United Kingdom Automotive Infotainment Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

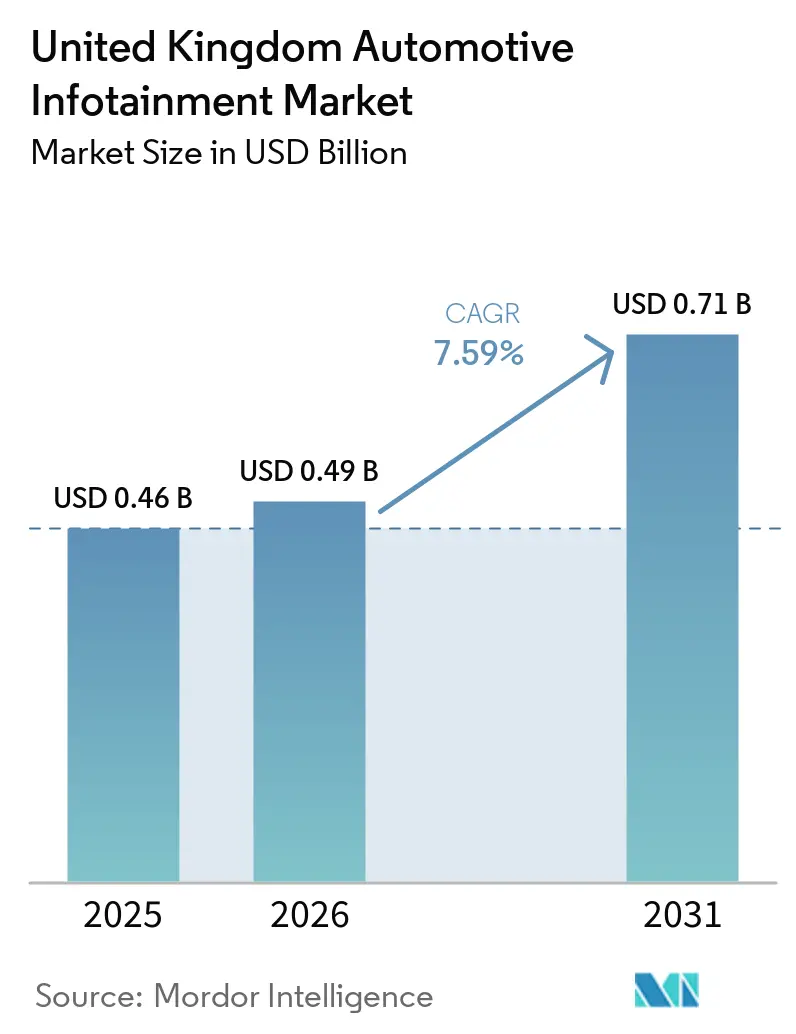

| Base Year Market Size (2025) | USD 0.46 Billion |

| Market Size (2026) | USD 0.49 Billion |

| Market Size (2031) | USD 0.71 Billion |

| Growth Rate (2026 - 2031) | 7.59% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Automotive Infotainment Market Analysis by Mordor Intelligence

The United Kingdom automotive infotainment market size was valued at USD 0.46 billion in 2025 and is expected to increase from USD 0.49 billion in 2026 to reach USD 0.71 billion by 2031, growing at a 7.59% CAGR over 2026-2031. Sustained battery-electric-vehicle (BEV) adoption keeps cockpit digital-content demand high, while the shift to centralized domain-controller architectures reduces wiring and enables frequent over-the-air feature updates. Ongoing nationwide 5G roll-out expands in-car bandwidth, opening the door for premium streaming, cloud gaming, and vehicle-to-everything services. Government financing under the DRIVE35 program directs capital toward electrification plants and digital infrastructure upgrades, reinforcing the country’s role as a testbed for software-defined vehicles. Competitive pressure intensifies as Chinese brands bundle advanced infotainment features into entry-level trims, pushing incumbents to accelerate software-centric strategies. Suppliers that vertically integrate key components mitigate chip cost volatility and shorten product qualification cycles.

Key Report Takeaways

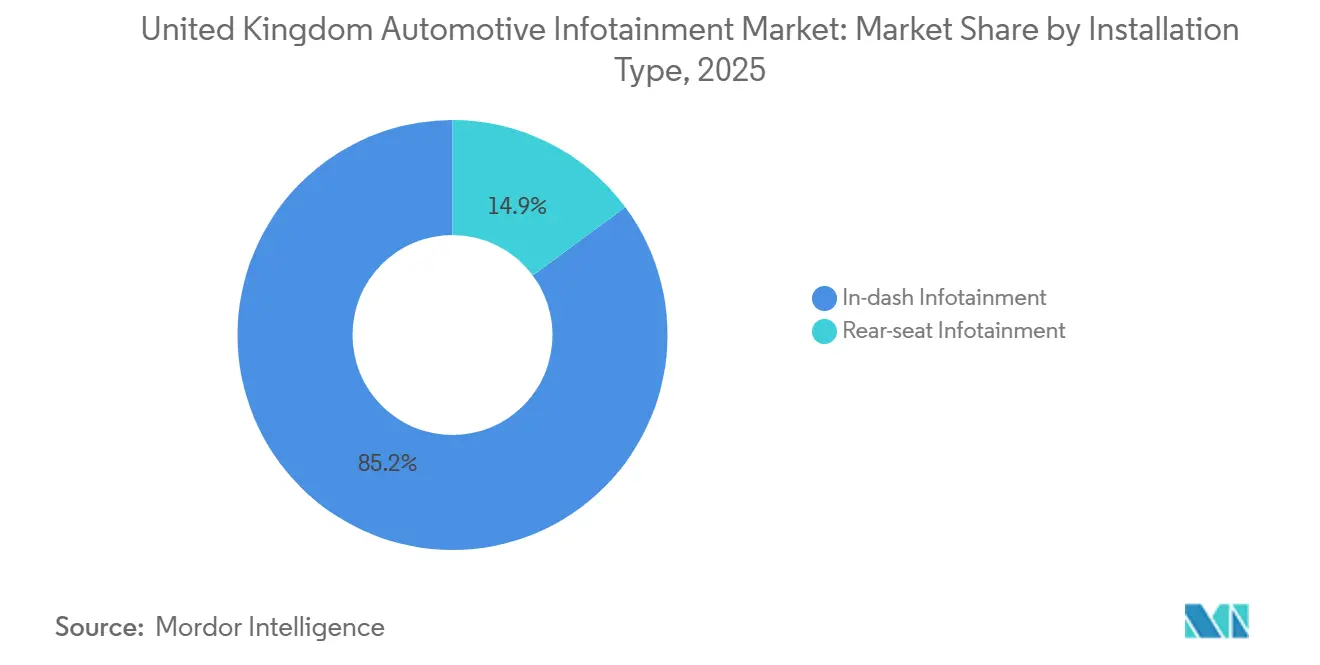

- By installation type, in-dash systems held 85.15% of the United Kingdom automotive infotainment market share in 2025; rear-seat systems are forecasted to expand at an 8.54% CAGR through 2031.

- By vehicle type, passenger cars led the United Kingdom automotive infotainment market with 67.13% market share in 2025 and are projected to grow at a 10.47% CAGR to 2031.

- By component, displays commanded a 45.25% share of the United Kingdom automotive infotainment market in 2025; operating-system software and apps are advancing at a 8.15% CAGR through 2031.

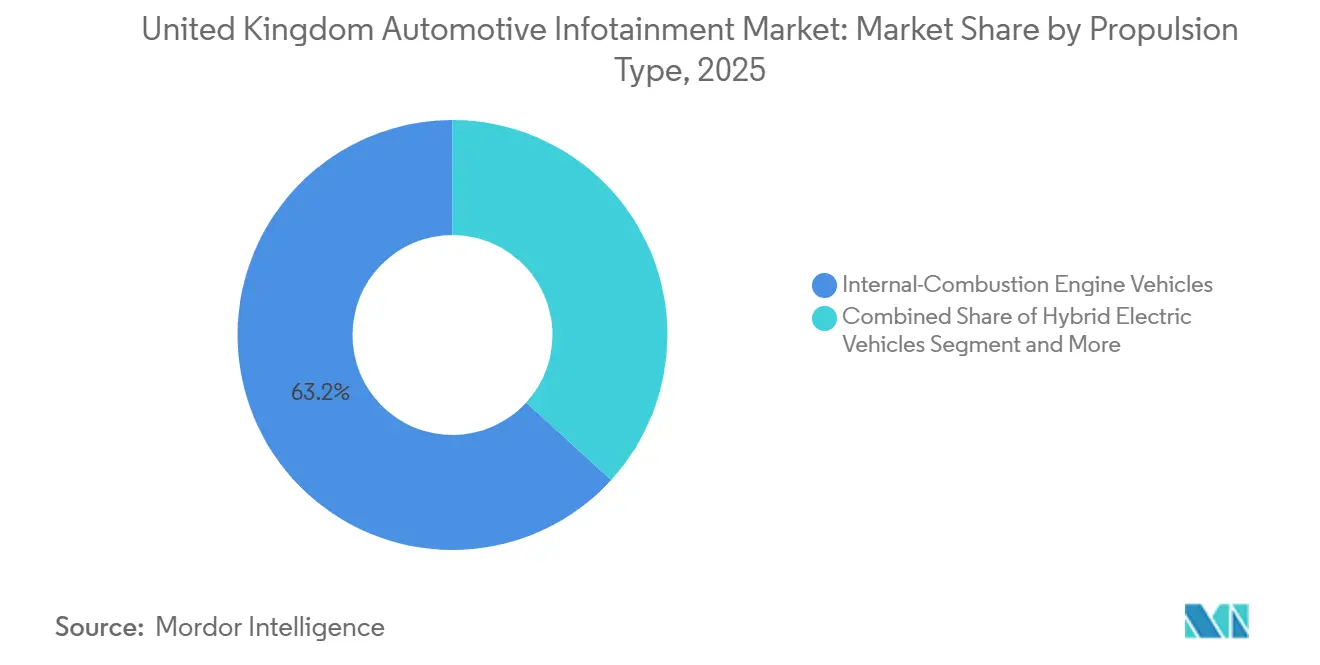

- By propulsion, internal-combustion engine vehicles accounted for 63.21% of the United Kingdom automotive infotainment market share in 2025, yet BEV infotainment content is rising at a 10.47% CAGR through 2031.

- By connectivity generation, 4G LTE dominated the United Kingdom automotive infotainment market with 72.06% market share in 2025, while 5G modules are expanding at a 9.22% CAGR through 2031.

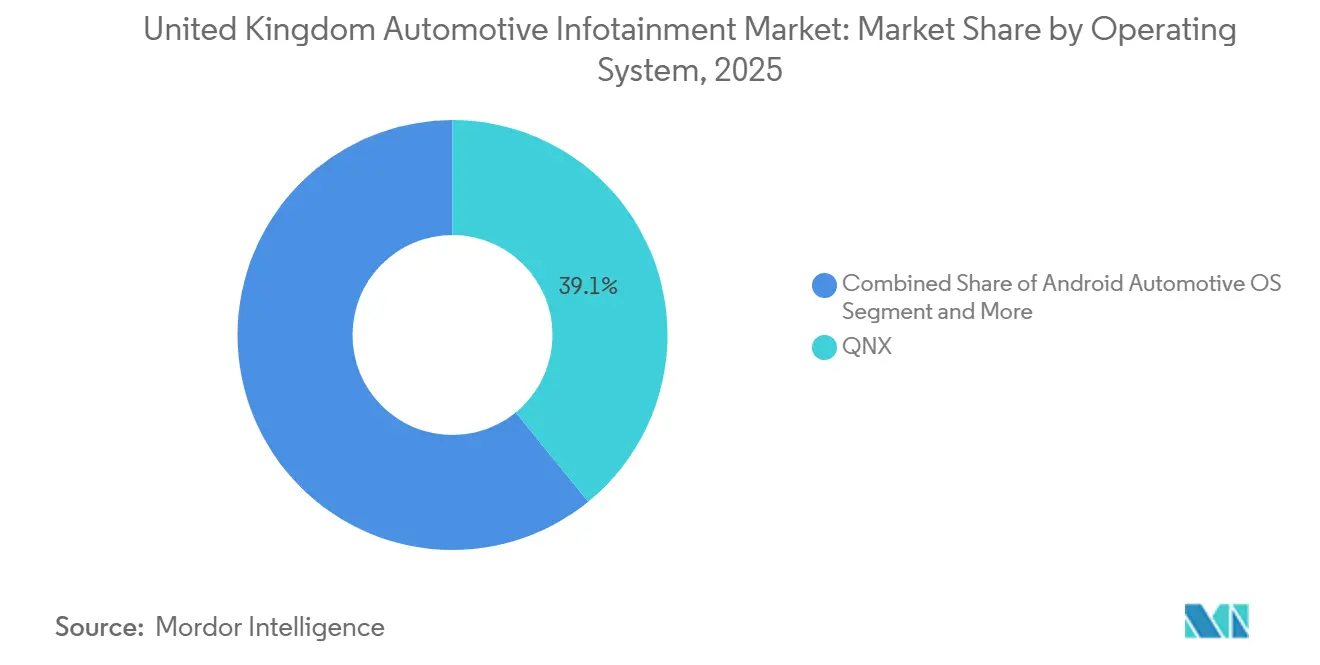

- By operating system, QNX held 39.12% of the United Kingdom automotive infotainment market share in 2025; Android Automotive OS is the fastest-growing, at a 9.77% CAGR through 2031.

- By sales channel, OEM-installed systems accounted for 79.34% of the United Kingdom automotive infotainment market share in 2025, but the aftermarket is increasing at an 8.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Automotive Infotainment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated EV Adoption Requires HMI | +2.1% | National | Medium term (2-4 years) |

| Connected-Car and Smartphone-Integrated Features | +1.8% | United Kingdom urban areas | Short term (≤ 2 years) |

| Nationwide 5G Roll-Out Enables Services | +1.5% | United Kingdom-wide | Medium term (2-4 years) |

| Centralized Domain Controllers In Vehicles | +1.3% | National OEM plants | Long term (≥ 4 years) |

| Infotainment for Insurance Data Monetization | +0.9% | United Kingdom-wide | Short term (≤ 2 years) |

| Mobility as a Service Differentiation | +0.7% | Urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated EV Adoption Requiring Richer HMI Experiences

BEV registrations reached 473,348 units in 2025, equal to 23.4% of new-car sales, and early-2026 figures show continued momentum despite tapering incentives[1]"EV market stats 2026," Zapmap, www.zapmap.com. Buyers of emission-free models expect wider OLED panels, augmented-reality navigation, and voice assistants that schedule charging, so OEMs invest in display innovation and software ecosystems. Centralized electrical architectures free cabin space for pillar-to-pillar screens, while over-the-air updates create durable revenue streams. Government funding accelerates charging-network integration, giving suppliers a clear commercial path. The positive feedback loop between BEV uptake and cockpit content sustains double-digit growth for this sub-segment.

Rising Demand for Connected-Car and Smartphone-Integrated Features

Consumers want seamless handoffs between phones and dashboards, driving the adoption of automaker-curated app stores. Regulators, however, link screen interaction to distracted-driving incidents, so suppliers integrate driver-monitoring cameras that dim displays when attention strays. Balancing convenience and compliance shapes the user interface roadmap and keeps connected-service adoption on a steady climb.

Nationwide 5G Roll-Out Enabling High-Bandwidth In-Car Services

Vodafone’s 80% coverage of the West Midlands Future Mobility testbed exemplifies low-latency infrastructure that supports cloud gaming and real-time mapping[2]"Vodafone 5G network enables first autonomous vehicle testing on UK public roads," Vodafone Limited, www.vodafone.co.uk. Automakers are standardizing 5G telematics control units to unlock subscriptions ranging from video streaming to pay-as-you-drive insurance. Ofcom’s spectrum-slicing pilots guarantee quality of service for safety-critical data paths. These upgrades shorten service-development cycles and encourage developers to build vehicle-native apps, accelerating near-term infotainment adoption.

Centralized Domain Controllers in Software-Defined Vehicles

Single-chip platforms that run infotainment, clusters, and driver-assistance software reduce wiring weight, lower costs, and simplify cybersecurity certification. European OEMs deploying such controllers can activate new functions remotely, converting one-time hardware sales into recurring digital revenue. The architecture also eases compliance with UN cybersecurity and update regulations, raising competitive barriers for low-volume players. Regional suppliers collaborating with local universities add further momentum to the trend.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost for Advanced Displays | -1.2% | National | Short term (≤ 2 years) |

| Regulations Limiting Visual UX | -0.8% | United Kingdom-wide | Short term (≤ 2 years) |

| Legacy Fleet Retrofit Complexity | -0.6% | Commercial fleets | Long term (≥ 4 years) |

| Escalating Cyber-Insurance Premiums | -0.4% | United Kingdom-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High BOM Cost for Advanced Displays and Processors

Sharp increases in memory and OLED panel pricing squeeze supplier margins just when OEMs seek cost offsets for batteries. Larger incumbents mitigate pressure through vertical integration and long-term supply contracts, yet smaller tier-twos risk program delays. Price volatility may temper near-term display-area expansion, slightly dampening growth expectations.

Driver-Distraction Regulations Limiting Visual UX

An updated 2022 U.K. rule subjects any misuse of an interactive device to fines and penalty points, and a 2026 consultation could mandate attention-warning systems. European distraction-warning standards are also influencing design choices. Suppliers must invest in gaze-tracking and simplified menus, adding costs while limiting creative differentiation. The restraint is moderate yet influential, especially in premium segments where large screens dominate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Installation Type: Rear-Seat Adoption Accelerates

In-dash systems held 85.15% of the United Kingdom automotive infotainment market share in 2025. Their dominance stems from being the primary human-machine interface, combining navigation, media, and driver-assistance cues in a single focal point. Carmakers refine these front-row displays with richer graphics, adaptive widgets, and voice-first controls to satisfy safety regulators and tech-savvy drivers. Suppliers collaborate with chipmakers and UI studios to reduce latency and deliver context-aware content that shifts seamlessly between the cluster and the center screen. Continuous over-the-air updates keep the interface up to date without requiring hardware swaps.

Rear-seat systems are expanding at an 8.54% CAGR through 2031, the fastest rate within the installation segment. Luxury brands and ride-hailing fleets view individual passenger screens as a differentiator that justifies premium fares. Electric-vehicle floor layouts free space for larger seat-back panels, while 5G connectivity lets each rider stream personalized content without buffering. Integrators are adding wireless-casting, multi-zone audio, and parental-control modes to broaden appeal beyond executive shuttles. The result is a virtuous circle in which rising service revenues encourage still more cabin-entertainment innovation.

By Vehicle Type: Passenger Cars Dominate

Passenger cars accounted for 67.13% of the United Kingdom automotive infotainment market share in 2025. Their large addressable base lets manufacturers amortize software-development costs across high volumes, encouraging feature-rich dashboards even in entry trims. Competitive pressure from new entrants pushes incumbents to shorten release cycles and integrate smartphone-style ecosystems. Consumers now expect intuitive voice assistants, seamless phone pairing, and cloud-synced preferences as standard equipment. These expectations elevate infotainment from a nice-to-have to a central purchase criterion.

The segment posts the fastest growth, advancing at a 10.47% CAGR through 2031. Silent powertrains spotlight cabin acoustics and screen clarity, so OEMs fit pillar-to-pillar OLED bars and augmented-reality navigation to heighten the sensory experience. Centralized electronic architectures simplify adding new apps that manage energy use or locate high-speed chargers. Regulators rewarding zero-emission fleets add momentum by aligning incentives with connected services rollouts. Together, these factors make BEV infotainment a bellwether for future design language.

By Component: Software Gains Momentum

Display modules accounted for 45.25% of the United Kingdom automotive infotainment market share in 2025, making them the largest single hardware component. Panel makers invest in thinner stacks and improved brightness to maintain leadership amid rising competition. Automotive stylists use these advances to create curved surfaces that blend clusters and center screens into unified glass cockpits. Adhesive and lamination suppliers, meanwhile, refine optical bonding techniques that reduce glare and enhance touch response. These collaborative gains reinforce the panel’s position at the heart of cockpit value creation.

Operating-system software and apps are climbing at an 8.15% CAGR, the fastest within the component mix. As business models tilt toward recurring revenue, OTA-delivered features become more lucrative than hardware margins. Carmakers curate branded app stores, bundling navigation, streaming, and diagnostics under subscription umbrellas. Developers target these storefronts because the installed base ensures predictable monetization. This symbiosis between platform owners and content providers shifts bargaining power toward software firms that can keep vehicles fresh over time.

By Propulsion Type: BEVs Spur Premium Cockpits

Internal-combustion models still anchor the fleet, accounting for 63.21% of the United Kingdom automotive infotainment market share in 2025, but they now compete with more digitally compelling alternatives. Their dashboards rely on proven ECUs and mature user-interface frameworks, which lowers development risk and preserves affordability. Suppliers serving this base focus on incremental improvements, such as faster boot times and broader voice-command vocabularies. They also retrofit connected services to extend the life of existing platforms. This pragmatic approach safeguards margins even as the market pivots toward electrification.

BEV infotainment shows the sharpest climb, mirroring the 10.47% CAGR recorded within passenger-car infotainment. Eliminating exhaust tunnels frees cabin real estate for panoramic displays and configurable ambient lighting, features that reinforce the vehicles’ tech-forward image. Software teams leverage the high-voltage backbone to power advanced GPUs and AI co-processors, enabling real-time route optimization that accounts for charging stops. Government grants for both charging networks and digital infrastructure nurture this ecosystem. Collectively, these levers cement BEVs as the showcase for next-gen cockpit experiences.

By Connectivity Generation: 5G Adoption Quickens

4G LTE retained a dominant 72.06% of the United Kingdom automotive infotainment market share in 2025 due to mature nationwide coverage. Automakers rely on its stable performance for mainstream telematics, remote diagnostics, and cloud-synced navigation. Suppliers optimize antenna arrays and carrier-aggregation techniques to extend 4G’s lifespan in cost-sensitive trims. Regulatory clarity around sunset timelines helps fleet managers plan hardware refresh cycles. This predictability keeps 4G entrenched even as faster links emerge.

The 5G segment is growing at a 9.22% CAGR, the swiftest among connectivity options. Low-latency uplinks support cloud gaming, high-definition video calls, and vehicle-to-everything safety messages. Network-slicing pilots ensure that lane-keeping and collision-avoidance packets remain prioritized, boosting OEM confidence. Content providers embrace the extra bandwidth to deliver immersive in-car experiences such as holographic navigation. As carriers densify coverage, premium and eventually mid-segment models will migrate to 5G by default.

By Operating System: Android Automotive OS Rises

QNX held the largest share at 39.12% of the United Kingdom automotive infotainment market in 2025, favored for its safety certification and deterministic behavior. Tier-ones embed it in mixed-criticality cockpits, where instrument clusters and driver-assistance modules coexist with entertainment systems. Integrators appreciate its long support cycles and mature toolchains, making it a conservative yet reliable choice. OEMs also benefit from a wide bench of engineers skilled in POSIX-compliant development. These attributes maintain QNX’s stronghold in safety-centric domains.

Android Automotive OS increases fastest at a 9.77% CAGR through 2031. Automakers prize its user-friendly developer portal and seamless tie-ins to Google services. Frequent OTA updates keep the UI fresh, while App-Store revenue shares sweeten the business case. Hypervisor layers let engineers sandbox safety functions, mitigating concerns about exposure to open-source code. As the ecosystem matures, more brands will dual-source or shift fully to Android for non-critical infotainment zones.

By Sales Channel: Aftermarket Momentum Builds

OEM-installed systems accounted for 79.34% of the United Kingdom automotive infotainment market share in 2025, underscoring manufacturers’ preference for tightly integrated solutions. Factory fit gives brands end-to-end control over user experience, data privacy, and warranty. Automakers leverage this control to bundle telematics, insurance, and content subscriptions at the point of sale. Extensive validation and compliance testing protect against liability, reinforcing consumer trust. As a result, factory channels remain the baseline for most new vehicles.

The aftermarket grows at an 8.95% CAGR, the fastest pace within sales channels. Fleet operators retrofit aging vans with 5G modems, larger screens, and usage-based insurance dongles to avoid full replacement. Reverse-engineering tools decode proprietary CAN messages, cutting installation time while preserving factory diagnostics. Retailers market plug-and-play kits that mirror smartphone interfaces, widening appeal among budget-minded drivers. These developments establish the aftermarket as a lively complement to factory distribution.

Geography Analysis

Midlands and North East clusters focused on centralized domain-controller manufacturing and AR head-up display pilots in partnership with regional academic labs. Government DRIVE35 grants funnel capital into plant retooling and local supply chains, cementing the region as a hub for the United Kingdom automotive infotainment market. High 5G penetration in the West Midlands enables real-world validation of low-latency services such as cloud-rendered graphics. London and the South East concentrate premium-vehicle demand, giving infotainment vendors an urban showroom for subscription-based features.

The market's growth is outlined by the North East’s pivot from combustion-engine production to battery and electronics assembly. Consistent BEV uptake, confirmed by 2025 registration data, underpins investment in large-format displays and centralized architectures. Rural Scotland and Wales lag in cellular coverage, so offline navigation and satellite links remain differentiators. Post-Brexit regulatory alignment with EU software-update rules ensures that U.K.-built head units remain export-ready.

The smaller but strategic markets in Cardiff and Belfast, where 5G roll-outs and aerospace know-how open avenues for component cross-pollination. Regional income disparities shape feature-adoption curves, with affluent suburbs selecting subscription bundles sooner than cost-conscious northern districts. Collectively, these dynamics sustain a diverse yet integrated landscape for the United Kingdom automotive infotainment market.

Competitive Landscape

The United Kingdom automotive infotainment arena showcases moderate concentration. Long-standing tier-ones leverage deep vehicle-systems know-how to package displays, domain controllers, and connectivity in turnkey bundles. They invest heavily in software platforms that can unlock subscription revenue long after delivery. Partnerships with cloud providers enhance voice assistants and over-the-air workflows, raising switching costs for automakers. Meanwhile, joint laboratories in the Midlands foster rapid prototyping of augmented-reality interfaces, keeping legacy suppliers at the forefront of cockpit innovation.

New entrants from Asia compete on cost efficiency and rapid iteration cycles that compress program timelines. Their vertically integrated supply chains reduce dependence on global semiconductor spot markets, insulating them from price swings. These firms bundle large touchscreens, robust processors, and voice-enabled operating systems in mid-range vehicles, forcing traditional brands to accelerate feature roadmaps. Incumbents respond by forming alliances with software specialists to enhance app ecosystems and personalize user journeys. Heightened competition ultimately benefits consumers by accelerating the diffusion of premium features.

Software providers with roots in mobile and cloud computing are reshaping value capture. They supply operating systems, app stores, and data analytics dashboards that transform the cockpit into an always-connected platform. Automakers weigh these offers against in-house solutions, balancing control over brand identity with speed to market. Regulators scrutinize data-sharing agreements, prompting all players to adopt transparent consent flows and robust privacy controls. The upshot is an industry moving toward open yet secure ecosystems where revenue stems as much from digital services as from hardware supply.

United Kingdom Automotive Infotainment Industry Leaders

-

Robert Bosch GmbH

-

Harman International

-

Continental AG

-

Panasonic Automotive Systems Co., Ltd.

-

Alps Alpine

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Farizon unveiled the V7E electric van at the Commercial Vehicle Show, integrating a 12.3-inch infotainment screen with Apple CarPlay and Android Auto.

- April 2026: Škoda announced software upgrades for its Elroq and Enyaq models, featuring enhanced infotainment and advanced driver-assistance systems.

- January 2026: P3 Digital Services and VNC Automotive commercially launched a pre-integrated solution that delivers full mobile phone connectivity to SPARQ OS-powered infotainment systems.

United Kingdom Automotive Infotainment Market Report Scope

The United Kingdom Automotive Infotainment market is analyzed across installation type, vehicle type, component, propulsion type, connectivity generation, operating system, and sales channel.

By Installation Type, the market is segmented into In-dash Infotainment and Rear-seat Infotainment. By Vehicle Type, the market is segmented into Passenger Cars, Light Commercial Vehicles, and Medium and Heavy Commercial Vehicles. By Component, the market is segmented into Display / Touchscreen, Head Unit / Media Player, Operating System, and Connectivity Module. By Propulsion Type, the market is segmented into Internal-Combustion Engine (ICE), Hybrid Electric Vehicle (HEV), and Battery Electric Vehicle (BEV). By Connectivity Generation, the market is segmented into 4G LTE, 5G, and Legacy 2G/3G. By Operating System, the market is segmented into Linux-Based, QNX, Android Automotive, and Others (Proprietary). By Sales Channel, the market is segmented into OEM-Installed and Aftermarket.

Market forecasts are provided in terms of Value (USD).

| In-dash Infotainment |

| Rear-seat Infotainment |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Display / Touch-screen Module |

| Head Unit / Domain Controller |

| Operating-System Software and Apps |

| Connectivity ICs and Antenna Modules |

| Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| 4G LTE |

| 5G |

| Legacy 2G/3G |

| Linux-Based (AAOS, AGL, etc.) |

| QNX |

| Android Automotive OS |

| Others (Proprietary, RTOS) |

| OEM-Installed |

| Aftermarket |

| By Installation Type | In-dash Infotainment |

| Rear-seat Infotainment | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | |

| By Component | Display / Touch-screen Module |

| Head Unit / Domain Controller | |

| Operating-System Software and Apps | |

| Connectivity ICs and Antenna Modules | |

| By Propulsion Type | Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles | |

| Battery Electric Vehicles | |

| By Connectivity Generation | 4G LTE |

| 5G | |

| Legacy 2G/3G | |

| By Operating System | Linux-Based (AAOS, AGL, etc.) |

| QNX | |

| Android Automotive OS | |

| Others (Proprietary, RTOS) | |

| By Sales Channel | OEM-Installed |

| Aftermarket |

Key Questions Answered in the Report

What is the current size of the United Kingdom automotive infotainment market?

The market was valued at USD 0.46 billion in 2025 and is expected to increase from USD 0.49 billion in 2026 to reach USD 0.71 billion by 2031, growing at a 7.59% CAGR over 2026-2031.

Which segment holds the largest United Kingdom automotive infotainment market share?

In-dash systems accounted for 85.15% of installations in 2025, leading all other installation types.

Which vehicle category is growing fastest for infotainment adoption?

Passenger cars show the highest growth, with their infotainment content advancing at a 10.47% CAGR.

How will 5G impact automotive infotainment in the UK?

Nationwide 5G coverage enables high-bandwidth services such as cloud gaming and real-time navigation, driving faster uptake of connected features.

Page last updated on: