Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

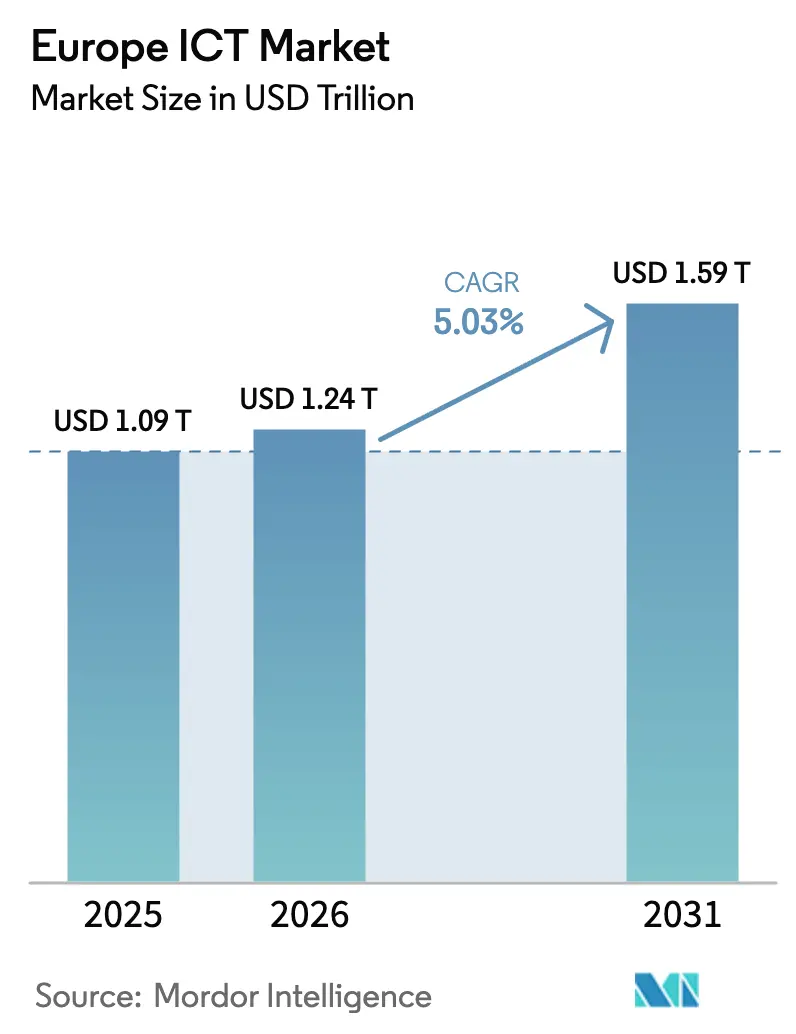

| Base Year Market Size (2025) | USD 1.09 Trillion |

| Market Size (2026) | USD 1.24 Trillion |

| Market Size (2031) | USD 1.59 Trillion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

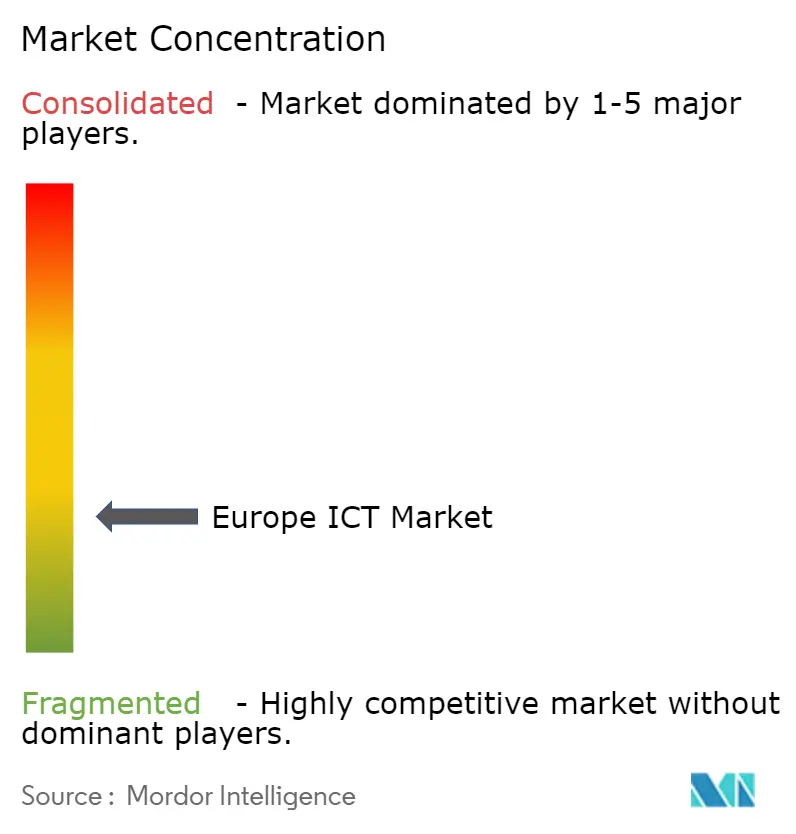

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe ICT Market Analysis by Mordor Intelligence

The Europe ICT Market size is expected to increase from USD 1.09 trillion in 2025 to USD 1.24 trillion in 2026 and reach 1.59 trillion by 2031, growing at a CAGR of 5.03% over 2026-2031. Strong sovereign-cloud mandates, sustained 5G roll-outs, and expanding edge infrastructure are boosting capital expenditure, while Digital Decade grants continue to subsidize broadband and enterprise cloud adoption. Heightened cybersecurity requirements under NIS2, the EU Green Deal’s efficiency targets for data centers, and the rapid pivot toward generative-AI workloads are reshaping vendor roadmaps and compressing time-to-market for new solutions. Competitive intensity is sharpening as hyperscalers address data-residency scrutiny with sovereign offerings and regional champions leverage local compliance expertise to win public-sector deals. The convergence of industrial IoT, edge analytics, and 5G standalone networks is spawning new B2B revenue streams, particularly in manufacturing hubs that demand sub-10-millisecond latency.

Key Report Takeaways

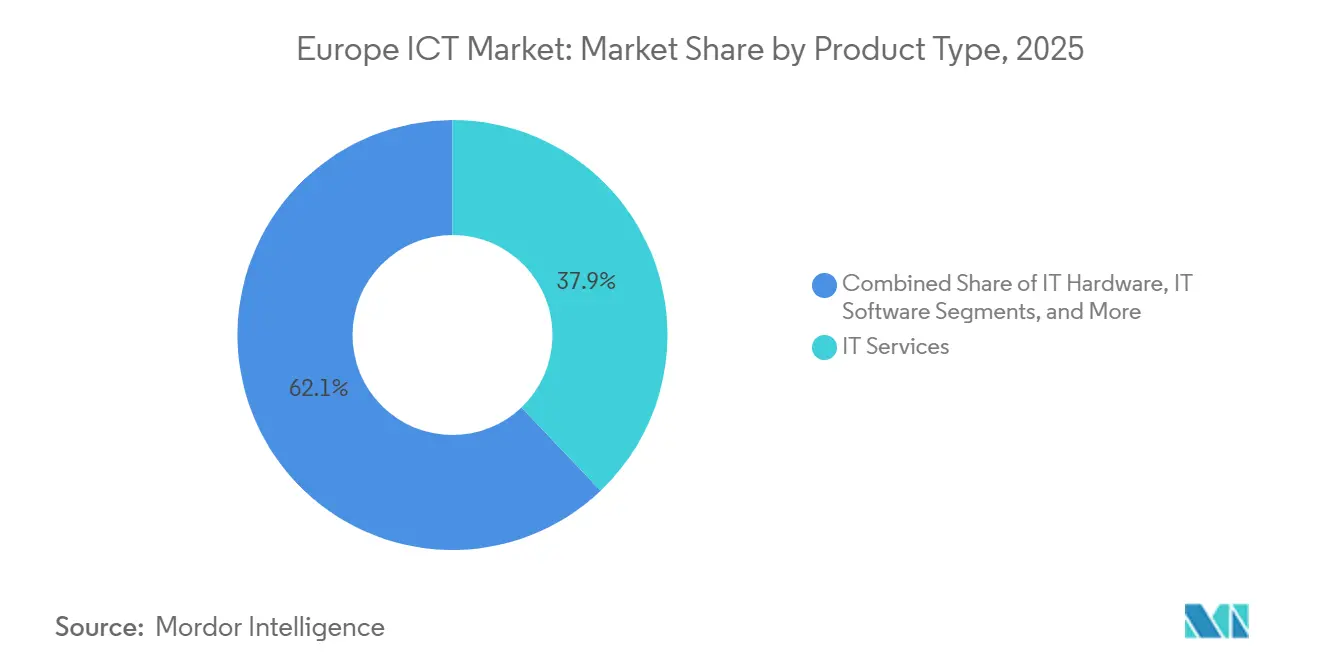

- By product type, IT services led with 37.89% market share in 2025 while IT security and cybersecurity held 7.26% CAGR growth leadership between 2026-2031, outpacing legacy IT hardware.

- By enterprise size, large enterprises retained 71.92% of Europe ICT market share in 2025, while SMEs posted the fastest projected CAGR at 5.41% through 2031.

- By vertical, healthcare advanced at a 6.02% CAGR during 2026-2031, eclipsing banking, financial services, and insurance in growth momentum even as the latter commanded an 18.07% revenue share in 2025.

- By country, Germany led with a 20.04% contribution to the Europe ICT market size in 2025, but Spain recorded the highest 8.13% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated EU Digital Decade Funding 2021-2030 Catalyzing Cloud and 5G Roll-outs | +0.9% | Pan-European, with concentration in Germany, France, Netherlands, Nordics | Medium term (2-4 years) |

| Surge in Sovereign Cloud and Data Residency Requirements Post-Schrems II Ruling | +1.2% | Pan-European, particularly France, Germany, Netherlands | Short term (≤ 2 years) |

| Industrial Edge Computing Demand Driven by Europe's Industry 4.0 Corridors | +0.8% | Germany, Italy, France, Spain (manufacturing hubs) | Medium term (2-4 years) |

| Rising ICT Sustainability Mandates (EU Green Deal) Fueling Green Data Centres | +0.6% | Nordics, Netherlands, Germany (renewable energy leaders) | Long term (≥ 4 years) |

| O-RAN Trials and Early 5G Standalone Deployments Enabling New B2B Services | +0.7% | United Kingdom, Germany, France, Italy | Medium term (2-4 years) |

| Generative AI Upskilling Programmes Stimulating Software and Consulting Spend | +0.9% | Pan-European, with early adoption in United Kingdom, Germany, France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated EU Digital Decade Funding 2021-2030 Catalyzing Cloud and 5G Roll-outs

Large-scale public funding is front-loading network infrastructure timelines. By December 2025, member states had already invested EUR 58 billion toward gigabit connectivity and rural 5G coverage, compressing project cycles that previously stretched to the end of the decade. Vodafone Germany alone switched on 15,000 5G standalone sites in 2025, opening network-slicing pathways for automotive telematics and remote surgery.[1]Vodafone, “5G Stand-Alone Roll-outs in Germany,” vodafone.com SME migration incentives covering up to half of cloud-adoption costs expanded the addressable base for platform vendors, evidenced by a 34% year-on-year rise in SME cloud take-up in 2025. Funding delays tied to state-aid reviews, however, slowed disbursements in Italy and Spain, highlighting execution risk within the bloc.

Surge in Sovereign Cloud and Data-Residency Requirements Post-Schrems II Ruling

The invalidation of the EU-US Privacy Shield triggered sweeping workload repatriation. By 2025, nearly two-thirds of large European enterprises had shifted sensitive data to EU-domiciled providers or on-premises stacks. OVHcloud booked double-digit revenue growth on the back of public-sector wins, while Deutsche Telekom partnered with a major hyperscaler to deliver a Kubernetes-based sovereign cloud aligned with German federal rules. Colocation operators followed suit, expanding low-latency facilities in Frankfurt, Amsterdam, and Paris to serve finance and public-sector users that demand strict jurisdictional control. Elevated legal-review costs continue to lengthen migration cycles, yet overall momentum favors providers with clear data-sovereignty credentials.

Industrial Edge-Computing Demand Driven by Industry 4.0 Corridors

Automotive, machinery, and packaging clusters deployed thousands of new edge nodes in 2025 to support real-time quality control, predictive maintenance, and autonomous-mobile-robot coordination. Strategic partnerships, such as Siemens-Microsoft, embedded analytics directly on the plant floor, cutting unplanned downtime by almost one-quarter across early deployments.[2]Siemens, “Azure Industrial IoT Partnership,” siemens.com Targeted EU-level grants helped Italy and France bring edge platforms to SMEs that traditionally lacked capital for such upgrades, while latency-sensitive use cases validated hardware investments by Schneider Electric and ABB. The region’s emphasis on advanced manufacturing ensures edge installations will remain a growth engine through the medium term.

Rising ICT Sustainability Mandates Under the EU Green Deal Fueling Green Data Centers

New facilities must now achieve a sub-1.3 PUE and source at least 75% renewable electricity by 2027, accelerating corporate power-purchase agreements in wind-and-hydro-rich Nordic countries. Global cloud operators committed multi-billion-euro budgets to carbon-free energy procurement, and retrofits such as direct-to-chip liquid cooling are cutting cooling loads by 40%. The January 2026 lift in carbon-credit prices under the EU ETS rendered coal-powered capacity economically untenable, pushing operators toward locations with abundant renewables. These measures create a dual benefit of lower operating costs and stronger ESG positioning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-Intensive Data Centres Facing Escalating Power and Carbon Taxes | -0.5% | Pan-European, acute in Germany, Netherlands, Belgium | Short term (≤ 2 years) |

| Persistent Digital Skills Gap Slowing Project Timelines | -0.7% | Pan-European, severe in Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Fragmented Spectrum Policies Hindering 5G Economies of Scale | -0.4% | Pan-European, particularly Italy, Spain, Eastern Europe | Medium term (2-4 years) |

| Heightened Cyber-Sovereignty Concerns Limiting US Hyperscaler Penetration | -0.3% | France, Germany, Netherlands, public sector across Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Energy-Intensive Data Centers Facing Escalating Power and Carbon Taxes

Data-center electricity demand hit 104 terawatt-hours in 2025, with hubs in Frankfurt, Amsterdam, and Dublin accounting for almost two-thirds of consumption. A EUR 90-per-tonne carbon-allowance price, effective January 2026, raised operating expenses for non-renewable sites by low-double-digit percentages.[3]European Environment Agency, “EU Emissions Trading System,” eea.europa.eu National interventions reinforce the pressure: Ireland’s moratorium on new Dublin connections and the Netherlands’ energy tax on large facilities are prompting operators to place incremental capacity in Nordic markets or to co-locate near renewable-generation assets. Participation in demand-response programs is compulsory for new German sites above 10 MW, forcing architectural redesigns and accelerating the adoption of battery-backed microgrids.

Persistent Digital-Skills Gap Slowing Project Timelines

Europe lacked roughly half a million ICT professionals in 2025, with Germany alone reporting 96,000 open roles in cloud engineering and cybersecurity. Vacancy rates exceeded 8% across several member states, delaying smart-city initiatives and 5G network deployments by up to nine months. Wage inflation is further compressing service-provider margins, as median salaries for cloud-certified talent in Frankfurt climbed to EUR 85,000 in 2025. EU-sponsored upskilling programs have yet to reach scale, enrolling fewer than 15% of their multi-year targets, which means integration partners must continue to rely on near-shoring and global-delivery centers to bridge capability gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Security Spend Overtakes Legacy IT Horizons

IT security and cybersecurity are projected to expand at a 7.26% CAGR, buoyed by the NIS2 directive’s 24-hour incident-reporting rule that covers 18 critical sectors. Identity and access management stands out, reflecting EU-wide zero-trust mandates that require multi-factor authentication across banking and public services. Cloud-security posture-management tools are growing as enterprises automate compliance checks, while endpoint protection faces price compression due to bundled offerings from major operating-system vendors. Meanwhile, the Europe ICT market size for IT services retains scale leadership, yet automation-rich platform offerings are shrinking traditional consulting effort. Hardware refresh cycles continue to stretch as hybrid work stabilizes, compressing demand for desktop and notebook replacements. Communication-services revenues remain steady due to vendor consolidation and unified-communications bundles that lower total cost of ownership for distributed workforces. Infrastructure spending tilts toward edge form factors, partially offsetting softer demand for large on-premises servers.

Second-generation security controls that combine threat-intelligence feeds with machine-learning analytics are spreading beyond critical infrastructure to mid-market users, signaling a deeper addressable base. Network-security spend benefits from 5G core launches, which embed distributed denial-of-service mitigation at the edge. Application-security adoption also rises as software suppliers face liability under the Cyber Resilience Act, incentivizing secure-by-design practices. Collectively, these patterns confirm that security allocations will continue to capture a rising share of the Europe ICT market.

By Enterprise Size: SMEs Narrow the Digital-Transformation Gap

Large enterprises commanded 71.92% of Europe ICT market share in 2025, driven by complex ERP, supply-chain, and AI-training workloads. Yet small and medium-sized enterprises are forecast to log a 5.41% CAGR, shrinking the adoption divide. Voucher schemes in Germany, Spain, and France subsidize up to half of cloud-migration or e-commerce costs, unlocking latent demand among firms with fewer than 250 employees. Low-code development platforms allow “citizen developers” to automate workflows without specialist coding, reducing dependency on scarce IT talent. On the downside, limited cybersecurity maturity leaves many SMEs vulnerable to ransomware, spurring managed-security-service providers to introduce per-endpoint packages that fit constrained budgets.

Large-enterprise spending is increasingly oriented toward platform modernization and data-sovereignty compliance, reinforcing demand for sovereign-cloud stacks and hybrid architectures. SMEs, conversely, are gravitating toward bundled SaaS suites that integrate CRM, marketing automation, and analytics at predictable monthly rates. Hybrid work patterns persist for more than 70% of SMEs, supporting ongoing investment in collaboration and endpoint-management tools.

By End-User Vertical: Healthcare Surges, BFSI Maintains Scale

Banking, financial services, and insurance retained an 18.07% revenue share in 2025, propelled by open-banking API traffic that more than doubled over two years. Healthcare is slated to grow at a 6.02% CAGR through 2031, as the European Health Data Space mandates cross-border interoperability of electronic health records. Telemedicine remains a mainstream service in primary care, and EU-funded hospital modernization programs in France and Germany are fast-tracking upgrades to EHRs, e-prescribing, and medical imaging. Government and public-sector spend steadied after pandemic peaks but still backs large identity-and-cloud projects such as the EU Digital Identity Wallet. Manufacturing advances stem from Industry 4.0 investments that deploy thousands of edge nodes for real-time analytics, while retail adoption of omnichannel platforms supports inventory visibility across stores and online channels.

The Europe ICT market size for energy and utilities climbs with smart-meter deployments that enable demand-response billing, whereas telecom operators balance network roll-out costs with internal IT-budget constraints. Other segments, including transportation, logistics, education, and hospitality, show steady mid-single-digit expansion as AI-enhanced scheduling and route-optimization applications mature.

Geography Analysis

Germany remains the largest spender, with industrial automation and sovereign-cloud compliance shaping enterprise roadmaps. Automotive OEMs invested heavily in software-defined architectures in 2025, while federal digital strategy funds drove fiber backbone upgrades toward nationwide gigabit coverage. An uptick in ransomware incidents, including a high-profile port outage, catalyzed accelerated cybersecurity roll-outs across logistics and critical infrastructure operators. Persistent talent shortages and wage inflation, however, elongate implementation cycles.

Spain’s momentum builds on expansive fiber networks and Next Generation EU grants that prioritize rural connectivity and SME innovation. National 5G standalone deployments support network slicing for logistics hubs in Madrid and Barcelona, while regional programs in Catalonia and the Basque Country finance edge-computing pilots for manufacturing SMEs. Progressive digital-skills initiatives complement the infrastructure push, compressing adoption barriers for cloud ERP and CRM solutions.

France advances digital sovereignty goals by shifting sensitive workloads to certified providers and funding modernization of tax and healthcare systems. Public-sector contracts underpin steady services revenue for domestic integrators, and a vibrant AI-start-up ecosystem benefits from government-backed research hubs. Meanwhile, the United Kingdom navigates post-Brexit data-adequacy assessments that delay certain cross-border migrations, and Italy accelerates digital-public-administration projects supported by recovery funds. The Netherlands, Nordics, and Eastern Europe round out regional dynamics, each leveraging specific advantages - interconnection density, renewable energy, or near-shoring talent pools - to attract ICT investment.

Competitive Landscape

Europe’s ICT landscape is moderately fragmented, with the top 10 vendors holding about 38% of total revenue. Global hyperscalers continue to scale infrastructure but increasingly partner with regional operators to deliver sovereign clouds that satisfy GDPR and sector-specific mandates. OVHcloud broadened its footprint to 42 data centers across 12 countries by January 2026, targeting public-sector and financial-services clients that require strict data-residency guarantees. Deutsche Telekom teamed with a leading platform provider to launch a sovereign Kubernetes stack aimed at German agencies, blending public-cloud functionality with on-premises control.

Indian heritage service providers increased their share of European outsourcing contracts by leveraging cost-competitive delivery models and robust ISO 27001 compliance, intensifying price competition for incumbents. Cybersecurity specialists gained traction in the SME segment by offering bundled managed-detection-and-response subscriptions that undercut enterprise-grade alternatives. In networking, Ericsson and Nokia vie for Open RAN deployments, while colocation operators such as Equinix expand edge facilities to capture latency-sensitive workloads from finance and gaming customers.

Strategic differentiation increasingly hinges on verticalized solutions, AI-native feature sets, and transparent ESG credentials, all of which influence procurement decisions in a region defined by stringent regulatory oversight.

Europe ICT Industry Leaders

IBM Corporation

Dell Technologies Inc.

Microsoft Corporation

Amazon Web Services, Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Microsoft announced a EUR 3.2 billion (USD 3.6 billion) investment to build a new Azure cloud region in Poland, comprising three availability zones and 200 MW of renewable-powered capacity, with commercial launch set for Q3 2026.

- December 2025: Deutsche Telekom and SAP extended their sovereign-cloud partnership, adding 12 public-sector clients in Germany and France to the RISE with SAP S/4HANA Cloud on T-Systems infrastructure stack.

- November 2025: Google committed EUR 3 billion (USD 3.4 billion) to 24-hour carbon-free energy contracts in Denmark and Finland, ensuring its Hamina and forthcoming Fredericia data centers operate on renewable power.

- October 2025: Accenture acquired Zühlke Group, adding 1,800 engineers across 17 European sites to bolster Industry 4.0 and embedded-system capabilities for automotive and machinery customers.

- September 2025: Orange France activated a 5G-stand-alone core that provides 20-millisecond-latency network slices for logistics and healthcare applications in Paris, Lyon, and Marseille.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the European ICT market as all business and public-sector spending on IT hardware, enterprise software, IT services, data-center and cloud infrastructure, cybersecurity solutions, and fixed or mobile communication services that enable the creation, movement, storage, and protection of digital information, expressed in USD value terms. Mordor Intelligence maps spending at vendor invoice level to consuming industry verticals and deployment models, then aggregates to a regional view.

Scope exclusion: purely consumer electronics such as game consoles, smart TVs, and wearables are left outside the market boundary.

Segmentation Overview

- By Product Type

- IT Hardware

- Computer Hardware

- Networking Equipment

- Peripherals

- IT Software

- IT Services

- IT Consulting and Implementation

- IT Outsourcing (ITO)

- Business Process Outsourcing (BPO)

- Managed Security Services

- Cloud and Platform Services

- IT Infrastructure

- IT Security/Cybersecurity

- Application Security

- Cloud Security

- Data Security

- Network Security

- Endpoint Security

- Infrastructure Protection

- Integrated Risk Management

- Identity and Access Management (IAM)

- Communication Services

- Fixed Voice and Data

- Mobile Voice and Data

- Unified Communications and Collaboration

- IT Hardware

- By Enterprise Size

- Small and Medium-Sized Enterprises

- Large Enterprises

- By End-User Industry Vertical

- BFSI

- Government and Public Sector

- Oil and Gas

- IT and Telecom

- Retail, E-Commerce and Consumers

- Manufacturing and Industrial

- Energy and Utilities

- Healthcare

- Other End-User Industry Verticals

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Nordics

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed CIOs, procurement heads, cloud-service partners, and telecom regulators across Germany, France, the United Kingdom, Spain, the Nordics, and Eastern Europe. Conversations tested adoption rates for cloud and cybersecurity, confirmed average service price points, and clarified how recovery-fund grants translate into ICT outlays, thereby filling gaps evident in public statistics.

Desk Research

We gathered baseline spending pools from open datasets such as Eurostat ICT expenditure tables, the European Commission's Digital Economy and Society Index, OECD digital economy outlooks, ITU telecommunication revenue statistics, and GSMA Intelligence on 5G subscriber growth. Trade releases, listed-company filings, and policy papers (for example, the EU Digital Decade targets) supplied country-level splits, while paid libraries like D&B Hoovers and Dow Jones Factiva helped verify vendor revenues and deal activity. The sources named here are illustrative; many additional databases, journals, and regulatory portals were referenced to cross-check figures and definitions.

Market-Sizing & Forecasting

We begin with a top-down reconstruction of regional ICT outlays using Eurostat industry value added and DESI investment ratios, which are then validated through selective bottom-up checks such as sampled vendor revenue roll-ups and channel shipment audits. Key variables include: 1. Gross fixed capital formation on ICT assets, 2. Cloud workload penetration in enterprise servers, 3. 5G subscriber base versus total mobile connections, 4. Cybersecurity spend per employee in regulated sectors, 5. EU Recovery and Resilience Facility digital allocations, 6. Average contract price for managed services. A multivariate regression model links these drivers to historical spend and projects them forward; ARIMA smoothing handles short-term shocks. Where vendor disclosures lack granularity, ratios from analogous markets and expert feedback bridge the gaps, and results are iterated until the variance against primary inputs stays within five percentage points.

Data Validation & Update Cycle

Outputs pass automated anomaly scans, second-analyst reviews, and senior sign-off. We refresh every twelve months, with mid-cycle updates triggered when exchange-rate moves, major policy shifts, or mega-mergers alter spending baselines. Before release, an analyst revisits each assumption so clients receive the most current view.

Why Mordor's Europe ICT Baseline Commands High Reliability

Published numbers often diverge because firms pick different spending buckets, currency conversions, and refresh cadences. Mordor anchors its baseline in investment statistics aligned to EU definitions, blends them with live price-volume evidence, and updates annually, which reduces scope drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.18 Trillion (2025) | Mordor Intelligence | |

| USD 1.20 Trillion (2024) | Global Consultancy A | Includes consumer electronics and duplicate online advertising spend, inflating totals |

| USD 2.28 Trillion (2023) | Industry Database B | Uses vendor revenue booked in Europe without netting intra-company sales; limited primary validation |

The comparison shows how varying scopes and unchecked double counting can widen estimates. By grounding values in official investment metrics and corroborating them with field intelligence, Mordor delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and reproducible steps.

Key Questions Answered in the Report

How large is the Europe ICT market in 2026 and what growth is expected?

The market stands at USD 1.24 trillion in 2026 and is forecast to reach USD 1.59 trillion by 2031, reflecting a 5.03% CAGR.

Which product segment is expanding the fastest?

IT security and cybersecurity leads, supported by NIS2 compliance, posting a 7.26% CAGR over 2026-2031.

Why is Spain growing faster than other European countries?

Spain benefits from EUR 20 billion of Next Generation EU grants that finance broadband, 5G, and SME digitalization, resulting in an 8.13% CAGR outlook.

What drives healthcare technology investment across Europe?

The European Health Data Space regulation mandates cross-border electronic-health-record interoperability by 2027, accelerating hospital spending on EHR and telemedicine solutions.

How are sustainability mandates affecting data centers?

The EU Green Deal imposes strict efficiency and renewable-energy targets, prompting operators to adopt liquid cooling and secure green power contracts to control operating costs.

What role do sovereign clouds play in Europe’s ICT strategy?

Sovereign clouds address GDPR data-residency requirements, leading many public-sector agencies and regulated industries to migrate sensitive workloads to EU-domiciled infrastructure.

Page last updated on: