India Poultry Feed Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

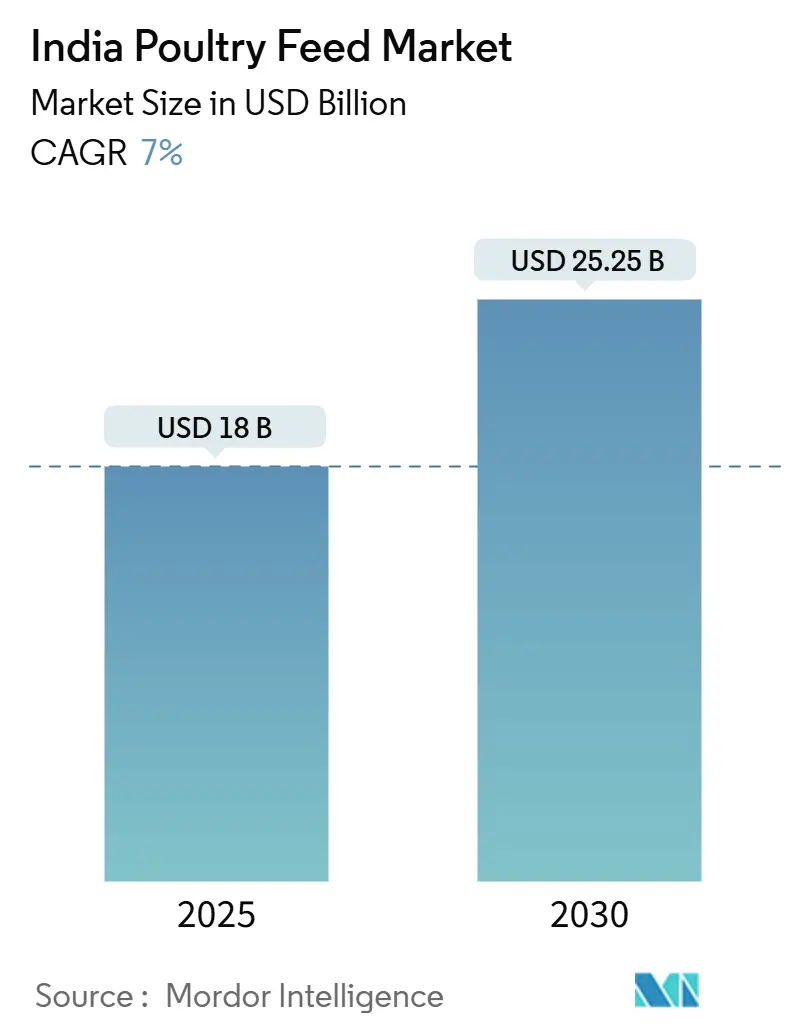

| Market Size (2025) | USD 18 Billion |

| Market Size (2030) | USD 25.25 Billion |

| Growth Rate (2025 - 2030) | 7.00% CAGR |

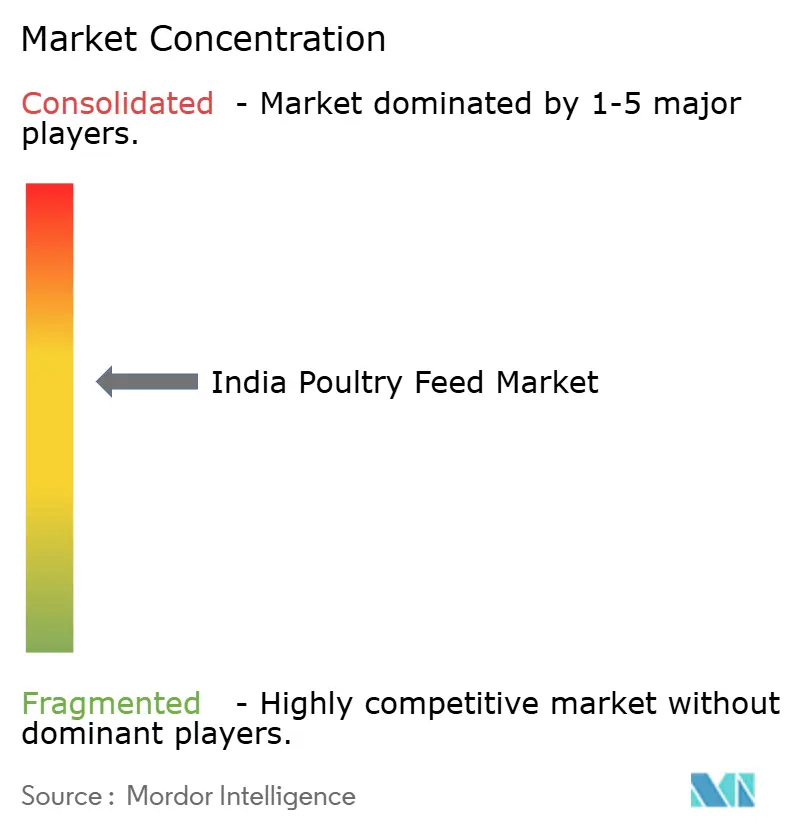

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Poultry Feed Market Analysis by Mordor Intelligence

The Indian poultry feed market size stood at USD 18.0 billion in 2025 and is projected to reach USD 25.25 billion by 2030, expanding at a 7.0% CAGR. Rising contract farming, sustained consumer demand for affordable animal protein, and continuous feed-processing upgrades are reinforcing volume growth even though feed inputs still account for a major share of production cost. The expansion of commercial broiler integration is creating structured purchasing cycles that stabilize demand for compound feed across organized clusters. Simultaneously, the widespread consumer preference for antibiotic-free chicken is accelerating the shift toward functional formulations that support bird health without the use of therapeutic drugs. Ingredient diversification into insect meal and Dried distillers' grain with solubles (DDGS) is easing pressure on traditional maize and soybean supplies, while pelleting technology improvements are lifting feed conversion efficiency. Strategic consolidation, particularly among top manufacturers pursuing feed-to-fork control, underpins competitive differentiation and capital allocation.

Key Report Takeaways

- By feed ingredient, maize accounted for a 46% share of the Indian poultry feed market size in 2024, while insect meal is poised for a 28% CAGR between 2025 and 2030.

- By additive type, Amino Acids commanded a 30% share of the Indian poultry feed market size in 2024, and enzymes are advancing at a 9.5% CAGR to 2030.

- By form, pellets commanded a 52% share of the Indian poultry feed market size in 2024 and are advancing at an 8.5% CAGR to 2030.

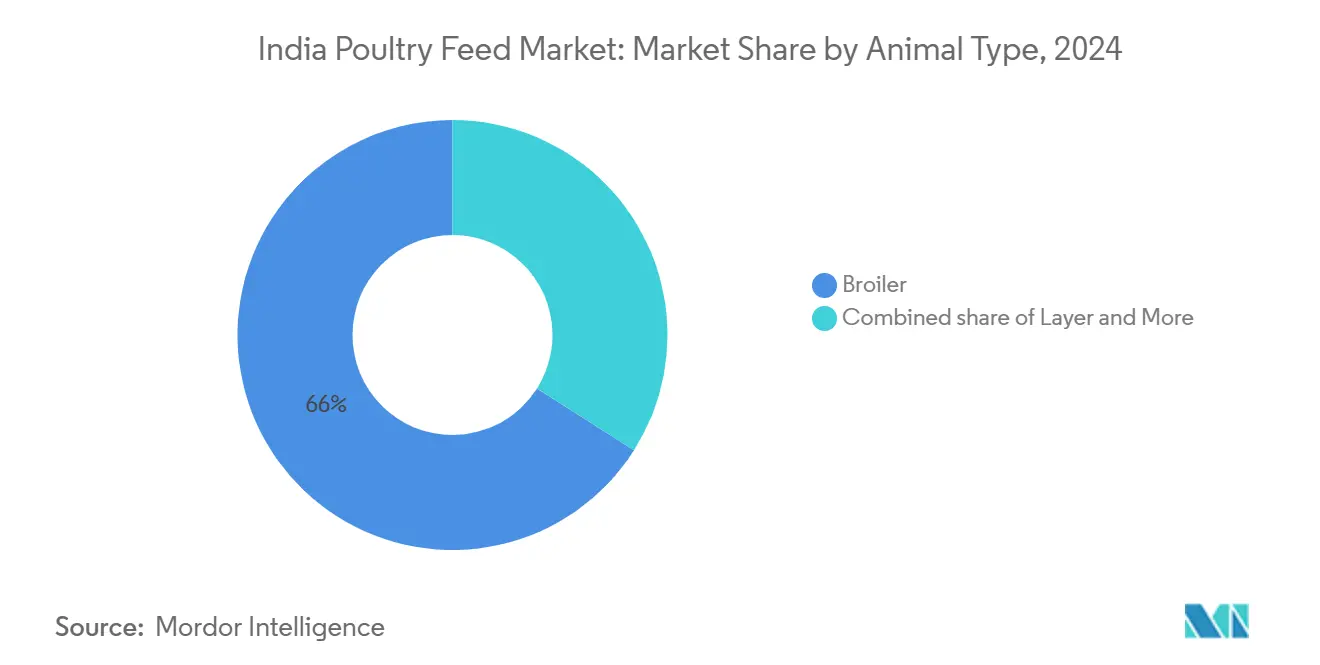

- By animal type, broiler feed led with 66% of India's poultry feed market share in 2024, and breeder feed is forecast to register the fastest 9.2% CAGR through 2030.

India Poultry Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating commercial broiler integration | +1.8% | National, dense in South and West India | Medium term (2-4 years) |

| Growing demand for antibiotic-free meat | +1.2% | Urban centers countrywide | Medium term (2-4 years) |

| Government subsidies on maize and soybean | +1.0% | National, strongest in producing states | Short term (≤2 years) |

| Expansion of organized retail cold chain | +0.8% | Metro and Tier-1 cities nationwide | Long term (≥4 years) |

| Surge in insect-protein inclusion | +0.6% | South India pilots, scaling nationally | Long term (≥4 years) |

| Adoption of AI-enabled precision feeding | +0.4% | Large commercial farms in progressive states | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Escalating Commercial Broiler Integration

Contract farming is realigning procurement as integrators internalize feed production to curb volatility. Companies such as Suguna Foods and Venky's India operate captive mills that match flock genetics with customized micromixes, improving feed conversion ratios and reducing wastage. Typical farm capacity has shifted to 10,000-15,000 birds per cycle from earlier units below 5,000, magnifying single-site demand and fostering large-batch deliveries. Automation technologies, including sensor-controlled feeders, reinforce precise nutrient delivery. While integration secures margins for large producers, it squeezes independent mills that rely on spot sales, heightening market consolidation pressures.

Growing Demand for Antibiotic-Free Meat

Urban consumers favor transparent labels and are willing to pay 15-20% premiums for birds raised on drug-free feed. Formulations increasingly incorporate probiotics, essential oils, and organic acids, driving an 8-12% rise in ingredient cost that manufacturers offset through brand-driven pricing. Multinational additive suppliers such as Alltech and Kemin have expanded domestic facilities for natural growth enhancers, underscoring the shift from preventive medication to functional nutrition. The Food Safety and Standards Authority of India has tightened residue thresholds, reinforcing this trajectory while creating export headroom into high-compliance markets.

Government Subsidies on Maize and Soybean

Minimum support prices and transport rebates flatten raw-material volatility in feed clusters distant from grain belts. State freight incentives lower inbound logistics bills, particularly for maize mills in southern coastal zones. Policy alignment with the nationwide ethanol program raises maize demand yet also yields distillers dried grains with solubles, supplying protein-rich Dried distillers' grain with solubles (DDGS) to the feed sector. Higher Minimum Support Prices (MSP) for soybeans encourage acreage expansion, while government-backed drought-resistant hybrids shield yields against erratic rainfall. These programs moderate input swings over the next two seasons, sustaining balanced ration economics for compounders.

Surge in Insect-Protein Inclusion

Pilot projects led by the Indian Council of Agricultural Research-Central Institute of Brackishwater Aquaculture (ICAR-CIBA) on Black Soldier Fly larvae are transitioning toward commercial scale with protein content near 45%, offering a sustainable alternative to imported soybean meal. Early inclusion trials report comparable growth performance at up to 10% dietary replacement. Feed firms are locking supply agreements as insect farms expand bio-conversion capacity using food waste streams, reducing the ingredient’s carbon footprint. Regulatory vetting under the Food Safety and Standards Authority of India (FSSAI) remains methodical, yet approval momentum aligns with global precedents, positioning insect meal for national rollout by 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High volatility in corn and soy prices | -1.4% | Nationwide, intense in import-dependent regions | Short term (≤2 years) |

| Inadequate last-mile feed logistics | -0.8% | Rural East and Northeast India | Medium term (2-4 years) |

| Rising mycotoxin incidents due to climate change | -0.6% | Humid storage-limited areas | Medium term (2-4 years) |

| Limited farmer access to credit for feed purchase | -0.5% | Smallholder-heavy rural belts | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Volatility in Corn and Soy Prices

Price swings of 40% were recorded during pandemic disruptions, squeezing mill gross margins. Import reliance for soybean meal leaves processors exposed to currency fluctuations, while seasonal monsoon variability stirs domestic supply risk. Thin forward-contracting instruments preclude effective hedging for smaller operators, compelling reactive sourcing strategies that elevate inventory costs. Storage deficits further magnify spot-market buys, perpetuating volatility.

Inadequate Last-Mile Feed Logistics

Weak rural roads, single-lane bridges, and sparse trucking capacity raise delivery costs by 15-25% in distant districts, deterring adoption of formulated feeds. During monsoon months, washed-out routes delay consignments, forcing farmers to shift to home-mixed rations that often lack balanced amino-acid profiles. Limited cool storage for vitamins and enzymes accelerates nutrient degradation, reducing feed efficacy upon arrival. Digital payment gaps also prolong dealer credit cycles, adding finance charges that inflate on-farm prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feed Ingredient: Maize Dominance Faces Protein Diversification

Maize retained 46% of end-use inclusion in 2024, yet faces mounting demand imbalance as annual poultry basal-grain needs could rise toward 31 million metric tons by 2030 versus current domestic output[1]Source: Food and Agriculture Organization, “Livestock Industrialization, Trade and Social-Health-Environment Issues for the Indian Poultry Sector,” fao.org . India's poultry feed market continues to show strong demand for maize, while processors are increasingly adopting alternative inputs. Dried distillers' grain with solubles (DDGS) offers comparable crude protein to soybean meal and is gaining adoption on cost merit. Insect meal volumes, though small, are experiencing a higher growth rate of 28% CAGR due to state-backed pilot plants. Feed labs are refining inclusion rates to maintain amino-acid ratios, ensuring palatability and digestibility on par with conventional soybean meal.

Growth prospects also hinge on rice DDGS availability in paddy-heavy states, trimming logistic miles relative to maize shipments. Regulatory clearance for novel proteins under the Food Safety and Standards Authority of India (FSSAI)’s 2024 feed standards offers a framework for broader market entry, though dossier preparation and shelf-life validation extend lead times. Ingredient sourcing diversification serves as both a risk mitigation strategy and a means to develop sustainable formulations that align with global Environmental, Social, and Governance (ESG) standards.

By Additive Type: Functional Nutrition Drives Premium Segments

Amino acids, particularly lysine and methionine, account for 30% of the market value, highlighting their critical role in supporting lean growth in fast-growing broilers. Dependence on imports sustains firm prices, driving interest in local manufacturing feasibility studies. Import dependency keeps prices firm, encouraging local manufacturing feasibility studies. Antibiotic-free production pushes probiotics, prebiotics, and organic acids into double-digit growth trajectories, with vitamin-E stabilized variants addressing oxidative stress in hotter climates. Indian poultry feed industry suppliers are leveraging microencapsulation to preserve bioactivity through pelleting. Enzymes enhance feed economics by breaking down non-starch polysaccharides. Protease complexes, now prevalent in finisher diets to reduce nitrogen excretion, are projected to grow at a 9.5% CAGR through 2030.

Market education is shifting from price-per-kilogram comparisons toward return-on-investment metrics like feed efficiency and mortality reduction. Additive firms provide on-farm technical audits and data-driven ration tweaks, embedding themselves deeper into integrator workflows. Domestic chemical intermediates are under review for quality accreditation, potentially lowering finished-additive landed cost and aligning with the government’s Make in India program.

By Form: Pellets Optimize Nutrition and Handling Efficiency

Pellets accounted for 52% of the volume in 2024 and are the fastest-growing segment, with a CAGR of 8.5% during the forecast period, reflecting their operational advantages. Uniform density simplifies bulk transport and reduces dust losses, while thermal processing enhances starch gelatinization for superior digestibility. The Indian poultry feed market size for pelleted feed is rising alongside demand for high-performance broilers that reach slaughter weight within 38-40 days. Investment in high-capacity conditioners and variable-frequency drives cuts energy expense per ton and improves throughput. Crumble feed retains relevance for starter diets requiring smaller particle sizes, whereas mash persists in low-income segments.

Large plants above 4,550 metric tons per day, such as those operated by United Nutrients, achieve economies of scale and maintain consistent pellet durability is more than 90%, minimizing fines. Ongoing R&D in die metal alloys and steam conditioning reduces outage frequency and expands plant uptime. However, localized power tariffs and biomass fuel costs still influence regional cost structures, prompting select mills to adopt solar boilers for partial thermal heating.

By Animal Type: Broiler Integration Reshapes Demand Patterns

Broiler rations accounted for 66% of total feed offtake, underscoring the dominance of quick-cycle meat production. While layers anchor steady demand for egg-production feed, breeders post the strongest expansion at 9.2% CAGR as integrators scale parent-stock farms to secure chick supply lines. India's poultry feed market share for specialized breeder diets is therefore widening, emphasizing micronutrient density and specific amino-acid ratios for hatching-egg quality. Export-oriented processors also mandate traceability and residue compliance, incentivizing precisely formulated breeder and finisher feeds that align with destination standards.

Contract farming enables mills to design phase-wise formulations synchronized with integrator performance dashboards, enabling nutritional fine-tuning over the bird’s lifecycle. This strategic approach increases feed volumes per site and secures long-term supply agreements, supporting capital investments in additional mill capacity.

Geography Analysis

Southern India remains the leading region in production volume. Andhra Pradesh, Tamil Nadu, and Karnataka benefit from port access, facilitating soybean imports and outbound meat shipments, which reduces logistics costs for feed mills. Major integrators operate multiple plants, and port-side warehousing facilitates year-round ingredient availability. Conversely, land and water constraints limit future greenfield farm sites, prompting expansion into interior districts.

Northern India registers rising demand on the back of organized retail penetration in Delhi NCR, Punjab, and Haryana. Proximity to the grain basket reduces inbound freight for maize and wheat by-products. Skylark’s FY 2023 revenue of USD 83.5 million underscores the region’s commercial viability. Cold-chain extensions into secondary cities encourage scale-up of contract grower networks that anchor feed volume growth.

Western India balances industrial consumption with feedstock diversity. Maharashtra’s ethanol plants generate Dried distillers' grain with solubles (DDGS), integrating circular supply chains for nearby poultry clusters. Meanwhile, East and Northeast India face road infrastructure gaps that elevate feed prices and dampen adoption. Government freight corridors and fresh storage subsidies aim to bridge these hurdles, yet river-flooded terrain poses seasonal transport risks. Humid climate in the east also heightens mycotoxin surveillance needs, spurring demand for toxin binders in formulations supplied to those markets.

Competitive Landscape

The India poultry feed market remains moderately concentrated, with the five largest producers controlling a significant market share. Their focus on vertical integration shapes competitive strategy across the value chain, starting with in-house seed production and extending through branded retail distribution. In 2025, Godrej Agrovet’s purchase of the remaining equity in Creamline Dairy for USD 112.0 million illustrates the push toward full feed-to-fork consolidation. Contract-farming arrangements reinforce this model by giving integrators a captive customer base for compound feed, allowing them to eliminate intermediary margins and guarantee consistent offtake.

Manufacturers leverage technology as a key differentiator. By employing IoT sensors in silos and AI-driven precision-feeding software, they optimize feed conversion ratios in real-time, leading to cost reductions and enhanced uniformity in bird weight[2]Source: A. Turgut and S. Singh, “Real-time optimization of poultry feed using IoT sensors,” International Journal of Intelligent Systems and Applications in Engineering, ijaiae.org. The most significant growth potential lies in organic feed, insect-protein blends, and region-specific formulations utilizing local raw materials. In 2025, signaling the industry's allure, JK Paper, branching out from its core, invested USD 36.1 million in acquiring Quadragen VetHealth, marking its foray into animal nutrition. While multinationals tap into global R&D pipelines to dominate the premium segment, domestic firms focus on cost efficiency and an extensive distribution network.

Regulation, led by the Food Safety and Standards Authority of India (FSSAI), expanded feed-quality mandate, rewards mills with advanced QA systems, and raises the bar for smaller rivals. Bureau of Indian Standards (BIS) norms covering plant equipment and nutrient specifications further tilt the field toward capital-rich firms able to upgrade processes[3]Source: Bureau of Indian Standards, “Standards for poultry feed manufacturing equipment,” bis.gov.in. Technical service teams staffed by qualified nutritionists have become central to customer retention, especially as producers transition to antibiotic-free regimens that rely on phytogenic additives and other natural growth promoters. Export expansion requires ISO-aligned traceability, favoring companies with end-to-end digital documentation.

India Poultry Feed Industry Leaders

Godrej Agrovet Limited (Godrej Group)

Suguna Foods Pvt. Ltd.

Venky's India Limited (VH Group)

Skylark Feeds Pvt. Ltd. (Skylark Group)

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Allana Group has signed a term sheet to acquire a 30% stake in Kasturi Poultry Farms, representing a strategic step toward strengthening its position in the country's poultry market. This acquisition is expected to contribute to the growth of the Indian poultry feed market by driving demand for high-quality feed to support the enhanced operations and production capacity of Kasturi Poultry Farms.

- March 2025: The Indian Poultry Alliance (IPA), a part of the Allana Group, has acquired Kwality Animal Feeds Pvt Ltd. Furthermore, IPA plans to bolster and expand the operations of the newly acquired entity, solidifying its dominance in the Indian poultry feed market and underscoring its vision for a consolidated industry future.

- August 2024: Godrej Agrovet's board has approved the establishment of a new animal feed plant in Maharashtra. This strategic move aims to enhance the company's production capacity and cater to the growing demand for poultry feed in the country.

- July 2023: Amul Dairy has introduced a new range of poultry feed products by utilizing its well-established cattle feed production facilities and distribution network. With six months of development, Amul leveraged its extensive expertise in animal feed production to address the expanding Indian poultry feed market.

India Poultry Feed Market Report Scope

| Maize |

| Soybean Meal |

| DDGS |

| Insect Meal |

| Other Feed Ingredients |

| Amino Acids |

| Vitamins and Minerals |

| Coccidiostats |

| Enzymes |

| Other Additives |

| Mash |

| Pellets |

| Crumbles |

| Other Forms |

| Broiler |

| Layer |

| Breeder |

| By Feed Ingredient | Maize |

| Soybean Meal | |

| DDGS | |

| Insect Meal | |

| Other Feed Ingredients | |

| By Additive Type | Amino Acids |

| Vitamins and Minerals | |

| Coccidiostats | |

| Enzymes | |

| Other Additives | |

| By Form | Mash |

| Pellets | |

| Crumbles | |

| Other Forms | |

| By Animal Type | Broiler |

| Layer | |

| Breeder |

Key Questions Answered in the Report

What is the current value of the India poultry feed market and how fast is it growing?

The market is worth USD 18.0 billion in 2025 and anticipated to reach USD 25.25 billion by 2030 at a 7.0% CAGR.

Which feed ingredient contributes most to poultry rations?

Maize supplies 46% of total formulations, remaining the primary energy source, though insect meal is emerging fast.

Why are pellets preferred over mash feed in commercial farms?

Pelleting improves feed conversion by 5-8%, eases bulk handling, and now captures 52% of nationwide feed volume.

Which animal type segment is projected to grow fastest through 2030?

Breeder feed leads growth at a 9.2% CAGR as integrators scale parent-stock operations to back expanding broiler demand.

Page last updated on: