Fluid Biopsy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

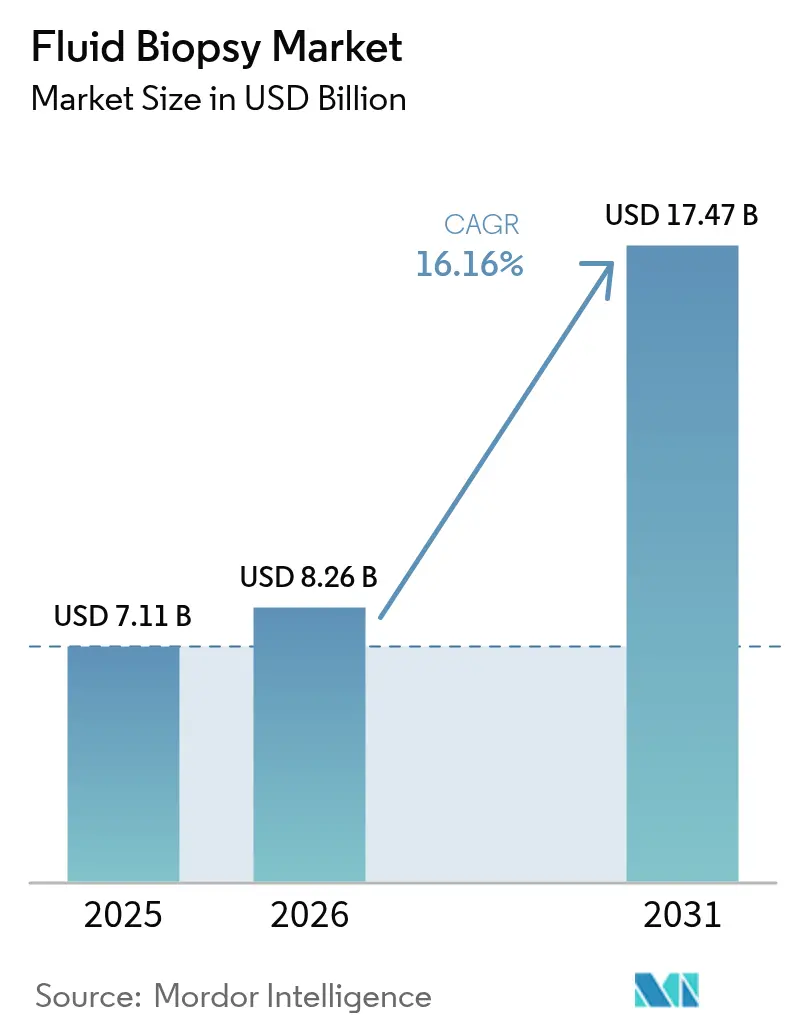

| Market Size (2026) | USD 8.26 Billion |

| Market Size (2031) | USD 17.47 Billion |

| Growth Rate (2026 - 2031) | 16.16% CAGR |

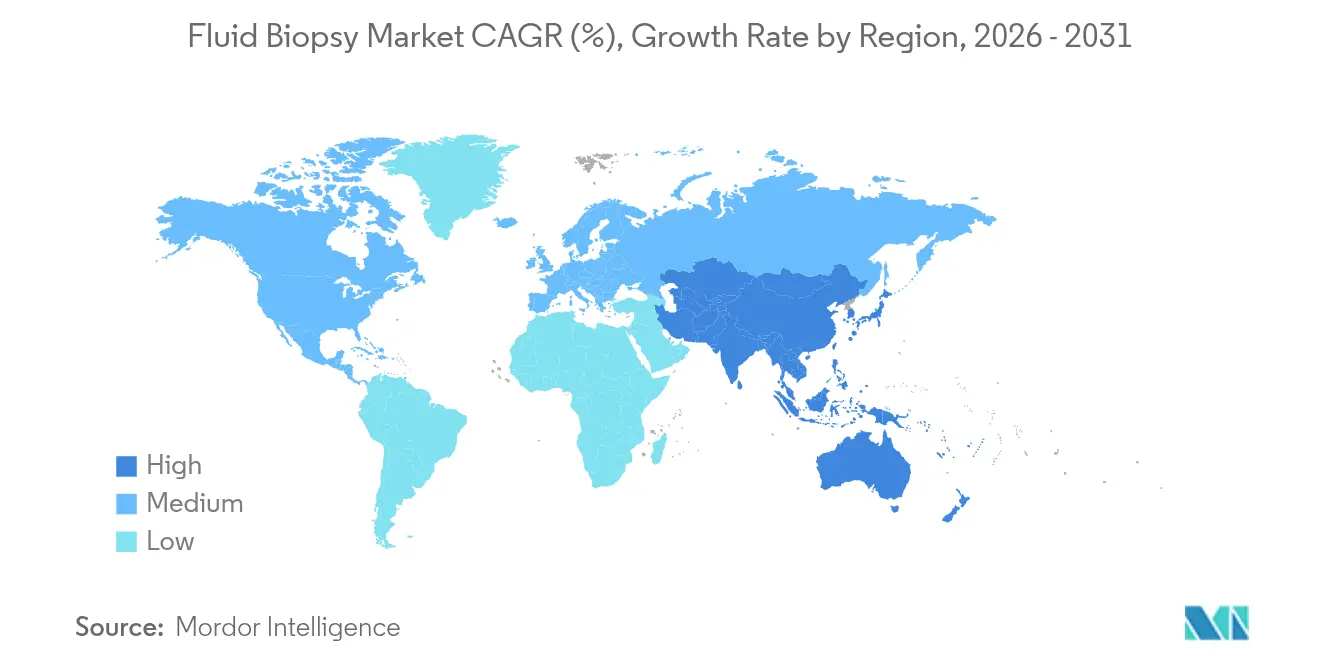

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

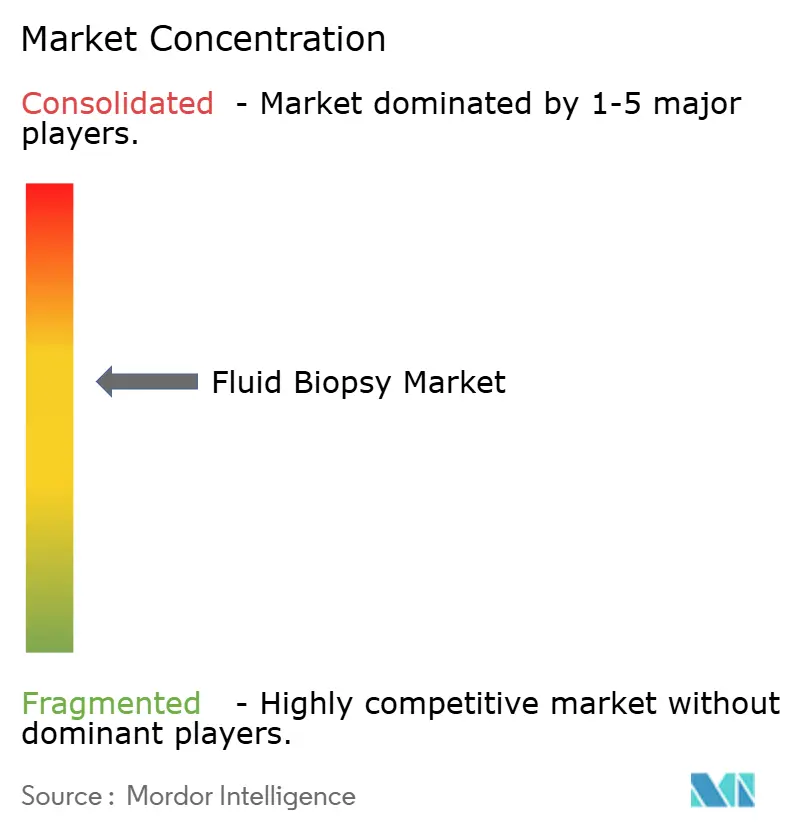

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fluid Biopsy Market Analysis by Mordor Intelligence

The fluid biopsy market size in 2026 is estimated at USD 8.26 billion, growing from 2025 value of USD 7.11 billion with 2031 projections showing USD 17.47 billion, growing at 16.16% CAGR over 2026-2031. Rapid AI-guided signal-enrichment techniques, broader Medicare coverage, and multiple FDA breakthrough device designations position fluid biopsies as a routine component of precision oncology workflows. Machine-learning fragmentomics improves detection of circulating tumor DNA (ctDNA) in early-stage cancers, mitigating the low-yield barrier that once limited screening programs. Investment momentum remains strong: single funding rounds now exceed USD 105 million for platform developers that combine next-generation sequencing (NGS) with decentralized automation to shorten turnaround times. Competitive intensity is rising as emerging players deliver software-centric tools that challenge incumbents on sensitivity, price, and scalability. Asia-Pacific’s regulatory agility and large at-risk population create outsized growth potential, while North America retains leadership through reimbursement certainty and research depth.

Key Report Takeaways

- By indication, lung cancer led with 33.12% of the fluid biopsy market share in 2025; pancreatic cancer indications are projected to expand at an 17.98% CAGR through 2031.

- By biomarker, ctDNA captured 45.10% revenue in 2025; extracellular vesicles and exosomes are advancing at a 18.82% CAGR.

- By product & service, kits and reagents dominated with 44.05% 2025 revenue; bioinformatics software posts the fastest 19.60% CAGR.

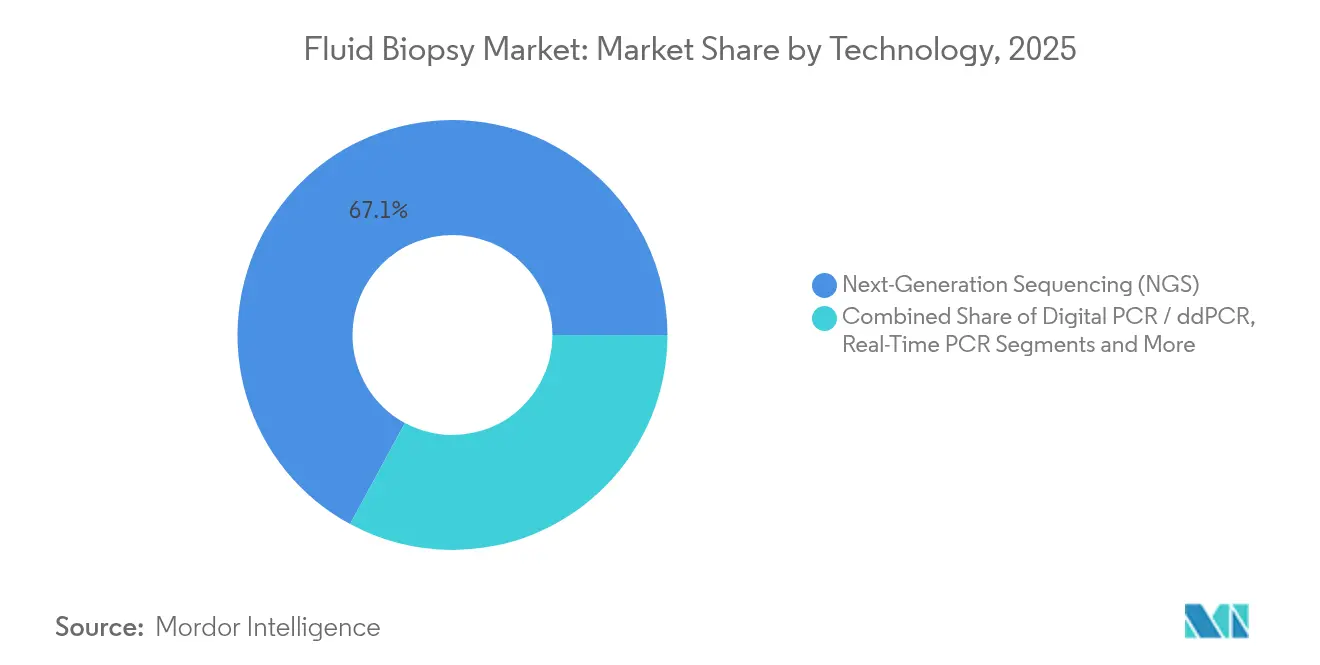

- By technology, NGS held 67.10% of the fluid biopsy market size in 2025; digital PCR usage is growing at 17.93% CAGR.

- By end user, hospital and physician labs accounted for 38.30% 2025 revenue; reference laboratories record the highest 18.90% CAGR.

- By sample type, blood maintained 67.25% share in 2025; urine-based tests are set to rise at an 17.86% CAGR.

- By geography, North America commanded 38.20% of 2025 revenue; Asia-Pacific is poised for a 19.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fluid Biopsy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Preference For Non-Invasive Oncology Diagnostics | +3.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Rapid Increase In Global Cancer Incidence | +2.8% | Global, concentrated in aging populations | Long term (≥ 4 years) |

| Sequencing-Cost Decline & NGS Workflow Automation | +2.1% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Reimbursement Expansion For Minimal Residual-Disease (MRD) Blood Tests | +1.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| AI-Driven Fragmentomics Boosting Early-Stage Detection Accuracy | +2.5% | Global, led by North America research centers | Medium term (2-4 years) |

| Venture Capital Inflow To Decentralized Fluid-Biopsy Platforms | +1.8% | North America & EU venture ecosystems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Non-Invasive Oncology Diagnostics

Patient demand for safer procedures has re-shaped cancer work-ups. Medicare’s 2025 coverage of Guardant Health’s Shield assay validates liquid biopsy utility for routine screening and extends access to Veterans Affairs beneficiaries[1]Guardant Health, “Guardant Health Announces Strategic Collaboration With Pfizer,” investors.guardanthealth.com. Elderly cohorts gain most because tissue biopsy complications rise sharply with comorbidities. Real-time blood-based monitoring allows oncologists to modify therapy sooner than imaging-based schedules, giving fluid biopsy market solutions a complementary role rather than a replacement one. Outpatient clinics adopt the tests quickly because sample collection requires only phlebotomy skills. The trend reinforces decentralized testing demand and underpins recurring reagent revenue.

AI-Driven Fragmentomics Boosting Early-Stage Detection Accuracy

Machine-learning models now interpret fragment length, end motif, and methylation patterns from cell-free DNA to identify early tumors with 92% sensitivity at 90% specificity in non-small cell lung cancer trials. Weill Cornell Medicine’s MRD-EDGE protocol detects residual disease months before radiographic relapse, facilitating pre-emptive therapy switches. Johns Hopkins’ ARTEMIS-DELFI platform provides real-time pancreatic cancer response metrics, addressing a malignancy that historically evaded surveillance. These advances make AI the core infrastructure for future fluid biopsy market platforms. Continuous algorithm training with global data sets will likely widen performance gaps between AI-native and conventional assays.

Sequencing-Cost Decline & NGS Workflow Automation

NGS reagent prices have fallen faster than Moore’s law benchmarks, and Ultima Genomics’ UG100 system further slashes whole-genome costs for 30x coverage. Automation strips out manual pipetting, reducing variability and technician time, which allows regional labs to add liquid biopsy to existing menus without complex validation. Roche’s USD 50 billion US investment commitment underscores a scaling strategy aimed at high-volume, low-cost distribution[2]Roche, “Roche to invest USD 50 billion in pharmaceuticals and diagnostics in the United States,” roche.com. Lower costs unlock large-population screening pilots and accelerate multi-cancer early detection programs inside public health budgets. Standardized workflows also reduce batch-to-batch variability, strengthening payer confidence.

Reimbursement Expansion for Minimal Residual-Disease Blood Tests

Adaptive Biotechnologies’ clonoSEQ obtained an updated Clinical Laboratory Fee Schedule rate of USD 2,007, confirming robust reimbursement for MRD testing. Similar positive coverage determinations in Europe indicate harmonizing payer views on outcome-linked diagnostics. Reimbursement certainty allows laboratories to invest in equipment and recruit specialized personnel, expanding test availability in regional cancer centers. Evidence showing reduced chemotherapy cycles and earlier intervention supports cost-effectiveness claims, encouraging further policy alignment. Sustainable payment structures drive broader adoption, especially in community oncology networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Test Cost & Reimbursement Hurdles | -2.1% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Emerging Optical-Biopsy & Imaging Substitutes | -1.3% | North America & EU advanced healthcare systems | Long term (≥ 4 years) |

| Pre-Analytical Sample-Handling Variability | -1.7% | Global, concentrated in decentralized settings | Short term (≤ 2 years) |

| Low Ctdna Yield In Early-Stage Tumors | -2.3% | Global, affecting screening applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Test Cost & Reimbursement Hurdles

Comprehensive liquid biopsy panels still average USD 2,800 per use, challenging adoption in systems with constrained oncology budgets. Health-economic models indicate prices must drop by two-thirds for second-line colorectal screening to reach cost-effectiveness thresholds. Payer review cycles remain lengthy, demanding robust clinical-utility evidence rather than analytical-validity data. Emerging markets face additional currency fluctuation risks that complicate budgeting for imported reagents. Until scalable manufacturing achieves double-digit cost reductions, uptake outside premium tertiary centers may remain modest.

Low ctDNA Yield in Early-Stage Tumors

Early tumors shed scant DNA, lowering detection sensitivity in screening contexts where intervention benefits are highest. Signal-enrichment algorithms and multi-analyte approaches alleviate but do not fully solve this limitation. Population-level screening pilots thus focus first on high-risk cohorts to mitigate false negatives. Research consortia now investigate extracellular vesicles, microRNAs, and tumor-educated platelets to provide additive sensitivity. Implementation timelines hinge on securing regulatory approval for these novel biomarkers, which may stretch into the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: Lung Dominance and Pancreatic Momentum

In 2025, lung applications generated 33.12% of overall revenues, consolidating leadership through multiple FDA-cleared companion diagnostics that guide EGFR, ALK, and MET inhibitor therapy selections. The fluid biopsy market benefits from well-mapped mutation profiles and the clinical necessity of repeat testing at progression, which boosts reagent pull-through. Pancreatic programs, although starting smaller, post an impressive 17.98% forecast CAGR on the strength of AI-enabled response monitoring platforms that deliver actionable insight within days. Broad payer support for therapy-selection panels encourages hospitals to integrate liquid biopsy into baseline staging protocols.

Real-world data show breast and colorectal oncology teams now add blood-based surveillance between imaging cycles, cutting average radiology utilization by 15%. Prostate cancer indications gain traction after BRCA-positive metastatic castration-resistant approvals expanded testing beyond genomic labs to urology clinics. Ovarian and gastric trials progress steadily as multi-omics assays uncover epigenetic signatures absent in mutation-centric panels. Adoption diversity across tumor types helps cushion revenue cycles against single-indication reimbursement headwinds and keeps the fluid biopsy market on a stable expansion path.

By Biomarker Type: ctDNA Strength and Vesicle Upside

ctDNA supplied 45.10% of the 2025 biomarker revenue, reflecting a decade of cumulative clinical validation and regulatory clearance. However, vesicle-based assays are scaling at a 18.82% CAGR because lipid membranes protect analytes from degradation, yielding higher analytical sensitivity in Stage I diagnoses. Combined protein and RNA cargo analysis inside exosomes supplies orthogonal data that improve false-positive discrimination. Multi-analyte tests pairing ctDNA with vesicle metrics push positive predictive values into imaging-equivalent ranges without procedural risks.

Circulating tumor cells hold niche relevance for phenotyping metastatic progression, while microRNA signatures supplement histology-agnostic programs. Integrative AI pipelines now fuse fragmentomics, methylation, and vesicle-cargo data, enabling tissue-of-origin predictions with sub-10-millimeter tumor burden. Investors prioritizing early-detection claims channel capital into vesicle startups, anticipating premium reimbursement for screening code sets once sensitivity hurdles are cleared. The biomarker race diversifies revenue streams, reducing single-analyte dependence and fostering innovation across the fluid biopsy industry.

By Product & Service: Consumable Leadership and Software Upswing

Kits and reagents represented 44.05% of 2025 turnover because every test run consumes extraction cartridges, library prep reagents, and sequencing consumables. High recurring-use elasticity makes consumables the economic backbone of the fluid biopsy market. Yet software and bioinformatics now compound at a 19.60% CAGR as laboratories outsource pipeline analytics to cloud platforms that enable real-time quality control. Subscription-based models generate predictable revenue and facilitate rapid deployment of algorithmic upgrades without hardware swaps.

Instruments maintain steady sales inside core pathology labs but face elongated replacement cycles. Testing-service contracts grow in clinics lacking internal genomics personnel, and reference laboratories use these agreements to aggregate national specimen volumes. Comprehensive product-service ecosystems yield lock-in advantages, because customers value end-to-end validation frameworks that comply with ISO-accredited workflows. Market entrants focusing solely on consumables risk commoditization pressures unless paired with differentiated software that pushes sensitivity boundaries.

By Technology: NGS Rule and Digital PCR Challenge

NGS contributed 67.10% of all technology revenues in 2025, driven by its ability to interrogate thousands of loci in a single run. Accuracy, read-depth scalability, and continuously falling per-gigabase costs keep NGS the backbone for multi-cancer assays. Digital PCR, advancing at 17.93% CAGR, offers absolute quantification at lower sample input, making it attractive for MRD surveillance when mutation targets are already known. Bio-Rad’s planned acquisition of Stilla Technologies bolsters throughput and multiplexing, positioning digital PCR for cost-sensitive follow-up testing.

Labs frequently deploy qPCR for confirmatory calls where speed outranks breadth. Nanopore sequencing experiments cache real-time field applicability, but read-accuracy gaps still restrict clinical deployment. Hybrid architectures that pipeline targeted digital PCR pre-screens into broad NGS profiling are under validation, promising cost advantages without sensitivity loss. Such workflow flexibility keeps technology choice tied to clinical context rather than vendor lock-in, stimulating demand diversity across the fluid biopsy market.

By End User: Hospital Hubs and Reference Lab Surge

Hospital-based molecular labs held 38.30% 2025 revenue because integrated care networks prioritize point-of-care diagnostics for treatment initiation speed. Reference laboratories, projected to outpace all other settings at 18.90% CAGR, leverage scale to negotiate reagent pricing and deliver complex analytics nationwide. Strategic partnerships between NeoGenomics and Adaptive Biotechnologies illustrate how specialist labs extend reach by pooling sales channels and informatics infrastructure.

Academic centers remain R&D epicenters, generating peer-reviewed evidence that underpins payer policy. Pharmaceutical sponsors increasingly place liquid biopsy in adaptive trial designs, fueling sample volume in contract research organizations. Physician-office labs show incremental adoption as turnkey benchtop instruments become CLIA-waived, easing compliance burdens. Diverse end-user profiles necessitate tiered support models, from 24-hour enterprise informatics to simple web dashboards, broadening total addressable demand.

By Sample Type: Blood Core and Urine Emergence

Blood sampling captured 67.25% of 2025 specimen volume because venipuncture requires minimal logistics and has decades of established phlebotomy protocols. The fluid biopsy market size for blood-based assays is forecast to sustain double-digit expansion given its versatility across tumor types. Urine pipelines, growing at an 17.86% CAGR, gain traction in urological malignancies and repeat-sampling wellness programs because collection is painless and home-compatible.

Saliva and sputum assays provide localized genomic insights in head-and-neck or lung lesions when plasma signal is diluted. Cerebrospinal fluid testing supports central nervous system metastasis monitoring, where blood biomarker permeability is limited by the blood-brain barrier. Pleural and peritoneal effusion sampling address mesothelioma and ovarian surveillance niches. Broadening sample-matrix compatibility increases the resilience of the fluid biopsy market against modality-specific constraints.

Geography Analysis

North America controlled 38.20% of global fluid biopsy market revenue in 2025, supported by FDA breakthrough pathways, generous Medicare coverage, and a dense ecosystem of academic-industry collaborations. United States oncology networks absorb the majority of test volumes, while cross-border patients to Canada and Mexico augment regional demand. Ongoing policy efforts to harmonize sample-handling standards aim to reduce inter-lab variability and protect reimbursement levels tied to quality measures.

Asia-Pacific records the fastest 19.05% CAGR through 2031 as China, Japan, and India expand molecular oncology budgets. China’s 2024 approval of a methylation-based liver cancer assay underscores regulatory willingness to catalyze domestic innovation. Japan’s recent companion diagnostic endorsements for targeted therapies reflect sophisticated regulator–industry dialogue that accelerates product cycles. Government-linked manufacturing incentives lower localized reagent costs, further stimulating uptake.

Europe occupies a mature but still expanding position. Harmonized in-vitro diagnostic regulation, coupled with growing evidence packages, prompts national payers to reimburse MRD monitoring beyond pilot programs. Germany, France, and the United Kingdom anchor market demand through comprehensive cancer centers that value integrated genomic reports. Southern Europe and Scandinavia follow via pan-European procurement schemes that cut acquisition costs. Middle East, Africa, and South America remain nascent but demonstrate increasing trial participation, foreshadowing longer-term commercial opportunities once reimbursement pathways formalize.

Competitive Landscape

The competitive field displays moderate concentration, with Guardant Health, Roche, and Illumina holding sizable but not dominant shares. Guardant capitalizes on multi-indication FDA approvals and AI software that layers new biomarkers onto the Guardant360 franchise. Roche leverages its diagnostic manufacturing footprint to shorten reagent lead times for hospital clients worldwide. Illumina’s post-GRAIL strategy refocuses on core sequencing innovation while continuing to supply flow cells to third-party liquid biopsy developers.

Strategic partnerships shape the competitive chessboard. Foundation Medicine joined with Fulgent Genetics to introduce germline panels that complement somatic profiling, producing cross-sell synergies. Bio-Rad’s offer to acquire Stilla Technologies signals convergence in digital PCR, consolidating IP and accelerating assay menu expansion. Venture-backed entrants push pricing down by 15% to win contracts in high-volume reference labs, forcing incumbents to expand value-added software and biostatistics services.

Product differentiation hinges on analytical sensitivity, sample-to-answer turnaround, and AI-driven interpretive reporting. Vendors overlay cloud portals that integrate with electronic medical records, reducing clinician friction. Subscription-based informatics unlock sustainable revenue independent of commodity reagent margins. The fluid biopsy industry thus shifts from hardware competition toward data-centric ecosystems that embed deeply into oncology care pathways, making switching costs progressively higher.

Fluid Biopsy Industry Leaders

Bio-Rad Laboratories

Guardant Health

Qiagen NV

Roche Diagnostics

Illumina Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Multi-cancer early detection (MCED) and broader screening access create whitespace beyond therapy selection and recurrence monitoring, supported by a faster commercial and clinical-readout cadence. In 2026, Caris Life Sciences commercially launched Caris Detect as an AI-integrated MCED offering, and Freenome reported that its updated SimpleScreen CRC blood test met primary and secondary endpoints with PMA review ongoing. This reinforces the shift from research-only programs toward regulated, population-scale testing pathways. Access improvements also matter for near-term adoption, including Guardant Health making its Shield colorectal cancer screening test available through Quest Diagnostics national ordering and collection, which reduces operational friction for community sites without in-house genomics.

MRD and longitudinal surveillance represent a second opportunity lane, with platform differentiation increasingly centering on multiomic and AI-driven analytics that improve signal yield from small inputs and early-stage disease. CareDx entering liquid biopsy via its agreement to acquire Naveris (up to USD 260 million) underscores strategic interest in MRD-style monitoring using tumor-associated viral DNA (TTMV) alongside ctDNA-centric menus. On commercialization infrastructure, May 2026 FDA classification actions for circulating tumor cell (CTC) enrichment devices into Class II with special controls, alongside payer mechanisms such as MolDX coverage decisions used for liquid biopsy offerings, point to a more standardized route to market for newer biomarker classes (CTCs, fragmentomics, methylation) and multi-analyte workflows across hospitals, reference labs, and decentralized collection settings.

Recent Industry Developments

- July 2026: Caris Life Sciences commercially launched Caris Detect, a blood-based multi-cancer early detection test using AI-integrated whole genome and transcriptome sequencing. The launch broadens competitive pressure in MCED by combining multiomic content with an AI interpretation layer tailored for screening use cases.

- May 2026: SOPHiA GENETICS and Synnovis partnered to bring blood-based cancer testing to patients across the UK, initially focusing on lung and breast cancer applications. The agreement connects a bioinformatics platform with a major laboratory services provider, supporting larger-scale deployment within NHS-aligned workflows.

- May 2025: Guardant Health introduced new smart liquid biopsy applications for its Guardant360 Liquid test, adding expanded tumor profiling features and AI-driven biomarker identification. The update strengthens software-led differentiation around interpretive reporting and supports broader utilization across precision oncology workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from fluid biopsy tests and workflows that detect and track disease signals from blood or other body fluids, including the associated consumables, instruments, software, and lab services used to generate clinical or research results.

Scope exclusions: We exclude conventional tissue biopsy and histopathology, and we also exclude imaging-led optical biopsy approaches and non-oncology prenatal or transplant testing.

Segmentation Overview

- By Indication

- Lung Cancer

- Breast Cancer

- Colorectal Cancer

- Prostate Cancer

- Pancreatic Cancer

- Other Indications

- By Biomarker Type

- Circulating Tumour Cells (CTCs)

- Circulating Tumour DNA (ctDNA)

- Cell-free DNA (cfDNA)

- Extracellular Vesicles / Exosomes

- Other Biomarkers (miRNA, TEPs, proteins)

- By Product & Service

- Kits & Reagents

- Instruments & Platforms

- Software & Bioinformatics

- Testing Services

- By Technology

- Next-Generation Sequencing (NGS)

- Digital PCR / ddPCR

- Real-Time PCR

- Microarray & qPCR

- Other (Nanopore, Lab-on-Chip, etc.)

- By End User

- Reference Laboratories

- Hospital & Physician Labs

- Academic & Research Centers

- CROs & Biopharma

- By Sample Type

- Blood (Plasma/Serum)

- Urine

- Saliva / Sputum

- Cerebrospinal Fluid

- Other Body Fluids

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by setting the science and demand context, then checking what can be measured consistently across regions. We used public sources such as the World Health Organization for cancer burden, the International Agency for Research on Cancer for incidence trends, and the US FDA plus the European Commission public databases for approvals and labeling language that indicates what is actually commercialized.

We also reviewed clinical trial registries (such as ClinicalTrials.gov) and peer reviewed journals to map which biomarkers and sample types are moving from research into routine use, and to understand how often tests are repeated for monitoring. Company filings, investor decks, and credible press materials were used to validate the business mix, installed base narratives, and commercial scale-up timing. Where needed, paid subscriptions for company financials and intelligence, news and financials, and patent databases were used to cross-check funding, launches, and IP intensity. The sources listed here are illustrative, and many additional public documents were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to stress-test what desk research cannot show clearly, including average testing frequency along the patient pathway, typical pricing movement as volumes rise, and which care settings place orders for these tests. We spoke with a mix of assay developers, lab service teams, hospital and lab decision-makers, and domain experts across major regions, so we could adjust assumptions where local reimbursement and adoption patterns differ.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 43% |

| Mid tier: 47% | Functional/Unit leaders: 37% | EMEA: 36% |

| Smaller Players: 17% | Managers: 51% | Americas: 21% |

Market-Sizing & Forecasting

Sizing begins with a top-down demand pool build-up where oncology testing volumes are reconstructed from incidence, eligible patient share, and likely repeat testing for therapy selection and monitoring, then translated into value using typical price bands by assay type and setting. Once the first view is built, we corroborate it with selective bottom-up checks, including sampled revenue disclosures, channel conversations on kit pull-through, and lab workflow throughput assumptions. Totals are adjusted when the two views do not align.

Inputs that matter for this market include the split between therapy selection and monitoring use, the penetration of ctDNA and other biomarker classes in routine care, the share of tests run as in-house kits versus reference lab services, pricing movement as payers expand coverage, and the pace of regulatory clearances that broaden claimed use. Forecasting is run using scenario analysis, since adoption and pricing sensitivity tracks reimbursement decisions and evidence generation timelines. Scenario weights are aligned to what experts expect to be realistic in the next few years. Where bottom-up data is thin in smaller countries, we fill gaps using proxy adoption rates from similar health systems, then re-check the result against regional diagnostic spending signals.

Data Validation & Update Cycle

Outputs are validated through cross-checks that look for logical fit with independent signals, including cancer testing intensity, clinical trial activity, and disclosed commercial scale of leading workflows. If an unexpected jump appears, we return to the driver layer, verify currency conversion timing, and re-check whether a pricing or volume assumption was applied to the correct patient pool.

Before sign-off, the model and narrative pass through multiple analyst reviews so calculation logic and scope remain consistent across regions and years. Reports are refreshed annually, with interim updates when material events occur, such as major approvals or reimbursement changes. Right before delivery, we do a final pass so the client receives the latest updated view.

Mordor Intelligence's Fluid Biopsy Market Size Compared With Other Published Estimates

Published market sizes for fluid biopsy can vary widely because the term is used differently across sources, and because test pricing and adoption are not uniform across regions and care settings. The biggest gaps usually come from what is counted as in-scope revenue and how fast pricing is assumed to normalize as volumes increase.

The main gap comes from mixing broader liquid biopsy uses into the total. Mordor Intelligence counts oncology-focused fluid biopsy revenue tied to biomarker interrogation workflows (kits, instruments, software, and reference lab services) and keeps non-oncology prenatal or transplant testing outside the market size.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.26 B (2026) | |

| Industry Publisher A | USD 5.08 B (2025) | Uses a broader, longer forecast window with a lower near-term value and appears to blend disease areas beyond oncology, which shifts the demand pool and lowers implied testing intensity for cancer-focused workflows. |

| Research Outlet B | USD 5.60 B (2023) | Anchors on an earlier base year and groups a narrower set of technologies, which can undercount newer assay categories and the related software and service revenue that scales with clinical adoption. |

The spread in values is mostly explained by scope choices, base-year timing, and how each source treats technology breadth and repeat testing behavior. Our approach keeps the model traceable to practical drivers, such as eligible patients, testing frequency, and realistic price bands, which makes the final number easier to audit and update as adoption shifts.

Key Questions Answered in the Report

What is the current value of the fluid biopsy market?

The fluid biopsy market size is USD 8.26 billion in 2026 and is on track to reach USD 17.47 billion by 2031.

Which cancer indication generates the most revenue for fluid biopsies?

Lung cancer leads with 33.12% fluid biopsy market share owing to multiple FDA-approved tests for targeted therapy selection.

Why is Asia-Pacific viewed as the fastest-growing region?

Regulatory approvals in China and Japan, rising cancer incidence, and expanding reimbursement drive a 19.05% CAGR for Asia-Pacific through 2031.

How does AI improve liquid biopsy sensitivity?

AI-based fragmentomics interprets cell-free DNA patterns, achieving early-stage cancer detection sensitivities above 90%, surpassing traditional mutation-only assays.

What technologies dominate liquid biopsy testing?

Next-generation sequencing controls 67.10% of 2025 revenue, while digital PCR grows quickly for targeted minimal-residual-disease monitoring.

What are the biggest barriers to wider liquid-biopsy adoption?

High per-test costs, complex reimbursement processes, and low ctDNA yield in early-stage tumors remain key restraints despite ongoing technological progress.

Page last updated on: