Biotechnology Reagents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

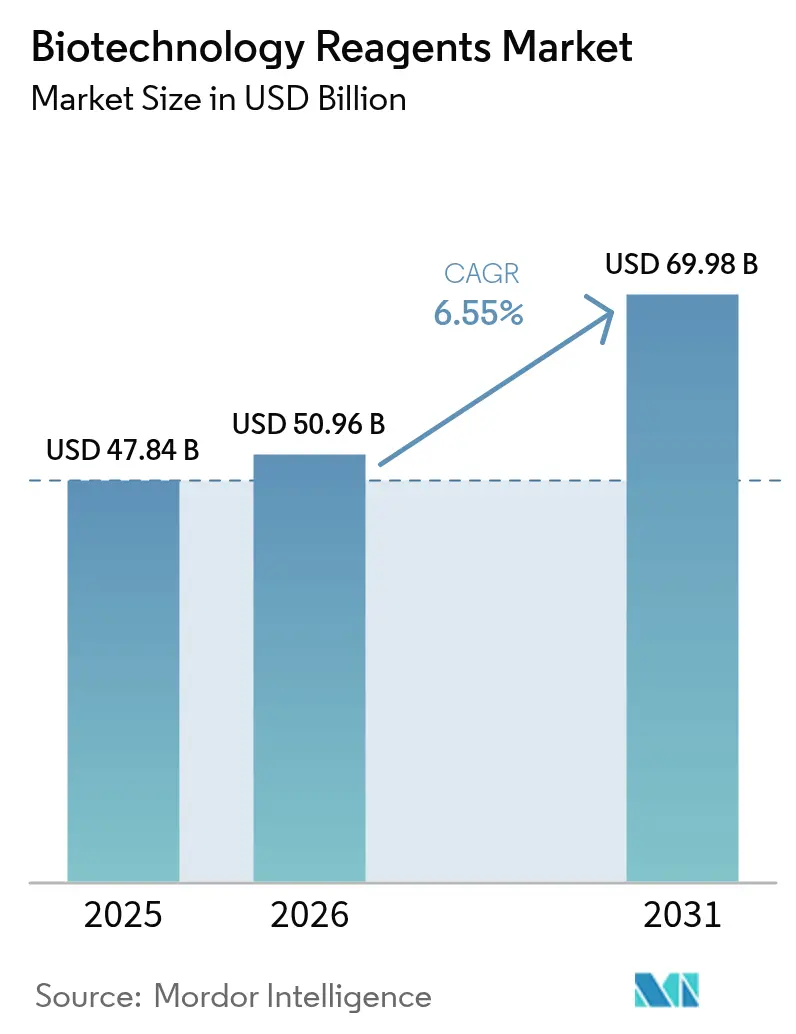

| Market Size (2026) | USD 50.96 Billion |

| Market Size (2031) | USD 69.98 Billion |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biotechnology Reagents Market Analysis by Mordor Intelligence

Biotechnology Reagents Market size in 2026 is estimated at USD 50.96 billion, growing from 2025 value of USD 47.84 billion with 2031 projections showing USD 69.98 billion, growing at 6.55% CAGR over 2026-2031.

Intensifying investment in AI-enabled drug discovery, growing biomanufacturing capacity, and rapid adoption of single-cell analytics enlarge the addressable demand for high-performance reagents. Multinational mergers that integrate consumables with data-analysis platforms accelerate end-to-end solution uptake, while government incentives in Asia support local production of GMP-grade inputs. Ongoing digitalisation of laboratories further boosts demand for pre-optimised, automation-ready reagent kits, particularly in oncology and regenerative-medicine pipelines. Meanwhile, stricter global quality standards lengthen product-validation cycles, pressuring smaller suppliers to partner with established players.

Key Report Takeaways

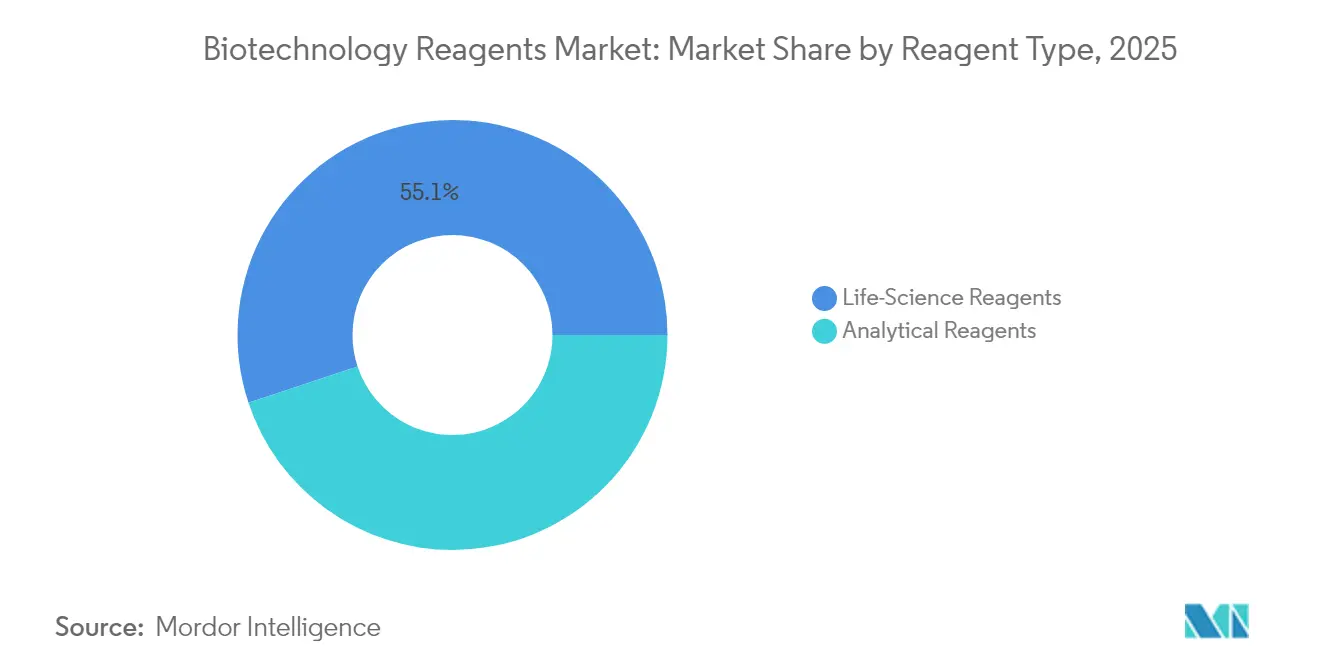

- By reagent type, life-science reagents led with 55.10% revenue share in 2025, whereas analytical reagents are projected to grow at a 8.85% CAGR through 2031.

- By application, DNA & RNA analysis accounted for 29.65% of the biotechnology reagents market share in 2025, while single-cell gene expression is expanding at an 10.95% CAGR to 2031.

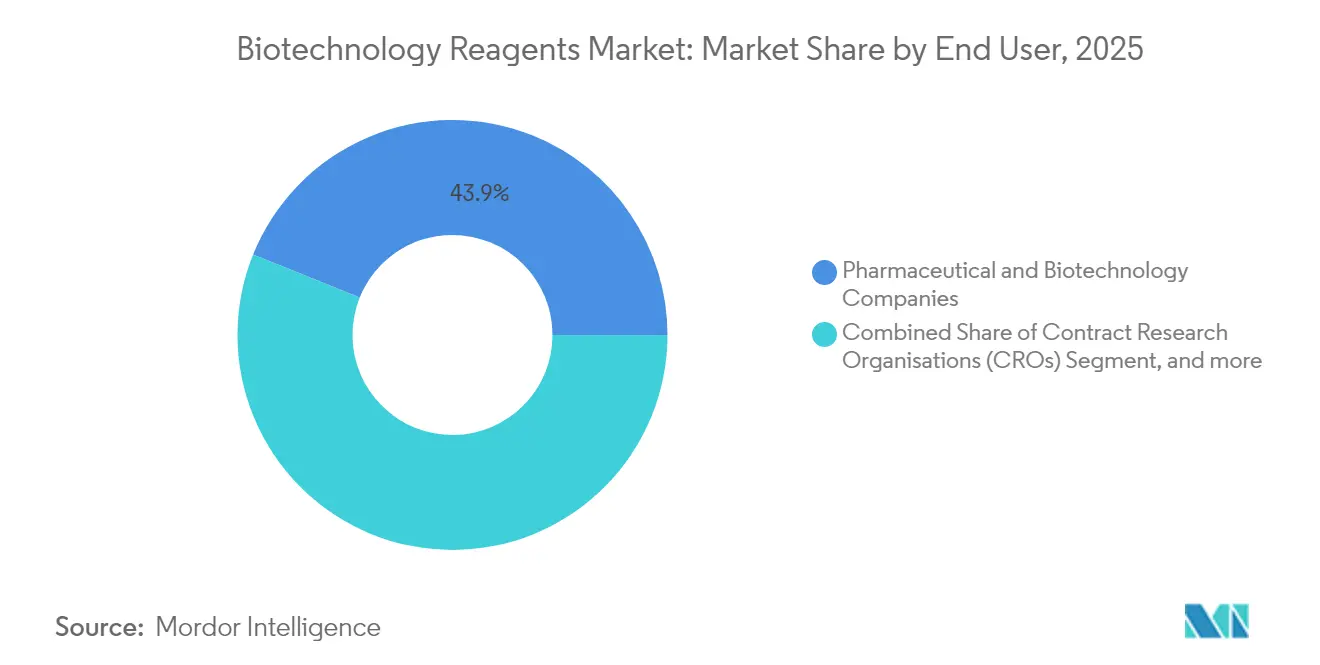

- By end user, pharmaceutical & biotechnology companies represented 43.90% of the biotechnology reagents market size in 2025; contract research organizations posted the fastest-growing demand at 9.55% CAGR.

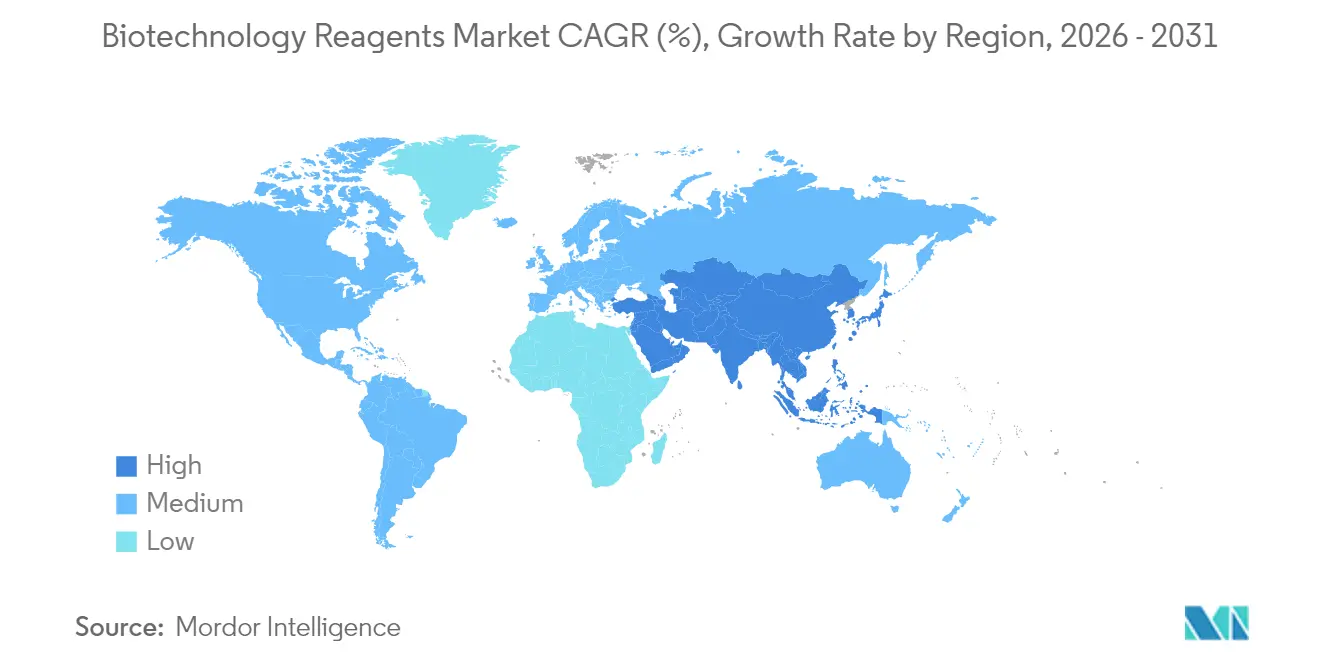

- By geography, North America commanded 38.80% revenue share in 2025, whereas Asia-Pacific is set to grow at a 9.15% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biotechnology Reagents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D spending by biotech firms & startup pipeline | +1.8% | North America & Europe; spill-over to APAC | Medium term (2-4 years) |

| Expanding stem-cell & regenerative-medicine studies | +1.2% | North America & APAC | Long term (≥ 4 years) |

| Oncology-centric omics projects | +1.5% | Global, with APAC acceleration | Medium term (2-4 years) |

| AI-assisted reagent optimisation | +1.1% | North America & Europe; emerging in APAC | Medium term (2-4 years) |

| Rising point-of-care molecular diagnostics | +0.9% | APAC core; expanding to MEA & Latin America | Short term (≤ 2 years) |

| Government biomanufacturing localisation incentives | +0.8% | APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High R&D Spending by Biotech Firms & Swelling Startup Pipeline

Venture funding in precision fermentation and synthetic biology startups surged, channeling USD 2 billion into new platforms that rely on premium-grade reagents for cell—and gene-therapy workflows.[1]Mitsui & Co., “Investment Trends in Precision Fermentation,” mitsui.com Each biologic candidate requires bespoke analytical consumables, driving recurring demand in the global bioprocess technology market. Fragmented demand lets specialist suppliers command premium pricing, while platform-based discovery models push labs to standardise reagent systems compatible with multiple targets. Consequently, procurement strategies increasingly favour vendors that offer modular, AI-ready kits with validated performance data.

Expanding Stem-Cell & Regenerative-Medicine Studies

Adult stem-cell protocols dominate, prompting innovation in isolation and expansion reagents that preserve phenotype. APAC governments co-fund large-scale GMP facilities, such as Aurora Biosynthetics’ AUD200 million (USD 129.4 million) plant, boosting regional demand for compliant consumables. As personalised regenerative procedures proliferate, suppliers must deliver flexible formulations capable of small-batch, patient-specific processing.

Oncology-Centric Omics Projects Demanding High-Throughput Reagents

Long-read sequencing for liquid biopsies requires novel chemistries optimised for GC-rich cell-free DNA, while single-cell RNA-seq platforms like 10x Genomics’ Chromium drive uptake of speciality barcoding kits. AI-enhanced molecular optimisation registers success rates above 80%, intensifying throughput needs for high-purity screening reagents. Clinical deployment of point-of-care oncology assays further stimulates demand for lyophilised, room-temperature stable reagents compatible with decentralised settings.

AI-Assisted Reagent Optimisation Shortening Development Cycles

Deep-learning engines such as DrugGen achieve 99.9% validity in molecule generation, enabling predictive design of reagent compositions that dramatically cut iteration time. Pharmaceutical manufacturers are integrating automated synthesis robots that rely on standardised reagent libraries; vendors providing digitally-traceable, lot-consistent kits gain preferred-supplier status. Real-time monitoring of reactions through embedded sensors places additional emphasis on data-rich, machine-readable packaging.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-jurisdictional quality & safety certifications | −1.3% | Global; complexity peaks in EU & APAC | Medium term (2-4 years) |

| Volatile bioprocess raw-material supply chain post-COVID | −0.8% | Global; acute in APAC manufacturing hubs | Short term (≤ 2 years) |

| Rising average selling price of premium-grade reagents | −0.7% | Global; highest impact in emerging markets | Short term (≤ 2 years) |

| Sustainability pressures on hazardous components | −0.5% | EU & North America; spreading to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Jurisdictional Quality & Safety Certifications

FDA and EMA divergence on reference-standard validation forces suppliers to duplicate studies, adding 6-12 months to product launches and raising development costs by up to 30%.[2]U.S. Food & Drug Administration, “Quality Management Systems for Biologics,” fda.gov Achieving ISO 13485 certification for each production site strains smaller firms, while Quality-by-Design documentation now covers entire life-cycles, pushing demand toward larger, vertically integrated players able to absorb compliance costs.

Volatile Bioprocess Raw-Material Supply Chain Post-COVID

Chromatography resin and critical media shortages persist as drought-affected shipping lanes and geopolitical tensions disrupt logistics.[3]BioProcess International, “Global Resin Shortages Persist,” bioprocessintl.com Manufacturers hedge risk through dual-sourcing strategies and higher safety stocks, yet this ties up working capital and compresses margins. Localisation moves in Asia require parallel investments in cold-chain and warehousing infrastructure to stabilise reagent supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Reagent Type: Life-Science Leadership and Analytical Upside

Life-Science Reagents captured 55.10% of biotechnology reagents market share in 2025. Strong utilisation in PCR-based diagnostics and next-generation sequencing keeps the segment ahead, while continuing investment in COVID-era molecular infrastructure supports baseline demand. Analytical Reagents, though smaller, are set to surpass overall biotechnology reagents market growth with a 8.85% CAGR, benefitting from regulatory emphasis on deep characterisation and the proliferation of mass-spectrometry-driven proteomics. Emerging hybrid kits that integrate sample prep with assay reagents promise workflow simplification valued by high-throughput labs.

Second-generation chromatography buffers and single-use filtration reagents enable continuous bioprocessing, while electrophoresis consumables optimise resolution for cell-free systems. Suppliers increasingly bundle software licences with reagents to capture recurring analytics revenue, signalling convergence between wet-lab and digital offerings.

By Application: Single-Cell Analytics Gain Momentum

DNA & RNA Analysis remained the largest application, holding 29.65% of biotechnology reagents market size in 2025 through entrenched usage in genomic surveillance and virus-variant monitoring. Yet Single-Cell Gene Expression is advancing at 10.95% CAGR, spurred by oncology and immunology research that leverages granularity unattainable with bulk assays. Vendors capable of lowering per-cell costs without compromising data quality stand to unlock new cohorts of users in academic and translational labs.

Downstream, protein-purification reagents benefit as biotherapeutic pipelines swell, particularly monoclonal antibodies and mRNA-based vaccines. Demand for multiplexed assay kits that permit simultaneous proteomic and transcriptomic readouts further blurs application boundaries, calling for reagents engineered for cross-modality compatibility.

By End User: CROs Drive Outsourced Demand

Pharmaceutical and Biotechnology Companies maintained a 43.90% stake in 2025 consumption, but Contract Research Organizations are projected to outpace with 9.55% CAGR as developers outsource specialised analytics and early-stage screening. CRO consolidation produces mega-sites able to negotiate reagent bulk discounts, pushing suppliers to craft volume-tiered pricing and just-in-time delivery services.

Academic institutes remain foundational customers, especially where government funding funds basic research and shared-resource facilities. Diagnostic laboratories expand molecular-testing menus, adopting lyophilised PCR kits that reduce cold-chain dependence in emerging markets, a trend that diversifies end-user procurement cycles.

Geography Analysis

North America anchored 38.80% of 2025 revenues on the back of entrenched biopharmaceutical clusters, deep venture capital pools, and a supportive regulatory climate. Federal programmes promoting advanced biomanufacturing generate steady requisitions for GMP-validated reagents. In Europe, continued adherence to sustainability mandates propels interest in green-chemistry formulations and recyclable packaging, prompting suppliers to revamp product life-cycle assessments.

Asia-Pacific tops global expansion, expected to post 9.15% CAGR through 2031. China’s Circular No. 53 has trimmed review timelines and expanded data-protection windows, catalysing local innovation and inbound partnerships. Japan’s goal of tripling its biotech economy by 2030 underwrites domestic demand for clinical-grade reagents, while Southeast Asia’s CDMO rise creates fresh outlets for single-use consumables. Local suppliers leverage government subsidies to close capability gaps, although adherence to international QC standards remains a hurdle.

Markets in the Middle East, Africa, and South America record mid-single-digit growth. Technology-transfer agreements sponsored by multilateral health agencies facilitate local reagent fill-finish operations, reducing import reliance. However, limited cold-chain infrastructure and fluctuating currency valuations temper the adoption of premium products, incentivising suppliers to offer modular, cost-tiered reagent lines tailored to regional purchasing power.

Competitive Landscape

The biotechnology reagents market continues to consolidate as strategics chase vertical integration. Danaher fused Cytiva with Pall into a USD 7.5 billion bioprocess powerhouse, coupling upstream media with downstream analytics to offer seamless workflows. Its USD 5.5 billion Abcam buy extends reach into antibody and proteomics reagents, reinforcing multiproduct lock-in across discovery and manufacturing. Thermo Fisher’s purchase of Solventum’s Purification & Filtration unit for USD 4.1 billion exemplifies similar portfolio-broadening moves, supported by an active USD 40-50 billion M&A pipeline.

Meanwhile, technology-centric challengers harness AI to formulate reagents with accelerated iteration cycles, as evidenced by DrugGen’s near-perfect molecular-validity output. Startups introducing lyophilised RT-LAMP kits aim to disrupt traditional PCR segments by removing cold-chain constraints, appealing to decentralised testing environments. Regulatory sandboxes like the FDA Platform Designation fast-track give nimble entrants a clear route to market, forcing incumbents to escalate R&D spend and partnership activity.

Suppliers also diversify revenue through data-service models, bundling cloud-based analytics and reagent subscription plans that lock users into ecosystems. Firms able to guarantee uninterrupted supply and regulatory-compliant quality documentation differentiate themselves as customers seek risk-mitigation in the wake of pandemic-era shortages.

Biotechnology Reagents Industry Leaders

Bio-Rad Laboratories

Becton Dickinson & Company

Danaher Corporation (Beckman Coulter Inc)

Agilent Technologies

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum’s Purification & Filtration business for USD 4.1 billion to expand its bioproduction footprint and capture USD 125 million in annual synergies by year five.

- January 2025: Illumina partnered with NVIDIA to integrate AI models into sequencing workflows, enabling faster multiomic data interpretation for drug-target discovery

- October 2024: Bio-Rad Laboratories launched Vericheck ddPCR Empty-Full Capsid Kit to improve AAV-vector quality control in gene-therapy development.

- September 2024: Aurora Biosynthetics opened a GMP facility in New South Wales with AUD200 million (USD 129.4 million) state support to supply plasmid DNA and mRNA reagents to Asia-Pacific cell-&-gene-therapy clients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the biotechnology reagents market as the value generated by liquid, lyophilized, or kit-based chemical and biologic preparations that enable molecular, cellular, and analytical procedures in life-science laboratories, diagnostic centers, and bioprocess development. These include PCR mixes, cell-culture supplements, chromatography buffers, electrophoresis dyes, flow-cytometry stains, and similar consumables used up during an assay or experiment.

Scope Exclusion: Stand-alone instruments, single-use bioreactor plastics, and routine clinical chemistry reagents remain outside this assessment.

Segmentation Overview

- By Reagent Type

- Life-Science Reagents

- PCR

- Cell Culture

- Hematology

- In-vitro Diagnostics

- Other Technologies

- Analytical Reagents

- Chromatography

- Mass Spectrometry

- Electrophoresis

- Flow Cytometry

- Other Analytical Reagents

- Life-Science Reagents

- By Application

- Protein Synthesis & Purification

- Gene Expression

- DNA & RNA Analysis

- Drug Testing

- Other Applications

- By End User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organisations (CROs)

- Academic & Research Institutes

- Clinical & Diagnostic Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Desk Research

We mapped baseline volumes and spending from publicly available tier-1 sources such as the United States FDA 510(k) database, Eurostat trade codes for HS 3822 reagents, NIH and Horizon Europe grant ledgers, and annual survey data from the Japanese Reagent Association. Company 10-Ks, investor decks, and press releases complemented production cost and average selling price signals. Select licensed resources, including D&B Hoovers for financial snapshots and Dow Jones Factiva for global tender notices, helped us cross-check revenue disclosures and shipment routes. Numerous other open and subscription sources were also reviewed for context, regulatory updates, and pipeline activity.

Primary Research

Mordor analysts interviewed laboratory managers, procurement heads at biopharma firms, reagent formulators, and regional distributors across North America, Europe, and Asia-Pacific. These discussions clarified stocking cycles, price dispersion, and emerging demand around single-cell omics, thereby filling quantitative gaps and tempering early desk-based assumptions.

Market-Sizing & Forecasting

A top-down reconstruction begins with reagent import-export values and R&D outlay by end users, which are then split by technology using reported consumption ratios. Supplier roll-ups and sampled ASP × volume checks provide a selective bottom-up overlay to validate totals. Key variables, including funded gene-editing projects, installed PCR cyclers, sequencing run counts, and cell-therapy batch releases, feed a multivariate regression that projects demand to 2030 while capturing price normalization trends. Missing bottom-level datapoints are bridged through regional growth proxies agreed upon with expert respondents.

Data Validation & Update Cycle

Outputs pass variance checks versus historical trade flows and quarterly earnings. Senior reviewers challenge anomalies, and material events trigger mid-cycle refreshes. Reports are fully updated every twelve months, with a final analyst pass just before client delivery.

Why Mordor's Biotechnology Reagents Baseline Earns Confidence

Published figures differ because firms pick unequal technology baskets, convert currencies on separate dates, or assume uniform pricing curves. By anchoring values to verifiable trade and usage indicators, Mordor keeps its base case centered and repeatable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 47.84 B (2025) | Mordor Intelligence | - |

| USD 91.75 B (2024) | Global Consultancy A | Includes capital equipment and bulk media concentrates; no currency harmonization |

| USD 109.68 B (2024) | Regional Consultancy B | Uses aggregated "life-science supplies" category and applies single ASP across regions |

| USD 0.48 B (2024) | Trade Journal C | Covers only reagent-grade chemicals for academic labs, excluding diagnostics and bioprocess |

The comparison shows that market values swing when scope or pricing logic shifts. By using transparent variables, an annual refresh, and multi-step reviews, Mordor delivers a balanced baseline decision-makers can rely on.

Key Questions Answered in the Report

What is the current size of the biotechnology reagents market?

It was valued at USD 50.96 billion in 2026 and is projected to hit USD 69.98 billion by 2031.

Which reagent type dominates market revenue?

Life-Science Reagents held 55.10% of revenue in 2025, benefiting from widespread use in PCR and sequencing.

Why are Contract Research Organizations growing faster than in-house pharma labs?

Drug developers increasingly outsource specialised analytics, giving CROs a forecast 9.55% CAGR through 2031.

Which geography offers the fastest expansion opportunity?

Asia-Pacific leads with a 9.15% CAGR, aided by policy incentives and expanding CDMO capacity.

How is AI influencing reagent development?

AI platforms predict optimal reagent formulations, shortening design cycles and raising demand for automation-ready kits.

What are the key hurdles for new reagent suppliers?

Obtaining multi-region quality certifications and securing resilient supply chains add cost and delay market entry.

Page last updated on: