Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

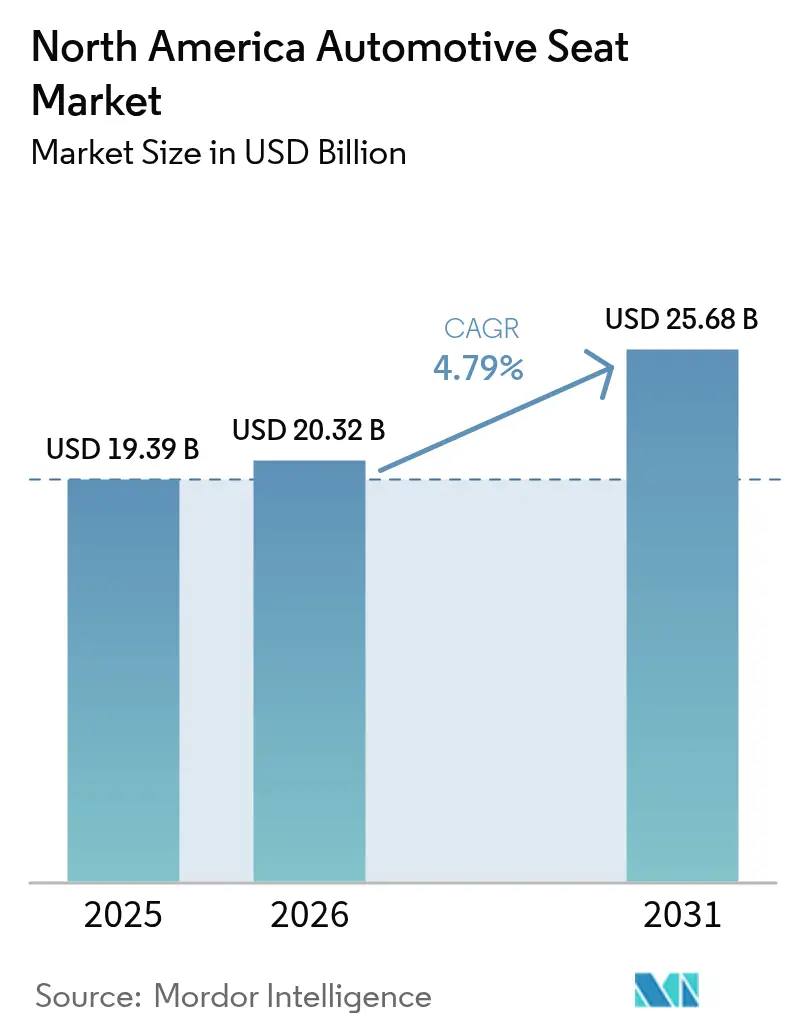

| Base Year Market Size (2025) | USD 19.39 Billion |

| Market Size (2026) | USD 20.32 Billion |

| Market Size (2031) | USD 25.68 Billion |

| Growth Rate (2026 - 2031) | 4.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automotive Seat Market Analysis by Mordor Intelligence

The North American automotive seat market size is expected to grow from USD 19.39 billion in 2025 to USD 20.32 billion in 2026 and is forecast to reach USD 25.68 billion by 2031 at 4.79% CAGR over 2026-2031. The expansion is propelled by premium SUV and pickup demand, electrification mandates that reshape interior architectures, and supplier investments in AI-enabled production that shorten lead times. Advanced comfort functions—ventilation, heating, and massage—are moving from luxury nameplates into mid-range trims, expanding the value pool. At the same time, USMCA rules accelerate near-shoring of sub-assemblies, giving regional suppliers an edge over more distant competitors. Persistent semiconductor constraints and tightening PFAS regulations temper the pace of powered-seat adoption and spur design innovation in lightweight mechatronics and compliant foams.

Key Report Takeaways

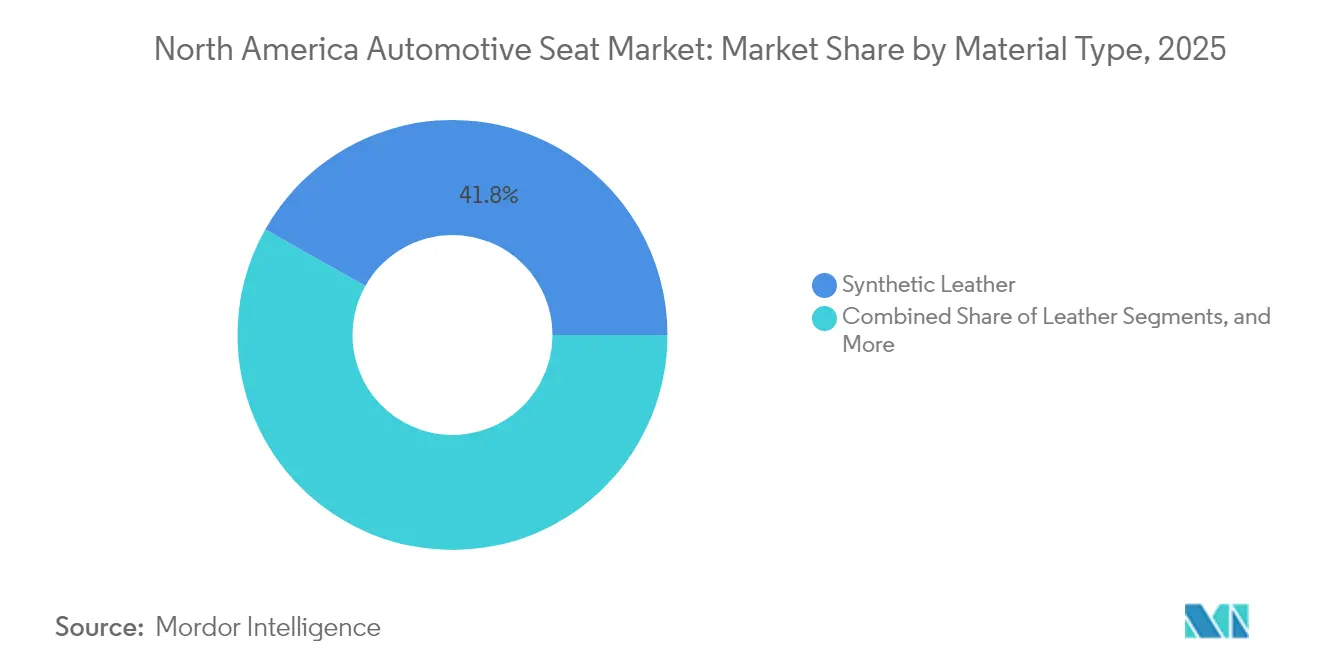

- By material type, synthetic leather led with 41.83% of the North America automotive seat market share in 2025; genuine leather is advancing at a 7.38% CAGR through 2031.

- By technology, standard seats accounted for a 61.85% share of the North America automotive seat market size in 2025, while massage and wellness variants are expanding at a 6.21% CAGR to 2031.

- By vehicle type, passenger cars captured 73.60% of the North America automotive seat market in 2025, yet light commercial vehicles posted the fastest 6.92% CAGR to 2031.

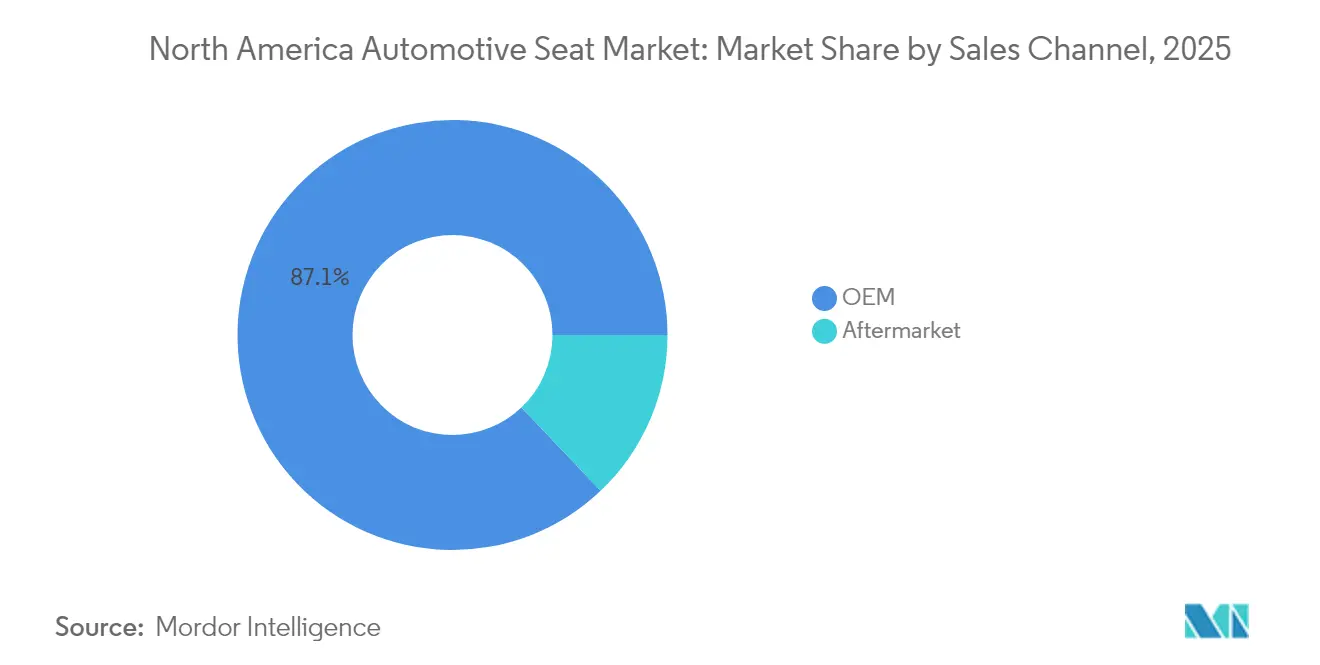

- By sales channel, OEM fitment held 87.10% of the North America automotive seat market size in 2025; the aftermarket is growing at a 7.52% CAGR through 2031.

- By powertrain, ICE models still accounted for 86.55% of the North America automotive seat market in 2025, but battery-electric vehicles recorded a 7.15% CAGR through 2031.

- By price band, mid-range trims dominated, with 51.70% of the North America automotive seat market in 2025, whereas luxury trims grew at a 6.72% CAGR through 2031.

- By country, the United States controlled 84.90% of the North America automotive seat market size in 2025; Mexico posts the quickest 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Automotive Seat Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium SUV and Pickup Demand For Ventilated Seating | +1.2% | United States and Canada; spillover to Mexico luxury | Medium term (2-4 years) |

| Comfort Features Migrating to Mid-Segment Vehicles | +0.9% | North America core markets; Mexico premium | Medium term (2-4 years) |

| OEM Lightweighting Favoring Synthetic and Bio-Based Materials | +0.8% | Global; early United States. adoption | Long term (≥ 4 years) |

| USMCA Driving Near-Shoring of Seat Sub-Assemblies | +0.7% | United States–Mexico border; Canada secondary | Short term (≤ 2 years) |

| AI-Enabled JIT Mass-Customized Production Lines | +0.6% | Michigan, Ontario, Nuevo León | Long term (≥ 4 years) |

| Municipal EV Mandates Boosting Ultralight Seat Demand | +0.5% | California; Northeast expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Premium SUVs and Pickups Boosting Demand for Powered, Ventilated Seating

Premium truck-based nameplates now integrate 30-way adjustment, active massage, and climate-control features that command higher transaction values. Lincoln’s Navigator Perfect Position seats and Ford’s Active Motion massage illustrate how comfort innovation reduces driver fatigue[1]“Active Motion Seats Reduce Driver Fatigue,”, Ford Media Center, fordmotorcompany.com. Full-size pickup registrations keep rising across North America, magnifying seat-content growth opportunities for vendors able to deliver premium functions at mainstream price points.

Integration of Advanced Comfort Functions in Mid-Segment Vehicles

Lear’s ComfortMax, debuting with GM in Q1 2025, heats or cools 40% faster with 50% fewer parts, proving that modular design shrinks bill-of-material cost [2]“ComfortMax Seat Launch,”, Lear Corporation, lear.com. Magna’s FreeForm trim, already specified for four new 2025 models, delivers high concavity and 50% recycled back-panel content. Vitesco pinpoints 48V architectures and power-over-Ethernet harnesses as enablers for energy-intensive seat features without bulky wiring. As consumers equate wellness with mobility, massage and thermal functions become necessary in mid-price vehicles.

OEM Lightweighting Targets Accelerating Adoption of Synthetic and Bio-Based Seat Materials

The automotive seating industry is transforming due to regulatory pressures and sustainability goals. Lightweight carbon-fiber seat backs reduce component mass, while bio-based foams from suppliers like Woodbridge scale eco-friendly materials for industrial use. Innovations from Covestro and Bcomp, such as low-carbon polyurethane and flax-based composites, cut lifecycle emissions by nearly 50%. With stricter emissions standards, OEMs are prioritizing curb-weight reduction. This urgency accelerates R&D timelines as seating suppliers meet stringent quality standards like IATF 16949. Success depends on balancing crash safety with environmental compliance, favoring firms that innovate quickly without compromising performance.

Municipal EV Fleet Mandates Driving Demand for Ultralight Commercial-Vehicle Seats

California’s rule for 50% zero-emission fleet purchases by 2024 and 100% by 2027 shapes a specialized seat market valuing weight savings and sustainable materials. FORVIA’s truck seat trims CO₂ using NAFILean Vision composites and Ecorium vegan upholstery [3]“NAFILean Vision Composite Seats,”, FORVIA, forvia.com. As northeastern states replicate CARB protocols, commercial fleets seek modular designs that support 24/7 duty and simplified maintenance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Leather and Petrochemical Volatility Inflating BOM Costs | -0.9% | Global; United States luxury concentration | Short term (≤ 2 years) |

| Semiconductor Shortages Crimping Powered-Seat Output | -0.7% | North America; Asia-centric supply | Medium term (2-4 years) |

| PFAS / VOC Rules Raising Foam Compliance Spend | -0.6% | United States; Canada extension | Long term (≥ 4 years) |

| Skilled-Labor Shortages and Wage Hikes At JIT Plants | -0.4% | Michigan, Ontario, Northern Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Leather and Petrochemical Price Volatility Inflating BOM Costs

Synthetic leather uses polyurethane derived from oil-based feedstocks, tying seat economics to crude swings. Genuine hides track livestock cycles and environmental constraints. OEM price-freeze contracts force suppliers to hedge or absorb volatility, tightening margins. Start-ups like Rheom offer bio-based leather to stabilize input costs, but validation and scale remain hurdles.

Semiconductor Shortages Limiting Powered-Seat Output

Due to allocation constraints on motor control units, position sensors, and rare-earth magnets, manufacturers must temporarily switch to manual adjusters. This change reduces the functionality and convenience of powered seats, which serve as a significant selling point in modern vehicles. Moreover, premium trims face difficulty sustaining market appeal when features like massage or memory functions are excluded. These exclusions lower the perceived value of premium offerings and threaten revenue streams, as consumers may choose lower trims or competing brands with better feature sets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Gains Within Synthetic Dominance

Synthetic leather retained the largest 41.83% slice of the North America automotive seat market in 2025, underscoring its cost benefit and animal-free appeal. Nevertheless, genuine leather is the fastest-rising material, charting a 7.38% CAGR through 2031 as luxury SUV and pickup buyers equate authenticity with status. Suppliers hedge volatility by trialing bio-based polymers that meet durability metrics without PFAS additives. Rheom’s plant-based surfaces illustrate how sustainability and premium cues can converge.

The North American automotive seat market size tied to genuine leather is projected to expand at the segment-leading pace, encouraging tanners to localize finishing operations under USMCA. Fabric remains prevalent in entry cars and vocational trucks, while polyurethane foams evolve toward low-VOC blends to satisfy California regulations. Magna’s FreeForm back panels, embedding up to 50% recycled plastic, highlight how material innovation underpins design freedom and regulatory compliance.

By Technology Type: Wellness Seats Extend Beyond Luxury

Standard manual units hold 61.85% share of the North America automotive seat market in 2025; fleet buyers prize simplicity and uptime. Massage and wellness seats will clock a 6.21% CAGR to 2031, reflecting demographic trends and heightened health awareness. Lear’s ComfortMax module fuses rapid-response micro-climate control with massage nodes, shrinking packaging to fit mid-size crossovers.

The North American automotive seat market share for powered, heated, and cooled configurations widens as 48V networks proliferate, letting OEMs avoid heavy-gauge wiring. Vitesco’s power-over-Ethernet approach reduces harness mass, aiding lightweighting goals. As wellness features normalize, tier-one suppliers pivot toward software-defined seat controllers capable of over-the-air function upgrades, opening aftermarket revenue streams.

By Vehicle Type: Passenger Scale, Commercial Velocity

Passenger cars commanded a 73.60% share of the North America automotive seat market in 2025, reflecting their dominance of the region’s installed base even as crossover and SUV body styles swell within the category. The North American automotive seat market size tied to passenger applications grows steadily because interior differentiation—ventilated cushions, digital controls—remains an OEM battleground. Full-size pickups, classified under passenger vehicles, further skew value content upward due to large-format frames and premium trim take rates. In contrast, heavy commercial vehicles and transit buses generate smaller absolute volumes but demand high-durability seating that commands premium pricing.

Light commercial vehicles are the sprint leader with a 6.92% CAGR through 2031, spurred by e-commerce logistics, municipal EV mandates, and last-mile delivery start-ups. FORVIA’s CO₂-reduced truck seat shows how commercial electrification prizes ultralight frames and modular maintenance access. As delivery operators value the total cost of operation, quick-swap cushions and washable trim gain favor, altering the specification mix. Suppliers that tailor ergonomic designs to multi-shift duty cycles stand to capture disproportionate margins in this fast-moving sub-segment.

By Sales Channel: Factory Control, Aftermarket Upside

OEM fitment captured 87.10% share of the North America automotive seat market in 2025, underscoring tight integration between seat modules and vehicle electrical architectures. Automakers lock in suppliers early, demanding just-in-sequence deliveries that satisfy stringent traceability and warranty standards. Hardware-software coupling—memory profiles stored in central gateways—further cements the OEM channel’s dominance because retrofitting these features post-sale is rarely cost-effective. Nonetheless, the aging vehicle fleet and consumer appetite for comfort upgrades seed a robust replacement market for trim covers, heating pads, and foam kits.

The aftermarket grows fastest at 7.52% CAGR through 2031, as owners extend vehicle lifecycles and gig-economy drivers invest in personal comfort. E-commerce platforms simplify SKU discovery and comparison, fueling price transparency and category penetration. Seat suppliers partner with certified repair chains to offer retrofit massage inserts that connect via 12 V power, reducing installation complexity. Regulation also nudges growth: fleet safety audits increasingly score driver ergonomics, prompting seat replacements that cut injury claims.

By Powertrain: ICE Scale, Electric Momentum

Internal-combustion vehicles still account for 86.55% share of the North America automotive seat market in 2025, underscoring the gradual nature of the propulsion transition. The North American automotive seat market share within ICE platforms remains sizable because legacy model programs extend well into the 2030s. Seat engineers emphasize lightweight frames and thin foams to compensate for more rigid U.S. fuel-economy rules, but packaging remains familiar. Battery-electric vehicles, however, post a class-leading 7.15% CAGR through 2031, as expanding charging infrastructure and tax credits nudge adoption upward. EV skateboard chassis free interior volume, letting suppliers propose lounge layouts with swivel bases and ottoman extensions.

New thermal-management demands accompany BEVs: HVAC inefficiencies penalize range, so climate-controlled seating migrates earlier in trim ladders. Yanfeng’s Smart Cabin Seat integrates displays and steer-by-wire input to eliminate instrument panels, previewing cockpit consolidation trends. Hybrid and fuel-cell variants lag in growth but keep niche relevance, each imposing unique weight and integration rules. Suppliers capable of modular architectures that flex between powertrains without retooling win program synergies and lower capex.

By Price Band: Mid-Range Volume, Luxury Acceleration

Mid-range trims owned a 51.70% share of the North America automotive seat market in 2025, matching North American buyer preference for well-equipped vehicles that balance features against affordability. OEMs load these models with heated cushions and power recline, ensuring baseline differentiation. Cost-optimized luxury cues—contrast stitching, soft-touch bolsters—allow suppliers to repurpose premium look-and-feel at lower BOM. At the other extreme, luxury nameplates accelerate at a 6.72% CAGR through 2031 as affluent households chase premium SUVs and pickups equipped with multi-mode massage, winged headrests, and reclining rear lounges.

Luxury growth has multiplier effects: authentic leather recovers share, recirculating lumbar bladders and active axis tilting raise actuator content, and glass-cockpit integration shifts control interfaces to touch-sensitive door panels. Economy segments stay steady, primarily servicing fleet and value niches where durability outweighs comfort. Price-band polarization pushes suppliers to develop scalable platforms: a standard metal frame with upgradeable foam and trim kits lowers tooling amortization while preserving brand-specific aesthetics.

Geography Analysis

The United States captured an 84.90% share of the North America automotive seat market in 2025, benefiting from the country’s high content per vehicle and robust pickup sales. Michigan and Kentucky anchor engineering hubs that co-locate with OEM final assembly, cementing supplier relationships. The North American automotive seat market size, attributable to the demand in the United States, will keep growing, yet its CAGR lags Mexico because of saturation.

Mexico registers a brisk 7.05% CAGR through 2031, as Chinese OEMs and tier-twos rush to establish USMCA-compliant capacity. Shanghai Daimay’s Ramos Arizpe facility and three forthcoming plants in Parras de la Fuente epitomize this inflow. Logistics upgrades across Laredo and Otay Mesa expedite seat-set flow into the United States assembly plants, narrowing delivery windows and widening the country’s cost advantage.

Canada maintains steady volume backed by integrated supply chains and parallel regulatory frameworks. Ontario’s push into AI-based manufacturing aligns with provincial incentives for automation retrofits, allowing seat suppliers to offset higher labor costs. Cross-border harmonization of safety standards ensures Canadian plants can feed U.S. and Mexican OEM lines with minimal revalidation effort.

Competitive Landscape

The North American automotive seat market shows a moderate level of concentration. With their long-standing industry presence, Adient, Lear, and FORVIA have secured global purchase agreements. Lear integrates electronics, combining seat controls with thermal and massage features. Adient focuses on modular metal-frame architectures that are adaptable from compact to full-size vehicles. FORVIA prioritizes sustainability, introducing a truck seat that reduces cradle-to-gate CO₂ emissions using NAFILean Vision composite structures.

Magna International, leveraging its expertise in cockpit systems, offers integrated seating, doors, and console modules. Disruptive players like China's Daimay use Mexican factories to undercut established players on pricing and localization. Additionally, software startups specializing in seat-based biometric monitoring have become prime acquisition targets for tier-one companies eyeing data-centric services. While high barriers to entry exist, including IATF 16949, ISO 14001 standards, and OEM warranty liabilities, niche players find relief as AI-driven design tools simplify prototyping challenges.

North America Automotive Seat Industry Leaders

Adient PLC

Lear Corporation

Toyota Boshoku Corporation

Faurecia SE (FORVIA)

Magna International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Adient introduced the ModuGo seat, a modular automotive seating solution. The design allows automakers to improve manufacturing efficiency and reduce costs while offering consumers customizable and adaptable seating options. The modular approach simplifies product development and manufacturing processes.

- March 2025: Pasubio opened a new leather-cutting plant in León, Guanajuato, Mexico, with a USD 16 million investment. The facility, situated in the PILBA industrial park, specializes in crafting leather for seats, headrests, and door panels.

North America Automotive Seat Market Report Scope

Automotive seats are designed to provide comfortable seating to the driver and passenger in the vehicle. An automotive seat typically consists of a frame, a backrest, a headrest, a seat base, and armrests. They are made of various materials, metals, composites, foam, and polyester or leather.

North America Automotive Seat Market is segmented into material type, technology, vehicle type, and country.

Based on the material type, the market is segmented into Leather, Fabric, and Other Materials.

Based on the technology, the market is segmented into Standard Seats, Powered Seats, Ventilated Seats, and Other Seats.

Based on the vehicle type, the market is segmented into passenger cars and commercial vehicles.

Based on the country, the market is segmented into the United States, Canada, and the Rest of North America.

For each segment, market sizing and forecast have been done on the basis of value (USD Billion).

By Material Type

| Leather |

| Fabric |

| Synthetic Leather |

| Polyurethane Foam and Others |

By Technology Type

| Standard (Manual-Adjust) Seats |

| Powered Seats |

| Heated Seats |

| Ventilated / Cooled Seats |

| Massage and Wellness Seats |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles and Buses |

By Sales Channel

| Original Equipment Manufacturer (OEM) |

| Aftermarket (Replacement / Retrofit / Customization) |

By Propulsion

| Internal-Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid (PHEV) |

| Battery Electric Vehicle (BEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

By Price Band (OEM Trim Alignment)

| Economy |

| Mid-range |

| Luxury |

By Country

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Material Type | Leather |

| Fabric | |

| Synthetic Leather | |

| Polyurethane Foam and Others | |

| By Technology Type | Standard (Manual-Adjust) Seats |

| Powered Seats | |

| Heated Seats | |

| Ventilated / Cooled Seats | |

| Massage and Wellness Seats | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles and Buses | |

| By Sales Channel | Original Equipment Manufacturer (OEM) |

| Aftermarket (Replacement / Retrofit / Customization) | |

| By Propulsion | Internal-Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) | |

| Plug-in Hybrid (PHEV) | |

| Battery Electric Vehicle (BEV) | |

| Fuel-Cell Electric Vehicle (FCEV) | |

| By Price Band (OEM Trim Alignment) | Economy |

| Mid-range | |

| Luxury | |

| By Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North American automotive seat market in 2026?

The market is valued at USD 20.32 billion in 2026 and is set to reach USD 25.68 billion by 2031.

Which material is growing fastest in North American automotive seating?

Genuine leather posts the highest 7.38% CAGR as premium SUVs and pickups favor authentic trim.

Why are massage and wellness seats gaining traction?

Wellness seats migrate to mid-range vehicles as suppliers slash costs and consumers prioritize comfort and health on longer commutes.

How are EV mandates influencing commercial-vehicle seats?

Fleet electrification rules drive demand for ultralight, sustainable seats that offset battery mass and align with zero-emission procurement criteria.

What role does USMCA play in seat supply chains?

The trade pact’s 75% regional-value rule is prompting suppliers to near-shore production to Mexico and the U.S. for tariff compliance and logistics savings.

Page last updated on: