Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

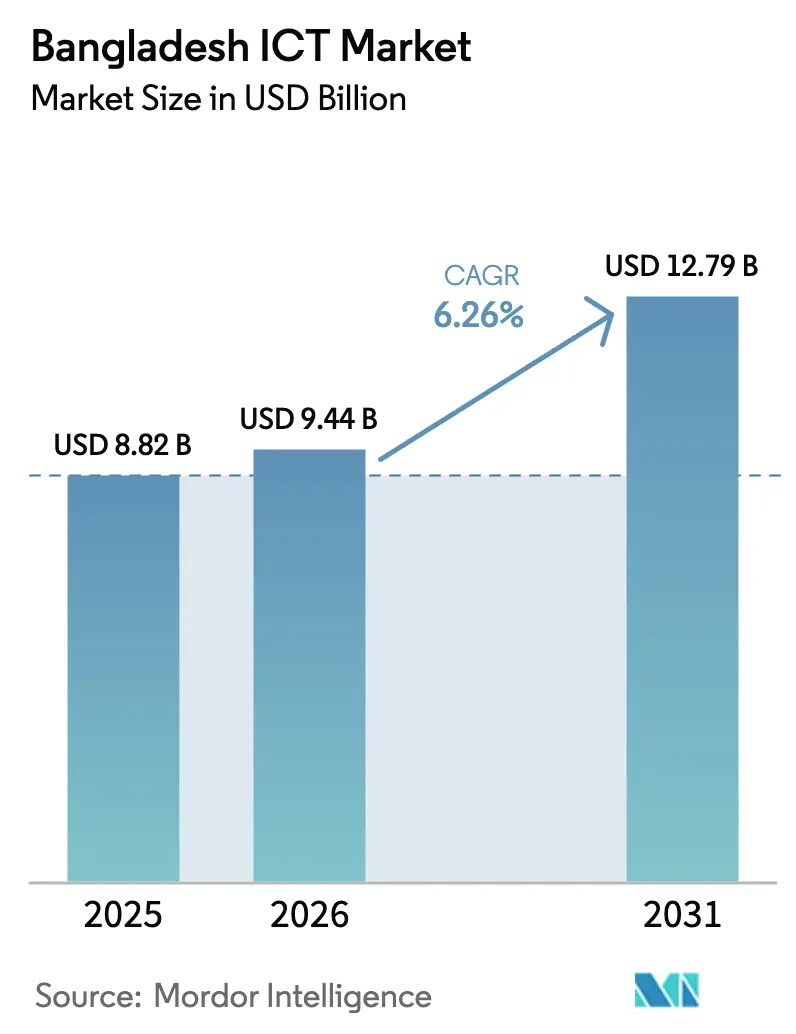

| Base Year Market Size (2025) | USD 8.82 Billion |

| Market Size (2026) | USD 9.44 Billion |

| Market Size (2031) | USD 12.79 Billion |

| Growth Rate (2026 - 2031) | 6.26% CAGR |

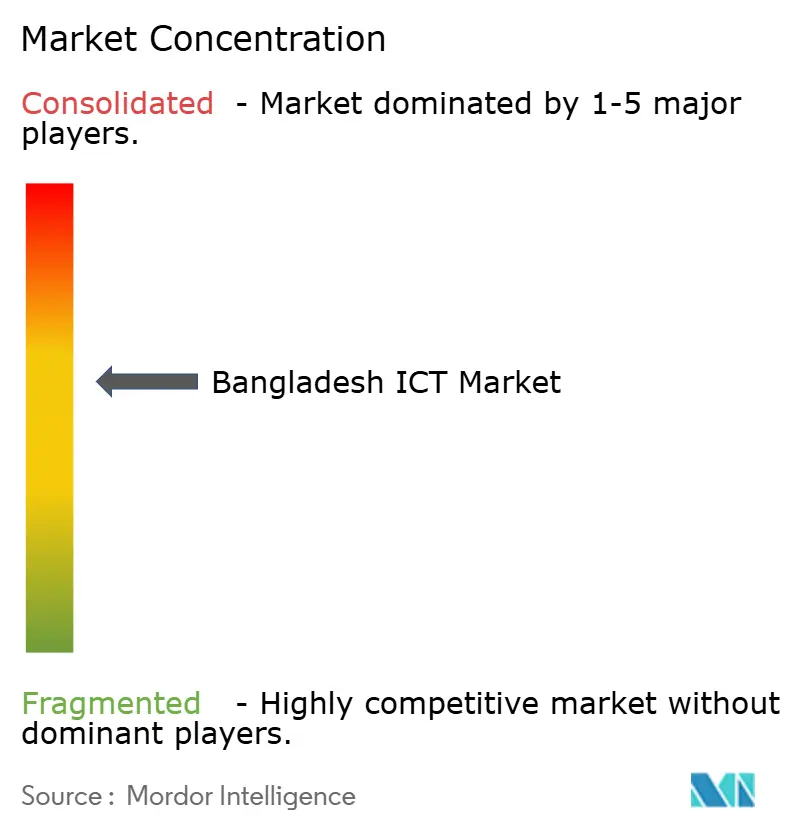

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bangladesh ICT Market Analysis by Mordor Intelligence

The Bangladesh ICT Market size is projected to be USD 8.82 billion in 2025, USD 9.44 billion in 2026, and reach USD 12.79 billion by 2031, growing at a CAGR of 6.26% from 2026 to 2031. A pivotal transition from discrete hardware purchases toward subscription-based cloud, cybersecurity, and managed services is underway as enterprises align with the Smart Bangladesh 2041 digital vision. Cloud adoption is gaining critical mass because local data-center capacity, SaaS billing in local currency, and hybrid deployment models now meet the data-sovereignty rules of the Digital Security Act 2018. At the same time, spectrum availability and foreign-ownership liberalization are reshaping investment flows, enabling mobile carriers and hyperscale cloud platforms to accelerate 5G and edge rollouts even while elevated spectrum fees consume 16% of operator revenue, far above the 10% Asia-Pacific median. Hardware sales remain hampered by 25% import tariffs, yet production clustering inside the Sheikh Hasina Hi-Tech Parks is slowly tempering the cost base and supporting the emergence of a local manufacturing hub. Cybersecurity talent shortages, rural backhaul gaps, and execution delays in government e-service projects continue to weigh on the Bangladesh ICT market, but sustained policy focus and private-public partnerships are expected to keep investment momentum intact through the forecast window.

Key Report Takeaways

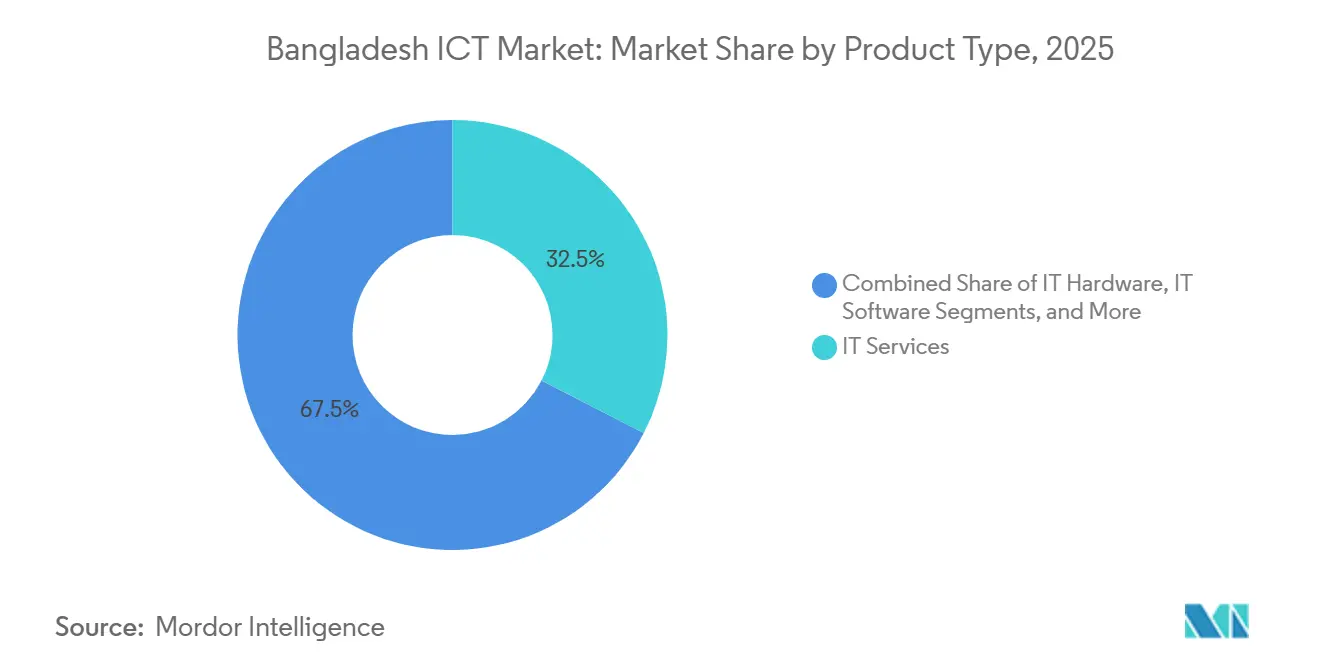

- By product type, IT services led with 32.54% revenue share in 2025, while cloud and platform services are projected to expand at a 6.82% CAGR through 2031.

- By enterprise size, large enterprises accounted for 57.32% of the Bangladesh ICT market share in 2025, whereas small and medium-sized enterprises are forecast to log the fastest growth at 7.18% CAGR between 2026-2031.

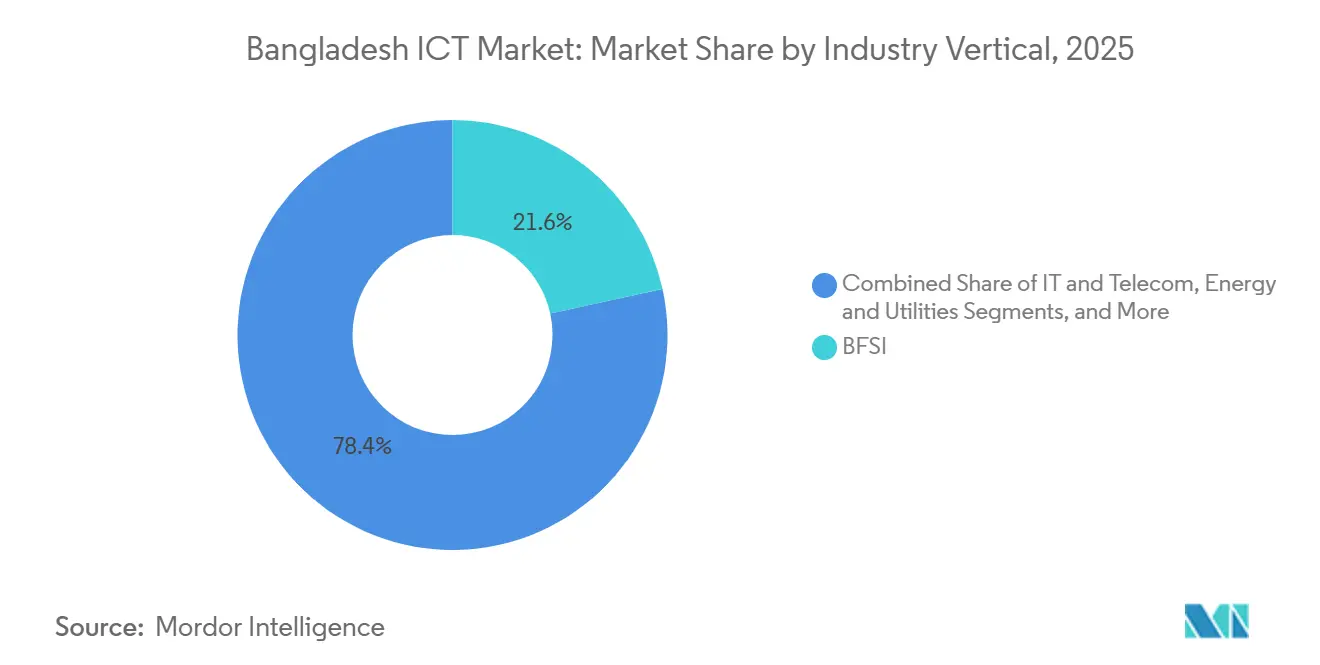

- By industry vertical, banking, financial services, and insurance held 21.56% of spending in 2025, and healthcare and life sciences are expected to expand at an 8.13% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government's Digital Bangladesh Vision 2041 Investments | +1.8% | National, with concentration in Dhaka, Chittagong, and divisional headquarters | Long term (≥ 4 years) |

| Rapid Growth of Mobile Internet Subscribers | +1.2% | National, urban saturation driving rural expansion focus | Medium term (2-4 years) |

| Rising Demand for Cloud and Platform Services Among SMEs | +1.5% | National, early adoption in Dhaka, Chittagong, Sylhet industrial zones | Medium term (2-4 years) |

| Expansion of 4G and Upcoming 5G Network Rollout | +1.0% | Urban centers (Dhaka, Chittagong), gradual tier-2 city coverage | Medium term (2-4 years) |

| Emergence of Sheikh Hasina Hi-Tech Parks as Domestic Tech Manufacturing Hubs | +0.6% | Kaliakoir, Jashore, Mohakhali, Rajshahi, Sylhet | Long term (≥ 4 years) |

| Increasing Adoption of Islamic FinTech Solutions Within BFSI Sector | +0.9% | National, concentrated in urban and semi-urban banking corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government's Digital Bangladesh Vision 2041 Investments

BDT 500 billion (USD 4.5 billion) has been earmarked through the Eighth Five-Year Plan to digitize public services, roll out 10,000 rural digital centers, and establish 64 district-level innovation hubs. Contracts already awarded for e-government resource planning suites, biometric citizen databases, and cloud-hosted tax platforms have solidified a multiyear pipeline for local system integrators.[1]Ministry of Finance, “Budget Documents 2025-2026,” MOF.GOV.BD Public-private interfaces, exemplified by social assistance disbursement via bKash and Nagad mobile wallets, showcase how policy can catalyze demand for secure APIs, managed hosting, and identity-as-a-service. Yet execution risk persists because line-ministry technical capacity gaps have historically elongated project timelines by up to two years, keeping revenue recognition lumpy for vendors tied to government cycles.

Rising Demand for Cloud and Platform Services Among SMEs

SME cloud spending is scaling at 7.18% CAGR as entrepreneurs migrate from manual ledgers to mobile-first SaaS applications in Bangla. The Bangladesh Bank’s December 2025 mandate that every registered business accept digital payments compelled 200,000 shops to onboard point-of-sale, inventory, and analytics modules, rapidly enlarging the addressable pool for localized SaaS providers. Microsoft Azure and Amazon Web Services now co-sell via DataSoft Systems and Aamra Companies to satisfy data-residency clauses, reducing migration anxiety for exporters and garment units. Intermittent power supply and cyber-risk awareness remain barriers, but device-financing by micro-lenders and the proliferation of regional language user interfaces are steadily dissolving adoption hurdles across the Bangladesh ICT market.

Rapid Growth of Mobile Internet Subscribers

Subscriber losses from 135.99 million in July 2025 to 131.49 million by October 2025 marked the first pullback in half a decade. Affordability constraints in low-income segments and a shortage of compelling 5G use cases turned the strategic spotlight toward rural expansion, average-revenue-per-user uplift, and platform monetization. To mitigate churn, carriers introduced subsidized smartphone bundles and micro-recharge packs, pivoting network focus from capacity expansion to service quality. Government subsidy of BDT 12 billion (USD 108 million) for rural towers is material, but bureaucratic bottlenecks left one-third of the funds undisbursed in 2025, delaying backhaul upgrades that are crucial for cloud adoption in underserved districts.

Expansion of 4G and Upcoming 5G Network Rollout

The January 2026 700 MHz auction released only 25 MHz of spectrum, leaving limited headroom for ultra-capacity 5G deployments and edge-computing business models. The USD 21.4 million reserve price per MHz exceeds regional benchmarks by 30%, straining carrier balance sheets already absorbing 16% revenue leakage into licensing fees. Grameenphone and Robi piloted 5G in Dhaka and Chittagong, but coverage remains confined to central business districts because fiber reach to towers is still sparse and edge data-center footprints are embryonic. Vendor-financing from Ericsson and Huawei eases capital pressure, yet 25% import tariffs on RAN gear erode the return on invested capital. Monetization thus hinges on enterprise IoT pilots in garments, ports, and power grids where low-latency analytics can command premium pricing inside the Bangladesh ICT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate Rural IT Infrastructure | -1.2% | Rural unions, northern and southern peripheral districts | Long term (≥ 4 years) |

| Shortage of Advanced Cybersecurity Talent | -0.8% | National, acute in Dhaka and Chittagong enterprise hubs | Medium term (2-4 years) |

| Persistent Underinvestment in Local Data Center Redundancy | -0.6% | National, affecting tier-1 cities with enterprise concentration | Medium term (2-4 years) |

| Import Tariff Volatility on ICT Hardware Components | -0.5% | National, impacting hardware procurement and project timelines | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inadequate Rural IT Infrastructure

Fewer than 30% of rural unions had fiber backhaul by late 2025, forcing operators to rely on microwave links that deliver erratic latency incompatible with cloud workspaces and telehealth. Commercial towers in low-density areas yield average revenue per user below BDT 150 (USD 1.35) per month, deterring private capital. Land-title disputes and right-of-way approvals add an average of nine months to tower construction, perpetuating a coverage gap that curtails the addressable base for cloud and e-government applications.

Shortage of Advanced Cybersecurity Talent

A deficit of 15,000 certified cybersecurity specialists in 2025 inflates wage costs and curtails the rollout of managed security services.[2]Bangladesh Computer Council, “Cybersecurity Workforce Assessment 2025,” BCC.GOV.BD Enterprises thus operate with incomplete threat-detection stacks, and only 15% maintain 24/7 security operations centers. While the Cybersecurity Skills Development Program aims to train 5,000 professionals by 2027, curriculum lags and inadequate hands-on labs reduce its near-term impact, leaving the Bangladesh ICT industry exposed to escalating ransomware incidents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Dominance Masks Hardware Tariff Pressure

IT services accounted for 32.54% of 2025 revenues, underscoring the role of consulting, integration, and outsourcing in the backbone of the Bangladesh ICT market. Cloud and platform offerings, although smaller in absolute terms, posted the fastest growth and are projected to command a larger slice of the Bangladesh ICT market as migrations accelerate. Vendor competition is intensifying as Microsoft, AWS, and Oracle have forged alliances with domestic integrators to embed local-language interfaces and ensure data-residency compliance. Hardware demand remains strong, but import tariffs averaging 25% compress margins and lengthen project timelines, prompting resellers to bundle equipment with managed services to protect profitability.

A second growth pocket is managed security, catalyzed by a 40% increase in ransomware attempts in 2025.[3]Bangladesh Bank, "Payment Systems and Digital Financial Services Report 2025," bb.org.bd Although adoption remains concentrated among banks and telecom operators, rising compliance demands are prompting manufacturers and retailers to explore endpoint detection and managed detection and response subscriptions. The Bangladesh ICT market share for traditional communication services continues to shrink in percentage terms because subscriber growth has plateaued, shifting revenue capture toward digital platforms, IoT connectivity, and edge analytics.

By Enterprise Size: SME Digitalization Outpaces Corporate Refresh Cycles

Large enterprises still controlled 57.32% of 2025 spend, anchored by multi-year ERP upgrades, core-banking refreshes, and telecom network modernization. These buyers favor hybrid cloud architectures that balance on-premises control with public cloud agility, resulting in complex systems-integration contracts that sustain consulting billings. However, budget reallocation from capital expenditure to operating expenditure is lengthening hardware refresh cycles, tempering growth in legacy segments of the Bangladesh ICT market.

In contrast, SMEs show the highest velocity. Affordable subscription bundles, device-financing models, and regulatory nudges toward digital invoicing and payment acceptance are closing the technology gap. The SME Foundation’s BDT 3 billion (USD 27 million) grant program subsidized software licenses and connectivity, enabling micro-retailers and light-manufacturing units to deploy accounting, CRM, and e-commerce portals rapidly. As a result, SMEs are expected to contribute an increasingly larger portion of the Bangladesh ICT market size, aided by localized SaaS solutions that reduce language friction and training overhead.

By Industry Vertical: Healthcare Digitalization Accelerates Beyond BFSI Maturity

Banking, financial services, and insurance retained 21.56% of 2025 outlays, sustained by Islamic fintech growth, core-banking modernization, and heightened regulatory scrutiny on cybersecurity. With 70 million bKash customers and interoperable wallets, digital finance constitutes a primary use case propelling API gateways, fraud analytics, and cloud storage services. Yet the most dynamic segment is healthcare, projected to grow at an 8.13% CAGR as the Digital Health Strategy 2026-2032 funds electronic health records, telemedicine hubs, and diagnostic imaging networks.

Public hospitals must digitize patient files by December 2027, and the Bangladesh ICT market is responding through partnerships between hospital chains, cloud providers, and medical-device OEMs. Logistics and retail are also scaling investments in omnichannel platforms, warehouse automation, and last-mile delivery software as online shopping penetrates 15% of urban households. Energy, utilities, and manufacturing remain comparatively nascent adopters, but pilot programs for smart grids and IoT-enabled garment factory floors signal future upside once technical-skills bottlenecks ease.

Geography Analysis

Dhaka and Chittagong jointly account for more than 65% of Bangladesh's ICT market, driven by concentrated corporate headquarters, banking hubs, and telecom switching centers. High fiber density, multiple tier-III data centers, and wide 4G coverage create fertile ground for cloud migration and the uptake of managed services. Edge data center construction is emerging to serve export-oriented garment clusters on the outskirts, reducing latency for computer vision quality-control applications.

Tier-2 cities such as Khulna, Rajshahi, and Sylhet are posting double-digit year-on-year spending as enterprise branches modernize point-of-sale and ERP suites. Government e-service kiosks in district headquarters are driving incremental demand for biometric devices, VSAT connectivity, and managed hosting.

Rural unions remain investment-starved because fiber backhaul covers less than one-third of locations. Microwave links fill the gap but limit consistent throughput, constraining video consultation, distance learning, and payment acceptance. Universal Service Obligation Fund disbursements, if fully executed, could add 5,000 towers by 2028, gradually unlocking new revenue pools for the Bangladesh ICT market.

Competitive Landscape

The Bangladesh ICT market exhibits moderate fragmentation with overlapping spheres of influence. Grameenphone maintained leadership at 85.6 million subscribers in Q3 2025, but revenue growth is tilting toward value-added digital services rather than raw connectivity. Robi Axiata and Banglalink inked network-sharing deals to dilute capital intensity and accelerate rural coverage. On the hardware front, Samsung, Huawei, Cisco, and Dell compete via channel-led enterprise engagements, while IBM and Oracle focus on core-banking and analytics stacks.

Domestic systems integrators such as Aamra Companies, DataSoft Systems, Spectrum Engineering Consortium, and Dohatec New Media secure public-sector tenders by offering Bangla-language support and agile customization. Fintech disruptors bKash and Nagad are diversifying into micro-insurance and credit scoring, challenging traditional banks and nudging core-banking vendors to expose open APIs. Intellectual-property enforcement gaps, however, continue to deter foreign venture capital and depress software license value capture.

Strategic moves in 2025 included Microsoft-Azure’s partnership with DataSoft for localized cloud support, Dell’s rollout of pre-packaged edge servers for garment-factory IoT pilots, and Huawei’s vendor-financed 5G radio deployments in Dhaka. As policy now allows up to 85% foreign ownership in mobile operators, Telenor and Axiata have signaled larger capital commitments, setting the stage for intensified competition across connectivity, cloud, and fintech value chains within the Bangladesh ICT market.

Bangladesh ICT Industry Leaders

-

Grameenphone Ltd.

-

Robi Axiata Limited

-

Banglalink Digital Communications Limited

-

Samsung Electronics Company Limited

-

Huawei Technologies Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Bangladesh Telecommunication Regulatory Commission auctioned 25 MHz of 700 MHz spectrum at a base price of BDT 237 crore (USD 21.4 million) per MHz, constraining 5G capacity headroom and lifting carrier capital requirements.

- December 2025: bKash and Nagad enabled wallet-to-wallet interoperability for 90 million users, lowering friction and expanding payment use cases.

- November 2025: The Digital Health Strategy 2026-2032 received cabinet approval with a BDT 15 billion (USD 135 million) budget for electronic medical records and telemedicine rollouts.

- October 2025: Grameenphone retained market leadership at 85.6 million subscribers, offsetting urban churn via rural-focused tiered data plans.

Bangladesh ICT Market Report Scope

The Bangladesh ICT Market Report is Segmented by Product Type (IT Hardware [Computer Hardware, Networking Equipment, and Peripherals]. IT Software (IT Services [IT Consulting and Implementation, IT Outsourcing, Business Process Outsourcing, Managed Security Services, and Cloud and Platform Services] IT Infrastructure, IT Security/Cybersecurity, Communication Services), Enterprise Size (Small and Medium-sized Enterprises, and Large Enterprises), and Industry Vertical (Government and Public Administration, BFSI, IT and Telecom, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, Other Industry Verticals). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Industry Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Industry Verticals | ||

Key Questions Answered in the Report

How large is the Bangladesh ICT market in 2026?

The Bangladesh ICT market size is estimated at USD 9.44 billion in 2026, and it is projected to reach USD 12.79 billion by 2031.

What is the expected growth rate of the Bangladesh ICT market through 2031?

The market is forecast to expand at a 6.26% CAGR between 2026 and 2031, underpinned by cloud migration, fintech expansion, and government digitalization.

Which product segment is growing fastest inside Bangladesh’s technology landscape?

Cloud and platform services are the fastest-growing product category, projected to rise at 6.82% CAGR over the forecast window as SMEs adopt SaaS and hybrid-cloud architectures.

Why are SMEs important for future ICT spending in Bangladesh?

Affordable SaaS bundles, regulatory mandates for digital payments, and device-financing programs are accelerating technology adoption among SMEs, making them the fastest-expanding customer cohort.

Which vertical will outpace others in technology spending growth?

Healthcare and life sciences are set to grow at an 8.13% CAGR to 2031 because of mandated electronic medical records, telemedicine, and public funding under the Digital Health Strategy 2026-2032.

What challenges could slow ICT growth in Bangladesh?

Key obstacles include limited rural fiber backhaul, a shortage of certified cybersecurity professionals, high import tariffs on hardware, and the constrained release of affordable 5G spectrum.

Page last updated on: