Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

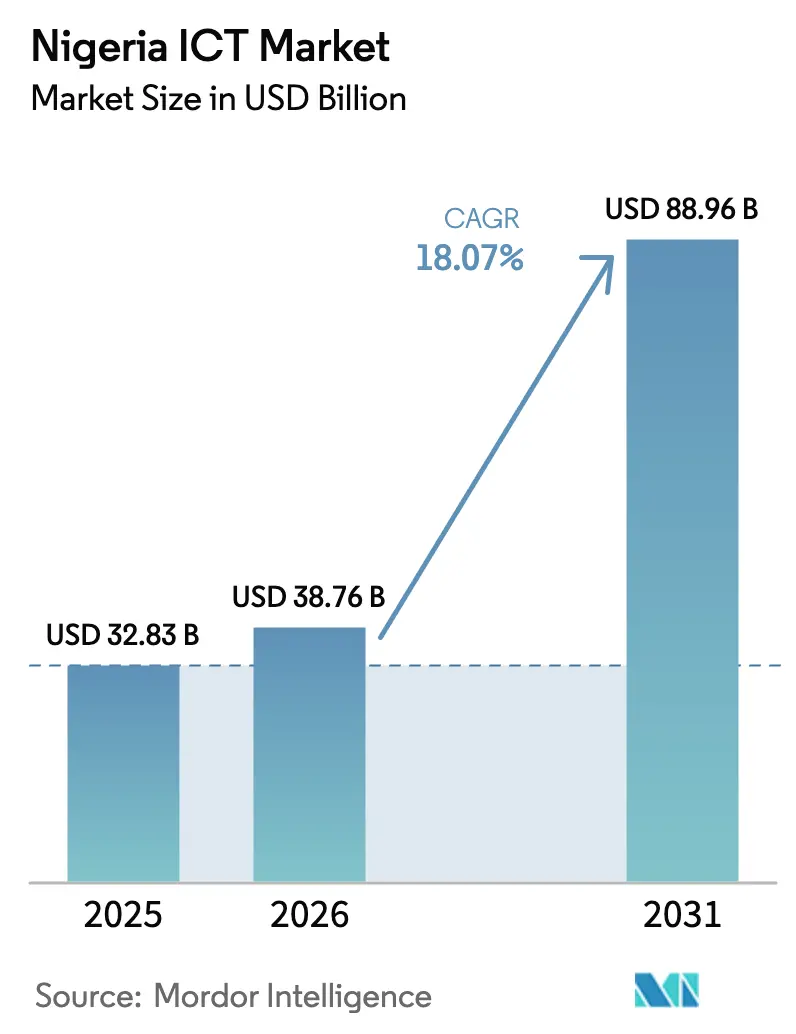

| Base Year Market Size (2025) | USD 32.83 Billion |

| Market Size (2026) | USD 38.76 Billion |

| Market Size (2031) | USD 88.96 Billion |

| Growth Rate (2026 - 2031) | 18.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria ICT Market Analysis by Mordor Intelligence

The Nigeria ICT market size is expected to grow from USD 32.83 billion in 2025 to USD 38.76 billion in 2026 and is forecast to reach USD 88.96 billion by 2031 at 18.07% CAGR over 2026-2031. Rapid enterprise digitization, accelerated 5G deployment, and government cloud‐first mandates form the backbone of this expansion. Tier-III and Tier-IV data‐center build-outs beyond Lagos, coupled with multiple sub-sea cable landings, are broadening nationwide connectivity. Currency depreciation is nudging firms toward locally billed cloud alternatives while simultaneously inflating imported hardware costs. Competitive strategies now hinge on hybrid deployment models, indigenous content requirements, and power-resilient infrastructure investments. Managed security services are poised for strong uptake as the cyber-talent gap widens, even as the Nigeria ICT market attracts record data-center inflows from telecom operators and hyperscalers.

Key Report Takeaways

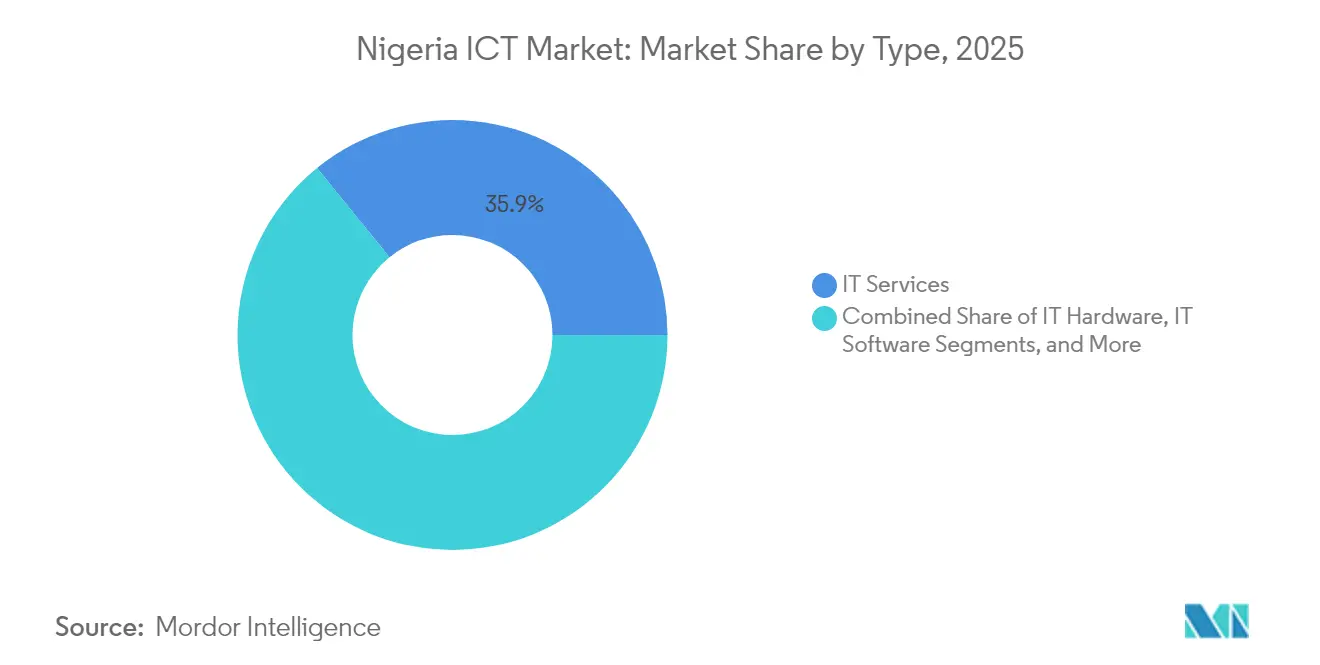

- By type, IT Services led with 35.85% revenue share in 2025; Cloud Services is forecast to expand at a 19.78% CAGR to 2031.

- By enterprise size, Large Enterprises held 58.10% of the Nigeria ICT market share in 2025, while SMEs record the highest projected CAGR at 15.90% through 2031.

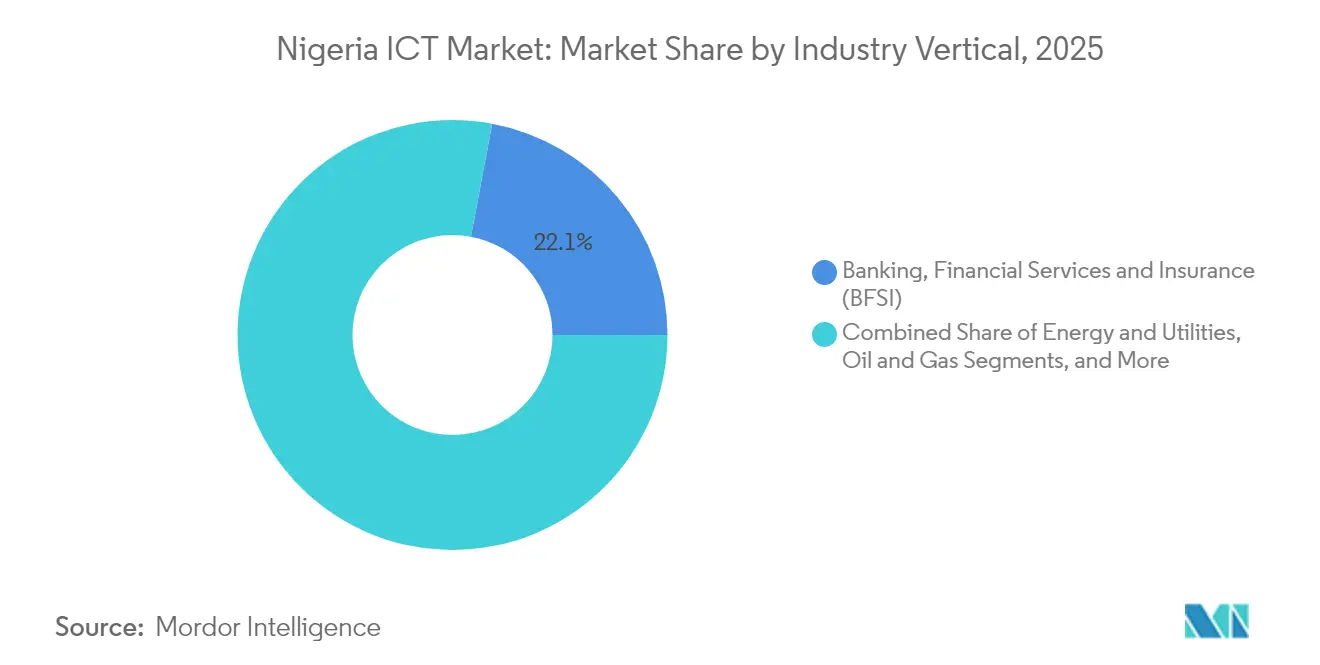

- By industry vertical, BFSI captured 22.05% share of the Nigeria ICT market size in 2025 and Gaming and Esports is advancing at a 21.45% CAGR through 2031.

- By deployment model, On-premise led with 42.30% revenue share in 2025; Cloud-only is forecast to expand at a 20.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise-wide digitalization surge | +4.2% | Lagos, Abuja, Port Harcourt | Medium term (2-4 years) |

| Nationwide 5G roll-out | +3.8% | Urban commercial hubs | Long term (≥ 4 years) |

| Cloud-first and e-government policy push | +3.1% | Federal and state agencies | Medium term (2-4 years) |

| Fintech-driven cash-lite economy | +2.9% | Nationwide, rural agent networks | Short term (≤ 2 years) |

| Tier-III/IV data-center expansion | +2.4% | Abuja, Port Harcourt, Kano, Ibadan | Long term (≥ 4 years) |

| Sub-sea cable landings | +1.8% | Coastal states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Enterprise-Wide Digitalization

Large corporates are prioritizing cloud-native workloads and AI analytics to remain competitive. Zenith Bank’s leap in pre-tax profit underscores measurable returns from digital banking investments, while the federal 3 Million Tech Talent program targets the skills deficit hampering adoption. Manufacturing is embracing Industry 4.0 platforms to curb downtime and cut energy costs, and the EU’s EUR 820 million pledge underpins multi-sector upgrade momentum [1]U.S. Department of Commerce, “Nigeria – Digital Economy,” trade.gov.

Nationwide 5G Roll-out and Spectrum Auctions

Subscriber uptake crossed 4 million within two years of launch, with MTN covering 35.70% of the population - outpacing regional peers[2]Nigerian Communications Commission, “Press Release: ITU Ranks Nigeria High in Digital Transformation Readiness,” ncc.gov.ng. Airtel’s fresh spectrum purchase validates long-term monetization prospects, and the regulator’s early exploration of 6G showcases a forward-looking spectrum policy. While Nigeria ranks 105th on the global 5G/4G index, the Authorisation Framework now gives operators clearer guidelines for small-cell densification.

Government Cloud-First and E-Government Mandates

The National Digital Economy Policy and Strategy assigns ICT a central role in GDP uplift, and the Nigerian Data Stack - due within months - will rationalize public-sector data consolidation. State agencies must adhere to 40% local‐content sourcing, bolstering domestic providers. The Nigeria Data Protection Act anchors trust by prescribing penalties of up to 2% of annual gross revenue for breaches, making compliance a non-negotiable line item.

Explosion of Fintech and Cash-Lite Transactions

Digital payments account for the bulk of new transaction value, aided by the cNGN stablecoin and eNaira NFC rollout. Instant‐payment value hit NGN 387 trillion in 2023, and international investors continue to funnel capital into payment gateways. SMEs leverage these rails to expand addressable markets, reinforcing a virtuous cycle of fintech innovation and usage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-grid unreliability | -3.7% | Nation-wide; acute for data centers | Long term (≥ 4 years) |

| Foreign-exchange shortages | -2.9% | All import-dependent sectors | Medium term (2-4 years) |

| Cyber-talent out-migration | -2.1% | Lagos and Abuja tech clusters | Medium term (2-4 years) |

| Post-subsidy inflation | -1.8% | Low-income consumer segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Power-Grid Unreliability Inflating OpEx

Only 60% of Nigerians have grid access, compelling ICT operators to budget aggressively for diesel or hybrid power. Data-center players must build N+1 redundancy, raising total cost of ownership and stretching payback periods. The 2023 Electricity Act decentralizes regulation, enabling states like Lagos to court independent power producers. Parallel minigrid initiatives financed by a USD 750 million World Bank loan aim to narrow the access gap [3]IEEE Spectrum, “Nigerians Seek Freedom from Failing National Grid,” spectrum.ieee.org.

Prolonged FX Shortages Hurting Hardware Imports

The naira has slid 70% against the USD since mid-2023, pushing up hardware procurement costs and squeezing capital budgets. Import volatility has already shuttered hundreds of manufacturers, and telecom capex inflows fell 70.5% in 2023. To hedge, enterprises pivot toward naira-denominated cloud services and stretch asset life cycles, but network quality risks materialize when upgrades are deferred.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cloud Services Disrupt Traditional IT Hierarchy

Cloud Services is set to add the largest absolute dollar value to the Nigeria ICT market size, expanding at a 19.78% CAGR as enterprises modernize legacy estates. Local cloud startups advertise data-sovereignty compliance and sub-second latency, undercutting global hyperscalers on pricing. IT Services remains indispensable for systems integration, although tighter FX liquidity is prompting managed-service providers to source refurbished hardware locally. Communication Services benefit from the 2Africa cable, which trims international bandwidth costs and supports over-the-top application growth.

The Nigeria ICT market continues to witness bundled offerings that merge colocation, connectivity, and cloud under a single SLA. Hyperscalers such as Huawei and Microsoft have invested in regional availability zones to guarantee in-country data residency, while telcos bundle edge compute with 5G to serve latency‐sensitive uses. IT Hardware faces import headwinds, but 5G radios and optical fiber remain procurement priorities. NITDA’s 40% local-content rule channels federal spend toward indigenous software vendors, injecting fresh demand for coding, testing, and DevOps talent.

By Enterprise Size: SME Digital Adoption Accelerates

Large Enterprises constitute the bulk of 2025 spending on account of mandatory core‐banking, ERP, and cybersecurity renewals, locking in 58.10% of the Nigeria ICT market share. Yet SMEs are the growth engine, climbing at 15.90% CAGR as cloud marketplaces remove entry barriers. Mobile point-of-sale devices and agent banking networks enable small retailers to tap digital payments economically. Cisco’s EDGE Center and similar accelerators democratize access to training, helping SMEs to leapfrog fixed-line constraints with cloud telephony and SaaS back offices.

Fintech collaboration is integral to SME inclusion, with unified digital identity enrollment catalyzing a 25% uptick in new account openings. Grant schemes targeting blockchain and AI start-ups sweeten the investment climate, and pay-as-you-go compute models align well with cashflow cycles. Large Enterprises, however, are adopting zero-trust architectures and multi-cloud disaster-recovery sites, a trend that trickles down as service providers productize these features for the mid-market.

By Industry Vertical: Gaming Disrupts Traditional BFSI Leadership

BFSI continues to account for the single-largest slice of Nigeria ICT market size as open-banking APIs and digital KYC automations proliferate. Gaming and Esports, while starting from a smaller base, is expanding fastest at 21.45% CAGR, fueled by youth demographics and rising 4G/5G handset penetration. International publishers partner with local studios to tailor content for regional tastes, and telcos bundle gaming passes with data plans to monetize incremental traffic.

Regulatory clarity from the Central Bank and Securities and Exchange Commission sustains BFSI spending on risk analytics and digital channels. Healthcare and Life Sciences deploy telemedicine stacks to reach underserved communities, riding on improved broadband. Energy and Utilities digitize endpoints via smart meters, while oil and gas firms automate pipeline surveillance using drone data feeds. Across verticals, immersive customer experience is the new battleground, stitching together AI chatbots, rich media, and seamless payment flows.

By Deployment Model: Hybrid Strategies Gain Ground

On-premises still commanded 42.30% of 2025 expenditures, reflecting statutory data-sovereignty requirements and low-latency workloads. Yet cloud-only configurations are advancing at 20.35% CAGR as connectivity improves and FX risk makes capex less attractive. Hybrid architectures satisfy regulatory conditions by housing sensitive datasets in local facilities while bursting non-critical workloads to public cloud.

The Nigeria ICT market rewards providers that offer seamless orchestration, unified billing in naira, and automated compliance reporting. Data-center operators supplement colocation with bare-metal cloud nodes, letting enterprises migrate incrementally. Sub-sea cable capacity and 10,000 kilometers of new domestic fiber are cutting latency to major cloud regions, supporting latency-sensitive SaaS such as unified communications and fintech micro-services.

Geography Analysis

Lagos remains the epicenter of the Nigeria ICT market, absorbing the majority of data-center capex and hosting 30% of national GDP activity. The state’s new Electricity Law compels generators to earmark 2% of operating expenditure for community investment, indirectly supporting ICT infrastructure. MainOne’s 2Africa cable landing in Qua Iboe anchors the South-South region as an alternate digital corridor, enhancing redundancy and peering choices.

Abuja leverages its role as the administrative capital to lead in cloud-first procurement and identity-management pilots. Federal data centers increasingly collocate with commercial providers to benefit from shared backup power and cooling economies of scale. Northern markets such as Kano and Kaduna show nascent momentum around e-agriculture platforms and rail digitalization, though coverage gaps persist.

Urban-rural disparities remain stark: urban broadband penetration approaches 50%, versus 15% in rural districts. Satellite internet has emerged as a credible backfill, with Starlink now Nigeria’s second-largest ISP. The National Broadband Plan targets 70% national penetration by 2025, and cross-border fiber builds position Nigeria to resell capacity to land-locked neighbors - extending the Nigeria ICT market’s regional influence.

Competitive Landscape

Nigeria’s ICT arena displays moderate concentration, with top telcos and hyperscalers sharing infrastructure dominance yet ceding niche spaces to agile domestic providers. MTN logged USD 651 million revenue in Q1 2025 and leads in 5G roll-out, while Airtel sustains competitive parity via fresh spectrum wins. Hyperscalers Microsoft and Google compete on sovereign-cloud credentials, signing multi-year enterprise transformation deals.

Domestic cloud vendors such as Galaxy Backbone exploit naira billing and local support to secure public-sector workloads. Data-center incumbents Equinix and MainOne extend their footprints to Tier-2 cities to capture edge-compute demand. Infrastructure sharing through IHS Towers tempers capex requirements, lowering barriers for MVNO entrants and private-network roll-outs.

A scarcity of certified cybersecurity professionals - only 5,000 nationwide - creates an opening for MSSP consolidation. Providers bundle AI-driven threat detection with compliance dashboards, offering subscription models attractive to both SMEs and heavily regulated sectors. Currency volatility and power risk incentivize total-cost-of-ownership-focused buying decisions, rewarding vendors able to guarantee uptime and hedge exchange exposure.

Nigeria ICT Industry Leaders

Microsoft Corporation

Oracle Corporation

Google

Cognizant

HCL Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: MTN Nigeria launched the USD 150 million Dabengwa Data Centre in Lagos, its largest single infrastructure investment.

- June 2025: First Ally Capital acquired 60% of Migo, an AI-driven credit platform, after regulatory clearance.

- May 2025: President Tinubu approved Nigeria Startup House in San Francisco to boost global visibility.

- April 2025: Equinix commissioned its LG2.3 data-center expansion in Lagos.

Nigeria ICT Market Report Scope

The ICT market includes manufacturing and service enterprises. Its products mainly focus on information processing and electronic communication, covering transmission and display. This market is crucial for spearheading technological progress, elevating productivity, and improving overall output.

The Nigerian ICT market is segmented by type (hardware, software, IT services, and telecommunication services), size of the enterprise (small and medium enterprises and large enterprises), and industry vertical (BFSI, IT, and telecom, government, retail and e-commerce, manufacturing, energy and utilities, and other industry verticals). The market sizes and forecasts are provided in value terms (USD) for all the above segments.

By Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| Communication Services |

By Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By Industry Vertical

| Government and Public Administration |

| Banking, Financial Services and Insurance (BFSI) |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas (Up-, Mid-, Down-stream) |

| Gaming and Esports |

| Other Verticals |

By Deployment Model

| On-premises |

| Cloud-only |

| Hybrid |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas (Up-, Mid-, Down-stream) | ||

| Gaming and Esports | ||

| Other Verticals | ||

| By Deployment Model | On-premises | |

| Cloud-only | ||

| Hybrid | ||

Key Questions Answered in the Report

What is the forecast size of the Nigeria ICT market by 2031?

The market is projected to reach USD 88.96 billion by 2031 at an 18.07% CAGR.

Which ICT segment will grow fastest in Nigeria through 2031?

Cloud Services is expected to post a 19.78% CAGR, outpacing all other categories.

How much of the market do large enterprises control?

Large enterprises held 58.10% of Nigeria ICT market share in 2025.

Why are SMEs accelerating ICT spending?

Affordable cloud subscriptions and fintech payment rails lower entry barriers, driving a 15.90% CAGR for SME spending.

Which vertical shows the highest growth momentum?

Gaming & Esports is advancing at a 21.45% CAGR, buoyed by mobile penetration and youth demographics.

Page last updated on: