Bird Food Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

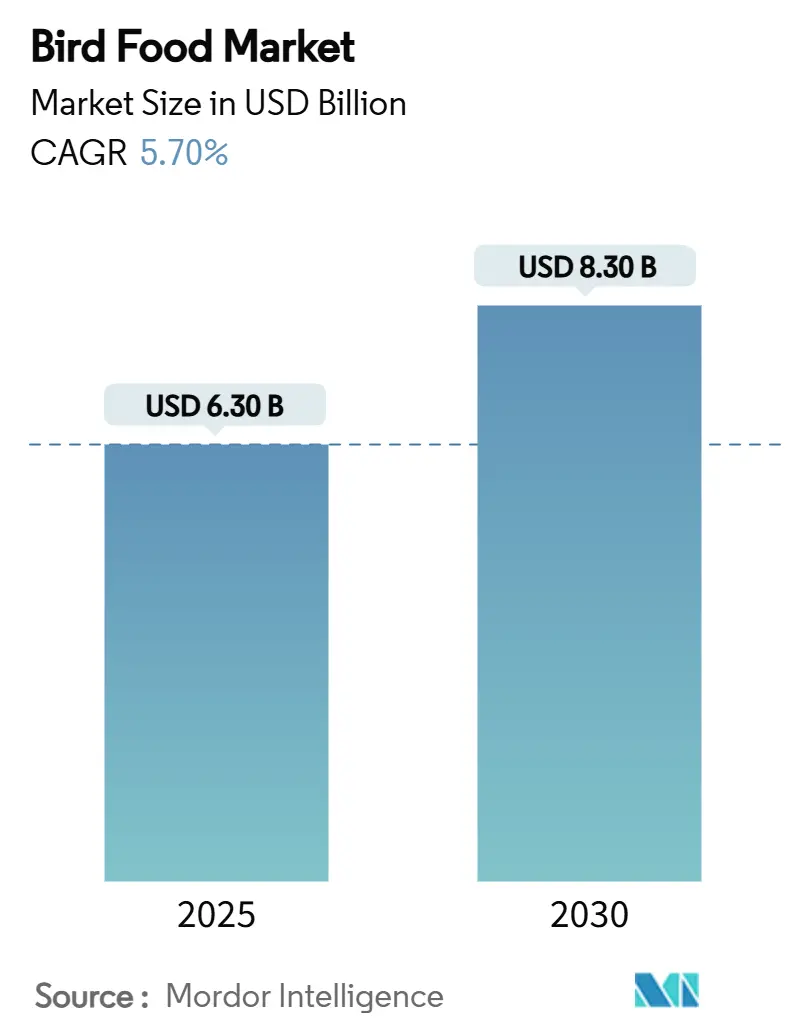

| Market Size (2025) | USD 6.30 Billion |

| Market Size (2030) | USD 8.30 Billion |

| Growth Rate (2025 - 2030) | 5.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bird Food Market Analysis by Mordor Intelligence

The bird food market size stands at USD 6.3 billion in 2025 and is forecast to reach USD 8.3 billion by 2030, advancing at a 5.7% CAGR through the period. Robust demand stems from two intertwined forces, including a rebound in pet bird ownership among younger urban households and the surge in wild-bird feeding, a hobby that now involves 96 million Americans who collectively spend USD 107.6 billion each year on bird-related activities[1]Source: U.S. Fish and Wildlife Service, “Birding in the United States: A Demographic and Economic Analysis,” fws.gov. Regulatory approval of insect protein for feed, rising online penetration, and premiumization across both wild and companion segments add further momentum. Simultaneously, price instability for key seeds and recurring avian-influenza events inject cost uncertainty, prompting producers to diversify ingredient baskets and invest in supply-chain risk mitigation. In this environment, the bird food market rewards firms that couple flexible sourcing with digital engagement and transparent sustainability credentials.

Key Report Takeaways

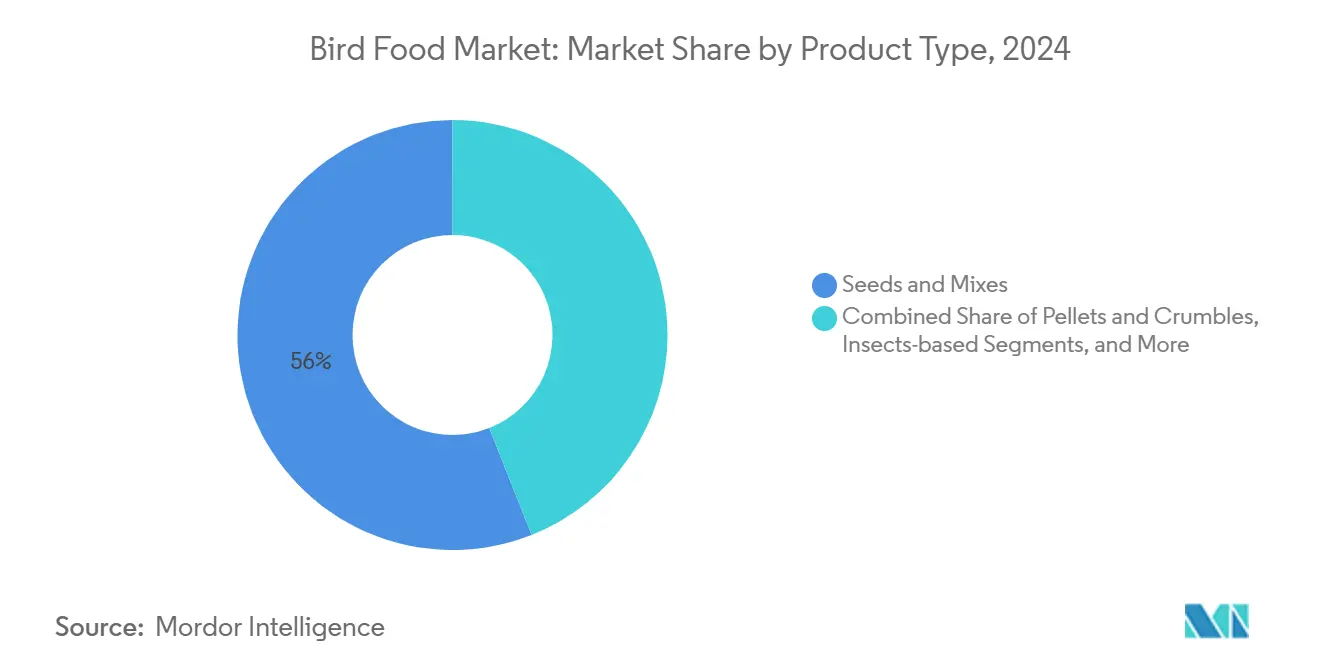

- By product type, seeds and mixes led with 56% of the bird food market share in 2024, while insect-based feed is projected to climb at a 10.8% CAGR through 2030.

- By bird category, wild birds accounted for 60% of the bird food market size in 2024, and pet and caged birds are set to expand at a 7.5% CAGR to 2030.

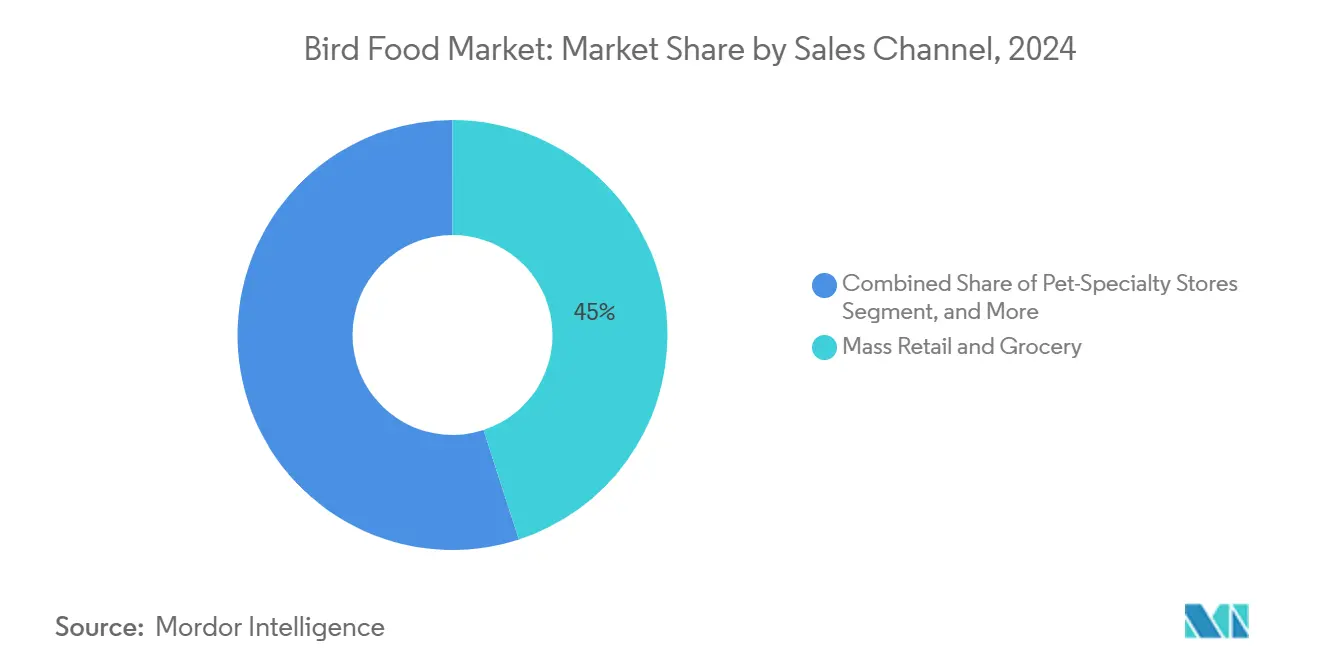

- By sales channel, mass retail and grocery held 45% revenue share in 2024, whereas online retailer sales are growing at 11.8% CAGR.

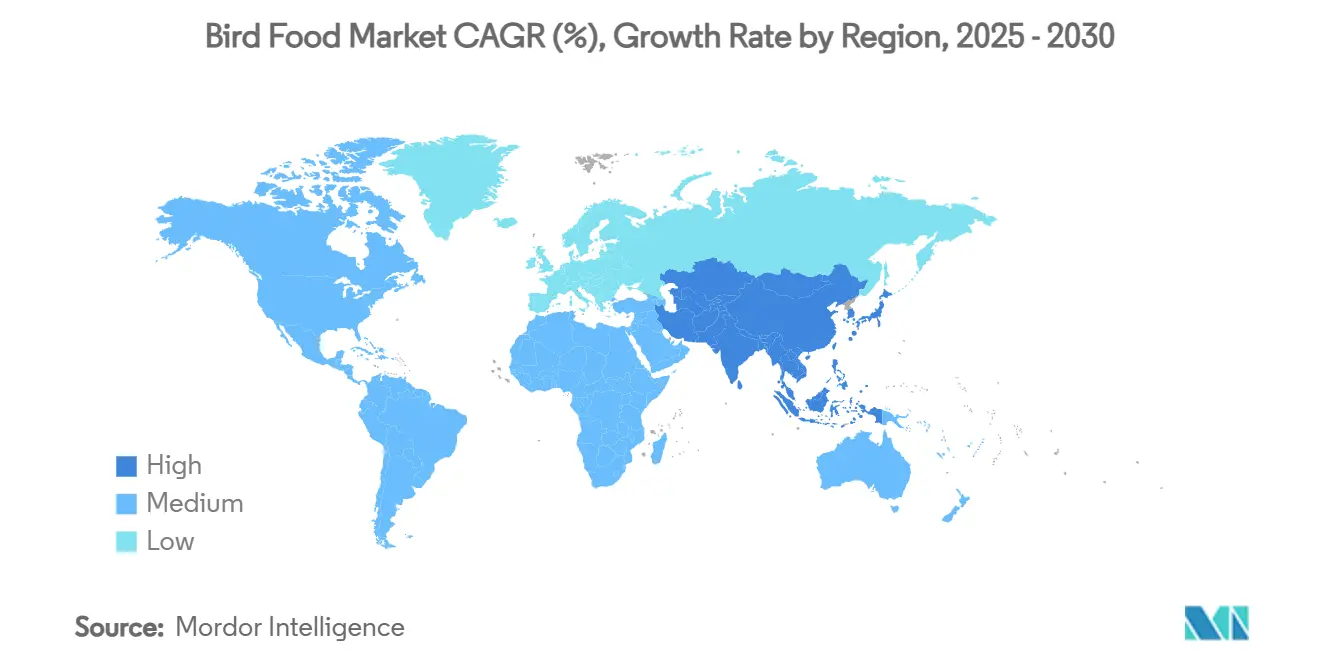

- By geography, North America dominated with the largest share 43% in 2024, while Asia-Pacific is the fastest-growing geography at a 7.1% CAGR through 2030.

- The top five companies captured 64.5% share of the bird food market in 2025.

Global Bird Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global ownership of pet and companion birds | +1.2% | North America and Asia-Pacific | Medium term (2-4 years) |

| Increasing popularity of wild-bird feeding as a hobby | +1.5% | North America and Europe | Long term (≥4 years) |

| Premiumization and human-grade trend in pet nutrition | +0.8% | North America andEurope | Medium term (2-4 years) |

| Rapid growth of online and DTC sales channels | +0.9% | Developed markets | Short term (≤2 years) |

| Regulatory green-light for insect protein in bird feed | +0.4% | Europe and North America | Long term (≥4 years) |

| Climate-resilient specialty seeds entering bird-food supply | +0.3% | Drought-prone regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Global Ownership of Pet and Companion Birds

Gen Z and millennial households are rediscovering birds as affordable, space-saving pets, pushing United States pet bird ownership to 12.6 million animals across 4.6 million homes and lifting global demand for formulated diets that prevent selective feeding. Two-thirds of these younger owners now prioritize nutrition quality over price, favoring pelleted blends fortified with vitamins and probiotics. The shift widens the addressable bird food market by introducing specialty lines for exotic species and racing pigeons. Brands that pair educational content with subscription replenishment are converting first-time buyers into repeat purchasers. Retailers also see higher basket sizes as owners add treats, supplements, and enrichment accessories alongside core feed.

Increasing Popularity of Wild-Bird Feeding as a Hobby

Backyard birding transformed from a niche pastime into a USD 107.6 billion economic engine that supports 1.4 million United States jobs. Pandemic-era participation spikes, 11% of current feeders joined during COVID-19, have not faded. Also, many households now view bird feeding as a permanent wellness routine. Ecotourism adds a USD 41 billion revenue stream that cross-pollinates with retail demand for high-energy seed cakes, suet, and habitat products. The hobby’s universal appeal spans age and gender cohorts, insulating the bird food market from narrow demographic risk. To capture this resilient spend, manufacturers are introducing season-specific blends that address breeding, molting, and migration needs.

Premiumization And Human-Grade Trend in Pet Nutrition

The humanization wave sweeping pet care is reshaping bird menus. Owners seek organic, non-GMO, and even human-grade ingredients, mirroring premium dog and cat diets. Online portals, which account for over half of pet product searches, amplify this preference by offering ingredient transparency and influencer reviews. Formulated pellets fortified with omega-3s and antioxidants now outpace plain seeds in specialty stores. European clearance of insect protein opens an ultra-premium tier that commands price premiums while reducing environmental footprints[2]Source: European Commission, “Commission Implementing Regulation on Tenebrio molitor,” ec.europa.eu. Packaging follows suit, with resealable pouches and recycled paper bags replacing single-use plastic.

Rapid Growth of Online and DTC Sales Channels

E-commerce is on track to represent 42% of all United States pet retail by 2028, powered by auto-ship models that lock in predictable demand. Direct-to-consumer start-ups leverage social media to reach pigeon fanciers and exotic-bird owners underserved by mass retail. Subscription cadence data helps companies adjust formulas based on seasonal shifts and feedback loops, shortening innovation cycles. Large incumbents respond with omnichannel strategies, and Mars Petcare’s USD 1 billion technology investment aims to double digital revenue by 2030. The race for online visibility is reshaping promotional budgets and favoring brands with search-optimized content and robust fulfillment networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices for key grain and oil-seed inputs | −1.1% | Global | Short term (≤2 years) |

| Avian-influenza led trade disruptions in feed supply | −0.7% | Outbreak regions | Medium term (2-4 years) |

| Bans on invasive seed species in certain export markets | −0.3% | Selected corridors | Medium term (2-4 years) |

| Consumer pushback on single-use plastic packaging | −0.4% | Europe, and North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices for Key Grain and Oil-Seed Inputs

Sunflower seed prices swung between USD 0.48 and USD 2.35 per kg in recent months, while millet slid 10.42% to USD 3.61 per bushel in 2024, squeezing manufacturer margins[3]Source: U.S. Department of Agriculture, “Grain and Oilseed Outlook 2025,” usda.gov. Weather shocks, biofuel demand, and shipping bottlenecks amplify these swings. Public producers like Central Garden and Pet warn that commodity costs remain the primary determinant of quarterly gross margin performance. To cope, companies hedge futures, adopt flexible formulations, and lock volume contracts with growers, yet such tactics add financial complexity. High interest rates further inflate inventory-carrying expenses, challenging working-capital management.

Avian-Influenza Led Trade Disruptions in Feed Supply

In February 2025, the United States Department of Agriculture (USDA) earmarked USD 1.8 billion to combat highly pathogenic avian influenza after outbreaks in British Columbia and Alberta triggered import restrictions on Canadian poultry products[4]Source: USDA APHIS, “Avian Influenza Response Update,” aphis.usda.gov. Beyond poultry, quarantine zones limit regional bird feeding and disrupt ingredient flows like egg products used in premium pellets. The Food and Drug Administration (FDA) has advised pet-food plants to tighten hazard plans against HPAI contamination, raising compliance costs [5]Source: U.S. Food and Drug Administration, “HPAI Guidance for Pet Food Facilities,” fda.gov. Racing pigeon circuits also face cross-border movement bans that affect feed demand in niche performance diets. These episodic yet severe shocks create planning uncertainty across the bird food market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Seeds Drive Volume While Insects Lead Innovation

Seeds and mixes generated 56% of the bird food market size in 2024 as sunflower, safflower, and millet remained staple ingredients for both backyard and companion birds. Within this flagship segment, sunflower alone accounts for a large share due to its high oil content and universal palatability. Price volatility in these commodities makes gross profits cyclical, yet high turnover and entrenched consumer familiarity sustain baseline demand. Producers differentiate through cleaning grades, regional sourcing stories, and blended ratios tailored to specific species, cementing seeds as the category workhorse.

Insect-based feed, while still niche, is climbing at a 10.8% CAGR through 2030. European regulatory approval has emboldened early adopters to showcase crickets, black soldier fly larvae, and mealworms as sustainable complete proteins. Single-serve pouches of dried mealworms command shelf premiums that offset higher raw costs, while pelleted hybrids add insect meal for balanced amino-acid profiles. Pellets and crumbles more broadly win converts among veterinarians who tout their role in curbing selective feeding and obesity. Fruits, nectar, and functional treats bolster seasonal demand, particularly for hummingbirds and parrots, underscoring the expanding sophistication of the bird food market.

By Bird Category: Wild Birds Dominate While Pet Segment Accelerates

Wild birds retained 60% of the bird food market share in 2024, lifted by 96 million United States participants who view feeding as recreation and citizen science. Seasonal promotions timed to migration peaks spur spikes in seed, suet, and high-energy cakes. Land-grant universities and conservation groups publish feeding guidelines that further normalize the practice. Because spending ties to outdoor leisure rather than household budgets, the segment proved resilient during economic downturns, stabilizing revenue visibility for retailers.

Pet and caged birds, however, deliver the fastest growth, expanding at a 7.5% CAGR. Gen Z renters favor budgies, cockatiels, and lovebirds for their low noise and modest space needs, stimulating demand for nutritionally complete pellets and enrichment snacks. Racing pigeons, though a small subset, purchase performance diets high in fat and electrolytes, pushing average selling prices upward. As avian veterinarians increasingly recommend fortified diets over seed-only regimens, household penetration of premium formats is set to climb, further enlarging the bird food market.

By Sales Channel: Mass Retail Leads While E-commerce Surges

Mass retail and grocery outlets commanded 45% of 2024 revenue by offering convenience and competitive pricing on commodity seeds. End-caps and seasonal garden displays tempt impulse buys during spring clean-up and holiday gifting seasons. Retailers secure private-label supply contracts that expand margins and lock shelf space, reinforcing the channel’s dominance. Yet foot-traffic shifts and SKU rationalization pressure brands to justify facings with data-driven sell-through.

Online retailers are growing at an 11.8% CAGR driven by the subscription replenishment and specialty assortment unreachable in brick-and-mortar. Automatic shipping guarantees uninterrupted feeding routines, and algorithmic recommendations drive cross-selling of feeders and health supplements. Pet specialty storefronts, with a 37% share, still serve as education hubs where staff guide owners toward species-specific formulas, blending experiential retail with premium price realization. Farm and feed stores remain vital in rural regions, but their growth lags as younger demographics pivot online.

Geography Analysis

North America holds a 43% share of the bird food market, propelled by a mature culture of backyard feeding, robust retail channels, and high discretionary income. The United States alone hosts 96 million bird watchers whose purchases contribute to USD 107.6 billion in annual economic output. Canada, while smaller, shows parallel enthusiasm, although recent avian influenza containment zones temporarily disrupted cross-border seed flows. North America is projected to grow as premium blends and insect proteins gain shelf space.

Asia-Pacific represents the fastest-expanding frontier, forecast to grow at 7.1% CAGR. Rising middle-class incomes, urban pet ownership, and e-commerce adoption across China, Japan, and Australia fuel the uptake of formulated diets. Cross-border online platforms reduce channel fragmentation, enabling United States and European specialty brands to tap demand with minimal physical infrastructure.

Europe maintains a measured 3.5% CAGR, underpinned by strict environmental standards and a sophisticated garden-center network. The continent leads globally in approving insect meal, granting local producers a regulatory head start that shields them from immediate global competition. Northern European consumers, historically quick to embrace sustainability claims, already pay premiums for low-carbon bird feed in recyclable kraft bags. In contrast, the Middle East and Africa, and South America exhibit moderate growth between 4.8% and 5.3%, constrained by lower disposable income and patchy retail infrastructure, yet long-term urbanization trends suggest gradual acceleration.

Competitive Landscape

The bird food market sits in a moderately consolidated state, with the top five suppliers controlling 64.5% of global revenue in 2025. Central Garden & Pet Co. is a prominent market player, leveraging integrated seed cleaning, extrusion, and nationwide distribution. The Scotts Miracle-Gro Company follows with a majority share. Also, Mars, Incorporated is another significant market player among the top three. This concentration affords purchasing scale advantages but still leaves room for regional specialists and innovative start-ups to carve profitable niches.

Competitive dynamics center on three pillars. First, vertical integration secures ingredient supply and protects margins from grain volatility. Cargill’s acquisition of feed mills in September 2024 in Denver and Kansas City exemplifies this move. Second, digital transformation reshapes customer acquisition. Mars, Incorporated Petcare’s USD 1 billion technology plan targets AI-driven product personalization and predictive inventory. Third, sustainability differentiates premium offerings, European firms champion insect protein and climate-resilient seeds, while U.S. brands pilot recyclable paper packaging at scale. Firms unable to articulate credible ESG narratives risk losing share to erosion among environmentally conscious buyers.

Private-label penetration continues to climb within big-box retail, pressuring branded margins but also expanding overall category volume. Meanwhile, online retailer challengers use agile contract manufacturing to test small-batch functional concepts, such as probiotic-fortified pellets, reducing time-to-market from years to months. Strategic collaborations with conservation groups bolster authenticity and grant access to bird-watcher communities that sway peer purchasing. Given these forces, the bird food market favors players balancing cost discipline with innovation.

Bird Food Industry Leaders

Central Garden & Pet Co.

The Scotts Miracle-Gro Company

Spectrum Brands Holdings Inc.

Versele-Laga NV

Mars, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: European Commission authorized UV-treated powder of whole Tenebrio molitor larvae as a novel food, granting Nutri’Earth five-year exclusivity.

- January 2025: JBT Corporation acquired Marel and Wenger Manufacturing, expanding extrusion capabilities for high-density bird pellets.

- November 2024: General Mills purchased Whitebridge Pet Brands for USD 1.45 billion, adding Tiki Pets and Cloud Star to its portfolio.

- September 2024: Cargill bought two feed mills from Compana Pet Brands, boosting capacity to serve specialty-feed makers.

Global Bird Food Market Report Scope

| Seeds and Mixes |

| Pellets and Crumbles |

| Insect-based Feed |

| Fruits, Nectar and Treats |

| Others (Calcium blocks, Grit, etc.) |

| Wild Birds |

| Pet/Caged Birds |

| Racing Pigeons |

| Pet-Specialty Stores |

| Mass Retail and Grocery |

| Farm and Feed Stores |

| Online Retailers |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| New Zealand | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Seeds and Mixes | |

| Pellets and Crumbles | ||

| Insect-based Feed | ||

| Fruits, Nectar and Treats | ||

| Others (Calcium blocks, Grit, etc.) | ||

| By Bird Category | Wild Birds | |

| Pet/Caged Birds | ||

| Racing Pigeons | ||

| By Sales Channel | Pet-Specialty Stores | |

| Mass Retail and Grocery | ||

| Farm and Feed Stores | ||

| Online Retailers | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| New Zealand | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the bird food market?

The bird food market size is USD 6.3 billion in 2025 and is projected to reach USD 8.3 billion by 2030 at a 5.7% CAGR.

Which region leads the bird food market?

North America holds the largest share, anchored by a mature backyard feeding culture and strong retail infrastructure.

What is the fastest-growing product segment in the bird food market?

Insect-based feed lead growth with a forecast 10.8% CAGR through 2030, supported by recent regulatory approvals in Europe.

How significant is e-commerce for bird food sales?

Online and direct-to-consumer channels are expanding at 11.8% CAGR and are anticipated to capture 42% of U.S. pet retail sales by 2028.

Why are insect proteins gaining traction in bird food?

Insects provide complete amino acids, require less land and water than soy, and now benefit from regulatory clearance, making them attractive for premium and sustainable formulations.

How does avian influenza affect the bird food industry?

Outbreaks disrupt trade flows of poultry-derived ingredients, raise biosecurity costs, and can temporarily suppress regional demand, trimming the industry’s growth outlook.

Page last updated on: