operations in Berryville, Arkansas, creating more than 20 jobs with production beginning in the second half of 2026.

Global Medical Gases And Equipment Market Report Scope

As per the scope of this report, medical gases and equipment are defined as gases and equipment used for therapeutic diagnosis and curative purposes, as well as for pharmaceutical and biotechnology research.

The segmentation for the medical gases and equipment market is segmented by product type, gas type, equipment type, application, end user, and geography. By product type, it includes medical gases and medical gas equipment. By gas type, the market is segmented into oxygen, nitrous oxide, medical air, carbon dioxide, nitrogen, and helium & others. By equipment type, it covers cylinders & tanks, pipelines & MGPS, manifolds & regulators, vacuum & compressor systems, and monitoring & alarm systems. By application, the market is divided into therapeutic, diagnostic & imaging, and pharmaceutical manufacturing & research. By end user, the segmentation includes hospitals, ambulatory surgical centers, home healthcare settings, and academic & research institutions. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (in USD) for the above segments. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

| Medical Gases |

| Medical Gas Equipment |

| Oxygen |

| Nitrous Oxide |

| Medical Air |

| Carbon Dioxide |

| Nitrogen |

| Helium & Others |

| Cylinders & Tanks |

| Pipelines & MGPS |

| Manifolds & Regulators |

| Vacuum & Compressor Systems |

| Monitoring & Alarm Systems |

| Therapeutic |

| Diagnostic & Imaging |

| Pharmaceutical Manufacturing & Research |

| Hospitals |

| Ambulatory Surgical Centers |

| Home Healthcare Settings |

| Academic & Research Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Medical Gases | |

| Medical Gas Equipment | ||

| By Gas Type | Oxygen | |

| Nitrous Oxide | ||

| Medical Air | ||

| Carbon Dioxide | ||

| Nitrogen | ||

| Helium & Others | ||

| By Equipment Type | Cylinders & Tanks | |

| Pipelines & MGPS | ||

| Manifolds & Regulators | ||

| Vacuum & Compressor Systems | ||

| Monitoring & Alarm Systems | ||

| By Application | Therapeutic | |

| Diagnostic & Imaging | ||

| Pharmaceutical Manufacturing & Research | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Home Healthcare Settings | ||

| Academic & Research Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will demand for portable concentrators grow through 2031?

Portable concentrators remain the chief driver for home healthcare, and units lighter than 2 kg underpin an 8.42% CAGR through 2031 in home settings reported for the medical gases and equipment market.

Which gas type will post the highest growth?

Helium & other specialty gases are forecast to rise at a 10.73% CAGR through 2031 as MRI operators pivot to recovery systems and helium-free magnets.

What is the primary factor restraining new pipeline projects in emerging markets?

Up-front capital of USD 220,000-280,000 for a mid-sized hospital and currency volatility delay installations despite long-term cost savings.

Why are PSA plants spreading quickly in Asia-Pacific hospitals?

On-site oxygen generation cuts delivered gas costs from USD 0.25 to USD 0.08 per cubic meter and aligns with government mandates in China and India.

Page last updated on: