Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

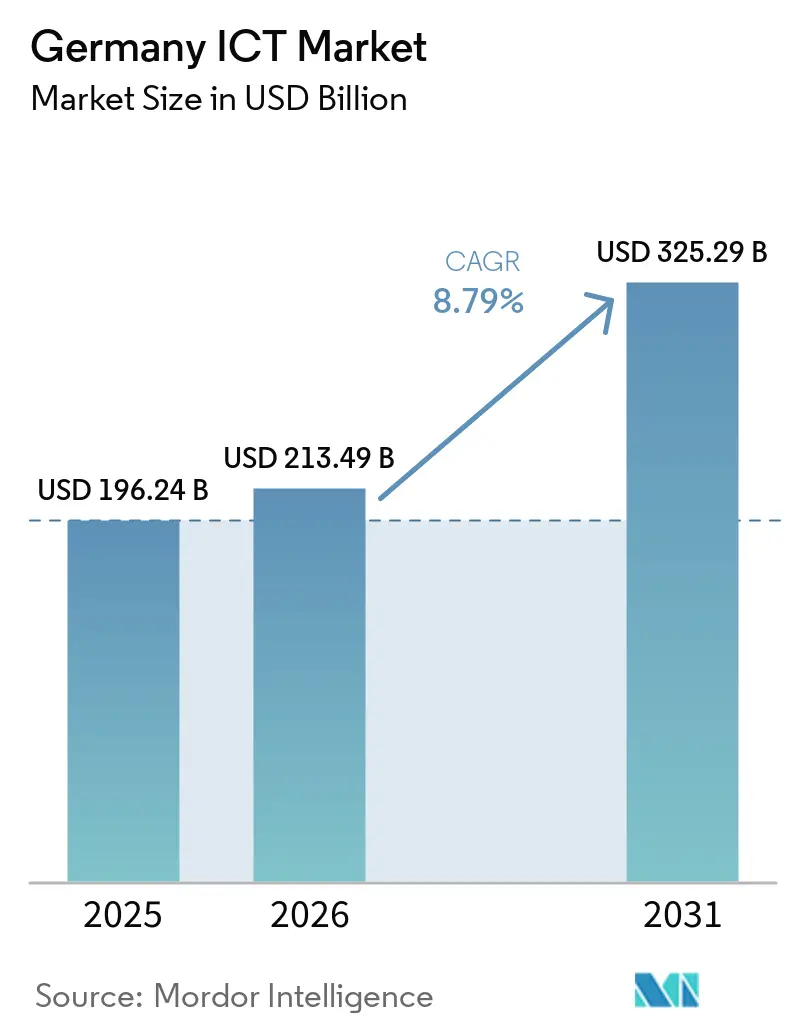

| Base Year Market Size (2025) | USD 196.24 Billion |

| Market Size (2026) | USD 213.49 Billion |

| Market Size (2031) | USD 325.29 Billion |

| Growth Rate (2026 - 2031) | 8.79% CAGR |

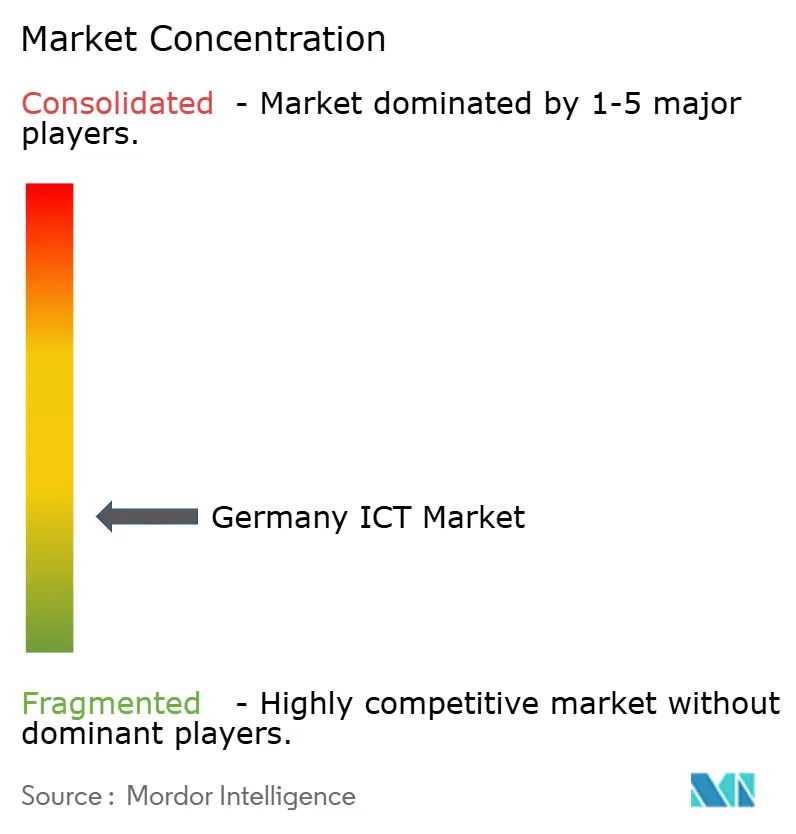

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany ICT Market Analysis by Mordor Intelligence

The Germany ICT market size was valued at USD 196.24 billion in 2025 and estimated to grow from USD 213.49 billion in 2026 to reach USD 325.29 billion by 2031, at a CAGR of 8.79% during the forecast period (2026-2031). Enterprise digitalisation, sovereign-cloud adoption and accelerated artificial-intelligence rollouts provide the structural lift behind this trajectory, while sustained CAPEX by hyperscalers such as Microsoft and OpenAI confirms Germany’s position as Europe’s third-largest AI arena. Government incentives attached to the EU Chips Act, advanced 5G networks covering more than 95% of households and a rapidly maturing Mittelstand cloud culture continue to unlock demand for software-defined infrastructure and data-driven services. Meanwhile, industrial leaders from Siemens to Deutsche Telekom demonstrate tangible productivity gains—up to 69% in selected factories—by fusing operational technology with digital twins and edge AI platforms. Despite rising energy prices and a persistent cyber-talent gap, the Germany ICT market is expected to sustain double-digit growth, with vendors that offer sovereign controls and sector-specific platforms positioned to capture outsize share. [1]Siemens AG, “World Economic Forum: Siemens factory in Erlangen named Digital Lighthouse Factory,” siemens.com

Key Report Takeaways

- By type, IT services retained the largest share of the Germany ICT market in 2025, while software is set to advance at an 8.92% CAGR through 2031.

- By deployment model, on-premises solutions led the Germany ICT market share in 2025; public-cloud workloads are projected to grow at 13.95% CAGR to 2031.

- By enterprise size, large enterprises held the dominant Germany ICT market share in 2025, whereas SMEs are forecast to expand at 9.99% CAGR over 2026-2031.

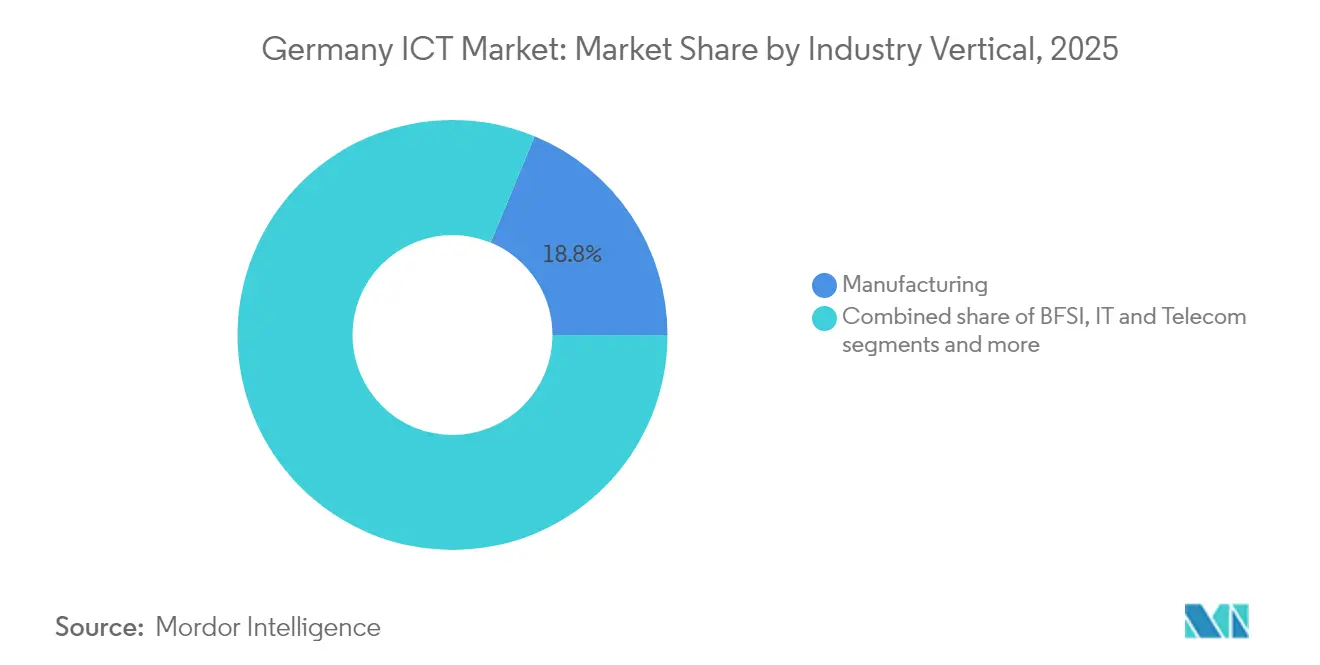

- By industry vertical, manufacturing commanded the largest Germany ICT market size in 2025, yet healthcare and life sciences are primed for the fastest 11.42% CAGR through 2031.

- Amazon Web Services, Microsoft, Google Cloud, Deutsche Telekom and SAP collectively controlled an estimated 47.35% of 2025 revenue, reflecting a moderately concentrated playing field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rise in enterprise digitalisation | 2.10% | National, concentrated in Bavaria, Baden-Württemberg, North Rhine-Westphalia | Medium term (2-4 years) |

| 5G rollout & private-network pilots | 1.80% | National, with urban centers leading deployment | Short term (≤ 2 years) |

| Cloud-native migration of Mittelstand | 1.50% | National, strongest in manufacturing regions | Medium term (2-4 years) |

| Gen-AI investment boom post-GPT | 2.30% | National, with tech hubs in Berlin, Munich, Hamburg | Short term (≤ 2 years) |

| EU Chips Act-linked semiconductor CAPEX | 1.20% | Regional, focused on Dresden, Magdeburg, Bavaria | Long term (≥ 4 years) |

| Growth of sovereign-cloud & Gaia-X nodes | 0.80% | National, with data center concentrations in Frankfurt, Berlin | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Rise in Enterprise Digitalisation

Three out of four German companies had fully articulated digital strategies by 2024, a proportion that continues to climb as regulatory regimes such as the Digital Operational Resilience Act standardise technology risk management across industries. Manufacturing leaders including Siemens report productivity uplifts of nearly 70% after embedding digital-twin workflows in their Erlangen Lighthouse Factory. Financial institutions accelerate cloud and cybersecurity spending to comply with resilience mandates, while Mittelstand firms exploit sovereign cloud offerings like Open Telekom Cloud to achieve similar compliance without prohibitive capital outlays. The resulting demand spike for secure infrastructure, managed services and AI-enabled analytics underpins a structural uplift in the Germany ICT market.

5G Rollout & Private-Network Pilots

Nationwide 5G coverage surpassed 95% of households in 2024, with Deutsche Telekom at 97%, Vodafone at 92% and O2 at 96%. Private-network pilots in automotive and logistics hubs validate low-latency use-cases such as real-time robotic control and high-definition machine vision. Vodafone’s partnership with Autobahn GmbH added 150 macro sites along the 13,200 km highway grid, enabling vehicle-to-infrastructure applications that cut traffic-management delays. Enterprise appetite for network slicing is translating into fresh service-revenue pools for telcos and systems integrators, propelling the Germany ICT market toward higher-value connectivity and IoT solutions.

Cloud-Native Migration of Mittelstand

Iconic mid-market manufacturers such as Schmitz Cargobull completed multi-module SAP migrations to Microsoft Azure, reducing on-premises hardware by close to 60% and shrinking release cycles in overseas subsidiaries. Similar patterns emerge across specialty software vendors such as Diamant Software, whose shift to Open Telekom Cloud enables multi-tenant scaling and privacy-compliant data residency. These case studies overturn historical risk perceptions and energise demand for migration tooling, integration services and hybrid architectures. SME digital maturity is now a critical competitiveness lever, further enlarging the customer base of the Germany ICT market. [2]Deutsche Telekom AG, “5G Coverage Report 2024,” telekom.com

Gen-AI Investment Boom Post-GPT

The domestic AI segment is projected to book EUR 11.7 billion (USD 13.1 billion) in 2024 revenue, buoyed by Microsoft’s EUR 3.2 billion infrastructure push and OpenAI’s new German footprint. Deutsche Telekom and NVIDIA added momentum by launching Europe’s first industrial AI cloud packing 10,000 GPUs, aimed squarely at manufacturing and research workloads. Siemens’ Industrial Copilot, winner of the 2025 Hermes Award, slashes machine code-development time and error rates in factory environments. A vibrant startup scene led by Aleph Alpha augments the ecosystem with sovereign language models optimised for European data protection needs. These forces collectively heighten AI intensity across the Germany ICT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent skills shortage in cybersecurity & AI | -1.40% | National, acute in Berlin, Munich, Hamburg tech hubs | Medium term (2-4 years) |

| High energy prices for data-center ops | -0.90% | National, concentrated in data center regions | Short term (≤ 2 years) |

| Lagging FTTP coverage vs EU peers | -0.70% | National, rural areas most affected | Long term (≥ 4 years) |

| Inflation-driven IT CAPEX deferrals by SMEs | -1.10% | National, manufacturing regions most impacted | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Skills Shortage in Cybersecurity & AI

Vacancies for IT professionals reached 149,000 in 2024, and the labour-market gap could balloon to 780,000 by 2026, creating structural hiring bottlenecks. Cybersecurity talent is in particularly short supply: 70% of organisations reported measurable business impact from AI-enabled cyberattacks in 2024. Rising wage inflation forces SMEs to compromise on security postures or outsource critical functions, tempering the growth outlook of the Germany ICT market. [3]Bundesamt für Sicherheit in der Informationstechnik, “Cybersecurity Report 2024,” bsi.bund.de

High Energy Prices for Data-Centre Operations

Electricity costs averaging EUR 78.51 per MWh in 2024 weighed on data-centre margins and deterred some expansion plans. Operators now consume roughly 3.7% of national power output, but the market continues to expand as efficiency gains and renewable-energy purchase agreements offset some input-cost pressure. Vodafone’s solar-panel roll-out across 200 network locations and AWS’s long-term offshore-wind contracts illustrate industry-led mitigation strategies. Still, energy price volatility remains a drag on hyperscale build-outs and challenges the pace at which the Germany ICT market can absorb new AI and cloud workloads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Software Outpaces Services in Growth Momentum

IT services held the largest Germany ICT market share of 31.72% in 2025 thanks to integration projects required to weave legacy architectures into modern cloud environments. The software segment, however, is charting the fastest 8.92% CAGR as enterprises pivot toward off-the-shelf platforms that scale globally and embed AI out of the box. Software spending contributed USD 52 billion to the Germany ICT market size in 2025 and is slated to reach USD 86.84 billion by 2031, buoyed by SaaS ERP conversions and low-code development suites. Hardware revenue remains pressured by commoditised margins, though the EU Chips Act has unlocked local wafer-fab investments that may induce an up-cycle in semiconductor equipment demand from 2027 onward. Siemens’ Xcelerator illustrates how software-centric portfolios can stretch across industrial domains, while telecom services capture incremental ARPU from 5G enterprise contracts. Together, these dynamics underline an enduring shift from bespoke services to repeatable, cloud-native software within the Germany ICT market.

Second-order effects are equally telling. ISVs inject embedded AI modules that compress decision-making time in plant operations, customer service and compliance monitoring. Systems integrators respond with packaged migration services to preserve relevance, while channel partners push outcome-based pricing. The result is a virtuous cycle: software penetration fuels recurring revenues, improves vendor gross margins and reinforces investment capacity, further accelerating the Germany ICT market expansion.

By Enterprise Size: SMEs Become the Pace-Setters

Large corporates continued to generate more than 60% of the Germany ICT market size in 2025, reflecting complex multi-year modernisation programmes and sizeable managed-service contracts. Yet SMEs now represent the growth frontier, with a projected 9.99% CAGR that exceeds the overall market by 120 basis points. This acceleration stems from cloud operating models that turn traditional CAPEX into scalable OPEX, freeing cash for AI pilots, e-commerce integrations and cybersecurity upgrades. Public-cloud hyperscalers deepen localisation measures—data-centre regions staffed by EU citizens and privacy-shielded support—to unlock the latent Mittelstand opportunity.

SME adoption patterns also drive ecosystem change. Domain-specific marketplaces deliver drop-in microservices, reducing the need for in-house developers and smoothing digital skill deficits. Financial institutions roll out embedded-finance APIs that simplify cross-border trade for manufacturing exporters, nudging fresh infrastructure spend. As SMEs climb the technology maturity curve, the Germany ICT market benefits from broadened demand diversity and resilience against sector-specific downturns.

By Industry Vertical: Healthcare Takes the Growth Crown

Manufacturing maintained the lion’s share of Germany ICT market revenue with 18.76% in 2025, underpinned by Industry 4.0 investments that synchronise robotics, edge analytics and digital twins across factory floors. Even so, healthcare and life sciences now exhibit an 11.42% CAGR—the fastest among all sectors—as electronic patient records, tele-diagnostics and AI-based imaging systems receive legislative and reimbursement backing. Hospitals push cloud-hosted platforms to meet stringent data-protection standards while enabling cross-institutional data exchange for research.

Adjacent verticals are equally active. Banks and insurers expand cyber-resilience architectures to align with Digital Operational Resilience Act obligations, driving uptick in zero-trust networks and advanced SOC services. Public-sector entities pursue citizen e-government portals, and retailers deploy predictive inventory algorithms to contain inflationary cost pressures. These cross-vertical advancements reinforce the breadth of opportunity within the Germany ICT market, encouraging vendors to invest in sector-specific blueprints and compliance overlays.

By Deployment Model: Public-Cloud and Sovereign Variants Accelerate

On-premises environments still dominate the Germany ICT market share owing to legacy application footprints and stringent compliance regimes in sectors such as defence and public administration. Nevertheless, public-cloud workloads are expected to clock a striking 13.95% CAGR over 2026-2031, propelled by AWS’s EUR 7.8 billion European Sovereign-Cloud roadmap and comparable offerings from Microsoft and Google Cloud. The Germany ICT market size for public-cloud deployments is projected to jump from USD 32 billion in 2025 to USD 70.12 billion by 2031, narrowing the on-premises gap.

Hybrid and private-sovereign constructs flourish in parallel. Gaia-X-compliant nodes leverage open-source frameworks and trusted-connector models to preserve data sovereignty without compromising hyperscale economics. T-Systems’ Sovereign Cloud and Schwarz Group’s stack on Google Cloud illustrate how retailers, manufacturers and energy utilities balance regulatory adherence with innovation velocity. This architectural pluralism ensures that every workload—from latency-sensitive factory control to bursty AI model training—finds a cost-efficient, compliant landing zone, magnifying the growth canvas of the Germany ICT market.

Geography Analysis

Germany ICT market is fueled by automotive and industrial automation clusters in Munich, Stuttgart and Nuremberg. Berlin has emerged as the national nucleus for AI startups, drawing venture flows of USD 2.4 billion in 2024, while Hamburg and Bremen apply ICT innovation to maritime logistics and port optimisation use-cases. North Rhine-Westphalia, Germany’s most populous state, extends the footprint with large enterprise users in chemicals, steel and consumer goods.

Digital-infrastructure disparities remain pronounced. While urban hubs enjoy fibre penetration above 70%, rural localities in Mecklenburg-Western Pomerania and Saxony-Anhalt linger below 20%, constraining edge-computing rollout and smart-agriculture pilots. Federal grants target 50% nationwide fibre-to-the-home coverage by 2025 and universal reach by 2030, a milestone that could unleash another adoption wave across the Germany ICT market. Frankfurt’s DE-CIX continues to reign as Europe’s largest internet-exchange point, yielding unrivalled interconnection density that attracts additional datacentre builds and cloud on-ramps.

Geopolitical and energy variables shape location choices. The Rhine-Neckar and Lusatia regions tout surplus renewable capacity and vacant industrial land, luring hyperscale operators eager to cap energy costs and hit carbon targets. Cross-border integration projects with Austria, Poland and the Netherlands foster trans-European data flows and harmonise spectrum policies, making Germany an indispensable node in the continent-wide digital backbone. Collectively, these regional dynamics create a multilayered demand profile that broadens the addressable Germany ICT market.

Competitive Landscape

Competition is vigorous yet relatively concentrated: the top five vendors commanded nearly half of 2024 spend, giving the Germany ICT market a moderate-concentration profile. Deutsche Telekom, Vodafone and Telefónica anchor network services, while SAP dominates enterprise applications and AWS, Microsoft and Google Cloud split the bulk of public-cloud workloads. Each of these incumbents strengthens local credentials through sovereign-cloud controls, German-language support and in-country SOCs to comply with national privacy statutes.

Incumbent partnerships reveal a strategic tilt toward ecosystem alliances. Deutsche Telekom’s industrial AI cloud with NVIDIA bundles telco connectivity, GPU compute and certified data governance into a single proposition tailored for Mittelstand manufacturers. Siemens and Accenture’s 7,000-strong venture targets software-defined manufacturing, fusing operational domain know-how with AI and data-engineering skills. Start-ups such as Aleph Alpha and 1NCE penetrate niches of sovereign AI and global IoT connectivity, leveraging German regulatory familiarity as a competitive differentiator.

M&A activity intensified in 2024-2025, with HMS Networks buying PEAK-System for automotive-grade CAN solutions and VINCI Energies acquiring Fernao Group to bulk up cybersecurity reach. This consolidation trend supports a layered market where infrastructure heavyweights, specialised ISVs and regional integrators share the value chain. Their co-opetition, underpinned by joint go-to-market programmes, injects both innovation and price discipline into the Germany ICT market. [4]Amazon Web Services, “AWS European Sovereign Cloud,” aboutamazon.eu

Germany ICT Industry Leaders

Deutsche Telekom AG

SAP SE

Amazon Web Services

Microsoft Deutschland GmbH

Vodafone GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amazon Web Services announced a EUR 7.8 billion investment in its European Sovereign Cloud, fully located and governed within the EU.

- June 2025: Deutsche Telekom and NVIDIA launched Europe’s first industrial AI cloud packing 10,000 GPUs for design, engineering and robotics workloads.

- April 2025: Bechtle won a EUR 770 million framework contract to supply 300,000 Apple devices to German federal agencies.

- April 2025: Siemens and Accenture formed the Accenture Siemens Business Group, employing 7,000 experts to accelerate software-defined manufacturing.

Germany ICT Market Report Scope

The information and communication technology (ICT) sector combines manufacturing and service businesses whose products primarily fulfill or allow information processing and communication via electronic methods, including transmission and display. The ICT sector contributes to technical advancement, increased output, and productivity.

The Germany ICT Market is segmented by type (hardware, software, IT services, telecommunication services), size of an enterprise (small and medium enterprises, large enterprises), industry vertical (BFSI, IT and telecom, government, retail and e-commerce, manufacturing, energy and utilities, and other industry verticals).

The market sizes and forecasts are in value (USD million) for all the above segments.

By Type

| Hardware |

| Software |

| IT Services |

| Telecommunication Services |

By Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By Industry Vertical

| BFSI |

| IT and Telecom |

| Government and Public Sector |

| Retail and E-commerce |

| Manufacturing |

| Energy and Utilities |

| Healthcare and Life-Sciences |

By Deployment Model

| On-Premise |

| Public Cloud |

| Private/Sovereign Cloud |

| Hybrid Cloud |

| By Type | Hardware |

| Software | |

| IT Services | |

| Telecommunication Services | |

| By Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By Industry Vertical | BFSI |

| IT and Telecom | |

| Government and Public Sector | |

| Retail and E-commerce | |

| Manufacturing | |

| Energy and Utilities | |

| Healthcare and Life-Sciences | |

| By Deployment Model | On-Premise |

| Public Cloud | |

| Private/Sovereign Cloud | |

| Hybrid Cloud |

Key Questions Answered in the Report

What is the projected value of the Germany ICT market by 2031?

The market is forecast to reach USD 325.29 billion by 2031, expanding at a 8.79% CAGR.

Which segment is growing fastest within the Germany ICT market?

Public-cloud deployments lead with a 13.95% CAGR outlook, driven by sovereign-cloud initiatives and hyperscaler investments.

How significant is AI spending in Germany’s ICT landscape?

AI revenues are projected to hit EUR 11.7 billion (USD 13.1 billion) in 2024, boosted by major investments from Microsoft, OpenAI and Deutsche Telekom.

Why are SMEs critical to Germany’s ICT growth?

SMEs adopt cloud-first models that cut upfront CAPEX and unlock agile innovation, underpinning a 9.99% CAGR that outpaces larger enterprises.

What are the main challenges holding back the Germany ICT market?

A shortage of cybersecurity and AI specialists, together with elevated energy prices for data centres, act as the primary brakes on growth.

Which industries are investing most aggressively in ICT solutions?

Manufacturing remains the largest spender, but healthcare and life sciences register the fastest 11.42% CAGR due to digital-health reforms.

Page last updated on: