Biochemical Reagents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 46.92 Billion |

| Market Size (2031) | USD 66.34 Billion |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

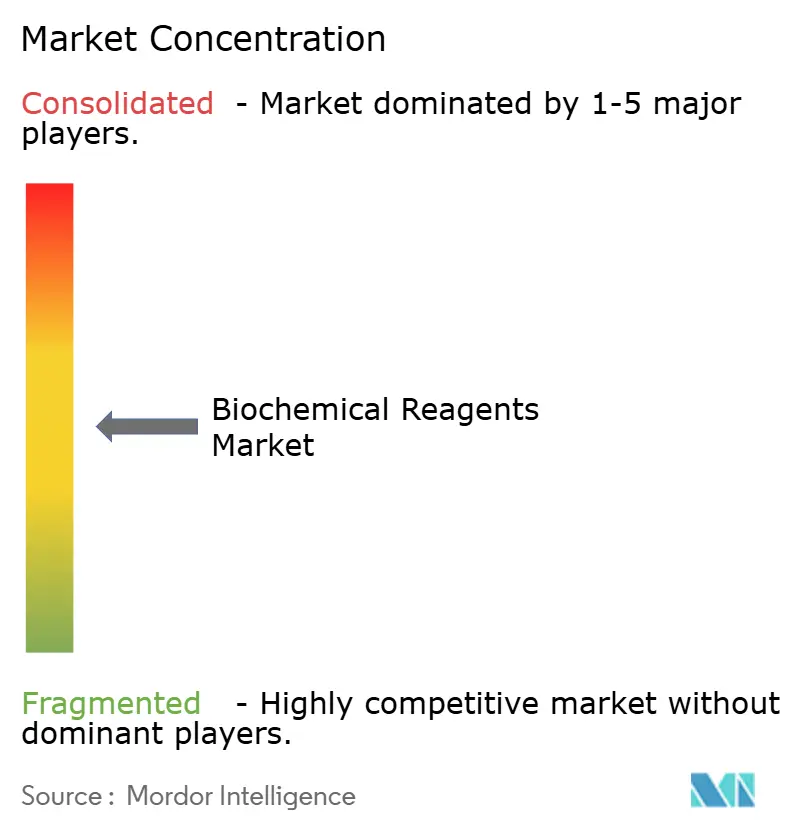

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biochemical Reagents Market Analysis by Mordor Intelligence

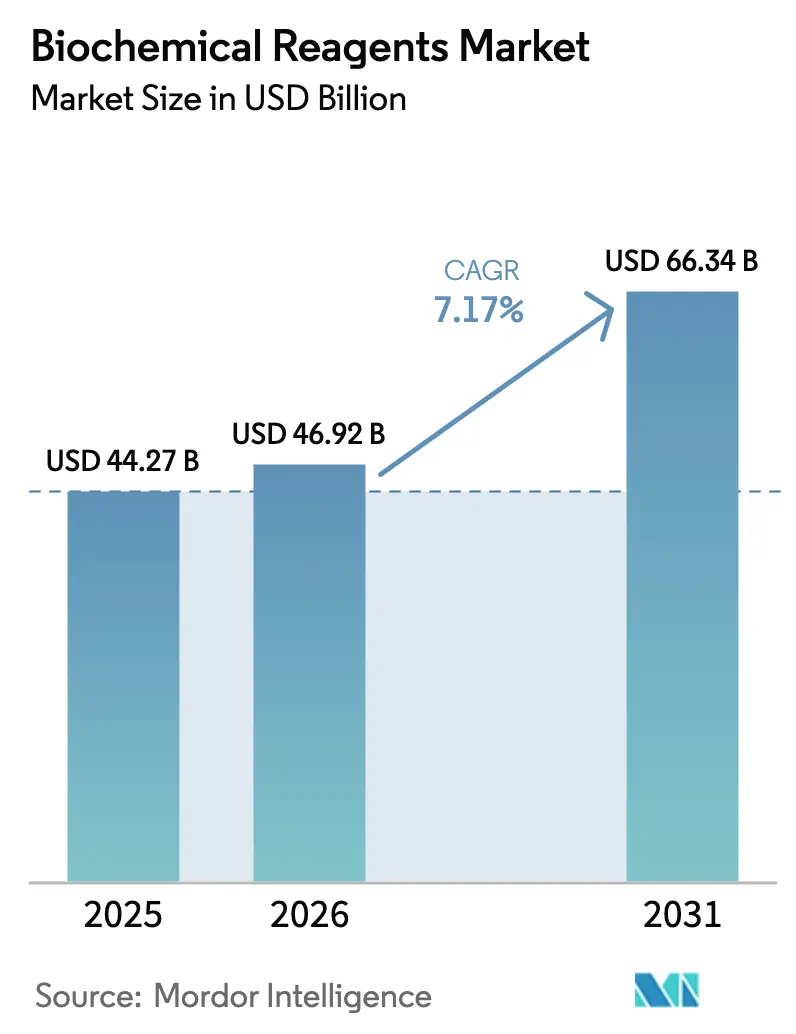

The Biochemical Reagents Market size is expected to increase from USD 44.27 billion in 2025 to USD 46.92 billion in 2026 and reach USD 66.34 billion by 2031, growing at a CAGR of 7.17% over 2026-2031.

Sovereign funding pushes are reshaping supply chains, led by the United States where the National Institutes of Health set aside USD 50.1 billion for fiscal 2025 to support genomics and proteomics programs that depend on high-purity reagents.[1]National Institutes of Health, “Budget for Fiscal Year 2025,” nih.gov Parallel growth stems from the U.S. Advanced Research Projects Agency for Health, which secured up to USD 2.5 billion to accelerate next-generation sequencing and molecular diagnostics platforms, further enlarging the biochemical reagents market.[2]Advanced Research Projects Agency for Health, “Funding Overview,” arpa-h.gov Structural incentives favor domestic production as policymakers guard against enzyme-supply shocks that emerged during 2024-2025 geopolitical tensions, and firms that can guarantee uninterrupted deliveries are securing long-horizon contracts. The biochemical reagents market is also benefiting from automation-ready kit formats that reduce labor costs in high-throughput screening centers and from AI-driven formulation tools that shorten development cycles for custom mixes.

Key Report Takeaways

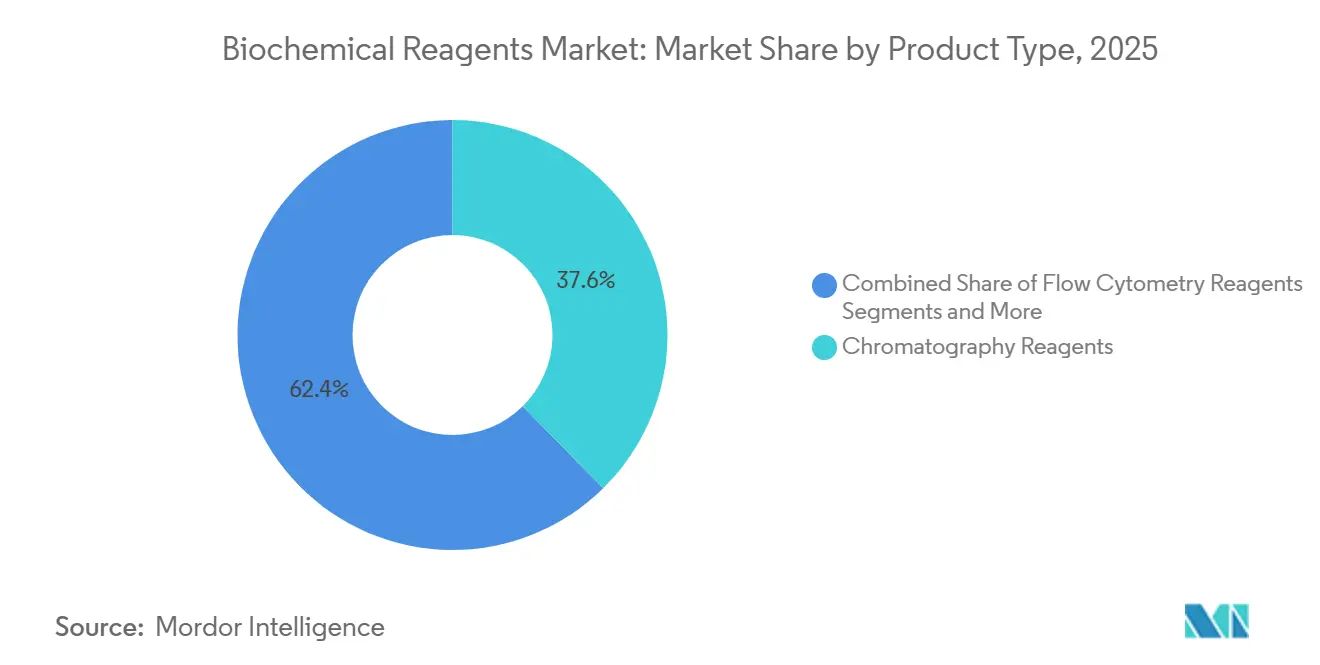

- Chromatography reagents accounted for a 37.63% biochemical reagents market share in 2025, while PCR kits are projected to advance at a 10.44% CAGR through 2031 as the fastest growing product category.

- By end user, biotechnology companies led with 31.56% of the biochemical reagents market in 2025, whereas contract research organizations are expanding at a 10.06% CAGR, the strongest pace among customer groups.

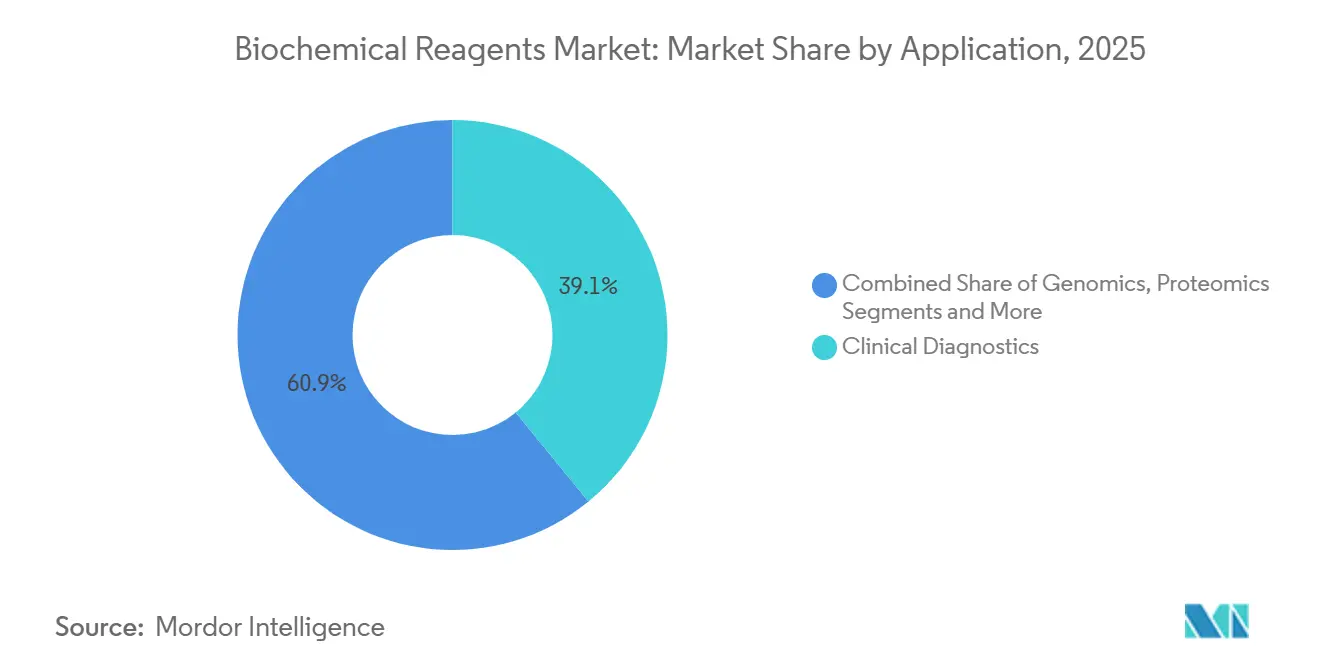

- Within applications, clinical diagnostics held a 39.11% share in 2025, yet genomics use cases are on track for an 11.63% CAGR and will narrow the gap by 2031.

- PCR technology dominated with a 44.23% share in 2025; however, next-generation sequencing reagents are forecast to climb at a 10.34% CAGR as large-scale population sequencing intensifies.

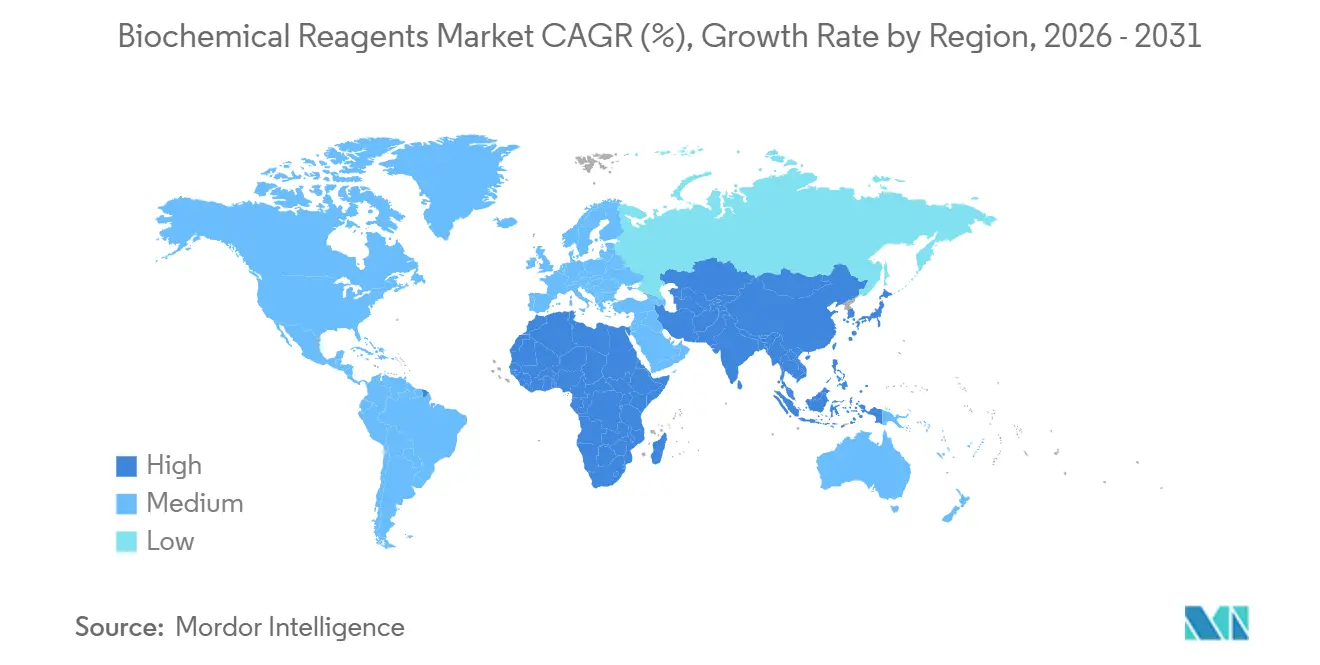

- North America captured 44.42% of global revenue in 2025, while Asia-Pacific is expected to register a 9.35% CAGR—the quickest regional trajectory—supported by local manufacturing hubs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biochemical Reagents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring Demand for Molecular Diagnostics | 1.8% | Global, with peak intensity in North America & Europe | Short term (≤ 2 years) |

| Expansion of Genomics & Proteomics Research | 1.5% | Global, led by North America, Europe, and Asia-Pacific (China, Japan, Singapore) | Medium term (2-4 years) |

| Rising Biopharma R&D Budgets Worldwide | 1.3% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Automation & High-Throughput Screening Adoption | 1.0% | North America, Europe, and APAC (China, Japan, South Korea) | Medium term (2-4 years) |

| AI-Optimized Reagent Formulation Pipelines | 0.9% | North America & Europe, early adoption in APAC | Long term (≥ 4 years) |

| Localized Manufacturing Hubs In Emerging Markets | 0.7% | APAC core (China, India), spill-over to MEA and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Demand for Molecular Diagnostics

Point-of-care settings now rely on ready-to-use PCR and isothermal mixes, lifting reagent throughput in hospital networks. The U.S. Food and Drug Administration cleared 23 new in-vitro diagnostic assays in 2025, 17 of which utilize PCR or NGS chemistries. Europe’s IVDR is forcing suppliers to reformulate products with stronger stability data, driving incremental sales of enhanced buffer systems. Infectious-disease surveillance remains central, highlighted by the World Health Organization’s 2025 AMR network that enrolled 120 countries, each standardizing PCR kits for pathogen detection.[3]World Health Organization, “Global AMR Surveillance System 2025,” who.int Lyophilized formulations that ship without refrigeration already represented 18% of PCR unit sales in 2025 and are expanding quickly as telehealth services proliferate.

Expansion of Genomics and Proteomics Research

Population-level sequencing is transitioning from pilots to national programs. The United Kingdom plans to sequence 5 million genomes by 2028, translating into roughly 15 million library prep kits over the span. Japan earmarked USD 800 million in 2025 to link genomic data with electronic medical records, prompting bulk orders for high-throughput sequencing reagents. On the proteomics front, the European Molecular Biology Laboratory established a data repository that sets common sample-prep specifications across laboratory networks. Single-cell sequencing programs funded by the U.S. National Science Foundation are spreading barcoding reagent demand across 30 academic sites.

Rising Biopharma R&D Budgets Worldwide

Roche reported CHF 15.2 billion (USD 17.1 billion) in R&D spending for 2025 with a 40% allocation toward oncology and immunology workflows that intensively use flow-cytometry and cell-culture reagents. Pfizer earmarked USD 13.8 billion for R&D, including USD 2.1 billion devoted to mRNA vaccine platform expansion that leans on nucleotide analogs. CDMOs such as Lonza have followed suit, adding USD 1.2 billion in capacity and locking in reagent supply contracts. Novel therapies such as antibody-drug conjugates consume 3-5 times the reagent volume of traditional small-molecule processes, sustaining double-digit growth across chromatography and conjugation chemistries.

Automation and High-Throughput Screening Adoption

Reagents pre-validated for robotic liquid handlers grew 22% year on year for Thermo Fisher in 2025, triple the pace of manual format products. Danaher reported USD 1.8 billion in automation-compatible reagent sales for 2025, confirming strong laboratory migration to 384-well plates. Accreditation bodies now embed automation performance in their audits, encouraging clinical labs to retire in-house mixes for standardized kits. The combination of speed, lower error rates, and compliance advantages positions automated reagents as a durable growth catalyst.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory & Compliance Burden | -0.8% | Global, most acute in North America & Europe | Short term (≤ 2 years) |

| Short Shelf-Life and Cold-Chain Costs | -0.6% | APAC, MEA, South America, with moderate impact in rural North America & Europe | Medium term (2-4 years) |

| Enzyme-Supply Geopolitical Concentration Risk | -0.5% | Global, with highest exposure in APAC and MEA dependent on Western suppliers | Medium term (2-4 years) |

| Escalating IP Litigation Delaying Launches | -0.4% | Global, concentrated in North America & Europe due to patent-enforcement infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Compliance Burden

Europe’s IVDR imposes clinical evidence demands that add USD 0.5-2 million to each diagnostic reagent, delaying launches by up to 18 months. The FDA also signaled tighter control over laboratory-developed tests in 2025, unsettling hospital labs that historically prepared their own mixes. Only 40% of Asia-Pacific suppliers held ISO 13485 certification by 2025, limiting their ability to win global contracts. Environmental frameworks such as REACH added 18 solvents to restriction lists, triggering expensive reformulations.

Short Shelf-Life and Cold-Chain Costs

A 2024 PLOS ONE study found that 22% of PCR shipments into sub-Saharan Africa arrived partially degraded, compromising diagnostic accuracy. Temperature-controlled logistics add 15-25% to landed cost in tropical settings, undermining competitiveness versus locally produced goods. Lyophilization increases manufacturing cost by up to 40%, while global cold-chain airfreight capacity grew only 4% in 2025 against 9% demand growth. Hospitals discard 10-12% of inventory annually due to expiry, which deters economies of scale in procurement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCR Kits Surge while Chromatography Retains Purification Role

Chromatography reagents held 37.63% of the biochemical reagents market share in 2025 and remain central to monoclonal-antibody purification. PCR kits are on course for a 10.44% CAGR to 2031, underpinned by point-of-care testing mandates and wide infectious-disease surveillance. The biochemical reagents market size for PCR kits is projected to grow from USD 11.2 billion in 2026 to USD 18.3 billion by 2031, reinforcing their momentum. Cell and tissue culture reagents continue to climb, energized by the maturing cell-therapy pipeline, while electrophoresis reagents experience moderate growth due to rising adoption of microfluidic alternatives.

Second-generation flow cytometry dyes now support 20-plus-parameter panels, driving 8-9% annual growth in that subcategory. NGS and genomics reagents are set for a steady 9-10% CAGR, buoyed by falling sequencing-run costs and population genomics. Specialty mixes aimed at CRISPR applications and single-cell barcoding grow fastest on a smaller base, capturing premium prices due to their customization level.

By End User: CROs Accelerate as Biotech Holds Top Rank

Biotechnology firms consumed 31.56% of the biochemical reagents market in 2025, sustained by heavy early-stage research pipelines. CRO demand is advancing at 10.06% CAGR through 2031, lifted by the outsourcing model favored by big pharma, pushing the biochemical reagents market size among CROs to a projected USD 9 billion by 2031. Pharmaceutical companies maintain a large yet steady footprint, whereas CDMOs represent a rising buyer block, particularly in cell culture media and chromatography resins used for contract biologics manufacture.

Hospitals and diagnostic reference labs are tightening quality controls by migrating to standardized kits. Academic and research institutes remain price sensitive, although new grants for large scale sequencing and proteomics bolster reagent procurement volumes.

By Application: Genomics Growth Outpaces Diagnostics

Clinical diagnostics commanded 39.11% of revenue in 2025, but genomics applications will clock an 11.63% CAGR as more nations roll out population sequencing. That surge will push the biochemical reagents market share of genomics applications closer to one-third of global sales by 2031. Proteomics is rising on the back of improved mass-spectrometry workflows, while drug discovery applications expand steadily as phenotypic assays become mainstream in high-content screening.

By Technology: PCR Dominates yet NGS Advances Rapidly

PCR accounted for 44.23% of sales in 2025, underscoring its diagnostic ubiquity. NGS reagents nevertheless will capture incremental share at a 10.34% CAGR, reflecting the broadening of whole-genome and transcriptome sequencing. Isothermal amplification reagents grow quickly although from a smaller base, and digital PCR enjoys a double-digit trajectory in precision-oncology testing.

Geography Analysis

North America generated 44.42% of global revenue in 2025 due to a robust reimbursement environment, mature regulatory pathways, and heavy public research funding. The United States accounts for three-quarters of regional sales and concentrates demand in bioclusters anchored by California and Massachusetts. Canada leverages Genome Canada’s USD 180 million precision-medicine program to drive 5-6% annual growth. Mexico is expanding as pharma manufacturing shifts south, but logistics hurdles slow uptake.

Asia-Pacific is forecast to post a 9.35% CAGR, the fastest for any region. China is progressing from import dependence toward domestic supply, helped by a USD 2.3 billion enzyme facility initiative aimed at 30% local share by 2028. India’s Department of Biotechnology introduced a USD 500 million cold-chain subsidy that improves penetration in tier-2 cities. Japan’s aging population is boosting companion diagnostic volumes, while South Korea capitalizes on biosimilar expansion.

Europe, anchored by Germany, France, and the United Kingdom. Full IVDR enforcement prompted the withdrawal of about one-third of legacy kits, creating white-space for re-engineered offerings. The Middle East and Africa rise at 6-7% as Saudi Arabia and the United Arab Emirates build genomic centers to diversify their economies. South America advances at a similar clip, led by Brazil where ANVISA’s streamlined approval rules cut regulatory drag.

Competitive Landscape

The biochemical reagents market remains moderately consolidated. Vertically integrated manufacturing and multi-year supply contracts shield incumbents, yet regional challengers such as Vazyme Biotech and Takara Bio are capturing Asia-Pacific share through 20-30% lower price points and faster delivery. AI-driven reagent design is becoming a competitive frontier; Thermo Fisher reported a 40% cut in time-to-market for bespoke mixes released through its machine-learning platform in 2025. Smaller firms exploit niche gaps with enzyme variants for difficult templates or antibodies validated for new biomarkers, often commanding premium prices despite limited volume. Compliance hurdles—including ISO 13485 certification timelines of up to 24 months—continue to deter new entrants, reinforcing incumbents’ scale advantages.

Biochemical Reagents Industry Leaders

Agilent Technologies Inc.

Merck KGaA

Bio-Rad Laboratories

Thermo Fisher Scientific Inc.

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Synthego formally entered molecular and clinical diagnostic reagents, expanding its CRISPR expertise into validated assay consumables.

- December 2025: iGeneTech unveiled premixed reagent strips compatible with its IGT-AS12 workstation, offering fast, ready-to-load library prep.

- September 2025: Illumina launched Illumina Protein Prep, bringing NGS-based proteomics discovery to full commercial availability and enabling integrated multi-omics studies.

Global Biochemical Reagents Market Report Scope

Biochemical reagents can be defined as chemical agents extracted from any biological system for biological research. The production of biochemical reagents is done by three basic procedures, namely chemical synthesis, isolation and purification of the chemical substance from the organisms, and fermentation.

The Biochemical Reagents Market Report is segmented by Product Type, End User, Application, Technology, and Geography. By Product Type, the market is segmented into PCR Reagent Kits, Cell & Tissue Culture Reagents, Electrophoresis Reagents, Chromatography Reagents, Flow Cytometry Reagents, NGS & Genomics Reagents, and Other Specialty Reagents. By End User, the market is segmented into Biotechnology Companies, Pharmaceutical Companies, CROs, CDMOs, Hospitals, Diagnostic Laboratories, and Academic & Research Institutes. By Application, the market is segmented into Genomics, Proteomics, Clinical Diagnostics, Drug Discovery & Development, and Others. By Technology, the market is segmented into PCR, Next-Generation Sequencing, Isothermal Amplification, Microarray, and Others. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| PCR Reagent Kits |

| Cell & Tissue Culture Reagents |

| Electrophoresis Reagents |

| Chromatography Reagents |

| Flow Cytometry Reagents |

| NGS & Genomics Reagents |

| Other Specialty Reagents |

| Biotechnology Companies |

| Pharmaceutical Companies |

| Contract Research Organisations (CROs) |

| CDMOs |

| Hospitals |

| Diagnostic Laboratories |

| Academic & Research Institutes |

| Genomics |

| Proteomics |

| Clinical Diagnostics |

| Drug Discovery & Development |

| Others |

| PCR |

| Next-Generation Sequencing |

| Isothermal Amplification |

| Microarray & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | PCR Reagent Kits | |

| Cell & Tissue Culture Reagents | ||

| Electrophoresis Reagents | ||

| Chromatography Reagents | ||

| Flow Cytometry Reagents | ||

| NGS & Genomics Reagents | ||

| Other Specialty Reagents | ||

| By End User | Biotechnology Companies | |

| Pharmaceutical Companies | ||

| Contract Research Organisations (CROs) | ||

| CDMOs | ||

| Hospitals | ||

| Diagnostic Laboratories | ||

| Academic & Research Institutes | ||

| By Application | Genomics | |

| Proteomics | ||

| Clinical Diagnostics | ||

| Drug Discovery & Development | ||

| Others | ||

| By Technology | PCR | |

| Next-Generation Sequencing | ||

| Isothermal Amplification | ||

| Microarray & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the biochemical reagents market in 2031?

It is expected to reach USD 66.34 billion by 2031, expanding at a 7.17% CAGR from 2026.

Which product segment is forecast to grow the fastest?

PCR reagent kits are set for a 10.44% CAGR, benefiting from widespread deployment in point-of-care diagnostics.

How large is North America’s share of global sales?

North America accounted for 44.42% of revenue in 2025, the largest regional share.

Why are CROs increasing reagent purchases?

Outsourcing trends in pharmaceutical R&D are driving CRO reagent demand at a 10.06% CAGR through 2031.

Which technology is gaining ground on PCR?

Next-generation sequencing reagents are increasing at a 10.34% CAGR as whole-genome studies proliferate.

Page last updated on: