Molecular Biology Enzymes, Kits And Reagents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

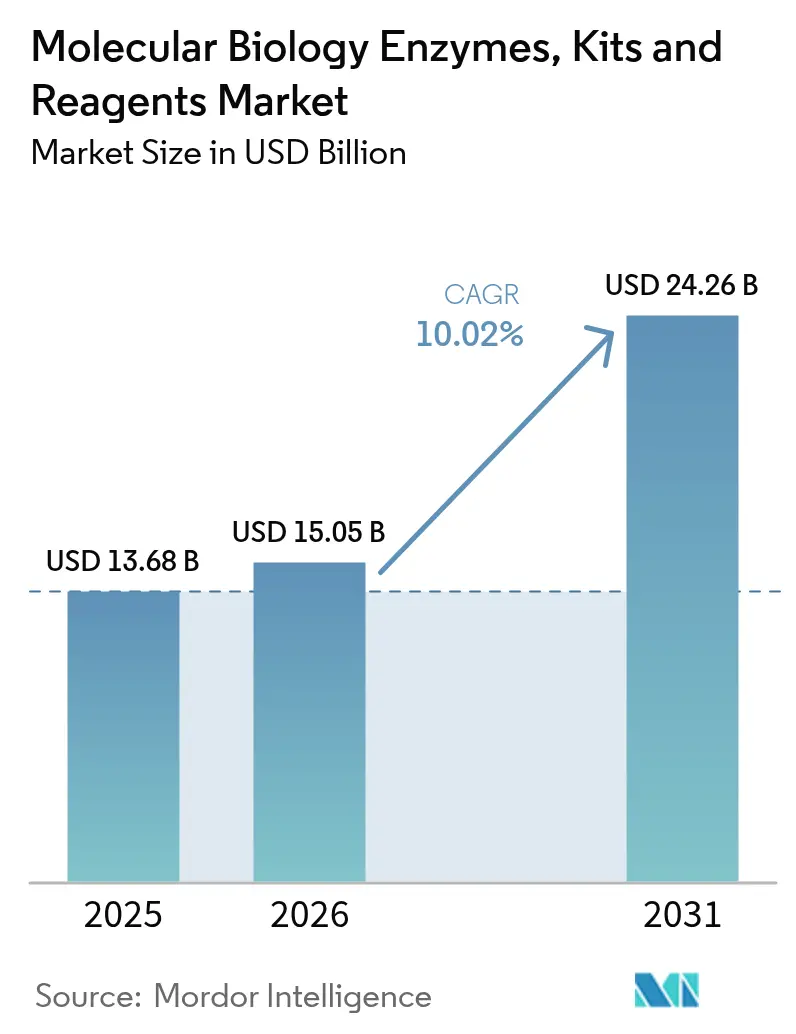

| Market Size (2026) | USD 15.05 Billion |

| Market Size (2031) | USD 24.26 Billion |

| Growth Rate (2026 - 2031) | 10.02% CAGR |

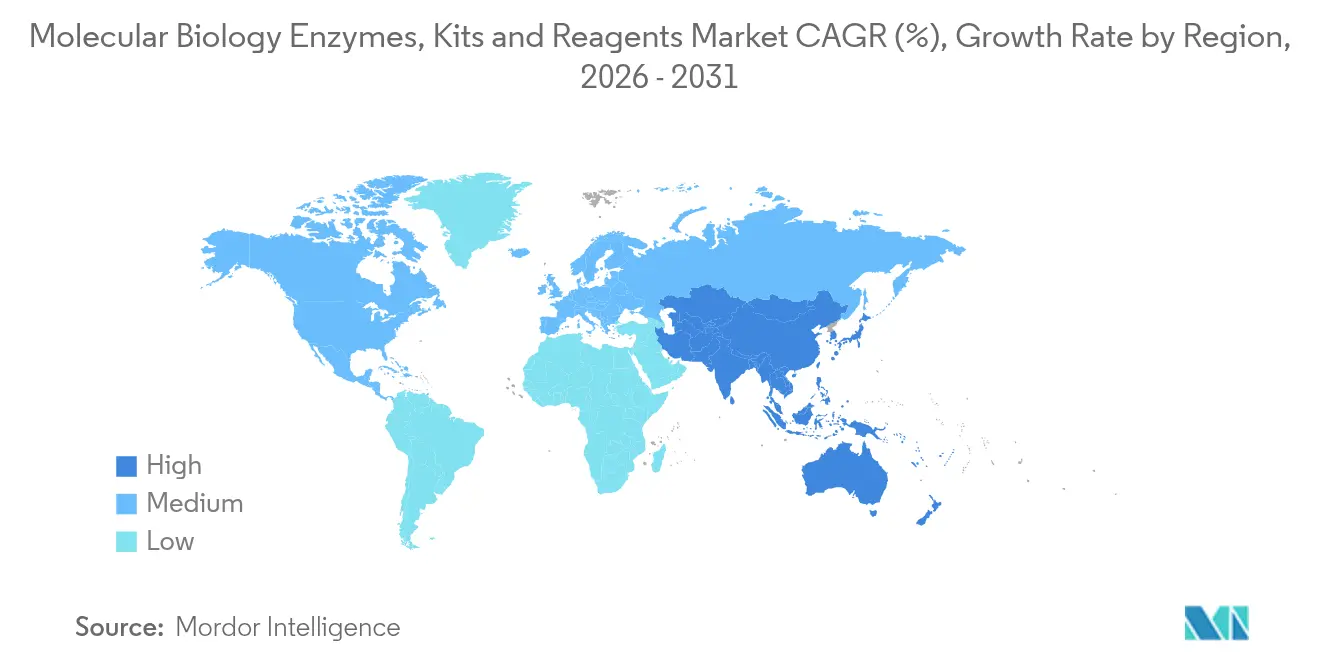

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Molecular Biology Enzymes, Kits And Reagents Market Analysis by Mordor Intelligence

The molecular biology enzymes, kits & reagents market size in 2026 is estimated at USD 15.05 billion, growing from 2025 value of USD 13.68 billion with 2031 projections showing USD 24.26 billion, growing at 10.02% CAGR over 2026-2031. Strong momentum comes from next-generation sequencing platform upgrades, growing clinical adoption of single-cell multi-omics assays, and the shift toward field-deployable, lyophilized diagnostics. Ultra-high-fidelity enzyme innovations are raising analytical precision, enabling detection of rare mutations and supporting CRISPR-based therapeutic pipelines. At the same time, sustained federal R&D spending in North America and Europe, coupled with intensified life-science investment in Asia-Pacific, is enlarging the customer base for high-value consumables. Competitive rivalry is intensifying as large suppliers pursue strategic acquisitions to integrate sample preparation, amplification, detection, and data-analysis capabilities, while smaller specialists stake out opportunities in sustainable consumables and machine-learning-guided enzyme engineering.

Key Report Takeaways

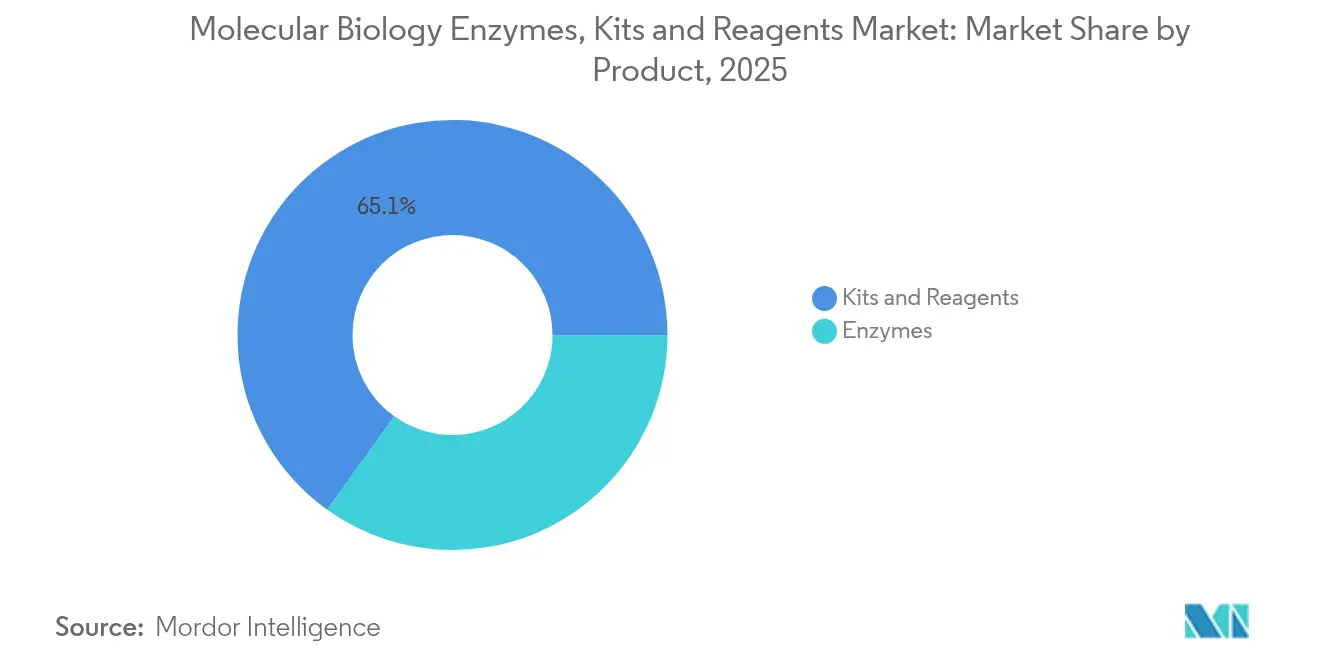

- By product category, kits & reagents led with 65.10% revenue share in 2025, while enzymes are advancing at a 12.05% CAGR through 2031.

- By application, PCR retained 45.10% of the molecular biology enzymes, kits & reagents market share in 2025, whereas next-generation sequencing is projected to expand at 15.95% CAGR to 2031.

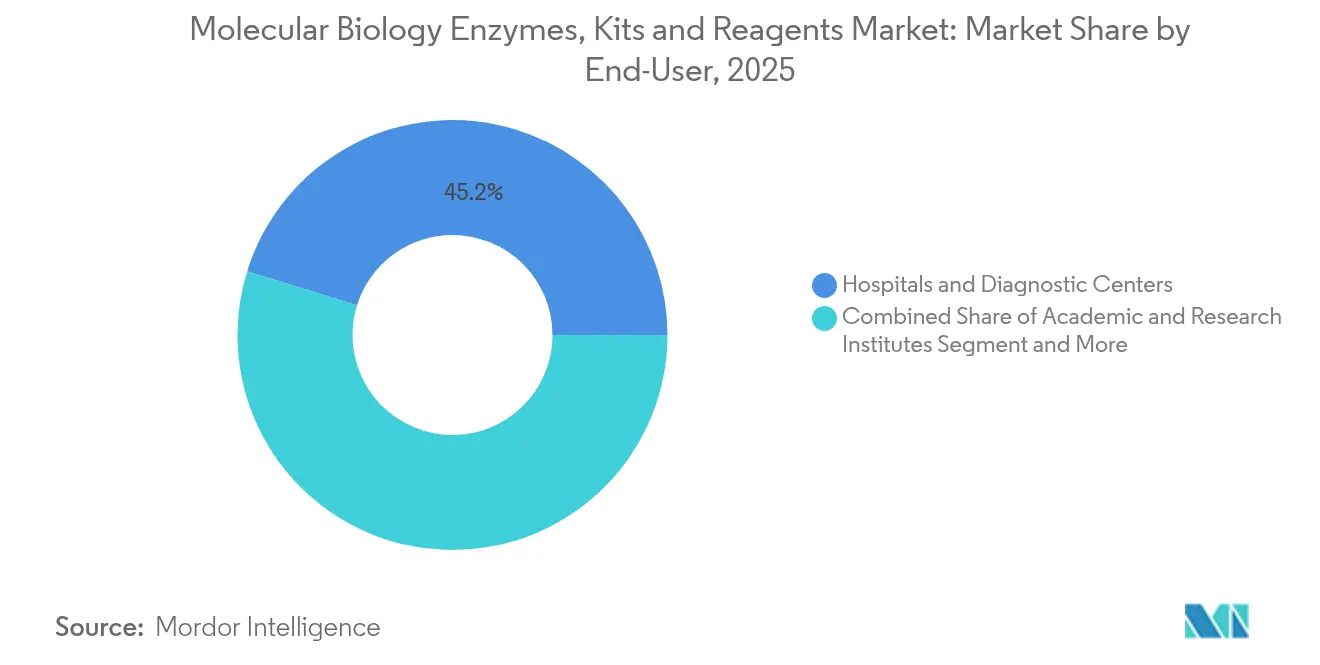

- By end-user, hospitals & diagnostic centers commanded 45.20% of the molecular biology enzymes, kits & reagents market size in 2025; contract research & manufacturing organizations post the quickest growth at 12.98% CAGR.

- By form, liquid products held 58.10% revenue share in 2025; lyophilized formats are rising at 14.10% CAGR as cold-chain-free diagnostics gain traction.

- By geography, North America dominated with 38.40% market share in 2025, while Asia-Pacific is forecast to grow at 11.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Molecular Biology Enzymes, Kits And Reagents Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Advances In NGS, qPCR & dPCR Platforms | +2.3% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Rising Incidence Of Infectious Diseases & Genetic Disorders | +2.1% | Global, with concentrated impact in APAC and MEA | Medium term (2-4 years) |

| Growing Adoption Of Precision-Medicine Diagnostics | +1.9% | North America & EU, expanding to APAC urban centers | Long term (≥ 4 years) |

| Expanding Life-Science R&D Budgets | +1.8% | North America & EU core, spillover to APAC | Short term (≤ 2 years) |

| Ultra-High-Fidelity Enzymes Enabling Single-Cell Multi-Omics | +1.2% | Global research hubs, concentrated in North America and EU | Long term (≥ 4 years) |

| Field-Deployable Lyophilized Kits Reduce Cold-Chain Costs | +0.9% | Global, with highest impact in resource-limited settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Infectious Diseases & Genetic Disorders

COVID-19 highlighted the value of rapid nucleic-acid testing, accelerating demand for portable molecular platforms such as a lyophilized LAMP-based Dragonfly system that achieved 96.1% sensitivity for mpox detection[1]Jesús Rodríguez-Manzano, “Portable molecular diagnostic platform for rapid point-of-care detection of mpox and other diseases,” Nature Communications, nature.com. Health systems now view early molecular surveillance as essential for outbreak containment and cost control. Expanded newborn genetic-disorder screening and population-level carrier testing require enzymes with extremely low error rates to spot rare variants. CRISPR-based detection chemistries and microfluidic cartridges are entering frontline laboratories, enlarging the addressable market for high-value reagents.

Expanding Life-Science R&D Budgets

A 2025 survey showed overall academic research budgets rising 4%, even as some capital-equipment lines stayed flat, signaling a tilt toward high-turnover consumables. Contract research organizations increasingly win bulk-supply agreements, encouraging vendors to offer customized master mixes and sustainably packaged kits.

Rapid Advances in NGS, qPCR & dPCR Platforms

Third-generation sequencers such as Oxford Nanopore and PacBio reduce amplification steps, yet drive demand for specialty polymerases tolerant of long reads and modified bases. Enzymatic DNA synthesis has achieved 1,005-mer oligonucleotides at 99.9% yield, cutting hazardous waste relative to phosphoramidite chemistry. Takara Bio’s SmartChip ND system performs 5,184 qPCR reactions in under 30 minutes, underscoring the need for heat-stable enzymes and pre-aliquoted reagent plates. Machine-learning-guided cell-free expression accelerates screening of 10 million polymerase mutants per day, shrinking development cycles.

Growing Adoption of Precision-Medicine Diagnostics

Genomic profiling is moving beyond oncology into neurology and immunology. The myeloMATCH trial employs a one-day NGS workflow to place acute myeloid leukemia patients into matched studies, illustrating clinical demand for rapid library-prep kits. Companion-diagnostic partnerships tie reagent sales to drug launches, yet U.S. MolDX coverage policies still require exhaustive clinical-utility data, delaying revenue recognition[2]Centers for Medicare & Medicaid Services, “Billing and Coding: Genetic Testing for Oncology,” cms.gov.

Restraints Impact Analysis of Molecular Biology Enzymes, Kits And Reagents Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost & Limited Reimbursement For Genetic Testing | -1.6% | Global, most pronounced in North America and EU | Short term (≤ 2 years) |

| Fragile Supply Chain For Specialty Recombinant Reagents | -1.1% | Global, with acute impact in APAC manufacturing | Medium term (2-4 years) |

| Complex IP & Licensing Landscape For Enzyme Patents | -0.8% | Global, concentrated in innovation hubs | Long term (≥ 4 years) |

| Sustainability Pressure On Single-Use Kit Plastics | -0.7% | EU and North America leading, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost & Limited Reimbursement For Genetic Testing

Medicare’s MolDX program uses stringent clinical-utility thresholds, leaving many novel assays uncovered or reimbursed below cost. Private insurers now demand real-world evidence, adding time and expense to test launches. Smaller labs struggle to fund multi-site trials, constraining innovation until payers harmonize evidence standards.

Complex IP & Licensing Landscape for Enzyme Patents

More than 11,000 CRISPR-related patents create a thicket that newcomers must navigate[3]World Intellectual Property Organization, “CRISPR-Cas: Navigating the Patent Landscape to Explore Boundless Applications,” wipo.int. Ongoing UC–Broad disputes over Cas9 raise licensing uncertainties that ripple across polymerase and ligase portfolios. Royalty stacking inflates bill-of-materials costs and can deter investment in next-generation editing enzymes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Molecular Biology Enzymes, Kits And Reagents Market Segment Analysis

By Product:

Reagents Lead While Enzymes AccelerateKits & reagents contributed 65.10% of 2025 revenue, underlining their consumable nature in routine workflows. The enzymes portion, though smaller, is climbing at 12.05% CAGR as researchers demand ultra-high-fidelity polymerases for single-cell sequencing. DNA polymerases remain the dominant enzyme class, bolstered by a screening platform that can assay 10 million variants daily. Within the molecular biology enzymes, kits & reagents market size, Takara Bio’s mutant T7 RNA polymerase cuts double-stranded RNA by 90%, addressing mRNA-therapeutics quality needs.

Recurrence-driven revenue from PCR master mixes and NGS library kits cements reagent leadership. Yet enzymes capture premium pricing because single-amino-acid tweaks can halve error rates and improve CRISPR specificity. Machine-learning-aided evolution lets vendors tailor catalytic optima to new sequencing chemistries, ensuring double-digit growth for the enzymes slice of the molecular biology enzymes, kits & reagents market.

By Application:

PCR Dominates As NGS SurgesPCR held 45.10% market share in 2025, reflecting ubiquity in diagnostics and QA. However, NGS is expanding at 15.95% CAGR on the back of falling per-genome costs and rapid oncology adoption. A new amplification method, AMPLON, shortens run time 50% without sacrificing accuracy, widening PCR’s reach into rapid screening.

CRISPR workflows are the fastest-growing niche inside the molecular biology enzymes, kits & reagents market, fueled by engineered Cas12a variants that deliver allele-specific edits. Epigenetics assays and protein-analysis kits also gain traction as multi-omic studies proliferate, creating cross-selling potential for integrated reagent bundles.

By End-User:

Hospitals Lead While CROs AccelerateHospitals & diagnostic centers generated 45.20% of 2025 revenue thanks to mainstream use of molecular tests for infectious-disease panels and oncology markers. The CRO CMO segment is growing at 12.98% CAGR as drug-development firms outsource specialized assays requiring bespoke reagent lots. Federal agencies estimate academic basic-research obligations grew in 2022, sustaining demand from universities.

Pharmaceutical innovators increasingly partner with CROs for single-cell RNA-seq and CRISPR screening, enlarging bulk-purchase contracts within the molecular biology enzymes, kits & reagents market. Forensic labs, meanwhile, adopt low-stutter STR kits such as Promega’s new enzyme formulation, ensuring stable if smaller-volume demand.

By Form:

Liquid Dominates While Lyophilized Gains GroundLiquid mixes accounted for 58.10% of 2025 sales owing to plug-and-play compatibility with automated platforms. Lyophilized products are rising at 14.10% CAGR because they travel at room temperature and cut cold-chain overhead. A colorimetric RT-LAMP kit retained full sensitivity after 28 days at ambient temperature.

Sustainability pressure encourages migration toward biobased plates and concentrated reagents that shrink plastic waste. Vendors in the molecular biology enzymes, kits & reagents industry now bundle lyophilized pellets with low-profile eco-friendly consumables to win procurement points under green-lab guidelines.

Geography Analysis

North America Molecular Biology Enzymes, Kits And Reagents Market

North America held 38.40% of 2025 revenue, anchored by NIH and NSF funding lines that sustain reagent consumption across academic and clinical labs. Strong reimbursement for molecular tests, despite MolDX hurdles, keeps hospital throughput high, and U.S. start-ups continue to spin out novel enzymes, maintaining regional leadership.

Europe Molecular Biology Enzymes, Kits And Reagents Market

Europe posted steady mid-single-digit growth. Regulatory alignment under IVDR is driving demand for validated kit components, benefiting suppliers able to document performance to CE-IVD standards. Investment in antimicrobial-resistance surveillance has led to rollout of high-density qPCR systems capable of thousands of reactions per run, spurring reagent pull-through.

APAC Molecular Biology Enzymes, Kits And Reagents Market

Asia-Pacific registers the fastest trajectory at 11.05% CAGR. China recorded a 35.84% jump in drug and device filings in 2023, with IVD reagents comprising nearly one-quarter of submissions. Japan is revising laboratory-developed-test frameworks, giving clarity to local innovators. South Korea’s tiered approval pathway expedites low-risk molecular assays, widening market access. APAC public-health agencies also invest in field-deployable diagnostics for rural clinics, accelerating uptake of lyophilized formats within the molecular biology enzymes, kits & reagents market size.

MEA and LATAM Molecular Biology Enzymes, Kits And Reagents Market

The Middle East & Africa are smaller today but pursue national genomics programs that mandate kit localization, signaling long-run upside. Latin America sees procurement spikes tied to disease-surveillance campaigns, though currency volatility moderates spending cycles.

Competitive Landscape

The market is moderately fragmented. Thermo Fisher Scientific, Illumina, and Roche collectively deploy multibillion-dollar M&A war chests to assemble end-to-end workflows; Thermo Fisher alone targets USD 40–50 billion in future acquisitions. Bio-Rad seeks to close its Stilla Technologies purchase to round out digital PCR capabilities.

Mid-tier players such as New England Biolabs and Promega focus on proprietary enzyme engineering and sustainability-oriented consumables. Start-ups leverage AI-driven protein design to shorten R&D cycles, drawing venture funds toward niche CRISPR editing enzymes or synthetic-biology toolkits. Intellectual-property cross-licensing remains a gating factor; vendors with broad patent portfolios can bundle freedom-to-operate assurances into contracts, tipping competitive bids.

White-space opportunities include ultra-stable polymerases for microfluidic NGS, single-use plastics derived from renewable feedstocks, and automation-ready lyophilized mastermixes. The race to commercialize enzymatic DNA synthesis is another potential disruptor, as lower-cost gene assembly would further expand applications and pull reagent demand.

Molecular Biology Enzymes, Kits And Reagents Industry Leaders

Agilent Technologies

F. Hoffmann-La Roche Ltd

Merck KGaA

Qiagen NV

Thermo Fisher Scientific

- *Disclaimer: Major Players sorted in no particular order

Molecular Biology Enzymes, Kits And Reagents Market Companies Covered in this Report

- Agilent Technologies

- Thermo Fisher Scientific

- Roche

- Illumina

- Merck

- QIAGEN

- Takara Bio

- New England Biolabs

- Promega

- Lucigen (LGC Biosearch)

- Bio-Rad Laboratories

- PerkinElmer

- Oxford Nanopore Technologies

- Pacific Biosciences

- BGI

- Bio-Techne

- Enzymatics (Cell Signaling Tech)

- Genscript

- ArcherDx (Invitae)

Read Analysis of Molecular Biology Enzymes, Kits And Reagents Companies

Recent Industry Developments in Molecular Biology Enzymes, Kits And Reagents Market

- April 2025: BioSkryb Genomics and Tecan launched a single-cell multi-omics workflow delivering sequencing-ready libraries in under 10 hours for cancer research.

- February 2025: Bio-Rad issued a binding offer to acquire Stilla Technologies, a next-generation digital PCR specialist, with closing expected in Q3 2025.

Molecular Biology Enzymes, Kits And Reagents Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the molecular biology enzymes, kits and reagents market as the global sales value of polymerases, ligases, nucleases, restriction enzymes, cloning and amplification kits, sequencing library preparation kits, and buffer or substrate reagents supplied ready to use for research, diagnostic, and therapeutic workflows that involve PCR, NGS, cloning, mutagenesis, and epigenetic analysis. We measure only finished commercial products sold through catalog or direct channels and exclude captive, in-house formulations.

Scope exclusion: Bulk industrial enzymes, proteomics reagents, and stand-alone laboratory instruments are outside this scope.

Segments Covered in This Report

- By Product

- Enzymes

- DNA Polymerases

- Reverse Transcriptases

- Ligases & Kinases

- Nucleases & Restriction Enzymes

- Modifying Enzymes

- Other Specialty Enzymes

- Kits & Reagents

- PCR Master-Mix & qPCR Kits

- NGS/Library-Prep Kits

- DNA/RNA Extraction & Purification Kits

- Lyophilized Field-Use Kits

- Buffers, dNTPs & Additives

- Enzymes

- By Application

- Polymerase Chain Reaction

- Next-Generation Sequencing

- Epigenetics

- Cloning & Synthetic Biology

- Gene-Editing / CRISPR Workflows

- Protein Analysis & Proteomics

- By End-User

- Hospitals & Diagnostic Centers

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Contract Research & Manufacturing Organizations

- Forensic & Security Laboratories

- Food, Environmental & Agricultural Testing Labs

- By Form

- Liquid (Cold-Chain)

- Lyophilized (Ambient)

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed laboratory managers, procurement heads at biotech firms, hospital molecular diagnosticians, and regional distributors across North America, Europe, Asia-Pacific, and Latin America. These discussions confirmed reagent consumption rates, pricing dispersion, emerging CRISPR workflows, and validated assumed transition timelines from legacy PCR to NGS kits.

Desk Research

We collected foundational statistics from tier-one sources such as the National Institutes of Health budget tracker, FDA 510(k) clearance archives, World Bank R&D spend tables, UN Comtrade HS-3822 shipment data, and peer-reviewed studies indexed in PubMed that quantify kit usage in oncology and infectious disease testing. Company filings, investor presentations, and life science association white papers further revealed price bands and demand shifts after pandemic funding. Our paid access to D&B Hoovers and Dow Jones Factiva supplied revenue splits for specialized suppliers and distribution partners. The sources listed here are illustrative; many other open databases, conference proceedings, and regulatory portals supported data collection, validation, and clarification.

Market-Sizing & Forecasting

We began with a top-down reconstruction of global kit volumes using HS-3822 trade data and public production disclosures, which are then aligned with average selling prices gathered through primary calls. Select bottom-up supplier roll-ups and channel checks tightened totals. Key variables in our model include PCR test throughput, sequencing instrument installed base, NIH and Horizon Europe genomics funding, biotech venture capital inflows, and standard kit utilization coefficients per reaction. A multivariate regression, refreshed annually, projects these drivers through 2030 while scenario analysis tests upside from rapid point of care adoption.

Data Validation & Update Cycle

Before release, our team compares outputs with independent shipment trends, revisits outliers, and escalates variances for senior review. Reports refresh once every twelve months, with interim updates triggered by material regulatory or funding events, so clients always receive the latest baseline.

How Mordor Intelligence's Molecular Biology Enzymes, Kits And Reagents Market Size Compares to Other Published Estimates

Published estimates often diverge because firms pick different product mixes, price assumptions, and refresh timings, yet decision makers still need one dependable number. Our disciplined scope, annual update cadence, and dual path modeling keep the base year firmly anchored.

Key gap drivers include whether consumables for proteomics are bundled, how aggressively future ASP erosion is modeled, and the depth to which vendor revenue statements are validated against trade data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.68 B (2025) | Mordor Intelligence | |

| USD 15.48 B (2024) | Regional Consultancy A | Bundles general lab consumables and uses infrequent mid-2024 snapshot |

| USD 25.24 B (2024) | Global Consultancy B | Counts proteomics reagents and relies solely on vendor revenue without trade cross checks |

In short, Mordor Intelligence delivers a balanced, transparent baseline that links clear variables with repeatable steps, giving stakeholders a reliable view they can audit with confidence.

Key Questions Answered in the Report

What is the current size of the molecular biology enzymes, kits & reagents market?

The molecular biology enzymes, kits & reagents market size stands at USD 15.05 billion in 2026, with a projected value of USD 24.26 billion by 2031.

Which segment is expanding the fastest?

Enzymes are the quickest-growing product segment, advancing at a 12.05% CAGR due to demand for ultra-high-fidelity polymerases and CRISPR-specific nucleases.

Why are lyophilized kits gaining popularity?

Lyophilized formulations enable room-temperature shipping and storage, lowering cold-chain costs and supporting field diagnostics where infrastructure is limited.

How do reimbursement policies affect market growth?

Restrictive coverage criteria under programs such as Medicare MolDX can delay adoption of innovative tests, trimming projected CAGR by an estimated 1.6%.

Which geographic region offers the highest growth potential?

Asia-Pacific shows the highest CAGR at 11.05% through 2031, fueled by rising R&D investments, regulatory reforms, and expanding precision-medicine programs.

Page last updated on: