Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | 831.40 Thousand tons |

| Market Volume (2026) | 845.69 Thousand tons |

| Market Volume (2031) | 921.08 Thousand tons |

| Growth Rate (2026 - 2031) | 1.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Container Glass Market Analysis by Mordor Intelligence

The Belgium container glass market size was valued at 831.40 thousand tonnes in 2025 and estimated to grow from 845.69 thousand tonnes in 2026 to reach 921.08 thousand tonnes by 2031, at a CAGR of 1.72% during the forecast period (2026-2031). This measured growth trajectory reflects Belgium's mature glass packaging ecosystem, where established recycling infrastructure and regulatory frameworks create stability rather than explosive expansion. The market's evolution centers on sustainability imperatives and technological modernization, with Belgium achieving a 97% glass recycling rate that positions it as a European leader in circular economy practices. Belgium's container glass landscape demonstrates pronounced segmentation dynamics that underscore shifting consumption patterns and industrial priorities. The beverages segment commands 60.19% market share in 2024, driven by the country's robust beer culture and growing wine consumption linked to tourism recovery. However, the cosmetics and personal care segment emerges as the fastest-growing application at 3.17% CAGR through 2030, reflecting Belgium's position as a European hub for luxury packaging and pharmaceutical glass solutions. Color segmentation reveals flint glass maintaining 57.73% market dominance in 2024, while amber glass accelerates at 2.96% CAGR, primarily supporting pharmaceutical applications and premium beverage packaging, where light protection becomes critical. Competitive intensity remains moderate, with established players like Gerresheimer AG and SAVERGLASS Group leveraging technological capabilities to defend market positions against emerging sustainability pressures. The market structure benefits from Belgium's strategic location within the EU single market, enabling efficient cross-border trade and supply-chain optimization. Major capacity investments, including Ciner Glass Belgium's EUR 504 million (USD 567 million) facility in Lommel with 1,300 metric tons daily capacity expected by 2026-2027, signal confidence in long-term demand fundamentals despite near-term headwinds from energy costs and alternative packaging competition. Primary market risks include escalating energy expenses that disproportionately impact glass manufacturing's energy-intensive processes, alongside intensifying competition from lightweight alternatives such as PET and aluminum containers.

Key Report Takeaways

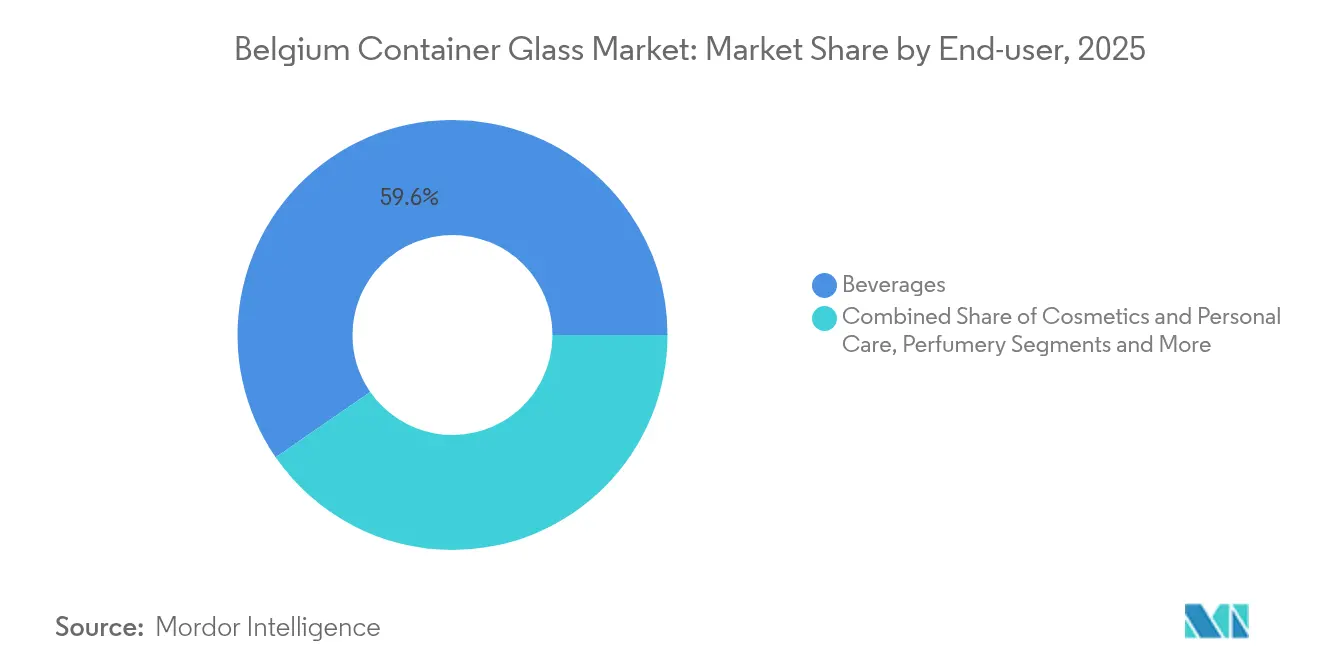

- By end-user, beverages captured 59.63% of the Belgium container glass market share in 2025.

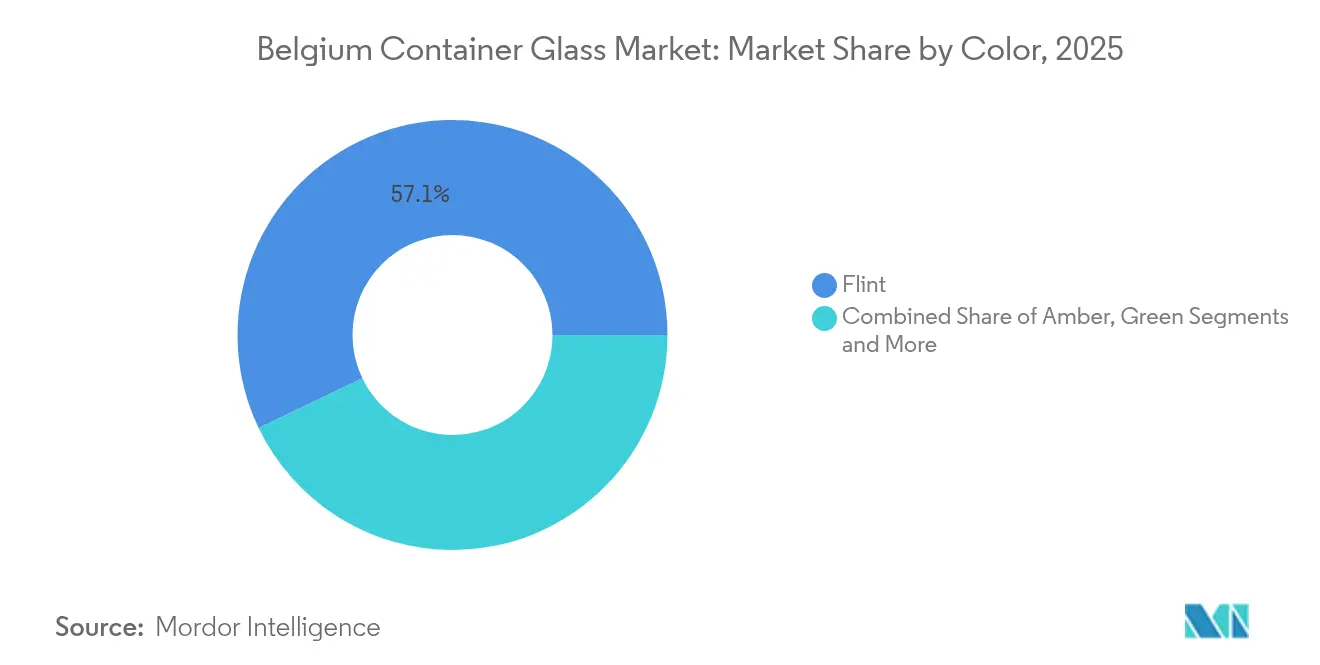

- By color, the Belgiam container glass market for amber glass is projected to grow at a 2.81% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Belgium Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Pharmaceutical and Biotech Packaging | +0.4% | National, with concentration in Flanders region | Medium term (2-4 years) |

| Tourism-Driven Beverage Consumption | +0.3% | National, with peaks in Brussels and coastal regions | Short term (≤ 2 years) |

| Export Potential and EU Market Integration | +0.2% | National, with spillover to neighboring EU markets | Long term (≥ 4 years) |

| Technological Advancements in Glass Manufacturing | +0.3% | National, focused on major production facilities | Medium term (2-4 years) |

| Government Regulations Supporting Recycling | +0.2% | National, aligned with EU directives | Long term (≥ 4 years) |

| Rising Demand from Food and Beverage Sector | +0.3% | National, with regional variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Pharmaceutical and Biotech Packaging

Belgium's pharmaceutical sector expansion drives container glass demand through specialized vial and ampoule requirements that leverage glass's superior barrier properties and chemical inertness. The country's pharmaceutical exports reached significant volumes in 2024, with companies like Johnson & Johnson investing USD 150 million in cell-therapy facilities in Ghent, creating downstream demand for sterile glass packaging solutions. Belgium's regulatory environment, governed by EU Good Manufacturing Practice guidelines and FDA compliance for export markets, necessitates high-quality glass containers that meet stringent sterility and stability requirements. This trend accelerates as Belgium positions itself as a European hub for biotechnology manufacturing, with glass packaging serving critical roles in vaccine storage, injectable drug delivery, and diagnostic applications.

Tourism-Driven Beverage Consumption

Belgium's tourism recovery following pandemic disruptions catalyzes beverage glass-packaging demand, particularly for beer, wine, and spirits consumed in hospitality settings. The country's Horeca (hotels, restaurants, cafes) sector demonstrated resilience with digital enforcement measures like certified cash-register systems improving transaction traceability and formal procurement practices. Tourism patterns favor premium beverage experiences that align with glass packaging's perceived quality advantages over alternative materials. Belgium's beer culture, combined with growing wine appreciation among international visitors, sustains demand for distinctive glass bottles that enhance brand differentiation and consumer experience. The seasonal nature of tourism creates demand fluctuations that require flexible supply-chain management, with peak summer months driving inventory buildup in glass packaging.

Export Potential and EU Market Integration

Belgium's strategic position within the EU single market enables container glass producers to access broader European markets without trade barriers, amplifying domestic production-capacity utilization beyond local consumption limits. The country's well-developed logistics infrastructure and port facilities in Antwerp facilitate efficient export operations to neighboring markets, particularly Germany, France, and the Netherlands. EU packaging harmonization initiatives, including standardized recycling targets and design-for-recycling criteria, create competitive advantages for Belgian producers already compliant with stringent environmental standards. Cross-border trade in glass packaging benefits from reduced regulatory complexity and standardized quality requirements across EU member states.

Technological Advancements in Glass Manufacturing

Innovation in glass production technology enables Belgian manufacturers to improve energy efficiency, reduce carbon emissions, and enhance product quality while maintaining cost competitiveness against alternative packaging materials. Saint-Gobain's successful hydrogen testing in glass furnaces, achieving 30% hydrogen-fuel integration with potential for 70% CO₂ emission reductions by 2030, demonstrates the technical feasibility of decarbonization strategies that address regulatory pressures and customer sustainability requirements.[1]Saint-Gobain, “Yearbook 2023-2024: Towards Ever More Sustainable Construction,” saint-gobain.com Advanced furnace designs and process optimization reduce energy consumption per tonne of glass produced, directly impacting production costs in an energy-intensive industry. Digital monitoring and control systems improve quality consistency while reducing waste and rework costs. Automated handling and packaging systems enhance operational efficiency and worker safety while enabling 24/7 production capabilities that maximize asset utilization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Lightweight Alternatives (Plastic, Aluminum) | -0.3% | National, with higher impact in cost-sensitive segments | Short term (≤ 2 years) |

| High Energy Consumption in Glass Production | -0.2% | National, concentrated at production facilities | Medium term (2-4 years) |

| Carbon Footprint and Emissions from Manufacturing | -0.2% | National, with EU regulatory implications | Long term (≥ 4 years) |

| Cost Sensitivity in Domestic and Export Markets | -0.1% | National and EU export markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from Lightweight Alternatives (Plastic, Aluminum)

Alternative packaging materials present persistent competitive pressure through superior logistics, economics, and lower production costs that appeal to price-sensitive market segments. PET plastic containers offer weight advantages that reduce transportation costs by 40% compared to equivalent glass packaging, creating compelling value propositions for high-volume, low-margin applications. Belgium's first PET recycling plant, operated by Filao, demonstrates the country's commitment to developing circular-economy solutions for plastic packaging that compete directly with glass-recycling infrastructure. Aluminum containers benefit from superior recyclability rates and consumer-convenience factors, particularly in beverage applications where portability and safety considerations favor metal packaging. The competitive landscape intensifies as alternative materials improve barrier properties and aesthetic appeal through advanced coatings and printing technologies.

High Energy Consumption in Glass Production

Energy-intensive glass manufacturing processes expose Belgian producers to volatile energy costs that directly impact production economics and competitive positioning. Glass melting requires sustained high temperatures that consume significant electricity and natural gas, making energy costs a substantial portion of total production expenses. European energy-price volatility, exacerbated by geopolitical tensions and renewable-energy transition challenges, creates unpredictable cost structures that complicate pricing strategies and margin management. Belgium's industrial energy costs remain elevated compared to global competitors, particularly in Asia, creating pressure on export competitiveness and domestic market-share defense. Energy-efficiency investments, while beneficial for long-term cost reduction, require substantial capital expenditures that strain cash flows and delay other strategic initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Dominate Despite Cosmetics Acceleration

Belgium's beverage applications command 59.63% market share in 2025, reflecting the country's deeply embedded beer culture and expanding wine consumption driven by tourism recovery and changing consumer preferences. The alcoholic-beverage segment, particularly beer packaging, benefits from Belgium's international reputation for craft-brewing excellence, with premium glass bottles serving as essential brand-differentiation tools that justify higher retail prices. Wine packaging experiences growth acceleration as Belgium's import market expands and domestic consumption patterns shift toward higher-quality products that demand glass containers for optimal preservation and presentation. Spirits packaging maintains steady demand through duty-free channels and premium positioning strategies that leverage glass's perceived quality advantages.

The cosmetics and personal-care segment emerges as the fastest-growing application at 2.98% CAGR through 2031, driven by Belgium's position as a European hub for luxury packaging solutions and specialized glass-manufacturing capabilities that serve international beauty brands. Food applications, including jams, condiments, and specialty products, maintain stable demand through premium positioning and consumer preference for glass containers in gift and artisanal-product categories. Pharmaceutical packaging, while representing a smaller-volume segment, commands premium pricing and demonstrates resilience through regulatory requirements that favor glass containers for sterile applications and long-term stability testing.

By Color: Flint Leadership Challenged by Amber Growth

Flint glass maintains a 57.12% market share in 2025 through versatility across multiple applications and consumer preference for transparent packaging that showcases product quality and brand aesthetics. Clear glass containers dominate food and beverage applications where visual product presentation drives purchasing decisions, particularly in premium segments where transparency signals quality and purity. The cosmetics sector increasingly favors flint glass for luxury positioning and sophisticated packaging designs that enhance brand perception and justify premium-pricing strategies. However, amber glass accelerates at 2.81% CAGR through 2031, driven primarily by pharmaceutical applications requiring UV protection and premium beverage segments where light-sensitive products demand specialized packaging solutions.

Green glass applications remain concentrated in wine packaging and specialty beverage segments, maintaining a stable market share through traditional consumer associations and regional preferences. Other color variants, including cobalt blue and specialty tints, serve niche applications in luxury packaging and artisanal products where a distinctive appearance creates brand differentiation. The color segmentation reflects broader market trends toward premiumization and product differentiation, with specialized glass formulations commanding higher margins while serving specific functional requirements that alternative materials cannot replicate effectively.

Geography Analysis

Belgium's container glass market operates within a highly integrated European context where domestic production serves both local consumption and export opportunities across EU member states. The country's strategic location provides efficient access to major European markets, with established trade relationships facilitating cross-border glass-packaging flows that optimize production-capacity utilization beyond domestic demand limits. Belgium's well-developed logistics infrastructure, anchored by the Port of Antwerp and comprehensive rail networks, enables cost-effective distribution to neighboring markets, including Germany, France, and the Netherlands.

The domestic market benefits from stable consumption patterns driven by established beverage preferences, growing pharmaceutical-sector demand, and tourism-related hospitality consumption that creates seasonal demand fluctuations requiring flexible supply-chain management. Regional production capacity concentrates in Flanders, where major facilities like Ciner Glass Belgium's EUR 504 million (USD 567 million) Lommel investment demonstrate confidence in long-term market fundamentals and export potential. The Wallonia region contributes through specialized glass-manufacturing capabilities and proximity to French markets that facilitate cross-border trade relationships.

Brussels serves as a consumption center where hospitality-sector demand drives beverage glass-packaging requirements, while regulatory and administrative functions influence policy development affecting the broader glass-packaging industry. Belgium's EU membership provides regulatory advantages through harmonized packaging standards and environmental requirements that create competitive benefits for producers already compliant with stringent sustainability criteria. Export opportunities expand through EU market-integration initiatives that reduce trade barriers and standardize quality requirements across member states.

Competitive Landscape

Belgium's container glass market exhibits moderate concentration with established players leveraging technological capabilities and strategic positioning to maintain market share against both domestic competition and import pressure from neighboring EU producers. The competitive environment favors companies with integrated operations spanning raw-material sourcing, manufacturing efficiency, and customer-relationship management, as evidenced by major capacity investments like Ciner Glass Belgium's EUR 504 million (USD 567 million) facility expansion that signals a long-term commitment to market leadership.

Strategic patterns emphasize sustainability initiatives, energy-efficiency improvements, and specialized-product development that create differentiation beyond pure cost competition. White-space opportunities emerge in pharmaceutical packaging applications where regulatory requirements and technical specifications create barriers to entry that protect margin structures from commodity competition. Advanced glass formulations for cosmetics and personal-care applications represent another growth vector where Belgian manufacturers can leverage proximity to European luxury brands and specialized manufacturing capabilities.

Technology adoption focuses on energy-efficiency improvements, automated production systems, and digital-monitoring capabilities that reduce operational costs while improving quality consistency. Emerging disruptors include alternative packaging materials that compete on cost and convenience factors, requiring glass manufacturers to continuously justify premium positioning through superior performance characteristics and sustainability credentials.[3]Source: Fost Plus, “About Fost Plus,” fostplus.be

Belgium Container Glass Industry Leaders

Gerresheimer AG

SAVERGLASS Group

Konings plc

Bormioli Rocco

AXA GLASS bv/srl

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ciner Glass Belgium commenced construction of its EUR 504 million (USD 567 million) container-glass facility in Lommel, representing one of Europe's largest glass-manufacturing investments in recent years.

- April 2025: SCR-Sibelco completed its acquisition of Strategic Materials Inc., strengthening its position in recycled-glass supply chains that serve Belgium's container-glass manufacturers.

- March 2025: Belgium implemented enhanced deposit-return-system regulations for beverage containers, aligning with EU directives requiring 90% collection rates by 2029.

- February 2025: Fost Plus reported Belgium's beverage-can collection rate reached 62% through selective collection systems.

Belgium Container Glass Market Report Scope

Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents. It is often chosen for products where purity, safety, and environmental sustainability are paramount concerns.

The Belgium container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How big is the Belgium container glass market in 2026 and where is it headed by 2031?

Volume stands at 845.69 thousand tons in 2026 and is projected to reach 921.08 thousand tons by 2031, reflecting steady expansion.

What compound annual growth rate is forecast for Belgium’s container glass segment?

The market is expected to advance at a 1.72% CAGR over the 2026-2031 period.

Which application holds the highest share of container glass demand in Belgium?

Amber’s 2.81% CAGR through 2031 is fueled by pharmaceutical and premium-beverage needs for light protection, whereas flint serves broader but slower-growing uses.

How are EU recycling directives influencing Belgian glass producers?

Mandatory deposit-return targets and higher recycled-content thresholds reward firms already operating within Belgium’s 97% glass-recycling ecosystem and spur investments in circular practices.

What threat do energy costs pose to Belgium’s glass manufacturers?

High and volatile power and gas prices elevate production expenses, pressuring margins and prompting investments in efficiency and alternative fuels such as hydrogen.

Page last updated on: