Belgium Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

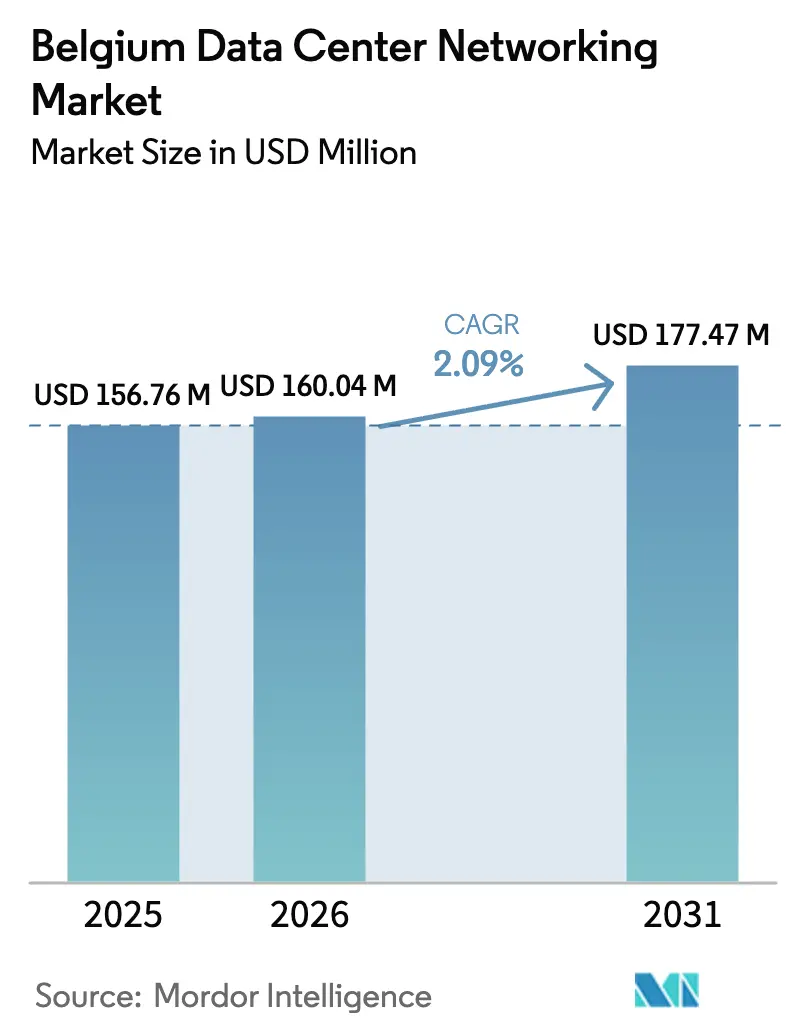

| Base Year Market Size (2025) | USD 156.76 Million |

| Market Size (2026) | USD 160.04 Million |

| Market Size (2031) | USD 177.47 Million |

| Growth Rate (2026 - 2031) | 2.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Data Center Networking Market Analysis by Mordor Intelligence

Belgium data center networking market size in 2026 is estimated at USD 160.04 million, growing from 2025 value of USD 156.76 million with 2031 projections showing USD 177.47 million, growing at 2.09% CAGR over 2026-2031. This steady trajectory mirrors the market’s gradual maturation as Belgian operators upgrade for AI-optimized traffic flows, sovereign data-routing mandates, and power-efficient designs. Heightened demand is reinforced by Google’s EUR 1 billion expansion pledge at St. Ghislain and by EU Digital Decade funds that earmark EUR 205 billion for regional digital transformation. Grid-connection bottlenecks and talent shortages temper momentum, yet policy-driven investments in climate-neutral edge nodes, offshore-wind PPAs, and 400 GbE switching sustain a stable growth outlook for the Belgium data center networking market. Vendors capable of combining hardware, software, and services around AI, security, and sustainability enjoy a strategic advantage as enterprises pursue cloud-first strategies and hyperscalers race to deploy capacity ahead of neighboring Netherlands and Germany.

Key Report Takeaways

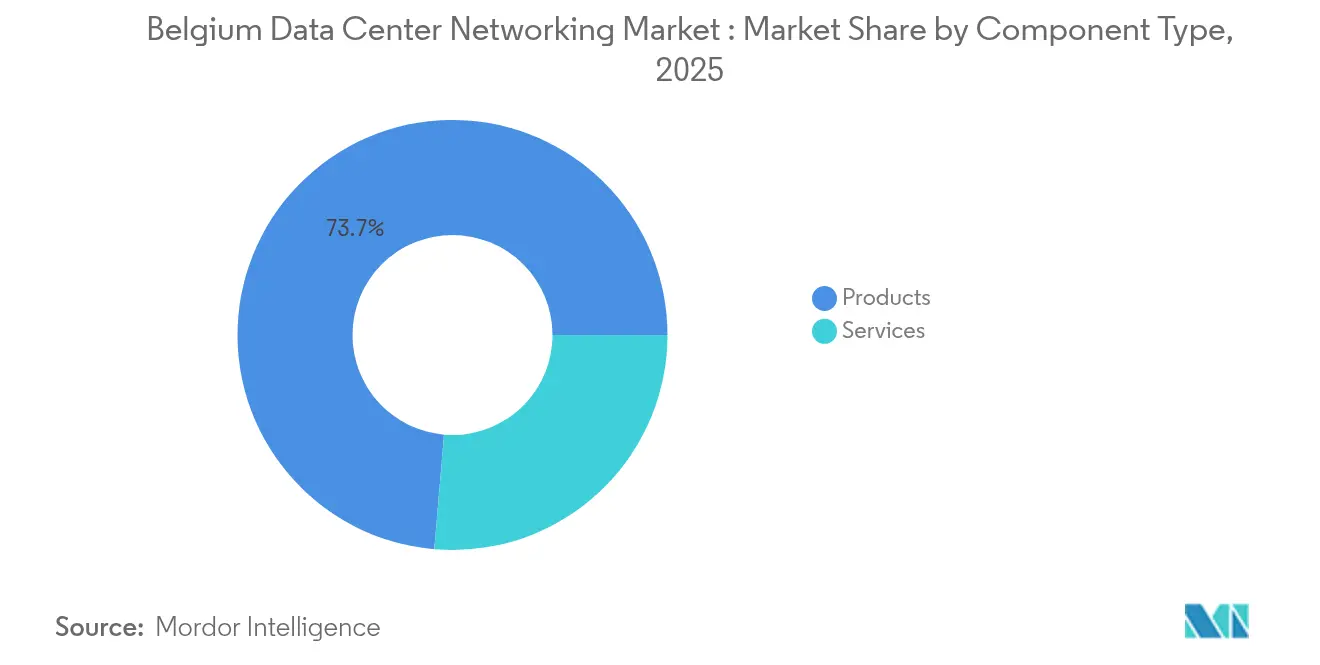

- By component, Products accounted for 73.65% of Belgium's data center networking market share in 2025, while Services are projected to expand at a 5.12% CAGR through 2031.

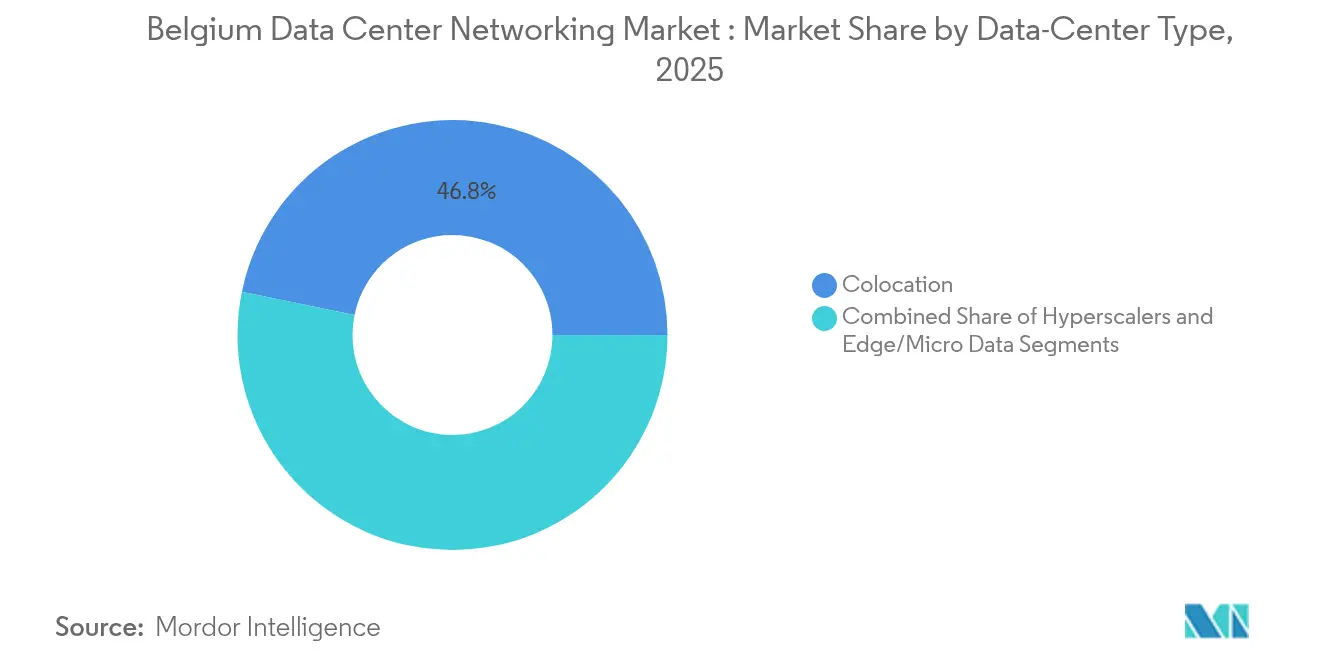

- By data-center type, Colocation held 46.78% of the Belgium data center networking market size in 2025; Hyperscalers and Cloud Service Providers post the fastest CAGR at 7.05% to 2031.

- By end-user, IT & Telecommunications captured 31.95% of 2025 revenue, whereas Healthcare & Life Sciences is forecast to grow at a 6.05% CAGR over 2026-2031.

- By bandwidth, the 50-100 GbE category commanded 32.85% of Belgium data center networking market share in 2025, yet >100 GbE bandwidth is rising at a 6.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Belgium operates as part of an interconnected international environment rather than as a self-contained country level unit. The data center networking market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

Belgium Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cloud-storage workloads | +0.8% | Global, concentrated in Brussels-Antwerp corridor | Medium term (2-4 years) |

| Surge in AI/ML traffic requiring 400 GbE+ switching | +0.6% | National, early adoption in hyperscaler facilities | Short term (≤ 2 years) |

| Edge-data-center roll-outs along Belgium’s 5G corridors | +0.4% | National, focused on TEN-T transport networks | Medium term (2-4 years) |

| EU Digital Decade funds for sovereign data-routing | +0.3% | EU-wide, Belgium benefits from strategic location | Long term (≥ 4 years) |

| Green-PPA incentives tied to North Sea offshore wind | +0.2% | Coastal Belgium, extending to inland facilities | Long term (≥ 4 years) |

| Brussels-based financial-sector data-localization mandates | +0.1% | Brussels Capital Region, spillover to Flanders | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cloud-Storage Workloads

Enterprise cloud adoption is recasting network-design priorities as hybrid and multi-cloud architectures become standard. Workload mobility between private racks and global hyperscale fabrics forces Belgian operators to deploy higher-bandwidth links, embrace SDN for policy-driven routing, and adopt zero-trust segmentation. Financial institutions such as Euroclear signed seven-year cloud deals with Microsoft to boost AI analytics, exemplifying the sector’s appetite for burstable traffic corridors. Cloud-first roadmaps compel upgrades from 25 GbE leaf-spine to 100 GbE or 400 GbE trunks, fueling sustained hardware refresh cycles and managed-service demand. Belgian managed service providers profit by bundling connectivity, observability, and compliance into outcome-based contracts that offset talent shortages. As more workloads shift into SaaS and PaaS offerings, latency-sensitive storage replication across regionally diverse availability zones cements long-term demand for the Belgium data center networking market.

Surge in AI/ML Traffic Requiring 400 GbE+ Switching

Large language models and computer-vision pipelines create elephant flows that saturate legacy 100 GbE fabrics. Operators respond by adopting 400 GbE leaf-spine designs, RDMA over Converged Ethernet, and congestion-avoidance algorithms that minimize head-of-line blocking. The Ultra Ethernet Consortium’s protocol work accelerates adoption paths toward 800 GbE and 1.6 TbE. Cisco Nexus HyperFabric AI, co-engineered with NVIDIA, bundles telemetry, liquid-cooling-ready optics, and trust-domain isolation, enabling Belgian facilities to deliver deterministic bandwidth for training clusters.[1]Cisco Systems, “Introducing Cisco Secure AI Factory,” Cisco, cisco.com Early movers report double-digit efficiency gains in GPU utilization, strengthening the business case for capex-heavy optical upgrades. The competitive race among hyperscalers to scale AI drives front-loaded demand, keeping the Belgium data center networking market on a hardware-refresh cycle shorter than the historical five-year average.

Edge-Data-Center Roll-Outs Along Belgium’s 5G Corridors

EU TEN-T logistics routes intersect Belgium’s ports, airports, and rail hubs, creating fertile ground for low-latency edge nodes that support connected mobility, warehouse automation, and smart-city analytics. The 5 G-Blueprint pilot between Antwerp and Vlissingen showcases cross-border teleoperations that depend on under-10-ms round-trip latency. Edge nodes require ruggedized 100 GbE switches, timing accuracy below 50 ns, and automated service chaining that can scale across hundreds of micro-locations. Municipalities partner with operators to host curbside micro-datacenters that backhaul into larger colocation campuses via dark-fiber rings. Vendors supplying hardened optics and simplified zero-touch provisioning gain an early foothold before volume deployments ramp after 2026. As private 5 G licenses proliferate, campus-edge convergence blurs the line between telco and enterprise networks, expanding total addressable demand for the Belgian data center networking market.

EU Digital Decade Funds for Sovereign Data-Routing

The Digital Decade policy earmarks climate-neutral edge nodes and cross-border corridors that keep EU-citizen data within sovereign routes.[2]European Commission, “Digital Decade Policy Programme 2030,” European Commission, ec.europa.eu Belgium’s junction between London-Amsterdam-Frankfurt traffic and subsea cables positions it as a preferred hand-off point for regulated industries. To win grants, operators must demonstrate compliance with ENISA conformity assessments and the upcoming Cyber-Resilience Act. That drives uptake of European-developed routers featuring crypto-agile hardware, deterministic telemetry, and data-sovereign path selection. Belgium-based integrators package AAA, lawful-intercept, and quantum-safe key-exchange into their managed WAN services, capturing incremental revenue and lifting service CAGR above hardware growth. Over the long term, these policy funds embed digital-sovereignty compliance as a baseline feature in every new build, anchoring growth for the Belgian data center networking market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified DC-network engineers | -0.4% | National, acute in Brussels and Antwerp | Short term (≤ 2 years) |

| Grid-connection queues delaying new halls | -0.3% | National, severe in high-demand areas | Medium term (2-4 years) |

| Escalating capex for 400 GbE optics and liquid cooling | -0.2% | Global, affecting all market segments | Short term (≤ 2 years) |

| EU Eco-design directive raising compliance costs | -0.1% | EU-wide, Belgium implementing by September 2024 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified DC-Network Engineers

Recruitment pipelines lag the pace of facility expansion, with half of Belgian operators reporting unfilled vacancies for network architects, automation engineers, and security specialists. Competition from fintech and cybersecurity firms drives turnover, while remote-work flexibility lures talent toward global roles. Although the Flemish regional government funds micro-credential programs for SDN, only a minority of graduates gain hands-on exposure to 400 GbE optics or liquid-cooling deployments. Projects, therefore, lean on high-cost contractors, lengthening integration timelines and trimming margins. Some operators postpone refresh cycles, depressing near-term hardware revenue inside the Belgium data center networking market. Managed-service providers capture share by offering outcome-based SLAs, but overall CAGR softens until reskilling initiatives bear fruit.

Grid-Connection Queues Delaying New Halls

European transmission operators face thousands of megawatts in queue backlogs, and Belgium’s grid-access approvals have stretched beyond five years for new megawatt-scale halls. Without guaranteed power, developers defer fibre-pull and networking procurements, slowing addressable demand. Operators pivot to on-site batteries and diesel-gensets to shorten timelines, yet those interim solutions raise opex and carbon intensity, conflicting with EU taxonomy rules. A national task force is exploring shared-grid upgrades around port zones, but relief is unlikely before 2027. The drag on facility-go-live schedules translates directly into fewer switch and router shipments in the near term, tempering growth for the Belgium data center networking market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Momentum Despite Product Dominance

The Services segment is projected to grow at a 5.12% CAGR, even though Products still delivered 73.65% of 2025 revenue. Managed network services, driven by AI workload complexity and scarce engineering talent, underpin this outperformance. Training, integration, and lifecycle automation are in high demand as enterprises outsource to specialists instead of building in-house skills. Large public-sector contracts, such as the Belgian Ministry of Defense hiring Legrand Data Center Solutions for turnkey deployments, signal longer multi-year service engagements. Meanwhile, product sales mature because switch-replacement cycles lengthen once 400 GbE fabrics are deployed. Nevertheless, AI cluster roll-outs ensure a premium tier of optics and DPUs sustains core hardware revenue in the Belgium data center networking market.

Operators increasingly procure bundled hardware-plus-services to guarantee SLA compliance around jitter, packet loss, and energy efficiency. Installation projects now incorporate liquid-cooling loops, structured cabling rated for 1.6 TbE, and digital-twin modelling for predictive maintenance. This hybrid procurement style blurs the boundary between capex and opex, providing steady annuity income to integrators. Consequently, while Products remain the largest slice of the Belgium data center networking market size, Services’ rising contribution signals a shift toward outcome-based economics that aligns with AI-driven continuous deployment cycles.

By End-User: Healthcare Digitization Accelerates Networking Demand

Healthcare & Life Sciences registers the fastest CAGR at 6.05% through 2031, despite IT & Telecommunications retaining the largest 2025 share. Digitally transforming hospitals deploy telemedicine, AI diagnostics, and real-time monitoring, pushing up bandwidth and latency requirements. To meet GDPR and NIS2 directives, operators integrate in-line encryption and micro-segmentation into healthcare networks. Electronic Health Record sync and imaging archiving demand east-west traffic patterns that reward spine-leaf architectures. In contrast, financial services networks stabilise after early cloud migrations, though data-localization statutes still necessitate high-resilience, low-latency circuits in the Brussels cluster.

Pharmaceutical research parks adopt edge analytics for lab automation and genomic sequencing, creating micro-data-center opportunities in Wallonia. Manufacturing adds demand by wiring predictive-maintenance sensors to on-prem edge stacks, but growth lags healthcare due to more conservative capex cycles. Cumulatively, these vertical shifts diversify the Belgium data center networking market and promote specialized service offerings around sector-specific compliance frameworks.

By Data-Center Type: Hyperscalers Drive Infrastructure Evolution

Hyperscalers and cloud service providers are forecast to expand at a 7.05% CAGR, outpacing colocation, although the latter retains 46.78% of 2025 revenue. Google’s EUR 1 billion expansion exemplifies hyperscalers’ appetite for renewable-powered, AI-ready Belgian capacity. These builds standardize on high-density racks, phased-array optics and fabric automation, lifting average network spend per megawatt. Colocation operators counter by adding high-speed cross-connect ecosystems that mimic cloud on-ramps, prolonging their relevance and preserving the Belgium data center networking market share associated with multi-tenant models.

Edge and micro-data-centers, while still a small slice, surge in port cities and along 5G corridors. Their needs differ: compact form factors, temp-hardened equipment, and autonomous orchestration. Vendors that modularize switch-OS stacks and supply line-card options for harsh environments gain a first-mover edge. This heterogeneity across facility types expands the solution mix and cushions the Belgium data center networking market against single-segment volatility.

By Bandwidth: High-Speed Adoption Accelerates AI Readiness

The greater than 100 GbE tier is rising at a 6.38% CAGR as GPU clusters demand wider pipes, whereas 50-100 GbE still held 32.85% of 2025 spend. Operators leapfrog intermediate speeds, retiring less than or equal 10 GbE and 25-40 GbE links to curb operational complexity. Linear pluggable optic transceivers at 800 GbE reduce heat to help facilities meet EU Eco-design power targets. Standard-setting bodies advance 1.6 TbE roadmaps, signaling another upgrade wave inside the forecast window, which will reinforce high-end revenue inside the Belgium data center networking market size for bandwidth-intensive applications.

Adoption barriers remain: steeper optic prices and the need for liquid-cooling retrofits. Yet AI training efficiency gains outweigh capex premiums for hyperscalers. Enterprises follow suit in smaller increments, adopting 100 GbE Top-of-Rack and 400 GbE spines, keeping the sales funnel healthy across product classes.

Geography Analysis

Belgium’s central location and multilingual workforce help it capture spillover demand from grid-saturated Netherlands and compliance-restricted United Kingdom. Brussels anchors government and finance workloads, enjoying sovereign-cloud mandates that insist on in-country routing. Flanders attracts greenfield hyperscale builds thanks to available land parcels near offshore-wind interconnects, aligning with corporate carbon-neutral pledges and EU taxonomy requirements. Wallonia, traditionally manufacturing-oriented, now promotes defense-cloud and aerospace analytics, prompting specialized edge facilities.

Cross-border fibre with France and Germany accelerates data-localization adherence, requiring encrypted, telemetry-rich routers capable of auditing path compliance. Subsequent demand filters into the Belgium data center networking market through high-capacity DWDM gear and intent-based WAN controllers. The Princess Elisabeth Island power hub will feed 3.5 GW of wind into the grid, freeing new megawatts for data centers while obliging operators to implement grid-interactive networking gear for power-modulation telemetry. Dutch congestion yields near-term migration of projects to Ghent or Liège campuses, mitigating queue risks and granting Belgium an interim capacity advantage.

Regional 5G and edge initiatives foster distributed micro-facilities along transport corridors. Antwerp’s port rolls out private 5G to enable autonomous cranes, necessitating local packet-core and compute nodes with sub-5 ms latency. These nodes cascade incremental switch and firewall sales into the Belgium data center networking market. Collaboration with Luxembourg on financial clearing houses spurs resilient backbone builds that traverse both countries, underlining Belgium’s role as an inter-EU data hub.

The data center networking market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Europe, North America, and South America, along with detailed country-level analysis for Italy, Germany, United States, Brazil, Norway, and Netherlands.

Competitive Landscape

Industry consolidation produces a moderately concentrated field, led by Cisco, VMware, NVIDIA, and a cadre of optical component specialists. Cisco’s Nexus platform continues to dominate spine-leaf architectures, and its Secure AI Factory demonstrates a deep pivot toward vertically integrated AI fabrics. VMware leverages its vSphere heritage to lock in existing enterprises despite uncertainty after Broadcom’s acquisition. NVIDIA’s integration of Mellanox technology propels it from accelerator vendor to end-to-end network infrastructure supplier, especially for AI fabric deployments. Arista Networks registers outsized growth in 400 GbE shipments, signalling intensifying competition in the high-performance segment.

Strategic partnerships cluster around AI and sustainability: Dell-Equinix supply private AI stacks; Nutanix allies with Pure Storage, NVIDIA, and Cisco to present an alternative to VMware; and Nokia’s O-RAN contract with Deutsche Telekom widens its credibility in open networking. Belgian procurement remains relationship-driven, advantaging incumbents proficient in local compliance regimes and bilingual support. White-box and software-only challengers struggle with certification cycles and channel coverage, limiting disruption in the Belgium data center networking market.

Key vendor tactics include co-designing photonic roadmaps with optic makers, embedding telemetry ASICs for energy accounting, and offering consumption-based pricing that syncs with enterprise cloud budgets. Sustainability badges tied to Eco-design compliance and Scope 3 reporting move from marketing differentiators to RFP gatekeepers. Overall, competitive positioning now hinges on breadth of AI readiness, sustainability roadmaps and managed-service overlay.

Belgium Data Center Networking Industry Leaders

Cisco Systems Inc.

Dell Technologies Inc.

Hewlett Packard Enterprise Co.

Broadcom Inc. (incl. Brocade)

Juniper Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cisco and NVIDIA introduced the Cisco Secure AI Factory architecture, bundling vertically integrated compute, fabric, and security modules for enterprise AI centers, with general availability slated for late 2025.

- March 2025: Proximus divested its data-center portfolio to DataCenter United, signalling consolidation and potential network-refresh programs.

- May 2025: Nutanix expanded alliances with NVIDIA, Pure Storage, and Cisco to position itself as a VMware alternative in AI-ready hybrid-cloud stacks.

- December 2024: Equinix partnered with Dell Technologies to deliver private AI solutions through IBX campuses and the Dell AI Factory with NVIDIA.

- December 2024: Nokia secured an O-RAN swap deal with Deutsche Telekom covering 3,000 German sites, illustrating European telco diversification.

- April 2024: Google committed EUR 1 billion to a new Belgian data center, boosting local demand for 400 GbE switching and renewable PPAs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Belgium data center networking market as the annual revenues generated within the country from switches, routers, network interface cards, storage-network fabrics, load balancers, and related software that are deployed inside colocation, hyperscale, edge, and enterprise data centers. The figure stands at USD 156.76 million for 2025, as captured by Mordor Intelligence analysts. This definition follows industry practice by measuring original equipment sales and recurring software licenses booked to Belgian facilities, regardless of vendor headquarters.

Scope exclusion: Structured premises cabling, building-management systems, and wide-area carrier services are left outside this sizing because they are treated in separate Mordor coverage.

Segmentation Overview

- By Component

- Products

- Ethernet Switches

- Routers

- Storage Area Network (SAN)

- Application Delivery Controllers (ADC)

- Network Security Appliances

- Software-Defined Networking (SDN) Controllers

- Optical Interconnects

- Services

- Installation and Integration

- Training and Consulting

- Support and Maintenance

- Managed Network Services

- Products

- By End-User

- IT and Telecommunications

- Banking, Financial Services and Insurance (BFSI)

- Government and Defense

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Other End-Users

- By Data-Center Type

- Colocation

- Hyperscalers/Cloud Service Providers

- Edge/Micro Data Centers

- By Bandwidth

- Less Than or Equal to 10 GbE

- 25–40 GbE

- 50–100 GbE

- Greater than 100 GbE

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed network architects at Belgian colocation providers, procurement leads at two hyperscalers, and local system integrators spanning Flanders and Wallonia. These conversations confirmed real-world equipment lifecycles, discount ladders, and expected migrations to 800 GbE, filling gaps that secondary material could not address.

Desk Research

We began with publicly available Belgian customs exports, Eurostat PRODCOM codes for communications hardware, and annual utilisation data published by BNIX, the national internet exchange. Trade-body whitepapers from BELTUG, Proximus investor filings, and vendor 10-Ks supplied shipment and average-selling-price markers. To corroborate trends, our team accessed D&B Hoovers for company revenue splits and Dow Jones Factiva for contract awards that signal hardware refresh cycles. Finally, patent analytics from Questel helped estimate the cadence of 400 GbE design wins. The desk sources mentioned illustrate our approach; many additional documents were reviewed to validate and clarify inputs.

A second pass mapped European Commission Digital Decade funding releases, Google and Microsoft hyperscale CAPEX notes, and Brussels-Antwerp fiber roll-out milestones, ensuring macro factors were correctly encoded in the model.

Market-Sizing & Forecasting

A top-down build linked Belgium's installed rack count and average port density to hardware replacement rates, which were reconstructed from production, import, and trade data. Select bottom-up checks sampled vendor shipments and channel price audits served as guardrails for each component line. Key variables include: 1. Rack adds driven by new MW of IT load, 2. Average switch ports per rack, 3. Port-speed mix shift toward >100 GbE, 4. Mean equipment resale values, 5. Service attach rates for managed support. Five-year forecasts employ multivariate regression blended with ARIMA to project each driver, and consensus outlooks from our interviews moderate the final curve. Where supplier roll-ups under or overshot top-down outcomes, gap-filling rules apportioned variance to the most volatile inputs before finalizing totals.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, peer review by a senior analyst, and sign-off by the data-quality team. We refresh the model every twelve months and trigger interim revisions when facility announcements or currency shifts exceed preset thresholds.

Why Mordor's Belgium Data Center Networking Baseline Commands Reliability

Published estimates often diverge because firms apply dissimilar scopes, price bases, and refresh cadences.

Key gap drivers for Belgium include whether campus LAN gear is blended with data-center-only products, how euro values are converted to dollars, and if analysts report shipment year or installation year. Our disciplined scoping and annual refresh make the baseline dependable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 156.76 M (2025) | Mordor Intelligence | - |

| USD 378 M (2023) | Regional Consultancy A | Includes enterprise campus switches and passive cabling, uses list prices |

| USD 800 M (2023) | Trade Journal B | Covers all networking products, not limited to data centers, applies broader channel estimates |

In short, clients gain a transparent, repeatable view anchored to data-center-exclusive hardware and grounded in variables that matter most to Belgium's operators. This is why many stakeholders rely on Mordor's numbers when sizing opportunities or benchmarking investment plans.

Key Questions Answered in the Report

What is the current size of the Belgium data center networking market?

The Belgium data center networking market size at USD 160.04 million in 2026 and is projected to rise to USD 177.47 million by 2031.

Which segment is growing fastest within the market?

Services deliver the fastest growth at a 5.12% CAGR, driven by demand for managed network operations, integration and AI-fabric consulting.

How are AI workloads influencing networking investments in Belgium?

AI training clusters require 400 GbE and 800 GbE switching fabrics, pushing operators toward liquid-cooled optics, congestion-aware protocols and telemetry-driven automation.

Why are grid-connection delays considered a restraint?

Lengthy power-access queues postpone new data-hall commissioning, which in turn delays networking hardware purchases and cools near-term market growth.

What role does the EU Digital Decade play in Belgium’s market outlook?

Digital Decade funding promotes sovereign data-routing and climate-neutral edge nodes, creating fresh opportunities for compliant, energy-efficient networking solutions.

Which bandwidth tier holds the largest share today?

The 50-100 GbE tier commands 32.85% of 2025 revenue, though >100 GbE is expanding more rapidly at a 6.38% CAGR.

Page last updated on: