Benelux Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

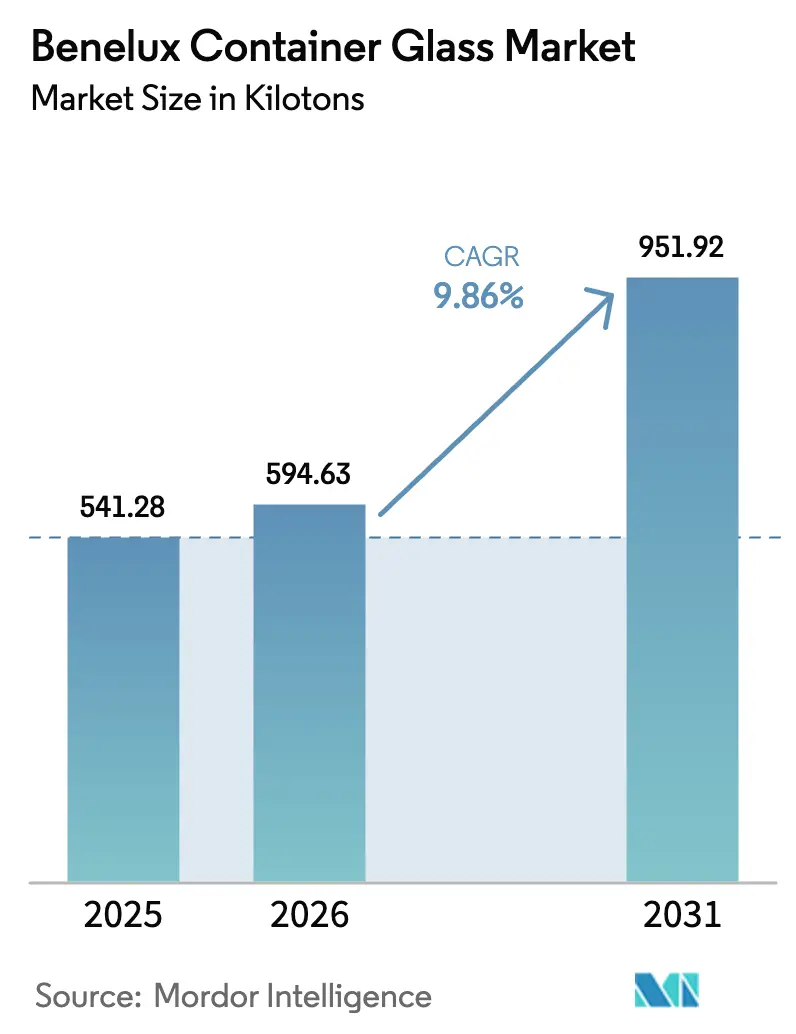

| Base Year Market Size (2025) | 541.28 kilotons |

| Market Volume (2026) | 594.63 kilotons |

| Market Volume (2031) | 951.92 kilotons |

| Growth Rate (2026 - 2031) | 9.86% CAGR |

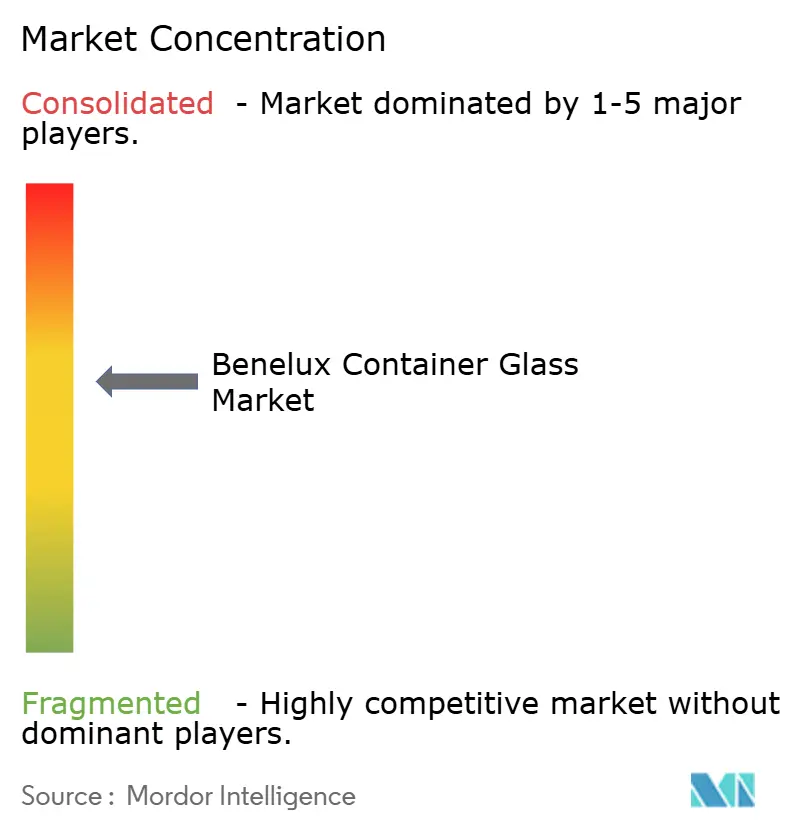

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benelux Container Glass Market Analysis by Mordor Intelligence

Benelux container glass market size in 2026 is estimated at 594.63 kilotons, growing from 2025 value of 541.28 kilotons with 2031 projections showing 951.92 kilotons, growing at 9.86% CAGR over 2026-2031. Growth is underpinned by Belgium’s leadership in extended producer responsibility rules, the proliferation of premium beverage launches that rely on glass to convey authenticity, and steady progress in lightweight furnace technology, which reduces production emissions while safeguarding margin resilience.[1]FEVE, “Glass Recycling,” feve.org Incremental advances in cullet utilization, exemplified by Saverglass achieving 90% recycled content at its Ghlin facility, further amplify the competitiveness of glass against aluminum and plastic rivals. Craft breweries continue to adopt differentiated formats that enhance shelf presence and consumer experience, while luxury cosmetics brands accelerate the adoption of refillable glass systems to reinforce their premium positioning and environmental stewardship. Collectively, these factors propel the Benelux container glass market toward a period of sustained capacity expansion, even as producers confront volatile energy prices and intensifying competition from alternative materials.

Key Report Takeaways

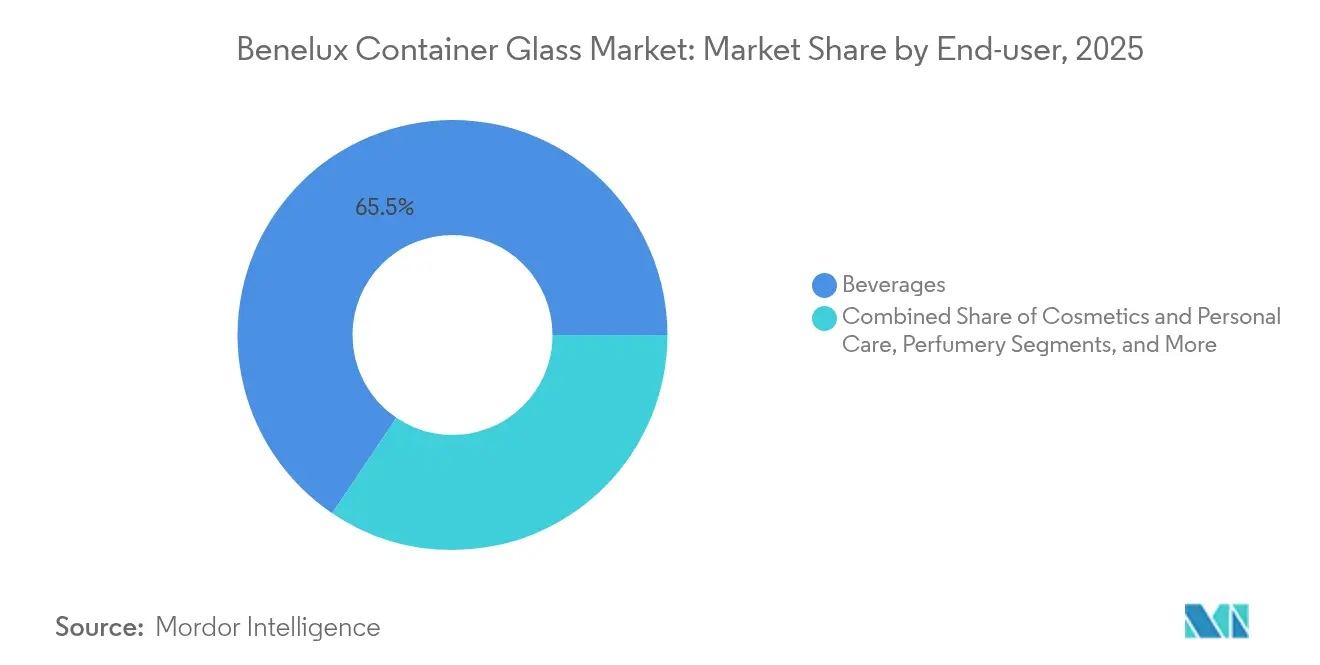

- By end-user, beverages captured 65.54% of the Benelux container glass market share in 2025.

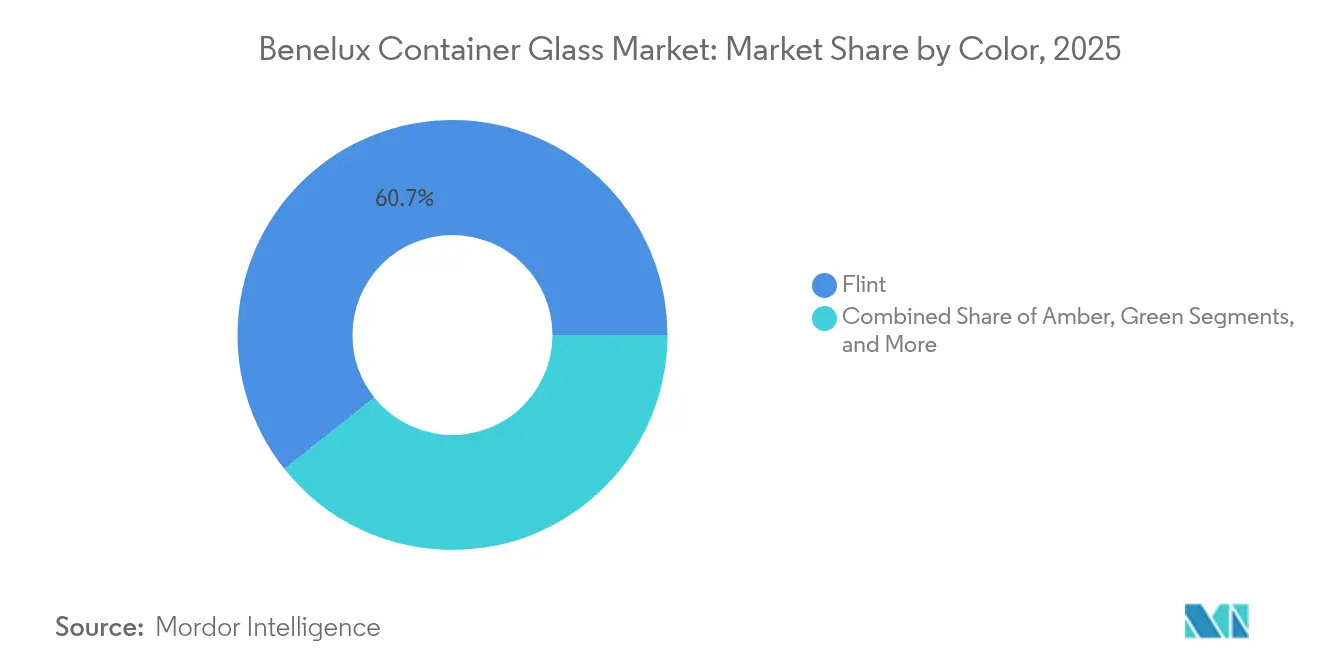

- By color, the Benelux container glass market size for the amber glass segment is projected to grow at 11.53% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Benelux Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for sustainable packaging in Belgium | +2.8% | Belgium core, spillover to the Netherlands and Luxembourg | Medium term (2-4 years) |

| Expansion of craft breweries is boosting glass bottle usage | +2.1% | Benelux region-wide, strongest in Belgium | Short term (≤ 2 years) |

| Government incentives for circular economy initiatives | +1.9% | Belgium and Netherlands primary, Luxembourg emerging | Long term (≥ 4 years) |

| Rising popularity of premium alcoholic beverages | +1.7% | Region-wide with export focus | Medium term (2-4 years) |

| Technological advancements in lightweight glass production | +1.2% | Regional manufacturing hubs | Long term (≥ 4 years) |

| Increased export activities from Belgium | +0.9% | Belgium primary, Netherlands distribution | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Sustainable Packaging in Belgium

Belgium’s Vlaanderen Circulair program incentivizes brands to adopt infinitely recyclable materials, placing glass at the forefront of corporate packaging roadmaps. Producers able to certify high cullet ratios enjoy preferential supplier status as consumer goods companies race to meet 2030 recycled-content pledges. Saverglass’s Ghlin plant exemplifies this advantage, running at 90% cullet in colored glass streams and showcasing closed-loop production as a commercial differentiator.[2]Saverglass, “CSR Report 2022-2023,” saverglass.com Sustainability credentials now intersect with premium branding, encouraging beverage and personal-care labels to exploit glass’s perceived quality. Logistics synergies across the Benelux region enable Belgian cullet to supply Dutch and Luxembourg furnaces, promoting regional demand coherence. The resulting virtuous cycle amplifies glass adoption and strengthens the Benelux container glass market against the risk of material substitution.

Expansion of Craft Breweries Boosting Glass Bottle Usage

Specialty beer exports have risen from 10% of Belgian production in 1990 to more than 50% in recent estimates, increasing demand for bespoke glass bottles that can withstand long-haul transit and effectively accentuate brand storytelling. Premium brewers secure higher per-liter prices, justifying investment in customized embossing and limited-edition formats that deepen consumer engagement. Dutch and Luxembourg breweries emulate this playbook, leveraging the Benelux region’s collective brewing heritage to secure shelf space abroad. Large groups such as Duvel Moortgat integrate eco-design principles while retaining iconic glass shapes, signaling that environmental mandates will reinforce rather than dilute premium packaging standards. Consequently, craft dynamics continue to elevate glass volumes and reinforce the Benelux container glass market’s trajectory.

Government Incentives for Circular Economy Initiatives

Benelux policy frameworks align on ambitious waste-reduction targets, creating predictable demand for recyclable packaging solutions. Belgium’s roadmap assigns clear milestones for packaging recovery, spurring investments in sorting technology and municipal collection that elevate glass return rates.[3]Renewi, “Partnership to Strengthen Glass Recycling,” renewi.com The Netherlands is debating the introduction of deposit-return systems for glass, a policy shift that could significantly expand the supply of cullet and lower production costs. Luxembourg pairs subsidies with advisory services to accelerate the deployment of reusable glass in hospitality venues. The convergence of fiscal and regulatory incentives amplifies the Benelux container glass market’s growth runway by mitigating one of the sector’s historic bottlenecks, feedstock availability.

Rising Popularity of Premium Alcoholic Beverages

Premium spirits, craft wines, and artisanal liqueurs are increasingly relying on colored glass to preserve flavor integrity and differentiate themselves on crowded shelves. Saverglass reports expanding order books for tall-neck and heavy-base bottles tailored to aged rum and small-batch gin, signaling robust demand in higher-margin SKUs. Export-oriented brands use glass design to reinforce regional authenticity, supporting value capture in North American and Asian markets. Amber and violet glass formats also meet functional requirements by filtering out damaging wavelengths, thereby reducing the need for additives. The nexus of premiumization and sustainability strengthens the Benelux container glass market, as glass simultaneously conveys luxury and environmental responsibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy consumption in glass manufacturing | -1.8% | Regional manufacturing centers | Short term (≤ 2 years) |

| Competition from alternative packaging materials | -1.4% | Benelux region-wide | Medium term (2-4 years) |

| Fluctuating raw material prices affecting production costs | -0.9% | Regional supply chains | Short term (≤ 2 years) |

| Infrastructure challenges in recycling processes | -0.7% | Netherlands and Belgium primary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Energy Consumption in Glass Manufacturing

Natural gas currently supplies around 73% of the sector’s energy mix, exposing producers to price shocks and carbon-trading costs that erode margins. Volatility intensified after geopolitical disruptions in 2024, prompting accelerated investment in electric melters and hybrid furnaces. O-I’s USD 65 million electrification outlay at Veauche illustrates the scale of capital required to decarbonize legacy assets. Smaller Benelux plants face funding constraints that could induce consolidation if energy prices remain elevated. Although technology solutions are progressing, the near-term cost burden remains the most significant headwind to the Benelux container glass market.

Competition from Alternative Packaging Materials

Aluminum cans cool faster, weigh less, and already achieve high recycling rates, making them attractive to beverage producers keen to reduce logistics emissions. Plastic suppliers tout enhanced barrier resins and mono-material designs that facilitate chemical recycling, eroding the traditional functional advantages of glass in food and personal care. Some beverage multinationals now adopt dual-format strategies, selecting cans for e-commerce and glass for on-premise channels. At the same time, premium beverages and pharmaceuticals continue to rely on glass, substitution pressure forces Benelux manufacturers to elevate design innovation and sustainability communication to defend volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Drive Volume While Cosmetics Accelerate Growth

Beverages accounted for 65.54% of the Benelux container glass market share in 2025, reflecting entrenched brewing traditions and an expanding premium spirits base that relies on specialized formats for brand storytelling. The alcoholic subsegment favors heavy-base bottles and custom embossing to signal authenticity, while craft sodas and cold-pressed juices adopt clear flint containers that accentuate natural colors. These dynamics underpin the Benelux container glass market size for beverages at 354.86 kilotons in 2025, projected to increase steadily through 2031 as regional exports expand. In parallel, non-alcoholic beverages leverage returnable glass systems in hospitality channels, underpinning steady baseline demand.

The cosmetics and personal care sector represents the fastest-growing application, with an 10.72% CAGR, driven by luxury skincare labels that position glass as both a premium material and a reusable vessel. Refillable jars, featuring zamak outer shells and replaceable glass inserts, exemplify innovation that balances aesthetics with waste reduction. Niche perfumery houses in Luxembourg further amplify value per ton by commissioning intricate flacons that merge artistic design and functional barrier performance. Consequently, the Benelux container glass market size allocated to cosmetics is poised to nearly double by 2031, raising competition for furnace capacity traditionally dedicated to beverages.

By Color: Flint Dominance Meets Amber Innovation

Flint glass held 60.72% of the Benelux container glass market share in 2025 because transparency supports ingredient visibility and label versatility across food, beverages, and cosmetics. Producers leverage economies of scale to keep Flint unit costs low, preserving its role as the default choice for cost-sensitive applications. Nevertheless, higher purity requirements constrain recycled content levels, prompting sustainability-minded brands to explore colored alternatives. The segment’s growth remains steady but modest compared with specialty shades.

Amber glass, expanding at an 11.53% CAGR, satisfies stringent photoprotection needs for pharmaceuticals, premium beer, and botanicals. The segment benefits from the ability to incorporate larger cullet volumes without compromising aesthetics, enhancing environmental credentials. Miron Violetglass pushes the frontier with biophotonic properties that filter specific wavelengths, commanding premium pricing in wellness and gourmet segments. As consumer interest in natural preservatives grows, demand for light-shielding containers is likely to outpace the growth of flint, increasing the complexity of color mixes within the Benelux container glass market.

Geography Analysis

Belgium anchors production with legacy facilities that combine high-end craftsmanship and advanced sustainability practices. Saverglass’s Ghlin plant exemplifies circular manufacturing, reaching 90% cullet in colored runs and supplying export-oriented beverage clients across Europe. Government programs such as Vlaanderen Circulair provide financial incentives that offset furnace retrofit costs, thereby stabilizing the Benelux container glass market size in the country and supporting incremental capacity upgrades.

The Netherlands functions as the region’s logistics and recycling linchpin. Partnerships between Renewi and Maltha Glasrecycling bolster cullet throughput, ensuring consistent feedstock for Dutch and Belgian furnaces. Hoogeveen-based Miron Violetglass capitalizes on multimodal freight corridors to ship biophotonic containers worldwide, underscoring the country’s pivotal role in value-added export flows. The ongoing policy debate on deposit-return schemes is expected to increase collection rates, directly benefiting the Benelux container glass market by reducing raw material costs and emissions.

Luxembourg, despite its small geography, commands outsized influence in premium niches. Affluent consumers readily pay for artisanal condiments and prestige cosmetics packed in distinctive glass, attracting boutique fillers that use the country as a launchpad for wider EU distribution. Cross-border e-commerce integration allows Luxembourg producers to tap Dutch and Belgian fulfillment networks, amplifying the Benelux container glass market’s aggregate value capture without necessitating large-scale furnace infrastructure locally.

Competitive Landscape

The Benelux container glass market is moderately consolidated, with global giants such as Ardagh, O-I, and Gerresheimer operating alongside specialized brands like Saverglass and Miron Violetglass. Scale allows large groups to negotiate favorable energy contracts and invest in hybrid melting technologies; Gerresheimer targets a 25,000-tonne annual CO₂ cut through partial electrification at its Lohr furnace, reinforcing its sustainability brand proposition. O-I’s Fit-to-Win program signals further rationalization, with at least 7% global capacity earmarked for closure by mid-2025, potentially reducing regional supply slack.

Regional specialists exploit agility to serve premium micro-segments. Saverglass leverages design studios in Belgium and France to create bespoke spirits bottles that command higher margins, while Miron Violetglass scales patented light-filtering technology through direct-to-brand sales channels. Consolidation continues, evidenced by Verallia’s USD 251 million acquisition of Vidrala’s Italian assets and TricorBraun’s entry into the DACH glass distribution arena. These moves underscore the pursuit of geographic and portfolio diversification to buffer against demand cyclicality.

Manufacturers increasingly compete on environmental metrics, publishing annual ESG targets and engaging in multi-stakeholder recycling initiatives. Hybrid furnace pilots, closed-loop cullet sourcing, and lightweight bottle platforms represent key battlegrounds. The interplay of scale economies and niche specialization suggests ongoing mergers at one end of the spectrum and vibrant entrepreneurial activity at the other, shaping the competitive contours of the Benelux container glass market through 2030.

Benelux Container Glass Industry Leaders

Gerresheimer AG

Ardagh Group S.A

O-I Glass, Inc.

Gaasch Packaging

Saverglass Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Gerresheimer announced hybrid furnace deployment at Lohr, Germany, aiming for 50% green electricity utilization and a 25,000-tonne annual CO₂ reduction.

- January 2025: TricorBraun agreed to acquire Euroglas and Glaspack, expanding its European reach.

- July 2024: Verallia completed its EUR 230 million (USD 251 million) acquisition of Vidrala’s Italian operations, adding 225,000 tonnes capacity.

- July 2024: O-I Glass invested USD 65 million in electrification at its Veauche, France site to lower emissions.

Benelux Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

Benelux Container Glass Market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, by color (green, amber, flint and other colors) and by country (Belgium, Netherlands, and Luxembourg).). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large is the Benelux container glass market in 2026?

The Benelux container glass market size stands at 594.63 kilotons in 2026 with a 9.86% CAGR outlook to 2031.

Which segment contributes the most volume?

Beverages account for 65.54% of total volume, underpinned by the region’s brewing heritage and premium spirits demand.

What is the fastest-growing application area?

Cosmetics and personal care lead growth with an 10.72% CAGR through 2031, driven by refillable luxury packaging.

Why is amber glass gaining traction?

Amber offers superior light protection, making it ideal for pharmaceuticals and specialty beverages, and is expanding at an 11.53% CAGR.

How are manufacturers reducing carbon emissions?

Producers invest in hybrid and electric furnaces, lightweight bottle designs, and higher cullet incorporation to cut energy use and CO₂ output.

Which country dominates production capacity?

Belgium hosts the largest furnace capacity, benefiting from established glass clusters and supportive circular economy policies.

Page last updated on: