Pharmaceutical Excipients Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

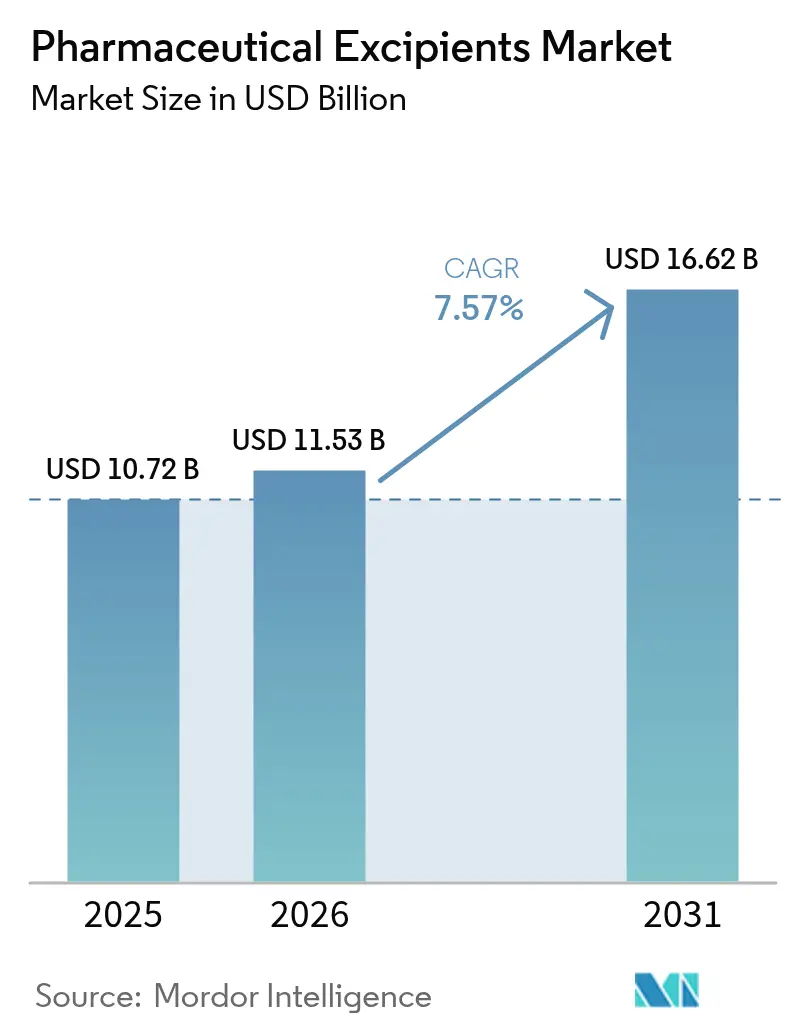

| Market Size (2026) | USD 11.53 Billion |

| Market Size (2031) | USD 16.62 Billion |

| Growth Rate (2026 - 2031) | 7.57% CAGR |

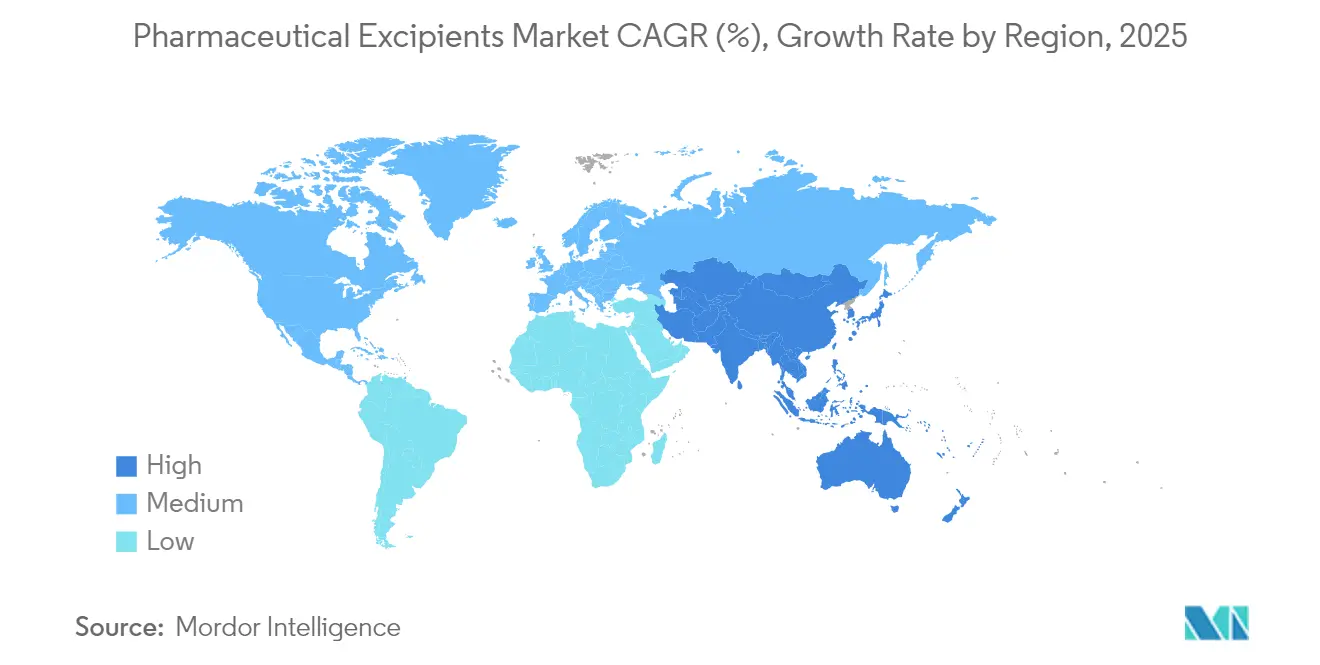

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Excipients Market Analysis by Mordor Intelligence

The pharmaceutical excipients market size is expected to grow from USD 10.72 billion in 2025 to USD 11.53 billion in 2026 and is forecast to reach USD 16.62 billion by 2031 at 7.57% CAGR over 2026-2031. Robust expansion stems from the growing use of sophisticated drug-delivery platforms, the shift toward continuous manufacturing, and rising demand for excipients that stabilize high-potency active ingredients. Polymer-based processing aids suited to twin-screw granulation and hot-melt extrusion underpin formulation efficiencies, while biosimilar proliferation elevates the need for protein-friendly stabilizers. Manufacturers are relocating production to cost-efficient regions to mitigate supply-chain risk and leverage local sourcing advantages, especially across Asia-Pacific, which supports a diversified supplier base and competitive pricing.

Key Report Takeaways

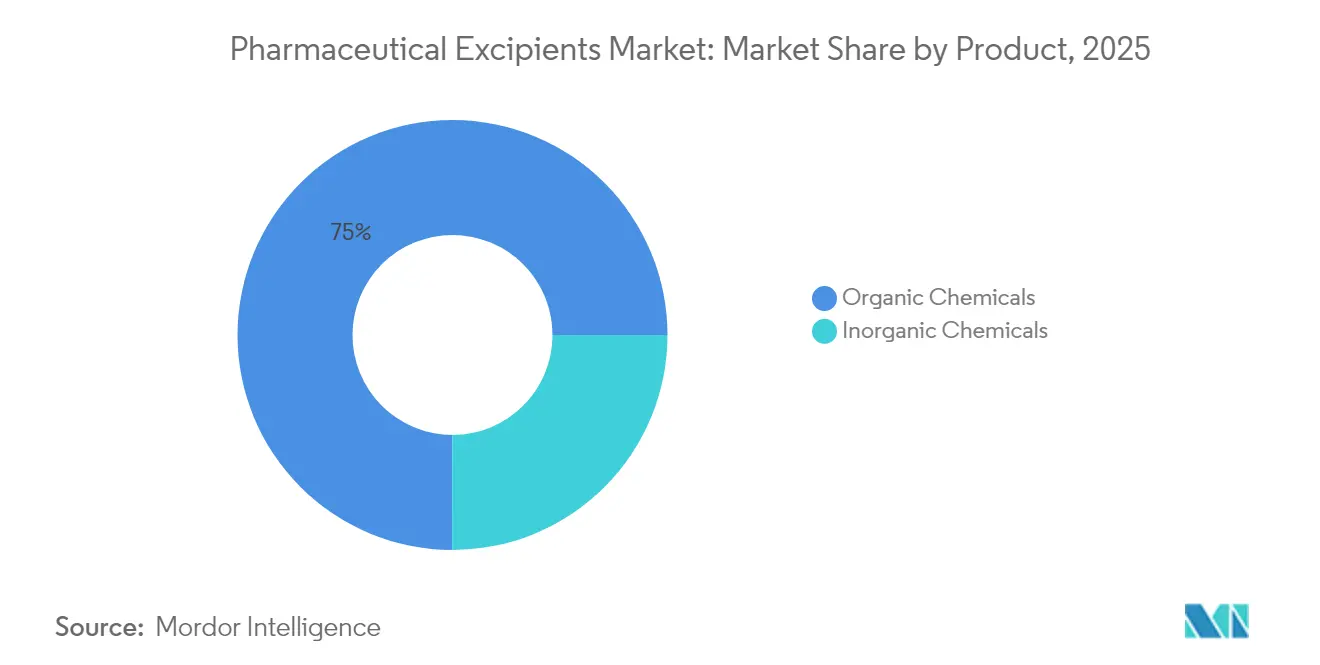

- By product type, organic chemicals accounted for 74.97% of the 2025 pharmaceutical excipients market share, while inorganic halites are forecast to register the strongest CAGR of 7.41% through 2031.

- By functionality, sustained-release agents are projected to advance at a high single-digit CAGR of 7.12%, whereas fillers and diluents retained the largest 2025 volume share at 32.12% of the pharmaceutical excipients market size.

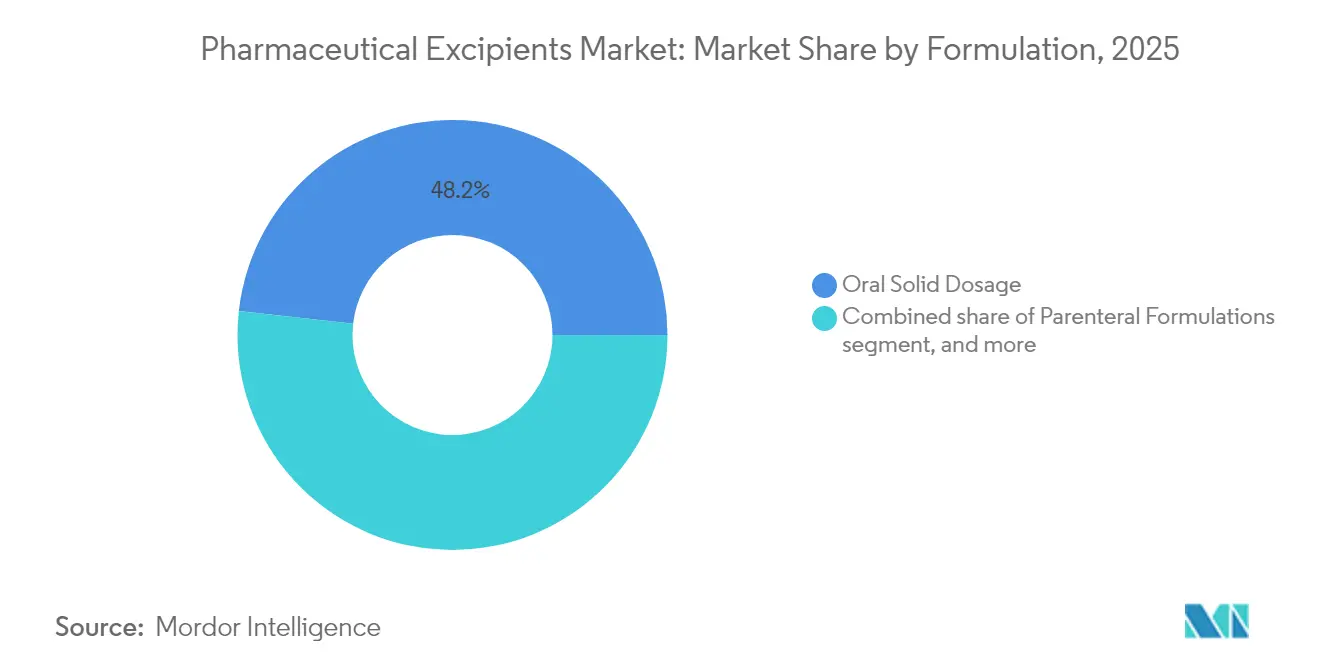

- By formulation, parenteral is projected to deliver 8.01% of CAGR from 2026 to 2031, outpacing tablets even though oral solids still held 48.22% of 2025 demand.

- By source, plant-based materials achieved a 31.76% share of the pharmaceutical excipients market in 2025, reflecting heightened sustainability and clean-label mandates.

- Regionally, Europe led with 37.26% of 2025 revenue; the Middle East is on track for a 6.34% CAGR between 2026 and 2031, the fastest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Excipients Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multifunctional novel excipients for high-potency APIs | +1.2% | North America & EU; global adoption | Medium term (2–4 years) |

| Biopharmaceutical excipients supporting biosimilar expansion | +1.8% | North America & Asia-Pacific | Long term (≥ 4 years) |

| Growth in orally disintegrating tablets boosting superdisintegrants | +0.9% | Developed markets worldwide | Short term (≤ 2 years) |

| Continuous manufacturing requiring polymer-based aids | +1.4% | North America & EU; expanding in Asia-Pacific | Medium term (2–4 years) |

| Formulation outsourcing relocation to India | +0.8% | Asia-Pacific core; spill-over to MEA | Long term (≥ 4 years) |

| Preference for plant-derived excipients | +0.7% | Global; regulatory push in EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rise of Multifunctional Novel Excipients for High-Potency APIs

Formulators working with potent oncology and immunology drugs now demand excipients that combine binding, disintegration, and flow-enhancing roles in one material[1]Chirag Parmar, “Co-Processed Excipients for High-Potency APIs,” Expert Opinion on Drug Delivery, tandfonline.com. Co-processed platforms reduce unit operations, lower dust exposure, and deliver uniform content, making them attractive for continuous lines. Regulatory dossiers remain challenging because safety data must cover combined functionalities, which lengthens approval cycles. North American innovators hold early know-how, yet European manufacturers are rapidly scaling pilot plants to capture demand. Over the medium term, rising potency thresholds in pipeline molecules will keep multifunctional grades at the center of purchasing decisions.

Surging Demand for Biopharmaceutical Excipients Supporting Biosimilars Expansion

Biosimilar launches following monoclonal antibody patent cliffs have lifted global requirements for high-purity sugars, amino acids, and surfactants that guard protein structure during processing[2]Dorra Lahmo, “Biosimilar Wave Spurs Excipients Demand,” BioPharm International, biopharminternational.com. Suppliers often co-develop stabilizers to match reference biologics’ profiles while demonstrating bioequivalence with different compositions. Liquid formulations for at-home autoinjectors further magnify stability demands, making low-endotoxin and low-aggregate excipients critical. Costs remain high because multi-column chromatography and aseptic filtration add complexity, yet large-scale capacity in Asia-Pacific is narrowing price gaps. Long-term growth hinges on maintaining stringent microbial specs as volumes ramp.

Growth in Orally Disintegrating Tablets Driving Superdisintegrants Consumption

Pediatric and geriatric adherence programs motivate formulators to design tablets that disperse within 30 seconds, pushing uptake of crospovidone and sodium starch glycolate. The FDA’s first 3-D-printed ODT approvals demonstrate how additive manufacturing meets personalization goals. Superdisintegrants must now balance rapid swelling with mechanical strength to survive downstream packaging. Natural variants sourced from sago starch offer clean-label benefits and address petrochemical solvent concerns. Short-term growth is concentrated in Europe and the United States, yet emerging markets are quickly adopting ODTs for over-the-counter lines.

Shift Toward Continuous Manufacturing Requiring Polymer-Based Processing Aids

Regulators actively encourage continuous lines that deliver real-time release testing and fewer deviations, prompting demand for microcrystalline cellulose grades optimized for twin-screw granulation. Excipients require narrow particle-size distribution and consistent moisture sorption to fit small operating windows. Suppliers are investing in process-analytical-technology toolkits to help customers integrate materials seamlessly. Adoption began in North America and Western Europe but is now accelerating among Indian contract development and manufacturing organizations. Continuous processing is expected to reshape raw-material specifications industry-wide over the next four years.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory variability across regions | -1.1% | Global; emerging markets most affected | Long term (≥ 4 years) |

| High purity requirements escalating costs | -0.8% | Developed markets worldwide | Medium term (2–4 years) |

| Agricultural commodity price volatility | -0.6% | Global; dependent on sourcing mix | Short term (≤ 2 years) |

| Toxicological concerns over petrochemical residuals | -0.4% | EU & North America; spreading globally | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Regulatory Variability Across Regions Limiting Global Launch Harmonization

Differing dossier formats and excipient listing rules among the FDA, EMA, and regulators in India, Brazil, and China prolong development timelines. The International Council for Harmonisation continues to draft Q14 and Q2(R2) guidelines, yet risk-assessment philosophies vary, especially for multifunctional materials. Companies maintain region-specific master files, inflating administrative overhead and delaying worldwide rollouts. Variability is especially burdensome for small and midsize innovators that lack dedicated regulatory teams. Harmonization progress remains slow, suggesting the restraint will linger into the next decade.

Toxicological Concerns Over Residual Solvents in Petrochemical Excipients

Authorities scrutinize polyethylene glycol, povidone, and other petroleum-derived materials for potential ethylene glycol contamination, prompting United States Pharmacopeia monograph revisions that tighten impurity limits[3]United States Pharmacopeia, “Revision Bulletin: Polyethylene Glycol 40 Castor Oil,” usp.org. Europe’s precautionary principle magnifies risk perception, encouraging a slow pivot away from certain synthetic vehicles. Compliance pushes suppliers toward costly revalidation programs and drives reformulation projects across finished-dose lines. Although the impact on CAGR is smaller than other restraints, ongoing safety assessments sustain medium-term headwinds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Dominance of Organic Chemicals Amid Inorganic Innovation

Organic chemicals made up 74.97% of pharmaceutical excipients market share in 2025, underscoring continued reliance on cellulose, lactose, and starch derivatives for tableting efficiency. The pharmaceutical excipients market size linked to organic categories is expanding steadily because cellulosics match clean-label preferences and retain robust compendial support. Continuous manufacturing further elevates demand for polymer grades engineered to withstand shear and moisture variability. In contrast, inorganic halites such as sodium chloride and potassium chloride display the quickest 7.41% CAGR through 2031, owing to their role in osmotic pumps and modified-release cores. These mineral salts offer stable ionic strength profiles critical for high-load APIs in specialized dosage forms.

Innovation is creating cross-category synergies: oleochemicals derived from fatty acids bridge parenteral and oral use by offering low immunogenicity alongside lubricity advantages. Protein-based stabilizers, though smaller by volume, command premium pricing because they avert aggregation in biologics. Formulators scrutinize petrochemicals for solvent residues, nudging them toward bio-based analogs with equivalent flow properties. As continuous lines proliferate, excipients with tight PSD controls and low endotoxin profiles will dominate procurement lists.

By Functionality: Fillers Led While Sustained-Release Agents Accelerate

Fillers retained 32.12% share of the pharmaceutical excipients market in 2025, reflective of their indispensable role in achieving target tablet weights and mechanical strength. Lactose monohydrate and microcrystalline cellulose remain default options, yet DMF-graded mannitol and isomalt gain traction where moisture sensitivity persists. The rise of controlled-release therapies elevates sustained-release polymers, which are forecast to grow at 7.12% CAGR to 2031, highlighting patient-centric adherence objectives. These hydrophilic matrices moderate plasma peaks, supporting chronic disease regimens.

Binders designed for twin-screw wet granulation deliver consistent viscosity under elevated shear, meeting continuous-processing specs. Superdisintegrants graduate from simple swelling agents to critical performance determinants in fast-dissolve formats. Meanwhile, coatings evolve from basic protective films to multifunctional layers providing enteric resistance, taste masking, and brand differentiation. Co-processed excipients blur functionality boundaries by merging binding and disintegration, simplifying bill-of-materials while easing regulatory change control.

By Formulation: Oral Dominance Challenged by Parenteral Growth

Oral solids accounted for 48.22% of pharmaceutical excipients market size in 2025, anchored by cost-effective manufacturing and patient familiarity. Tablets, capsules, and multiparticulates benefit from mature regulatory frameworks and high-speed processing lines. However, parenteral formulations exhibit the fastest 8.01% CAGR through 2031 because mAbs, recombinant proteins, and RNA therapeutics require injectable routes for bioavailability. Excipients for injections must be pyrogen-free and isotonic, driving higher purity specifications and specialized filtration steps.

Topical and transdermal platforms attract niche investments, leveraging permeation enhancers and bioadhesive polymers to deliver systemic dosing without needles. Pulmonary formulations witnessed renewed focus after mRNA vaccine dry-powder feasibility studies, spurring demand for low-density carriers such as mannitol. Ophthalmic solutions maintain strict microbial limits and particulate controls, keeping the category relatively insulated from raw-material substitutions. As self-administration devices proliferate, all formulation types will rely on excipients that support viscosity modulation and long-term stability.

By Source: Plant-Based Leadership Alongside Synthetic Precision

Plant-derived materials captured 31.76% of pharmaceutical excipients market share in 2025, propelled by sustainability campaigns and consumer trust. Corn-based dextrose, wheat starch, and microcrystalline cellulose gain certification under non-GMO and allergen-free programs, giving them a marketing edge. Synthetic excipients, though projected for the briskest 6.91% CAGR, shine where reproducible rheology and batch-to-batch uniformity are mandatory, particularly in complex injectables.

Animal-origin gelatin sees erosion due to halal, kosher, and porcine-free preferences, while marine polysaccharides such as chitosan carve out roles in wound dressings and mucoadhesive nasal sprays. Mineral sources gain relevance as formulators phase out titanium dioxide, turning to calcium carbonate for opacity and color masking. The pharmaceutical excipients industry balances ecological commitments with stringent performance benchmarks, fostering parallel growth tracks for botanical and engineered materials.

Geography Analysis

North America maintained 36.88% share of the pharmaceutical excipients market in 2025, boosted by a dense cluster of innovators, rigorous regulatory oversight, and early adoption of continuous processing. Suppliers capture premium margins on parenteral-grade polysorbates, cyclodextrins, and tailored celluloses used in biologics. Despite leadership, manufacturers face logistics vulnerabilities highlighted by recent supply shocks, prompting contingency sourcing initiatives.

Asia-Pacific is forecast to log a 6.18% CAGR through 2031, spearheaded by India’s formulation outsourcing surge and China’s scale-up of domestic biologic lines. Contract development and manufacturing organizations in Hyderabad and Suzhou secure multinational contracts that mandate local excipient supply under global quality standards. Investments in spray-dried mannitol, HPMC, and poloxamer plants support regional autonomy. Simultaneously, governments direct incentives toward compliance upgrades, closing historical quality gaps.

Europe represents a mature yet innovative territory, pioneering clean-label policies and biodegradable polymer research that ripple through global standards. Regulatory clarity enables swift uptake of plant-derived carriers and non-petrochemical lubricants. Latin America and the Middle East & Africa show incremental demand as national pharmacopeias toughen import regulations, catalyzing local production ventures for starches and calcium phosphates. Currency-risk mitigation and shorter lead times make domestic sourcing attractive, gradually reshaping trade flows.

Competitive Landscape

Moderate fragmentation characterizes the pharmaceutical excipients market, with leading multinationals leveraging process expertise, global plants, and broad dossiers to defend share. BASF SE, Ashland Global Holdings, and DuPont de Nemours compete by offering end-to-end technical service portals, accelerated sample shipping, and regional application labs. Their integrated supply chains support quick scale-ups, a vital differentiator as continuous processing shortens commercialization timelines.

Strategic consolidation is redefining competitive contours. Roquette’s USD 2.85 billion purchase of IFF Pharma Solutions in 2024 merged two cellulose and mannitol powerhouses, intensifying rivalry in oral-solids excipients. Meanwhile, BASF’s digital formulation tools ZoomLab and MyProductWorld integrate predictive models that trim formulation cycles for clients, embedding the supplier deeper into development pipelines. Collaboration models also proliferate; Avantor linked with Rubicon Research to co create gastro-retentive platforms that enhance drug residence time in the stomach.

New entrants target specialty niches such as low-endotoxin sugars or marine-based polymers, yet high capital barriers and stringent GMP audits shelter incumbents. Commodity suppliers face margin pressure from agricultural price swings and regulatory demands for traceability. Market participants who combine backward integration with robust quality systems stand to weather volatility better than import-reliant distributors.

Pharmaceutical Excipients Industry Leaders

BASF SE

Ashland Global Holdings Inc.

DuPont de Nemours Inc.

Roquette Frères SA

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: FDA draft guidance supported CBE-30 submissions when replacing color additives such as titanium dioxide.

- April 2025: European Pharmacopoeia Supplement 11.7 required Certificate of Suitability updates across several excipient classes.

- January 2025: The FDA finalized interim policy on compounding with bulk drug substances, increasing supply-chain oversight.

- October 2024: Clariant launched eight new VitiPure and Polyglykol excipients targeting bioavailability challenges.

- October 2024: Lotte Fine Chemical signed a USD 740 million, 10-year distribution deal with Colorcon for pharmaceutical cellulose products.

Global Pharmaceutical Excipients Market Report Scope

As per the scope of the report, pharmaceutical excipients are the pharmacologically inactive substances in the formulation that aid in manufacturing the finished pharmaceutical product. They also help transport the active pharmaceutical substance to the site of action in the body. The pharmaceutical excipients market is segmented by product (inorganic chemicals and organic chemicals), functionality (fillers and diluents, binders, suspension, and viscosity agents, coatings, flavoring agents, disintegrants, colorants, preservatives, and other functionalities), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Organic Chemicals | Carbohydrates |

| Petrochemicals | |

| Oleochemicals | |

| Proteins | |

| Other Organic Chemicals | |

| Inorganic Chemicals | Halites |

| Metal Oxides | |

| Silicates | |

| Other Inorganic Chemicals |

| Fillers & Diluents |

| Binders |

| Suspension and Viscosity Agents |

| Coatings (Film & Enteric) |

| Flavoring Agents |

| Disintegrants |

| Colorants |

| Preservatives |

| Other Functionalities |

| Oral Solid Dosage Forms |

| Parenteral Formulations |

| Topical & Transdermal |

| Pulmonary/Inhalation |

| Ophthalmic |

| Others (Sublingual, Buccal, etc.) |

| Plant-based |

| Animal-based |

| Synthetic |

| Mineral-based |

| Marine-based |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Organic Chemicals | Carbohydrates |

| Petrochemicals | ||

| Oleochemicals | ||

| Proteins | ||

| Other Organic Chemicals | ||

| Inorganic Chemicals | Halites | |

| Metal Oxides | ||

| Silicates | ||

| Other Inorganic Chemicals | ||

| By Functionality | Fillers & Diluents | |

| Binders | ||

| Suspension and Viscosity Agents | ||

| Coatings (Film & Enteric) | ||

| Flavoring Agents | ||

| Disintegrants | ||

| Colorants | ||

| Preservatives | ||

| Other Functionalities | ||

| By Formulation | Oral Solid Dosage Forms | |

| Parenteral Formulations | ||

| Topical & Transdermal | ||

| Pulmonary/Inhalation | ||

| Ophthalmic | ||

| Others (Sublingual, Buccal, etc.) | ||

| By Source | Plant-based | |

| Animal-based | ||

| Synthetic | ||

| Mineral-based | ||

| Marine-based | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the pharmaceutical excipients market?

The pharmaceutical excipients market was valued at USD 11.53 billion in 2026, with growth projected at a 7.57% CAGR to 2031.

Why are plant-based excipients gaining share?

Sustainability goals, clean-label requirements, and traceable supply chains have lifted demand for cellulose, alginates, and other renewable excipients, raising plant-based share to 31.76% in 2025.

What is driving demand for multifunctional excipients?

High-potency APIs benefit from cyclodextrin derivatives and co-processed blends that improve solubility and handling while cutting formulation steps, accelerating clinical timelines.

How is continuous manufacturing influencing excipient specifications?

Continuous lines require excipients with consistent flow and thermal profiles; low-viscosity hydroxypropylcellulose and similar polymers enable real-time release and reduce batch variability.

What challenges do excipient suppliers face in meeting parenteral purity standards?

High-purity injectable grades demand multi-stage purification and exhaustive impurity testing, raising production costs by up to 300% over oral grades.

Page last updated on: