Blood Transfusion Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

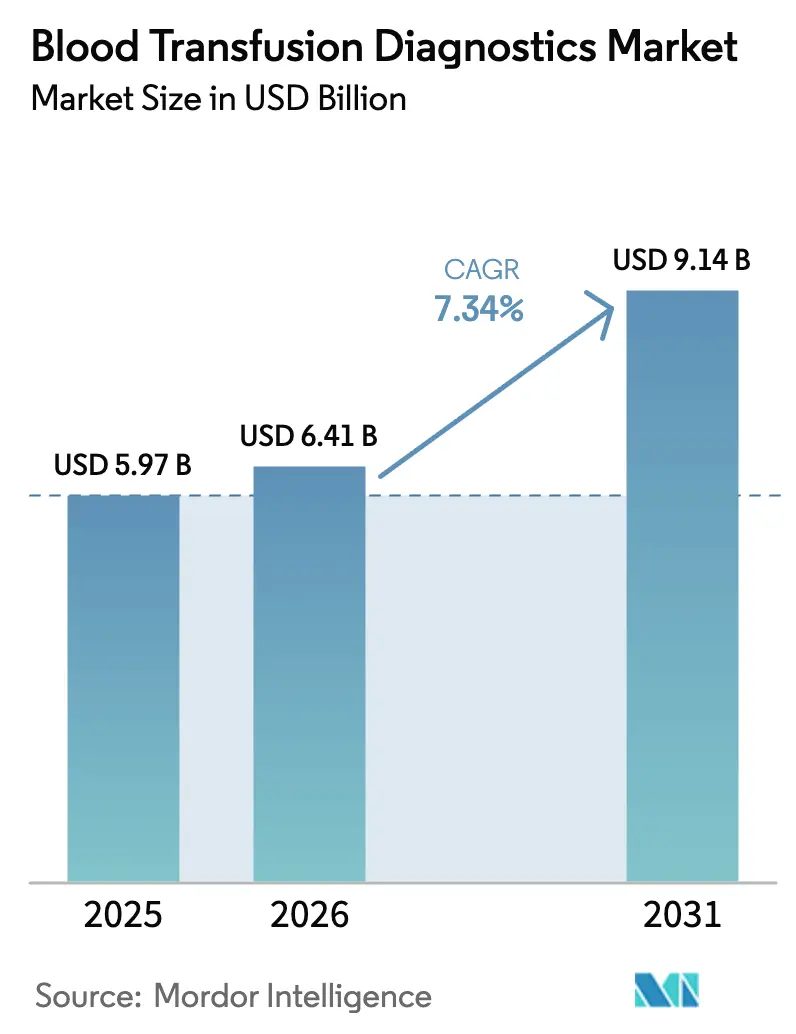

| Market Size (2026) | USD 6.41 Billion |

| Market Size (2031) | USD 9.14 Billion |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Transfusion Diagnostics Market Analysis by Mordor Intelligence

Blood transfusion diagnostics market size in 2026 is estimated at USD 6.41 billion, growing from 2025 value of USD 5.97 billion with 2031 projections showing USD 9.14 billion, growing at 7.34% CAGR over 2026-2031. Growth reflects the United States Food and Drug Administration’s decision to place laboratory-developed tests under full device regulations, widespread deployment of high-throughput nucleic acid testing platforms, and expanding donor-to-patient safety programs across emerging economies[1]U.S. Food and Drug Administration, “Laboratory Developed Tests Final Rule,” fda.gov. Upgrades in automation, artificial-intelligence-driven sample inspection, and fingertip capillary-blood devices shorten turnaround times, reducing staffing pressures in hospitals and blood banks. National donation campaigns in Asia-Pacific and Africa, rising surgical volumes in North America and Europe, and the increasing complexity of trauma care together expand baseline transfusion volumes. Simultaneously, industry players face cost inflation in reagents and logistics, prompting consolidation of purchasing through group-purchasing organizations while favoring manufacturers that already operate under robust quality systems.

Key Report Takeaways

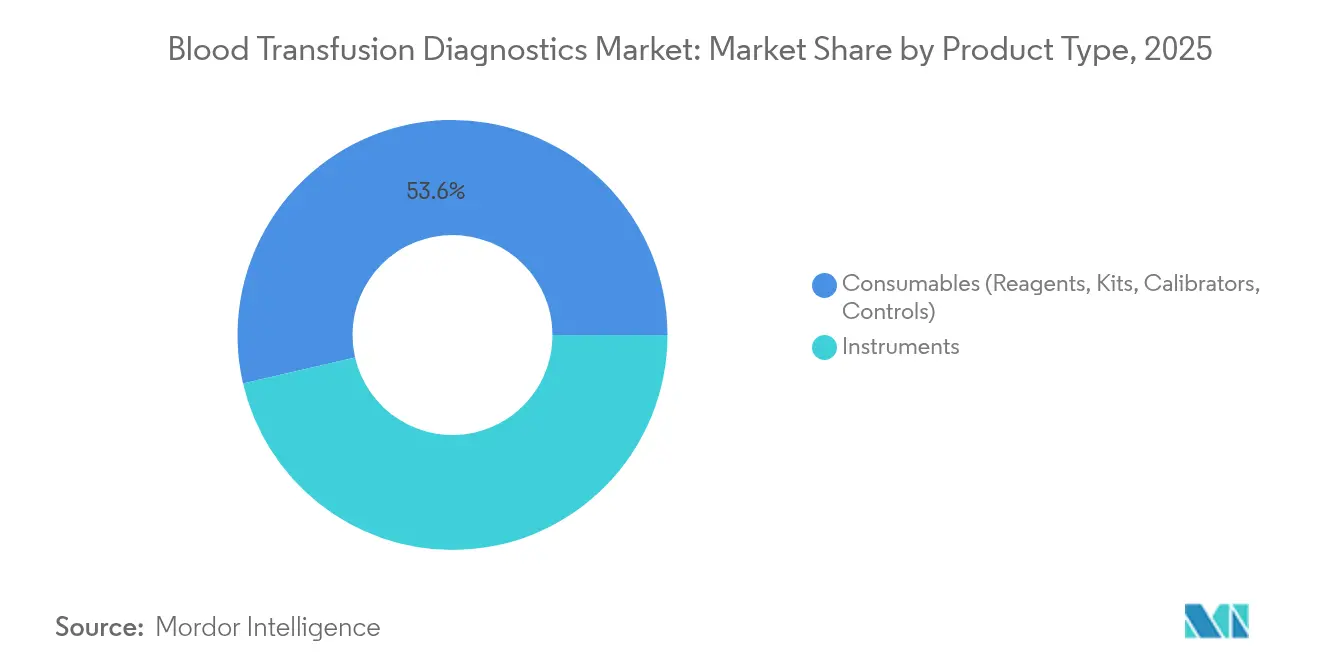

- By product type, consumables led with 53.62% revenue share in 2025, whereas instruments are projected to expand at a 8.95% CAGR to 2031.

- By technology, serology held 45.12% of the blood transfusion diagnostics market share in 2025, while nucleic acid testing records the fastest trajectory at 8.63% CAGR through 2031.

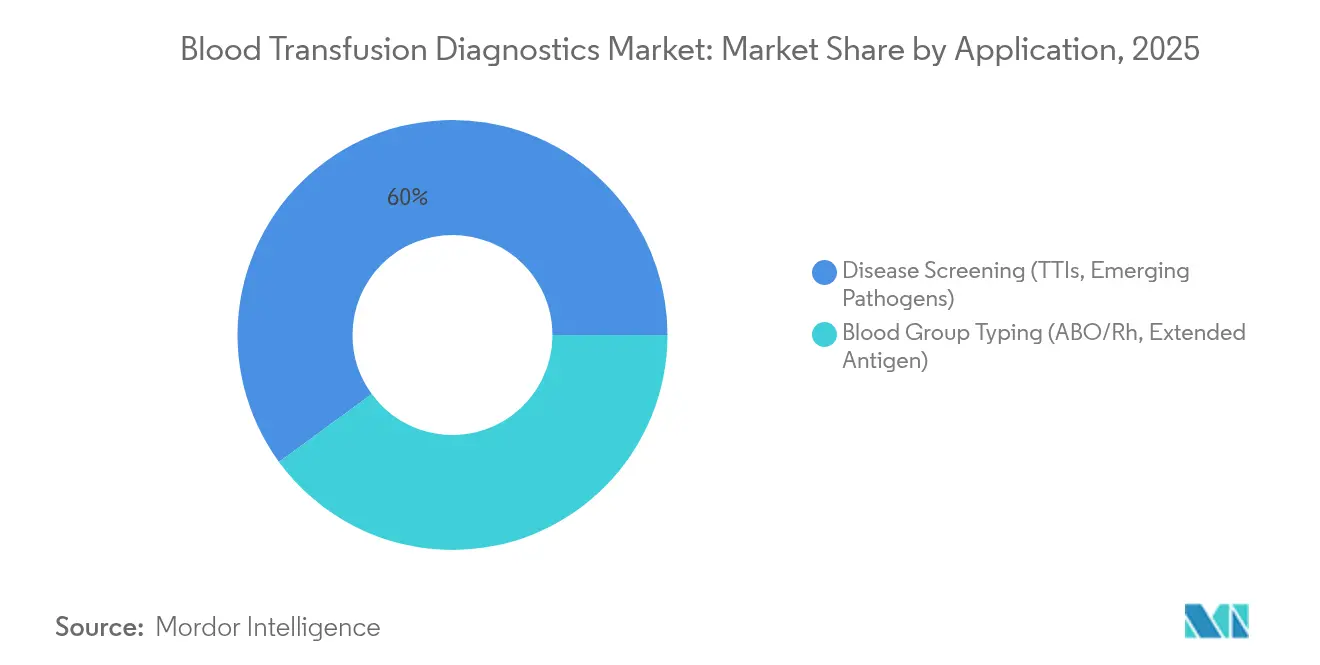

- By application, disease screening accounted for 60.05% of the blood transfusion diagnostics market size in 2025; blood group typing advances at 9.78% CAGR through 2031.

- By end user, hospitals commanded 46.12% share in 2025, yet blood banks show the highest forecast growth at 10.14% CAGR.

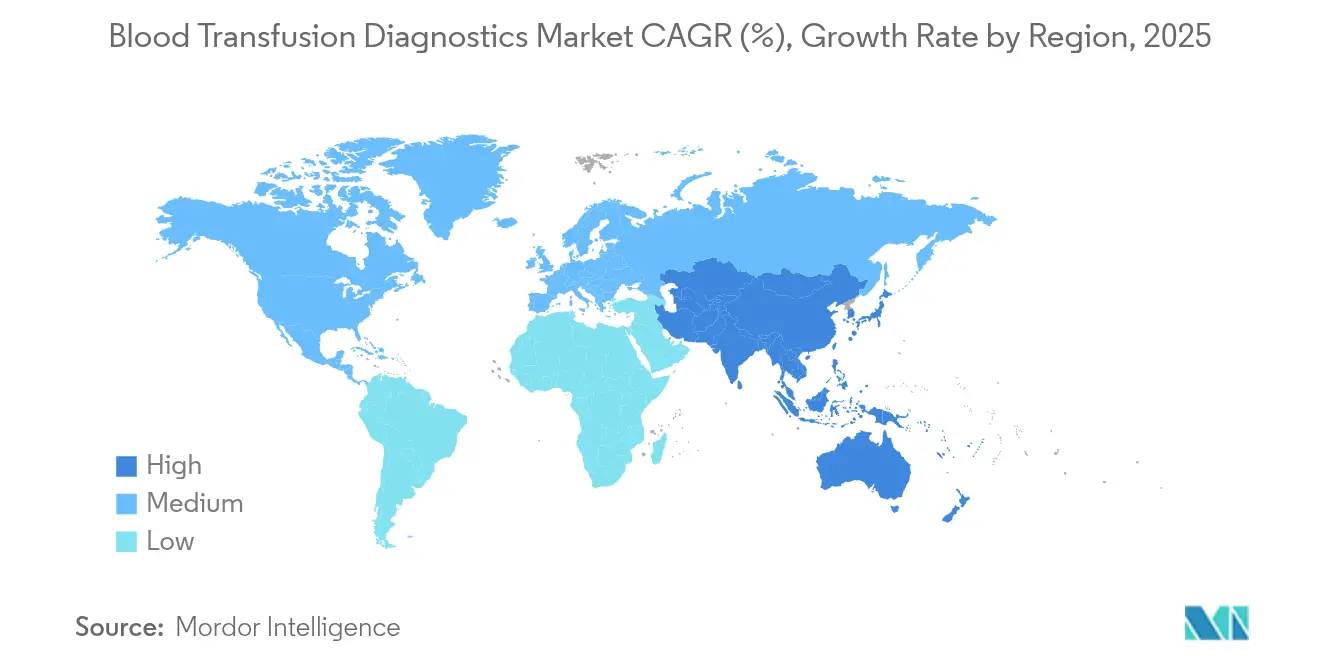

- By region, North America dominated with 39.12% share in 2025; Asia-Pacific is on track for the quickest rise at 8.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Blood Transfusion Diagnostics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global blood donations and transfusion demand | +1.8% | Asia-Pacific and Africa highest | Medium term (2-4 years) |

| Growing incidence of trauma and surgical procedures | +1.5% | Developed markets | Long term (≥ 4 years) |

| Technological advancements in transfusion diagnostics | +2.1% | North America & Europe lead | Short term (≤ 2 years) |

| Integration of point-of-care testing in blood banks | +1.2% | North America & Europe early adopters | Medium term (2-4 years) |

| Expansion of healthcare infrastructure in emerging markets | +1.6% | Core momentum in Asia-Pacific | Long term (≥ 4 years) |

| Adoption of cloud-based blood bank information systems | +0.9% | Faster uptake in high-income regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Blood Donations and Transfusion Demand

Voluntary donor drives and hemovigilance programs stimulate steady growth for the blood transfusion diagnostics market. China’s National Health Commission partners with youth organizations to broaden group donations, while India’s Hemovigilance Program trains more than 15,000 clinicians to improve adverse-event reporting[2]National Health Commission of the People’s Republic of China, “Youth Group Donation Initiative,” chinacdc.org. In the United States, college competitions supported by Abbott Laboratories raise public awareness, and Cerus Corporation’s INTERCEPT pathogen-reduction kits safeguard platelet and plasma components. Europe continues to call for 2 million extra donors to lessen import dependence, underscoring global supply challenges.

Growing Incidence of Trauma and Surgical Procedures

The blood transfusion diagnostics market benefits from rising trauma care complexity and higher surgical case loads. The 2025 Medicare Physician Fee Schedule recognizes pre-hospital transfusion as advanced life support, increasing reimbursement for ambulance providers that stock blood. A large Midwest academic center reported 323 massive transfusion activations in 2024, a 7% increase year on year. Point-of-care coagulation analyzers now guide intraoperative decisions, and machine-learning dashboards predict inventory surges, cutting wastage.

Technological Advancements in Transfusion Diagnostics

Next-generation platforms strengthen the blood transfusion diagnostics market by shortening diagnostic windows. Roche’s cobas Malaria assay, the first molecular malaria test cleared for U.S. donor screening, complements multiplex viral NAT panels. Metagenomic sequencing from Karius detects more than 1,000 pathogens in a single sample, tripling bloodstream infection detection versus culture methods. Deep-learning modules integrated into automated workstations improve buffy-coat recognition accuracy, streamlining nucleic-acid extraction.

Integration of Point-of-Care Testing in Blood Banks

Fingertip capillary sampling devices launched by BD and Babson Diagnostics need just six drops of blood, letting non-phlebotomists collect specimens. The FDA’s authorization of the first point-of-care hepatitis C RNA test delivers confirmatory results in one hour. bioMérieux’s acquisition of SpinChip Diagnostics adds a handheld immunoassay platform that produces lab-quality results within 10 minutes. Sysmex’s automated hematology analyzer with blood-bank mode counts residual leukocytes, raising efficiency in component processing.

Restraints Impact Analysis of Blood Transfusion Diagnostics Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced diagnostic instruments | -1.4% | Greatest drag in emerging markets | Medium term (2-4 years) |

| Stringent regulatory approval processes | -1.1% | Global, most stringent in Europe | Long term (≥ 4 years) |

| Limited availability of rare blood reagents | -0.8% | Worldwide supply-chain concentration | Short term (≤ 2 years) |

| Fragmented donor traceability systems | -0.6% | Primarily emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Diagnostic Instruments

Price tags on high-throughput analyzers restrain adoption in resource-constrained settings, challenging broader penetration of the blood transfusion diagnostics market. Routine assay reimbursements continue to drop, forcing laboratories to cross-subsidize molecular test investments. The FDA estimates annual compliance costs up to USD 3.56 billion as laboratory-developed tests transition to full device oversight. Hospital outpatient departments still bill three times more for identical tests than independent labs, underscoring procurement asymmetries[3]Health Care Cost Institute, “National Hospital Pricing Report,” healthcostinstitute.org.

Stringent Regulatory Approval Processes

Four-year phase-in periods for quality-system compliance and Europe’s In Vitro Diagnostic Regulation impose new documentation burdens. Hematology laboratories report that 75% of their in-house assays presently lack CE-marked equivalents, necessitating costly validations. The upcoming Regulation on Substances of Human Origin aims to unify European oversight yet demands IT upgrades and new donor-traceability rules for blood establishments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Blood Transfusion Diagnostics Market Segment Analysis

By Product Type:

Consumables Sustain Revenue Momentum, Instruments Trigger Upgrade CyclesConsumables generated 53.62% of the 2025 blood transfusion diagnostics market. Continuous demand for reagents, calibrators, and quality-control materials provides steady cash flows, especially as test menus now include malaria, Babesia, and Zika screening. Integrated cartridge designs minimize pipetting errors while lowering hands-on time.

The instrument segment is expected to advance at a 8.95% CAGR through 2031. AI-enhanced vision systems within new centrifuge and reader platforms drive throughputs exceeding 400 samples per hour. Partnerships such as the Siemens Healthineers–Sysmex supply deal illustrate how manufacturers combine hemostasis, immunohematology, and NAT modules within single middleware ecosystems. The blood transfusion diagnostics market size attributable to new instrument placements is set to widen as leasing models and reagent-rent contracts lower upfront capital barriers.

By Technology:

Serology Holds Ground, Nucleic Acid Testing Gains SpeedSerology retained 45.12% of revenue in 2025, capitalizing on cost-efficient enzyme-linked and chemiluminescent assays that fit legacy analyzers. Reagent refinements cut false positives, preserving donation throughput.

Nucleic acid testing exhibits the highest growth at 8.63% CAGR, narrowing diagnostic windows and improving blood safety. Roche’s cobas systems now screen tens of millions of donations annually for HIV, HBV, HCV, and malaria. The blood transfusion diagnostics market share associated with NAT platforms will expand further as regulators mandate multiplex screening for additional pathogens and as pooling protocols moderate per-donor costs.

By Application:

Disease Screening Dominates, Extended Typing SurgesDisease screening activities contributed 60.05% of total 2025 revenue. Mandatory viral testing and growing concern over vector-borne diseases sustain reagent pull-through. Middleware links donor records to national surveillance dashboards, improving outbreak response.

Blood group typing advances at a 9.78% CAGR. Laboratories now pursue extended antigen profiling to prevent alloimmunization, fueled by next-generation microarray and molecular kits. The blood transfusion diagnostics market size devoted to genotypic typing grows as payers acknowledge the downstream cost savings of reduced transfusion reactions.

By End User:

Hospitals Dominate, Blood Banks Accelerate DigitalizationHospitals accounted for 46.12% of 2025 revenue, leveraging in-house transfusion services to support trauma, oncology, and transplant programs. Integration with electronic medical records streamlines cross-department sample tracking.

Blood banks are projected to grow at 10.14% CAGR. Terumo BCT’s Reveos system trims manual processing from 26 to 9 steps, improving platelet yields. Cloud-based information systems offer predictive analytics for component usage, attracting smaller regional centers that previously lacked advanced informatics. The blood transfusion diagnostics industry is witnessing rapid skill-mix changes, with software specialists joining traditional laboratory teams.

Geography Analysis

North America Blood Transfusion Diagnostics Market

North America held 39.12% of global revenue in 2025. FDA guidance on device regulation and Medicare’s elevation of pre-hospital transfusion drive demand for high-sensitivity assays. Becton Dickinson’s USD 10 million domestic expansion underscores efforts to shorten supply chains. Persistent price gaps—hospital outpatient departments bill three times what independent labs charge—shape purchasing strategies.

APAC Blood Transfusion Diagnostics Market

Asia-Pacific is forecast to rise at an 8.31% CAGR, the strongest worldwide. China’s Healthy China 2030 plan funds modern blood-collection centers and supports Terumo BCT’s USD 15 million localization investment. India’s nationwide hemovigilance program lifts clinician competence, while Southeast Asian countries pilot cloud-based donor registries. Heterogeneous reimbursement and fragmented supply chains remain barriers, yet urban hospitals continue to adopt NAT and automation platforms.

Europe Blood Transfusion Diagnostics Market

Europe retains a substantial position amid unique supply and regulatory challenges. The region needs 2 million additional donors to cut reliance on imported plasma, a gap that primes demand for donor-recruitment analytics. Implementation of the Regulation on Substances of Human Origin will harmonize oversight by 2027, but labs must bridge gaps created by the In Vitro Diagnostic Regulation’s stricter evidence requirements. The blood transfusion diagnostics market continues to benefit from public-sector funding aimed at achieving self-sufficiency.

Competitive Landscape

The blood transfusion diagnostics market features medium concentration. Global leaders—Roche, Abbott, Grifols, and Danaher—combine regulatory expertise, broad assay menus, and global distribution. Roche’s dual approvals for malaria and Lp(a) tests demonstrate how expansive R&D pipelines secure first-mover advantage. Abbott aligns brand visibility with nationwide donor drives, reinforcing its Alinity analyzer footprint.

Strategic acquisitions reshape portfolios. BioMérieux’s EUR 111 million purchase of SpinChip Diagnostics secures microfluidic know-how. Werfen’s acquisition of Omixon strengthens next-generation sequencing for transplant diagnostics, while BD invests in Babson’s fingertip-blood technology.

Cost inflation drives hospitals and blood banks toward multi-year reagent-rental contracts that bundle service and informatics. Suppliers respond by embedding predictive maintenance and remote calibration to minimize downtime. Emerging entrants position cloud-native traceability platforms that integrate bar-coding, blockchain, and artificial intelligence, challenging incumbents on data-service features. The blood transfusion diagnostics industry thus balances entrenched equipment ecosystems with digital disruptors targeting workflow efficiency.

Blood Transfusion Diagnostics Industry Leaders

Grifols, S.A.

F. Hoffmann-La Roche Ltd.

Diasorin S.p.A

Bio-Rad Laboratories, Inc.

Quotient Suisse SA

- *Disclaimer: Major Players sorted in no particular order

Blood Transfusion Diagnostics Market Companies Covered in this Report

- Grifols

- Roche

- Abbott Laboratories

- Bio-Rad Laboratories

- Immucor

- Danaher (Beckman Coulter & Cepheid)

- Siemens Healthineers

- DiaSorin

- Werfen (Instrumentation Laboratory)

- Merck KGaA (MilliporeSigma)

- Sysmex Corp.

- QuidelOrtho Corp.

- Fresenius

- Haemonetics Corp.

- Beckton Dickinson

- Thermo Fisher Scientific

- Terumo Corp.

- Trinity Biotech

- bioMérieux

Recent Industry Developments in Blood Transfusion Diagnostics Market

- June 2022: Cerus Corporation promotes INTERCEPT pathogen-reduction kits during World Blood Donor Day.

- May 2025: Fujirebio receives FDA clearance for the Lumipulse G pTau 217/β-Amyloid 1-42 plasma test for Alzheimer’s assessment.

- May 2025: Bio-Rad Laboratories posts Q1 clinical diagnostics revenue of USD 356.8 million, noting higher demand for quality-control products.

- March 2025: FDA approves fitusiran for hemophilia along with the INNOVANCE Antithrombin companion diagnostic.

Blood Transfusion Diagnostics Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the blood transfusion diagnostics market as revenue generated from instruments and consumables that screen, type, and cross-match donated whole blood or components before any transfusion. We include serology analyzers, multiplex NAT platforms, gel cards, microplates, genotyping kits, and their control reagents sold to blood banks, hospital laboratories, and reference centers worldwide.

Scope Exclusion: Therapeutic apheresis systems and post-transfusion patient monitoring assays are outside this boundary.

Segments Covered in This Report

- By Product Type

- Instruments

- Consumables (Reagents, Kits, Calibrators, Controls)

- By Technology

- Serology (ELISA, CLIA, Agglutination)

- Nucleic Acid Tests (PCR, TMA, NAT)

- Microarray & Next-Generation Sequencing

- Rapid / Lateral Flow Assays

- By Application

- Disease Screening (TTIs, Emerging Pathogens)

- Blood Group Typing (ABO/Rh, Extended Antigen)

- By End-User

- Hospitals

- Diagnostic Laboratories

- Blood Banks

- Plasma Fractionation Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed hematologists, blood bank technologists, diagnostics distributors, and hospital buyers in North America, Europe, India, China, and Brazil. The conversations validated adoption curves, average selling prices, and the pace at which multiplex NAT is replacing single-target serology.

Desk Research

We collected baseline data on annual donation volumes, transfusion-transmissible infection rates, and screening mandates from open sources such as the WHO Global Database on Blood Safety, the US FDA Biologics statistics, the European Centre for Disease Prevention, and Japan Red Cross yearbooks. Industry financials were pulled from 10-K filings, and D&B Hoovers helped map revenue splits of kit suppliers. News flow and product launches were tracked through Dow Jones Factiva, while Volza shipment records confirmed regional reagent flows. This list is illustrative, and many additional public archives informed our desk review.

A second desk pass focused on clinical adoption trends counted in peer-reviewed hematology journals, customs data, and patent filings accessed via Questel. These sources grounded assumptions on NAT uptake, kit replacement cycles, and emerging multiplex genotyping.

Market-Sizing & Forecasting

We apply a hybrid top-down and bottom-up approach. Country donation totals are converted into tested units, linked to region-specific test menus, and valued with median ASPs refined in channel checks. Supplier roll-ups and sampled hospital spend offer a bottom-up sense check. Key model drivers include donation growth, compulsory NAT coverage, serology-to-molecular conversion, kit replacement cycles, and average tests per unit. A five-year multivariate regression, adjusted through scenario analysis where policy changes loom, produces the forecast.

Data Validation & Update Cycle

Outputs pass variance checks against historical positivity rates and installed instrument bases. Any anomaly triggers analyst review. Reports refresh every twelve months, with interim updates released when recalls, guideline shifts, or pandemics materially move demand.

How Mordor Intelligence's Blood Transfusion Diagnostics Market Size Compares to Other Published Estimates

Published estimates often diverge because each publisher picks its own product mix, geographic lens, ASP path, and refresh timing. When one source counts only instruments or projects blanket NAT uptake in emerging regions, headline values shift noticeably.

These comparisons show that once scope breadth, variable choice, and annual refresh are harmonized, Mordor's balanced figure stands as the dependable baseline planners can rely on.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.97 B (2025) | Mordor Intelligence | - |

| USD 5.33 B (2024) | Global Consultancy A | counts instruments only, omits consumables |

| USD 5.28 B (2025) | Industry Portal B | assumes uniform NAT adoption across all regions |

| USD 4.96 B (2025) | Trade Journal C | excludes private blood banks from volume pool |

Key Questions Answered in the Report

What is the current value of the blood transfusion diagnostics market?

The blood transfusion diagnostics market is valued at USD 6.41 billion in 2026.

How fast will the market grow through 2031?

It is projected to expand at a 7.34% CAGR, reaching USD 9.14 billion by 2031.

Which product category leads revenue generation?

Consumables account for 53.62% of 2025 revenue due to recurring reagent demand.

What technology segment is advancing the quickest?

Nucleic acid testing posts the highest growth rate at 8.63% CAGR.

Why is Asia-Pacific considered the fastest-growing region?

Government-backed blood-safety investments and rising surgical volumes support an 8.31% CAGR.

How do new FDA regulations affect diagnostic manufacturers?

Laboratory-developed tests now require device-level compliance, increasing costs but favoring suppliers with established quality systems.

Page last updated on: