Hematology Diagnostics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

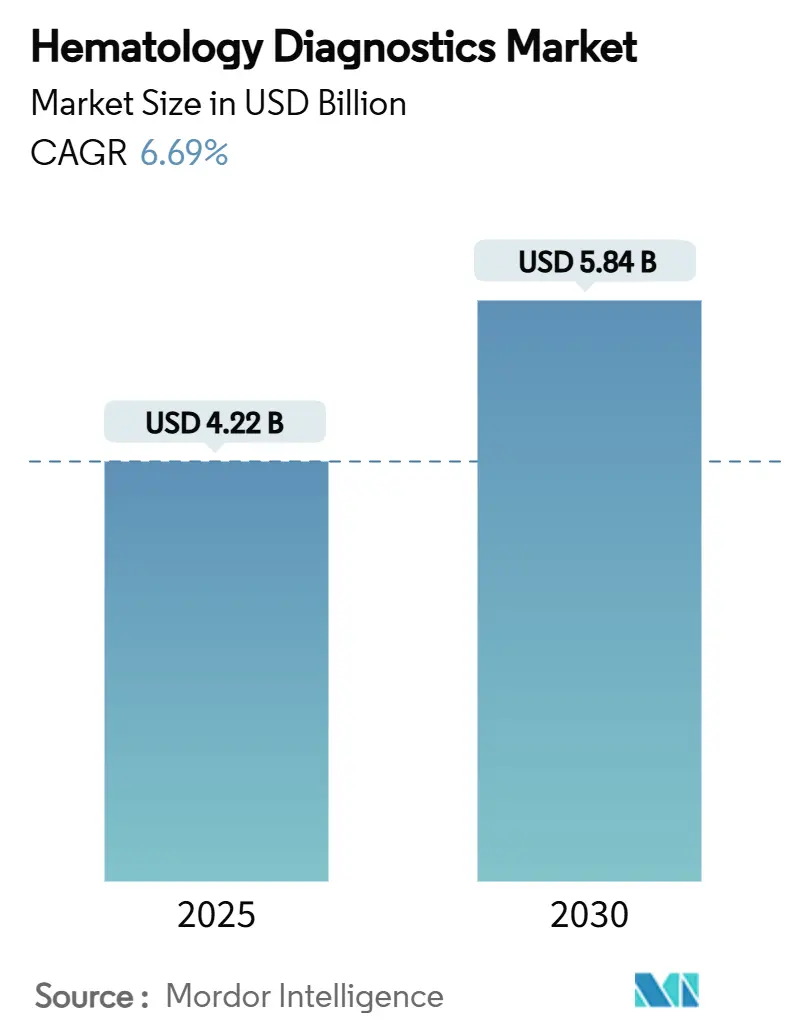

| Market Size (2025) | USD 4.22 Billion |

| Market Size (2030) | USD 5.84 Billion |

| Growth Rate (2025 - 2030) | 6.69% CAGR |

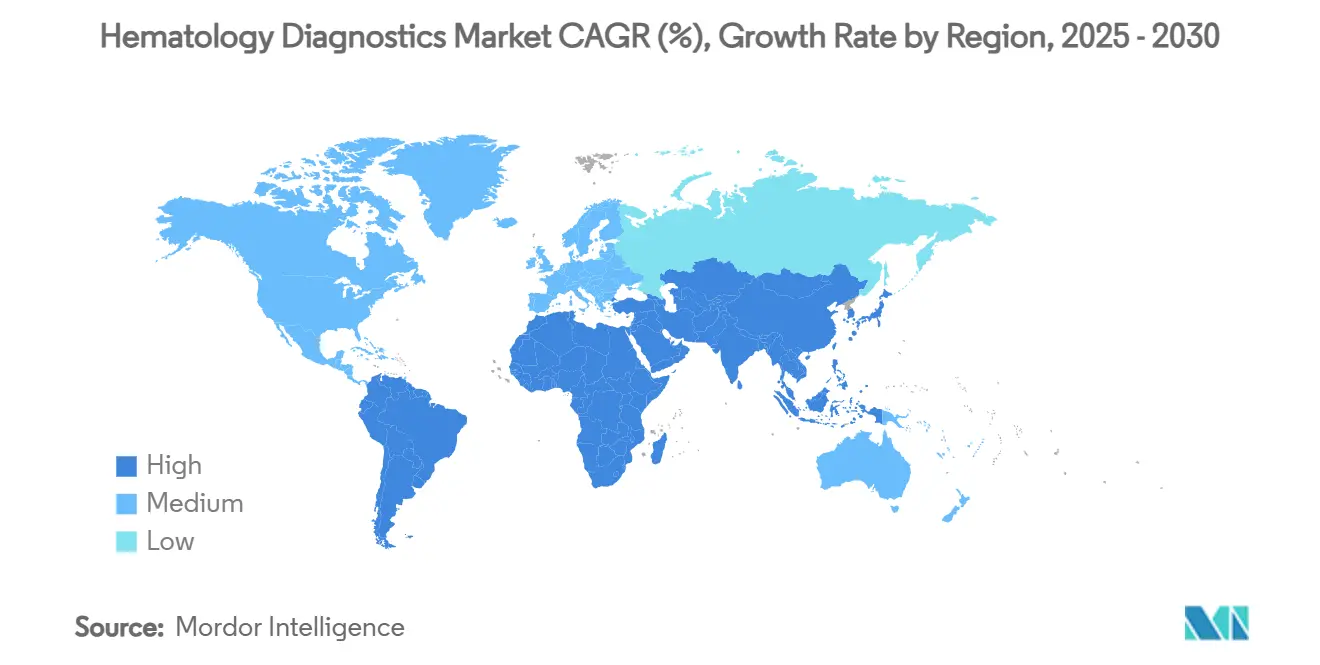

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hematology Diagnostics Market Analysis by Mordor Intelligence

The global hematology diagnostics market stands at USD 4.22 billion in 2025 and is forecast to reach USD 5.84 billion by 2030, expanding at a 6.69% CAGR over the period. Rising automation, AI-enabled analytics, and mounting workforce shortages push laboratories to replace manual processes with high-throughput analyzers, strengthening the hematology diagnostics market across every major region. Instrument upgrades that shorten turnaround time, integration of digital morphology, and connectivity with laboratory information systems improve clinical accuracy and workflow efficiency, while supportive reimbursement policies in developed economies reinforce capital spending. Growing diabetes prevalence drives adoption of HbA1c testing, and escalating sepsis incidence underscores the need for rapid blood cell analysis, all of which expand the hematology diagnostics market footprint into point-of-care and home-care environments. Continuous innovation from incumbents and startups cultivates a steady pipeline of molecular and digital platforms that distinguish the hematology diagnostics market through differentiated performance and user-centric design.

Key Report Takeaways

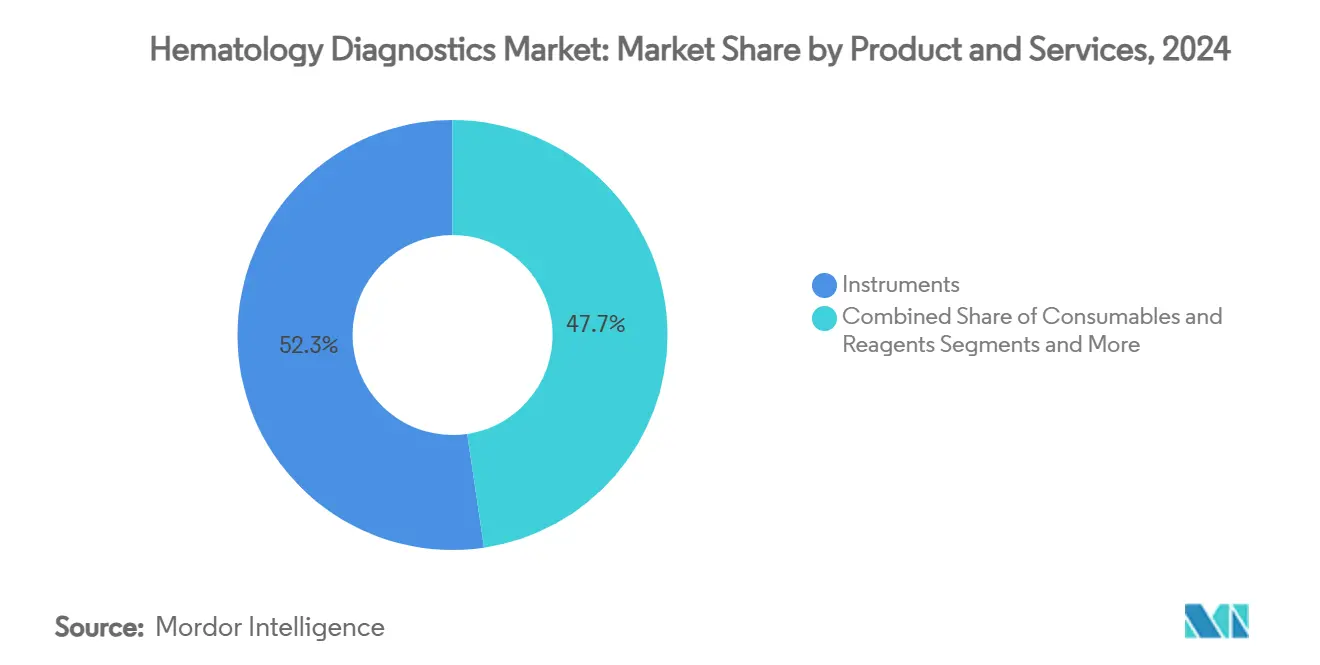

- By product & service, instruments held 52.34% of hematology diagnostics market share in 2024, while services & software is set to climb at 10.54% CAGR through 2030.

- By test type, complete blood count dominated with 36.47% revenue in 2024, whereas HbA1c & specialized tests are projected to grow fastest at 9.63% CAGR.

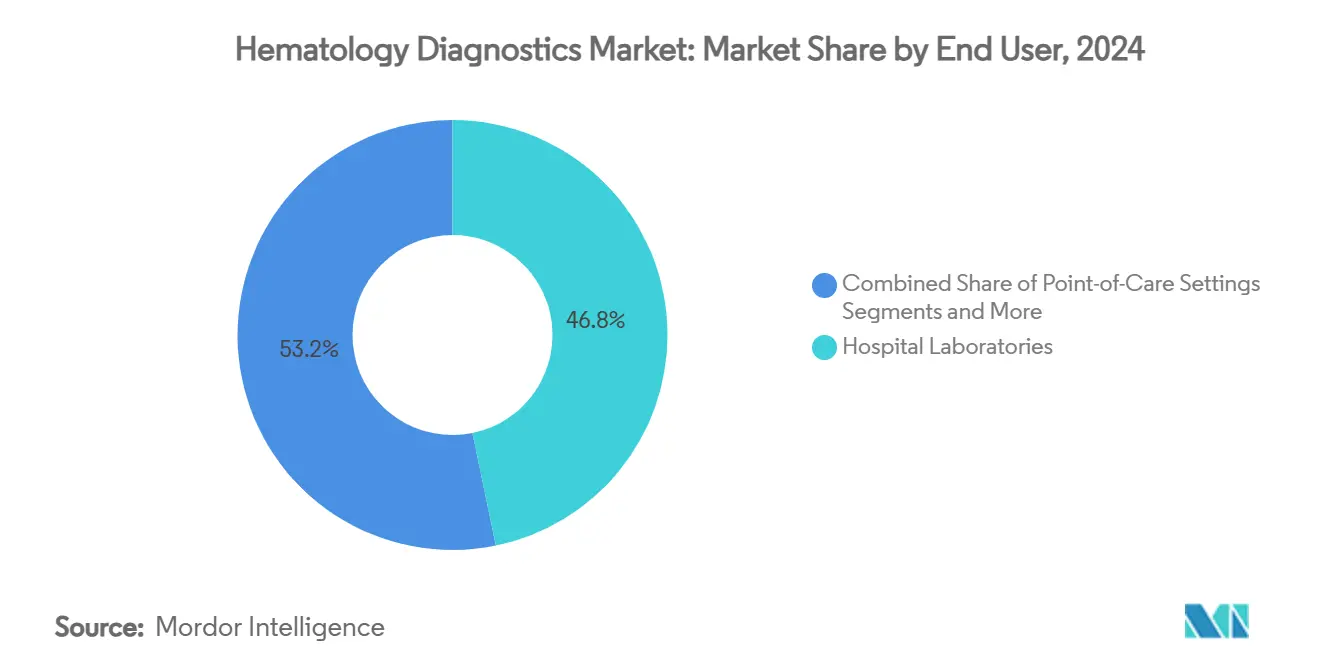

- By end user, hospital laboratories accounted for 46.78% of the hematology diagnostics market size in 2024; point-of-care is forecast to expand at 10.90% CAGR to 2030.

- By technology, 5/6-part differential analyzers led with 44.68% share of the hematology diagnostics market size in 2024, yet molecular & digital hematology technologies are advancing at 9.44% CAGR.

- By geography, North America captured 33.84% revenue in 2024, while Asia-Pacific is the fastest-growing regional segment at 8.82% CAGR through 2030.

Global Hematology Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automation-driven lab efficiency | +1.8% | Global; strongest in North America and EU | Medium term (2-4 years) |

| Rising blood-borne disease burden | +1.2% | Global; concentrated in Asia-Pacific and Sub-Saharan Africa | Long term (≥ 4 years) |

| Growing adoption of point-of-care hematology | +0.9% | Global; accelerated in rural and underserved regions | Short term (≤ 2 years) |

| AI-powered cell morphology analytics | +0.7% | North America and EU; expanding to Asia-Pacific | Medium term (2-4 years) |

| Lab-staff shortages accelerating analyzer upgrades | +0.6% | Global; most acute in developed markets | Short term (≤ 2 years) |

| Emerging veterinary hematology demand | +0.5% | North America and EU; emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Automation-Driven Lab Efficiency

Laboratories now implement fully automated “dark lab” workflows that remove up to 70% of manual steps and cut analytical errors by 40%. Platforms such as Sysmex XR-Series and HORIBA HELO can process more than 125 CBCs per square meter, integrating predictive maintenance modules that reduce downtime 30% compared with reactive models. Superior reproducibility and declining skill-mix requirements make automation fundamental to the hematology diagnostics market, especially where vacancies exceed 25% among clinical technologists.

Rising Blood-Borne Disease Burden

Bloodstream infections represent 15% of healthcare-associated infections and carry 25% mortality in severe cases.[1]Stacey L. Nagy, “Managing Blood Culture Bottle Shortages,” American Society for Microbiology, asm.orgCOVID-19 accentuated gaps when laboratories lost up to 60% capacity, spurring investment in rapid flow-cytometry-equipped hematology systems that shorten sepsis diagnosis from hours to minutes. The hematology diagnostics market benefits from combined molecular and cell-based workflows that support antimicrobial stewardship and improve patient outcomes in emerging economies.

Growing Adoption of Point-of-Care Hematology

Miniaturized analyzers that require finger-stick samples are moving CBC capability into physician offices, ambulances, and home-care settings.[2]María I. Núñez Rosas et al., “Last Trends in Point-of-Care Diagnostics for the Management of Hematological Indices in Home Care Patients,” Biosensors, mdpi.com Rice University’s gravity-driven, AI-enabled flow cytometer delivers laboratory-grade CD4 counts without pumps, raising access for HIV and COVID-19 management. These innovations broaden the hematology diagnostics market beyond centralized labs and support value-based care strategies that prioritize vicinity, speed, and cost.

AI-Powered Cell Morphology Analytics

Deep learning algorithms now identify myeloblasts with 91% sensitivity, trimming manual review by 60% while ensuring uniform reporting accuracy.[3]Toshihiro Shimizu et al., “P533: A Fully Automated Supervised AI-Based Cell Classifier,” HemaSphere, journals.lww.com Holotomographic flow cytometry further correlates cell morphology with genotype, opening new precision-diagnosis pathways in leukemia.[4]Yue Zhao et al., “From Genotype to Phenotype: Decoding Mutations in Blasts by Holo-Tomographic Flow Cytometry,” Nature Photonics, nature.com As these tools integrate into routine workflows they reinforce the competitiveness of the hematology diagnostics market through data-driven differentiation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cap-ex of advanced analyzers | –1.4% | Global; most constraining in emerging markets | Medium term (2-4 years) |

| Pricing pressure from IVD consolidation | –0.8% | Global; intensifying in mature markets | Short term (≤ 2 years) |

| Limited reimbursement for novel hematology tests | –0.6% | North America and EU; emerging in Asia-Pacific | Long term (≥ 4 years) |

| Supply-chain fragility for critical reagents | –0.4% | Global; acute in regions with limited suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cap-Ex of Advanced Analyzers

Sophisticated analyzers require USD 200,000–500,000 upfront plus service contracts near 15% of purchase price each year. Smaller facilities struggle to justify these outlays, extending analyzer life cycles to 7–10 years and slowing uptake of the latest technologies. Leasing models help, yet regulatory mandates still oblige specific configurations, limiting cost control.

Pricing Pressure from IVD Consolidation

Divestitures such as BD’s USD 3.4 billion diagnostics unit amplify competitive bidding, compressing margins for both incumbent and challenger vendors. Group purchasing organizations secure deeper discounts, forcing manufacturers to streamline operations in the hematology diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Instruments Drive Automation Momentum

Instruments represented the largest slice of the hematology diagnostics market in 2024, accounting for 52.34% revenue as laboratories prioritized high-throughput analyzers that combine sample loading, differential counting, and slide preparation in one footprint. Services & software, though smaller, is expanding at a 10.54% CAGR as laboratories seek data analytics, cloud connectivity, and predictive maintenance that extend analyzer uptime. Consumables & reagents remain the daily lifeblood of workflows, and supply assurances have prompted some vendors to integrate manufacturing for critical stains and flow-cytometry antibodies.

A deeper shift toward out-come-based service contracts ties analyzer availability to financial penalties, encouraging vendors to bundle remote diagnostics and automatic reagent restocking. This model converts one-time sales into annuity revenue, enhancing lifetime value and supporting the hematology diagnostics market trajectory. Digital pathology add-ons, offered through partnerships like Siemens Healthineers-Scopio Labs, unlock incremental revenue from existing analyzers by enabling morphology review without physical slides.

By Test Type: CBC Still Dominant, Specialized Panels Accelerate

The complete blood count held 36.47% of 2024 revenue, underscoring its status as a routine screening staple in primary care and oncology follow-up. However, HbA1c & specialized panels are on track for 9.63% CAGR, reflecting expanding diabetes screening mandates and personalized medicine initiatives. Molecular-fusion workflows merge next-generation sequencing panels with conventional hematology, improving detection of myeloid neoplasm mutations with 93% accuracy.

Coagulation and hemostasis assays benefit from wider use of direct oral anticoagulants, prompting launch of dedicated factor-Xa inhibitor tests. Flow-cytometry-based assays gain traction in measurable residual disease monitoring, capitalizing on improved high-sensitivity protocols. These dynamics reinforce diversified revenue streams and enhance resilience of the hematology diagnostics market across therapy areas.

By End User: Hospital Labs Guard Volume While POC Gathers Pace

Hospital laboratories retained 46.78% share in 2024 due to consolidated procurement power and integrated electronic health record connectivity that streamlines order-to-report cycles. Point-of-care venues, though smaller, are growing at 10.90% CAGR as low-volume devices reach accuracy parity with benchtop analyzers. BD’s finger-stick MiniDraw device exemplifies efforts to simplify collection and cut phlebotomy staffing requirements.

Reference laboratories win outsourced high-complexity tests from community hospitals, allowing smaller facilities to focus on rapid turnaround in the hematology diagnostics market. Veterinary clinics also post mid-single-digit growth, benefiting from pet insurance uptake and willingness to pay for advanced diagnostics.

By Technology: Molecular and Digital Platforms Gain Ground

5/6-part differential analyzers delivered 44.68% of 2024 sales, favored for routine workload and cost efficiency. Yet molecular & digital hematology platforms—themselves forecast at 9.44% CAGR—bring genetic insight and AI-assisted interpretation that elevate diagnostic value and support informed treatment selection. Automated flow cytometry complements these tools, offering rapid multiparameter panels that streamline leukemia classification.

Digital morphology solutions migrate slide review to cloud workstations, shrinking review time and reducing ergonomic strain for laboratory personnel. Coupled with high-sensitivity flow cytometry, these technologies expand measurable residual disease detection into community settings, underscoring a step change in the hematology diagnostics market.

Geography Analysis

North America anchored 33.84% of the hematology diagnostics market in 2024, powered by sophisticated hospital networks, early automation adoption, and reimbursement structures that encourage comprehensive laboratory testing. Vacancy rates above 25% for medical technologists accelerate analyzer upgrades that boost throughput without new hires. Robust R&D pipelines from Abbott, Danaher, and Beckman Coulter inject innovation, while Canada leverages universal healthcare to normalize test utilization and Mexico reallocates public spending to upgrade regional laboratories.

Asia-Pacific posts the highest 8.82% CAGR through 2030 as China and India broaden insurance coverage and invest in modern hospitals. Large population bases and rising non-communicable disease prevalence fuel demand for both routine and specialized testing. Japan’s oncology genome program seeks 100,000 sequences by 2029, embedding molecular diagnostics into hematology workflows and fostering ecosystem partnerships. Compact analyzers from regional firms like Mindray match cost sensitivities in mid-tier hospitals, allowing the hematology diagnostics market to penetrate secondary cities and rural communities.

Europe benefits from harmonized healthcare infrastructure and long-standing laboratory networks yet grapples with higher compliance costs from the In Vitro Diagnostic Regulation. While IVDR extends evidence demands, established vendors leverage regulatory expertise to strengthen market barriers. Germany, France, and the United Kingdom lead purchasing, whereas Southern Europe invests gradually, focusing on high-value upgrades. The Middle East and Africa, though comparatively small, invest in large reference centers to compensate for specialist shortages; South America aligns macroeconomic recovery with incremental lab modernization, signaling steady but uneven expansion of the hematology diagnostics market.

Competitive Landscape

The hematology diagnostics market is moderately fragmented. Sysmex dominates differential counting and automation modules; Danaher’s Beckman Coulter division leverages expansive reagent catalogs, and Abbott differentiates through Alinity’s high-volume integrated platform. Strategic partnerships, including Siemens Healthineers’ OEM hemostasis agreement with Sysmex, extend product breadth and distribution reach.

Emerging players challenge incumbents through AI-native design and miniaturized hardware that better suits distributed care. Mindray’s platelet-focused CAL 8000 line uses self-de-aggregation algorithms to minimize pseudothrombocytopenia false flags. Start-ups exploit software-as-a-service models where slide images are centrally reviewed, creating annuity revenue without large capital expenditures.

Consolidation trends reshape pricing dynamics; the pending BD divestiture invites fresh competition and aggressive price strategies. At the same time, reagent shortages trigger vertical integration bids such as in-house antibody production, solidifying supply while compressing margins. Overall, competitive intensity pivots on who can deliver integrated hardware-software-service ecosystems that address throughput, accuracy, and staffing challenges in the hematology diagnostics market.

Hematology Diagnostics Industry Leaders

Sysmex Corporation

Danaher

Abbott Laboratories

Siemens Healthineers

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Rice University researchers introduced a gravity-driven, AI-enabled flow cytometry device enabling CD4+ T cell counts in unpurified blood, targeting resource-limited settings.

- March 2025: BD and Babson Diagnostics reported that MiniDraw fingertip collection delivers equivalent accuracy to venous draws, facilitating broader access to testing.

- January 2025: Mindray launched AI-powered platelet counting technology within the CAL 8000 line to curtail pseudothrombocytopenia and deliver results in 30 minutes.

Global Hematology Diagnostics Market Report Scope

| Instruments |

| Consumables & Reagents |

| Services & Software |

| Complete Blood Count (CBC) |

| Hemoglobin/Hematocrit |

| Coagulation & Hemostasis |

| Flow Cytometry–Based |

| HbA1c & Specialized Tests |

| Hospital Laboratories |

| Independent/Reference Labs |

| Point-of-Care Settings |

| Academic & Research Institutes |

| Veterinary Clinics |

| 3-part Differential Analyzers |

| 5/6-part Differential Analyzers |

| Automated Flow Cytometry |

| Molecular & Digital Hematology |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product & Service | Instruments | |

| Consumables & Reagents | ||

| Services & Software | ||

| By Test Type | Complete Blood Count (CBC) | |

| Hemoglobin/Hematocrit | ||

| Coagulation & Hemostasis | ||

| Flow Cytometry–Based | ||

| HbA1c & Specialized Tests | ||

| By End User | Hospital Laboratories | |

| Independent/Reference Labs | ||

| Point-of-Care Settings | ||

| Academic & Research Institutes | ||

| Veterinary Clinics | ||

| By Technology | 3-part Differential Analyzers | |

| 5/6-part Differential Analyzers | ||

| Automated Flow Cytometry | ||

| Molecular & Digital Hematology | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current size of the hematology diagnostics market?

The hematology diagnostics market stands at USD 4.22 billion in 2025 and is forecast to reach USD 5.84 billion by 2030.

2. Which segment is growing fastest within the hematology diagnostics market?

Services & software is the fastest-growing segment, projected to rise at 10.54% CAGR through 2030, driven by demand for analytics, connectivity, and predictive maintenance.

3. Why is point-of-care hematology gaining traction?

Miniaturized analyzers and finger-stick sampling make CBC and HbA1c testing feasible outside central labs, supporting decentralized care models and improving access in rural areas.

4. How is AI impacting hematology diagnostics?

AI-powered algorithms enhance cell morphology analysis, reduce manual reviews by up to 60%, and support precision diagnosis in leukemia and other blood disorders.

5. Which region offers the highest growth potential?

Asia-Pacific is the fastest-growing region with an expected 8.82% CAGR, underpinned by healthcare modernization in China, India, and Southeast Asia.

Page last updated on: