Automotive Rear Seat Infotainment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

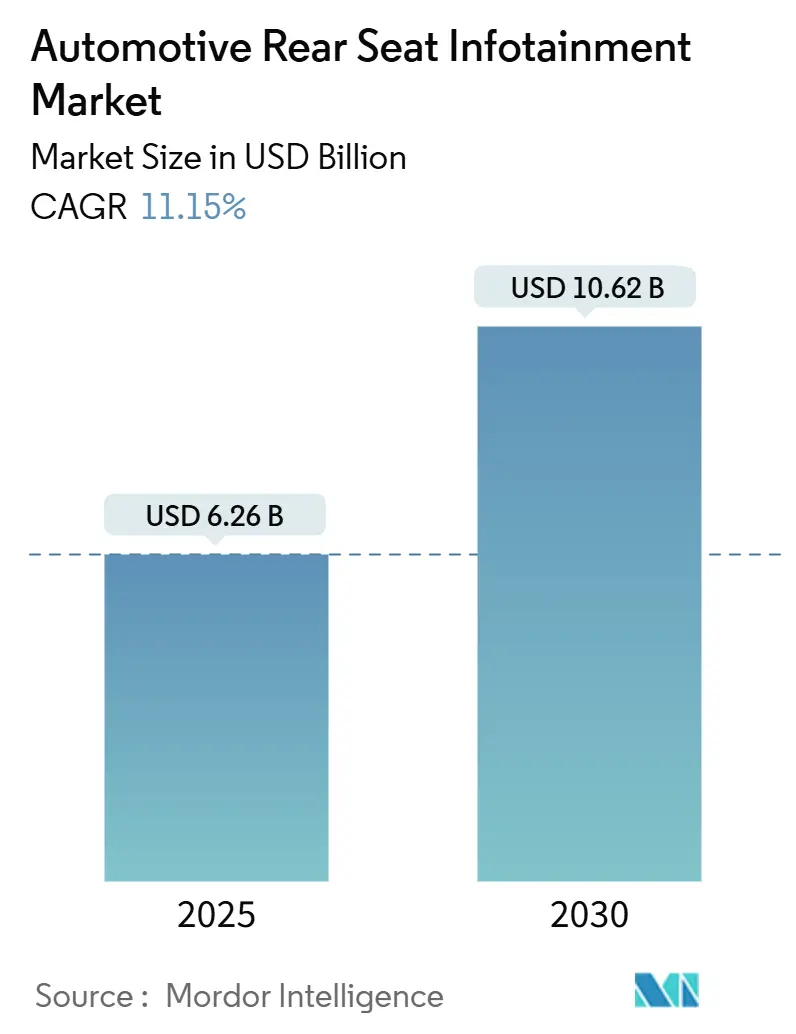

| Market Size (2025) | USD 6.26 Billion |

| Market Size (2030) | USD 10.62 Billion |

| Growth Rate (2025 - 2030) | 11.15% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

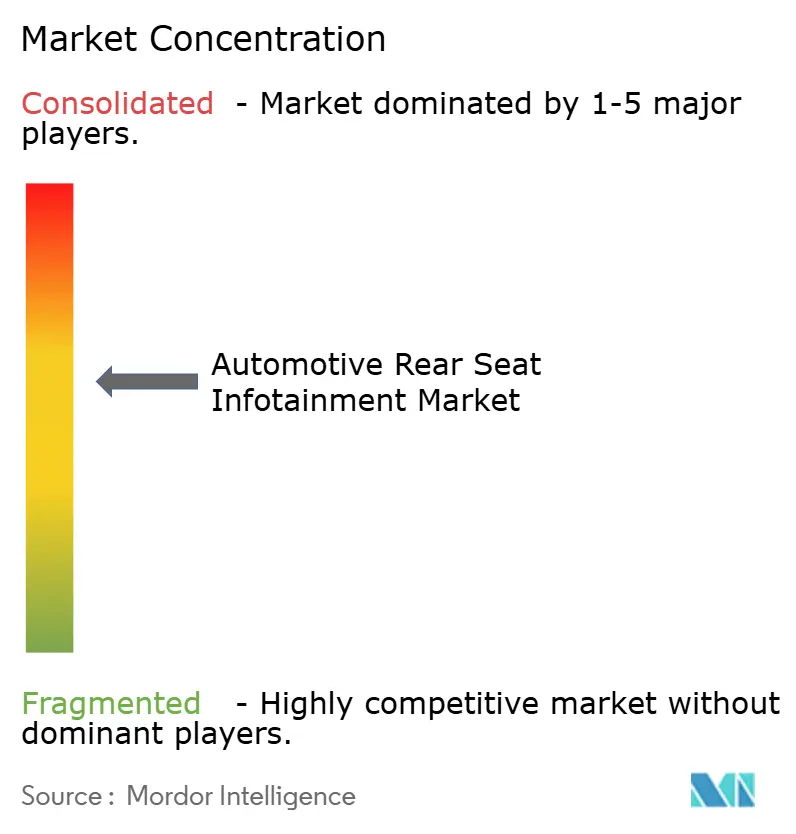

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Rear Seat Infotainment Market Analysis by Mordor Intelligence

The automotive rear seat infotainment market size stands at USD 6.26 billion in 2025 and is forecast to reach USD 10.62 billion by 2030, registering an 11.15% CAGR over the forecast period (2025-2030). This expansion highlights the evolution of in-vehicle entertainment, transitioning from basic audio playback to sophisticated software-defined platforms. These platforms now seamlessly integrate streaming video, gaming, smart-home features, and select vehicle-control functions. Rapid 5G rollouts, lower display and semiconductor costs, and rising consumer expectations for smartphone-style responsiveness inside the cabin reinforce demand across all vehicle classes. Automakers now view rear-seat systems as recurring-revenue engines, relying on over-the-air upgrades, content subscriptions, and targeted advertising. Competitive intensity is shifting from hardware differentiation toward full-stack solutions that merge displays, domain controllers, and cloud-connected operating systems.

Key Report Takeaways

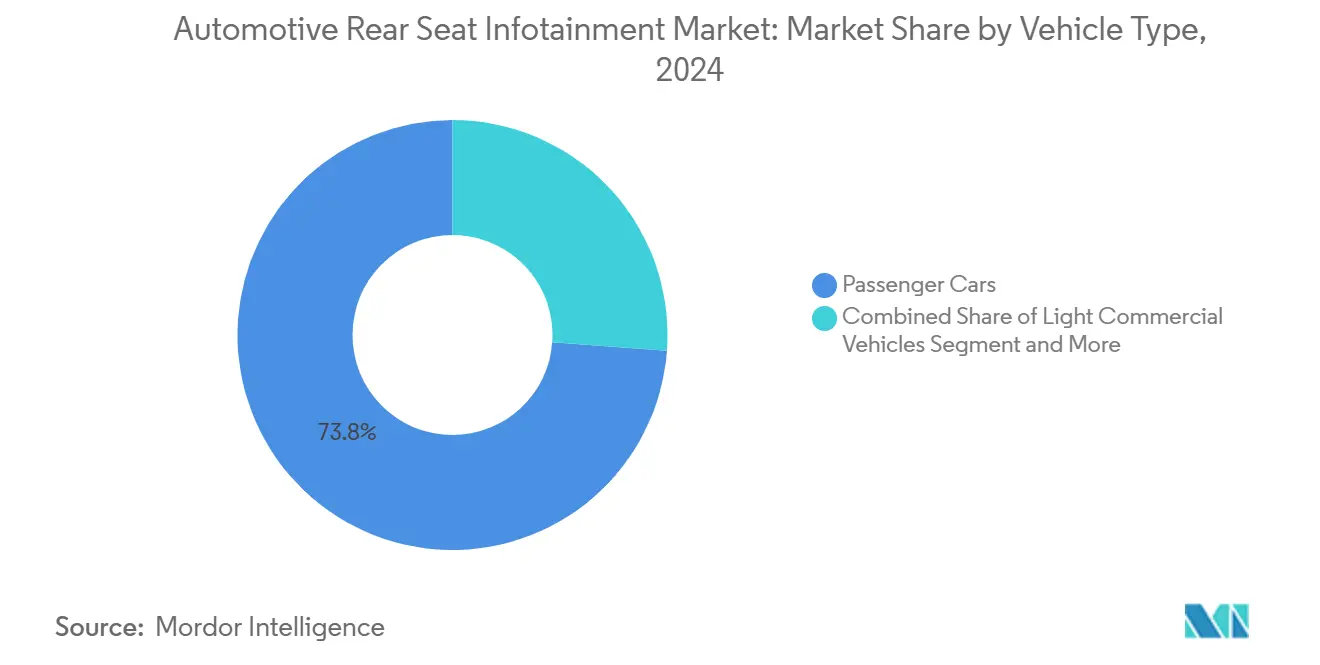

- By vehicle type, passenger cars led with a 73.84% share of the automotive rear seat infotainment market in 2024, and are projected to rise at a 24.96% CAGR during the forecast period (2025-2030).

- By component, display modules dominated the automotive rear seat infotainment market, with a 47.84% share in 2024; operating-system software and apps are forecasted to expand at a 13.97% CAGR during the forecast period (2025-2030).

- By propulsion type, internal-combustion vehicles retained a 64.48% share of the automotive rear seat infotainment market in 2024, whereas battery electric vehicles will post the quickest growth at 22.96% CAGR during the forecast period (2025-2030).

- By connectivity generation, 4G LTE accounted for a 60.32% share of the automotive rear seat infotainment market in 2024, while 5G connectivity is set to grow at a 26.85% CAGR during the forecast period (2025-2030).

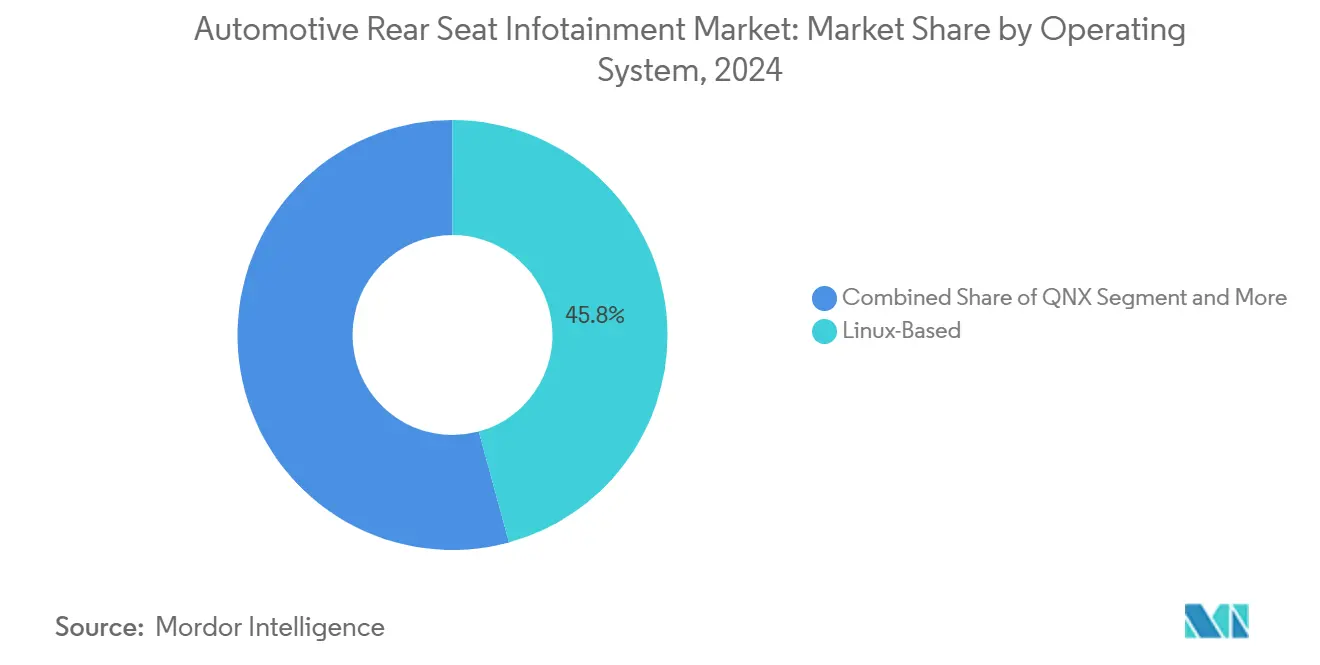

- By operating system, Linux-based platforms controlled a 45.76% share in 2024, and Android Automotive OS is projected to climb at a 13.62% CAGR during the forecast period (2025-2030).

- By sales channel, OEM-installed systems held an 86.32% share in 2024, while the aftermarket segment is poised for a 14.10% CAGR during the forecast period (2025-2030).

- By geography, Asia-Pacific captured the largest market share of 38.48% in 2024, while the Middle East and Africa are projected to be the fastest-growing regions, with a 14.25% CAGR during the forecast period (2025-2030).

Global Automotive Rear Seat Infotainment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Connected In-Car Entertainment | +2.8% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Rapid 5G/4G LTE Penetration | +2.6% | APAC core, spill-over to North America and EU | Short term (≤ 2 years) |

| Differentiation Through Rear-Seat Features | +2.1% | Global, concentrated in luxury segments | Medium term (2-4 years) |

| Display and Semiconductor ASPs | +1.9% | Global, with manufacturing cost benefits in APAC | Long term (≥ 4 years) |

| OTT and Cloud-Gaming Monetization | +1.7% | North America and EU early adoption, global expansion | Long term (≥ 4 years) |

| Ad-Supported Screens | +1.4% | North America and China pilot markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Consumer Demand for Connected In-Car Entertainment

Smartphone ubiquity shapes passenger expectations, making Wi-Fi-like speed, voice control, and app ecosystems baseline requirements. Stellantis models, equipped with SoundHound's on-device large-language model, demonstrate that the quality of conversations is approaching benchmarks set by smart speakers. Today, automakers are integrating AI voice assistants, enabling passengers to browse the web, manage cabin functions, and stream content, all without using their hands. Lucid’s “Lucid Assistant” demonstrates premium OEM emphasis on multilingual support, local processing for low latency, and privacy-centric design. As 5G coverage improves, rear-seat infotainment shifts from cache-and-play to true cloud services, paving the way for in-cabin e-commerce and immersive gaming. Continuous over-the-air upgrades keep features fresh, locking buyers into subscription bundles and boosting lifetime revenue per vehicle.

Rapid 5G/4G LTE Penetration Enabling HD Streaming

Dense 5G macro-cell and small-cell deployments in China, South Korea, and Japan deliver stable multi-gigabit links capable of running parallel video streams and telematics channels. Panasonic Automotive’s work with Qualcomm on Snapdragon Cockpit Elite integrates 5G modems, AI accelerators, and GPU resources into a single domain controller that can support independent display zones for each passenger[1]“Panasonic Automotive Systems and Qualcomm Expand Collaboration to Transform In-Vehicle Experiences with Snapdragon Cockpit Elite Platform,” Panasonic Automotive Systems Co., Ltd., panasonic.com. This architecture future-proofs infotainment by enabling software partitioning, lowering time-to-market for differentiated experiences. Early 5G coverage advantages in Asia-Pacific encourage content partnerships—Tencent Video, iQIYI, and Sony Pictures ink exclusive in-vehicle distribution deals—while North American carriers test dedicated network slices for automotive quality of service. HD streaming normalizes multi-screen setups even in compact vehicles, pushing display count and resolution higher.

OEM Differentiation Through Premium Rear-Seat Features

Luxury carmakers transform the second row into a lounge: retractable 4K OLED displays, active ambient lighting, and seat-embedded haptics turn commuting into leisure. Volvo's 2024 software update showcases the ability to enhance an existing fleet's UI with context-aware features without needing new hardware[2]“Volvo Announces Major Infotainment Upgrade for Millions of Vehicles,” Volvo Cars, volvocarsvilla.com. Mercedes-Benz’s MBUX updates blend cabin-control functions, climate, sunshades, massage, with entertainment on shared screens, signaling a shift to fully integrated user experiences. Ride-hail services pilot ad-supported infotainment, converting passenger dwell time into revenue, and corporate fleets equip limo-grade sedans as mobile offices with video-conferencing suites. As differentiators move from horsepower to user experience, rear-seat systems become pivotal in premium trims and influence vehicle pricing strategy.

Declining Display and Semiconductor ASPs

Smartphone panel overcapacity and mature 28 nm automotive SOC nodes drive double-digit annual component price erosion. High-brightness OLED yields improve, bringing 12–15 inch flexible displays into mainstream SUVs without premium mark-ups. Integrated domain-controller chips replace multiple ECUs, cutting wiring mass and boosting compute headroom for graphics and AI workloads. Suppliers bundle reference software with hardware to shorten integration time, exemplified by one-chip solutions that embed audio DSP, Bluetooth, Wi-Fi, and 5G. Price drops democratize features; mid-segment models in emerging markets now launch with dual 10 inch rear screens, blurring the line between mass and premium offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| System Integration Cost and Architectural Complexity | -1.8% | Global, particularly affecting smaller OEMs | Medium term (2-4 years) |

| Cybersecurity and Data-Privacy Concerns | -1.2% | EU and North America regulatory focus, global impact | Short term (≤ 2 years) |

| Driver-Distraction Homologation Rules | -0.9% | EU leading, North America following | Medium term (2-4 years) |

| OLED/QLED Panels and IC Shortage | -0.7% | Global supply chain, APAC manufacturing concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High System Integration Cost & Architectural Complexity

Moving from distributed ECUs to centralized domain controllers requires re-engineering of vehicle electrical architectures and imposes steep up-front investments in software tooling and validation labs. Smaller brands lacking in-house software cadres struggle to align with UNECE WP.29 cybersecurity mandates, pushing them toward costly third-party integrators. Middleware stacks such as BlackBerry QNX ease basic enablement yet still demand OEM-specific customization for branding, analytics, and connectivity back-ends. Complex supply chains for OLED panels and automotive SOCs magnify risk; a single foundry delay can halt an entire launch cycle. Over-the-air feature enablement helps amortize investments, but near-term capital outlay remains an adoption hurdle that tempers growth among resource-constrained automakers.

Rising Cybersecurity & Data-Privacy Concerns

As infotainment units interface with vehicle CAN and Ethernet backbones, attack surfaces multiply. EU regulators enforce whole-product-life cybersecurity management systems that extend years beyond production, requiring continuous patching and vulnerability disclosure. OEMs must also reconcile infotainment data capture with GDPR-level consent, complicating UI flows and backend architectures. White-hat demonstrations of display hijacking and remote microphone activation heighten public scrutiny, and insurers begin factoring cyber-risk premiums into fleet policies. Compliance demands frequent firmware updates, raising the specter of bricking vehicles if patch processes fail, so suppliers invest in resilient dual-partition storage and failsafe rollbacks. Security overhead adds cost and lengthens validation cycles, partially offsetting the margin gains from digital services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Remain the Revenue Anchor

Passenger cars commanded a 73.84% share of the automotive rear seat infotainment market in 2024 and are expected to register a CAGR of 24.96% during the forecast period (2025-2030), benefiting from scale economies that slash per-vehicle hardware costs and enable richer UX layers. Mainstream sedans and SUVs now debut with twin 10-inch displays and integrated voice assistants, narrowing the feature gap with luxury models. OEMs leverage immersive entertainment to compensate for charging downtime and showcase tech-forward brand positioning. The automotive rear seat infotainment market size for passenger cars is forecast to widen further as mid-segment EV launches accelerate.

Second-row demand in light commercial vans is rising as ride-hailing, shuttle, and last-mile delivery operators pursue advertising revenue and employee satisfaction. Medium and heavy trucks adopt restrained infotainment due to cost and safety priorities, though fleet buyers ask for connectivity that supports telematics and driver coaching. The Rivian-Volkswagen USD 5.8 billion software partnership signals convergence: code and cloud infrastructures developed for passenger EVs will flow into commercial platforms, compressing time-to-feature parity and expanding the automotive rear seat infotainment market across use cases.

By Component: Displays Dominate, Software Grows Fastest

Display modules represented a 47.84% share of the automotive rear seat infotainment market in 2024, anchored by consumer expectations for vibrant visuals and intuitive touch interaction. Larger, thinner, and higher-resolution panels migrate into mass-market trims, aided by OLED cost drops and shared production lines with tablets and laptops. At the same time, the automotive rear seat infotainment market share for operating-system software and apps is climbing fastest, riding a 13.97% CAGR during the forecast period (2025-2030), as automakers shift from one-off sales to lifetime digital services.

Domain controllers consolidate audio, video, and connectivity on a single board, reducing wiring and latency; head-unit vendors now bundle SDKs and reference apps, slashing OEM integration timelines. As systems become upgradable over the air, clients pay for optional app packs—gaming, edutainment, or live sports—unlocking new revenue streams that inflate the automotive rear seat infotainment market size tied to software layers. Suppliers who provide turnkey stacks that fuse hardware reliability with cloud agility are best positioned to capture value.

By Propulsion Type: Electrification Amplifies Experience-Centric Design

Internal-combustion models still held a 64.48% share of the automotive rear seat infotainment market in 2024, yet their growth lags electrified drivetrains that attract tech-savvy buyers. Battery electric platforms, unburdened by exhaust tunnels and mechanical linkages, free cabin volumes for larger screens and fold-out tables, are expected to grow at a 22.96% CAGR during the forecast period (2025-2030). The automotive rear seat infotainment market size linked to EVs also benefits from higher energy-efficient displays optimized for reduced power draw.

Hybrids act as a bridge, carrying over many high-end infotainment options while avoiding range anxiety, but incremental cost limits ultra-premium implementations. Waymo-equipped Hyundai IONIQ 5, an autonomous-ready EV, highlights the fusion of propulsion architecture with cabin entertainment. With no driver to engage, screen time during trips surges, boosting the market share of rear seat infotainment, especially from zero-emission vehicles.

By Connectivity Generation: 5G Enables Next-Gen Services

Legacy 4G LTE modems remained in a 60.32% share of the automotive rear seat infotainment market in 2024, sustaining existing telematics and streaming. Yet 5G’s expected to grow with a 26.85% CAGR during the forecast period (2025-2030), signals an inflection as carriers densify networks and slice capacity for automotive use. The automotive rear seat infotainment market size tied to 5G connectivity surges once sub-10 ms latency unlocks cloud gaming, holographic calls, and multi-camera social streaming.

Automakers plan staged rollouts: 5G hardware backfitting on 2025 facelifts, followed by 3GPP Release 18 features like AI network management. Variations in spectrum allocation mean Asia-Pacific pilots many premium services early, while rural North America relies on hybrid 4G/5G modules. Over time, the sunset of 2G/3G forces older head units off the network, stimulating aftermarket demand and supporting a parallel software-defined upgrade economy that expands the automotive rear seat infotainment market.

By Operating System: Open-Source Platforms Consolidate Power

Linux-based stacks, especially Android Automotive OS, delivered a 45.76% share of the automotive rear seat infotainment market in 2024 by offering a familiar UX and a robust developer pipeline. Android Automotive OS is expected to posts a 13.62% CAGR during the forecast period (2025-2030), integrating Google Play libraries and voice services that cut content-licensing friction. The automotive rear seat infotainment market share for proprietary RTOS solutions continues in safety-critical domains, yet pressure mounts as app ecosystems grow around open platforms.

Automotive Grade Linux garners backing from Japanese OEMs seeking neutrality, while QNX defends niches requiring ISO 26262 ASIL-D certification. Kia's launch of its AI Assistant underscores the pivotal role of OTA-centric platforms in hastening feature rollouts, thereby enhancing customer engagement and creating more upselling opportunities. Long term, subscription service revenue tied to OS-level controls will reinforce the automotive rear seat infotainment market size leadership of ecosystems that marry openness with robust security.

By Sales Channel: OEM Integration Tightens Grip

Factory-installed systems held an 86.32% share of the automotive rear seat infotainment market in 2024, reflecting close coupling with safety and powertrain networks that aftermarket kits rarely match. Regulatory demands around driver distraction and cyber-resilience further bias in favor of OEM-validated deployments. While the aftermarket is expected to posts a healthy 14.10% CAGR during the forecast period (2025-2030), its footprint centers on aging fleets in emerging economies and commercial vehicle segments where fleet operators seek specialized functionality and older passenger vehicles where owners desire modern connectivity features.

Integration complexity and safety regulations increasingly favor factory installation as infotainment systems integrate with vehicle safety systems, powertrain controls, and driver assistance features that require OEM validation and certification. Still, specialist installers carve niches, luxury shuttles, armored SUVs, where bespoke rear-seat solutions trump factory options. Overall, OEM dominance persists, underscoring their pivotal role in steering future growth of the automotive rear seat infotainment market.

Geography Analysis

Asia-Pacific retained a 38.48% share of the automotive rear seat infotainment market in 2024, owing to high vehicle output, competitive electronics clusters, and a tech-embracing middle class. Chinese automakers pack advanced displays and AI voice assistants into sub-USD 25,000 sedans, popularizing premium features at mass prices. Japanese and South Korean brands exploit domestic semiconductor ecosystems to refine integrated software-hardware stacks. Regional governments subsidize 5G rollouts and V2X corridors, supporting a 13.71% CAGR during the forecast period (2025-2030), reinforcing Asia-Pacific’s leadership position.

North America tallied a robust 10.81% CAGR as consumers pay premiums for in-cabin tech, and Silicon Valley partnerships deliver cutting-edge software. Tesla’s influence forces legacy OEMs to upgrade infotainment architectures rapidly, while subscription acceptance among U.S. drivers fuels revenue diversification. Canada’s tech workforce and Mexico’s assembly plants together form a vertically integrated supply chain that sustains competitiveness and enlarges the continent's automotive rear seat infotainment market size.

Europe posted a 9.31% CAGR amid stringent GDPR compliance that mandates secure data flows and robust consent management. German luxury marques pioneer rear-seat wellness suites with massage and AR overlays, while French and Italian brands experiment with low-cost Linux variants for compact cars. The Middle East & Africa outpaced all regions at 14.25% CAGR, led by Gulf states investing in smart-city mobility and premium SUVs that feature twin 12-inch entertainment displays. South America followed with 12.42% growth, propelled by urbanization and rising credit availability, making connected vehicles attainable.

Competitive Landscape

The automotive rear seat infotainment market exhibits moderate fragmentation, creating opportunities for specialized players while established leaders leverage scale advantages in component procurement and software development. Harman International leads, leveraging Samsung’s display IP to debut the world’s first Neo QLED 14-inch automotive screen in Tata’s Harrier.ev SUV[3]“HARMAN Launches Neo QLED Display for Tata Harrier.ev,” HARMAN Automotive, samsung.com. Panasonic Automotive capitalizes on joint SOC development with Qualcomm and long-standing relationships with Japanese OEMs.

Technology differentiation increasingly centers on AI-driven personalization, domain-controller consolidation, and cloud-managed content pipelines. Players with vertically integrated stacks, from panel hardware to app stores, command pricing power and cross-sell potential. Smaller specialists innovate in gesture control, 3D audio, and retrofit kits but face scale limitations, making them acquisition targets for larger Tier-1 suppliers.

Software capability now outweighs hardware pedigree; suppliers recruit cloud engineers and open satellite offices near tech hubs to secure talent. Compliance with UNECE WP.29 lifts entry barriers, while recurring revenue models reshape performance metrics from unit margins to lifetime ARPU. M&A activity is expected to intensify as companies race to secure AI algorithms, cybersecurity expertise, and global integration footprints.

Automotive Rear Seat Infotainment Industry Leaders

Harman International (Samsung)

Panasonic Automotive Systems

LG Electronics

Robert Bosch GmbH

Visteon Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tata Motors confirmed its forthcoming Sierra SUV will include fold-down tray tables, device chargers, and rear-seat entertainment screens.

- April 2025: Lenovo and Toyota Boshoku formed a partnership to co-develop intelligent cabin solutions, focusing on cross-device connectivity and advanced rear-seat entertainment.

- March 2025: Lexus India opened bookings for the LX 500d, which features dual 11.6-inch rear-seat touch displays, HDMI ports, and wireless remotes.

Global Automotive Rear Seat Infotainment Market Report Scope

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Display / Touch-screen Module |

| Head Unit / Domain Controller |

| Operating-System Software and Apps |

| Connectivity ICs and Antenna Modules |

| Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| 4G LTE |

| 5G |

| Legacy 2G/3G |

| Linux-Based (AAOS, AGL, etc.) |

| QNX |

| Android Automotive OS |

| Others (Proprietary, RTOS) |

| OEM-Installed |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Component | Display / Touch-screen Module | |

| Head Unit / Domain Controller | ||

| Operating-System Software and Apps | ||

| Connectivity ICs and Antenna Modules | ||

| By Propulsion Type | Internal-Combustion Engine Vehicles | |

| Hybrid Electric Vehicles | ||

| Battery Electric Vehicles | ||

| By Connectivity Generation | 4G LTE | |

| 5G | ||

| Legacy 2G/3G | ||

| By Operating System | Linux-Based (AAOS, AGL, etc.) | |

| QNX | ||

| Android Automotive OS | ||

| Others (Proprietary, RTOS) | ||

| By Sales Channel | OEM-Installed | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is demand for rear-seat entertainment expected to grow through 2030?

The automotive rear seat infotainment market is forecast to expand at 11.15% CAGR, lifting value from USD 6.26 billion in 2025 to USD 10.62 billion by 2030.

Which region will add the most new revenue over the next five years?

Asia-Pacific will account for the largest absolute revenue gain, supported by 13.71% CAGR and more than one-third of global shipments.

Why are battery electric vehicles important to rear-seat infotainment adoption?

BEVs post a 22.96% CAGR because longer charging stops and tech-savvy buyers encourage richer entertainment features, widening the segment’s addressable market.

What technology shift is most critical for future in-cabin experiences?

5G connectivity delivers sub-10 ms latency, enabling cloud gaming, multi-screen UHD streaming, and AI voice services that redefine rear-seat usage.

Is the aftermarket likely to overtake OEM-installed systems?

No, OEM-installed solutions will retain dominance, holding more than 80% share, as safety integration and over-the-air service models favor factory implementations.

Page last updated on: