Oxidative Stress Assay Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

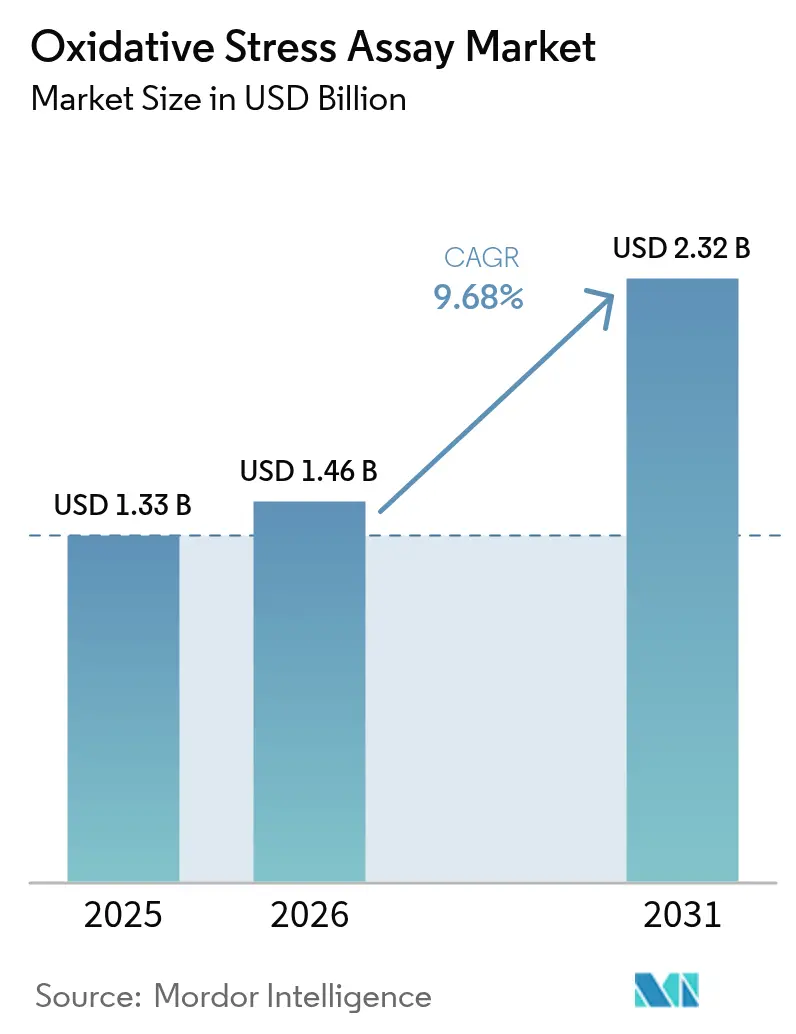

| Market Size (2026) | USD 1.46 Billion |

| Market Size (2031) | USD 2.32 Billion |

| Growth Rate (2026 - 2031) | 9.68% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

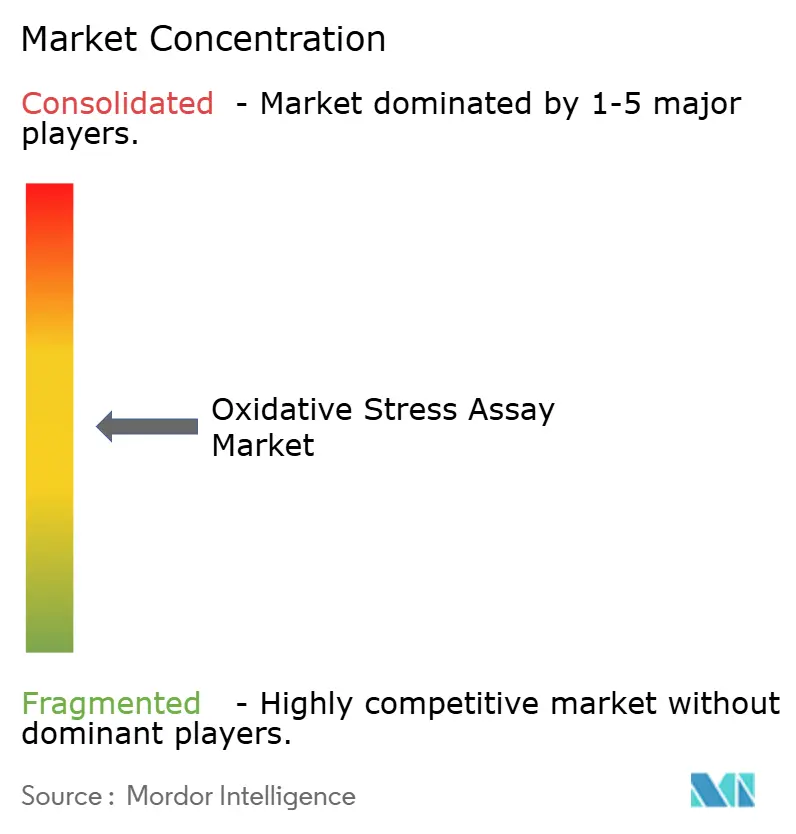

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oxidative Stress Assay Market Analysis by Mordor Intelligence

The oxidative stress assays market size was valued at USD 1.33 billion in 2025 and estimated to grow from USD 1.46 billion in 2026 to reach USD 2.32 billion by 2031, at a CAGR of 9.68% during the forecast period (2026-2031). Advancing biopharma scale-up, growing regulatory acceptance of in-vitro toxicology, and AI-enabled analytics are redefining how real-time reactive oxygen species measurement supports drug development. Instruments dominate current spending because high-throughput flow cytometry and mass spectrometry systems shorten screening cycles and improve data depth. Live-cell multiplex platforms that track mitochondrial dysfunction, lipid peroxidation, and antioxidant capacity in one workflow are replacing traditional single-endpoint kits, positioning the oxidative stress assays market for sustained technology-led growth.

Key Report Takeaways

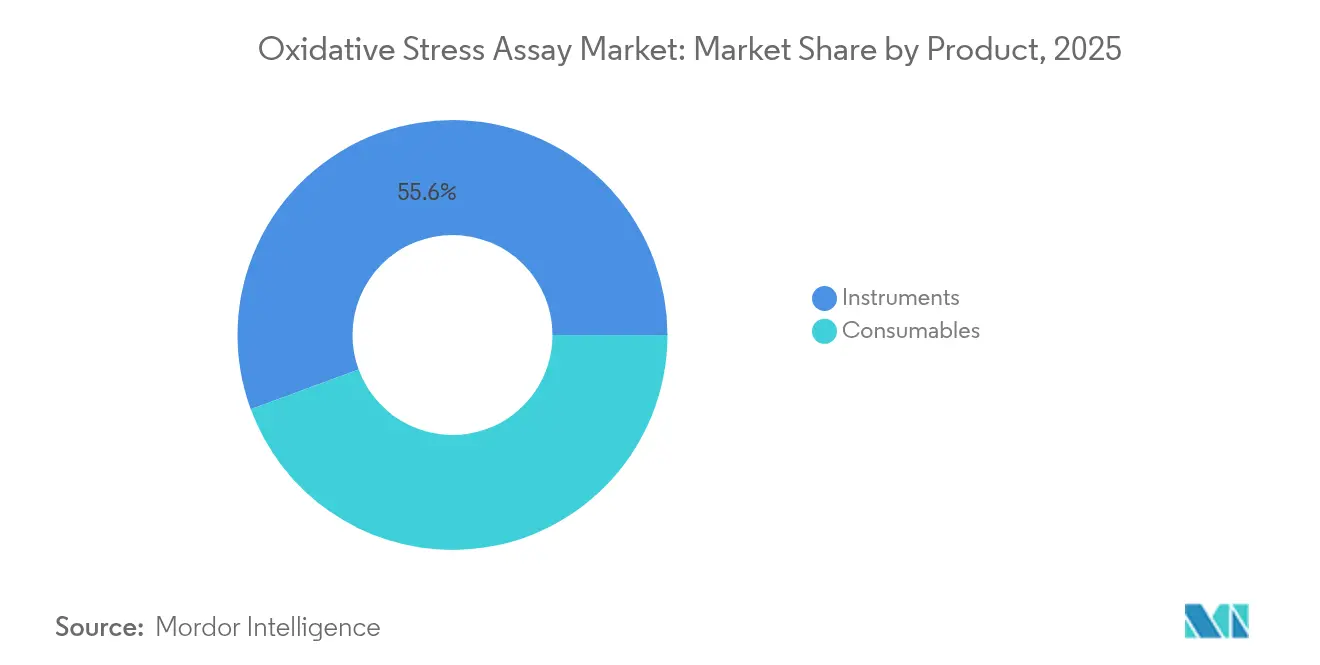

- By product type, instruments held 55.62% of oxidative stress assays market share in 2025; consumables will outpace with a 13.12% CAGR to 2031.

- By test type, ROS-based assays captured 29.10% of the oxidative stress assays market size in 2025 and will rise at 11.82% CAGR through 2031.

- By technology, flow cytometry led with 37.02% revenue share in 2025 while label-free impedance and real-time cell analysis record the highest projected CAGR at 11.66% to 2031.

- By disease type, cancer applications commanded 30.88% market share in 2025; neurodegenerative disorders will grow fastest at 10.79% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies accounted for 43.89% of 2025 revenue, whereas contract research organizations expand at 11.32% CAGR to 2031.

- By sample type, cell-based models represented 39.44% share and are advancing at 12.23% CAGR through 2031.

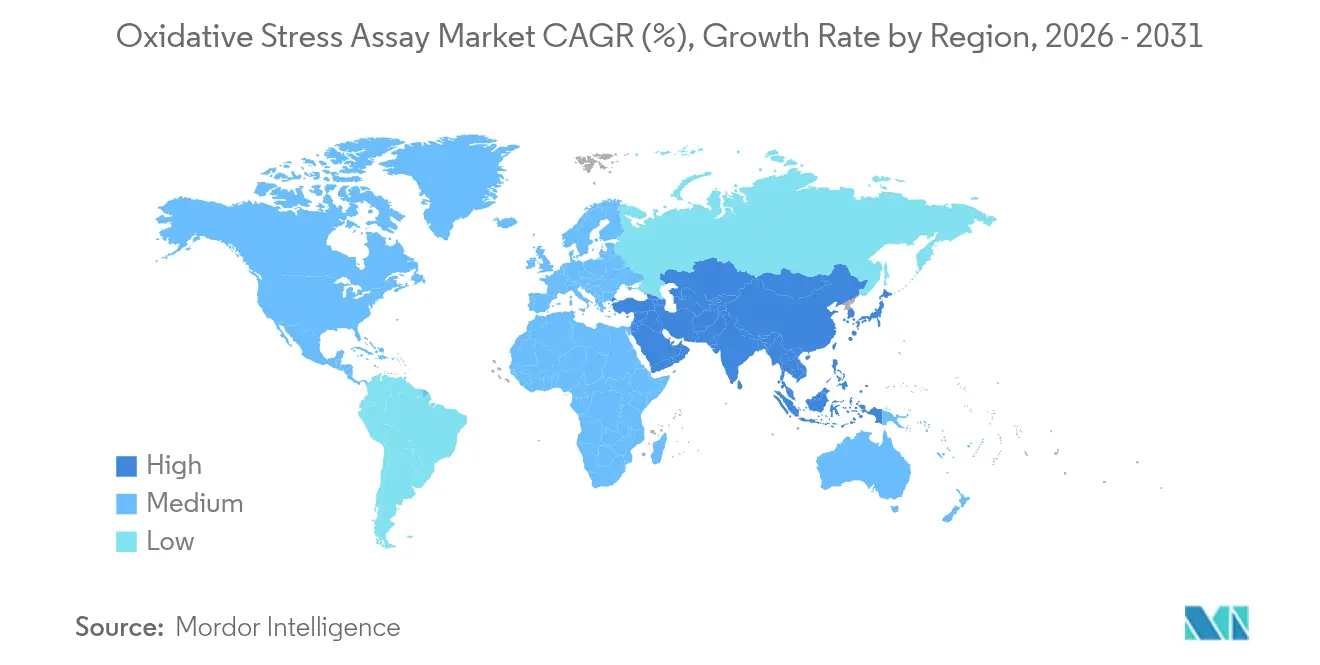

- By geography, North America retained 36.41% share in 2025 yet Asia Pacific posts the fastest 11.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oxidative Stress Assay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth In Biopharma & Biotech Manufacturing | +2.1% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Expansion Of High-Throughput Screening (HTS) For ROS Biomarkers | +1.8% | North America & APAC core, spill-over to EU | Short term (≤ 2 years) |

| Regulatory Push For In-Vitro Toxicology Alternatives | +1.5% | Global, led by North America & EU regulatory frameworks | Long term (≥ 4 years) |

| Mainstream Adoption Of Label-Free Live-Cell Imaging Assays | +1.3% | Global, with early adoption in North America | Medium term (2-4 years) |

| Novel Red-Fluorescent Probes For Real-Time Mitochondrial ROS | +1.0% | Global research institutions and biopharma | Short term (≤ 2 years) |

| Integration Of AI-Driven Assay Analytics | +0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Biopharma and Biotech Manufacturing

Expanding biopharma capacity is amplifying demand for oxidative stress assays that serve as real-time quality indicators during process scale-up. Thermo Fisher Scientific invested USD 22 million in oral solid dose facilities and embedded predictive AI to monitor oxidative stress signatures that threaten protein stability. Continuous manufacturing workflows now depend on inline assays able to flag metabolic shifts before they affect yield. Bio-Rad’s purchase of Stilla Technologies brought digital PCR sensitivity to oxidative biomarker detection, confirming that next-generation production relies on integrated analytical ecosystems. This transition positions oxidative stress measurement as a standard parameter alongside purity and potency in commercial biologics runs.

Expansion of High-Throughput Screening for ROS Biomarkers

High-throughput screening (HTS) systems let scientists assess thousands of oxidative stress conditions in parallel, cutting discovery timelines for antioxidants and sensitizers. Abcam’s FirePlex multiplex platform couples validated antibody pairs with automation, removing the bottleneck of sequential testing and increasing quantitative sensitivity tenfold over earlier kits. Merging HTS with deep-learning algorithms further lowers false positive rates while CRISPR-based functional screening pinpoints genes that mediate redox balance. Cost-reducing miniaturization means libraries can expand without proportional reagent spend, accelerating early-stage drug pipelines.

Regulatory Push for In-Vitro Toxicology Alternatives

Regulators worldwide advocate in-vitro oxidative stress assays to replace animal studies, citing both ethics and superior mechanistic insight. The FDA’s revised laboratory-developed test rule standardizes clinical validation for oxidative biomarkers and its biomarker qualification program clarifies acceptance criteria. European agencies reinforce the 3Rs principle, prompting industry to adopt human-relevant oxidative endpoints for safety dossiers. Oncology programs gain particular value because a single assay can reveal both efficacy and cardiotoxicity profiles, streamlining submissions.

Mainstream Adoption of Label-Free Live-Cell Imaging Assays

Label-free imaging tracks oxidative dynamics without probe-induced artifacts. Fluorescence lifetime imaging of endogenous NADH distinguishes shifts in metabolic redox state at single-cell resolution, giving researchers temporal insight lost in endpoint staining.[1]Brandon G. Reid, “Label-Free FLIM of NADH Reveals Cellular Energy Metabolism in Live Cells,” Communications Biology, nature.comRaman-based microfluidic chips monitor ferroptosis in defined microscale environments, while flexible bioimpedance sensors deliver continuous viability data at lower cost than colorimetric kits.[2]Yong-Hua Luo, “Flexible Bioimpedance Sensors Deliver Rapid Viability Readouts,” Chemosensors, mdpi.com These advances unlock longitudinal studies of mitochondrial health during drug exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost Of Detection Instruments | -1.4% | Global, particularly affecting emerging markets | Long term (≥ 4 years) |

| Lack Of Trained Personnel In Multi-Modal Data Interpretation | -1.1% | Global, with acute shortages in APAC | Medium term (2-4 years) |

| Photobleaching & Probe-Derived Artifacts | -0.8% | Global research institutions | Short term (≤ 2 years) |

| Limited Standardization Of ROS Reference Materials | -0.6% | Global, affecting regulatory acceptance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Detection Instruments

Top-tier orbitrap mass spectrometers exceed USD 1 million per unit, and many academic labs defer purchases because budgets trail the pace of innovation. Rapid obsolescence within seven years forces repeat investment, limiting diffusion into resource-constrained geographies. Leasing and pay-per-sample models are emerging but adoption remains low outside North America.

Lack of Trained Personnel in Multi-Modal Data Interpretation

Oxidative stress platforms produce complex outputs that span fluorescence, impedance, and genomic readouts. Analysts must understand biochemistry, statistics, and regulatory context, a combination still scarce in fast-growing Asia Pacific facilities.[3]Maria S. Domínguez, “Machine-Learning-Enabled Redox Signatures Enhance Cancer Therapy,” Antioxidants, mdpi.com While vendors run certification courses, the talent gap will persist until academic curricula align with new assay demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product – Instruments Propel Discovery While Consumables Accelerate Adoption

Instruments generated 55.62% of oxidative stress assays market revenue in 2025 and remain the backbone of advanced screening labs. Novel orbitrap analyzers that profile five times more compounds per run strengthen the segment’s appeal among pharmaceutical chemists who require deep metabolite coverage. Consumables, however, will register the fastest 13.12% CAGR to 2031 as kit-based workflows scale beyond top-tier centers. Ready-to-use red-fluorescent probes and standardized reference reagents simplify protocols for smaller labs, widening the oxidative stress assays market. Demand for consumables also benefits from recurring purchasing cycles that accompany ever-shorter assay turnaround expectations.

Second-generation probes with minimized autofluorescence broaden compatibility across flow cytometers and microscopes, boosting kit adoption. At the same time, instrument makers embed AI analytics directly on device firmware, condensing multi-step analysis into a single-click report. This convergence blurs the traditional boundary between hardware and consumables and sustains above-market growth for manufacturers able to provide end-to-end platforms that ensure data continuity.

By Test Type – ROS-Based Assays Retain a Leadership Position

ROS-based assays accounted for 29.10% of oxidative stress assays market share in 2025 and will grow at 11.82% CAGR as drug developers prioritize real-time insights into oxidative bursts that shape disease progression. Optogenetic H2O2 sensors achieve sub-cellular resolution and capture nanomolar fluxes, enabling researchers to correlate localized stress with pathway activation in cancer and neurodegeneration studies. Indirect assays that measure downstream products such as lipid peroxidation remain valuable when samples are fixed or when long-lived biomarkers are required for population studies.

Multiplex dashboards that combine ROS, antioxidant capacity, and protein oxidation endpoints on a single plate are now common, reducing experiment count and conserving precious primary cells. Such integrated testing shortens validation timelines and supports the oxidative stress assays market size expansion forecast to 2031.

By Technology – Flow Cytometry Maintains Versatility

Flow cytometry delivered 37.02% of 2025 revenue because single-cell resolution aligns with precision medicine goals. Next-generation protocols detect events below 0.001% frequency and allow researchers to isolate rare apoptotic populations. ELISA platforms still dominate regulated clinical workflows thanks to decades of accumulated validation, yet label-free impedance and real-time cell analysis achieve the fastest trajectory with continuous readouts that replace time-consuming endpoint staining.

Chromatography regains visibility as labs explore specific oxidative metabolites that cannot be captured by optical probes. Microscopy gains traction through fluorescence lifetime imaging modules that index metabolic reprogramming without dyes, further broadening the oxidative stress assays market.

By Disease Type – Oncology Drives Demand While Neurology Accelerates

Cancer applications delivered 30.88% of market revenue in 2025, fueled by the need to map tumor microenvironment redox states that influence therapy response. Machine-learning models now predict patient stratification based on redox signatures, positioning oxidative assays as a companion diagnostic input. Neurodegenerative disorders will outpace other segments with an 10.79% CAGR to 2031 as early-detection blood biomarkers progress toward clinical adoption.

Cardiovascular and COPD researchers continue to link oxidative biomarkers with endothelial dysfunction and pulmonary decline, validating assays as prognostic tools in chronic disease management. Cross-disciplinary uptake underpins healthy expansion across all disease-focused segments.

By End User – Pharma Dominates, CROs Expand Fastest

Pharmaceutical and biotechnology companies held 43.89% of 2025 spending because oxidative stress readouts are embedded in lead identification, safety assessment, and biomarker discovery. The segment benefits from FDA encouragement to include mechanistic biomarkers in regulatory packages. Contract research organizations deliver the highest 11.32% CAGR, as sponsors outsource multi-parameter analytics to specialists with validated workflows and regulatory expertise.

Academic and research institutes pioneer novel assay concepts that migrate to commercial settings, while service providers such as Creative Bioarray aggregate niche technologies into turnkey offerings that appeal to mid-size biotech firms.

By Sample Type – Cell-Based Models Gain Momentum

Cell-based assays captured 39.44% of revenue in 2025 and will expand at 12.23% CAGR to 2031 because 3D cultures and organoids reproduce human physiology more faithfully than traditional monolayers. Optimized lactate dehydrogenase protocols now quantify cytotoxicity in thick matrices, eliminating the need to section spheroids. Tissue homogenates remain essential for translational studies that confirm cellular findings within complex microenvironments.

Blood and plasma analysis grows as ultrasensitive kits detect low-abundance oxidative markers that mirror systemic stress. Non-invasive urine panels facilitate longitudinal monitoring, widening participation in large-cohort studies and advancing personalized medicine applications within the oxidative stress assays market.

Geography Analysis

North America maintained 36.41% revenue share in 2025 thanks to clear FDA biomarker qualification pathways and a dense biopharma infrastructure that rapidly pilots AI-driven assays from bench to clinic. Venture capital backing and equipment vendors headquartered in the United States foster rapid prototype adoption. Strategic collaborations, such as BioAge Labs partnering with Novartis to explore longevity targets, showcase how regional players leverage oxidative stress data to open new therapeutic frontiers.

Europe follows closely, propelled by stringent 3Rs directives that push laboratories toward validated in-vitro oxidative platforms. Academic centers supply a steady pipeline of assay innovations, while reagent companies emphasize standardized reference materials that meet European Medicines Agency expectations. Joint public–private projects accelerate technology translation and embed oxidative testing in sustainable research frameworks.

Asia Pacific records the fastest 11.05% CAGR through 2031. Chinese institutes advance electrochemical biosensors, and Japan aligns nutraceutical regulations with rigorous oxidative endpoint validation, broadening commercial demand. Government investment in biotechnology education is narrowing the analyst skills gap. Multinational suppliers expand distribution hubs and localized technical support, reflecting confidence in regional growth momentum.

Competitive Landscape

The oxidative stress assays market is moderately concentrated. Thermo Fisher Scientific, Abcam, and Merck KGaA leverage broad portfolios and global logistics to defend share, while agile specialists differentiate through proprietary probes or AI dashboards. Technology leadership outweighs price competition; customers value instruments that integrate data analytics and comply with evolving regulatory formats.

Mergers and alliances continue to reshape the field. Bio-Rad’s acquisition of Stilla Technologies bolstered digital PCR accuracy for redox markers, and Novartis joined BioAge Labs to mine aging datasets for oxidative targets. Start-ups focus on label-free, real-time sensing that bypasses fluorescent artifacts. Established firms counter by bundling consumables, software, and service contracts into platform subscriptions. Standardized ROS reference materials remain unmet needs that present white-space potential.

Oxidative Stress Assay Industry Leaders

Abcam plc

Merck KGaA

Thermo Fisher Scientific

Promega Corporation

Qaigen N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: IBL International partnered with Grifols to co-develop advanced biomarker panels for specialty diagnostics on single-molecule counting platforms.

- January 2025: Telomir Pharmaceuticals reported Telomir-1 fully reversed oxidative stress in human cell lines, highlighting therapeutic promise across age-related disorders.

Global Oxidative Stress Assay Market Report Scope

As per the scope of this report, Oxidative Stress Assay is a type of assay which is used to identify and screen the level of oxidative stress markers and reagents in cells. The Oxidative Stress Assay Market is segmented by Product (Instrument, Consumables, And Services), Test Type (Indirect Assays, Antioxidant Capacity Assays, Enzyme Based Assays and Reactive Oxygen Species Based Assays), Technology Type (Enzyme-Linked Immunosorbent Assay(Elisa), Flow Cytometry, Chromatography, Microscopy and Others), Disease Type (Cardiovascular Disease, Chronic Obstructive Pulmonary Disease(COPD), Cancer), End User (Pharmaceutical And Biotechnology Industries, Academic Research Institutes And Clinical Research Organizations) and Geography (North America, Europe, Asia-Pacific, Middle East And Africa, And South America). The report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values in USD million for the above segments.

| Instruments |

| Consumables |

| Indirect Assays |

| Antioxidant Capacity Assays |

| Enzyme-based Assays |

| Reactive Oxygen Species (ROS)-based Assays |

| Enzyme-linked Immunosorbent Assay (ELISA) |

| Flow Cytometry |

| Chromatography |

| Microscopy |

| Label-free Impedance & Real-Time Cell Analysis |

| Cardiovascular Diseases |

| Chronic Obstructive Pulmonary Disease (COPD) |

| Cancer |

| Neuro-degenerative Disorders |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Contract Research Organizations |

| Cell-based Samples |

| Tissue Homogenates |

| Blood / Plasma |

| Urine & Other Biofluids |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Instruments | |

| Consumables | ||

| By Test Type | Indirect Assays | |

| Antioxidant Capacity Assays | ||

| Enzyme-based Assays | ||

| Reactive Oxygen Species (ROS)-based Assays | ||

| By Technology | Enzyme-linked Immunosorbent Assay (ELISA) | |

| Flow Cytometry | ||

| Chromatography | ||

| Microscopy | ||

| Label-free Impedance & Real-Time Cell Analysis | ||

| By Disease Type | Cardiovascular Diseases | |

| Chronic Obstructive Pulmonary Disease (COPD) | ||

| Cancer | ||

| Neuro-degenerative Disorders | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| Contract Research Organizations | ||

| By Sample Type | Cell-based Samples | |

| Tissue Homogenates | ||

| Blood / Plasma | ||

| Urine & Other Biofluids | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the oxidative stress assays market?

The oxidative stress assays market is valued at USD 1.46 billion in 2026 and is on track to reach USD 2.32 billion by 2031.

Which product segment is expected to grow fastest?

Consumables are projected to register the fastest 13.12% CAGR as ready-to-use kits and probes gain traction.

Why are ROS-based assays so important for drug development?

They capture real-time fluctuations in reactive oxygen species, providing direct insight into disease mechanisms that guide lead optimization and safety profiling.

Which region shows the strongest growth momentum?

Asia Pacific posts the highest 11.05% CAGR through 2031, supported by expanding pharmaceutical R&D and rising healthcare investments.Asia Pacific posts the highest 11.05% CAGR through 2031, supported by expanding pharmaceutical R&D and rising healthcare investments.

How are regulators influencing assay adoption?

The FDA and European agencies promote in-vitro oxidative stress assays as humane, mechanistic alternatives to animal testing, accelerating market uptake in toxicology workflows.

What are the main barriers for new entrants?

High instrument costs and the shortage of analysts skilled in multi-modal data interpretation remain the largest hurdles for smaller laboratories.

Page last updated on: