Belgium ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

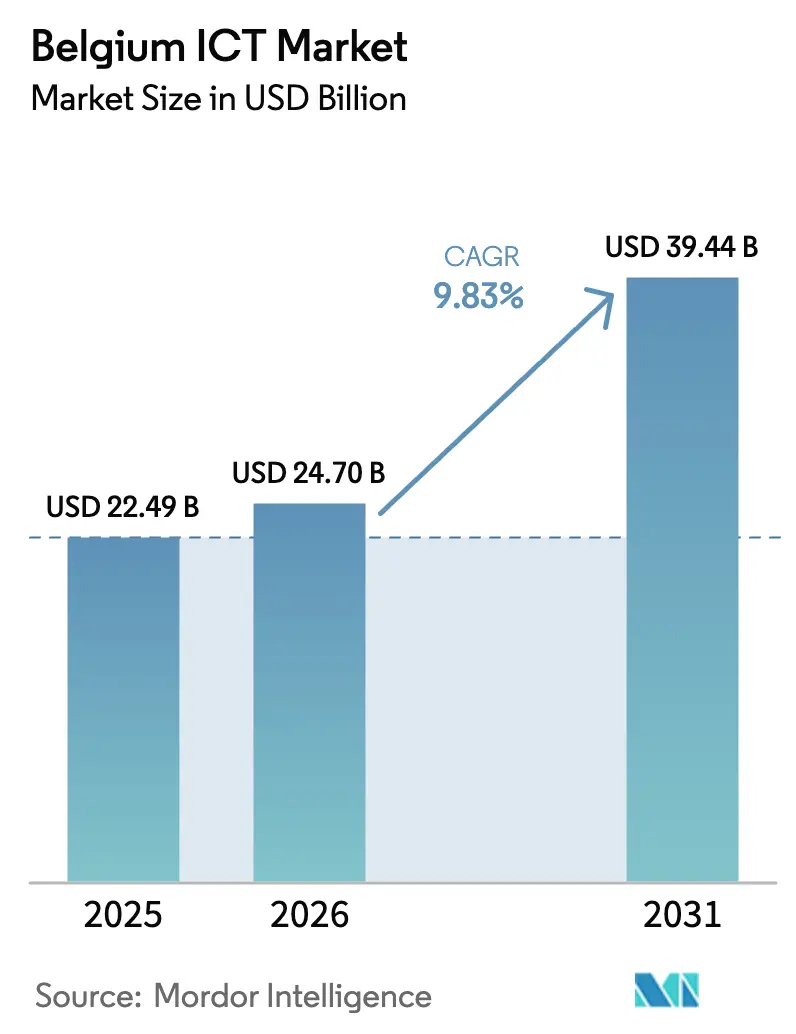

| Base Year Market Size (2025) | USD 22.49 Billion |

| Market Size (2026) | USD 24.7 Billion |

| Market Size (2031) | USD 39.44 Billion |

| Growth Rate (2026 - 2031) | 9.83% CAGR |

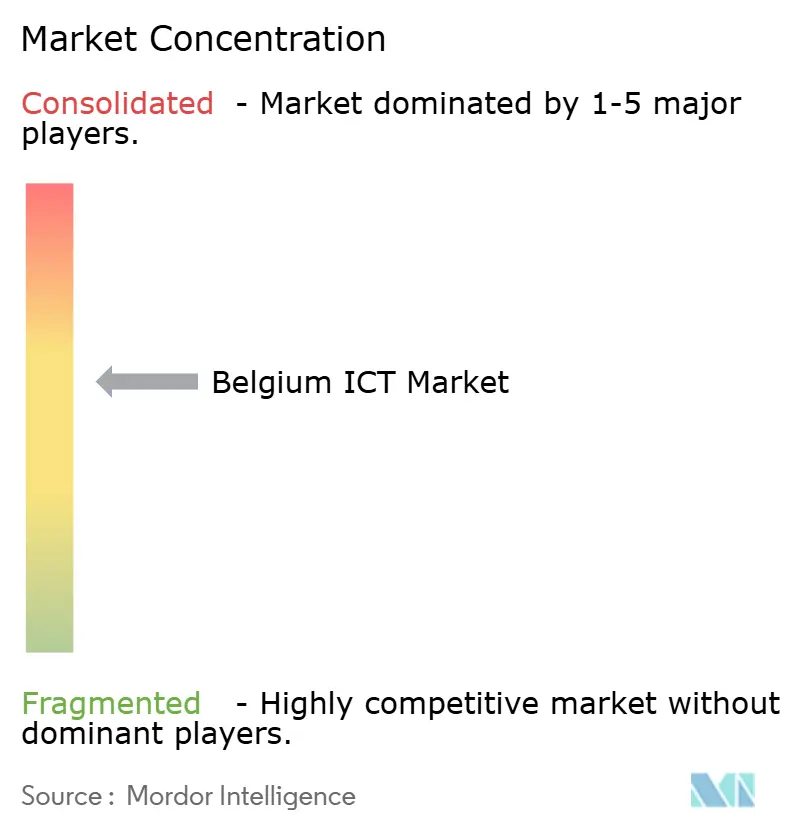

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium ICT Market Analysis by Mordor Intelligence

Belgium ICT market size in 2026 is estimated at USD 24.7 billion, growing from 2025 value of USD 22.49 billion with 2031 projections showing USD 39.44 billion, growing at 9.83% CAGR over 2026-2031. This trajectory reflects strong enterprise cloud migration, rapid 5G roll-outs and an assertive federal digital agenda, positioning the Belgium ICT market as one of Western Europe’s fastest‐expanding digital ecosystems. Brussels’ unique role as an EU regulatory capital and AI innovation hub amplifies technology demand across governance, healthcare and financial services, while nationwide data-center investments strengthen the country’s status as an EU latency-critical node. Competitive intensity remains moderate: domestic telecom incumbents hold essential network assets, yet global cloud hyperscalers deepen local footprints through sovereign-cloud arrangements. Parallel government incentives spur SME cloud adoption, raise cybersecurity baselines under NIS2 and drive greener ICT procurement, collectively widening addressable opportunities inside the Belgium ICT market.

Key Report Takeaways

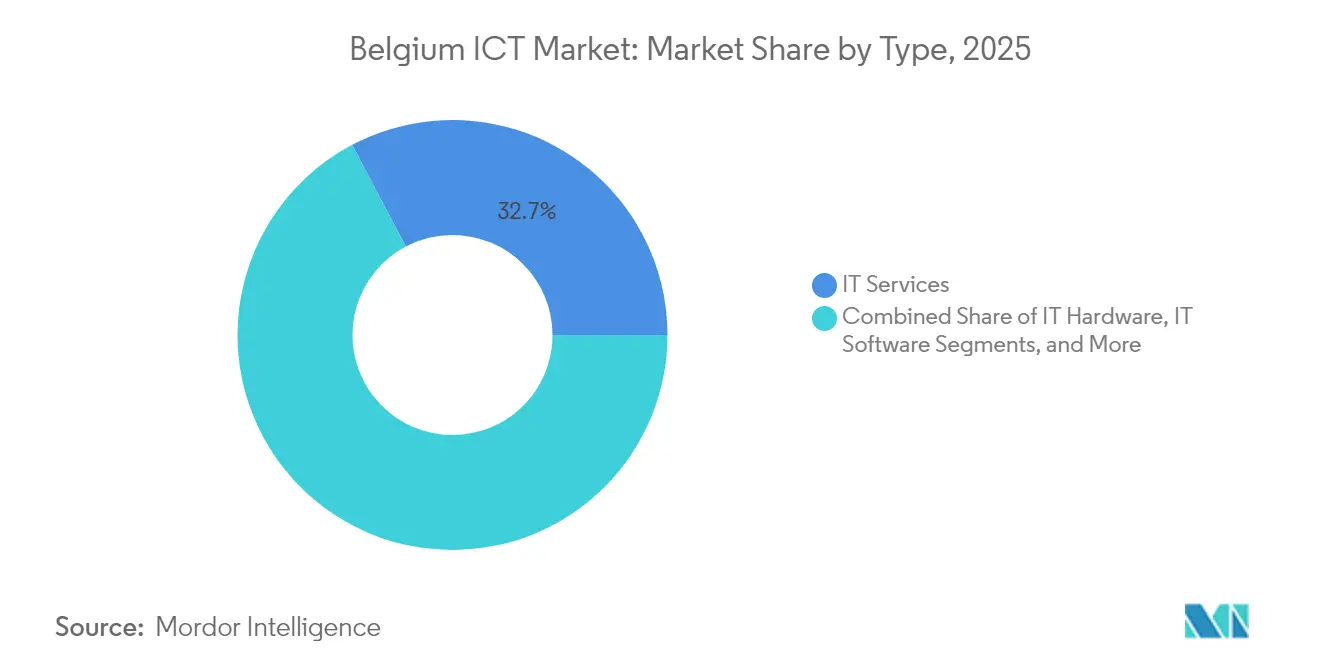

- By type, IT Services led with 32.73% Belgium ICT market share in 2025; Cloud Services is advancing at a 10.12% CAGR to 2031.

- By enterprise size, large enterprises held 60.52% of the Belgium ICT market size in 2025, whereas SMEs are projected to expand at a 10.31% CAGR through 2031.

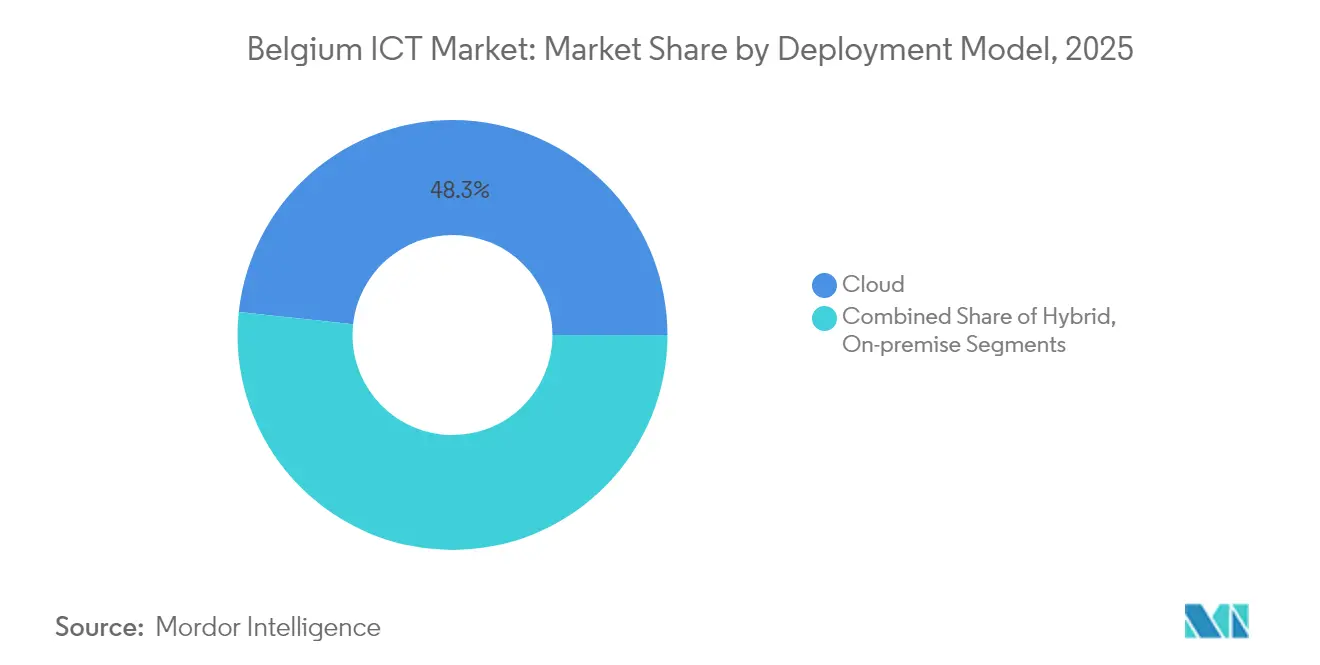

- By deployment model, cloud captured 48.29% of the Belgium ICT market size in 2025, while hybrid solutions post the highest CAGR at 10.92% between 2026-2031.

- By end-user vertical, government and public administration commanded 23.51% Belgium ICT market share in 2025, with healthcare and life sciences forecast to grow at an 11.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Belgium ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G roll-out | +1.8% | Brussels, Antwerp, Ghent corridors | Medium term (2-4 years) |

| Government digital agenda | +2.1% | Nationwide, Brussels-centered | Long term (≥ 4 years) |

| Cloud-first strategies in SMEs | +1.5% | Flanders lead | Medium term (2-4 years) |

| Expansion of e-government platforms | +1.3% | Federal and regional | Long term (≥ 4 years) |

| Green ICT aligned with EU climate goals | +1.2% | EU-wide, early Belgian uptake | Long term (≥ 4 years) |

| Edge data-center build-out around Brussels | +2.1% | Capital metro | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Roll-out

Nation-wide 5G spectrum auctions completed in 2024 enabled Proximus, Orange Belgium and Telenet to light up private 5G networks that power logistics automation in Antwerp Port and real-time imaging in az groeninge hospital. [1]Proximus, “Sovereign Cloud via Microsoft or Google,” proximus.be Low-latency connectivity catalyzes new SaaS, IoT and AR use cases, lifting upstream demand across the Belgium ICT market. Device makers and systems integrators bundle 5G modules with analytics services, creating recurring revenue streams that reinforce managed-services growth.

Government Digital Agenda

The federal convergence plan outlines 70 initiatives ranging from single-sign-on citizen portals to AI-based justice workflows, all of which mandate cloud-native architectures and stringent GDPR compliance. A reinforced G-Cloud framework standardizes sovereign-cloud procurement, pushing ministries toward multicloud orchestration and zero-trust security solutions that enlarge addressable spend for the Belgium ICT market.

Cloud-First SME Strategies

EU Digital Innovation Hubs deliver vouchers and assessments that let Belgian SMEs pivot from on-premise servers to managed SaaS platforms at predictable OpEx. Over 1,400 Belgian SMEs leveraging Amazon’s marketplaces generated EUR 350 million (USD 410.31 million) export revenue in 2023, underscoring cloud’s role as a growth lever. This switch accelerates subscription-based software uptake and fuels edge-security demand among cash-constrained but growth-oriented firms.

E-Government Platform Expansion

Digital Brussels and its “Once-Only” principle drive interoperability across 589 federal data sets, fostering API marketplaces and multilingual UX layers. As adoption scales, integrators see steady pipelines for workflow automation, identity management and analytics, sustaining double-digit services growth inside the Belgium ICT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High labor costs and IT-talent gaps | -1.4% | Brussels and Flanders | Short term (≤ 2 years) |

| Legacy public-sector systems | -0.9% | Federal and regional | Long term (≥ 4 years) |

| Tri-lingual regulatory complexity | -0.6% | Nationwide | Medium term (2-4 years) |

| Data-sovereignty concerns over non-EU clouds | -0.8% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy Public-Sector Infrastructure

Mainframe aging in social-security agencies and fragmented municipal ERP estates delay digital services and anchor Opex, muting innovation until phased migrations complete. Systems integrators engage in decade-long modernization contracts, but procurement cycles elongate revenue recognition. [2]Kyndryl, “How One Belgian Bank Boosted Its Regulatory Readiness,” kyndryl.com

High Labor Costs and Talent Gaps

Cybersecurity analyst salaries rose 13% YoY in 2024, outpacing EU averages and squeezing MSP margins. Enterprises compensate by adopting AIOps and low-code platforms that reduce headcount reliance, indirectly boosting platform software revenues in the Belgium ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Service-Centric Growth Sustains Momentum

IT Services accounted for 32.73% of Belgium ICT market share in 2025, underpinned by demand for regulatory compliance consulting and multilingual help-desk outsourcing. Cloud-Services posted the fastest 10.12% CAGR, elevating the Belgium ICT market size for subscription offerings as Proximus, Microsoft and Google launch sovereign zones that satisfy residency mandates. Hardware refresh cycles flatten because workloads shift into IaaS, yet networking equipment sales remain buoyant, tied to edge-node densification around Brussels.

Service providers pivot toward outcome-based contracts, blending AI-automation with managed security to mitigate talent shortages. Hardware vendors reposition as solution orchestrators, bundling appliances with managed storage or DRaaS. Security remains the cross-selling anchor as NIS2 compels critical-sector audits, sustaining double-digit revenue taps for MSSPs inside the Belgium ICT market.

By Enterprise Size: SME Digitization Outpaces Corporate Upgrades

Large enterprises generated 60.52% of Belgium ICT market size in 2025 on the back of compliance-heavy programs in BFSI, telecom and utilities. Yet SMEs log a sharper 10.31% CAGR, aided by grant-financed ERP roll-outs and SaaS invoicing that curb upfront capex. SMEs’ cloud-native greenfield stacks leapfrog legacy, tilting the Belgium ICT market toward platform-as-a-service add-ons, whereas corporates prioritize hybrid consolidation and FinOps discipline.

Scale-ups in Ghent and Leuven adopt AI-toolchains for product analytics, driving incremental demand for GPU instances and MLOps services. Conversely, enterprises confront data-gravity issues that tether sensitive workloads on-prem, catalyzing demand for data-fabric software and converged backup appliances.

By Deployment Model: Hybrid Architecture Gains Center Stage

Cloud deployments led with 48.29% Belgium ICT market size in 2025, anchored by SaaS HR and CRM workloads. Regulatory trepidation, however, propels hybrid models to an 10.92% CAGR as BFSI and healthcare oblige local data retention yet seek cloud elasticity. Multicloud brokerage portals and service-mesh overlays become must-have tooling, carving new sub-segments in the Belgium ICT market.

On-prem infrastructure declines in unit shipments but persists for latency-sensitive manufacturing and secure government enclaves. Vendors respond with edge-appliance form factors and “cloud-like” subscription pricing, blurring lines between capex and opex to preserve wallet share.

By End-User Vertical: Healthcare Leads Growth Curve

Government and public administration retained 23.51% Belgium ICT market share in 2025, but healthcare and life sciences accelerate at 11.24% CAGR as ePrescription, teleconsultation and AI imaging receive parliamentary funding. Private hospitals deploy private 5G for real-time telemetry; pharma clusters in Wallonia invest in high-performance computing for molecule discovery, enlarging storage-network demand inside the Belgium ICT market.

BFSI outfits like Belfius overhaul resiliency to align with DORA, commissioning hybrid DR sites and zero-trust overlays. Manufacturing orchestrates Industry 4.0 pilots using 5G and edge analytics, expanding the sensor footprint and real-time SCADA integrations.

Geography Analysis

Belgium’s compact territory speeds technology diffusion: 5G covers 98% population and average fiber availability exceeds 70%, offering fertile ground for latency-critical cloud services. Brussels doubles as EU rule-making hub and AI research cluster, attracting EUR 54 million (USD 63.30 million) in Horizon Europe funding for edge operating systems, cementing its place within the Belgium ICT market. The capital’s multilingual policy niche fuels demand for translation APIs and policy-tech platforms among institutions and NGOs.

Flanders commands startup dynamism; Ghent and Antwerp raised EUR 309.985 million (USD 363.21 million) in H1 2024 across proptech and robotics ventures, steering regional chip design demand and AI inference workloads that fortify the Belgium ICT market. Logistics heavyweights exploit 5G along Antwerp-Bruges Port corridor, deploying real-time container tracking, which lifts edge-network service revenues. Educational institutes like imec anchor semiconductor R&D, prompting colocation builds in Leuven that amplify regional data gravity.

Wallonia benefits from hyperscale investment: Google’s EUR 1 billion (USD 1.17 billion) data-center expansion in Farciennes plus Openchip’s AI-chip fab in collaboration with imec spark digital job creation. Local authorities prioritize green-energy sourcing, urging suppliers to certify carbon-free operations, which influences procurement scoring in the Belgium ICT market. Cross-border proximity to France, Luxembourg and Germany invites multinational deployments that leverage Belgium as a regulatory-stable, latency-optimized gateway.

Competitive Landscape

Domestic telcos-Proximus, Orange Belgium and Telenet-own fiber, mobile and edge-data-center assets, commanding network backbones vital for private 5G and sovereign-cloud offloads. Proximus’ partnerships with Microsoft and Google launch in-country sovereign zones, giving the Belgium ICT market native hyperscale capacity without cross-border data transfer. Orange Belgium pilots network-slicing APIs for B2B monetization, while Telenet bundles SD-WAN with security gateways for SMEs.

Home-grown integrators Cegeka, NRB and Inetum-Realdolmen specialize in multilingual public-sector and BFSI digitization. Cegeka’s EUR 150 million acquisition of U.S.-based CTG broadens nearshore delivery, evidencing outbound expansion strength. International vendors-Microsoft, AWS, IBM, SAP-localize offerings via Brussels-based data centers, embed EU AI-Act compliance tools and cultivate partner academies to alleviate talent shortages. Private-equity activity intensifies: IceLake Capital injects funds into Microsoft partner Rubicon, signaling confidence in cloud advisory niches.

Market rivalry shifts from pure pricing to compliance trust and sustainability credentials. Vendors differentiate through ISO 27001 extensions, sovereign hosting options and green PPA sourcing. Consolidation likelihood remains moderate; however, niche cybersecurity firms may attract mid-size integrators seeking NIS2 verticalization, reshaping competitive stakes in the Belgium ICT market.

Belgium ICT Industry Leaders

Proximus Group SA

Orange Belgium SA

Telenet Group Holding NV

Cegeka NV

NRB SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Openchip opened an AI-chip branch in Ghent’s Winter Circus with imec collaboration, targeting first production in 2027.

- March 2025: TINC, Datacenter United and Proximus closed a data-center transaction expanding Brussels-area edge capacity.

- December 2024: Cegeka finalized EUR 150 million CTG acquisition to boost global cloud services.

- July 2024: Corilus secured PSG investment to enhance digital-health platforms.

Belgium ICT Market Report Scope

Information and communications technology (ICT) is a broad term encompassing information technology (IT) with a focus on integrating telecommunications (both wired and wireless) with computing systems. This integration includes essential components like enterprise software, middleware, storage, and audiovisual tools. The goal is to facilitate users in accessing, storing, transmitting, and effectively utilizing information.

The report covers the Belgian ICT market companies. The market is segmented by type (hardware, software, IT services, and telecommunication services), size of enterprise (small and medium enterprises and large enterprises), and industry vertical (BFSI, IT and telecom, government, retail and e-commerce, manufacturing, energy and utilities, and other industry verticals). The report offers market sizes and forecasts in value (USD) for all the above segments.

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| (Up/Mid/Down-stream) |

| Gaming and Esports |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| (Up/Mid/Down-stream) | ||

| Gaming and Esports | ||

Key Questions Answered in the Report

How large is the Belgium ICT market in 2026 and what growth is expected by 2031?

It stands at USD 24.7 billion in 2026 and is projected to hit USD 39.44 billion by 2031, posting a 9.83% CAGR.

Which ICT segment generates the most revenue in Belgium?

IT Services leads, holding 32.73% market share in 2025, thanks to managed services and compliance consulting demand.

What deployment model is expanding fastest in Belgian enterprises?

Hybrid cloud shows the strongest pace with an 10.92% CAGR because firms balance data-sovereignty needs with cloud scalability.

Which vertical is forecast to grow quickest through 2031?

Healthcare and life sciences, supported by telehealth funding and private 5G hospital networks, will grow at 11.24% CAGR.

What is the biggest obstacle to ICT growth in Belgium?

High labor costs and a cybersecurity-talent gap reduce project agility and raise delivery costs.

Page last updated on: