Sugar-Based Excipients Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.05 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sugar-Based Excipients Market Analysis by Mordor Intelligence

Sugar-based excipients market size in 2026 is estimated at USD 1.64 billion, growing from 2025 value of USD 1.57 billion with 2031 projections showing USD 2.05 billion, growing at 4.56% CAGR over 2026-2031. This expansion reflects rising demand for multifunctional carriers that simplify direct compression, accelerate orally disintegrating tablet (ODT) launches, and improve taste masking in pediatric and geriatric therapies. Co-processed platforms, spray-dried polyols, and 3-D-printable sugar matrices are reshaping formulation workflows while lowering manufacturing costs for generic producers. Contract development and manufacturing organizations (CDMOs) are scaling continuous direct-compression lines, further boosting adoption of sugar-derived binders and fillers. Regionally, North America retains leadership on the back of robust regulatory support, whereas Asia-Pacific registers the fastest uptake as China and India upgrade capacity for global exports. Competitive activity centers on acquisitions and joint ventures that combine excipient expertise with advanced process-analytical technologies.

Key Report Takeaways

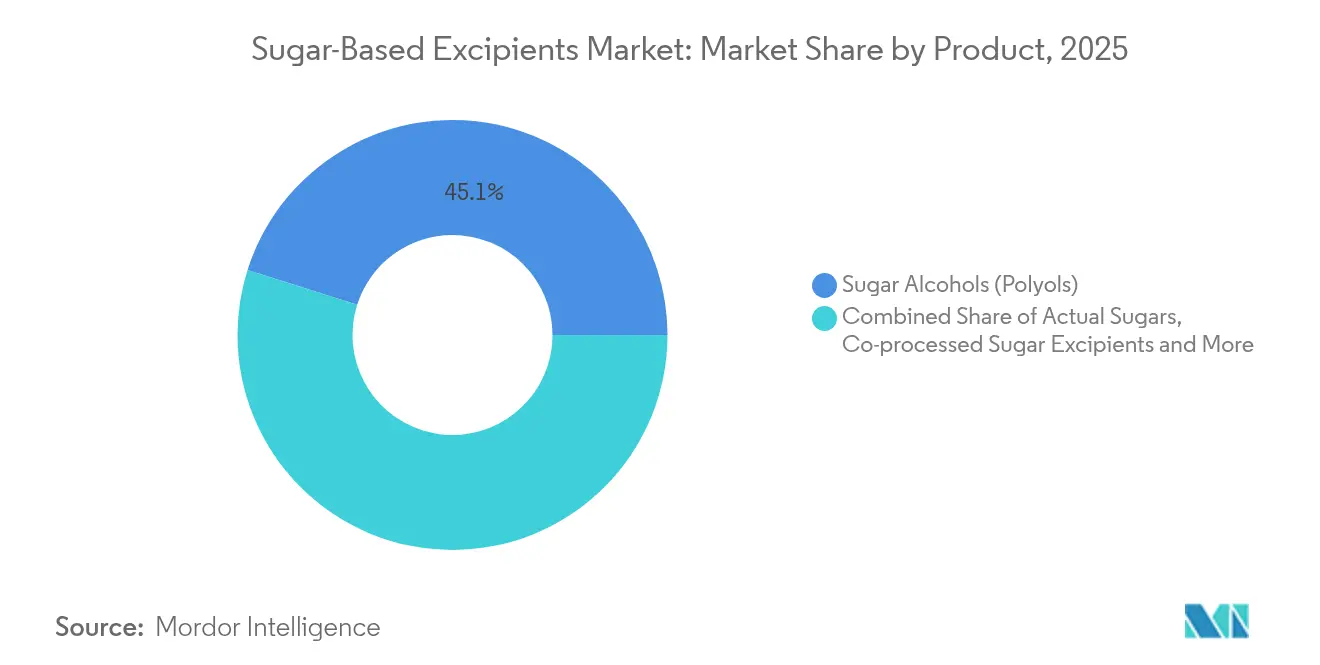

- By product category, polyols commanded 45.12% of sugar-based excipients market share in 2025, while co-processed sugars are projected to expand at an 8.18% CAGR through 2031.

- By form, direct-compression sugars held 37.12% share of the sugar-based excipients market size in 2025 and syrups & solutions are advancing at a 7.64% CAGR to 2031.

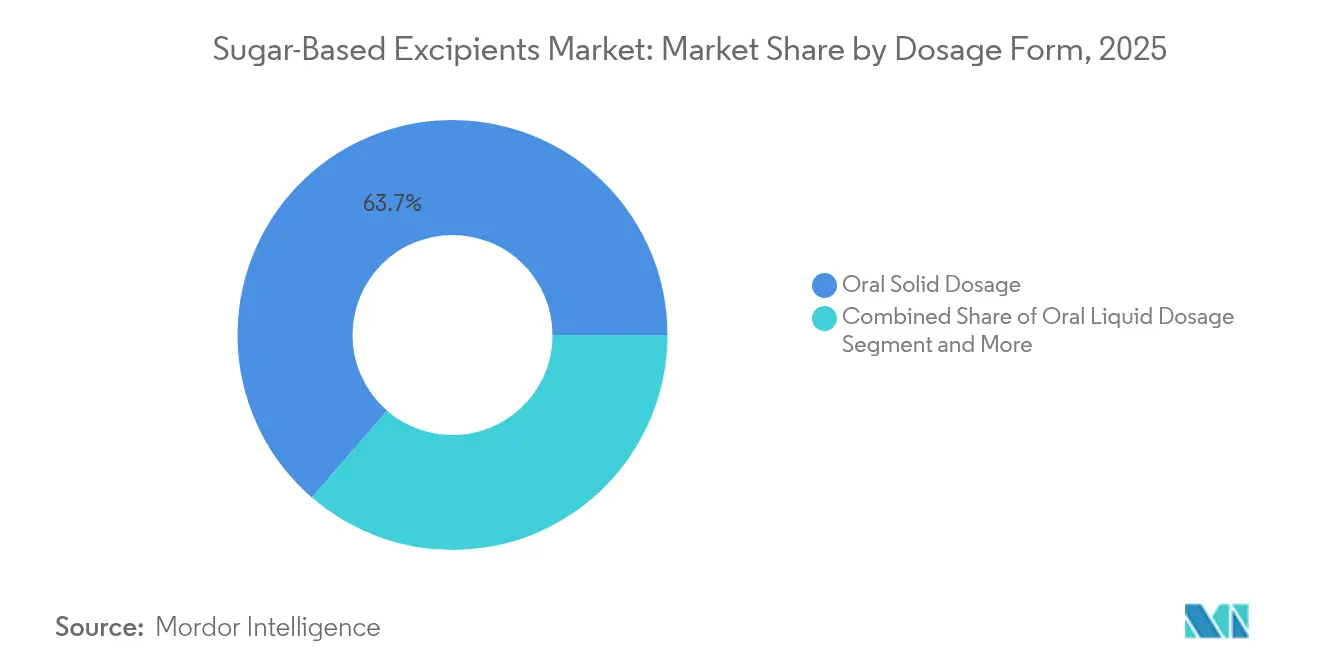

- By dosage form, oral solids accounted for 63.65% share of the sugar-based excipients market in 2025; oral liquids are set to grow at a 7.64% CAGR over the forecast period.

- By end user, generic manufacturers captured 49.78% of the sugar-based excipients market size in 2025, whereas CDMOs record the highest projected CAGR at 8.52% through 2031.

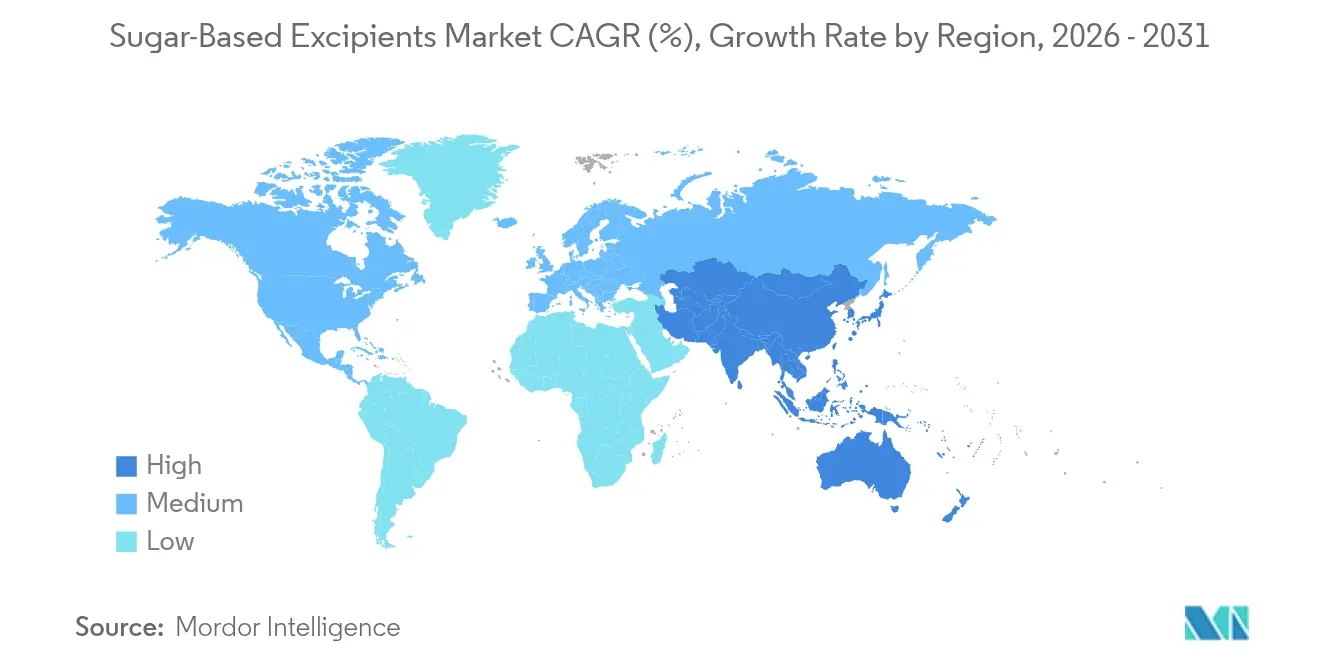

- By geography, North America led with 38.90% revenue share in 2025 and Asia-Pacific is forecast to post a 7.43% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sugar-Based Excipients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing use of co-processed excipients | +1.2% | North America & EU, spreading globally | Medium term (2–4 years) |

| Rapid expansion of the generics industry | +0.9% | Asia-Pacific core, spill-over to Latin America | Short term (≤ 2 years) |

| Surge in ODT launches | +0.8% | Developed markets worldwide | Medium term (2–4 years) |

| Demand for palatable pediatric & geriatric drugs | +0.7% | North America & EU, extending into Asia-Pacific | Long term (≥ 4 years) |

| 3-D-printed sugar matrices for personalized dosing | +0.4% | Pilot programs in North America & EU | Long term (≥ 4 years) |

| FDA novel excipient review pilot | +0.3% | United States with global ripple effects | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Increasing Use of Co-Processed Excipients

Co-processed sugars combine flowability, compressibility, and rapid dissolution in single particles that streamline direct compression and continuous manufacturing. The sugar-based excipients market is witnessing an 8.25% CAGR for these engineered blends as generic firms and CDMOs look to cut unit operations without sacrificing tablet robustness. Regulatory openness via the FDA Emerging Technology Program now shortens approval timelines for continuous direct-compression lines that rely on co-processed polyols, accelerating commercial uptake in North America and Europe[1]Food and Drug Administration, “News from Emerging Technology Program,” fda.gov.

Rapid Expansion of the Generics Industry

Generics manufacturers, which already absorb more than half of current sugar-based excipients market demand, require low-cost yet pharmacopoeia-compliant fillers to achieve bioequivalence quickly. Asian producers leverage domestic corn-based sorbitol and spray-dried mannitol to supply regional and export markets, pushing the sugar-based excipients market toward high-volume, flexible packaging formats that minimize freight and storage costs.

Surge in Orally Disintegrating Tablet Launches

ODTs improve adherence for patients who struggle with swallowing. Mannitol-rich blends deliver the desired mouthfeel and mechanical strength, and ready-to-use PEARLITOL Flash systems cut development time. Continuous 3-D printing of ODTs, recently cleared by the FDA, further strengthens demand for polyol-centered formulations in the sugar-based excipients market[2]Roquette, “Two-Component Simple Platform for ODT,” roquette.com.

Growing Demand for Palatable Formulations for Pediatric & Geriatric Cohorts

Up to 64% of pediatric non-adherence cases stem from unpleasant taste. Maltitol and mannitol mask bitterness while maintaining caloric neutrality and glycemic stability, enabling chocolate-based steroids and gummy formats that broaden therapeutic options. Updated EMA labeling rules underscore safety, reinforcing the role of well-characterized sugar excipients across vulnerable populations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-jurisdictional regulations | -0.8% | EU-US-Japan compliance triangle | Medium term (2–4 years) |

| Hygroscopicity-driven stability challenges | -0.6% | Humid regions worldwide | Short term (≤ 2 years) |

| Volatile pharma-grade sorbitol supply chain | -0.4% | Asia-Pacific production hubs | Short term (≤ 2 years) |

| Sustainability scrutiny of high-carbon sucrose | -0.3% | EU & North America regulators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Jurisdictional Regulatory Requirements

Divergent pharmacopoeial standards force manufacturers to run separate stability studies and maintain duplicate documentation, inflating development timelines. Recent EU updates on allergen disclosure add further complexity, requiring sugar-based excipient suppliers to validate every lot for residual proteins and heavy metals.

Hygroscopicity-Driven Stability Challenges

Polyols readily absorb ambient moisture, compromising tablet hardness and disintegrant efficiency. Investment in moisture-barrier coatings and desiccant blister packs raises cost of goods and slows scale-up for humidity-sensitive markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Polyols Retain Command, Co-Processing Gains Traction

Polyols account for 45.12% of sugar-based excipients market share due to their favorable compressibility, low reactivity, and familiarity among regulators. Spray-dried mannitol grades enhance flow and enable higher active loading, supporting mini-tablet and ODT formats. Actual sugars exhibit stable, niche-oriented demand in syrups and medicated confectionery. Meanwhile, the sugar-based excipients market size attributed to co-processed sugars is projected to expand at an 8.18% CAGR as formulators seek single-step solutions that deliver robust hardness and rapid dissolution. Polyol-cellulose hybrids illustrate how particle engineering delivers high bulk density with minimal dusting, translating directly into faster line speeds and lower operator exposure.

Advances in continuous direct compression technology further amplify co-processed demand by allowing feeders to meter multifunctional blends without pre-mixing. Regulatory validation under the FDA Emerging Technology Program shortens paths to commercial launch, spurring investment across both originator and generic pipelines. Suppliers that secure backward integration into raw sugar streams and invest in spray-agglomeration towers are best positioned to capture this high-margin growth pocket within the sugar-based excipients market.

By Form: Direct Compression Platforms Dominate While Liquid Systems Accelerate

Direct-compression sugars hold 37.12% share of the sugar-based excipients market. Spray drying, fluid-bed agglomeration, and co-spheronization techniques continue to improve compressibility and reduce lubricant sensitivity, aligning well with continuous tablet presses that operate at speeds exceeding 250,000 tablets/hour. Powders and granules still anchor conventional wet-granulation lines, but roll-compaction adoption is rising thanks to low-hygroscopic mannitol grades that withstand high shear without capping.

Conversely, syrups and solutions log a 7.64% CAGR, reflecting the market’s pivot toward patient-friendly liquid formats for pediatrics and geriatrics. Non-crystallizing sorbitol and glycerol-free maltitol solutions offer improved viscosity control and chemical stability, allowing formulators to reduce preservative loads. Single-phase aqueous concentrates simplify shipping and on-site dilution, cutting cold-chain requirements and widening access in emerging markets. This twin-track growth pattern underscores the sugar-based excipients market’s versatility across both high-speed solids and value-added liquid delivery channels.

By Functional Role: Fillers Anchor, Coatings Emerge

Fillers and diluents underpin 54.72% of current revenue as virtually every tablet requires bulking agents to achieve practical handling size. The sugar-based excipients market size for fillers grows in lock-step with oral solid output, driven by consistent pharmacopoeial acceptance and benign safety profiles. Binders such as syrup-solidified sucrose see steady uptake in controlled-release matrices where reproducible viscosity contributes to robust tablet integrity.

Coating agents deliver the strongest momentum with an 8.75% CAGR. Moisture-barrier films based on polyol-polysaccharide blends extend shelf life for hygroscopic active ingredients, while flavored coatings improve organoleptic profiles without adding artificial sweeteners. Nanothin mannitol layers created via fluid-bed deposition show promising moisture transmission rates and minimal weight gain, highlighting innovation depth in the sugar-based excipients market.

By Dosage Form: Oral Solids Prevail, Liquids Gain Ground

Oral solids dominate at 63.65% share of the sugar-based excipients market because tablets remain the most economical and stable dosage form. High-shear wet granulation and roller compaction integrate advanced mannitol polymorphs that enhance tablet hardness, facilitating mini-tablets for combination therapies. The surge in 3-D-printed oral solids introduces lattice geometries unattainable through traditional tooling, opening new vistas for personalized medicine.

Oral liquids expand at a 7.64% CAGR, powered by regulatory pushes for age-appropriate formulations and the rising prevalence of dysphagia. Multi-component syrup vehicles leveraging non-crystallizing sorbitol enable stable suspensions even at high active payloads, improving bioavailability for poorly soluble drugs. Sugar-free variants satisfy diabetic safety requirements, widening potential patient pools and adding to the sugar-based excipients market growth.

By End User: Generics Command, CDMOs Accelerate

Generics manufacturers account for 49.78% of sugar-based excipients market share as patent cliffs drive volume demand for cost-efficient ingredients with robust supply chains. Polyols satisfy bioequivalence criteria without altering dissolution compared with originator brands, making them the go-to choice in abbreviated new drug applications.

CDMOs, however, top growth charts at 8.52% CAGR. Their flexible asset base allows seamless integration of novel co-processed sugars and continuous mixing platforms demanded by biotech and niche pharma clients. Investments such as Hovione’s USD 170 million spray-drying capacity boost underline confidence that the sugar-based excipients market will increasingly rely on outsourced specialists for accelerated development timelines.

Geography Analysis

North America retains 38.90% of global revenue thanks to the FDA’s constructive stance on novel excipients, a deep bench of continuous manufacturing facilities, and active collaboration between academia and industry. Exclusive distribution deals, such as Univar Solutions’ agreement to supply niche cellulose-based carriers, further enrich the regional portfolio. Sustainability initiatives, exemplified by carbon-neutral blister packs derived from sugar cane, show that environmental credentials are now intertwined with excipient selection.

Europe presents a mature but innovation-driven arena. Regulatory updates on allergen labeling and a possible ban on titanium dioxide spur R&D into alternative colorants and coatings, releasing fresh opportunities for calcium-enriched sugar shells. Roquette’s USD 2.85 billion takeover of IFF Pharma Solutions marks the largest transaction in European excipients history, consolidating spray-dried polyol production under a single banner and signaling heightened competition in the sugar-based excipients market.

Asia-Pacific records the highest CAGR at 7.43%. China and India ramp up sorbitol and mannitol output, while South Korea and Singapore attract high-value biologics that require pharmaceutical-grade polyols as tonicity agents. Lotte Fine Chemical’s USD 740 million distribution pact with Colorcon positions it as the world’s largest pharmaceutical cellulose provider, underscoring the region’s strategic importance. Trade agreements under the Pharmaceutical Inspection Co-operation Scheme streamline export adherence and reinforce Asia’s role in the sugar-based excipients market.

Regulatory Landscape

Sugar-based excipients sit under global pharmaceutical excipient GMP and pharmacopoeial controls, with acceptance anchored in established compendial status and prior-use listings. In the United States, formulators reference the FDA Inactive Ingredient Database (IID) for precedent on excipient use levels and routes of administration, while the FDA Novel Excipient Review Pilot Program provides a pathway to review safety and quality packages for novel excipients outside a drug application, reducing development friction for co-processed sugars and advanced polyol grades. In Europe, the EMA clarifies expectations for co-processed excipients used in solid oral dosage forms through a risk-based classification framework, with the Q&A effective date of 01/08/2026 driving documentation improvements when co-processing changes functionality or introduces new quality attributes. Across major regions, compliance with elemental impurities controls aligned to ICH Q3D remains a core requirement, and USP procedures for elemental impurities have been updated to push excipient suppliers to tighten raw-material qualification, impurity monitoring, and lot-level traceability for pharma-grade sugars and polyols.

Value Chain Analysis

The value chain starts with agricultural feedstocks and by-products that feed sucrose and polyol pathways, then moves into purification and conversion steps to achieve pharmaceutical grade materials, typically involving multi-stage refining, activated carbon treatment, and ion-exchange polishing to meet impurity and microbiological specifications. For higher-value applications, manufacturers add ultra-high purity and low-endotoxin grades, along with processing steps like spray drying, agglomeration, or co-processing to meet direct-compression performance. Downstream, excipient makers supply through direct sales and distributors into pharma, generics, and CDMOs, where qualification and change-control shape demand. A key bottleneck remains capacity for ultra-high purity grades and GMP packaging, and long customer qualification cycles in biologics programs. North America functions as a high-value manufacturing hub but still relies on global sourcing for inputs like high-purity lactose, reinforcing dual sourcing and robust logistics for continuity.

Competitive Landscape

The sugar-based excipients market is moderately fragmented but trending toward consolidation. Roquette, ADM, and Ashland leverage acquisitions to secure raw sugar access, expand co-processing know-how, and deepen geographic footprints. Roquette’s IFF Pharma Solutions buyout adds continuous processing assets and proprietary film-coating polymers, reinforcing its leadership in the polyol segment[3]International Flavors & Fragrances, “Sale of Pharma Solutions Business,” iff.com.

Strategic collaborations complement M&A. Hovione’s joint venture with Zerion Pharma melds spray-drying expertise with drug-polymer dispersion technology, extending applicability of sugar carriers to poorly soluble molecules. Suppliers with robust process-analytical technology ecosystems, tablet press simulation capabilities, and 3-D-printing partnerships gain bargaining power with CDMOs looking for turnkey solutions.

Sustainability, supply resilience, and digital traceability emerge as new battlegrounds. Companies invest in biomass boilers, carbon-neutral logistics, and blockchain-based lot tracking to reassure clients of continuity and compliance. Those unable to certify low-carbon or GMO-free sugar streams risk exclusion from stringent EU and US supply chains, highlighting the competitive stakes ahead in the sugar-based excipients market.

Sugar-Based Excipients Industry Leaders

Roquette Group

The Lubrizol Corporation

DFE Pharma

Archer Daniels Midland

Ashland

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities center on localized pharma-grade manufacturing footprints in Asia and tighter supply assurance for high-specification excipient grades used in continuous tableting and advanced oral formats. The Ashland Ambernath facility construction (June 2026) anchors near-to-market supply for moisture-barrier and taste-masking systems that pair with sugar alcohol cores in ODTs and direct-compression platforms. Clariant's 80 million CHF expansion at its Daya Bay site (November 2025) reinforces the region as a production base for regulated export supply chains. Academic work published in September 2024 on D-xylose oxetane copolymers points to biobased building blocks that can support solubility and stability enhancements in sugar-derived excipients.

Recent Industry Developments

- June 2026: Ashland began construction of a film coatings manufacturing facility in Ambernath, Maharashtra, India, signaling a step-change in near-to-market supply for moisture-protective and taste-masking platforms used with sugar-based excipients. The project expands capacity and supports faster regional fulfillment for regulated markets.

- May 2025: Roquette completed its USD 2.85 billion acquisition of IFF Pharma Solutions and integrated the business into its Health and Pharma Solutions group, broadening its excipient portfolio and cross-functional capabilities for coating and delivery systems.

- May 2024: Roquette launched LYCAGEL Flex, a plant-based softgel excipient premix using hydroxypropyl pea starch for pharmaceutical capsules, expanding non-gelatin excipient options and intensifying competition in the specialty excipient space.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from sugar-derived excipients that are used as functional inactive ingredients in finished pharmaceutical and nutraceutical formulations, where they help with taste, stability, compressibility, and dose uniformity.

Scope exclusions: It excludes API value, primary packaging, and finished drug pricing and margins beyond the excipient component.

Segmentation Overview

- By Product

- Actual Sugars

- Sugar Alcohols (Polyols)

- Artificial / High-Intensity Sweeteners

- Co-processed Sugar Excipients

- By Form

- Powders & Granules

- Direct-Compression Sugars

- Crystals

- Syrups & Solutions

- By Functional Role

- Fillers & Diluents

- Binders

- Flavoring / Sweetening Agents

- Tonicity Modifiers

- Coating Agents

- By Dosage Form

- Oral Solid Dosage

- Oral Liquid Dosage

- Topical & Others

- By End User

- Branded Pharmaceutical Manufacturers

- Generic Pharmaceutical Manufacturers

- Nutraceutical & Dietary-Supplement Producers

- Contract Development & Manufacturing Organisations (CDMOs)

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with a clear mapping of sugar-based excipient chemistry and typical use in dosage forms, which helped keep product boundaries consistent. Public and official references were used to anchor assumptions, such as FDA Inactive Ingredient Database lookups, US Pharmacopeia and other pharmacopeial monographs, import and export statistics from customs portals, and healthcare and manufacturing statistics from agencies such as the US Census Bureau and Eurostat.

To connect supply signals to demand reality, we also reviewed company annual reports and investor presentations, excipient association websites, and peer-reviewed pharmaceutics journals that discuss direct compression performance, hygroscopicity, and ODT formulation trends. Paid database subscriptions for company financials and intelligence, patent databases, and an import and export shipment-level database were used selectively to cross-check volumes, product launches, and footprint changes. The sources listed above are illustrative, and other public references were also used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to pressure-test what desk research could not fully explain, especially how grade mix and functionality claims translate into pricing and usage rates across tablets, capsules, syrups, and specialty formats. We spoke with excipient manufacturers and distributors, formulation scientists, QA and regulatory professionals, and procurement teams from drug and nutraceutical manufacturers across APAC, EMEA, and the Americas, so assumptions could be aligned to real buying behavior. Where responses conflicted, follow-up questions were used to narrow down typical inclusion rates, substitution choices, and near-term demand changes driven by reformulation and capacity planning.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 19% | APAC: 48% |

| Mid tier: 49% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 20% | Managers: 50% | Americas: 20% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where excipient demand is reconstructed from the finished-dosage output pool and its typical excipient loading, and then filtered through the share that is sugar-derived in each major dosage form. In parallel, we corroborate totals with selective bottom-up approximations, such as sampled supplier revenue checks, regional channel discussions, and ASP times volume estimates for key sugar-based excipient groups, which are then used to adjust outliers.

The market model is guided by a small set of practical inputs that can be validated, including oral solid dose production trends, shifts toward direct compression and ODT adoption, grade and functionality mix (filler, diluent, tonicity, flavoring), average selling price progression by region, and regional manufacturing footprint changes that impact sourcing. When data gaps appear, the missing piece is bridged using proxy variables like formulation prevalence by dosage form and expert-validated price bands, and then reconciled back to the overall demand pool.

For forecasting, scenario analysis is used so the base case can reflect expected drug output growth plus formulation trends, while also allowing separate upside and downside paths for price changes and substitution effects. The final trajectory is refined using the consensus view from interviews on near-term capacity, regulatory-driven reformulation, and customer qualification timelines.

Data Validation & Update Cycle

Outputs are checked against independent signals, such as dosage-form production direction, trade movement patterns, and observed price ranges, before the numbers are signed off. If a country or region shows a jump that is not supported by at least two separate indicators, it is flagged for a deeper review and, when needed, respondents are re-contacted to confirm the cause.

A second analyst reviews the model logic, inputs, and calculations, followed by a final pass focused on reasonableness of growth rates and consistency of definitions across years. Reports are refreshed annually, and interim updates are made when material events occur, such as major capacity additions, regulatory changes affecting sweeteners and excipients, or sustained price shocks. Before delivery, an analyst completes a fresh data scan so clients receive an updated view that matches the latest available signals.

Mordor Intelligence's Sugar Based Excipients Market Size Versus Other Published Estimates

Published market sizes for sugar-based excipients often differ because the underlying scope and pricing logic are not the same, and because some models lean heavily on reported revenues while others infer demand from formulation activity. Differences also show up when a study chooses a different base year, uses a different currency timing, or does not fully reconcile dosage-form demand with excipient functionality mix.

The biggest gap driver is whether sugar-based excipients are counted only for pharma and nutraceutical formulation demand or whether food and personal care uses are also blended into the total, and in our approach Mordor Intelligence keeps the scope tied to excipient demand from these formulation uses and then validates pricing through grade-level checks rather than broad sweetener averages.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.64 B (2026) | |

| Global Report Publisher A | USD 1.49 B (2025) | Uses factory-gate value reporting with broader end-user coverage that can include non-pharma demand, and it also anchors the series to 2025 which can shift the total when prices move year to year. |

| Industry Research Publisher B | USD 1.16 B (2025) | Leans on a narrower priced demand pool with a different base year and a longer forecast window, and its category splits can lead to conservative counting when direct compression grades and functionality premiums are not fully reflected. |

Taken together, the spread mainly comes from what end uses are included and how pricing is translated from grades and functions into an average. By keeping variables explicit (dosage-form output, loading rates, grade mix, and regional price bands) and by re-checking them with interview feedback, the estimate stays traceable and repeatable even when the public data is limited.

Key Questions Answered in the Report

What is driving growth in the sugar-based excipients market?

Rising adoption of co-processed polyols, continuous direct-compression lines, and patient-centric ODTs are the main catalysts, underpinning a 4.56% CAGR to 2031.

Which segment holds the largest sugar-based excipients market share?

Polyols dominate with a 45.12% share in 2025 thanks to their compressibility, stability, and regulatory familiarity.

Why are CDMOs important for the sugar-based excipients industry?

CDMOs post an 8.52% CAGR because they offer flexible manufacturing capacity and advanced formulation expertise that drug sponsors increasingly outsource.

Which region is expanding fastest?

Asia-Pacific leads with a 7.43% CAGR as China and India scale low-cost production and South Korea invests in high-value biologics.

How are sustainability concerns affecting the market?

EU carbon-intensity metrics and potential titanium dioxide bans pressure suppliers to develop low-carbon sugar streams, biodegradable coatings, and transparent supply chains.

Page last updated on: