Beard Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

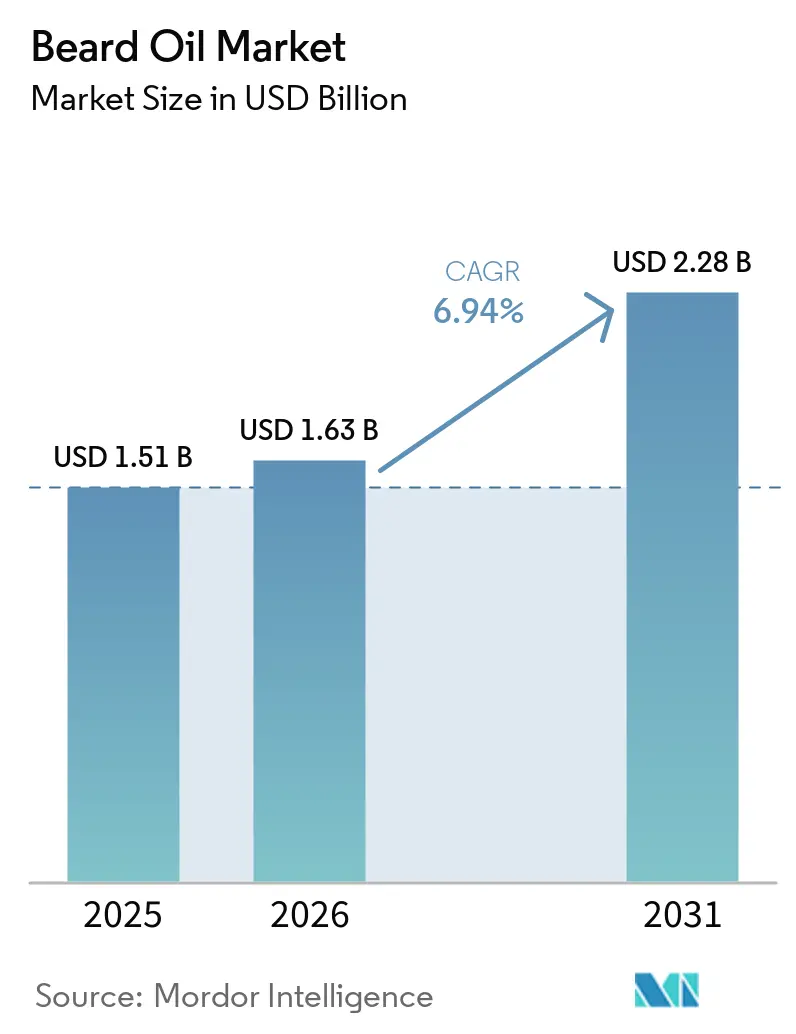

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.28 Billion |

| Growth Rate (2026 - 2031) | 6.94% CAGR |

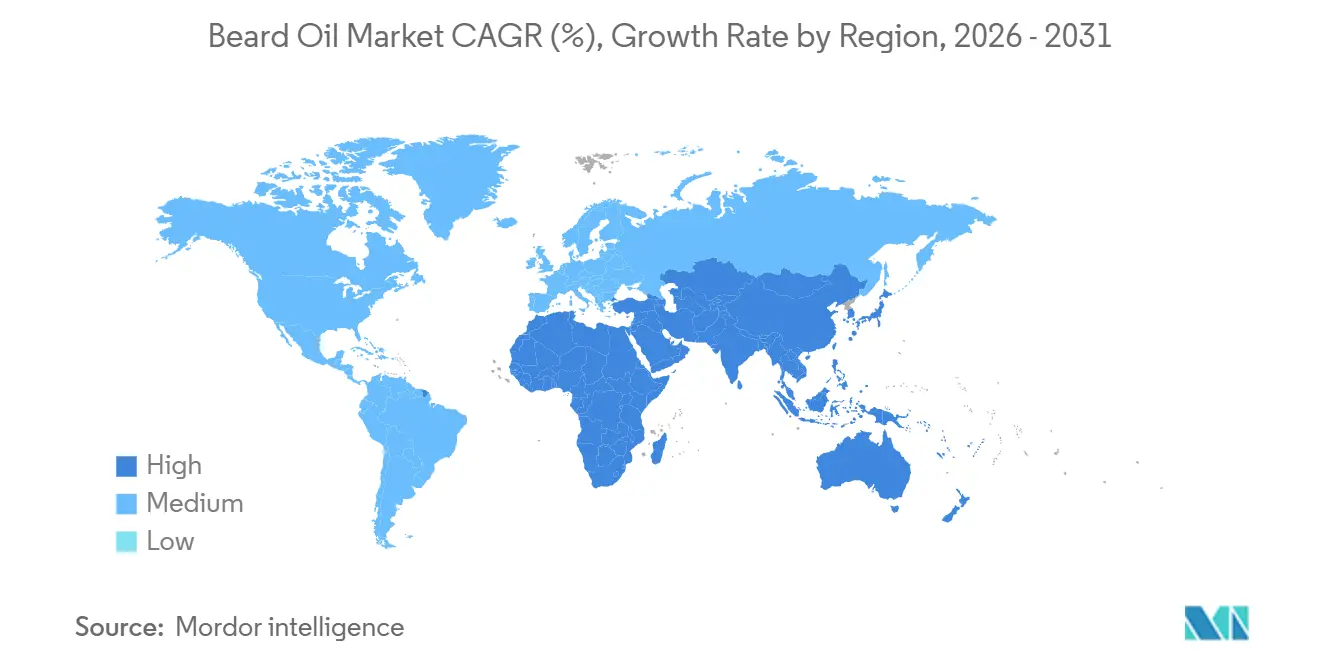

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Beard Oil Market Analysis by Mordor Intelligence

The beard oil market size is expected to grow from USD 1.51 billion in 2025 to USD 1.63 billion in 2026 and is forecast to reach USD 2.28 billion by 2031 at a 6.94% CAGR over 2026-2031. This growth trajectory is bolstered by the rising prominence of facial-hair aesthetics on social media, evolving male self-care routines, and the burgeoning direct-to-consumer (DTC) channels. Celebrity endorsements, like Dr. Squatch’s 2025 collaboration with Sydney Sweeney, have broadened the category's appeal, reaching audiences beyond just millennials. In a strategic move, major fast-moving consumer goods (FMCG) firms are acquiring DTC disruptors. This not only diversifies their innovation pipelines but also grants them access to invaluable first-party consumer data, effective viral-marketing strategies, and a premium market stance that's challenging for their legacy portfolios to achieve. However, the industry faces challenges: tightening global cosmetics regulations and climate-driven surges in prices for key oils like argan, coconut, and jojoba are squeezing gross margins. Yet, brands that lock in long-term contracts for these raw materials or pursue upstream vertical integration are reaping the rewards. Currently, the online channel holds a dominant 45.72% share of the beard oil market, consistently outpacing offline avenues, thanks to advantages like subscription models, targeted audience outreach, and seamless fulfillment.

Key Report Takeaways

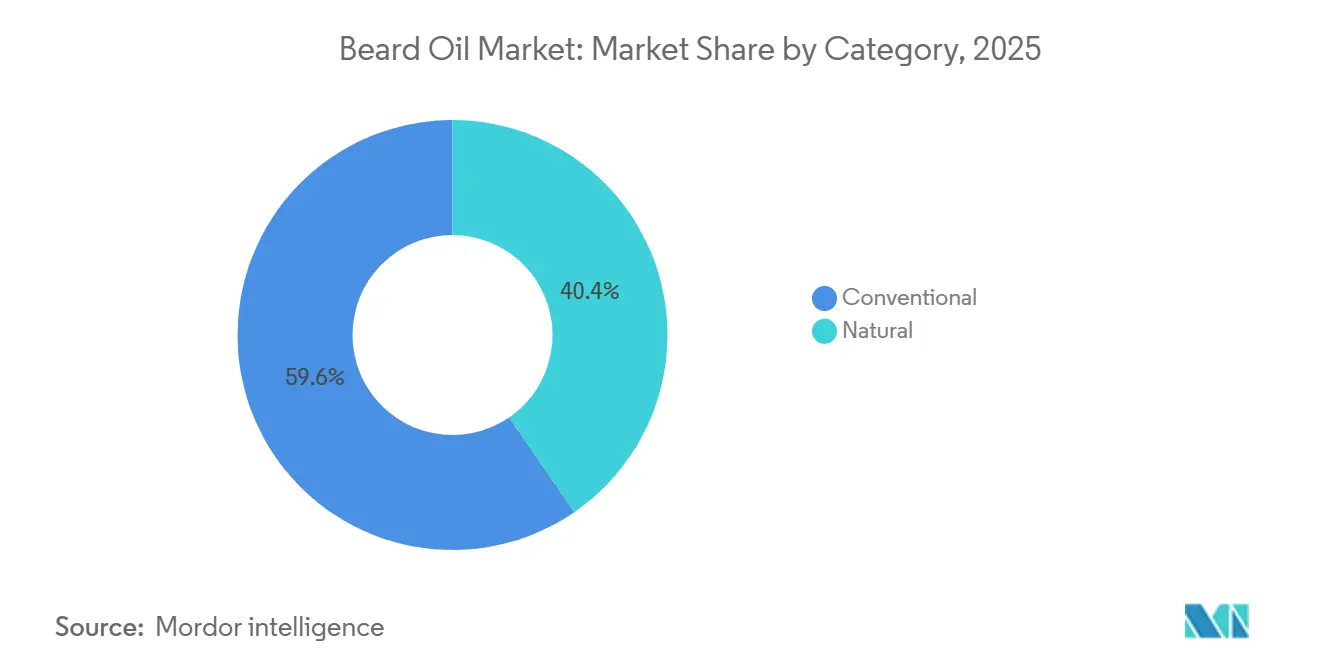

- By category, conventional formulations held 59.59% of the beard oil market share in 2025, whereas natural variants are forecast to grow at a 7.08% CAGR over 2026-2031.

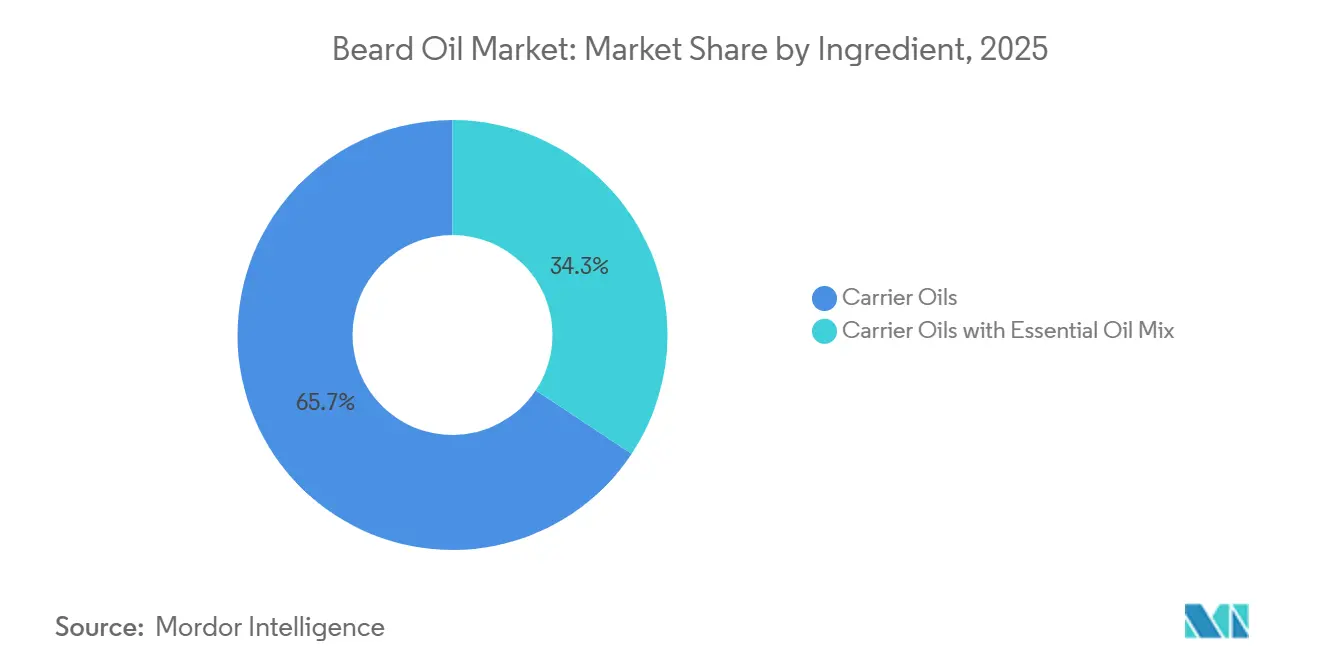

- By ingredient type, carrier oils captured 65.69% of the beard oil market share in 2025; carrier-plus-essential-oil blends are forecast to advance at a 7.67% CAGR to 2031.

- By distribution channel, online retail stores led with 45.72% of the beard oil market share in 2025, while health and beauty specialty stores are projected to expand at a 7.81% CAGR through 2031.

- By geography, North America commanded 35.40% of the beard oil market share in 2025, while Asia-Pacific is set to record the highest regional CAGR at 7.92% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Beard Oil Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising male grooming awareness | +1.2% | Global, with the strongest uptake in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Celebrity and social media-driven beard fashion trend | +0.9% | Global, particularly North America, Europe, urban centers in the Asia-Pacific, and Latin America | Short term (≤ 2 years) |

| Rapid growth of e-commerce grooming product sales | +1.5% | Global, led by North America, Europe, China, India, is accelerating in Southeast Asia and Latin America | Medium term (2-4 years) |

| Shift toward natural and organic formulations | +1.1% | North America, Western Europe, Australia; emerging in urban Asia-Pacific and affluent Middle East markets | Long term (≥ 4 years) |

| Direct-to-consumer micro-brand subscription models | +0.8% | North America, Europe, urban Asia-Pacific; nascent in Latin America and the Middle East | Medium term (2-4 years) |

| Demand for halal-certified beard oils in Muslim-majority markets | +0.7% | Middle East (UAE, Saudi Arabia, Egypt), South Asia (India, Pakistan, Bangladesh), Southeast Asia (Indonesia, Malaysia), Nigeria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Celebrity and Social Media-Driven Beard Fashion Trend

Beard fashion, once a niche aesthetic, has surged into the mainstream, thanks to celebrity endorsements and viral social media campaigns. In Q4 2025, Viking Revolution harnessed the power of TikTok, rolling out 18,000 creator videos and raking in a notable USD 1.5 million in sales via TikTok Shop[1]Source: Cosmetics Business, “TikTok Shop Sparks USD 1.5 Million Sales for Viking Revolution,” cosmeticsbusiness.com. This underscores the platform's prowess in driving both discovery and sales for grooming products. Dr. Squatch's strategic partnerships with icons like Sydney Sweeney and brands such as SpongeBob SquarePants and Call of Duty highlight the potency of pop-culture collaborations in broadening market reach, extending well beyond the conventional male grooming audience. Meanwhile, social-first marketing is leveling the playing field: micro-brands are now challenging FMCG behemoths by cultivating genuine communities and harnessing user-generated content, which often strikes a more resonant chord than traditional TV advertisements. This evolving landscape is also influencing product development: brands are unveiling limited-edition scents, teaming up with influencers for unique blends, and employing social listening to pinpoint and address unmet consumer needs. Scotch Porter, with a remarkable growth rate surpassing 70% annually, attributes its success to a keen focus on multicultural grooming demands and strategic alliances with Black influencers, effectively carving out a unique space in a saturated market.

Rapid Growth of E-Commerce Grooming Product Sales

Subscription models, tailored recommendations, and the ease of home delivery have propelled e-commerce to the forefront of beard oil sales. In 2025, online retail stores commanded a 45.72% share of the market, a lead they are poised to retain as digital-first brands expand and traditional retailers bolster their omnichannel strategies. Direct-to-consumer subscription models not only ensure steady revenue but also enhance customer lifetime value. For instance, Beardbrand, after revamping its fulfillment and manufacturing processes, surged its subscriber count from 1,500 to 11,000 in 2025, bouncing back to profitability after a challenging 2023-2024[2]Source: Cosmetics Business, “TikTok Shop Sparks USD 1.5 Million Sales for Viking Revolution,” cosmeticsbusiness.com. In China's bustling male grooming e-commerce scene, Douyin (the Chinese equivalent of TikTok) claimed 32.9% of online beard care sales, while Tmall secured 34.8% in the first half of 2025. This shift to e-commerce is paving the way for precision marketing: brands can now tailor offerings based on beard type, skin sensitivity, and scent preference, delivering customized product bundles and content that outperform traditional retail in conversion rates.

Shift Toward Natural and Organic Formulations

Across the beard oil category, formulation strategies are evolving in response to rising consumer demand for clean-label, organic, and sustainably sourced ingredients. Natural variants are set to outpace conventional products, with a projected growth rate of 7.08% CAGR through 2031. This shift comes as consumers increasingly scrutinize ingredient lists, seeking transparency in sourcing and processing. Brands are capitalizing on certifications from Ecocert and ETKO, using them to spotlight premium SKUs, especially with COSMOS-certified organic carrier oils like jojoba, argan, and castor, all boasting 100% organic purity. In February 2025, Beardbrand rolled out an organic beard oil line, specifically designed for the humid and hot climates of Indonesia and Vietnam, emphasizing lighter, fast-absorbing formulations. Regulatory pressures are amplifying the move towards natural formulations. The EU's broadened allergen disclosure mandates, coupled with the FDA's MoCRA framework, are nudging brands away from synthetic fragrances and preservatives, which often lead to compliance challenges. In February 2025, Beard Beasts introduced an eco-luxury collection, spotlighting hemp beard growth oil and bamboo combs, underscoring sustainability as a premium feature rather than an added cost. Brands with vertically integrated supply chains or enduring partnerships with organic farms stand to benefit most from this trend, especially given the potential margin erosion from spot-market volatility in premium carrier oils.

Demand for Halal-Certified Beard Oils in Muslim-Majority Markets

In Muslim-majority regions, halal certification is increasingly seen as essential for market access, with consumers seeking assurance that grooming products align with Islamic dietary and ethical standards. Brands like Halal Essentials by Biyah, Indus Valley, Tayyib Tree, WASIMI, and Kahf have introduced halal-certified beard oils, focusing on markets in the Middle East, South Asia, and Southeast Asia. These regions are witnessing a faster growth rate for halal cosmetics compared to their conventional counterparts. Third-party validation from certification bodies like JAKIM in Malaysia, the Halal Food Authority in the UK, and MUI in Indonesia ensures that ingredients, processing, and supply chains adhere to halal standards. This not only alleviates consumer skepticism but also allows for premium pricing. Marico's international division, which encompasses Beardo, recorded a 27% growth in the Middle East and North Africa for FY25, partly fueled by its halal-compliant product offerings. The appeal of halal certification transcends religious boundaries; it also denotes attributes like clean-label, cruelty-free, and ethically sourced, resonating with a wider audience. In 2025, Viking Revolution made its international foray into Saudi Arabia and India, introducing halal-certified SKUs. They acknowledged that such certification paves the way for distribution in modern trade channels and e-commerce platforms that emphasize compliance.

Restraints Impact Analysis of Beard Oil Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution threat from multifunctional beard balms and serums | -0.6% | Global, particularly in North America and Europe, where multifunctional products have gained traction | Short term (≤ 2 years) |

| Price sensitivity in developing regions | -0.4% | Asia-Pacific (excluding Japan, Australia), Latin America, Sub-Saharan Africa, parts of the Middle East | Medium term (2-4 years) |

| Allergic reactions triggering stricter essential-oil regulations | -0.3% | Europe (EU Regulation 2023/1545), North America (FDA MoCRA), Australia; spillover to export markets | Long term (≥ 4 years) |

| Climate-induced supply volatility for premium carrier oils | -0.5% | Global, with acute impact in Morocco (argan), the Philippines and Indonesia (coconut), Mediterranean (jojoba) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Substitution Threat from Multifunctional Beard Balms and Serums

Time-constrained consumers are increasingly gravitating towards multifunctional grooming products that seamlessly blend conditioning, styling, and skincare benefits, sidelining traditional single-purpose beard oils. The U.S. beard balm market is witnessing a notable upswing, with surveys revealing a clear preference among male grooming enthusiasts for multifunctional products. These products streamline routines by reducing the number of SKUs. Furthermore, 35% of consumers are leaning towards lightweight textures, spurring innovation in water-based hybrid balms that deliver oil-like conditioning without the added weight. Beard serums, known for their concentrated active ingredients like biotin, caffeine, and peptides, are emerging as performance-driven alternatives to conventional carrier-oil blends. This shift is particularly pronounced in mature markets, where consumers, having embraced basic beard care, are now opting for premium, efficacy-focused products. To navigate this evolving landscape, brands can bundle oils with complementary items like balms and washes in subscription boxes or reformulate oils to incorporate functional actives, enhancing their standalone appeal. Highlighting this trend, BIC's February 2026 debut of the Flex 5 Trim and Shave, a versatile 2-in-1 tool, underscores the growing consumer demand for consolidated, multi-use solutions.

Climate-Induced Supply Volatility for Premium Carrier Oils

Climate change is disrupting the supply of premium carrier oils, driving price volatility, and forcing brands to diversify sourcing or reformulate products. Morocco's prolonged drought has reduced argan forest coverage, and argan oil prices surged, compressing margins for brands that rely on this ingredient as a hero component. Coconut oil, a staple carrier oil, faced supply shocks in 2025 as exports from the Philippines and Indonesia, the world's top producers, fell 15.3% and 19% respectively during January-November, pushing spot prices up 35-45% and peaking at USD 2,742 per metric ton in August 2025. Jojoba cultivation in the Mediterranean and southwestern United States is also vulnerable to water scarcity and temperature extremes. Brands are responding by securing long-term supply contracts, investing in regenerative agriculture partnerships, and exploring alternative carrier oils such as baobab, marula, and hemp seed that offer similar performance with more resilient supply chains. The volatility also accelerates the shift toward synthetic or bio-fermented alternatives, though consumer acceptance of these ingredients remains mixed in the natural-formulation segment. Companies that vertically integrate or establish strategic partnerships with cooperatives, such as argan cooperatives in Morocco, can mitigate supply risk and lock in cost advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Beard Oil Market Segment Analysis

By Category:

Natural Variants Drive Premium MigrationIn 2025, conventional beard oil formats command a dominant 59.59% share of the market revenue. Their stronghold is attributed to widespread consumer familiarity, prime shelf placements, and competitive pricing, making them the preferred choice for newcomers. Bolstered by a stable supply chain and decades of demonstrated effectiveness, these products have cultivated deep consumer trust, solidifying their pivotal role in daily grooming. Despite intensifying competition, the reliability of conventional oils ensures their continued prominence. Many users, especially in budget-sensitive markets, are drawn to these formulations for their affordability and consistent performance. Thus, conventional beard oils stand as the cornerstone of the segment, integral to the grooming rituals of many.

Natural beard oil products are emerging as the fastest-growing segment in the category, boasting a projected CAGR of 7.08%. This surge is fueled by a rising consumer appetite for clean-label and eco-friendly choices. Shoppers, ready to invest more, link organic certifications with safer, sustainably sourced ingredients. Brands spotlighting transparent sourcing, ethical ingredient choices, and eco-friendly packaging are reaping the rewards of this trend. Moreover, natural beard oils are poised to chip away at the market share of traditional products, nudging established brands towards reformulation and innovation. As the beauty industry increasingly embraces sustainability and health, established brands are reshaping their portfolios to align with today's discerning, ingredient-savvy consumers. Meanwhile, regulatory shifts are easing the path for natural products, offering them lenient scrutiny and straightforward labeling. In contrast, traditional formulations grapple with heightened mandates, facing stricter allergen disclosures and rigorous safety testing requirements[3]Source:United States Food and Drug Administration," Guidance for Industry: Registration and Listing of Cosmetic Product Facilities and Products", www.fda.gov.

By Ingredient:

Essential Oil Blends Gain SophisticationIn 2025, carrier oils like jojoba and argan dominate the beard oil market, holding a substantial 65.69% share. Their emollient properties closely resemble natural sebum, effectively alleviating common beard issues such as itchiness and flaking. Valued for their moisturizing benefits, these oils play a crucial role in maintaining skin and hair health, solidifying their importance in most formulations. The trustworthiness and familiarity of these ingredients bolster their leading market position. Furthermore, sourcing practices that prioritize quality and ethical production, like cold-pressed Moroccan argan sourced from women's cooperatives, infuse compelling narratives that resonate with consumers. Such stories not only elevate brand allure but also strengthen consumer confidence in product authenticity.

Blended beard oils, which incorporate therapeutic essential oils like tea tree and cedarwood alongside carrier oils, are witnessing a robust growth rate of 7.67% CAGR. These blends not only provide benefits, like the antimicrobial properties of tea tree oil and the distinctive scent of cedarwood, but also cater to consumers desiring both effectiveness and a sensory experience. Yet, the addition of essential oils complicates quality control due to their susceptibility to oxidation and potential sensitivities in users. To navigate these hurdles, manufacturers are turning to micro-batch testing and thorough allergen panels, ensuring safety and consistency. In this rapidly expanding segment, differentiation hinges on transparent ingredient sourcing and traceability, bolstered by advancing digital platforms. As these multi-functional blends raise industry standards, brands that adeptly merge effectiveness, sensory allure, and responsible sourcing are poised for a competitive advantage.

By Distribution Channel:

Digital Transformation AcceleratesIn 2025, online retail captured a 45.72% share, nearly half of the global revenue in the beard oil market, thanks to its unmatched convenience and wide variety of SKUs. Consumers appreciate the ease of searching ingredient lists, reading peer reviews, and enjoying fast, often same-day, delivery options. These features align perfectly with the frequent replenishment cycle of grooming products. The digital platform's accessibility and vast product range cater to modern shoppers who prefer making quick, informed purchases from the comfort of their homes. Furthermore, online channels provide rich data insights, allowing brands to better understand and anticipate customer needs. As e-commerce technology continues to evolve, further streamlining the buyer's journey, the dominance of online retail in the beard oil market remains unchallenged.

Specialty store outlets, including barbershop boutiques, are emerging as the fastest-growing segment in the beard oil market, with projections indicating a 7.81% CAGR. These physical stores shine in offering tactile discovery and personalized product recommendations, fostering deeper consumer engagement and trust. Unlike their online counterparts, specialty stores provide sensory experiences, like scent testing and texture sampling, that are vital for premium grooming products. With the rise of omnichannel strategies, shoppers can effortlessly transition between the convenience of digital platforms and the hands-on evaluation in-store, boosting overall satisfaction. Brands are channeling investments into click-and-collect services, not only driving foot traffic to their brick-and-mortar locations but also gathering invaluable e-commerce customer data. This strategy blurs the lines of traditional channels, rewarding companies adept at creating a seamless, unified consumer experience across all platforms.

Geography Analysis

North America Beard Oil Market

In 2025, North America held a dominant 35.40% market share, driven by a deep-rooted grooming culture, a flurry of product launches, and robust disposable incomes. The U.S. led the regional turnover, capitalizing on celebrity endorsements and a vast retail network. Canada closely trailed, influenced by shared cultural cues and active cross-border e-commerce. Meanwhile, Mexico, despite its smaller size, is witnessing growth as its middle class increasingly engages with influencer content, aspiring to refined grooming standards.

APAC Beard Oil Market

Asia-Pacific, with a rapid 7.92% CAGR, is drawing significant attention. In China and South Korea, beauty-centric digital platforms and livestream shopping are driving momentum. Urban millennials are particularly keen on beard oil supplements. Southeast Asian nations are contributing to the growth as cross-border platforms simplify access to imported brands. Additionally, the region's preference for localized scents and lighter textures, tailored for humid conditions, is gaining traction.

Europe Beard Oil Market

Europe's growth is steady but more measured, influenced by strict safety regulations and a consumer tilt towards certified natural products. Germany and the UK spearhead consumption, while France's rich perfume legacy champions scent-centric blends. Eastern European nations, starting from a modest base, are expanding as economic recovery and Western media exposure reshape male grooming views. Furthermore, the EU Cosmetics Regulation's harmonized standards set a benchmark, ensuring non-European exporters elevate their product quality to meet these thresholds.

Competitive Landscape

The beard oil market exhibits a moderate concentration. Global giants like Unilever, L’Oréal, and Procter & Gamble are actively pursuing acquisitions, with Unilever's notable USD 1.5 billion acquisition of Dr. Squatch in June 2025 highlighting this trend. These industry leaders leverage global distribution networks, robust research and development infrastructures, and marketing synergies across their diverse portfolios. Meanwhile, mid-sized brands such as Beardo and Viking Revolution carve out their niche by emphasizing authenticity, often utilizing direct-to-consumer subscription models to foster closer ties with their audience.

Technology has emerged as a level playing field in the industry. Startups are harnessing AI-driven skin diagnostics, QR codes for authenticity verification, and adaptive pricing strategies, mirroring the capabilities of established enterprises. As consumers increasingly prioritize ingredient transparency and sustainability, established players are spotlighting their responsibly sourced ingredients, be it jojoba or fair-trade argan. Collaborations with grooming influencers craft compelling brand stories, while partnerships with barbershops lend professional credibility. Thus, the competitive landscape is shaped as much by the authenticity of storytelling as by pricing strategies or distribution channels.

Looking ahead, there are untapped opportunities in emerging markets, formulations tailored for ethnic hair, and products suited for varying climates. While barriers to entry are relatively low, with manageable manufacturing scales and online setups, long-term success hinges on navigating regulatory landscapes, combating counterfeits, and staying attuned to the rapidly evolving preferences of consumers in the beard oil sector.

Beard Oil Industry Leaders

-

Marico Ltd

-

L’Oréal S.A.

-

Unilever PLC

-

Procter & Gamble Co.

-

Honest Amish LLC

- *Disclaimer: Major Players sorted in no particular order

Beard Oil Market Companies Covered in this Report

- L'Oreal S.A.

- Unilever PLC

- Procter & Gamble Co.

- Marico Limited (Beardo)

- Honest Amish LLC

- Viking Revolution LLC

- Edgewell Personal Care (Bulldog Skincare)

- Mountaineer Brand Products.

- Grave Before Shave

- Beardbrand Inc.

- Wild Willies (Manscape Labs)

- Bossman Brands Inc

- Zeus Beard LLC

- Seven Potions Ltd

- Scotch Porter LLC

- Reuzel USA, Inc.

- Beardilizer

- Murdock London Ltd

- Ranger Grooming Company

- Ludovico Martelli srl (Proraso)

Recent Industry Developments in Beard Oil Market

- March 2026: Procter & Gamble launched Bevel body cream, expanding the brand's portfolio beyond shaving and beard care into full-body grooming. This move signals P&G's intent to capture higher wallet share from multicultural consumers by offering a comprehensive personal-care ecosystem under the Bevel brand, which has built equity through targeted marketing and distribution in specialty retailers such as Ulta Beauty.

- February 2026: BIC unveiled the Flex 5 Trim and Shave, a 2-in-1 grooming tool combining a five-blade razor with an integrated trimmer, and announced a global rollout throughout 2026. The product addresses consumer demand for multifunctional solutions that reduce the number of SKUs in grooming routines, positioning BIC to compete with premium brands by offering convenience at a mass-market price point

- January 2026: Viking Revolution expanded distribution into 900 Walmart stores across the United States, marking a strategic shift from pure-play e-commerce to omnichannel retail. The brand generated USD 50 million in revenue in 2025 and leveraged TikTok Shop to achieve USD 1.5 million in sales, demonstrating how digitally native brands can scale into brick-and-mortar once they achieve critical mass online.

Global Beard Oil Market Report Scope

Beard oil is a grooming product designed to moisturize, soften, and nourish facial hair and the underlying skin. The global beard oil market is segmented by category, ingredient type, distribution channel, and geography. By category, the market is segmented into natural and conventional. By ingredient type, the market is segmented into carrier oils and carrier oils with essential oil mix. By distribution channel, the market is segmented into supermarkets/hypermarkets, health and beauty stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

Segmentation Overview

| Natural |

| Conventional |

| Carrier Oils |

| Carrier Oils with Essential Oil Mix |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Category | Natural | |

| Conventional | ||

| Ingredient | Carrier Oils | |

| Carrier Oils with Essential Oil Mix | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the beard oil market in 2031?

The beard oil market size is forecast to reach USD 2.28 billion by 2031, according to Mordor Intelligence.

How fast is the beard oil market projected to grow between 2026 and 2031?

The market is anticipated to expand at a 6.94% CAGR during the forecast period 2026-2031.

Which distribution channel leads global sales of beard oils?

Online retail held 45.72% of 2025 sales and is expected to retain leadership thanks to subscriptions and targeted marketing.

Why are natural beard oils gaining traction?

Natural variants appeal to health-conscious buyers, align with stricter allergen regulations, and are growing at a 7.08% CAGR, faster than conventional products.

Page last updated on: