Sequencing Reagents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

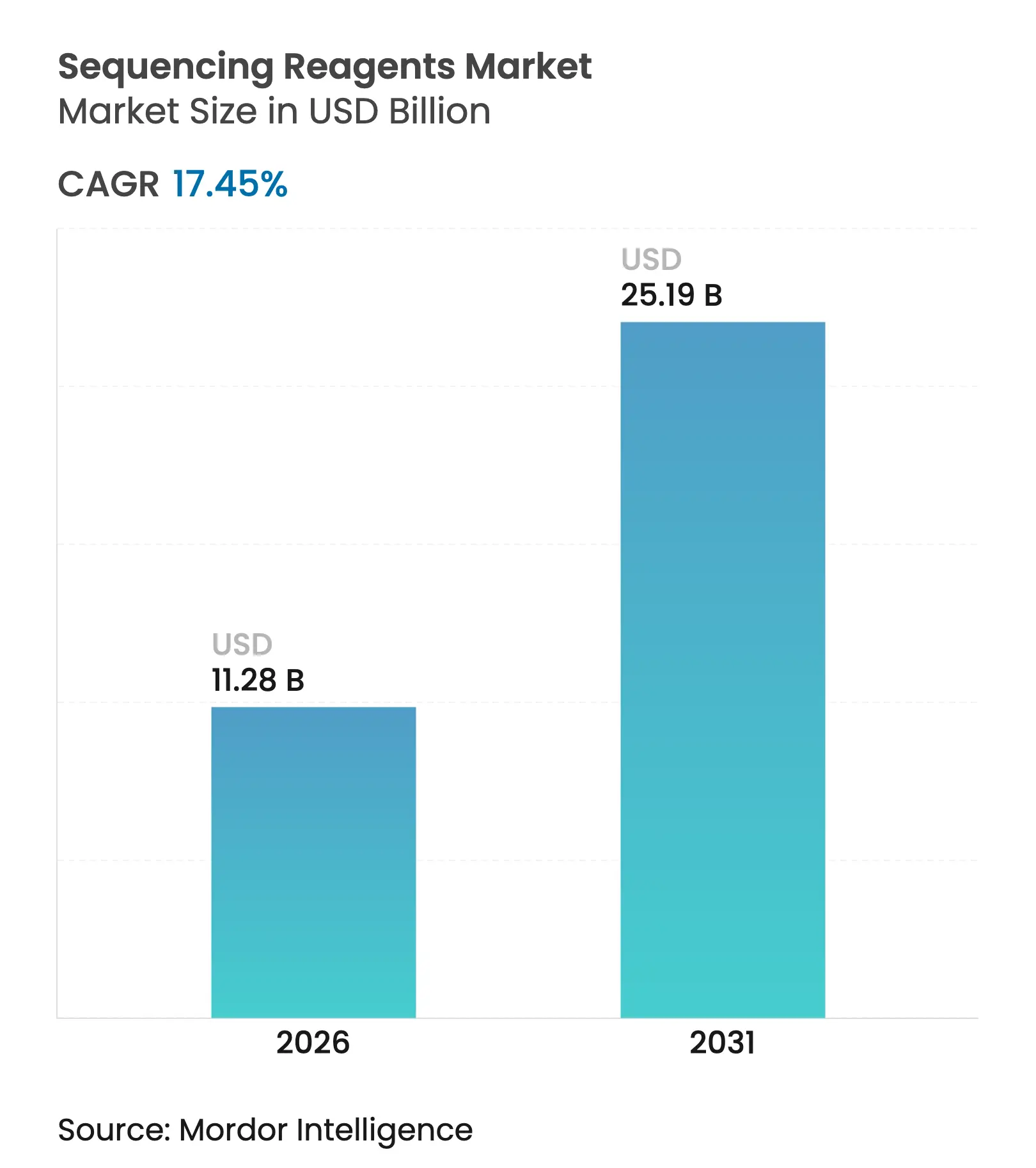

| Market Size (2026) | USD 11.28 Billion |

| Market Size (2031) | USD 25.19 Billion |

| Growth Rate (2026 - 2031) | 17.45 % CAGR |

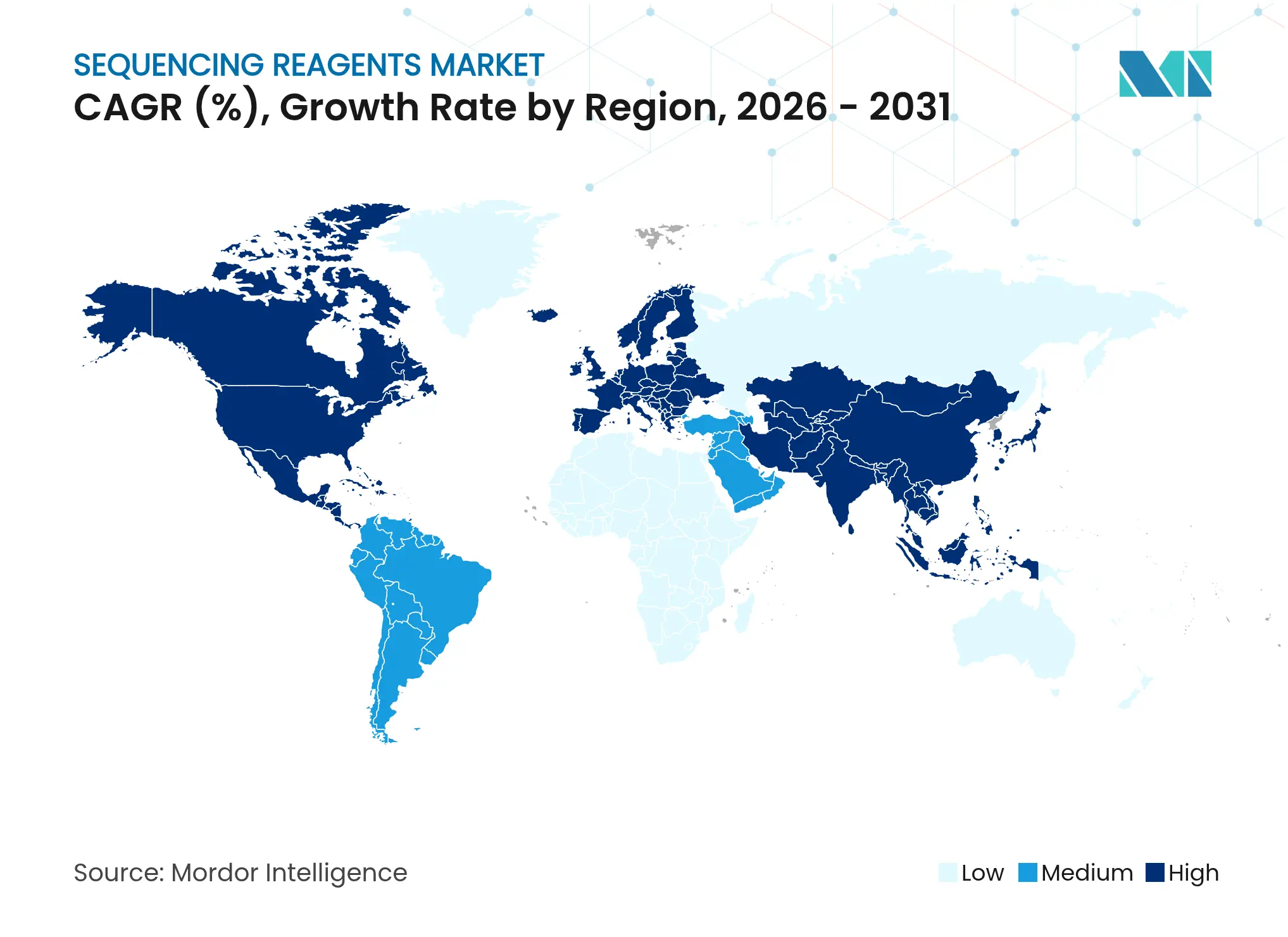

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Sequencing Reagents Market Analysis by Mordor Intelligence

The sequencing reagents market size is expected to grow from USD 9.6 billion in 2025 to USD 11.28 billion in 2026 and is forecast to reach USD 25.19 billion by 2031 at 17.45% CAGR over 2026-2031. Falling per-genome costs, wider clinical adoption across oncology and rare-disease testing, and new reagent chemistries that compress turnaround times are the primary engines of this double-digit growth. Library-prep kits remain indispensable because every sample must be converted into a sequencing-ready format; meanwhile, AI-driven enzymatic mixes are shaving hours off traditional protocols, letting high-throughput laboratories process larger daily volumes without extra staff. Demand is also receiving a structural lift from large population-genomics initiatives in Europe, Asia, and North America that lock in multi-year procurement contracts and stabilize pricing for bulk reagent purchases. Competitive pressure is intensifying as incumbents such as Illumina face rivals introducing ultra-fast platforms; Roche’s Sequencing by Expansion system offers seven whole genomes in just one hour and could pull the overall sequencing reagents market toward even faster chemistry cycles.

Key Report Takeaways

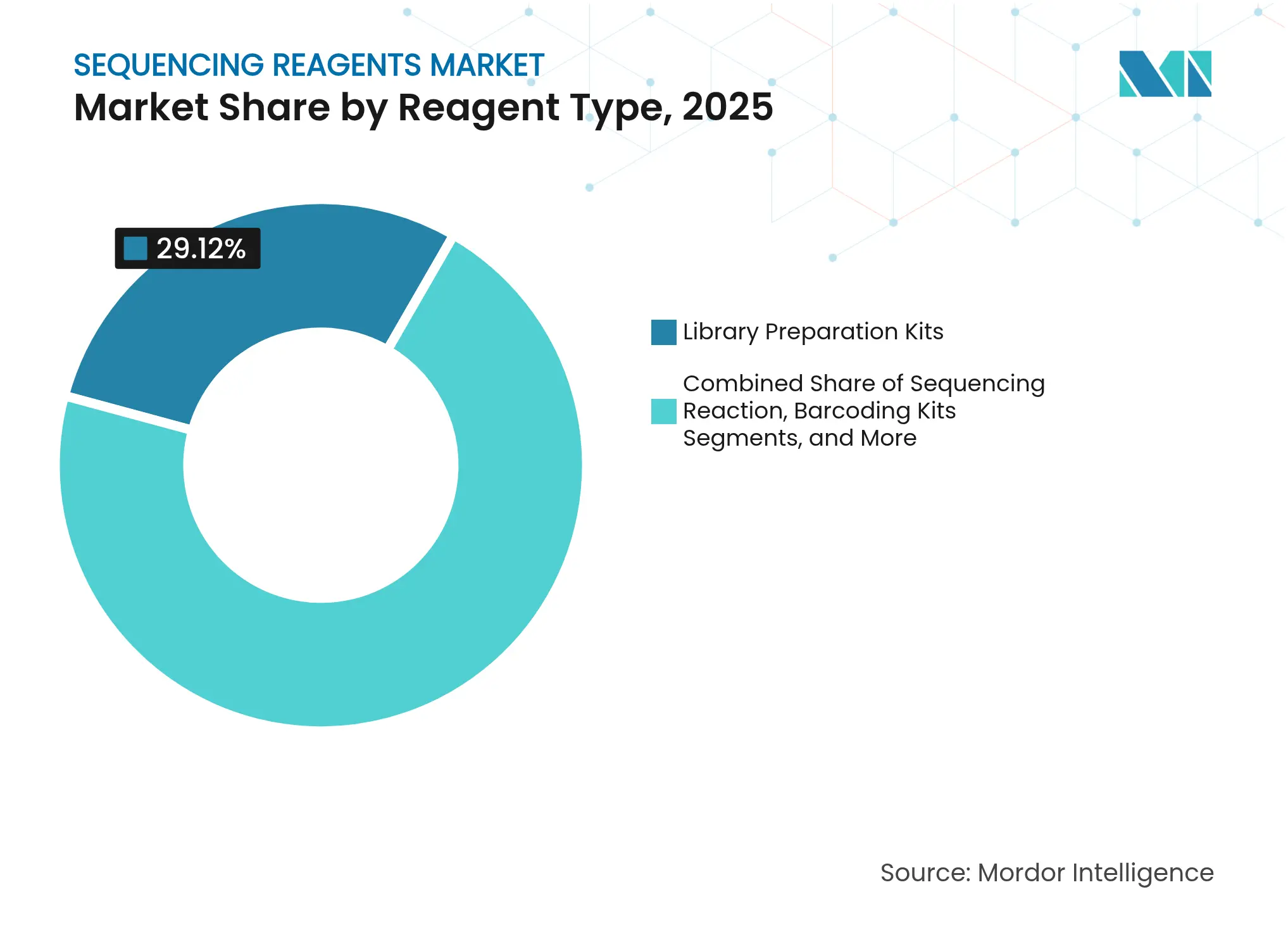

- By reagent type, library-preparation kits led with 29.12% of the sequencing reagents market share in 2025, whereas barcoding/indexing kits are set to advance at a 15.3% CAGR through 2031.

- By sequencing technology, next-generation sequencing held 49.25% of the sequencing reagents market size in 2025; single-cell/spatial and nanopore chemistries are expanding at 22.6% CAGR.

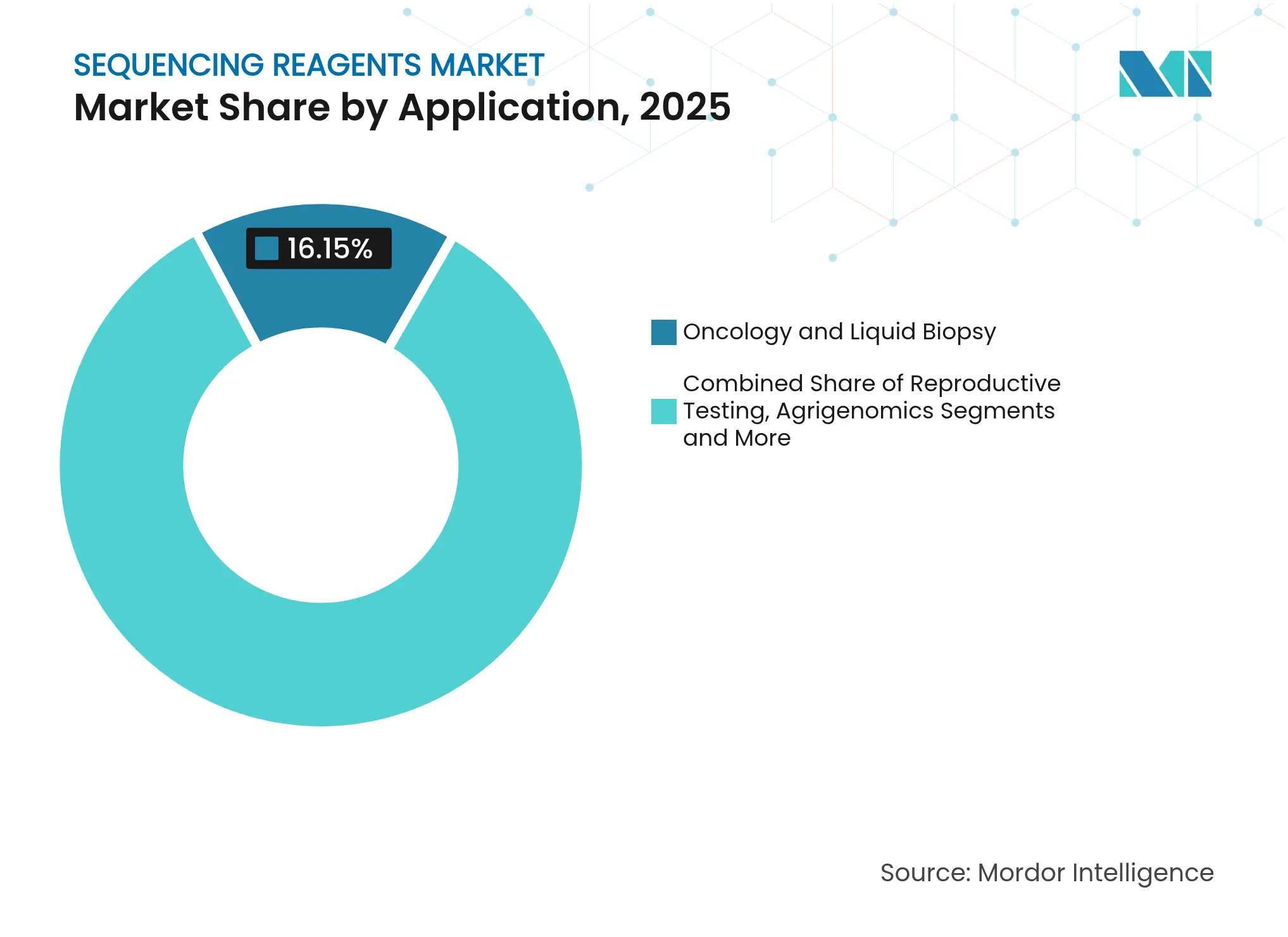

- By application, oncology and liquid biopsy accounted for a 16.15% share of the sequencing reagents market size in 2025, while oncology MRD and microbiome uses are projected to accelerate at a 21.05% CAGR.

- By geography, North America commanded 34.18% of revenue in 2025, yet Asia-Pacific is forecast to record the fastest regional CAGR of 12.75% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sequencing Reagents Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Declining NGS Cost Curve Accelerates Clinical Adoption Declining NGS Cost Curve Accelerates Clinical Adoption | +4.20% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+4.20% | Geographic Relevance:Global, with strongest impact in North America & Europe | Impact Timeline:Medium term (2-4 years) |

Surge In Large-Scale Population Genomics Programmes Surge In Large-Scale Population Genomics Programmes | +3.80% | Global, led by Europe & Asia-Pacific | Long term (≥ 4 years) | |||

Oncology Companion-Diagnostic Pipelines Expanding Oncology Companion-Diagnostic Pipelines Expanding | +3.10% | North America & Europe core, expanding to APAC | Medium term (2-4 years) | |||

Sample-Barcoding Chemistries Enabling Ultra-High-Throughput Screens Sample-Barcoding Chemistries Enabling Ultra-High-Throughput Screens | +2.70% | Global, with early adoption in North America | Short term (≤ 2 years) | |||

AI-Designed Enzymatic Kits Shortening Library-Prep Times AI-Designed Enzymatic Kits Shortening Library-Prep Times | +2.40% | North America & Europe, spill-over to APAC | Medium term (2-4 years) | |||

COVID-Era Installed NGS Base Driving Consumables Pull-Through COVID-Era Installed NGS Base Driving Consumables Pull-Through | +1.60% | Global, strongest in developed markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Declining NGS Cost Curve Accelerates Clinical Adoption

Whole-genome sequencing has breached the USD 500 threshold, a level at which hospitals can justify replacing multiple single-gene assays with one comprehensive test. Illumina’s NovaSeq X aims to push pricing near USD 200 per genome, converting cost savings into broader diagnostic menus. Comparative studies in metastatic lung cancer show that next-generation sequencing reduces per-patient costs by more than 50% while cutting therapy-selection delays from weeks to days. Clinical pathology labs have consequently shifted budgets toward larger multipanel workflows that rely on higher volumes of consumables. As payers recognize the downstream savings from faster, more accurate diagnoses, reimbursement coverage is widening for tumor-profiling tests. These converging factors keep reagent pull-through strong and elevate the sequencing reagents market as routine diagnostics standardize on NGS panels rather than legacy PCR.

Surge in Large-Scale Population Genomics Programmes

Europe’s Genome of Europe initiative is channeling EUR 45 million into a network of 51 institutes that will sequence 100,000 citizens, locking in multiyear reagent demand under harmonized protocols.[1]European Commission Health division, “Genome of Europe factsheet,” ec.europa.eu Private–public efforts are equally sizable: four biopharma companies have pledged USD 80 million to sequence 500,000 genomes of African ancestry, embedding long-term contract volumes for suppliers.[2]Warren Cornwall, “African ancestry sequencing initiative,” science.org Proposed megaprojects such as Human Genome Project II (targeting 1% of the global population) could consume billions of library-prep reactions, indexing primers, and quality-control kits. These initiatives also require specialized chemistries able to capture structural variants, increasing the average spend per sample. Bulk purchasing drives economies of scale that widen adoption among smaller regional labs participating in consortium studies. As a result, population genomics will become a strategic anchor for the sequencing reagents market over the next decade.

Oncology Companion-Diagnostic Pipelines Expanding

Targeted therapies approved in 2025 almost universally carry a genomic companion test, embedding reagents into the drug-development value chain. Thermo Fisher’s Genexus platform delivers same-day tumor profiles for the myeloMATCH trial, aligning sequencing run lengths with oncologist treatment windows. Liquid-biopsy kits are surging as minimally invasive monitoring tools, and the U.S. liquid-biopsy segment alone is predicted to triple this decade. Oxford Nanopore’s cell-free DNA workflows extend diagnostic reach to ultralong reads, requiring proprietary motor proteins and modified nucleotides. Pharmaceutical sponsors favor FDA-cleared reagent systems to derisk regulatory submission, so kits that secure clearance gain embedded demand for the life of the drug. Consequently, oncology remains the single largest revenue generator within the sequencing reagents market.

Sample-Barcoding Chemistries Enabling Ultra-High-Throughput Screens

Modern multiplexing methods allow hundreds of samples to be pooled in a single sequencing lane without index hopping. New England Biolabs offers 96 unique dual indexes plus combinatorial sets that raise barcode counts above 480. SeqWell’s LongPlex supports 8 kb inserts on PacBio instruments, broadening multiplexing to long-read workflows. Diagnostic groups have used species-specific RNA barcodes to identify influenza strains with nearly 97% recall rates at a cost lower than RT-PCR. AI-assisted barcode design cuts development cycles and flags potential cross-talk in silico, raising first-pass success rates. These advances slash reagent spend per sample yet boost total reagent volumes because far more samples are processed. High-throughput screens, therefore, amplify the overall sequencing reagents market trajectory.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Limited Reimbursement For Extensive Genomic Testing Limited Reimbursement For Extensive Genomic Testing | -2.80% | North America & Europe, varying by healthcare system | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-2.80% | Geographic Relevance:North America & Europe, varying by healthcare system | Impact Timeline:Medium term (2-4 years) |

Data-Privacy Regulations Raising Compliance Costs Data-Privacy Regulations Raising Compliance Costs | -1.90% | Global, strongest in Europe & North America | Long term (≥ 4 years) | |||

Global DNTP-Grade Raw-Material Shortages Global DNTP-Grade Raw-Material Shortages | -1.60% | Global, supply chain dependent regions | Short term (≤ 2 years) | |||

Wet-Lab Talent Deficit In Emerging Markets Wet-Lab Talent Deficit In Emerging Markets | -1.30% | Asia-Pacific & MEA, limited to emerging markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Limited Reimbursement for Extensive Genomic Testing

Insurance coverage lags scientific progress, and many multi-gene panels still fall outside payer benefit policies.[3]National Human Genome Research Institute, “Coverage landscape for genomic tests,” genome.govMedicare Advantage plans reimburse only tests deemed “reasonable and necessary,” excluding innovative panels without long-term outcomes data. Coding complexity under molecular pathology guidelines produces claim denials that erode laboratory margins and slow adoption. Liquid-biopsy assays illustrate the hurdle; economic models suggest costs must drop by two-thirds before payers view them as cost-effective for colorectal screening. Smaller community labs often lack billing specialists, forcing them to cap their test offerings. Until reimbursement frameworks keep pace with the clinical value of NGS, this restraint will temper the otherwise fast-growing sequencing reagents market.

Data-Privacy Regulations Raising Compliance Costs

The EU’s GDPR and emerging U.S. state-level laws treat genomic data as uniquely sensitive, compelling labs to invest heavily in encryption, access controls, and audit trails. FDA plans to bring laboratory-developed tests under IVD regulations, adding evidence requirements that may double validation spend for new assays. Cross-border data-transfer rules complicate multi-center trials, necessitating localized servers and duplicate analysis pipelines. The 23andMe breach in 2023 heightened public scrutiny, leading to steeper penalties and reputational risks for any mishandling of genetic data. Compliance budgets siphon funds away from reagent purchases, especially for resource-constrained institutions. Over time, stringent privacy mandates could slow global harmonization of workflows and pose a material headwind for the sequencing reagents market.

Segment Analysis

By Reagent Type: Library Preparation Dominates Despite Indexing Innovation

The sequencing reagents market size allocated to library-preparation kits stood at 29.12% of 2025 revenue, underscoring their universal role in converting DNA or RNA into platform-compatible fragments. Laboratories cannot bypass this step regardless of whether they run short-read or long-read instruments, making demand highly inelastic. Template-preparation chemistries for amplicon or long-insert workflows and sequencing-reaction mixes remain crucial for specific protocols, while control kits safeguard run quality. PCR and amplification reagents still underpin targeted assays that require enrichment or low-input compensation, and their volumes scale directly with oncology and infectious-disease testing. Supplier competition focuses on reduced hands-on time; AI-optimized bead-based clean-ups now consolidate multiple wash steps into one, halving bench work and reinforcing vendor lock-in.

The fast-rising barcoding/indexing subcategory will post a 15.3% CAGR through 2031 as population studies and hospital networks lean on multiplexing to curb per-sample costs. Dual-index products from New England Biolabs already mitigate index hopping for short-read runs, while seqWell’s kits extend similar protections to long-read platforms. Species-specific barcodes are spawning diagnostic niches such as multiplexed viral surveillance with accuracy exceeding 96%. AI-aided primer design shortens development cycles and raises yields, creating a positive feedback loop of efficiency and throughput. As a result, indexing reagents capture budget share from legacy single-sample workflows, yet they also expanded total consumable usage, reinforcing the growth outlook for the sequencing reagents market.

Note: Segment shares of all individual segments available upon report purchase

By Sequencing Technology: NGS Leadership Challenged by Emerging Platforms

Next-generation sequencing platforms accounted for 49.25% of the sequencing reagents market share in 2025, benefiting from more than a decade of installed instruments, validated assays, and reimbursement precedents. The reagent ecosystem around SBS chemistry enjoys economies of scale that keep per-base pricing low, supporting everything from germline testing to broad oncology panels. Sanger methods persist in confirmatory roles, while third-generation single-molecule approaches serve niche applications needing ultralong reads. Established NGS workflows also carry a pool of trained technicians and bioinformaticians, streamlining adoption for new laboratories.

Yet single-cell and spatial chemistries are scaling at 22.6% CAGR and could transform the competitive order by 2031. Illumina’s whole-transcriptome spatial kit delivers cell-level resolution on standard slide formats. Microfluidic droplet systems encapsulate individual cells for barcoded sequencing in minutes, driving demand for high-sensitivity reverse-transcriptase mixes and ligation enzymes. Roche’s Sequencing by Expansion promises >99.80% accuracy and seven genomes per hour, potentially catalyzing a new wave of ultra-rapid clinical sequencing. Oxford Nanopore has achieved telomere-to-telomere assemblies with improved pore proteins, opening multiomic horizons that require unique motor enzymes and adapter chemistries. These developments ensure the sequencing reagents market remains dynamic, with technology shifts forcing suppliers to refresh portfolios continuously.

By Application: Oncology Focus Drives Specialized Reagent Development

Oncology and liquid-biopsy uses held a 16.15% share of the sequencing reagents market size in 2025 as tumor profiling became a standard clinical practice. Comprehensive genomic profiling feeds precision-medicine algorithms that match patients to targeted therapies, cementing reagent demand for gene-panel enrichment and molecular barcodes that handle low-allele-frequency variants. Clinical diagnostics more broadly covers hereditary-disease panels, pharmacogenomics, and infectious-disease tests, each with specific reagent needs but unified by accuracy and turnaround-time imperatives. Reproductive health and agri-genomics represent stable, regulation-driven niches, whereas forensics depends on chain-of-custody compliant chemistries.

Oncology minimal-residual-disease and microbiome applications will grow 21.05% annually, pushing vendors to engineer kits sensitive enough to detect variant allele frequencies below 0.1% in circulating DNA. Oxford Nanopore’s direct cfDNA sequencing supports methylation calling, adding epigenomic layers to MRD tracking and requiring specialized adapter mixes. Gut-microbiome research is shifting toward integrated multi-omic protocols merging genomic, transcriptomic, and metabolomic data, prompting suppliers to bundle nucleic-acid extraction, library prep, and barcoding reagents in unified kits. The forensic microbiology field is likewise broadening beyond pathogen ID to include bioterror surveillance, demanding reagents validated under ISO-accredited workflows. These diverse yet converging application trends keep the sequencing reagents market on a steep growth trajectory.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America generated 34.18% of 2025 revenue, anchored by extensive clinical adoption, large installed instrument fleets, and payer frameworks that cover many hereditary and oncology tests. The National Human Genome Research Institute devoted nearly one-third of its FY 2023 budget to data-science grants, subsidizing reagent usage in cutting-edge projects. MyeloMATCH, spanning more than 2,200 sites, relies on same-day genomic reporting, boosting daily consumption of rapid-prep kits. A private USD 80 million diversity initiative focusing on African ancestry further entrenches multi-year reagent orders. Still, reimbursement heterogeneity across commercial payers remains a headwind, moderating growth for smaller labs lacking negotiation leverage.

Europe combines strong public funding with strict data-privacy rules. The Genome of Europe allocates EUR 45 million to modernize sequencing centers across 27 nations, guaranteeing baseline demand for library-prep and indexing reagents under centralized procurement. Rare-disease networks leverage cross-border data sharing but must comply with GDPR, prompting heavy investment in compliant cloud environments and encryption-friendly reagent-tracking software. Structural variant detection and long-read chemistries find traction in academic centers targeting complex genomic disorders, gradually expanding the sequencing reagents market despite regulatory overhead.

Asia-Pacific is projected to post a 12.75% CAGR to 2031, the fastest worldwide. Baker McKenzie estimates regional healthcare outlays reaching USD 138 billion by 2027, a fertile backdrop for genomic medicine. BGI claims participation in more than half of global sequencing projects, reinforcing a domestic supply chain for enzymes, nucleotides, and flow cells. China’s push for self-reliant genomics instruments through firms such as MGI Tech generates local competition for Western vendors. Pacific Biosciences partners with Thai newborn-screening programs to embed HiFi sequencing at birth, illustrating how international suppliers localize value propositions. Combined, these factors ensure Asia-Pacific will inject significant incremental volumes into the sequencing reagents market over the forecast horizon.

Competitive Landscape

Market Concentration

The top five companies accounted for a significant market share of 2024 revenue, signaling moderate concentration. Illumina retains a large installed base but now contends with Roche’s Sequencing by Expansion platform, which processes seven genomes per hour at >99.80% accuracy and could redefine clinical turnaround benchmarks. Element Biosciences raised USD 277 million to expand its Aviti instruments from 40 to over 190 units, intensifying price competition at the mid-throughput tier. Thermo Fisher’s USD 3.1 billion acquisition of Olink folds 5,300 protein markers into its assay catalog, advancing a multiomic bundling strategy.

White-space opportunities abound in spatial transcriptomics and microbiome multi-omics, where startups develop purpose-built chemistries. Oxford Nanopore’s telomere-to-telomere assembly kits open ultra-long-read clinical applications that require proprietary motor proteins. Consolidation continues: Deerfield offered USD 20.00 per share for Singular Genomics, a 254% premium that underscores the strategic value of installed platforms even when revenue is still nascent. Regeneron’s acquisition of 23andMe assets during bankruptcy shows how genomic databases are prized for drug-discovery pipelines.

Regional players leverage local manufacturing to win procurement contracts, especially in China where government policy favors domestic sourcing. BGI’s scale allows aggressive pricing that challenges importers on cost per gigabase. Meanwhile, technology convergence encourages platform-plus-reagent bundling; suppliers integrate sequencers, cloud analytics, and consumables into subscription models that lock customers into multi-year reagent streams. This strategy protects margins while creating high switching costs, reinforcing the growth path for the sequencing reagents market.

Sequencing Reagents Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Roche unveiled Sequencing by Expansion (SBX), delivering >99.80% SNV accuracy and seven whole genomes per hour.

- December 2024: Singular Genomics agreed to be acquired by Deerfield Management for USD 20.00 per share, a 254% premium.

- July 2024: Thermo Fisher Scientific completed its USD 3.1 billion acquisition of Olink Holding.

Table of Contents for Sequencing Reagents Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Declining NGS Cost Curve Accelerates Clinical Adoption

- 4.2.2Surge In Large-Scale Population Genomics Programmes

- 4.2.3Oncology Companion-Diagnostic Pipelines Expanding

- 4.2.4Sample-Barcoding Chemistries Enabling Ultra-High-Throughput Screens

- 4.2.5AI-Designed Enzymatic Kits Shortening Library-Prep Times

- 4.2.6COVID-Era Installed NGS Base Driving Consumables Pull-Through

- 4.3Market Restraints

- 4.3.1Limited Reimbursement For Extensive Genomic Testing

- 4.3.2Data-Privacy Regulations Raising Compliance Costs

- 4.3.3Global DNTP-Grade Raw-Material Shortages

- 4.3.4Wet-Lab Talent Deficit In Emerging Markets

- 4.4Supply Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Reagent Type

- 5.1.1Template Preparation Kits

- 5.1.2Library Preparation Kits

- 5.1.3Control Kits

- 5.1.4Sequencing Reaction Kits

- 5.1.5Barcoding/ Indexing Kits

- 5.1.6PCR & Amplification Reagents

- 5.1.7Others

- 5.2By Sequencing Technology

- 5.2.1Next-Generation Sequencing

- 5.2.2Third-Generation

- 5.2.3Sanger / Chain-Termination

- 5.2.4Single-cell / Spatial Transcriptomics-ready Chemistries

- 5.3By Application

- 5.3.1Clinical Diagnostics

- 5.3.2Oncology & Liquid Biopsy

- 5.3.3Reproductive & Prenatal Testing

- 5.3.4Agrigenomics & Veterinary

- 5.3.5Forensics & Security

- 5.3.6Drug Discovery / Functional Genomics

- 5.3.7Microbiome & Metagenomics

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1Illumina

- 6.3.2Thermo Fisher Scientific

- 6.3.3F. Hoffmann-La Roche

- 6.3.4Agilent Technologies

- 6.3.5Qiagen

- 6.3.6Oxford Nanopore Technologies

- 6.3.7BGI-Shenzhen

- 6.3.8Pacific Biosciences

- 6.3.9Takara Bio

- 6.3.10New England Biolabs

- 6.3.11Fluidigm / Standard BioTools

- 6.3.12Bio-Rad Laboratories

- 6.3.13Danaher (IDT)

- 6.3.14PerkinElmer

- 6.3.15Tecan Group

- 6.3.1610x Genomics

- 6.3.17Gencell Pharma

- 6.3.18Seqera Labs

- 6.3.19Element Biosciences

- 6.3.20Singular Genomics

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Sequencing Reagents Market Report Scope

As per the scope, sequencing reagents are used in the process of DNA sequencing, an important tool to determine the order of nucleotides. DNA sequencing has several types of research, the diagnostic and therapeutic application includes drug discovery, forensics, genomics, cancers, infectious disease, and many more.