Multi-layer Paperboard Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

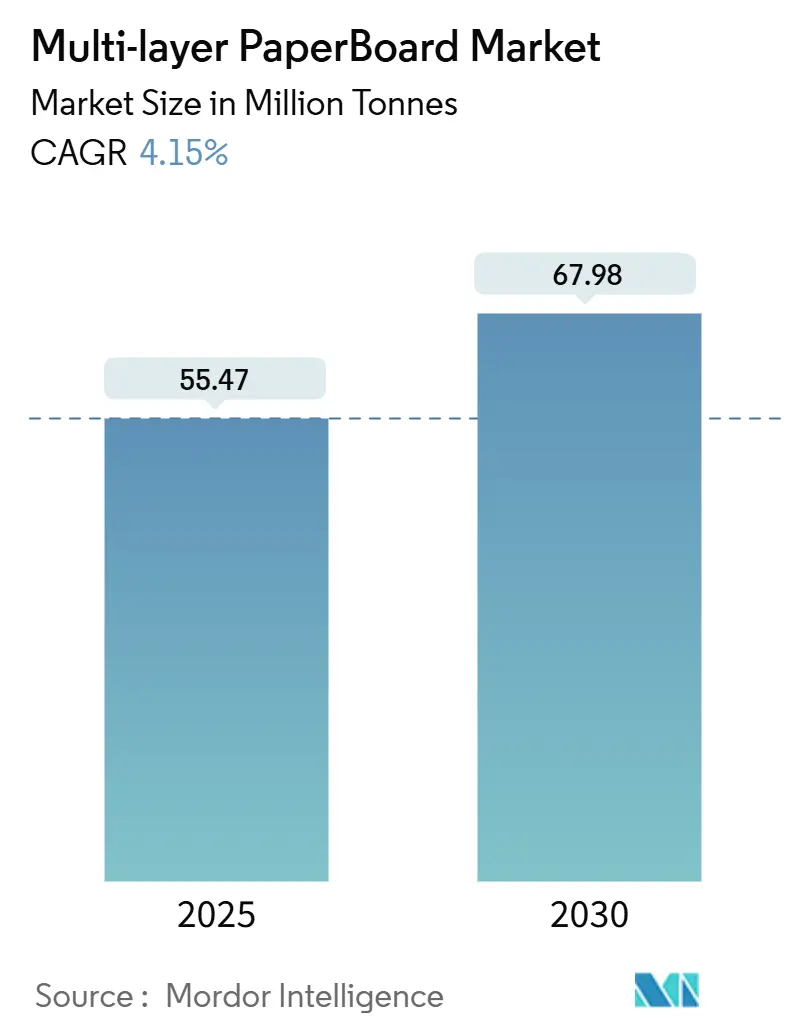

| Market Volume (2025) | 55.47 Million tonnes |

| Market Volume (2030) | 67.98 Million tonnes |

| Growth Rate (2025 - 2030) | 4.15% CAGR |

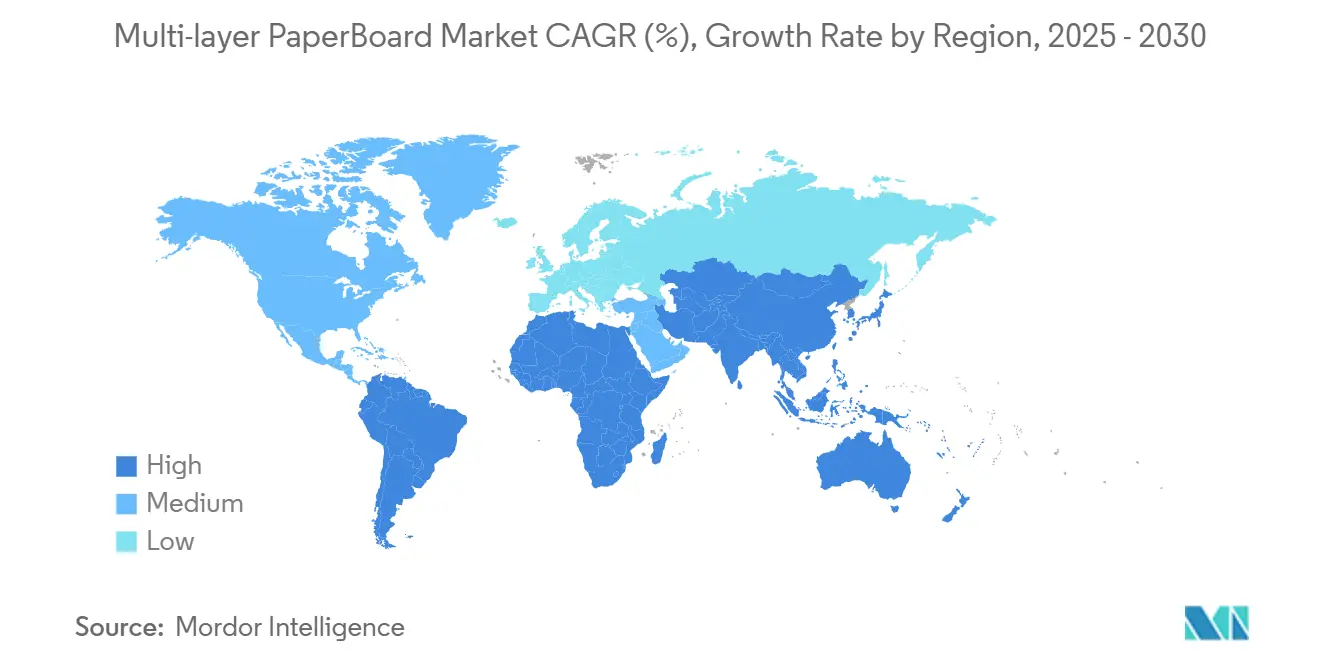

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

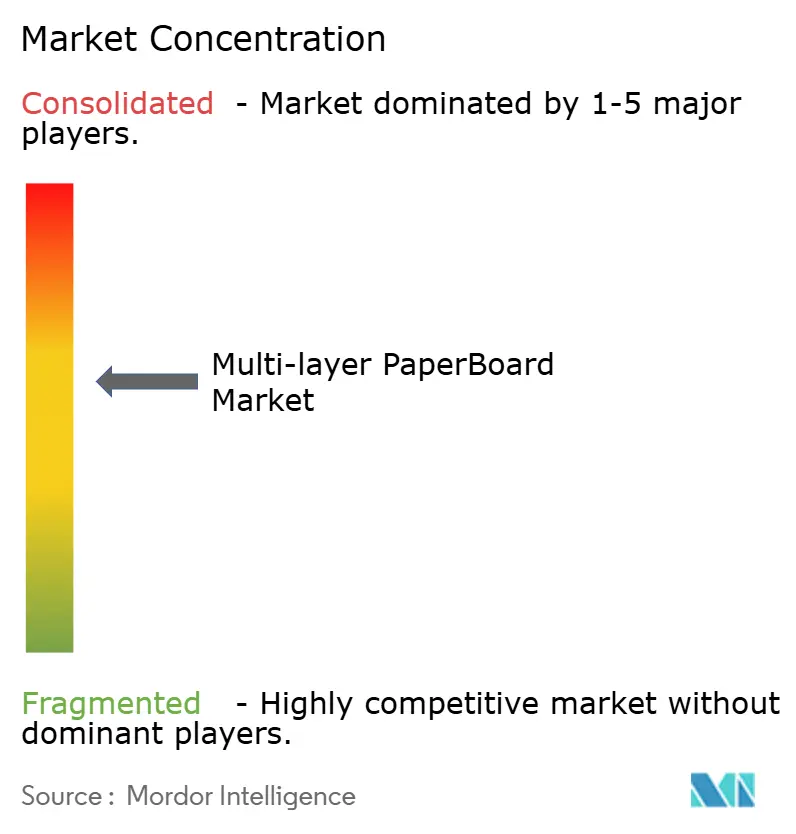

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi-layer Paperboard Market Analysis by Mordor Intelligence

The Multi-Layer Paperboard market size stood at 55.47 million tonnes in 2025 and is forecast to reach 67.98 million tonnes by 2030, expanding at a 4.15% CAGR. The upward trajectory reflects accelerating plastic substitution mandates, e-commerce packaging demand, and brand promises to phase out single-use plastics by 2030. Fiber-based solutions now capture share from rigid plastics in food, cosmetics, and pharmaceutical applications because they meet recyclability targets and resonate with consumers’ environmental concerns. Integrated producers benefit from surplus virgin-fiber capacity in Latin America that keeps input costs contained, while recycled-fiber grades gain traction under Extended Producer Responsibility (EPR) fee schedules rewarding circularity. Recent mergers, such as the Smurfit WestRock combination, further reshape competitive dynamics by pooling technology, pulp assets, and global converting footprints. At the same time, the PFAS phase-out has raised barrier-coating costs but opened a technology runway for cellulose-based alternatives that preserve grease resistance without fluorochemical. [1]U.S. Food and Drug Administration, “FDA, Industry Actions End Sales of PFAS Used in US Food Packaging,” fda.gov

Key Report Takeaways

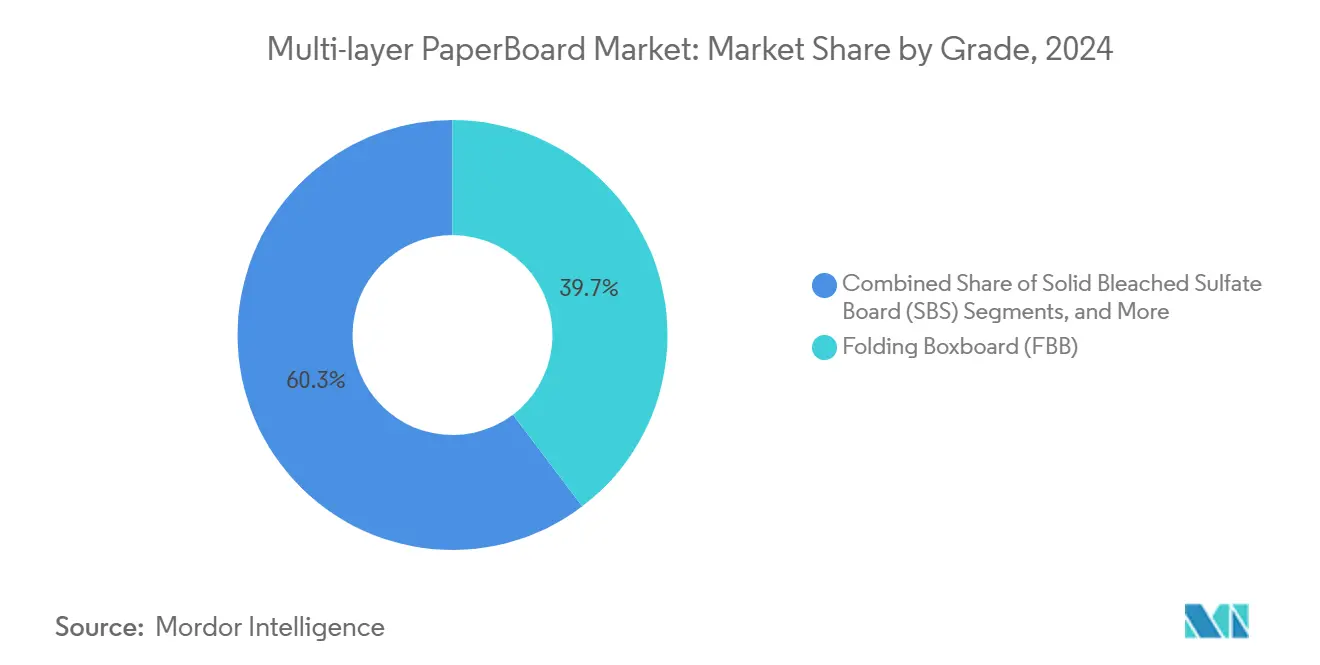

- By grade, Folding Boxboard led with 39.68% of the Multi-Layer Paperboard market share in 2024.

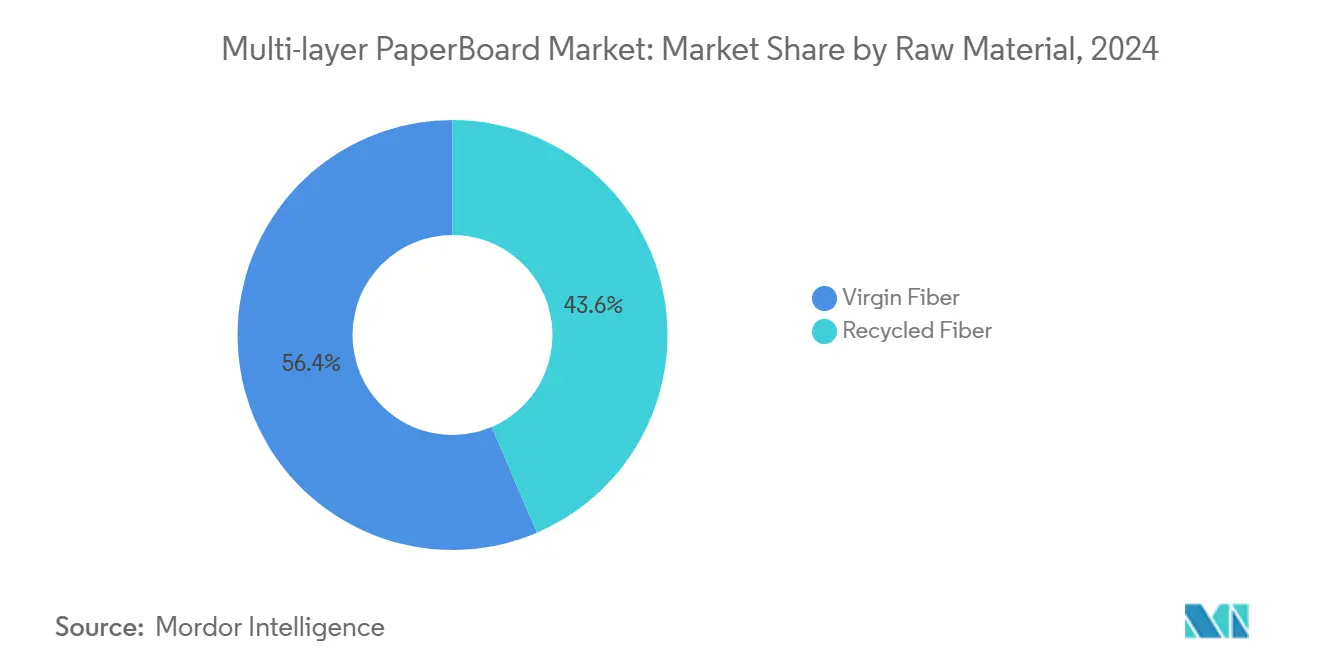

- By raw material, the Multi-Layer Paperboard market size for recycled fiber segment is projected to grow at a 5.52% CAGR between 2025-2030.

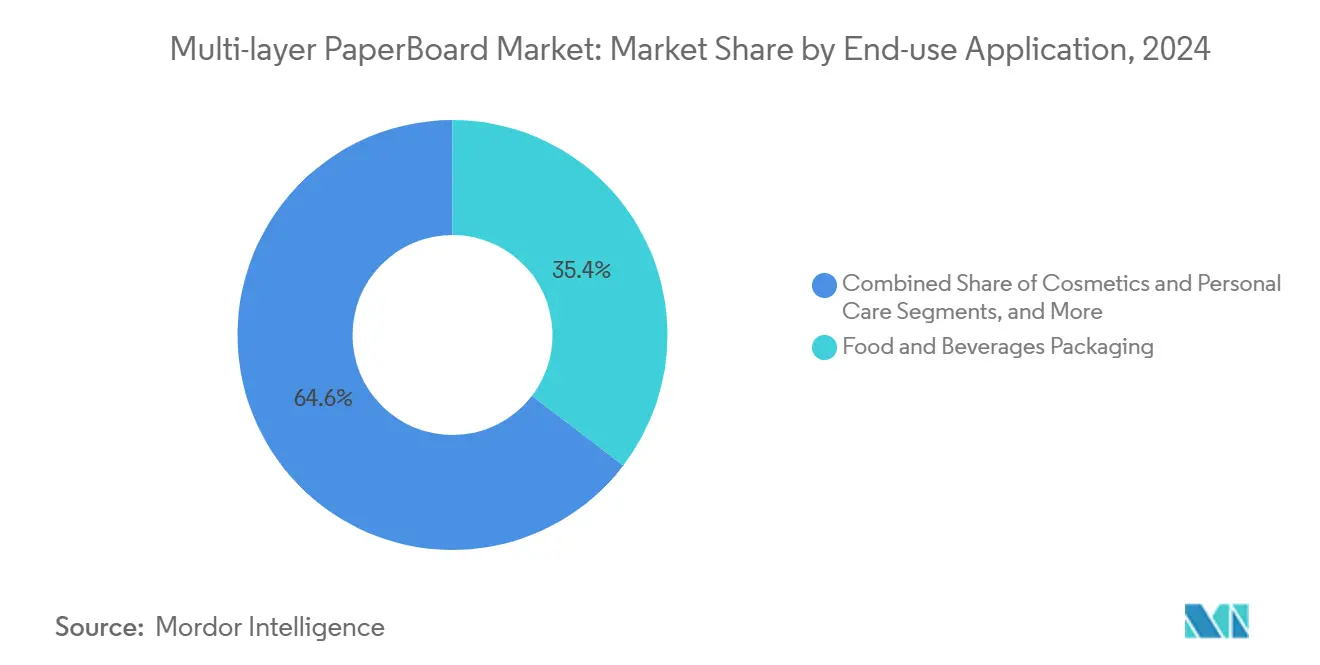

- By application, food and beverages captured 35.39% of the Multi-Layer Paperboard market share in 2024.

- By geography, the Multi-Layer Paperboard market size for Asia-Pacific region is projected to grow at a 5.37% CAGR between 2025-2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Multi-layer Paperboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce–led explosion in fiber-based secondary packaging | +1.2% | Global, concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Brand-owner plastics-substitution commitments (2030 targets) | +0.9% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Surplus virgin-fiber capacity in LATAM lowering input costs | +0.6% | LATAM core, spill-over to North America | Short term (≤ 2 years) |

| Lightweighting tech (micro-fibrillated cellulose layers) | +0.4% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Retail-ready multipacks for hard-to-recycle SKU sizes | +0.3% | North America and Europe | Medium term (2-4 years) |

| Extended Producer Responsibility (EPR) fees favoring fiber | +0.7% | Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce–led explosion in fiber-based secondary packaging

Global online retail continues to scale, and each parcel demands robust, printable secondary packaging. Amazon and other marketplaces specify heavier-basis paperboard that resists crush and moisture during multi-node shipping, accelerating demand for multi-ply constructions. International Paper’s Industrial Packaging segment recorded USD 15.6 billion sales in 2023, underscoring fiber’s central role in fulfilment networks. [2]International Paper Company, “2023 Annual Report,” internationalpaper.com Folding Boxboard and Solid Bleached Sulfate grades win share because they offer the print surfaces brands need for unboxing impressions. Capacity additions in North America lifted packaging paper output by 4.8% in 2023, mirroring e-commerce volume curves. Producers that can balance virgin and recycled furnish navigate Old Corrugated Container (OCC) volatility while trimming lead times for online sellers.

Brand-owner plastics-substitution commitments

Leading consumer-goods companies pledge that every retail pack will be recyclable or reusable by 2030, locking in long-term fiber demand. Graphic Packaging verified the elimination of 450 million plastic packs in 2023 alone, channeling that volume into recyclable paperboard. Procurement policies now prefer certified fiber even at price premiums, provided shelf appeal remains intact. WestRock disclosed that 97.8% of its 2024 portfolio already meets recyclability or compostability benchmarks, aligning with customers’ roadmaps. The voluntary goals sit atop a rising layer of EPR fees that penalize plastics, converting corporate vision statements into enforceable cost differentials.

Surplus virgin-fiber capacity in LATAM lowering input costs

Commissioning of Suzano’s Cerrado mill in 2024 injected 2.55 million tonnes of hardwood pulp into global trade flows, widening supply and tempering price spikes. Brazilian producers enjoy logistics upgrades that lower delivered fiber costs to North American and European board mills. Integrated LATAM players, such as Klabin, arbitrage between pulp exports and internal board conversion, giving them margin flexibility when OCC prices swing. Currency depreciation in the Brazilian real further reduces dollar-denominated input expense, though logistics inflation partially offsets this windfall.

Lightweighting tech (micro-fibrillated cellulose layers)

Micro-fibrillated cellulose (MFC) networks reinforce fiber bonds, allowing weight reductions without sacrificing stiffness. Nordic Pulp and Paper Research Journal found that a 4% MFC addition triples tensile strength, paving the way for grade down-gauging. Metsä Board’s micro-flute boxes illustrate commercial viability, cutting material use and carbon footprint while maintaining premium graphics. Early adopters lock in cost and sustainability gains, but installation of high-shear refiners and advanced control systems requires sizable capital, creating a barrier for smaller mills.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic OCC (old-corrugated-container) price volatility | -0.8% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Converting-line bottlenecks for >3-ply boards | -0.5% | Global, concentrated in high-volume facilities | Medium term (2-4 years) |

| PFAS phase-out raising barrier-coating costs | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Growing digitalisation cutting print and graphical board demand | -0.6% | Global, most pronounced in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic OCC price volatility

Recovered fiber costs often swing more than 40% within one quarter, complicating budgets for recycled-content grades. Supply tightness arises when export buyers absorb surplus containers, or when seasonal e-commerce surges elevate domestic demand. The Confederation of European Paper Industries reported a 7% drop in recycled-fiber consumption during 2023, underscoring destabilised feedstock flows. Integrated groups buffer volatility by dialing virgin-pulp ratios up or down, but mills dependent on secondary fiber face sharp EBITDA compression during spikes.

Converting-line bottlenecks for >3-ply boards

Producing four-or-five-ply structures requires precise headbox alignment and moisture balancing. Rayonier Advanced Materials runs North America’s sole multi-ply board machine at 180,000 tonnes per year, highlighting the limited installed base. [3]Rayonier Advanced Materials, “Form 10-K 2023,” ryam.com Retrofitting older assets demands high capital and prolonged downtime; ANDRITZ’s dedicated forming sections can solve the technical hurdle yet extend payback periods beyond midcycle earnings visibility. Where end-markets need thick, high-stiffness substrates, capacity constraints curb supply flexibility and elevate lead times.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Premium grades underpin revenue resilience

Folding Boxboard retained the largest 39.68% share of the Multi-Layer Paperboard market in 2024, serving fast-moving consumer goods that reward print clarity and moderate rigidity. The segment benefits from e-commerce’s need for attractive in-home presentation and from regulatory de-inking requirements that favor light-colored substrates. Solid Bleached Sulfate Board, though smaller, records the fastest 5.43% CAGR because luxury cosmetics and premium confectionery demand bright white surfaces free of recycled contaminants. Solid Unbleached Board and Coated Unbleached Kraft supply strength-critical packs for beverage carriers and DIY tools, but they trail premium grades in growth as brand owners elevate shelf aesthetics. Lightweighting enabled by MFC further differentiates premium offerings, allowing down-gauging while upholding edge crush ratings. Producers with in-house coating lines for retortable or heat-seal barriers monetize higher conversion margins, especially when aligned with pharmaceutical audits that certify low extractables.

By Raw Material Source: Circularity fuels recycled-fiber uptake

Virgin fiber still commands 56.42% of 2024 volume because food contact protocols restrict recycled inputs and because high-spec cosmetics require color consistency. LATAM pulp expansions suppress cost and secure long supply contracts, underpinning virgin-based operations. Nevertheless, recycled fiber posts the sharper 5.52% CAGR as EPR schedules introduce fee parity advantages and as mills install contaminant-removal stages that raise brightness ceilings. Hybrid furnish models pair outer virgin plies with recycled middles, producing a cooled cost curve without breaching food-contact thresholds. When OCC prices retreat, recycled-centric machines recover margin swiftly, but sustained price rallies expose their vulnerability, reinforcing the importance of dual-pulp sourcing strategies.

By End-use Application: Healthcare packaging outpaces baseline growth

Food and beverages held a 35.39% slice of 2024 Multi-Layer Paperboard market size thanks to everyday consumption and stricter bans on expanded polystyrene trays. Barrier-coated Folding Boxboard replaces plastic in cereal liners and frozen entrées, extending shelf life while meeting recyclability claims. Pharmaceutical packaging accelerates at 5.14% CAGR because aging populations in the United States, Europe, and Japan raise prescription volumes, and emerging economies broaden drug-dispensing infrastructure. Carton serialization mandates also call for sturdier substrates capable of holding tamper-evident features. Cosmetics trade up to premium virgin grades to meet brand identity criteria, while household goods leverage multipack formats that combine logistics efficiency and eye-level marketing.

Geography Analysis

Asia-Pacific generated the lion’s 43.15% share in 2024, led by China’s packaging boom and India’s blister-pack growth in generics manufacturing. Regional expansion at 5.37% CAGR stems from climbing disposable incomes and relocation of electronics assembly lines, both driving inner cartons and retail-ready outers. North America, although mature, enjoys steady uplift from omnichannel retail, with quick-commerce players demanding cushioning and return-ready designs. European demand grows more modestly as energy-price pressure hampers mill economics, yet the continent anchors regulatory innovation, adopting EPR and PFAS curves that later migrate worldwide. South American mills leverage hardwood eucalyptus cost advantages to feed both domestic FMCG and export linkages into the United States. Middle East and Africa represent nascent nodes, where infrastructure spend and population growth raise per-capita packaging usage from a low base; global majors increasingly partner with local converters to navigate complex import tariffs.

Competitive Landscape

Industry consolidation has shifted bargaining power toward vertically integrated giants. The USD 34 billion Smurfit WestRock group targets USD 400 million in annual synergies by pooling pulp, energy, and logistics footprints. International Paper’s USD 7.3 billion pickup of DS Smith opens European kraft-liner assets to North American virgin fluting, broadening grade diversity and cross-selling opportunities. Mondi’s EUR 1.2 billion (USD 1.40 billion) organic program adds semi-chem fluting and barrier-coated FBB lines to close regional supply gaps while lifting renewable-energy share. Technology barriers around MFC, multi-ply headboxes, and PFAS-replacement coatings reward R&D-heavy incumbents; smaller independents pivot to niche runs or toll-converting. Brand audits increasingly weigh Scope 3 emissions, advantaging mills with bio-energy boilers and on-site recycling loops. Negotiations over long-term offtake contracts now bundle carbon-footprint data and recyclability scores alongside traditional price and volume clauses.

Multi-layer Paperboard Industry Leaders

International Paper Company

Smurfit Westrock plc

Mondi plc

Graphic Packaging Holding Co.

Metsä Board Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Smurfit WestRock reported USD 7.5 billion combined 2024 net sales and USD 319 million net income, delivering integration synergies ahead of schedule.

- February 2025: International Paper closed the USD 7.3 billion acquisition of DS Smith, creating a USD 25 billion revenue platform across North America and Europe.

- January 2025: Stora Enso started up a EUR 1 billion (USD 1.17 billion) consumer board line in Oulu, Finland, targeting 450,000 tonnes annual capacity for premium food packs.

- December 2024: Graphic Packaging commissioned a USD 950 million recycled-paperboard mill in Waco, Texas, adding 400,000 tonnes to its coated recycled board network.

Global Multi-layer Paperboard Market Report Scope

| Folding Boxboard (FBB) |

| Solid Bleached Sulfate Board (SBS) |

| Coated Unbleached Kraft (CUK) |

| White-lined Chipboard (WLC) |

| Solid Unbleached Board (SUB) |

| Virgin Fiber |

| Recycled Fiber |

| Food and Beverages Packaging |

| Cosmetics and Personal Care |

| Pharmaceuticals |

| Household and Consumer Goods |

| Industrial and Electronics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Grade | Folding Boxboard (FBB) | ||

| Solid Bleached Sulfate Board (SBS) | |||

| Coated Unbleached Kraft (CUK) | |||

| White-lined Chipboard (WLC) | |||

| Solid Unbleached Board (SUB) | |||

| By Raw Material Source | Virgin Fiber | ||

| Recycled Fiber | |||

| By End-use Application | Food and Beverages Packaging | ||

| Cosmetics and Personal Care | |||

| Pharmaceuticals | |||

| Household and Consumer Goods | |||

| Industrial and Electronics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Indonesia | |||

| Thailand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected demand for Multi-Layer Paperboard by 2030?

Consumption is forecast to reach 67.98 million tonnes in 2030, reflecting a 4.15% CAGR from the 2025 base.

Which grades capture the most value in premium packaging?

Folding Boxboard delivers the largest volume, while Solid Bleached Sulfate Board records the highest growth in luxury food and cosmetics cartons.

How do Extended Producer Responsibility fees influence material choices?

Fee schedules in the United Kingdom, Denmark, and other early-adopter markets place lower charges on recyclable paperboard than on plastics, steering brand owners toward fiber packs.

Why is Asia-Pacific pivotal to future expansion?

The region contributes 43.15% of current demand and grows faster than any other territory, driven by Chinese e-commerce, Indian pharma exports, and Southeast Asian consumer-goods output.

How has the PFAS ban affected board production costs?

Eliminating PFAS raised barrier-coating expenses by 15-25%, but it has also accelerated investment in cellulose-based solutions that keep fiber competitive for grease-resistant food wraps.

Page last updated on: