Dry Pet Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

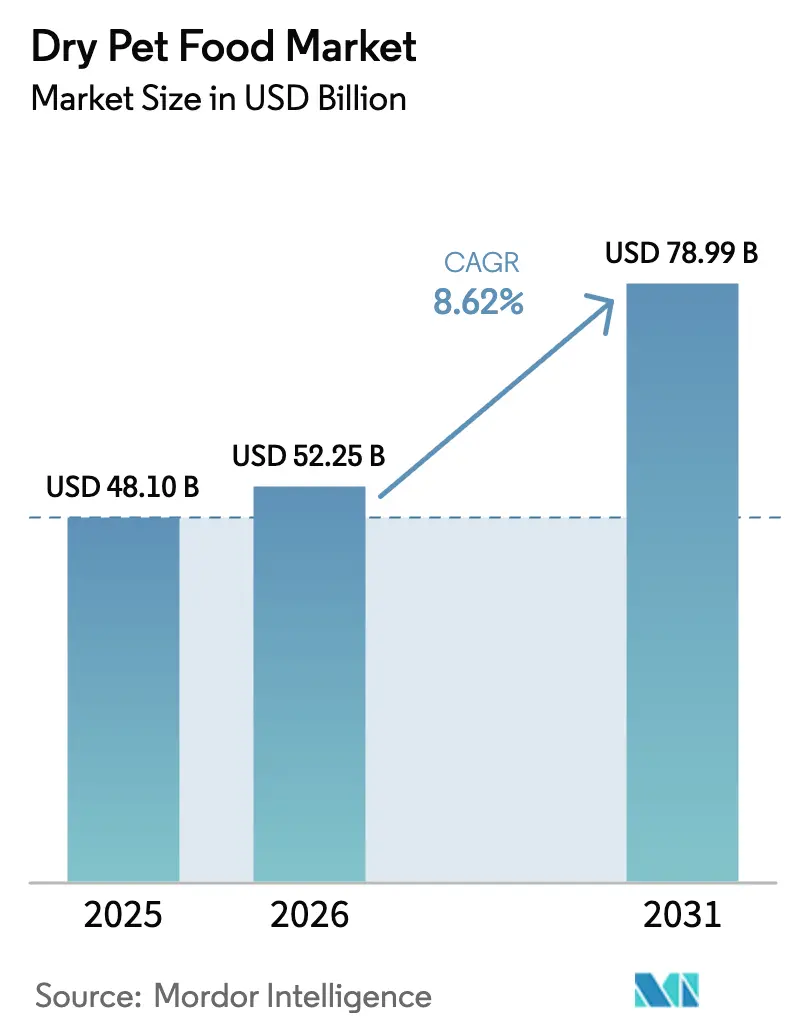

| Market Size (2026) | USD 52.25 Billion |

| Market Size (2031) | USD 78.99 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

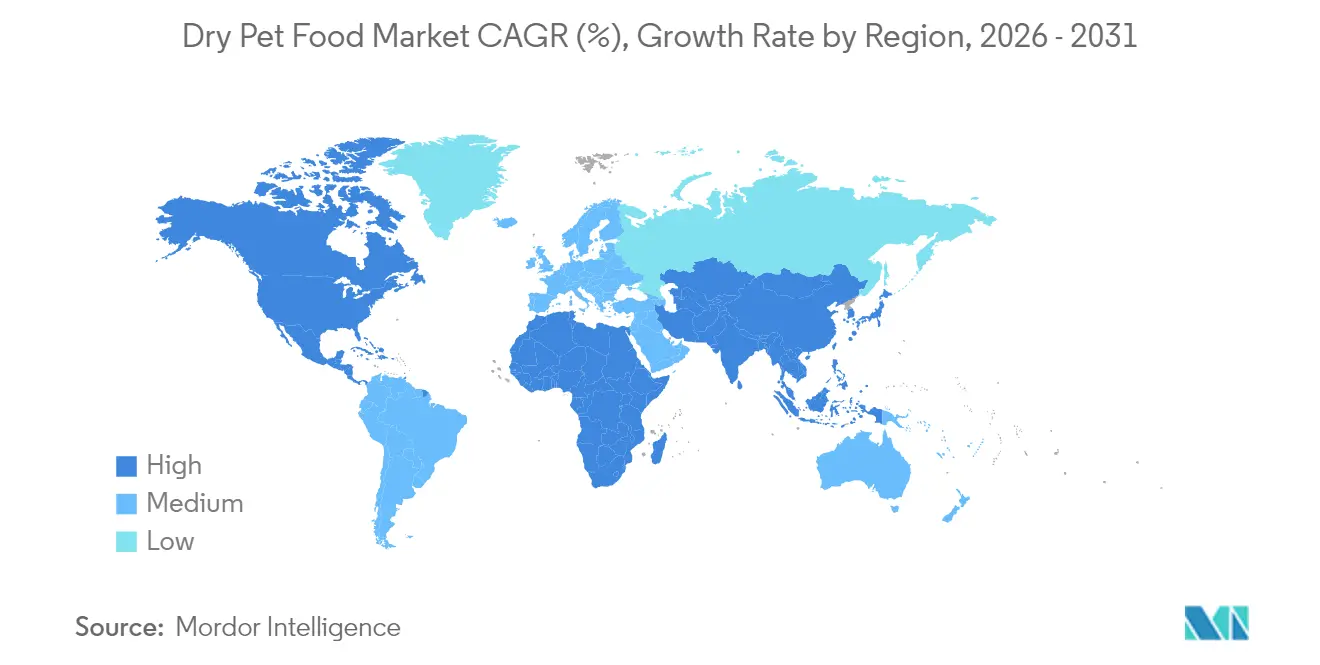

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dry Pet Food Market Analysis by Mordor Intelligence

The dry pet food market size is expected to grow from USD 48.10 billion in 2025 to USD 52.25 billion in 2026 and is forecast to reach USD 78.99 billion by 2031 at 8.62% CAGR over 2026-2031. The pet food industry is experiencing a significant transformation driven by changing consumer demographics and lifestyle patterns. Pet ownership has reached unprecedented levels across developed markets, with 66% of United States households owning a pet, which equates to 86.9 million households in 2023-2024. This surge in pet ownership has been particularly pronounced among millennials and urban professionals, who are increasingly viewing pets as integral family members. Premium functional diets, regulatory focus on nutritional accuracy, and alternative protein advances reinforce growth. Mars Inc. maintains category leadership while emerging direct-to-consumer brands push personalization technologies that elevate customer retention. Sustainability obligations on ingredients and packaging increase capital commitments, yet they also create product-differentiation opportunities for early movers. Online subscription models, freeze-dried entrants, and Asia-Pacific urbanization collectively accelerate revenue and margin expansion across the dry pet food market.

Key Report Takeaways

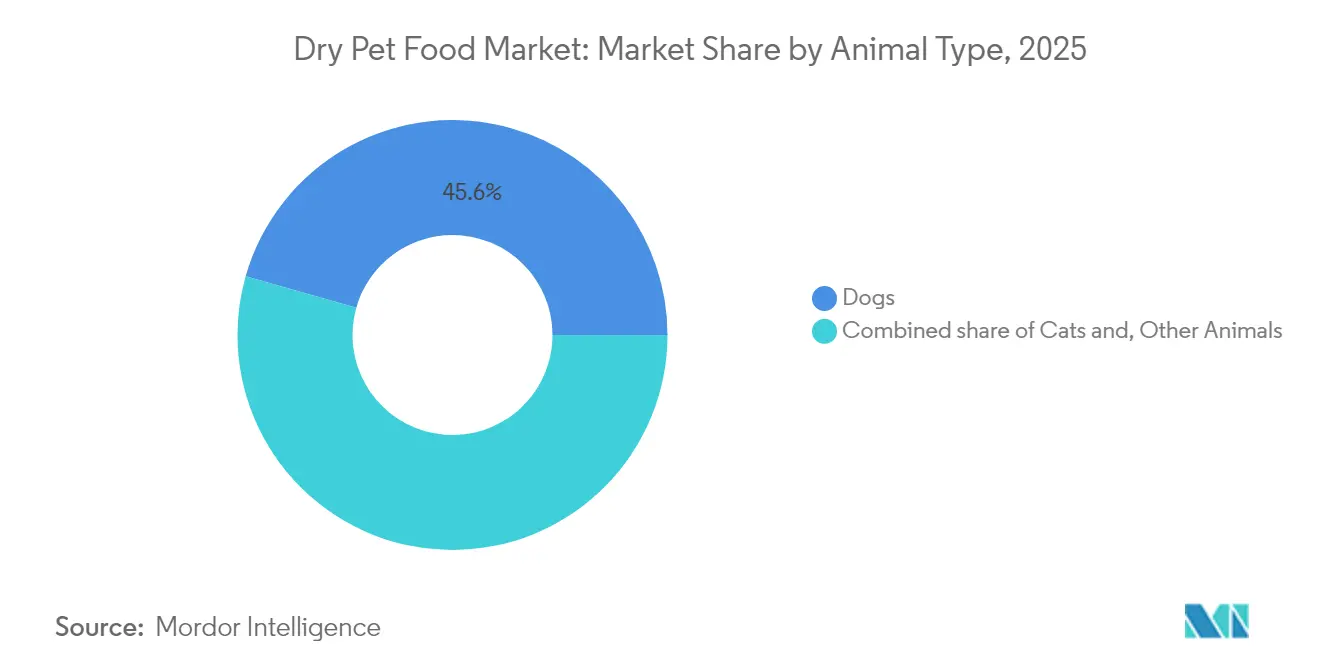

- By animal type, dogs led with 45.60% of the dry pet food market share in 2025, while cats are predicted to grow at a 7.45% CAGR through 2031.

- By product type, kibble held 57.20% of the dry pet food market size in 2025, while freeze-dried options are predicted to grow at a 9.25% CAGR through 2031.

- Cereals and cereal derivatives account for the largest share of ingredient types, at 51.40% in 2025, while protein ingredients are emerging as the fastest-growing segment, with a 6.55% CAGR through 2031.

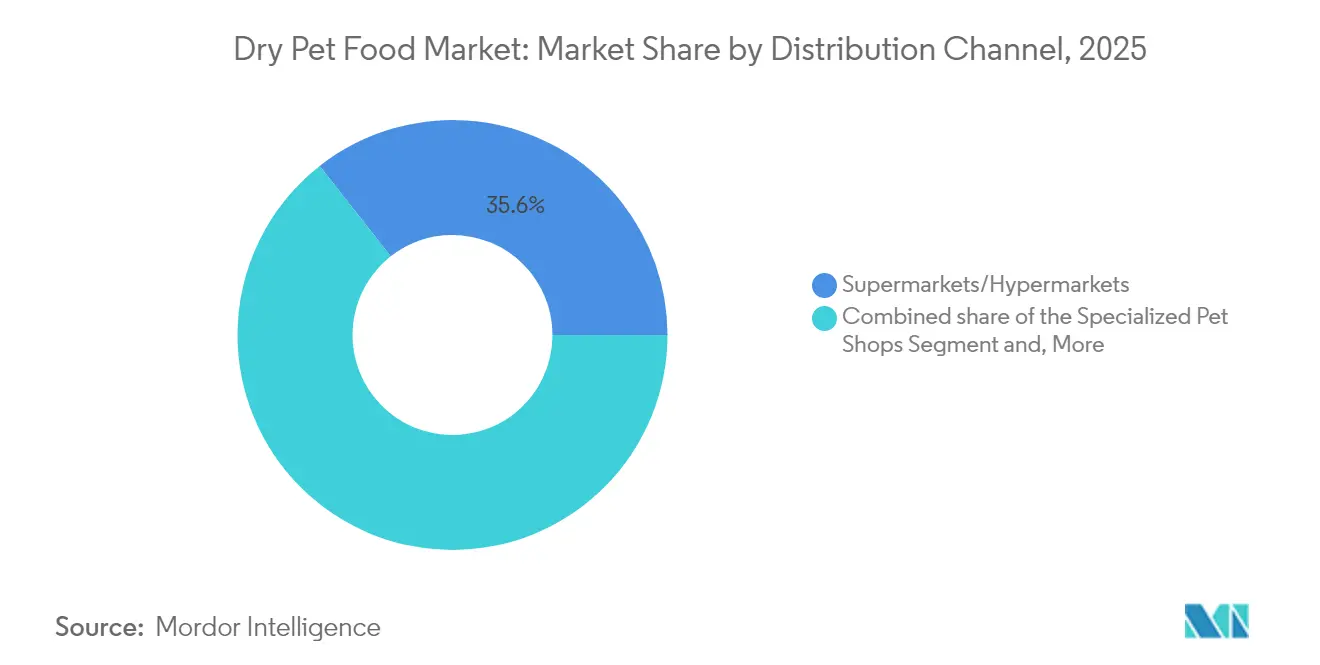

- By distribution channel, supermarkets/hypermarkets controlled a 35.60% market size in 2025, while online channels are predicted to grow at a 13.65% CAGR through 2031.

- North America held a 40.10% market share in the dry pet food market in 2025, while the Asia-Pacific region is projected to grow at an 7.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dry Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing trend of pet humanization | +1.2% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Growth of e-commerce and DTC models | +0.8% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Premiumization and functional nutrition demand | +0.6% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Accelerating urban single-pet households | +0.5% | Asia-Pacific core, spill-over to South America | Medium term (2-4 years) |

| Rise of clean-label and limited-ingredient diets | +0.4% | North America and Europe | Medium term (2-4 years) |

| AI-enabled personalization platforms | +0.3% | North America, selective European markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Trend of Pet Humanization

Pet humanization fundamentally reshapes purchasing decisions as owners increasingly view companions as family members requiring premium nutrition comparable to human food standards. This behavioral shift drives demand for organic, non-GMO, and human-grade ingredients, with pet parents willing to pay 25-30% premiums for products positioned as health-enhancing [1]Source: American Pet Products Association, “2023–2024 APPA National Pet Owners Survey,” americanpetproducts.org. The trend accelerates in developed markets where disposable income supports discretionary spending on pet wellness, creating opportunities for brands that successfully communicate functional benefits. Veterinary partnerships become crucial as humanization extends to preventive healthcare, with therapeutic diets gaining acceptance among owners seeking medical-grade nutrition solutions. The phenomenon particularly influences millennial and Gen Z demographics, who delay traditional life milestones while investing heavily in pet care, suggesting sustained long-term growth potential.

Growth of E-commerce and DTC Models

Digital commerce transformation accelerates as subscription-based models capture recurring revenue streams while reducing customer acquisition costs for manufacturers. Online channels grew 35% in 2024, with direct-to-consumer brands like Ollie and The Farmer's Dog leveraging personalization algorithms to create customized feeding plans. This shift enables smaller brands to bypass traditional retail gatekeepers and access consumers directly, intensifying competition for established players reliant on brick-and-mortar distribution. The convenience factor resonates particularly with urban professionals who value automated delivery schedules and portion-controlled packaging. The model requires significant investment in logistics infrastructure and customer service capabilities, creating barriers for companies without adequate digital transformation resources.

Premiumization and Functional Nutrition Demand

Functional nutrition emerges as a key differentiator as pet parents seek targeted health benefits beyond basic nutritional requirements. Products addressing specific conditions like joint health, digestive wellness, and cognitive function command premium pricing while building brand loyalty through perceived efficacy. The trend aligns with human health consciousness, where ingredients like probiotics, omega-3 fatty acids, and antioxidants translate from human supplements to pet formulations. Regulatory frameworks around functional claims create competitive moats for companies with clinical research capabilities and regulatory expertise. The premiumization wave particularly benefits established players with veterinary channel relationships, as therapeutic positioning requires professional endorsement and scientific validation.

Accelerating Urban Single-pet Households

Urbanization patterns in emerging markets drive single-pet household formation as space constraints and lifestyle factors favor individual companion ownership over multiple pets. This demographic shift creates demand for convenient, portion-controlled packaging and premium nutrition products as urban dwellers invest more per pet due to emotional attachment and higher disposable income. The trend particularly accelerates in Asia-Pacific metropolitan areas where Western pet-keeping practices gain adoption among affluent consumers. Single-pet households typically exhibit higher spending per animal and greater willingness to experiment with premium brands, creating opportunities for market share gains. The urbanization effect also drives demand for smaller packaging formats and subscription services that eliminate storage concerns in compact living spaces.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising raw-material and logistics costs | −0.7% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Stringent sustainability mandates on packaging | −0.4% | Europe and North America | Medium term (2-4 years) |

| Protein-sourcing volatility | −0.5% | Global, centered in protein-producing regions | Medium term (2-4 years) |

| Regulatory scrutiny on nutrient claims | −0.3% | North America, Europe, expanding Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Raw-material and Logistics Costs

Commodity price inflation creates margin pressure as key ingredients, including meat meals, grains, and functional additives, experience sustained cost increases. Livestock feed costs rose 15-20% in 2024, directly impacting protein ingredient pricing for pet food manufacturers who face difficult decisions between margin compression and consumer price increases [2]Source: U.S. Department of Agriculture, “Feed Grains Database,” usda.gov. Transportation costs compound the challenge as fuel price volatility and driver shortages increase distribution expenses, particularly affecting smaller regional players with limited logistics scale. The inflationary environment forces strategic decisions about ingredient sourcing, with some manufacturers exploring alternative protein sources or reformulating products to maintain price points.

Stringent Sustainability Mandates on Packaging

Environmental regulations increasingly target packaging materials as governments implement extended producer responsibility frameworks and plastic reduction mandates. European Union directives require recyclable packaging by 2025, forcing manufacturers to invest in alternative materials that often carry higher costs and technical challenges. The transition creates competitive dynamics as companies with early sustainability investments gain regulatory compliance advantages while others face catch-up costs. Consumer pressure reinforces regulatory requirements as environmentally conscious pet parents increasingly consider packaging sustainability in purchasing decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Dogs Drive Volume, Cats Accelerate Growth

Dogs generated 45.60% of the 2025 dry pet food market share, the largest slice of the dry pet food market, reflecting higher caloric intake due to body mass. The growth divergence between dogs and cats reflects demographic shifts in pet ownership patterns, with younger consumers increasingly favoring cats due to lifestyle compatibility and lower maintenance requirements. Therapeutic nutrition drives premium pricing in both segments, though cats show higher price sensitivity in mass-market channels. Innovation focuses on palatability enhancement for cats, whose selective eating behaviors create formulation challenges compared to dogs' broader acceptance of varied ingredients and textures.

Cats are projected to compound at 7.45% annually through 2031, driven by urban adoption patterns and increasing awareness of feline-specific nutritional requirements. In 2024, 32% of United States households owned a cat. The cat segment benefits from premiumization trends as owners recognize the importance of species-appropriate nutrition, particularly for indoor cats requiring specialized formulations to address hairball control and urinary health . Other animals, including small mammals and birds, represent niche opportunities with specialized nutritional needs but limited scale potential.

By Product Type: Kibble Dominance Faces Premium Disruption

Kibble accounted for 57.20% of the dry pet food market size in 2025, supported by cost efficiency and automated production scalability. As competition intensifies, major manufacturers acquire niche freeze-dry pioneers to secure technology know-how and shorten time to market. Premium pricing for freeze-dried formulas, often three times that of mid-market kibble, enhances gross margins and offsets smaller volumes. Brands reformulate kibble with probiotic coatings to convey functional benefits without leaving the mainstream price band. Packaging upgrades, such as resealable pouches, extend freshness and encourage bulk shopping. The diversification of processing methods broadens brand portfolios, cushioning exposure to any single consumer trend within the dry pet food market.

Freeze-dried SKUs, though smaller in volume, are forecast to achieve a 9.25% CAGR through 2031, as owners associate low-temperature processing with nutrient retention. Baked biscuits sustain demand in training and treat occasions but rarely serve as primary meals. Semi-moist products decline because shoppers scrutinize sugar and humectant content, reflecting clean-label priorities. Extruders now feature energy-recovery systems that lower operating costs and reduce emissions.

By Ingredient Type: Cereals Dominate, Proteins Accelerate

Cereals and cereal derivatives account for the largest share of ingredient types at 51.40% in 2025, reflecting the cost efficiency and palatability advantages they offer in mass-market formulations, despite narratives surrounding the grain-free trend. Cereal ingredients face ongoing scrutiny from grain-free advocates despite Association of American Feed Control Officials (AAFCO) nutritional adequacy validation and decades of safe use in commercial formulations. The regulatory compliance factors influence ingredient selection as manufacturers navigate complex approval processes for novel proteins while maintaining cost structures that support competitive pricing across distribution channels.

Protein ingredients, encompassing both animal-derived and plant-derived sources, are emerging as the fastest-growing segment at 6.55% CAGR through 2031, driven by premiumization trends and consumer preference for meat-first formulations. Novel protein sources, including insect-based and algae-based alternatives, gain regulatory approvals and consumer acceptance, with the European Food Safety Authority authorizing specific insect species for pet food applications in 2024. Functional additives including probiotics, omega-3 supplements, and joint-health compounds command premium pricing while building brand differentiation through targeted health benefits.

By Distribution Channel: Digital Transformation Accelerates

Supermarkets/hypermarkets retained 35.60% of the 2025 market share. The dry pet food market benefits from auto-ship discounts and AI-guided product recommendations that increase basket size. Specialized pet shops preserve a premium niche through staff expertise and curated assortments. Veterinary clinics, though lower in tonnage, deliver the highest unit prices owing to prescription diets. Rural feed stores maintain loyal patronage among multipet owners who value bulk economy.

While online platforms are registering a 13.65% CAGR through 2031, that is reshaping shopping norms. Digital penetration improves access for consumers in secondary cities, bridging assortment gaps left by physical retailers. E-commerce firms exploit data to launch house brands targeting price-sensitive shoppers, raising private-label penetration. Click-and-collect hybrids combine speed with convenience, suiting busy households. Real-time inventory visibility reduces out-of-stock incidents and fortifies retailer–supplier collaboration. Channel blurring continues as supermarkets develop in-house subscription programs to defend share against pure-play online competitors.

Geography Analysis

North America controlled 40.10% of the dry pet food market in 2025, as premiumization offsets category maturity. The United States remains the global spending leader, with subscription services and therapeutic formulas anchoring value growth. Canada benefits from cross-border e-commerce, while Mexico exhibits double-digit online uptake driven by mobile adoption and youthful demographics.

Asia-Pacific delivers the fastest trajectory at 7.95% CAGR through 2031, underpinned by rapid urbanization in China, India, and Southeast Asia. Disposable income gains fuel Western feeding practices, and single-pet households boost per-animal outlays. China is the largest contributor in absolute terms, whereas Japan and South Korea sustain higher average selling prices owing to entrenched premium segments. Regulatory coalitions across Asia-Pacific markets aim to harmonize labeling, enabling regional-scale efficiencies for multinationals.

Europe represented significant share in 2024 amid stringent environmental and safety regulations. Germany and the United Kingdom dominate the market in terms of volumes, while the Nordic countries are pioneers in insect-based adoption. Extended producer responsibility rules expedite recyclable packaging innovation. Strict health-claim substantiation standards elevate trust and set benchmarks emulated by other regions, reinforcing Europe’s status as a regulatory pacesetter in the dry pet food industry.

Competitive Landscape

The dry pet food market is characterized by intense innovation and strategic expansion activities among major players like Mars, Incorporated, Nestlé S.A., J.M. Smucker Company, Colgate-Palmolive Company, and General Mills Inc. The top five companies dominate global revenues, underscoring high market concentration, though emerging challengers continue to find niche opportunities. Companies are focusing on developing premium and specialized formulas that are grain-free, organic, promote oral health, and address the specific dietary needs of pets. Operational agility is demonstrated through investments in manufacturing facilities and supply chain optimization, enabling the meeting of growing demand. Strategic moves include partnerships with veterinary services, research institutions, and e-commerce platforms to strengthen market presence.

Companies are expanding their geographical footprint through new manufacturing facilities, particularly in emerging markets like India and Brazil, while also investing in sustainable production practices and innovative packaging solutions to meet evolving consumer preferences. Notably, leading pet food manufacturers like Mars Inc. are spearheading these initiatives. Strategic capital allocation favors capacity expansions near high-growth corridors. Mars invested USD 185 million to add freeze-dry lines in Illinois in 2024. Mergers and acquisitions accelerate as incumbents seek expertise in organic and sustainable formulations, illustrated by Nestle Purina’s USD 300 million purchase of Lily’s Kitchen. Technology investments target AI-driven personalization and supply-chain transparency, boosting customer retention and compliance confidence.

Private-label penetration intensifies in supermarket chains competing on price, pressuring branded volumes in mass channels. Nonetheless, strong intellectual property in functional additives and proprietary processing techniques shields leading products. Barriers for new entrants include clinical evidence costs, stringent labeling, and minimum efficient scale in distribution. The race for alternative proteins sees partnerships between pet food manufacturers and insect farms, signaling future battlegrounds for differentiation within the dry pet food market.

Dry Pet Food Industry Leaders

Nestlé S.A.

J.M. Smucker Company

Colgate-Palmolive Company

General Mills Inc.

Mars, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Mars, Incorporated expanded its US Royal Canin manufacturing operations by opening a 450,000-square-foot facility in Lewisburg, Ohio. The USD 450 million facility creates 270 new full-time positions within five years and produces dry pet food for 4 million pets annually. This expansion is part of Mars' USD 6 billion investment in US manufacturing operations over the past five years.

- April 2024: General Mills represented the sale of its European pet food operations to Affinity Petcare for USD 550 million, allowing the company to focus on its core North American Blue Buffalo brand while optimizing its global portfolio structure.

- February 2023: Mars Petcare, part of Mars Incorporated announced that it has completed its acquisition of Champion Petfoods a pioneer in the fast-growing premium pet food space, and its two premier brands, ORIJEN and ACANA. This acquisition enhances Mars Petcare's global portfolio, bolstering its offerings in pet nutrition products and health services.

Global Dry Pet Food Market Report Scope

Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. A dry diet, a biscuit diet, or a kibble diet is a processed pet food diet. The Dry Pet Food Market is segmented by Animal Type, Product Type, Ingredient Type, Distribution Channel, and Geography. The Animal Types are further segmented into Dogs and Cats. Product Types are further segmented into Kibble and Other Dry Pet Food. The Ingredient Types are further segmented into Protein, Cereal and Cereal Derivatives, and Other Ingredient Types. The Distribution Channels are further segmented into Specialized Pet Stores, Supermarkets/Hypermarkets, Online Channels, and Other Distribution Channels. The report is further segmented by Geography into North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The report offers the market size for all the above segments in terms of value (USD).

| Dogs |

| Cats |

| Other Animals |

| Kibble |

| Freeze-Dried |

| Others |

| Protein | Animal-derived |

| Plant-derived | |

| Cereals and Cereal Derivatives | |

| Others |

| Specialized Pet Shops |

| Supermarkets/Hypermarkets |

| Online Channels |

| Veterinary Clinics |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | Australia |

| China | |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Animal Type | Dogs | |

| Cats | ||

| Other Animals | ||

| By Product Type | Kibble | |

| Freeze-Dried | ||

| Others | ||

| By Ingredient Type | Protein | Animal-derived |

| Plant-derived | ||

| Cereals and Cereal Derivatives | ||

| Others | ||

| By Distribution Channel | Specialized Pet Shops | |

| Supermarkets/Hypermarkets | ||

| Online Channels | ||

| Veterinary Clinics | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | Australia | |

| China | ||

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the dry pet food market in 2026?

The dry pet food market size is USD 52.25 billion in 2026.

What is the projected growth rate for dry pet food through 2031?

The market is forecast to grow at a 8.62% CAGR, reaching USD 78.99 billion by 2031.

Which region is expanding the fastest for dry pet food?

Asia-Pacific is the fastest-growing region, registering an 7.95% CAGR through 2031.

Which product format is gaining share most quickly?

Freeze-dried dry pet food is recording a 9.25% CAGR due to premium positioning and convenience.

Page last updated on: