Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

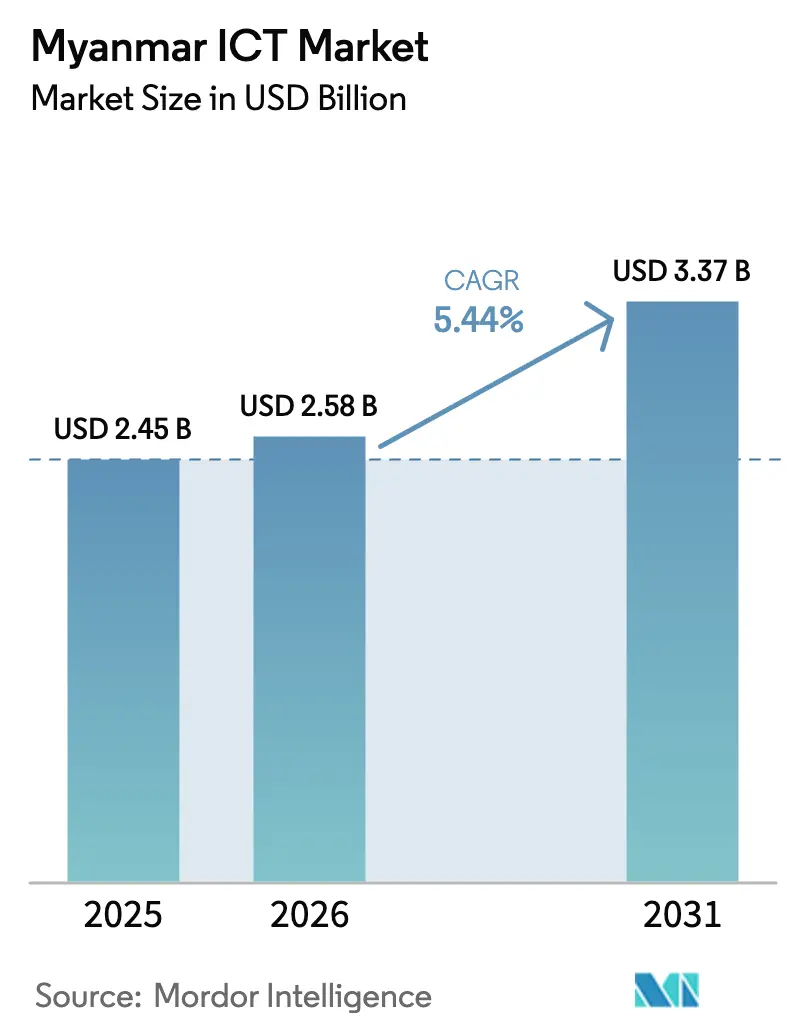

| Base Year Market Size (2025) | USD 2.45 Billion |

| Market Size (2026) | USD 2.58 Billion |

| Market Size (2031) | USD 3.37 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

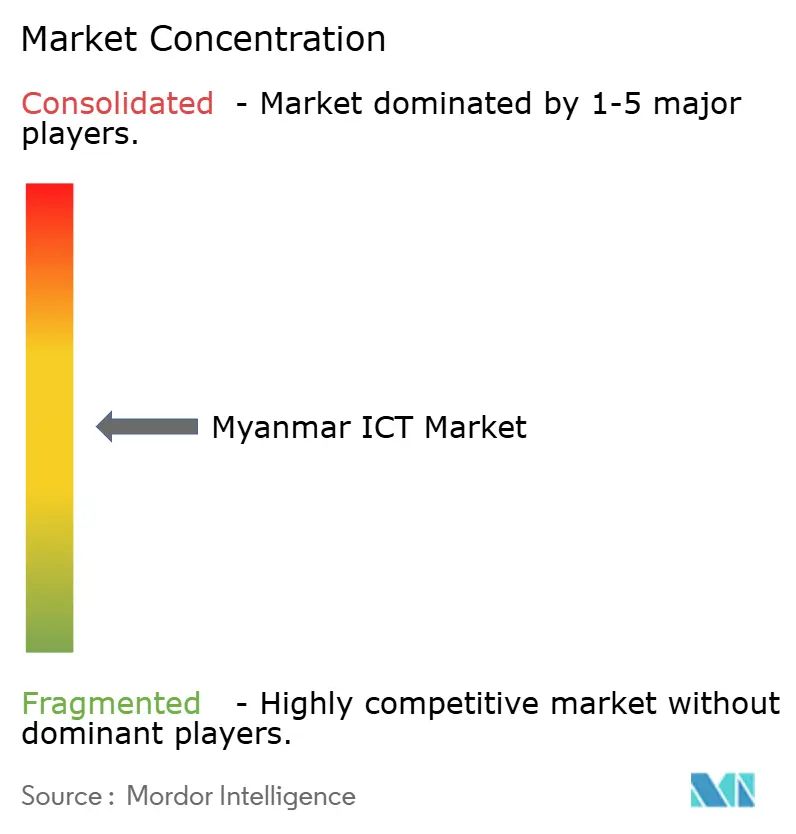

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Myanmar ICT Market Analysis by Mordor Intelligence

The Myanmar ICT market size was valued at USD 2.45 billion in 2025 and estimated to grow from USD 2.58 billion in 2026 to reach USD 3.37 billion by 2031, at a CAGR of 5.44% during the forecast period (2026-2031). Robust mobile adoption, government-backed digitization policies, and fresh subsea cable capacity shape the growth trajectory despite political risk and infrastructure gaps. Communication services anchor investment as operators accelerate 4G rollout and stage early 5G trials, while cloud-first strategies help enterprises sidestep capital constraints. Managed security gains traction after the 2025 Cybersecurity Law imposed new compliance mandates, and community wireless initiatives open rural demand. Gaming and esports show outsized momentum thanks to improved handset affordability and a growing pool of competitive players. Supply risks stem from chronic power outages, sanctions that limit foreign capital, and data-localization costs, yet local firms continue to capture whitespace left by risk-averse multinationals.

Key Report Takeaways

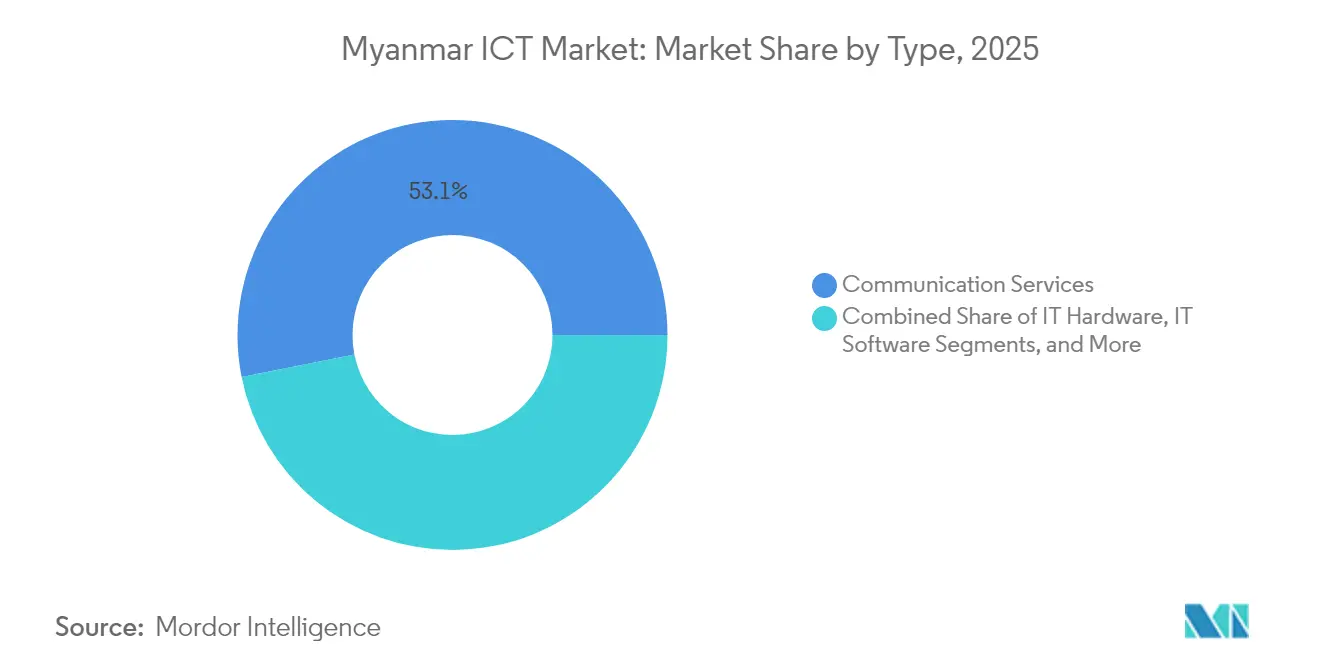

- By type, communication services led with 53.12% revenue share in 2025. IT services is forecast to expand at a 5.95% CAGR through 2031.

- By enterprise size, small and medium enterprises held 62.10% of the Myanmar ICT market share in 2025. The same segment is projected to grow at a 5.58% CAGR through 2031.

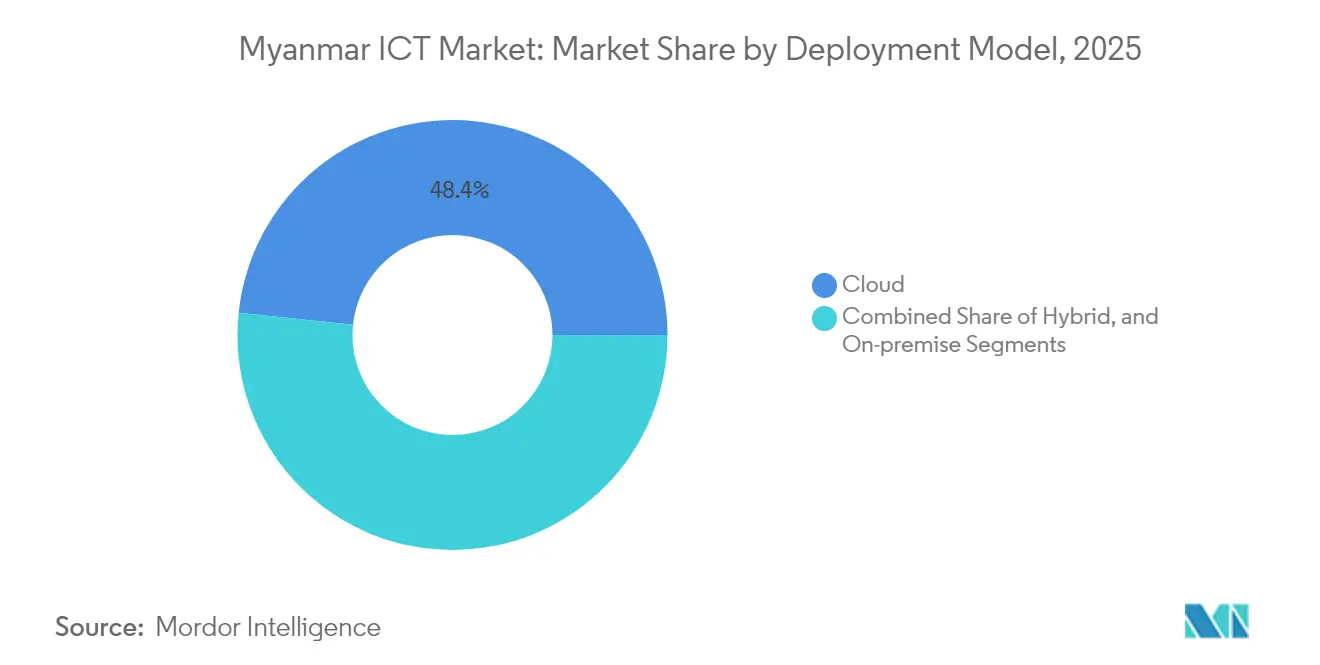

- By deployment model, cloud commanded 48.35% share of the Myanmar ICT market size in 2025. Cloud is projected to advance at a 5.60% CAGR between 2026-2031.

- By end-user vertical, government and public administration accounted for a 21.60% share of the Myanmar ICT market size in 2025. Gaming and esports is advancing at a 6.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Myanmar ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government digital transformation initiatives | +1.5% | Nationwide, early traction in Yangon, Mandalay, Naypyidaw | Medium term (2-4 years) |

| Rapid mobile and internet penetration | +1.2% | Urban centers spreading to rural areas | Short term (≤ 2 years) |

| Expansion of affordable 4G-5G infrastructure | +0.8% | Economic corridors | Medium term (2-4 years) |

| Surge in community wireless networks | +0.6% | Rural and conflict-affected regions | Long term (≥ 4 years) |

| Demand for managed security after e-commerce rules | +0.4% | Commercial hubs | Short term (≤ 2 years) |

| New subsea cable landings | +0.3% | Coastal regions extending inland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Digital Transformation Initiatives

Public-sector ICT spend is rising as 14 ministries execute the National Digital Government Strategy. Projects include e-ID rollout, inter-agency data platforms, and blockchain-based land records, lifting demand for cloud, integration, and cybersecurity services.

Rapid Mobile and Internet Penetration

Smartphone adoption surged as inexpensive Android models replaced feature phones, and operators expanded prepaid distribution to over 720,000 retail points. Rising data usage fuels cloud adoption and mobile commerce, expanding the Myanmar ICT market to rural districts.[1]Studio Dradio Durans, “Myanmar Mobile,” studiodradiodurans.com

Expansion of Affordable 4G-5G Infrastructure

ATOM Myanmar’s LTE-only launch drew 60,000 users in its first month, proving latent demand for fast data and mapping a path to shared-network 5G deployment that can lower unit costs for operators and enterprises.

New Subsea Cable Landings Enabling Data-Center Growth

The MIST cable and other systems cut latency and boost international bandwidth, spurring local data-center builds in a market that still hosts only six facilities, far below regional peers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political instability and sanctions | −0.9% | Nationwide, severe on foreign investment | Short term (≤ 2 years) |

| Chronic power outages | −0.7% | Rural and industrial areas | Medium term (2-4 years) |

| High-skill ICT brain drain | −0.5% | Urban tech hubs | Medium term (2-4 years) |

| Costly surveillance and data-localization mandates | −0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Political Instability and Sanctions

Uncertain regulations and targeted sanctions stalled several foreign-funded projects; however, the gap allowed regional partners to engage through joint ventures that align with new compliance realities.[2]Visual Rebellion, “In Myanmar, Solar Power Isn't Just About Being Green—It's a Matter of Survival,” visualrebellion.org

Chronic Power Outages

National generation capacity fell to 2,964 MW in 2022, forcing firms to buy generators or solar kits, which inflates ICT operating costs but also spurs off-grid renewable solutions for telecom towers and edge data sites.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Communication Services Drive Infrastructure Investment

Communication services accounted for 53.12% of the Myanmar ICT market size in 2025 and remain the backbone of digital growth. Network expansion enables downstream demand for IT services and security, while hardware sales track the rollout of base stations and customer-premise equipment. The Myanmar ICT market share for IT services is set to rise with a 5.95% CAGR as firms outsource migration, integration, and support tasks. Low-cost equipment providers help operators contain capex, and managed security vendors gain contracts linked to new compliance rules.

Steady hardware orders come from carrier network builds and end-user upgrades, although supply-chain hurdles may affect the timeline. Software adoption is on the rise as government e-services require process digitization and local language interfaces. Vendors bundle infrastructure, applications, and managed services, creating integrated deals that cater to resource-constrained buyers.

By Enterprise Size: SME Digital Acceleration

SMEs held 62.10% of the Myanmar ICT market share in 2025 and post a 5.58% CAGR outlook as mobile-first cloud tools lower entry barriers. Subscription SaaS and pay-as-you-go infrastructure fit cash-flow realities, letting firms digitize sales, finance, and supply management with minimal upfront spend. Large enterprises invest more per seat, often in hybrid clouds, advanced security, and analytics, supporting specialized service revenue for system integrators.

Local consultancies such as Information Matrix tailor e-government and SME solutions, illustrating a homegrown support ecosystem. Donor-funded programs that promote digital payments and e-commerce onboarding further propel SME tech use. Workforce skilling remains essential as talent outflow constrains scaling for both SME and large-enterprise projects.

By Deployment Model: Cloud-First Strategy Gains Momentum

Cloud deployments represented 48.35% of the Myanmar ICT market size in 2025 and are growing at 5.60% CAGR as firms bypass legacy hardware. Hybrid cloud interest rises when data-localization rules bind critical workloads inside the country yet need global platforms for scalability. On-premise persists in finance and government workloads that must meet strict control or latency needs.

The Myanmar ICT market benefits from forthcoming domestic data centers that allow hyperscale partners to meet location mandates while expanding regional node presence. Local providers shape service portfolios around compliance consulting, managed Kubernetes, and disaster recovery. Energy shortages push demand for efficient cooling and renewable energy in new facilities, influencing total cost of ownership calculations.

By End-user Industry Vertical: Government Leads Digital Transformation

Government and public administration contributed 21.60% of 2025 spending as ministries digitized citizen services and internal workflows. Procurements span biometric ID, blockchain land registration, and digital tax platforms, anchoring long-tail opportunities for local integrators. Gaming and esports, the fastest-growing vertical with a 6.10% CAGR, rides on mobile broadband availability and a player base that has earned USD 1.42 million in prize money across 267 athletes, placing the country 72nd globally.

BFSI modernizes core systems and mobile wallets, while utilities roll out smart-meter pilots. Hospitals also pilot telehealth calls, showing cost advantages of USD 1.6 per session compared to in-person care. The manufacturing adoption of Industry 4.0 remains early, but is catalyzed by 4G/5G private networks that enable sensor data and RPA on the shop floor.

Geography Analysis

Growth clusters in Yangon, Mandalay, and Naypyidaw where telecom density, enterprise headquarters, and skilled labor attract ICT rollouts. These corridors host most cloud implementations and data-center projects, tightening competition for limited colocation space and clean power. Government agencies based in Naypyidaw drive demand for secure communication links that interconnect provincial offices with central systems.

Border areas with Thailand and China gain from cross-border fiber and trade platforms that extend the Myanmar ICT market into logistics, e-commerce, and customs digitization. Enhanced subsea and terrestrial links reduce latency, encouraging regional cloud players to serve Myanmar workloads from nearby PoPs. Secondary cities see rising 4G coverage and pilot 5G zones as operators vie for early adopter mindshare.

Rural districts rely on community wireless and satellite links, giving specialized ISPs and equipment makers opportunities in low-power networking. Solar-backed base stations and micro data centers counter frequent outages and reduce diesel costs. NGOs and ed-tech providers leverage these setups to deliver health and learning apps, gradually narrowing the digital divide.

Competitive Landscape

The Myanmar ICT market features moderate fragmentation as sanctions prompted some foreign exits, while local firms scaled to fill supply gaps. Telecommunications remains concentrated among MPT, Ooredoo, and ATOM, yet IT services and software niches contain many small consultancies and start-ups. Domestic developers benefit from language localization skills and proximity to regulators navigating the 2025 cybersecurity mandates.

Partnership strategies dominate foreign engagement. Huawei continued supporting Ooredoo’s BSS overhaul through a services-led model that reduces political exposure. Regional cloud players pursue joint ventures with local data-center owners to align with localization rules. Managed security providers such as VSS Myanmar add value through compliance expertise amid rising breach risks.

Competitive tactics center on bundled offerings combining connectivity, cloud, and security. Pricing flexibility, rapid deployment, and local language support offer differentiation. Talent retention poses a threat as skilled engineers leave for overseas positions, leading firms to invest in upskilling programs and university partnerships to replenish the pipeline.

Myanmar ICT Industry Leaders

Myanma Posts and Telecommunications Public Co.

Ooredoo Myanmar Limited

Atom Myanmar Limited

Frontiir Co., Ltd.

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: ATOM Myanmar secured 60,000 LTE-only subscribers within one month of launch, underpinned by a modern BSS platform that enabled tiered data plans.

- January 2025: Myanmar Investments International Limited reaffirmed commitments in telecom, finance, and tech infrastructure with typical deal sizes of USD 5-25 million.

- January 2025: VSS Myanmar broadened cybersecurity offerings to meet localization and compliance demand.

- December 2024: Maharnet rolled out higher-speed broadband plans for Yangon and Mandalay homes and SMEs.

Myanmar ICT Market Report Scope

Myanmar's ICT market includes deep analysis of critical technology investments such as cloud technologies and artificial intelligence.

Myanmar ICT Market is segmented by type (hardware, software, IT services, telecommunication services), by the size of the enterprise (small and medium enterprises, large enterprises), by end-user vertical (BFSI, IT & Telecom, government, retail, and E-Commerce, manufacturing, energy, and utilities, and other industry verticals).

The market sizes and forecasts are provided in value (USD million) for all the above segments.

By Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

By End-User Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By Deployment Model

| On-premise |

| Cloud |

| Hybrid |

By End-user Industry Vertical

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| (Up/Mid/Down-stream) |

| Gaming and Esports |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By End-User Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| (Up/Mid/Down-stream) | ||

| Gaming and Esports | ||

Key Questions Answered in the Report

What is the current value of the Myanmar ICT market?

The Myanmar ICT market size is USD 2.58 billion in 2026 and is projected to reach USD 3.37 billion by 2031.

Which segment captures the largest share of ICT spending?

Communication services hold 53.12% of 2025 spending, reflecting the priority on connectivity rollout.

How fast is the cloud segment growing?

Cloud deployments are expanding at a 5.60% CAGR between 2026-2031 as enterprises adopt pay-as-you-grow models.

Why is gaming considered a high-growth vertical in Myanmar?

Mobile broadband access and a USD 1.42 million esports earnings pool support a 6.10% CAGR in the vertical.

What are the main risks facing technology investors in Myanmar?

Political instability, power shortages, and data-localization mandates weigh on cost and project timelines.

How concentrated is competition among telecom operators?

Three national operators dominate radio access networks, yet IT services and software remain fragmented, offering entry points for niche players.

Page last updated on: