Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

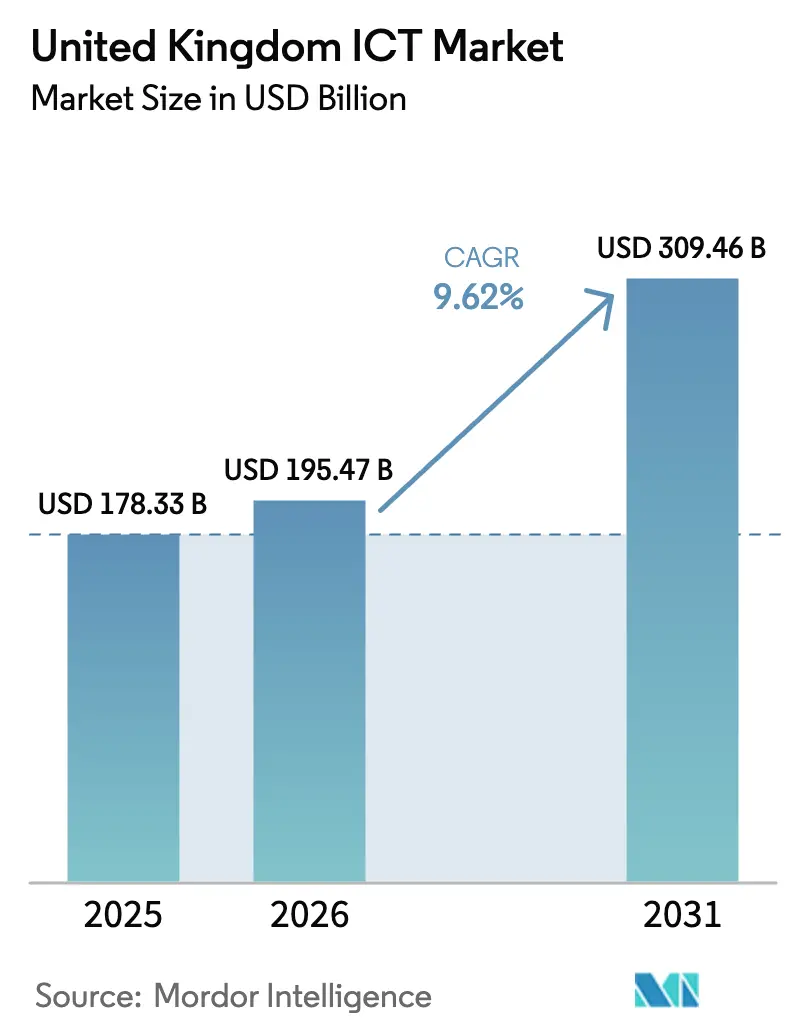

| Base Year Market Size (2025) | USD 178.33 Billion |

| Market Size (2026) | USD 195.47 Billion |

| Market Size (2031) | USD 309.46 Billion |

| Growth Rate (2026 - 2031) | 9.62% CAGR |

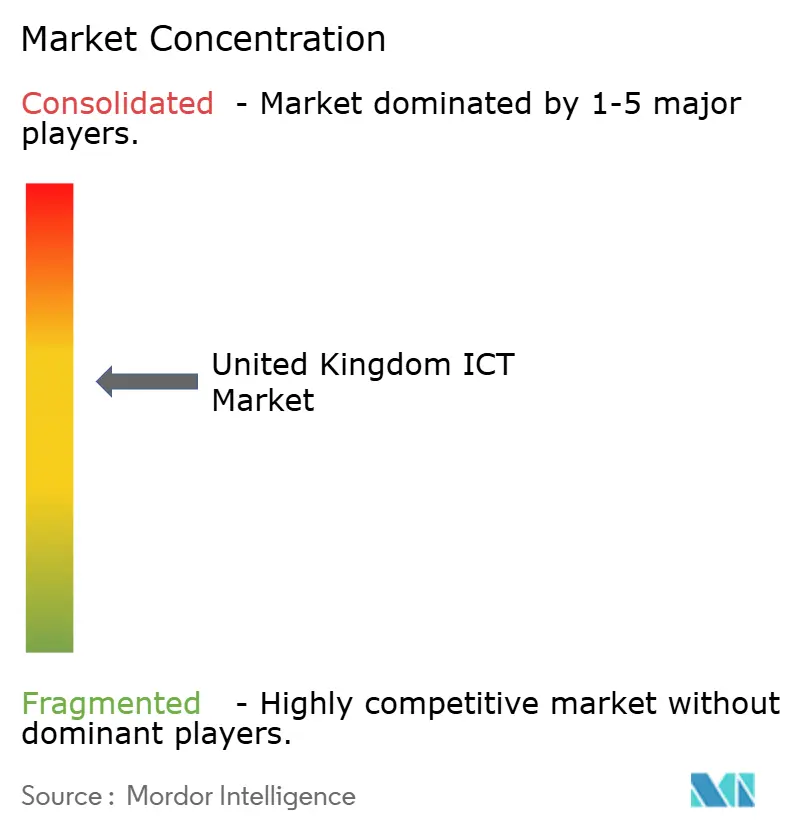

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom ICT Market Analysis by Mordor Intelligence

United Kingdom ICT market size in 2026 is estimated at USD 195.47 billion, growing from 2025 value of USD 178.33 billion with 2031 projections showing USD 309.46 billion, growing at 9.62% CAGR over 2026-2031.[1]Department for Science, Innovation & Technology, “National Semiconductor Strategy,” gov.uk The growth outperforms traditional infrastructure categories because public- and private-sector buyers treat technology as a value generator rather than a cost center. Demand accelerates on three fronts: large transformation programs in central government, hyperscale cloud investments by global providers, and an unprecedented wave of small-business digitalization support. At the same time, 5G rollout, quantum-ready data-center construction, and industry-specific SaaS offerings deepen the addressable base of the United Kingdom ICT market, attracting new entrants and reshaping incumbent strategies. Intensifying cyber-threat exposure pushes budgets toward zero-trust architectures, turning security from a compliance expense into a board-level resilience priority. Supply-chain volatility in semiconductors remains a drag, yet policy interventions such as the GBP 1 billion (USD1.34 billion ) National Semiconductor Strategy are designed to mitigate hardware bottlenecks and maintain momentum.

Key Report Takeaways

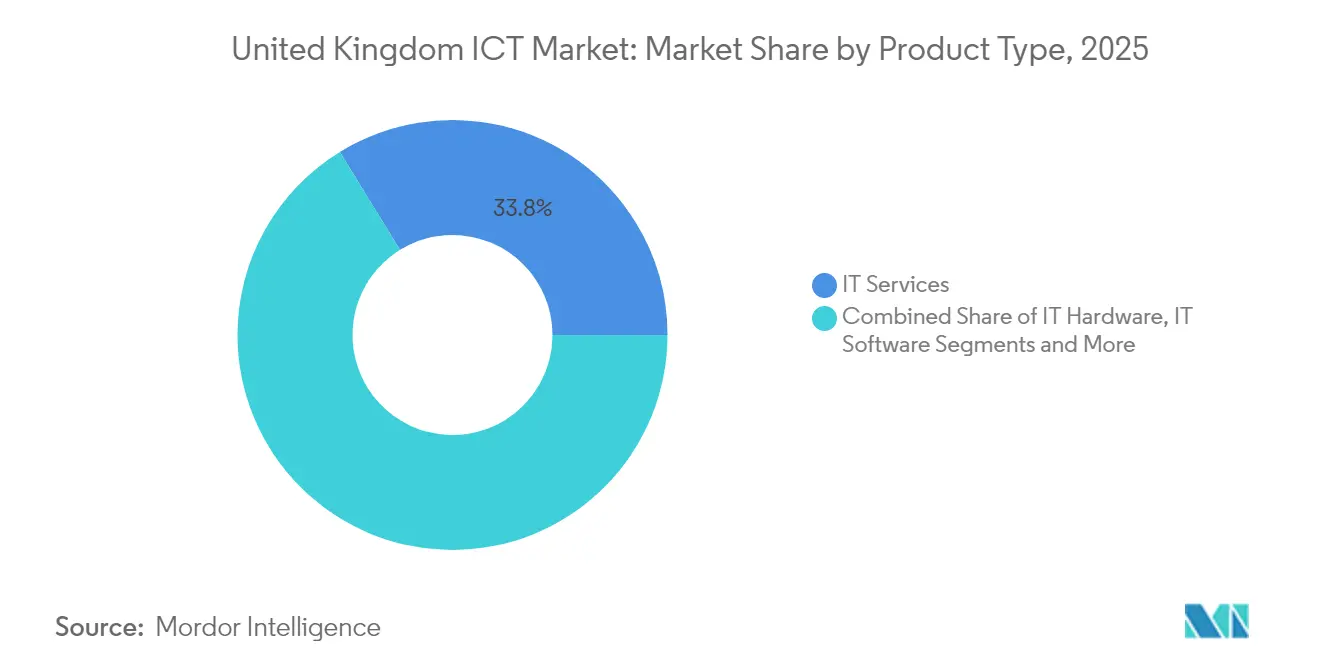

- By product type, IT services captured 33.78% of the United Kingdom ICT market share in 2025, with Security, the fastest-growing type at 9.71% CAGR through 2031.

- By enterprise size, large enterprises held 55.48% of the United Kingdom ICT market size in 2025, while SMEs recorded a 10.04% CAGR through 2031.

- By end-user vertical, Public administration contributed 18.11% market share in 2025, while gaming and esports is projected to expand at an 11.06% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SaaS demand surge | +2.1% | London and South East | Medium term (2-4 years) |

| Digital tech in healthcare | +1.8% | National (NHS) | Long term (≥ 4 years) |

| 5G infrastructure expansion | +1.5% | Urban clusters | Medium term (2-4 years) |

| Enterprise cyber-security spend | +1.4% | Nationwide | Short term (≤ 2 years) |

| SME digital incentives | +1.2% | Regions via Made Smarter | Medium term (2-4 years) |

| Quantum-ready data centers | +0.8% | Golden Triangle and Scotland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Surge in Demand for Software-as-a-Service (SaaS)

SaaS adoption extends from office productivity to mission-critical finance, HR, and supply-chain processes, rewriting procurement models that once favored perpetual licenses. The Help to Grow Digital program issued GBP 5,000 (USD 6,749.0) software vouchers to an addressable base of 1.2 million firms, creating a digitally enabled SME segment that now supports recurring SaaS revenues. Roughly 90% of UK companies used at least one cloud service in 2024, up from 78% in 2022, and vendors are pivoting to verticalized offerings addressing strict sectoral regulations. Freemium entry tiers, in-product AI assistants, and consumption-based billing make SaaS attractive to budget-conscious firms, while integrations with HMRC and Companies House APIs eliminate manual compliance effort.

Rise in Digital Technology Adoption Across Healthcare

Only 63% of NHS trusts had foundational electronic patient-record functionality in 2024, leaving a GBP 23.98 billion (USD 32.36 billion ) investment gap that is now earmarked for fulfillment by 2026 NHS.UK. Spending priorities encompass interoperable data warehouses, AI-assisted diagnostics, and zero-trust security layers to safeguard sensitive health information. Remote-monitoring pilots demonstrated 26% readmission reductions, encouraging scaling across integrated care systems. Vendors specializing in HL7-FHIR integration, medical-grade cloud hosting, and federated learning see accelerated procurement cycles as trusts move from proof of concept to production deployments. Telehealth services, normalized during COVID-19, remain above 30% of outpatient consultations, sustaining demand for secure video, IoT wearables, and analytics platforms.

Expansion of 5G Infrastructure Nationwide

Standalone 5G covers more than 85% of the UK population in 2025, enabling network slicing that supports dedicated enterprise use cases. Government 5G Testbeds and Trials funding of GBP 200 million (USD 269.96 billion) validated applications such as connected ambulances, smart ports, and agricultural drones. Manufacturing plants implementing private 5G report latency reductions from 40 ms on Wi-Fi to below 5 ms, unlocking closed-loop automation. Operators diversify from connectivity toward managed edge services, partnering with hyperscalers to co-locate MEC nodes inside data centers. Spectrum auctions in 700 MHz and 3.6 GHz bands reserve portions for local industrial licenses, fueling growth for integrators that bundle radios, IoT sensors, and application frameworks.

Escalating Cyber-Security Spending by UK Enterprises

Cyber-security revenue reached GBP 13.2 billion (USD 17.81 billion) in 2024 with 67,000 employees, reflecting a pivot from compliance-led spending to resilience investments. High-profile ransomware attacks such as the Synnovis breach triggered GBP 3.07 million (USD 4.14 million) in ICO fines, pushing boards to allocate 15-20% of IT budgets to security versus 9% three years earlier. Zero-trust network access, immutable backups, and cyber-security insurance are now mandatory line items. Financial services and public administration lead adoption of quantum-safe cryptography pilots. Domestic vendors leverage the UK’s NCSC guidelines as a market differentiator, exporting solutions to Commonwealth nations that mirror UK cyber regulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor supply volatility | -1.6% | Manufacturing and data centers | Medium term (2-4 years) |

| Ransomware prevalence | -1.2% | Healthcare and local gov. | Short term (≤ 2 years) |

| Post-Brexit compliance complexity | -0.9% | Multinationals and finance | Long term (≥ 4 years) |

| Advanced AI/ML talent shortage | -0.7% | London, Cambridge, Edinburgh | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply-Chain Volatility and Inflationary Pressure

The UK sources 98% of advanced chips from Asia, exposing data-center builds and device refresh cycles to prolonged lead times and 12-18% price inflations. Domestic revenue of GBP 9.6 billion (USD 12.95 billion) represents just 2% of the global semiconductor market, so the National Semiconductor Strategy directs GBP 1 billion (USD 1.34 billion) to design tools, compound fabs, and advanced packaging over ten years. Still, capacity additions will not mature before 2028, forcing integrators to redesign bill-of-materials around more readily available nodes and to expand die redistribution partnerships in Europe.

High Prevalence of Data Theft and Ransomware Incidents

Ransomware victim rates doubled to 1% of UK organizations between 2024 and 2025, equal to roughly 19,000 entities. Healthcare disruptions, including a blood-test backlog in southeast London, underscored the economic toll. The forthcoming Cyber Security and Resilience Bill mandates incident reporting within 72 hours and could prohibit public-sector ransom payments, adding compliance overhead yet improving data fidelity for threat intelligence. Budgets are reallocated from growth projects to endpoint detection, SOC as a service, and cyber-hygiene training, dampening discretionary ICT spending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type : Services Architecture Drives Market Evolution

The United Kingdom ICT market posted a service-heavy mix in 2025 as IT services commanded 33.78% of spending. Within this stream, managed services grew at 9.9% to mitigate skills shortages, and cloud professional services rose 12.4% on multi-cloud complexity. The convergence of infrastructure and communications produced turnkey platforms blending compute, storage, and connectivity. Hardware demand remained resilient for edge routers and ruggedized devices that support hybrid working and IoT.

The shift to subscription models redefined software cash flows, boosting the attach rate of AI inference engines and low-code platforms. Vendors monetize vertical APIs and compliance modules, turning ERP and CRM suites into ecosystems. Security, the fastest-growing type at 9.71% CAGR, now bundles threat intelligence and incident response, embedding services into licensing fees. This dynamic positions outcome-based providers to displace legacy product vendors across the United Kingdom ICT market.

By Enterprise Size: SME Digitalization Accelerates Market Dynamics

Large enterprises controlled 55.48% of 2025 outlays, benefiting from scale and global purchasing frameworks. They continue to integrate OT and IT systems, spending on API gateways and data fabric solutions. Meanwhile, SMEs representing 99.9% of UK businesses deliver the fastest incremental revenue, growing at 10.04% CAGR. Grants such as Made Smarter’s GBP 20,000 voucher for manufacturing SMEs catalyze robotics, MES, and predictive-maintenance deployments.

Cloud freemium tiers, pay-as-you-go analytics, and no-code automation tools flatten adoption barriers. SMEs increasingly tap managed security and virtual CIO services, accounting for 46% of new service desk tickets in 2025. Digital-flux SMEs improve turnover by 25% on average within a year of software adoption, reinforcing a positive feedback loop that enlarges the United Kingdom ICT market.

By End-User Industry Vertical: Public Sector Leadership Drives Adoption

Public administration contributed 18.11% to 2025 revenue, driven by HMRC’s Making Tax Digital, local council cloud migrations, and defense cybersecurity overhauls. Framework agreements such as G-Cloud 14 simplify call-offs and sustain volume.

Gaming and esports posted the highest CAGR at 11.06%, riding GBP 1.56 billion (USD 2.10 billion) mobile-gaming receipts, cloud-gaming infrastructure deals, and VR studio tax credits. BFSI digitizes AML and open-banking APIs, while energy utilities invest in smart-grid OT security. Manufacturing’s Industry 4.0 spend surpasses GBP 4 billion (USD 5.4 billion), with 69% of firms integrating AI by 2025. Healthcare digital projects pivot from record digitization to AI triage and surgical robotics, adding long-tail demand for secure high-bandwidth connectivity throughout the United Kingdom ICT market.

Geography Analysis

London and the South East contribute roughly 44.60% of the United Kingdom ICT market. Dense financial-services campuses require low-latency colocation and quantum-secure fiber, supporting an ecosystem of managed-service providers and fintech scale-ups. Data-center vacancy in Greater London fell below 4% in 2025 following hyperscaler expansions and sovereign-cloud launches.

The Cambridge-Oxford arc combines deep-tech venture funds with world-leading research universities, nurturing chip-design houses and quantum-computing startups. Local councils deploy 5G-connected autonomous shuttles and smart-city IoT, boosting regional ICT orders. Scotland’s Edinburgh-Glasgow corridor focuses on fintech and game development. Public-sector devolution grants fund rural broadband and digital-skills academies, spreading demand across the Highlands Wales leverages its compound-semiconductor cluster in Newport to court defense and automotive contracts, while Northern Ireland’s shared-services centers consume cloud HR and finance platforms. Levelling-Up funds channel 5G and fiber builds into the Midlands and North, pulling hyperscale edge nodes to Manchester and Leeds. The regulatory landscape, featuring retained EU GDPR alignment plus emerging UK Data Protection reform, requires vendors to architect multi-region data-sovereignty strategies across the United Kingdom ICT market.

Regulatory Landscape

The United Kingdom ICT market operates under an active telecoms and digital policy regime led by the Department for Science, Innovation and Technology (DSIT) and enforced by Ofcom. On 27 April 2026, DSIT issued its Statement of Strategic Priorities for telecommunications, directing Ofcom to prioritize economic growth, investment and network security, providing a clearer policy signal for gigabit-capable broadband, 5G rollout and business connectivity regulation.

Security and resilience compliance requirements continue to shape vendor and operator practices. The Telecommunications (Security) Act 2021 and the Electronic Communications (Security Measures) Regulations 2022 place security obligations on public telecoms providers with Ofcom oversight. Anti-fraud measures, including requirements to collect and share data on scam messages and phone numbers, also raise operational compliance needs across messaging and voice transit. In parallel, regulatory focus on the PSTN-to-VoIP migration and leased-line market rules influences enterprise communications refresh cycles and procurement timing.

Value Chain Analysis

The UK ICT value chain spans hardware and network equipment OEMs, electronic communications network operators, and wholesale connectivity providers through to cloud and platform providers, application providers (including IoT, M2M and managed services), systems integrators and MSPs, and finally enterprise and public-sector end users. Ofcom characterizes digital communications as an interlinked chain where connectivity underpins higher layers such as cloud, digital applications and content. This makes interoperability, service assurance and performance SLAs across tiers central to how solutions are designed and delivered.

Industry bodies help coordinate ecosystem needs and standards adoption across the chain, including techUK (technology and digital policy), ISPA (internet services), Comms Council UK (professional communications and hosted voice), and the Federation of Communication Services (FCS) (communications services and channels). Security legislation and operator assurance requirements add governance into procurement and supply chain decisions, shaping how network solution providers with local presence, including ZTE (UK), position equipment, software features and support models for compliance-aligned deployments.

Competitive Landscape

The United Kingdom ICT market is moderately concentrated. BT Group, Microsoft, AWS, and Vodafone anchor core infrastructure with long-term government contracts, while Capita, Softcat, and Computacenter provide integration reach into regional enterprises. Hyperscalers expand local zones, with AWS pledging USD 8 billion for new UK data-center capacity through 2030 AWS. Cisco and NVIDIA’s 2025 alliance injects AI-optimized Ethernet fabrics, aligning with demand for GPU-dense clusters.[3]IT Brief UK, “Cisco an NVIDIA Join Forces to Boost AI Data Centres,” itbrief.co.uk

Domestic cyber-security specialists such as Darktrace and NCC Group capture zero-trust adoption waves. Semiconductor design leaders ARM and Graphcore leverage government R&D credits, and quantum-computing startups like Quantinuum attract foreign investment. Vendors differentiate on sector credentials ISO 27001 for healthcare, FCA accreditation for BFSI increasing switching costs.

Strategic moves include BT and Toshiba’s quantum-secure network launch, Virgin Media O2’s GBP 700 million (USD 944.9 billion) radio upgrade, and Lenovo’s TruScale as-a-service push. Channel partners consolidate, as evidenced by Softcat acquiring regional MSPs to strengthen public-sector footprint. Sustainability mandates drive providers to procure 100% renewable power for data centers, influencing colocation site selection in the United Kingdom ICT market.

United Kingdom ICT Industry Leaders

ZTE Corporation

Cisco Systems, Inc.

Fujitsu Services Ltd

CommScope Holding Co. Inc.

Ciena Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Investment-oriented telecoms policy and regulation create whitespace for suppliers that bundle connectivity, cloud and managed services into outcomes-led propositions for enterprises and the public sector. DSITs 27 April 2026 Statement of Strategic Priorities and Ofcoms Telecoms Access Review 2026-31 provide a five-year framework centered on promoting competition and investment in fixed broadband, mobile and business connectivity. This supports demand for network build, upgrade and modernization programs across access, backhaul and core.

Two near-term opportunity areas stand out from market signals and program milestones: (i) the PSTN-to-VoIP migration, with a key Openreach customer milestone referenced for January 2027, which drives replacement cycles for voice, contact-center and unified communications alongside security and fraud controls; and (ii) AI-driven networking and wireless modernization in enterprises, supported by Cisco findings that 70% of UK organizations view wireless investments as critical for operational efficiency and productivity. Providers that can integrate Wi-Fi, private 5G, edge compute and zero-trust controls into managed offerings are positioned to win multi-year contracts tied to modernization, compliance and service assurance requirements.

Recent Industry Developments

- July 2026: The UK Governments Building Digital UK (BDUK) published a Project Gigabit rollout update citing 287,510 premises covered under the GBP 5 billion program. The milestone reinforces a long-cycle pipeline of procurement for access build, CPE, field services and systems integration in hard-to-reach areas, expanding addressable demand beyond major metros.

- June 2026: Cisco signed a Memorandum of Understanding with the UK Department for Science, Innovation and Technology (DSIT) to support the governments AI Opportunities Action Plan, including digital skills initiatives. The agreement strengthens public-private alignment around AI readiness, creating pull-through for campus networking, security and collaboration platforms used in workforce and public-sector modernization programs.

- December 2024: BT, Toshiba and Equinix activated a commercial quantum-key-distribution network in the UK aimed at finance clients. The launch highlighted a move from pilots toward deployable quantum-secure communications, supporting demand for specialized managed services and secure connectivity architectures in regulated sectors.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the United Kingdom ICT market is defined as the total revenues generated from ICT products and services sold for use in the UK, covering core IT and communications spending across business and public sector customers.

Scope exclusions: This sizing excludes informal or unpaid digital activity and generally does not count internal IT labor that is not billed as a commercial service.

Segmentation Overview

- By Product Type

- IT Hardware

- Computer Hardware

- Networking Equipment

- Peripherals

- IT Software

- IT Services

- IT Consulting and Implementation

- IT Outsourcing (ITO)

- Business Process Outsourcing (BPO)

- Managed Security Services

- Cloud and Platform Services

- IT Infrastructure

- IT Security/Cybersecurity

- Communication Services

- IT Hardware

- By Enterprise Size

- Small and Medium-sized Enterprises

- Large Enterprises

- By End-user Industry Vertical

- Government and Public Administration

- BFSI

- IT and Telecom

- Energy and Utilities

- Retail, E-commerce, and Logistics

- Manufacturing and Industry 4.0

- Healthcare and Life Sciences

- Oil and Gas

- Gaming and E-Sports

- Other Verticals

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to frame the market and set realistic input ranges before the model is built. We mainly rely on official statistics and sector publications to understand overall ICT demand, telecom and broadband indicators, and the policy backdrop that can affect investment cycles.

Public sources referenced include UK Office for National Statistics releases, Ofcom communications reports, DSIT updates on digital infrastructure, HMRC trade statistics for relevant equipment flows, and International Telecommunication Union indicators for cross-checking definitions. We also review company annual reports, investor presentations, reputable press coverage, and selected paid subscriptions for company financials, news and financials, import and export shipment-level checks, and patent landscaping where it helps confirm innovation and investment direction. This list is not exhaustive, and other references are used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what desk research cannot fully show, such as how spending splits across software, services, and communications are changing, and what pricing and contract structures are doing to reported revenues. We speak with a mix of suppliers, channel and delivery partners, enterprise buyers, and subject experts across the UK, then reconcile any conflicting inputs before finalizing assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 16% | |

| Mid tier: 45% | Functional/Unit leaders: 29% | |

| Smaller Players: 20% | Managers: 55% |

Market-Sizing & Forecasting

The core sizing starts with a top-down build where national ICT spend is reconstructed using UK-facing revenue pools across communications services and IT, and then broken down using adoption and intensity indicators. To keep the figures grounded, the totals are corroborated with selective bottom-up checks, such as sampled supplier revenue splits, channel feedback on run-rate demand, and ASP times volume sanity checks for common hardware and connectivity bundles.

Practical inputs that guide the model include mobile and fixed broadband subscriber trends, average revenue per user movement in communications, enterprise cloud and managed services uptake, data center capacity additions and utilization direction, and cybersecurity demand signals linked to compliance and incident frequency. Where bottom-up evidence is patchy, the gap is handled by using conservative ranges agreed with interviewees and by keeping adjacent categories from being double counted.

Forecasts are generated using scenario analysis supported by simple time-series smoothing on the more stable lines, and the final outlook is adjusted based on what primary respondents expect for budget cycles, renewal timing, and pricing resets over the next few years.

Data Validation & Update Cycle

Validation is done through several checks so the final market number does not rely on a single assumption. Model outputs are compared against independent signals like sector revenue direction, subscriber and infrastructure trendlines, and documented public spending priorities, which are then reviewed for abnormal jumps or breaks.

If a variance cannot be explained by known events, key inputs are rechecked and selected respondents are re-contacted to confirm what changed in the market. The work goes through multi-step analyst review before sign-off, and reports are refreshed annually with interim updates when material events occur. Before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's United Kingdom Ict Market Size Measured Against Other Published Estimates

Published market numbers for UK ICT can differ even when they look like they cover similar topics, because firms do not always follow the same product and service boundaries, or the same year and currency timing. Differences also show up when one estimate leans heavily on stated budgets while another uses realized revenues, which tends to shift the starting point.

The biggest gap drivers in this market usually come from whether data centers and cybersecurity are counted inside ICT totals, how communications services are treated (for example, consumer connectivity versus broader enterprise contracts), and how price effects are handled when contracts reset. The table points to this scope effect clearly, where IT infrastructure and security are included as separate revenue lines inside the ICT total, a choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 195.47 B (2026) | |

| Industry Publication A | USD 185.00 B (2024) | Uses an enterprise ICT budget lens and an earlier year, which can understate realized service revenues and misses later-period price resets and contract expansions. |

| Regional Consultancy B | USD 162.00 B (2023) | Starts from a narrower ICT grouping and earlier base year, and typically blends several adjacent categories without consistently separating data center infrastructure and cybersecurity as explicit revenue pools. |

Taken together, the spread is mainly explained by timing and what is counted inside ICT versus adjacent technology spending. By keeping the inputs tied to observable demand signals and reconciling them with supplier and buyer feedback, the resulting market value stays traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the United Kingdom ICT market in 2031?

Forecasts place the market at USD 309.46 billion by 2031, up from USD 195.47 billion in 2026.

Which segment grows fastest within UK ICT spending?

IT security leads with a 9.71% CAGR through 2031 as enterprises adopt zero-trust architectures.

How significant is SME demand for technology solutions?

SMEs post a 10.04% CAGR, aided by Made Smarter grants and cloud-based SaaS affordability.

What role does 5G play in enterprise transformation?

Standalone 5G enables low-latency private networks that support Industry 4.0, smart ports, and connected healthcare.

How are semiconductor supply issues being addressed?

The National Semiconductor Strategy allocates GBP 1 billion (USD 1.35 billion) to boost domestic design and advanced packaging capacity.

Why is hybrid deployment the dominant model?

Firms balance cloud scalability with on-prem sovereignty and performance needs, leading to a hybrid approach in most workloads.

Page last updated on: