Women's Health Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

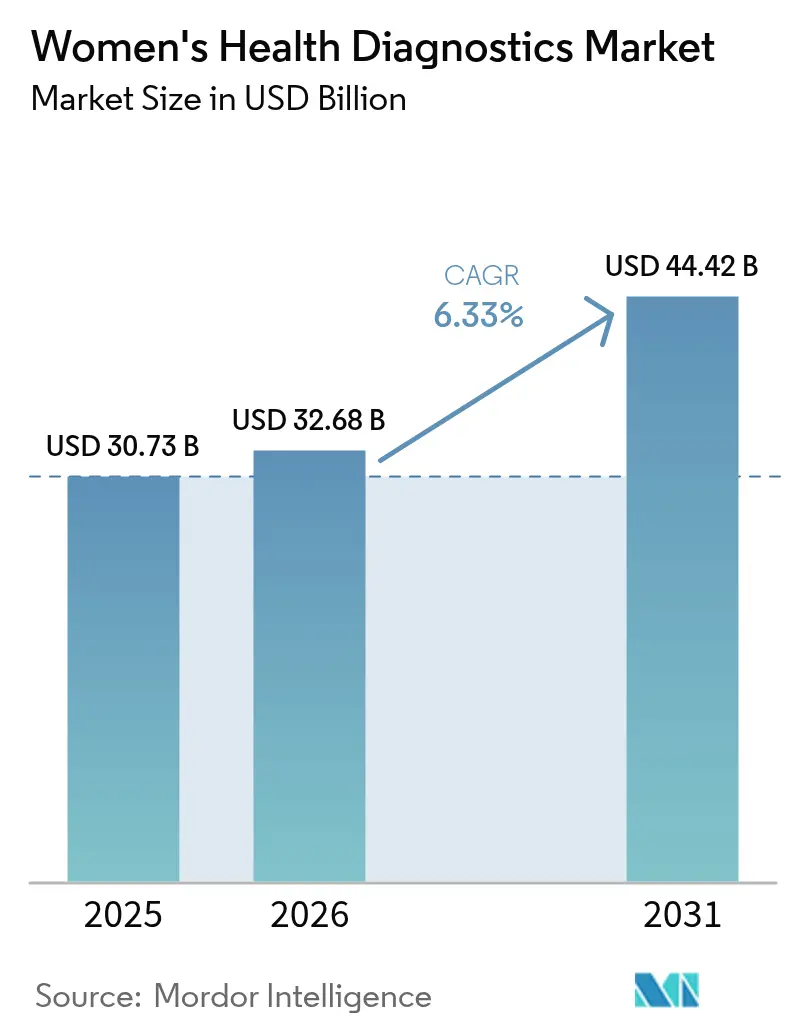

| Market Size (2026) | USD 32.68 Billion |

| Market Size (2031) | USD 44.42 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

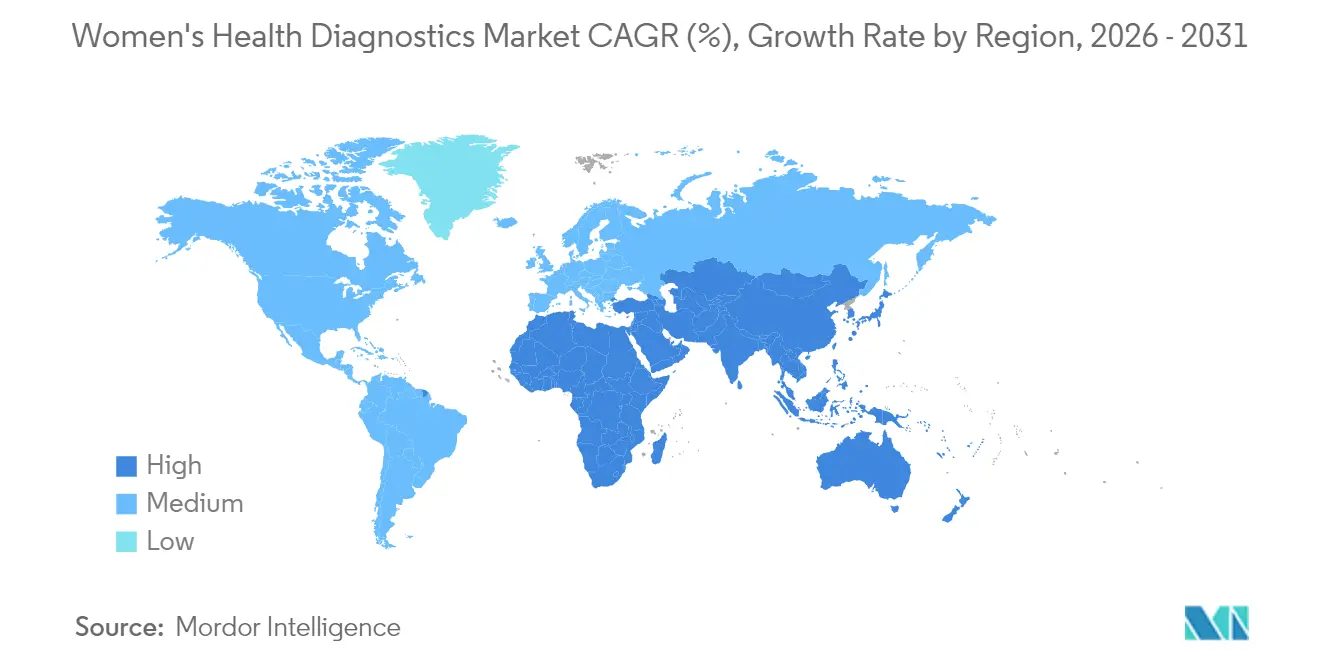

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Women's Health Diagnostics Market Analysis by Mordor Intelligence

The Women's Health Diagnostics Market size was valued at USD 30.73 billion in 2025 and estimated to grow from USD 32.68 billion in 2026 to reach USD 44.42 billion by 2031, at a CAGR of 6.33% during the forecast period (2026-2031).

Uptake of AI-enabled screening tools, streamlined pathways for laboratory-developed tests, and growing employer investment in preventive benefits will keep the women’s health diagnostics market on a steady growth path through the end of the decade. North America continues to anchor the field with 38.26% revenue in 2024, yet Asia-Pacific is advancing fastest as infrastructure spending and public awareness programs lift test volumes. Molecular assays are raising diagnostic accuracy for breast, cervical, and infectious diseases, while tele-health–facilitated self-collection models chip away at traditional access barriers. Competitive intensity is rising as multi-national device makers embed artificial intelligence across imaging and in-vitro platforms, even as fem-tech startups win share in direct-to-consumer channels.

Key Report Takeaways

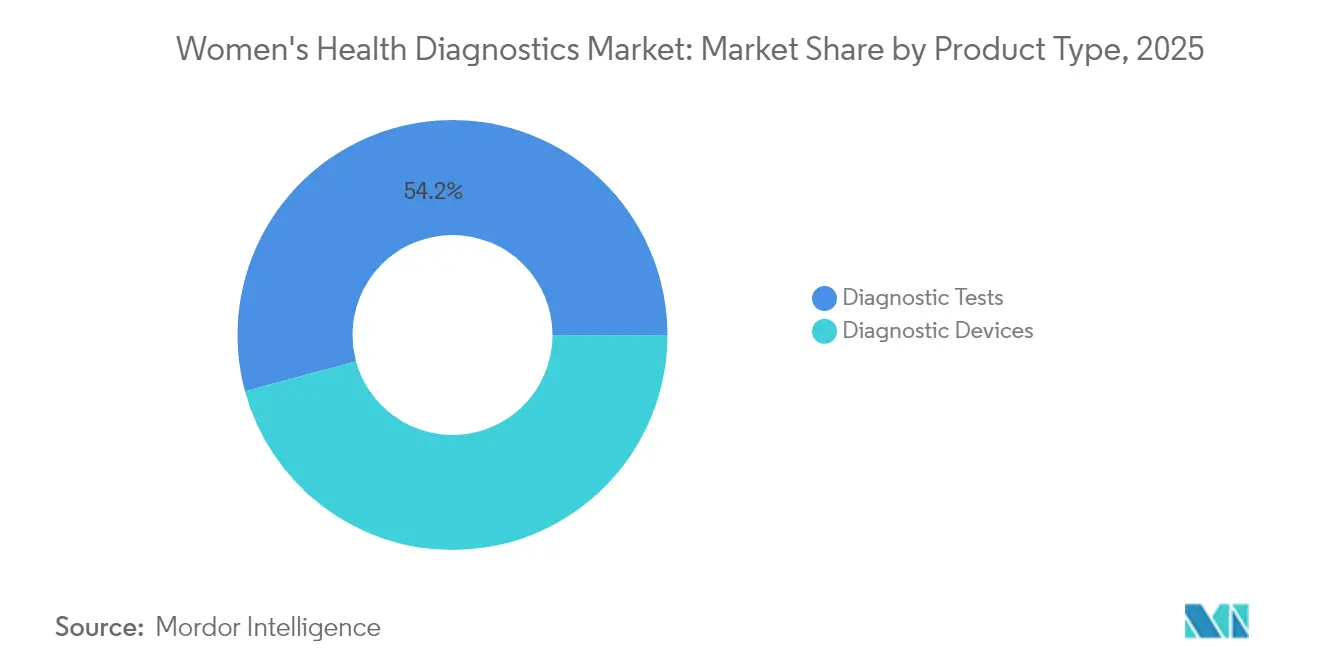

- By product category, diagnostic tests led with 54.21% of the women’s health diagnostics market share in 2025, while genetic & genomic panels are on course for a 9.10% CAGR through 2031.

- By technology, immunoassays accounted for 31.55% of the women’s health diagnostics market size in 2025, while AI-enabled analytics is projected to post an 8.22% CAGR through 2031.

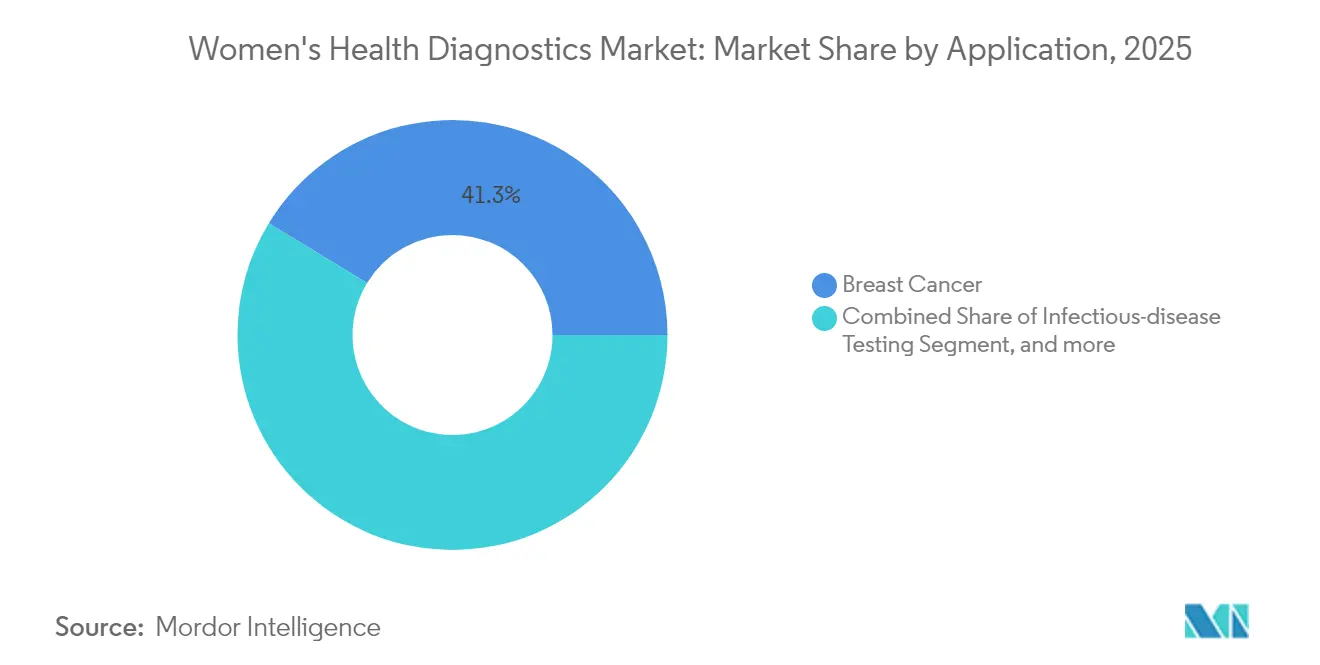

- By application, breast cancer testing held 41.30% of the women’s health diagnostics market size in 2025, whereas infectious disease panels are moving at a 7.60% CAGR to 2031.

- By end user, hospitals and diagnostic centers retained 69.05% of 2025 revenue, but home-care and self-testing are forecast to expand at 10.95% CAGR over 2026-2031.

- By geography, North America led with 37.90% share of the women’s health diagnostics market in 2025; Asia Pacific is projected to post an 9.60% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Women's Health Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Chronic & Lifestyle Disorders | +1.2% | North America, Europe, Global | Medium term (2-4 years) |

| Growing Number of Diagnostic & Imaging Centres | +0.8% | Asia-Pacific, Middle East & Africa | Short term (≤ 2 years) |

| Increased Adoption of POC & Rapid Diagnostic Tests | +1.5% | North America, Europe, Global | Short term (≤ 2 years) |

| Tele-Health Enabled At-Home Self-Collection Kits | +1.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| AI-Based Breast-Density Analytics Boosting Reimbursement | +0.9% | North America, Europe | Long term (≥ 4 years) |

| Employer-Sponsored Fem-Tech Benefits Accelerating Demand | +0.6% | North America, Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic & Lifestyle Disorders

The global growth in obesity, diabetes, and hormone-related cancers is translating into greater demand for early detection tools that can identify disease before symptoms appear. Cardiometabolic risk factors elevate female vulnerability to breast and endometrial cancers, prompting clinicians to widen screening protocols beyond age-based criteria.[1]Centers for Disease Control and Prevention, “Chronic Disease in Women,” cdc.gov Health ministries in Europe and North America now reimburse combined mammography and genetic panels for high-risk women, boosting test volumes across hospital networks. Wearable biosensors are being trialed to detect metabolic changes in real time, creating fresh datasets for predictive algorithms. As women’s lifespans lengthen, the clinical imperative to manage chronic disease upstream will continue to propel the women’s health diagnostics market.

Increased Adoption of POC & Rapid Diagnostic Tests

Point-of-care platforms shorten diagnostic cycles from days to minutes, making it easier to treat infections before complications arise. The FDA’s 2025 clearance of the first OTC molecular test for chlamydia, gonorrhea, and trichomoniasis allows consumers to perform triple-pathogen screening at home and receive results in 30 minutes.[2]U.S. Food and Drug Administration, “FDA Authorizes First Over-the-Counter Test for Multiple STIs,” fda.gov Mobile clinics in rural U.S. counties now deploy portable PCR units for same-day pelvic inflammatory disease management, while European pharmacies have introduced CLIA-waived pregnancy-related preeclampsia assays. Fast turnaround times minimize follow-up loss, improve antimicrobial stewardship, and help payers avoid costly late-stage interventions, reinforcing the positive impact on the women’s health diagnostics market.

Tele-Health Enabled At-Home Self-Collection Kits

Self-collection of cervical or vaginal samples closes a critical access gap for women who face logistical, cultural, or privacy barriers. Roche’s HPV self-collection system, cleared in Canada in 2024, demonstrated 99.9% sample adequacy and high user satisfaction in real-world rollouts.[3]Roche, “HPV Self-Collection Solution Receives Health Canada Approval,” roche.com National health systems are mailing kits to women overdue for screening, with tele-nurse support for result interpretation. Integration into electronic health records ensures clinicians receive actionable data without overburdening laboratory workflows. Similar models are emerging in Asia-Pacific, where smartphone registration and QR code logistics speed turnaround. By extending reach while maintaining clinical sensitivity, self-collection reinforces the shift toward patient-centered care within the women’s health diagnostics market.

AI-Based Breast-Density Analytics Boosting Reimbursement

Dense breast tissue masks malignancies, leading to missed diagnoses under conventional mammography. AI algorithms now quantify density automatically and flag suspicious areas for secondary review, improving detection by 20% and trimming recall rates by 30% in community clinics. Beginning in late-2024, U.S. providers must document breast density in every mammogram report, creating a standardized path for payer reimbursement. Early evidence of cost-effectiveness is prompting insurers to cover supplementary ultrasound or MRI in high-density cases, further expanding the women’s health diagnostics market size in breast imaging. Sustainably higher reimbursement is incentivizing hospitals to upgrade workstations and radiologist training, which should cement AI as a clinical mainstay over the forecast horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Diagnostic Imaging Systems | -0.7% | Global, Emerging Markets | Long term (≥ 4 years) |

| Stringent Regulatory Guidelines | -0.5% | North America, Europe, Global | Medium term (2-4 years) |

| Data-Privacy Concerns Over DTC Genetic Testing | -0.4% | North America, Europe, Global | Short term (≤ 2 years) |

| Lack of Sex-Specific AI Training Datasets | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Diagnostic Imaging Systems

Capital expenditure for MRI and advanced ultrasound can exceed USD 2 million per unit, a figure that challenges hospitals in emerging economies. Currency depreciation and import tariffs inflate acquisition costs, slowing replacement cycles and limiting geographic coverage. Although vendor financing and public-private partnerships are easing budget constraints, many facilities still operate analog systems that lack AI readiness. Elevated ownership costs thus temper the near-term rollout of cutting-edge modalities, creating a moderate drag on the global women’s health diagnostics market CAGR.

Data-Privacy Concerns Over DTC Genetic Testing

Direct-to-consumer labs collect vast genomic datasets that can expose sensitive reproductive information. Investigations into unauthorized data sharing have resulted in multimillion-dollar settlements and heightened public scrutiny. Legislators in the United States and European Union are weighing stricter consent rules and opt-out rights, and several states now require confirmatory testing before clinical use of consumer genomic data. Worries about privacy are prompting some women to cancel purchase plans, slowing order growth in a segment otherwise primed for rapid expansion. Market participants are responding with secure cloud architectures and transparent data-use policies, but lingering uncertainty could restrain sales during the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diagnostic Tests Lead Market Evolution

Diagnostic tests generated the majority of revenue, accounting for 54.21% of the women’s health diagnostics market in 2025. Molecular platforms are popular because they deliver multiplex detection of sexually transmitted infections, hereditary cancer mutations, and prenatal anomalies in a single run. High-throughput PCR systems equipped with sample-to-answer cartridges are now standard in many reference labs, reducing hands-on time and supporting same-day therapy initiation. Genetic and genomic panels represent the quickest-expanding product line at a 9.10% CAGR, mainly due to broader insurance coverage for BRCA and Lynch syndrome screening. Demand for digital pregnancy and ovulation tests remains steady, as smartphone linkages offer cycle tracking and tele-consultation portals.

Diagnostic devices held the remaining 45.79% share, led by AI-capable mammography, ultrasound, and bone densitometry equipment. Automated breast ultrasound systems integrate 3D reconstruction and density scoring, cutting scan time and operator variability. Biopsy tools are upgrading to vacuum-assisted needle designs that limit tissue trauma, and guided navigation software helps clinicians sample lesions with sub-millimeter precision. Over the forecast window, bundled device-and-software sales will allow manufacturers to cross-sell analytics modules, reinforcing their recurring revenue streams within the women’s health diagnostics market.

By Technology: AI-Enabled Analytics Drive Innovation

Immunoassays remained the most significant technology slice at 31.55% in 2025, valued for their versatility in hormone, oncology, and infectious disease testing. Continuous improvements in chemiluminescent substrates have shortened assay times to under 15 minutes, making them practical triage tools in emergency settings. Meanwhile, AI-enabled analytics is climbing fastest with an 8.22% CAGR, propelled by FDA clearances for algorithmic breast density and risk scoring. Deployment of cloud-based machine learning pipelines lets small clinics process imaging data without heavy on-premises hardware, democratizing access to advanced analytics.

Molecular diagnostics remains a powerhouse segment, thanks to loop-mediated isothermal amplification and CRISPR-based detection formats suited for decentralized testing. Imaging technology is not standing still: vendors are adding deep-learning reconstruction that improves image clarity at lower radiation doses. Together, these advances are widening clinical indications and boosting throughput, sustaining momentum in the women’s health diagnostics market.

By Application: Breast Cancer Dominates, Infectious Disease Accelerates

Breast cancer screening continued to command 41.30% of 2025 revenue, reflecting nationwide mammography mandates and growing use of adjunct modalities for dense-breast populations. AI triage cuts radiologist workload by flagging normal studies, allowing more focus on complex cases. Infection-related applications are expanding quickest at 7.60% CAGR, driven by global STI prevention programs and the rollout of decentralized molecular assays.

Employer-funded virtual care bundles that integrate hormonal tracking and genetic counseling benefit pregnancy and fertility monitoring. Long underutilized osteoporosis diagnostics are gaining visibility as clinicians screen peri-menopausal women earlier to curb fragility fracture risk.

By End User: Home-Care Segment Transforms Market Dynamics

Hospitals and diagnostics centers still captured 69.05% of 2025 spend, leveraging established infrastructure and cross-disciplinary expertise. High-volume imaging suites exploit economies of scale to deliver more affordable breast cancer and obstetric scans. Yet the home-care and self-testing group is advancing at 10.95% CAGR as regulatory bodies green-light consumer sampling kits and tele-medicine portals.

Employers are supplementing insurance plans with preventive screening vouchers, lowering out-of-pocket costs for staff and encouraging early detection. This shift decentralizes service delivery and introduces new data flows into clinical workflows, broadening revenue opportunities across the women’s health diagnostics industry.

Geography Analysis

North America led with 37.90% of 2025 revenue, underpinned by robust reimbursement policies and a steady cadence of FDA approvals that pull innovation from bench to bedside faster than any other region. United States insurers expanded coverage for AI-assisted mammography after mandated breast density reporting took effect in 2024. Canada’s HPV self-collection launch is lifting cervical screening compliance among underserved groups.

Asia-Pacific posted the quickest regional climb at a 9.60% CAGR, extending the women’s health diagnostics market into populous countries that previously lacked widespread screening infrastructure. China subsidizes rural imaging vans and genomic tumor-profiling grants, and Japan’s top private insurers now cover AI-assisted ultrasound for dense-breast patients. India is leveraging telemedicine platforms integrated with point-of-care PCR to reach remote villages, narrowing the urban-rural detection gap. Startups across Singapore, South Korea, and Australia are focusing on menstrual health analytics and fertility assessment, injecting local flavor into product pipelines.

Europe maintains a balanced position with established national screening programs that keep test volumes steady. Germany and the United Kingdom are leading adopters of cloud-based PACS linked to AI engines, while France is piloting bundled breast and ovarian cancer genetic screening in public hospitals. Southern European countries are harmonizing LDT validation processes in anticipation of the EU In-Vitro Diagnostic Regulation transition, protecting patient safety and sustaining trust. Together, these initiatives reinforce the long-term resilience of the women’s health diagnostics market across the continent.

Competitive Landscape

The women’s health diagnostics market shows moderate concentration, with global leaders Abbott, Roche, and Hologic supplying a broad suite of assays, imaging systems, and informatics platforms. Their geographic reach and R&D budgets facilitate early entry into high-growth segments such as AI-guided imaging and multiplex PCR. Hologic recently acquired a minimally invasive fibroid treatment firm to enrich its interventional portfolio, complementing its dominance in cervical cancer diagnostics.

Strategic alliances with AI specialists are accelerating product differentiation. GE HealthCare partnered with RadNet to deploy cloud-native mammography algorithms, cutting false positives and enabling value-based reimbursement models. Siemens Healthineers launched an AI-powered ultrasound series that automates fetal biometrics, improving consistency across obstetric clinics. These moves indicate an arms race to integrate software-as-a-medical-device, ensuring continued relevance amid rising digital competition.

Nimble fem-tech startups are carving out direct-to-consumer niches in fertility tracking, menopause monitoring, and at-home STI testing. Partnerships with big-box retailers and tele-health providers are giving these newcomers rapid market access, though data privacy compliance remains a hurdle. Incumbent manufacturers are countering by releasing FDA-cleared self-collection kits under familiar brand umbrellas, leveraging trust to retain share. As new entrants push innovation cycles faster, incumbents must balance hardware revenue with subscription-based analytics, shaping the next phase of competition in the women’s health diagnostics industry.

Women's Health Diagnostics Industry Leaders

Quest Diagnostics Inc.

Siemens Healthineers AG

Hologic Inc.

F. Hoffmann-La Roche AG

PerkinElmer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FDA grants marketing authorization for Visby Medical Women’s Sexual Health Test, the first home-use molecular assay for chlamydia, gonorrhea, and trichomoniasis; results delivered in 30 minutes, no prescription required

- March 2025: GE HealthCare introduces Invenia ABUS Premium 3D ultrasound with AI-driven dense-breast detection, cutting scan times while improving sensitivity

- February 2025: Roche secures FDA clearance for the Elecsys sFlt-1/PlGF ratio test, enabling early stratification of pregnant women at risk of severe pre-eclampsia.

- January 2025: GE HealthCare upgrades its Voluson Expert Series with AI features that streamline high-risk pregnancy imaging and workflow efficiency.

Global Women's Health Diagnostics Market Report Scope

As per the scope of the report, a wide range of laboratory testing options is available to improve the diagnosis and treatment of the disease in women. The women's health diagnostic methods include screening, testing or diagnosing, and monitoring several women-related disorders, such as breast cancer, ovarian cancer, cervical cancer, menopause, and pregnancy.

The women's health diagnostics market is segmented by type (diagnostic devices and diagnostic tests), application (breast cancer, infectious disease testing, osteoporosis testing, pregnancy and fertility testing, sexually transmitted disease testing, and other applications), end user (hospital and diagnostics centers and home care), and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America) The report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (in USD million) for the abovementioned segments.

| Diagnostic Devices | Biopsy Devices |

| Imaging & Monitoring Systems | |

| Digital & AI-enabled Imaging Workstations | |

| Diagnostic Tests | Breast-cancer Testing |

| PAP & HPV Tests | |

| Pregnancy & Ovulation Tests | |

| Infectious-disease Tests | |

| Genetic & Genomic Panels | |

| Other Tests |

| Immunoassay |

| Molecular Diagnostics |

| Imaging |

| AI-enabled Analytics |

| Breast Cancer |

| Infectious-disease Testing |

| Osteoporosis |

| Pregnancy & Fertility |

| Sexually Transmitted Diseases |

| Other Applications |

| Hospitals & Diagnostic Centres |

| Home-care / Self-testing |

| Corporate / Occupational Health Programs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Diagnostic Devices | Biopsy Devices |

| Imaging & Monitoring Systems | ||

| Digital & AI-enabled Imaging Workstations | ||

| Diagnostic Tests | Breast-cancer Testing | |

| PAP & HPV Tests | ||

| Pregnancy & Ovulation Tests | ||

| Infectious-disease Tests | ||

| Genetic & Genomic Panels | ||

| Other Tests | ||

| By Technology | Immunoassay | |

| Molecular Diagnostics | ||

| Imaging | ||

| AI-enabled Analytics | ||

| By Application | Breast Cancer | |

| Infectious-disease Testing | ||

| Osteoporosis | ||

| Pregnancy & Fertility | ||

| Sexually Transmitted Diseases | ||

| Other Applications | ||

| By End User | Hospitals & Diagnostic Centres | |

| Home-care / Self-testing | ||

| Corporate / Occupational Health Programs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the women’s health diagnostics market in 2026?

The women’s health diagnostics market size stands at USD 32.68 billion in 2026, with a projection to reach USD 44.42 billion by 2031.

What is the expected growth rate for women’s health diagnostics to 2031?

The market is forecast to expand at a 6.33% CAGR over the 2026-2031 period.

Which product category currently drives most revenue?

Diagnostic tests lead, generating 54.21% of 2025 revenue thanks to molecular platforms that cover infections, cancer markers, and prenatal conditions.

Which application area is growing fastest?

Infectious disease panels, supported by expanded STI screening and new at-home tests, are advancing at a 7.60% CAGR.

Why is Asia-Pacific considered the most attractive growth region?

Healthcare infrastructure investments, national screening campaigns, and a burgeoning tele-health sector are together driving a 9.60% regional CAGR.

How are AI tools influencing breast cancer diagnostics?

AI algorithms now quantify breast density and flag suspicious lesions, improving detection by 20% and reducing unnecessary recalls by 30%, leading payers to reimburse advanced imaging workflows.

Page last updated on: