Kazakhstan ICT Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

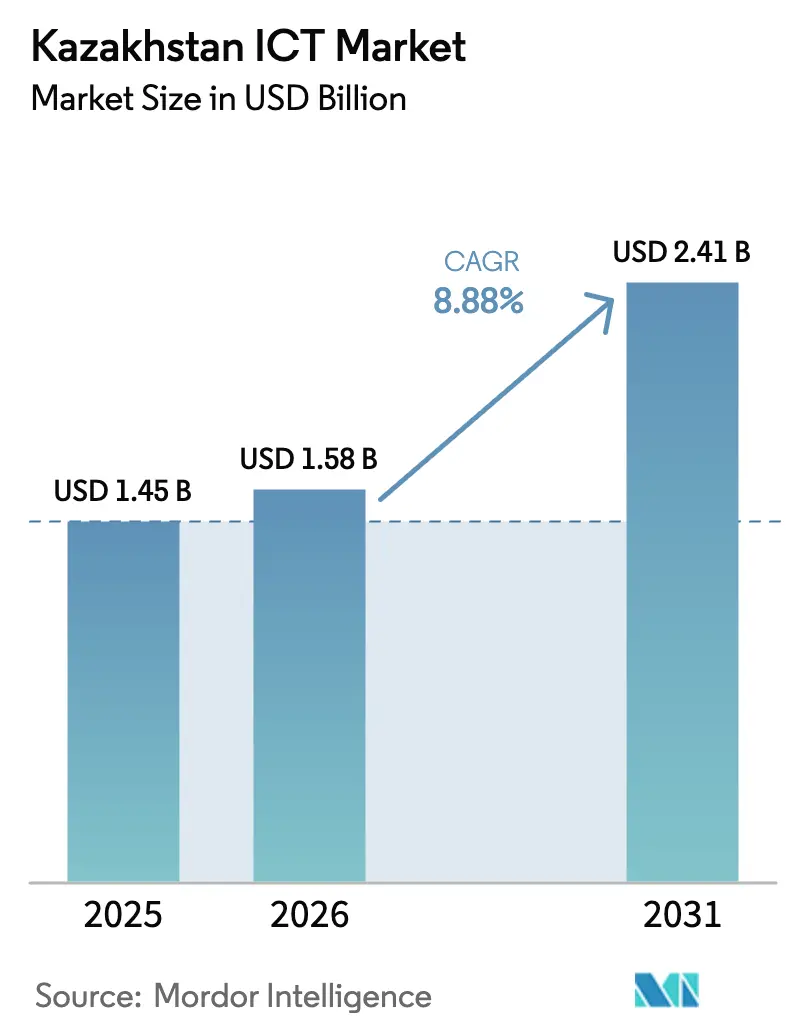

| Base Year Market Size (2025) | USD 1.45 Billion |

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 8.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kazakhstan ICT Market Analysis by Mordor Intelligence

The Kazakhstan ICT market size was valued at USD 1.45 billion in 2025 and estimated to grow from USD 1.58 billion in 2026 to reach USD 2.41 billion by 2031, at a CAGR of 8.88% during the forecast period (2026-2031). Government funding through the Digital Kazakhstan program, the nationwide 5G rollout, and rapid cloud migration are combining to keep spending on an upward trajectory. The market is also benefiting from regional investments such as the World Bank-backed DARE Project, which is broadening broadband access to more than 1 million residents.[1]World Bank, “World Bank to Help Expand Digital Infrastructure for Underserved Areas in Kazakhstan,” worldbank.org Momentum continues to swing toward cloud-led services, supported by new data-center capacity in Almaty and Astana and the entry of providers like Yandex Cloud. Large enterprise demand remains pivotal, while SME adoption is accelerating on the back of targeted tax incentives and technopark programs. Competitive intensity is moderate, with Kazakhtelecom holding dominant telecom positions and global vendors partnering with local integrators to address enterprise and public-sector opportunities.

Key Report Takeaways

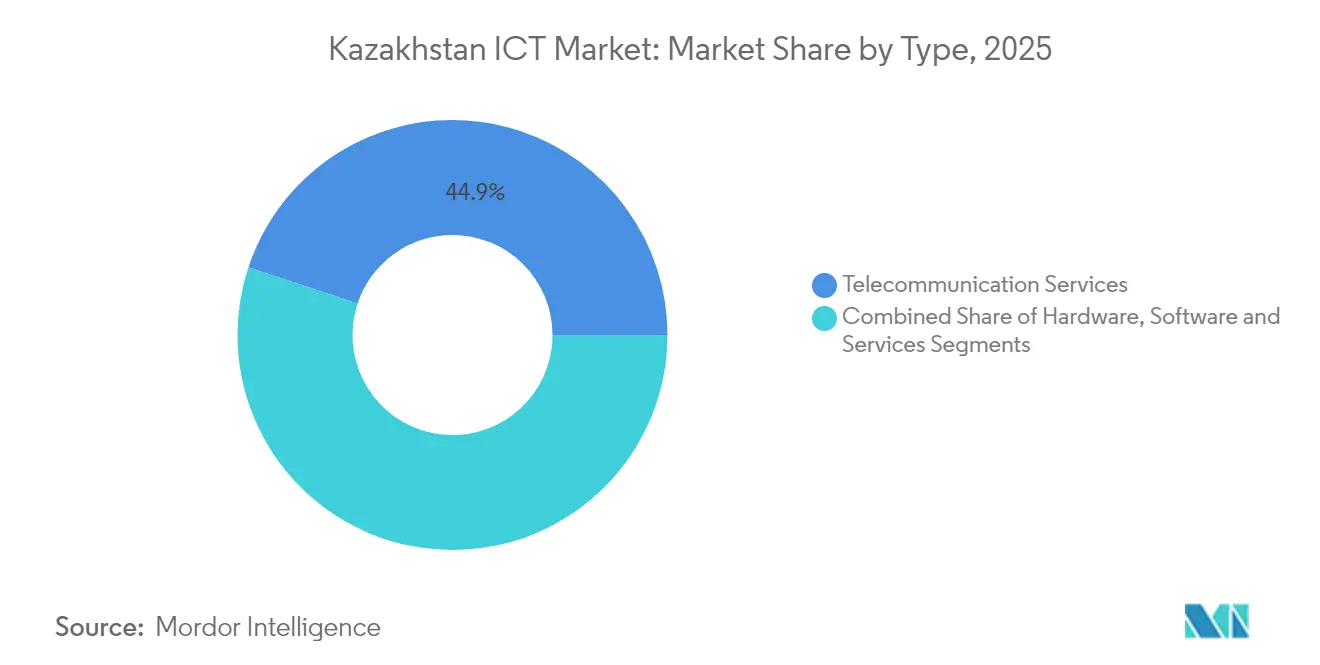

- By type, telecommunications services led with 44.90% revenue in 2025; cloud-led services are projected to expand at a 9.32% CAGR to 2031.

- By deployment model, on-premise implementations commanded 71.20% of the Kazakhstan ICT market size in 2025, while cloud deployments are forecast to climb at an 10.86% CAGR through 2031.

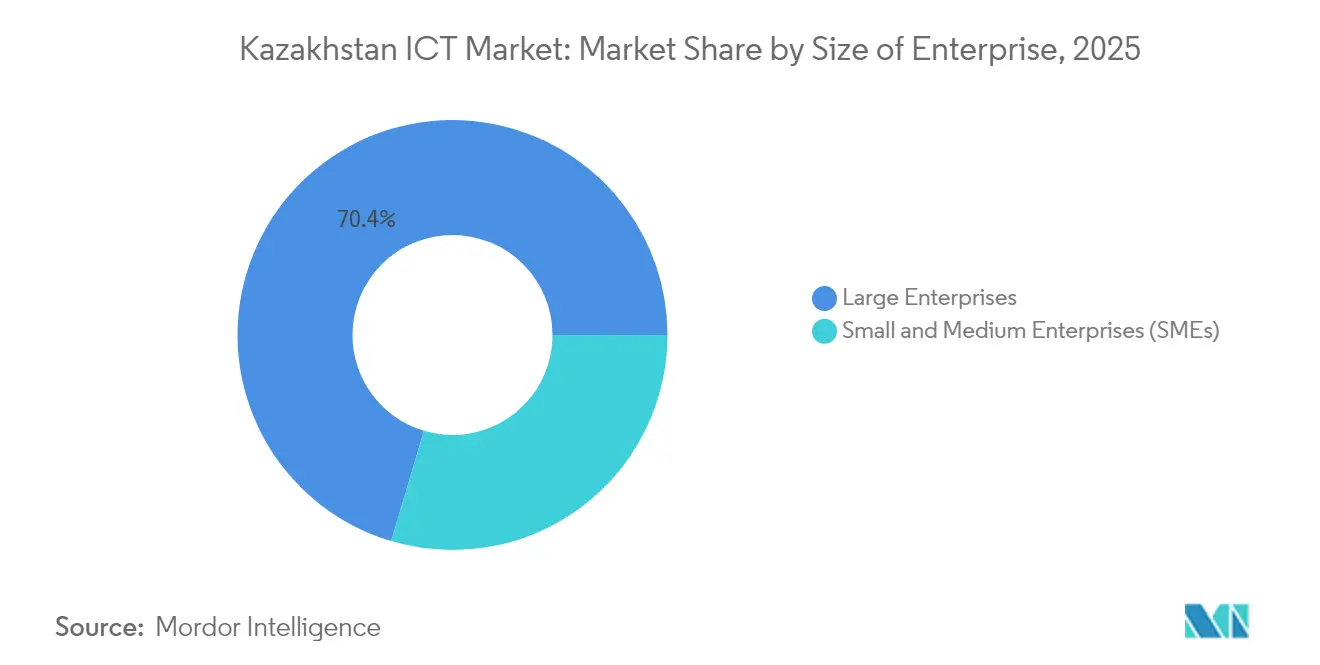

- By enterprise size, large enterprises captured 70.40% of the Kazakhstan ICT market share in 2025; SME spending is advancing at a 9.66% CAGR between 2026-2031.

- By industry vertical, BFSI held 18.60% of the Kazakhstan ICT market size in 2025, and healthcare is set to record the fastest growth at 10.08% CAGR to 2031.

- By region, Almaty City and Region held 38.50 of the Kazakhstan ICT market size in 2025, and South Kazakhstan, including Shymkent and Turkestan, is forecast to expand at a 10.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kazakhstan ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Led "Digital Kazakhstan" Program Accelerating Public-Sector IT Spend | +3.2% | National, with concentration in Astana & Almaty | Medium term (2-4 years) |

| Roll-Out of 5G and National Fiber Backbone Creating New ICT Demand | +2.1% | Urban centers initially, expanding to regional hubs | Medium term (2-4 years) |

| Surge in Cloud Migration Among Large Enterprises | +1.8% | Almaty, Astana, and major industrial centers | Short term (≤ 2 years) |

| Rapid Growth of Domestic Data-Centre Capacity and Colocation Services | +1.5% | Almaty, Astana, Karaganda | Medium term (2-4 years) |

| Rising Cyber-Security Compliance Requirements in Critical Infrastructure | +0.6% | National, with emphasis on energy and financial sectors | Short term (≤ 2 years) |

| Cross-Border E-Commerce Expansion Driving Omnichannel Retail Tech Adoption | +0.4% | Urban centers, particularly Almaty and Astana | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-Led Digital Kazakhstan Program Accelerating Public-Sector IT Spend

Public-sector digital spending is rising as 80% of government services are now delivered online, creating more than 120,000 technology jobs and positioning Kazakhstan as a regional e-government leader. High adoption of the eGov portal among 90% of the economically active population highlights user acceptance. The program’s integrated roadmap spans digital governance, sector digitization, and an innovation ecosystem that draws in UN collaboration for a new solutions center in Almaty. Hardware refreshes, software upgrades, and service outsourcing are therefore locked in across ministries and municipalities, anchoring demand through at least 2029.

Roll-Out of 5G and National Fiber Backbone Creating New ICT Demand

Government commitments exceeding 450 billion tenge (USD 900 million) will finalize a nationwide 5G network by end-2025.[2]Prime Minister of Kazakhstan, “5G Mobile Communication Rollout,” primeminister.kzParallel fiber projects target 3,010 villages, enabling 2.4 million new internet users. With traffic volumes up 61.5% since 2020, hardware vendors, tower operators, and managed service providers are securing contract pipelines for backhaul, small-cell, and edge-compute projects. These buildouts lift telecom revenues and create follow-on demand for enterprise connectivity and IoT applications in smart cities and logistics.

Surge in Cloud Migration Among Large Enterprises

Cloud services revenue climbed 69% in 2023, reflecting enterprise appetite for scalability and resilience. Local specialist QazCloud reported surging sign-ups for backup and DR offerings, while partnerships such as Kazakhtelecom-Smart Cities accelerate edge and municipal workloads. Yandex Cloud’s 2024 data-center entry and forthcoming Microsoft Azure stack integrations are intensifying competition and lowering entry barriers, especially for AI-enabled analytics and DevOps toolchains.

Rapid Growth of Domestic Data-Centre Capacity and Colocation Services

Investment in hyperscale facilities, such as the USD 1.4 billion project by GK Hyperscale Ltd in Astana, signals confidence in Kazakhstan’s role as a Central Asian compute hub. Co-location occupancy is rising as regional enterprises opt to host workloads locally to meet data-sovereignty rules and latency thresholds. Utility providers and municipal authorities are building renewable-energy tie-ins to manage power needs and improve sustainability scores.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Capital Expenditure for Digital Transformation Projects | -0.7% | National, particularly affecting SMEs | Medium term (2-4 years) |

| Limited Availability of Advanced IT Talent Within Kazakhstan | -0.5% | National, with acute shortages outside major cities | Long term (≥ 4 years) |

| Legacy Telecom Infrastructure Outside Major Cities Slowing Service Quality | -0.3% | Rural and remote regions | Medium term (2-4 years) |

| Currency Volatility Increasing Cost of Imported Hardware & Software Licences | -0.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capital Expenditure for Digital Transformation Projects

SMEs account for 99.44% of registered firms yet often stagger modernization plans because hardware, software, and consulting outlays strain budgets.[3]Cranfield University, “Digital Maturity and Readiness Model for Kazakhstan SMEs,” cranfield.ac.ukWhile grants and tax breaks through AstanaHub soften costs, typical payback windows still exceed acceptable thresholds in low-margin sectors. As a result, multi-phase deployments dominate, slowing aggregate digital maturity.

Limited Availability of Advanced IT Talent Within Kazakhstan

Despite government pledges to train 100,000 specialists by 2025, demand continues to outstrip supply, pushing average IT salaries up 54% to 673,000 tenge (USD 1,350). Shortfalls are acute in AI, cybersecurity, and cloud architecture, forcing enterprises to outsource or import talent under the Digital Nomad Visa scheme. Regional projects outside Almaty and Astana face delays and cost overruns because of limited local skill pools.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Telecommunications Services Dominate While Cloud-Led Services Accelerate

Telecommunications services generated 44.90% of 2025 revenue in the Kazakhstan ICT market. Mobile accounted for 57.80% of telecom receipts as operators monetized surging data traffic, while fixed broadband benefited from rural connectivity programs, lifting the Kazakhstan ICT market. Hardware demand remained healthy for end-user devices and network equipment, supported by hybrid-work policies across multinationals. Cloud-led services outpaced all categories, advancing at 9.32% CAGR on the strength of SaaS-based productivity suites and IaaS workloads migrating to local data centers.

Service providers are adopting bundled convergence strategies that package fiber, 5G, and managed security to capture wallet share. Device vendors are cooperating with operators through handset-finance plans that equip rural users with 4G smartphones. Data-center owners attract multinational clients by touting proximity to Eurasian trade corridors and emerging renewable-energy footprints to meet ESG mandates.

By Deployment Model: Cloud Adoption Accelerates Despite On-Premise Dominance

On-premise solutions still represent 71.20% of deployments in the Kazakhstan ICT market, reflecting sovereign-data rules in government and BFSI environments. However, cloud models are accelerating and are forecast to record an 10.86% CAGR to 2031 as regulators refine localization guidelines and classify data sensitivity. Hybrid architectures are the preferred transition path in banking, which retains core ledgers on-premise while moving customer-facing applications to the cloud. This balanced stance reduces capex and improves time-to-market for new services, broadening the Kazakhstan ICT market share for multi-cloud orchestration platforms.

Regulatory clarity continues to shape vendor roadmaps. The Ministry of Digital Development is drafting service-level standards and incident reporting rules that align with ISO 27001 and regional GDPR equivalents. System integrators are responding by creating reference architectures that combine domestic co-location, regional hyperscale zones, and sovereign backup nodes.

By Size of Enterprise: Large Enterprises Drive Spending While SMEs Show Faster Adoption

Large enterprises generated 70.40% of total outlays in the Kazakhstan ICT market in 2025, leveraging scale to deploy AI-driven analytics and private-cloud stacks. Spending priorities center on risk-weighted returns, with C-suite executives earmarking 12% of revenue for IT modernization in banking, energy, and telecom verticals. Conversely, SMEs are the fastest-growing cohort at 9.66% CAGR thanks to SaaS subscription models, micro-loans, and vendor-led training programs that compress deployment cycles and reduce upfront obligations.

The government is expanding the Tech Orda scholarship scheme and rolling out tax incentives for software exports, fostering a pipeline of cloud-native startups that target e-commerce, agritech, and healthtech opportunities. Vendor ecosystems now include SME-tailored bundles that combine accounting SaaS, cybersecurity packages, and ERP lite modules to accelerate digital entry and move the Kazakhstan ICT market size needle among smaller firms.

By Industry Vertical: BFSI Leads While Healthcare Shows Strongest Growth Potential

The BFSI sector captured 18.60% of 2025 spending as banks embraced fully digital channels, driving mobile-banking usage near universal levels and lifting transaction digitization to 89%. Regulatory directives such as the 5-year digital financial strategy emphasize open APIs, e-KYC, and digital wallets, further expanding the Kazakhstan ICT market share of fintech platforms. In contrast, healthcare is posting the fastest 10.08% CAGR, powered by a joint digital-health transformation program that funds electronic medical records, telemedicine hubs, and analytics engines.

Public administration continues to invest in citizen portals, biometric ID systems, and smart-city pilots. Utilities and manufacturing are deploying IoT sensors and predictive-maintenance systems to trim downtime. Education institutions are experimenting with cloud-hosted learning-management systems and satellite broadband to bridge rural learning gaps.

Geography Analysis

Almaty City generated 38.50% of Kazakhstan ICT market revenue in 2025, cementing its role as the national tech nucleus with a dense cluster of developers, accelerators, and data-center campuses. The municipal government allocates a budget to smart-mobility and public Wi-Fi projects, attracting domestic and foreign capital. As a result, venture funding rounds often stipulate physical presence in Almaty to tap talent pools and co-working infrastructure.

Astana and the broader Akmola Region form the second-largest node, supported by policymakers' emphasis on e-government, transport corridors, and energy-efficient public housing. The city’s “Green City” initiative embeds IoT sensors in transport and waste-management systems, generating real-time data flows that feed analytics dashboards across city agencies. With the construction of Central Asia’s largest data center, Astana is solidifying its role as a mission-critical hosting destination, further reinforcing the Kazakhstan ICT market size leadership among metropolitan areas.

South Kazakhstan, including Shymkent and Turkestan, is the fastest-growing region at 10.34% CAGR, propelled by broadband expansions financed through the World Bank DARE Project. Improved last-mile connectivity is unlocking e-commerce, tele-health, and e-learning demand. Local universities are spinning out tech incubators to retain graduates and spur software-export clusters.

Competitive Landscape

Kazakhtelecom controls 61.8% of fixed, mobile, and internet revenues, wielding scale economies in network buildout, shared services, and bundled pricing. The operator is leveraging its national fiber backbone for wholesale leasing and positioning its mobile subsidiary Kcell to capture 5G enterprise slices. International vendors such as Microsoft, Huawei, and Cisco embed their hardware and software within enterprise transformation projects. Huawei holds infrastructure contracts for 5G RAN equipment as well as smart-city camera grids, while Microsoft drives enterprise adoption of productivity and security SaaS suites through regional partners.

The cloud arena is heating up. QazCloud opened a new data center in Akmola to serve regulated workloads and state-owned enterprises. Yandex Cloud activated an Almaty facility in 2024, offering localized AI toolchains and pay-as-you-go compute options. These moves intensify price and feature competition, compelling system integrators to bundle managed migration, DevSecOps, and compliance consulting services.

Cybersecurity pure-plays such as G5 Cyber Security and the Center of Information Security are scaling managed detection and response (MDR) contracts in response to rising attack volumes. Vendor consolidation is underway as larger providers acquire niche players to integrate XDR, threat intel, and compliance dashboards, likely reducing fragmentation in the medium term.

Kazakhstan ICT Industry Leaders

Microsoft Corporation

Andersen Inc.

LeverX International Company LLC.

JSC Kazteleport

G5 Cyber Security

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: A digital solutions center opened in Almaty in partnership with the UN to incubate regional innovation and export-ready platforms.

- March 2025: The Ministry of Science and Higher Education rolled out the AI-Sana startup acceleration program to align academic R&D with market demand

- February 2025: The World Bank approved USD 92.43 million for the DARE Project to extend broadband to underserved regions.

- January 2025: Kazakhstan introduced a new supercomputer, the most powerful in Central Asia, to propel AI and scientific research initiatives.

Kazakhstan ICT Market Report Scope

Information and Communication Technology (ICT) encompasses a wide array of communication technologies. This includes wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and various media applications. Collectively, these tools empower users to store, access, transmit, retrieve, and manipulate digital information. The study of the market tracks the revenue by hardware and service & solution offerings through vendors.

Kazakhstan ICT market is segmented by type (hardware, software, services, and telecommunication services), size of enterprise (small and medium enterprises, and large enterprises), and industry vertical (BFSI, IT and telecom, government, retail and e-commerce, manufacturing, energy and utilities, and other industry verticals). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware | End-User Devices (PCs, Smartphones, Tablets) |

| Data-Centre Infrastructure (Servers, Storage, Networking) | |

| Network Equipment (Core, Access, Transmission) | |

| Software | Enterprise Applications (ERP, CRM, SCM) |

| Infrastructure Software (OS, Virtualisation, Database) | |

| Security Software | |

| Productivity and Collaboration Software (Office Suites, UCandC) | |

| Services | IT Services (Consulting, Integration, Support) |

| Managed Services | |

| Business-Process Outsourcing | |

| Telecommunication Services | Mobile Services |

| Fixed Broadband | |

| Fixed Voice | |

| Wholesale and Carrier Services |

| On-Premise |

| Cloud |

| Hybrid |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Public Administration |

| IT and Telecom |

| Retail and E-Commerce |

| Manufacturing |

| Energy and Utilities |

| Healthcare and Life Sciences |

| Other Verticals |

| Almaty City and Region |

| Astana and Akmola Region |

| West Kazakhstan (Atyrau, Aktobe, Mangystau) |

| South Kazakhstan (Shymkent, Turkestan) |

| East and North Kazakhstan |

| By Type | Hardware | End-User Devices (PCs, Smartphones, Tablets) |

| Data-Centre Infrastructure (Servers, Storage, Networking) | ||

| Network Equipment (Core, Access, Transmission) | ||

| Software | Enterprise Applications (ERP, CRM, SCM) | |

| Infrastructure Software (OS, Virtualisation, Database) | ||

| Security Software | ||

| Productivity and Collaboration Software (Office Suites, UCandC) | ||

| Services | IT Services (Consulting, Integration, Support) | |

| Managed Services | ||

| Business-Process Outsourcing | ||

| Telecommunication Services | Mobile Services | |

| Fixed Broadband | ||

| Fixed Voice | ||

| Wholesale and Carrier Services | ||

| By Deployment Model | On-Premise | |

| Cloud | ||

| Hybrid | ||

| By Size of Enterprise | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Industry Vertical | Banking, Financial Services and Insurance (BFSI) | |

| Government and Public Administration | ||

| IT and Telecom | ||

| Retail and E-Commerce | ||

| Manufacturing | ||

| Energy and Utilities | ||

| Healthcare and Life Sciences | ||

| Other Verticals | ||

| By Region | Almaty City and Region | |

| Astana and Akmola Region | ||

| West Kazakhstan (Atyrau, Aktobe, Mangystau) | ||

| South Kazakhstan (Shymkent, Turkestan) | ||

| East and North Kazakhstan | ||

Key Questions Answered in the Report

What is the current size of the Kazakhstan ICT market?

The market stands at USD 1.58 billion in 2026 and is projected to reach USD 2.41 billion by 2031.

Which segment generates the largest revenue?

Telecommunications services lead with 44.90% of 2025 revenue.

How fast is cloud adoption growing?

Cloud-led services are advancing at a 9.32% CAGR, driven by data-center expansion and regulatory support.

Which industry vertical spends the most on ICT?

The BFSI sector accounts for 18.60% of 2025 spending due to digital-banking initiatives.

What regions are growing the fastest?

South Kazakhstan, including Shymkent and Turkestan, is forecast to expand at a 10.34% CAGR through 2031.

Who dominates the Kazakhstan ICT market?

Kazakhtelecom maintains 61.80% of telecom revenue, while QazCloud and Yandex Cloud lead the domestic cloud arena.

Page last updated on: