Body Composition Analyzers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

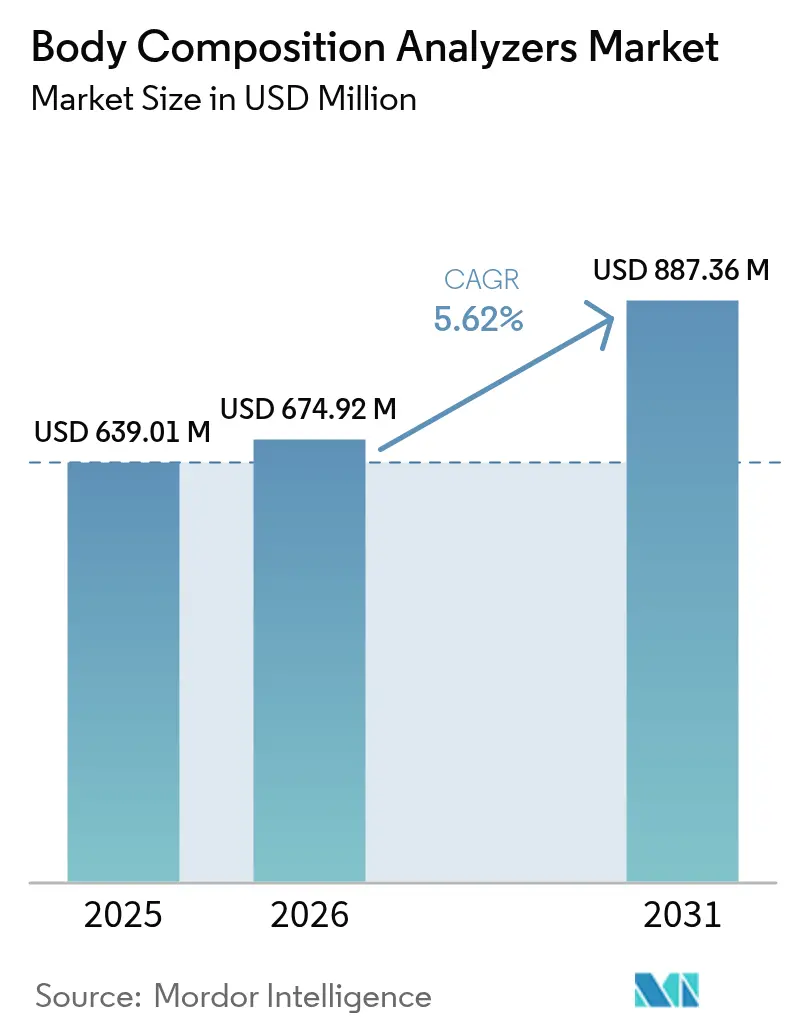

| Market Size (2026) | USD 674.92 Million |

| Market Size (2031) | USD 887.36 Million |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

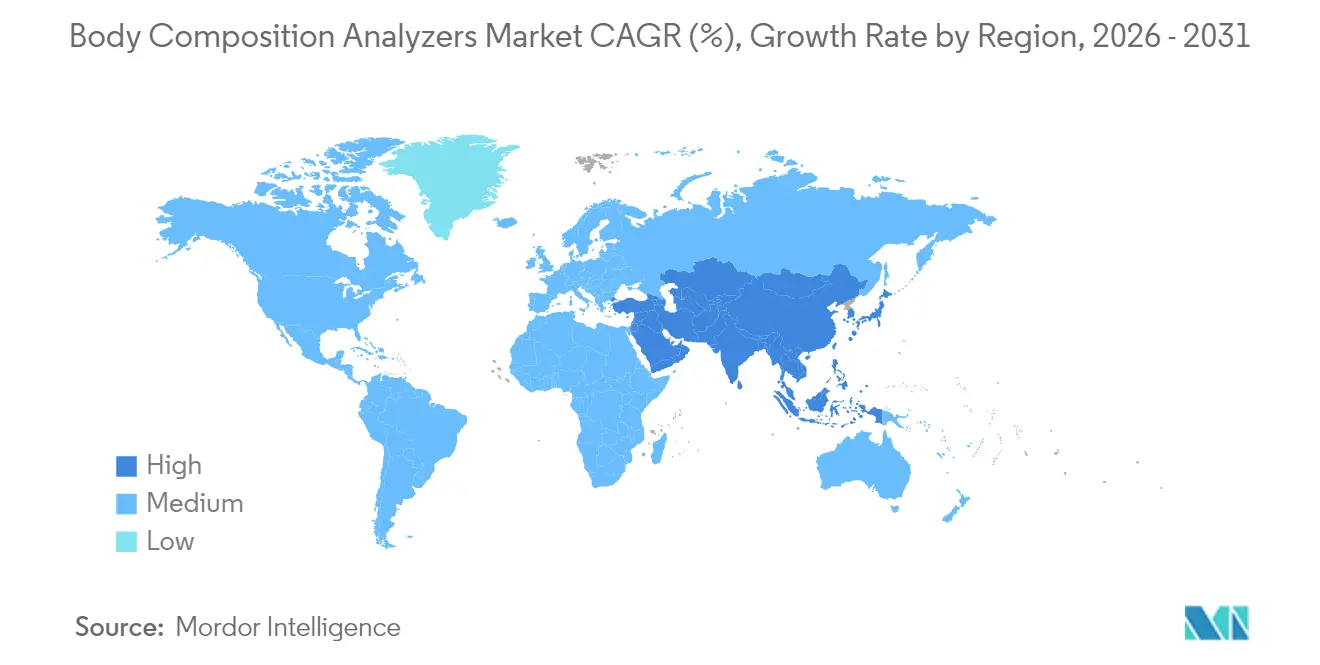

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Body Composition Analyzers Market Analysis by Mordor Intelligence

Body Composition Analyzers market size in 2026 is estimated at USD 674.92 million, growing from 2025 value of USD 639.01 million with 2031 projections showing USD 887.36 million, growing at 5.62% CAGR over 2026-2031.

Growth reflects a clear migration of body composition measurement from a niche diagnostic to a widely adopted health-monitoring tool across clinical, fitness, and household settings. Uptake is propelled by the convergence of rising global metabolic-disease prevalence, continual product miniaturization, and multi-frequency bioelectrical impedance innovations that now approach dual-energy X-ray absorptiometry (DEXA) accuracy while preserving portability and cost benefits. Regulatory support such as clearer U.S. Food and Drug Administration (FDA) device classifications and the gradual inclusion of metabolic screening in reimbursement schedules reinforces provider confidence, while home users embrace connected scales that translate raw impedance signals into actionable wellness guidance. Competitive activity shows established manufacturers refining algorithms for ethnic- and age-specific accuracy even as smartphone-based 3-D optical scanning gains traction, setting the stage for hybrid ecosystems that blend hardware precision with cloud analytics.

Key Report Takeaways

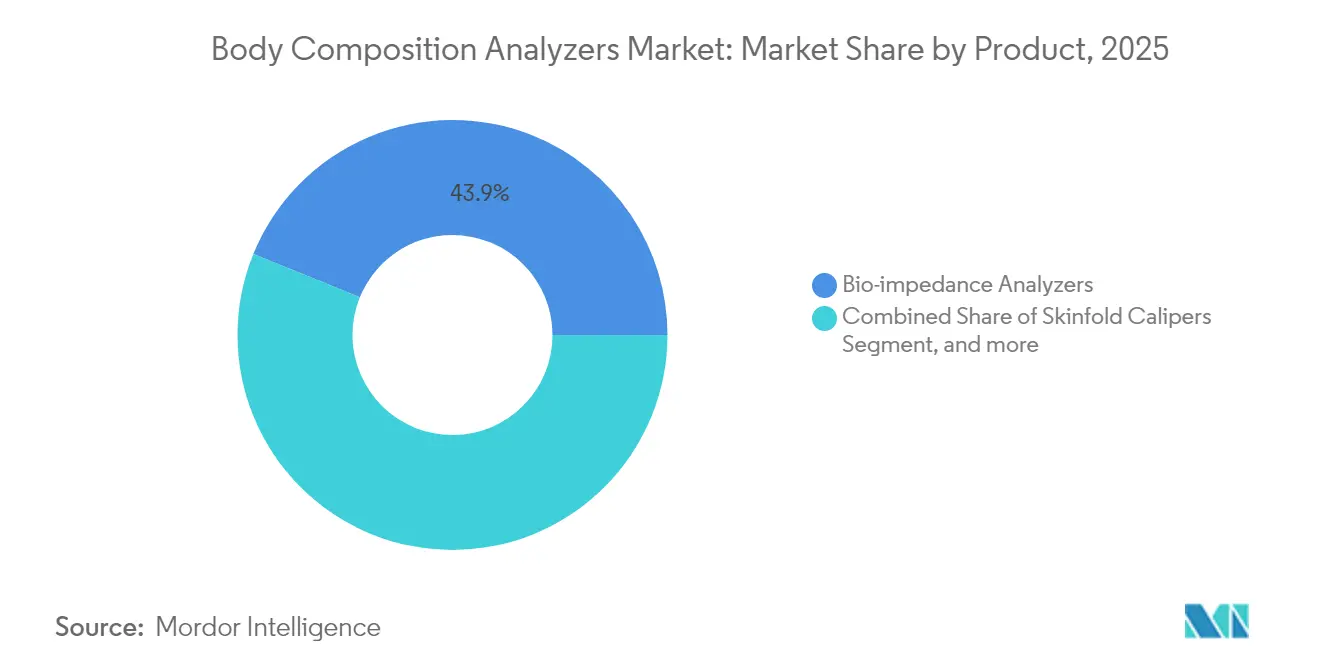

- By product category, bio-impedance analyzers led with a 43.85% share of the body composition analyzers market in 2025, while 3-D optical body scanners are projected to expand at a 7.22% CAGR through 2031.

- By measurement technology, multi-frequency BIA commanded 53.40% of the body composition analyzers market size in 2025 and is forecast to grow steadily, whereas Portable/Hand-held Systems register the quickest 8.05% CAGR to 2031.

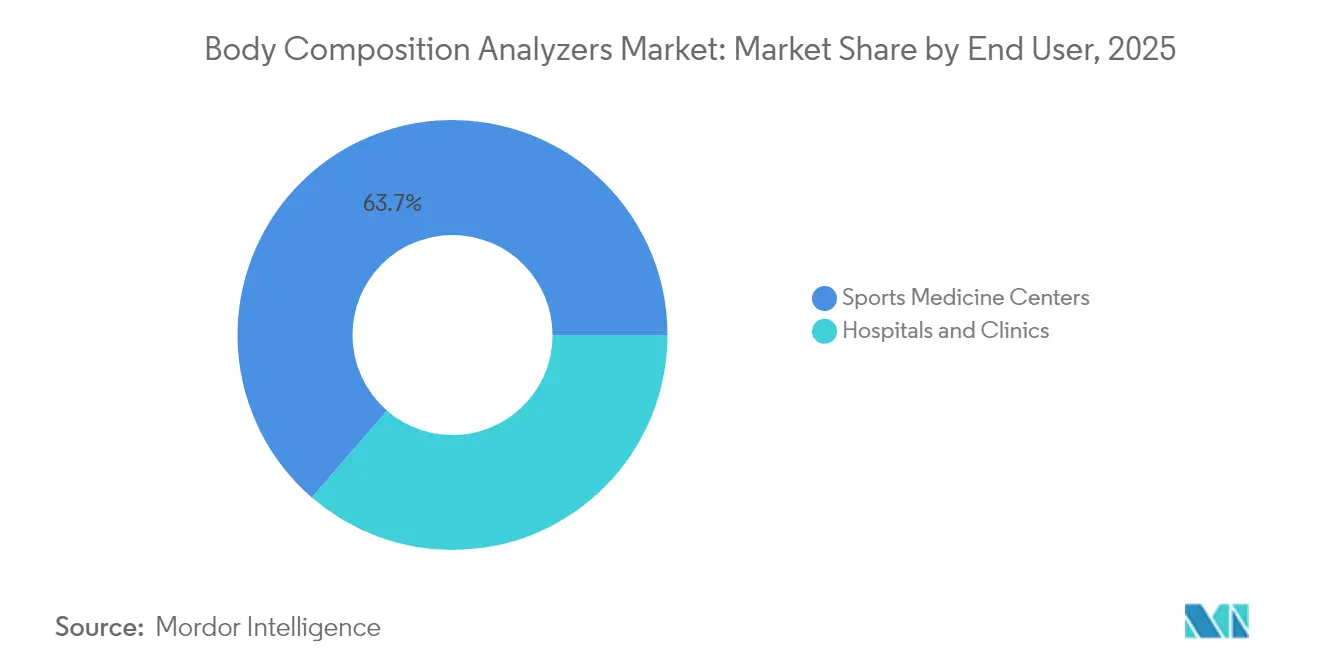

- By end user, hospitals & clinics maintained 36.35% revenue in 2025; home care settings show the fastest 8.45% CAGR, reflecting consumer empowerment and telehealth integration.

- By geography, North America retained 33.60% market prominence in 2025; Asia Pacific is the fastest-advancing geography at a 9.35% CAGR, fueled by infrastructure modernization and an aging population.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Body Composition Analyzers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large pool of obese and metabolic-disorder patients | +1.8% | North America, Europe, global reach | Long term (≥ 4 years) |

| Technological advancements in multi-frequency BIA | +1.2% | Global, APAC innovation hubs | Medium term (2-4 years) |

| Rising consumer awareness for health & fitness | +0.9% | North America, Europe, widening APAC | Medium term (2-4 years) |

| Expansion of preventive-care reimbursements | +0.7% | North America, Europe, gradual APAC | Long term (≥ 4 years) |

| Integration with tele-nutrition & telehealth platforms | +0.6% | Global | Short term (≤ 2 years) |

| Adoption in professional sports performance analytics | +0.4% | North America, Europe, emerging APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Large Pool of Obese & Metabolic-Disorder Patients

Obesity is rising at an unprecedented pace, with adults living with obesity projected to more than double to 1.13 billion by 2030. Clinical guidelines increasingly prefer body composition metrics over BMI because impedance-based analysis can uncover sarcopenic obesity hidden high-fat low-muscle profiles that BMI alone misses. Global estimates show 506 million people already living with metabolic disorders in 2024. Health systems are therefore upgrading diagnostic protocols to include impedance testing for visceral adiposity, transforming analyzers from optional equipment into core preventative-care devices. The shift aligns with payer incentives that reward early risk stratification; insurers see reduced long-term outlays when metabolic deterioration is caught early. Hospitals consequently incorporate analyzers into annual wellness checks and bariatric-surgery pathways, cementing demand over the long term.

Technological Advancements in Multi-Frequency BIA

Multi-frequency BIA measures intracellular and extracellular water separately, pushing correlation with DEXA beyond 0.973 in current clinical studies.[1]A. Bosy-Westphal et al., “Multi-Frequency BIA Accuracy Against DEXA,” Frontiers in Nutrition, frontiersin.org Advancements in eight-electrode placement and phase-angle analytics provide a window on cellular membrane integrity—useful for oncology, nephrology, and critical-care nutrition. Manufacturers embed artificial-intelligence routines that auto-select ethnic-specific equations, removing a key accuracy barrier in diverse populations. Wearable impedance patches now relay hydration and muscle-glycogen estimates to mobile dashboards, enabling continuous monitoring. Together these upgrades reduce inter-operator variability and extend use cases beyond weight management to comprehensive metabolic profiling.

Rising Consumer Awareness for Health & Fitness

Consumers increasingly link lean-mass preservation to healthy aging. Social platforms popularize “skinny-fat” warnings, spurring users to verify fat-percentage rather than scale weight. Gym chains bundle membership with free quarterly body composition scans, while health-app ecosystems sync impedance results with macro-nutrient targets. Retailers report sustained double-digit growth in connected scales as households prioritize data-driven wellness. Home devices now flag hydration status, basal metabolic rate, and visceral-fat scores, converting raw electrical readings into plain-language insights. These lifestyle drivers magnify the consumer slice of the body composition analyzers market, complementing clinical demand.

Expansion of Preventive-Care Reimbursements

The 2025 U.S. Physician Fee Schedule now reimburses impedance-based muscle-mass assessments under malnutrition screening codes.[2]M. Bundy et al., “Cellular Health and Phase Angle,” Bioengineering, mdpi.com European payers have started covering sarcopenia diagnostics following recommendations from the Global Leadership Initiative on Malnutrition.[3]J. Cederholm et al., “Global Leadership Initiative on Malnutrition Framework,” Current Opinion in Clinical Nutrition & Metabolic Care, oup.com Such policy momentum lowers cost barriers for small clinics and primary-care offices. Corporate wellness programs also subsidize onsite scans as part of metabolic-risk management, further widening the reimbursed user base. Over a longer horizon, broader payer acceptance in Asia Pacific is expected as pilot data confirm reductions in diabetes- and cardiovascular-treatment expenses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High equipment & maintenance costs | -0.8% | Global, emerging markets | Long term (≥ 4 years) |

| Measurement inconsistency across device types | -0.6% | Global | Medium term (2-4 years) |

| Data-privacy & cybersecurity compliance hurdles | -0.4% | Europe, North America | Short term (≤ 2 years) |

| Emerging optical/AI body-scan substitutes | -0.3% | North America, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Equipment & Maintenance Costs

Entry-level multi-frequency units start around USD 6,755 and climb to USD 50,000 for research-grade systems. Annual calibration, electrode replacement, and software-license renewals inflate lifetime cost, deterring small clinics and independently owned gyms. Emerging-market providers face higher financing costs and spotty service coverage, raising downtime risk. Leasing programs soften the blow but still require volume guarantees difficult to meet in sparsely populated regions. Until economies of scale drive pricing down, upfront expense will cap the body composition analyzers market penetration rate in cost-sensitive geographies.

Measurement Inconsistency Across Device Types

Algorithmic differences among manufacturers can swing fat-percentage readings by 2-4 points, challenging longitudinal tracking when facilities upgrade hardware or patients switch brands. Clinical guidelines recommend device consistency, yet cross-calibration standards remain nascent. Multi-frequency BIA narrows variance, but single-frequency consumer scales and 3-D optical apps introduce data heterogeneity that complicates electronic-health-record integration. Efforts by ISO committees to harmonize impedance reference models are ongoing but not yet universally adopted.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Bio-impedance Dominance Faces Optical Disruption

Bio-impedance Analyzers held a 43.85% body composition analyzers market share in 2025 due to extensive clinical validation and relatively modest capital requirements. 3-D Optical Body Scanners, however, post the fastest 7.22% CAGR to 2031 as computer-vision algorithms mature and hardware costs fall. Dual-energy X-ray Absorptiometry retains relevance for research and osteoporosis screening but remains limited by high purchase price and radiation protocols. Skinfold Calipers continue in educational settings where budget and technical simplicity outweigh precision. Air-Displacement Plethysmography and Hydrostatic Weighing serve research institutions seeking gold-standard accuracy, whereas smart connected scales attract cost-conscious home users. Continuous R&D in electrode materials, impedance signal filtration, and phase-angle analytics ensure that bio-impedance devices stay competitive amid optical advances.

The product landscape diversifies further as hybrid systems fuse impedance cores with optical cameras, delivering both internal composition metrics and external body-shape visuals. Such convergence positions manufacturers to tap fitness-app partnerships and leverage social-media-sharing trends. Intellectual-property filings reveal interest in dynamic electrode selection and miniaturized current-injection circuits, pointing to future wearables that deliver DEXA-like insight without clinic visits. Hence, while incumbents anchor volume today, innovators leveraging artificial intelligence and alternative sensing modalities will shape longer-term demand.

By Measurement Technology: Multi-frequency BIA Leads Innovation

Multi-frequency BIA secured 53.40% of the body composition analyzers market size in 2025 by offering granular intracellular-extracellular water separation and superior accuracy for clinical decision-making. Portable/Hand-held Systems expand fastest at an 8.05% CAGR as primary-care physicians, home-visiting nurses, and sports trainers favor lightweight devices that sync to mobile dashboards. Single-frequency instruments survive in budget-limited contexts but face gradual replacement. Segmental BIA gains popularity for rehabilitation and athlete monitoring where limb-level analysis guides targeted interventions. Wearable impedance sensors emerge, lining compression garments or watch straps to provide continuous, non-invasive monitoring of hydration and muscle-glycogen trends. Benchtop/Standalone Systems still dominate tertiary hospitals demanding full-featured analysis and electronic-medical-record integration.

Phase-angle analytics an indicator of cellular health broadens measurement output from mere body-fat readings to prognostic biomarkers relevant in oncology and critical-care nutrition. Software suites increasingly apply machine learning to adjust equations for pediatric, elderly, and ethnically diverse cohorts, mitigating historic bias and supporting wider clinical adoption. This trajectory consolidates multi-frequency BIA as the technological backbone of upcoming device generations.

By End User: Home Care Settings Drive Growth

Hospitals & Clinics controlled 36.35% revenue in 2025, reflecting entrenched use in bariatric medicine, nephrology, and oncology support. Procedures such as chemotherapy dosing and dialysis fluid management lean on impedance-derived fluid-compartment insights, reinforcing hospital demand. Home Care Settings, however, deliver the highest 8.45% CAGR to 2031 as consumers link composition metrics to wellness goals, and telehealth reimburses remote monitoring. Bluetooth-enabled scales now push encrypted readings to dietitians, enabling personalized meal plans without in-office visits.

Fitness Clubs & Wellness Centers adopt analyzers to differentiate membership packages, offering quarterly body scans that track fat-loss and muscle-gain programs. Sports Medicine & Performance Centers integrate high-frequency, segmental units into athlete support regimes to optimize training loads and recovery. Academic & Research Institutes propel methodological improvements through validation trials, often in collaboration with device vendors. Overall, cross-sector integration with digital platforms underscores the transition from episodic measurement to continuous, personalized health management.

Geography Analysis

North America held 33.60% of global revenue in 2025, anchored by well-funded healthcare systems, explicit CPT reimbursement codes, and mature telehealth infrastructure. Market expansion there now leans on replacement demand, software-subscription add-ons, and broader household uptake rather than first-time clinical purchases. Canada mirrors U.S. trends but adds provincial tele-nutrition pilots that outfit rural clinics with portable analyzers to offset specialist shortages.

Asia Pacific records a robust 9.35% CAGR through 2031, underpinned by aging populations, obesity escalation, and government-backed preventive-health campaigns. Japan’s sarcopenia-screening guidelines spur hospital procurement, while China’s fitness-club boom embraces connected scales for member engagement. Local manufacturing clusters in South Korea and China cut device cost, aiding price-sensitive segments. Telemedicine expansions across India and Southeast Asia unlock rural deployments, though device financing and physician-training gaps temper near-term volumes.

Europe remains steady, benefiting from stringent EU MDR compliance that assures device quality and GDPR-aligned data governance attractive to risk-averse providers. Public-health agencies promote malnutrition and sarcopenia screening, expanding clinical use. Nordic countries showcase near-universal electronic-health-record integration, setting benchmarks for seamless data flow. Southern and Eastern European nations advance gradually, balancing tight budgets with EU funding earmarked for digital health modernization.

Regulatory Landscape

In the United States, body composition analyzers marketed for medical measurement purposes are regulated by the U.S. Food and Drug Administration (FDA) as Class II devices under 21 CFR 870.2770, commonly referenced through FDA product codes such as MNW and PUH. The regulatory pathway depends on intended use, since devices positioned for general wellness claims can fall under specified 510(k) exemption limitations, while diagnostic or clinically intended analyzers typically follow the Class II special-controls framework and associated premarket and quality-system expectations.

In Europe, body composition analyzers fall under Regulation (EU) 2017/745 (EU MDR). Clinical measurement devices are commonly treated as Class IIa (for example, under Annex VIII classification logic such as Rule 10), with conformity assessment routes often aligned to Annex IX. Manufacturer Declarations of Conformity for MDR-marketed analyzers typically bundle MDR requirements with supporting compliance to core safety and software expectations, including electrical safety and wireless directives, and software lifecycle standards such as EN 62304 and EN 82304-1. Notified Body involvement is evidenced in updates such as Charder Electronic Co., Ltd's MDR declaration activity (DNV Product Assurance AS, NB 2460) issued in January 2025.

Competitive Landscape

The body composition analyzers market exhibits moderate concentration. InBody, Tanita, and seca maintain leadership by combining proprietary algorithms, multi-frequency capabilities, and broad regulatory clearances. seca’s 2025 release of the portable mBCA Alpha widens primary-care reach, while Tanita’s refreshed MC-980U Plus targets high-throughput fitness and clinical venues. InBody enhances cloud analytics to deliver cohort benchmarking dashboards, strengthening customer lock-in.

Competitive pressure rises from AI specialists embedding 3-D body scanning into smartphone apps. Partnerships such as Fit3D and Prism Labs illustrate an asset-light path that circumvents dedicated hardware. Start-ups like Neko Health secure substantial venture funding to extend camera-based screening platforms, eyeing rapid consumer scaling. Traditional vendors answer by adding optical modules or offering API gateways for third-party image analytics, thereby protecting installed bases.

Regulatory hurdles remain a double-edged sword: they slow newcomers but also raise compliance costs for incumbents. Cyber-security certifications and periodic algorithm-performance audits are now common tender prerequisites in hospital procurement. Further differentiation revolves around cloud-platform openness, real-time coaching features, and localized equation libraries that deliver accurate results across ethnicities.

Body Composition Analyzers Industry Leaders

Hologic Inc.

Bodystat Ltd

COSMED Srl

Charder Electronic Co. Ltd

InBody Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A gap is emerging at the intersection of clinical-grade bioelectrical impedance (multi-frequency, multi-zone or segmental) and consumerized delivery models (home scales and gym deployments) that retain professional rigor while reducing access friction. 2026 launches point to this direction, as Withings introduced BodyFit with 6-zone segmental analysis and 13-frequency BIS, and also released BodyScan 2 in the UK with added cardiometabolic markers. Together, these moves indicate product roadmaps that go beyond single-point body fat readings toward broader longitudinal screening and coaching ecosystems.

Partnerships and commercialization models also target utilization density outside hospitals, supporting higher device throughput as well as recurring software and service attachment. InBodys July 2026 partnership with HYROX North America standardizes body composition and performance assessment within a large-format fitness racing community, creating repeat measurement touchpoints and a data layer that can connect with coaching and member management. On the supply side, consolidation around BIA know-how continues, such as COSMEDs 2025 acquisition of Bioparhom, while provider-side adoption barriers are being addressed through financing approaches like InBodys 2024 leasing program for professional analyzers, which helps smaller fitness operators and clinics shift procurement from capex to opex.

Recent Industry Developments

- July 2026: InBody became the Official Body Composition and Performance Measurement Partner of HYROX North America. The partnership embeds standardized testing into an organized fitness racing format, increasing recurring measurement volume and reinforcing InBodys position in performance-centric use cases.

- September 2025: COSMED acquired Bioparhom, a French bio-impedance analysis (BIA) technology company, to strengthen its leadership in body composition and metabolic assessment. The deal expands COSMEDs internal BIA capability stack and supports tighter integration between metabolic and composition diagnostics across its portfolio.

- March 2024: InBody unveiled a leasing program for its professional body composition analyzers (including InBody380 and InBody580) at IHRSA in Los Angeles. By lowering upfront purchase barriers for gyms and wellness operators, the program broadens access to higher-end analyzers and supports faster installed-base growth in cost-sensitive channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers devices used to measure body composition and report outputs like fat mass, lean mass, and related indicators at the point of testing in clinical, fitness, and research settings across major regions.

Scope exclusions: We exclude pure software-only wellness apps and general weight-only scales that do not provide body composition outputs.

Segmentation Overview

- By Product

- Bio-impedance Analyzers

- Skinfold Calipers

- Hydrostatic Weighing Equipment

- Air-Displacement Plethysmography

- Dual-energy X-ray Absorptiometry (DEXA)

- 3-D Optical Body Scanners

- Smart Connected Scales

- Other Products

- By Measurement Technology

- Single-frequency BIA

- Multi-frequency BIA

- Segmental BIA

- Portable/Hand-held Systems

- Benchtop/Standalone Systems

- By End User

- Hospitals & Clinics

- Sports Medicine Centers

- Home Care Settings

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to map the addressable demand pool and build practical assumptions around testing locations, device replacement cycles, and pricing ranges. We relied on non-paywalled sources such as CDC obesity and health-statistics releases, WHO and OECD health indicators, NIH and PubMed indexed clinical literature on body composition measurement, and customs and trade statistics portals that help track relevant medical device shipments.

On top of that, we reviewed company filings, investor presentations, product brochures, and reputable press coverage to understand how devices are positioned by setting and measurement method. Select paid subscriptions were used only for company financials and structured news coverage so that revenue context and major events could be cross-checked. The desk source list is illustrative, and additional public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work centered on interviews and surveys with device makers, distributors, hospital and clinic users, fitness and wellness operators, and research users, so our assumptions could be tested against actual purchase and usage conditions. We used respondent input to confirm what is counted as a body composition analyzer sale (and what is excluded), refine average selling price ranges by device class, and sanity-check adoption changes across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 49% |

| Mid tier: 51% | Functional/Unit leaders: 33% | EMEA: 30% |

| Smaller Players: 18% | Managers: 54% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand reconstruction, where healthcare and fitness activity indicators are translated into an estimated pool of testing sites and device needs by region, and then converted into value using typical pricing bands. The totals are then checked with selective bottom-up approximations such as sampled ASP times expected annual unit flow for key channels, plus distributor feedback on order sizes and replacement timing, so the final number stays realistic.

Inputs that shape the model include obesity and metabolic health trends, growth of fitness clubs and wellness centers, hospital and clinic diagnostic activity, device replacement cycles (including calibration and wear factors), mix shift across BIA and other measurement methods, and observed pricing dispersion between portable and stationary systems. When bottom-up signals are incomplete for smaller countries, gaps are handled using proxy ratios from similar markets and then adjusted after interviews confirm whether adoption is above or below the proxy.

Data Validation & Update Cycle

Before sign-off, outputs are triangulated against independent signals like reported demand by care setting, trade flow directionality, and whether implied device counts look reasonable versus the estimated number of active sites. Outliers are investigated with variance checks on price, mix, and adoption, and then reviewed in more than one analyst pass so that simple input errors do not carry into the final tables.

The report is refreshed annually, and interim updates are made when material events can shift demand or pricing, such as regulatory moves, major product refreshes, or channel disruptions. Right before delivery, we do a final scan and re-contact sources when a key assumption no longer matches the latest public and interview signals.

Mordor Intelligence's Body Composition Analyzer Market Sizing Compared With Other Published Estimates

Published market sizes for body composition analyzers can differ even when they describe the same measurement outcome, because the counted products, selling settings, and the year used for currency conversion are not always aligned. Differences also show up when one estimate places more weight on consumer smart scales, or when another includes clinical-grade systems with higher prices.

Key gap drivers in this market are typically the inclusion of connected scales sold for home use, how DEXA and other adjacent imaging tools are treated, and whether the model assumes faster price inflation versus stable pricing. Another common driver is refresh timing, since new device launches and channel promotions can shift ASP and mix within a short window.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.67 B (2026) | |

| Global Consultancy A | USD 0.89 B (2025) | Uses a broader device universe that can extend into consumer-grade connected scales and wider wellness-grade devices, and it also references an earlier base year where pricing and mix assumptions may not match later-year channel conditions. |

| Industry Research Group B | USD 0.70 B (2024) | Anchors the model on an earlier year and applies a higher growth curve, which can reflect aggressive adoption assumptions for home and fitness settings without the same level of cross-checking against device replacement timing. |

The table shows a spread mainly tied to what gets included in the device scope and which year anchors the pricing and mix. In Mordor Intelligence's model, the value is tied to body composition analyzer device sales across defined measurement categories, rather than folding in weight-only consumer devices. When those scope lines are held steady and then validated with demand signals from care and fitness settings, the resulting total is easier to trace back to repeatable inputs.

Key Questions Answered in the Report

How large is the body composition analyzers market in 2026?

The body composition analyzers market size stands at USD 674.92 million in 2026, with a 5.62% CAGR projected to 2031.

Which product type currently leads global sales?

Bio-impedance Analyzers hold the largest 43.85% share, reflecting clinical validation and affordable ownership costs.

What end-user segment is expanding the fastest?

Home Care Settings post the highest 8.45% CAGR, driven by connected scales and telehealth integration.

Why are multi-frequency devices favored in hospitals?

Multi-frequency BIA distinguishes intracellular from extracellular water, enhancing diagnostic precision for metabolic and hydration status.

Which region offers the strongest growth outlook?

Asia Pacific leads with a 9.35% CAGR through 2031, supported by preventive-health campaigns and manufacturing cost advantages.

What key restraint could slow future adoption?

High equipment and maintenance costs, especially in emerging markets, continue to constrain broader penetration.

Page last updated on: