Passenger Car Seat Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 47.63 Billion |

| Market Size (2030) | USD 54.71 Billion |

| Growth Rate (2025 - 2030) | 2.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Passenger Car Seat Market Analysis by Mordor Intelligence

The passenger car seat market size stands at USD 47.63 billion in 2025 and is projected to reach USD 54.71 billion by 2030, tracking a 2.81% CAGR during the forecast period (2025-2030). Steady growth reflects how seating systems evolve from basic structures into technology platforms that deliver thermal comfort, biometric monitoring, and over-the-air upgrades. Electrification accelerates this transformation because battery-electric vehicles require lightweight frames, integrated electronics, and software-ready architectures that open new recurring-revenue streams. At the same time, sustainability mandates drive rapid material innovation, while tightening safety rules spur greater sensor integration. Competitive intensity remains moderate as the top five suppliers control 67% of global revenue, a level that supports large-scale investments yet still encourages differentiation through design, materials, and digital services.

Key Report Takeaways

- By technology, standard seats led the passenger car seat market with a 65.18% share in 2024, whereas powered seats are forecasted to expand at a 4.54% CAGR during the forecast period (2025-2030).

- By seat type, bucket seats captured 60.21% of the passenger car seat market share in 2024, while the bucket-seat segment is poised for a 4.79% CAGR during the forecast period (2025-2030).

- By trim material, fabric accounted for 49.14% of the passenger car seat market share in 2024, whereas synthetic leather is expected to grow the fastest at 5.71% CAGR during the forecast period (2025-2030).

- By component, armrests held 22.76% of the passenger car seat market share in 2024; pneumatic massage systems are projected to register the highest 7.29% CAGR during the forecast period (2025-2030).

- By propulsion type, internal-combustion vehicles supplied 73.57% of the passenger car seat market share in 2024, yet battery-electric vehicle seats will rise at a transformative 19.18% CAGR during the forecast period (2025-2030).

- By vehicle type, SUVs commanded 42.62% of the passenger car seat market share in 2024, and remain the fastest-growing category with a 6.02% CAGR during the forecast period (2025-2030).

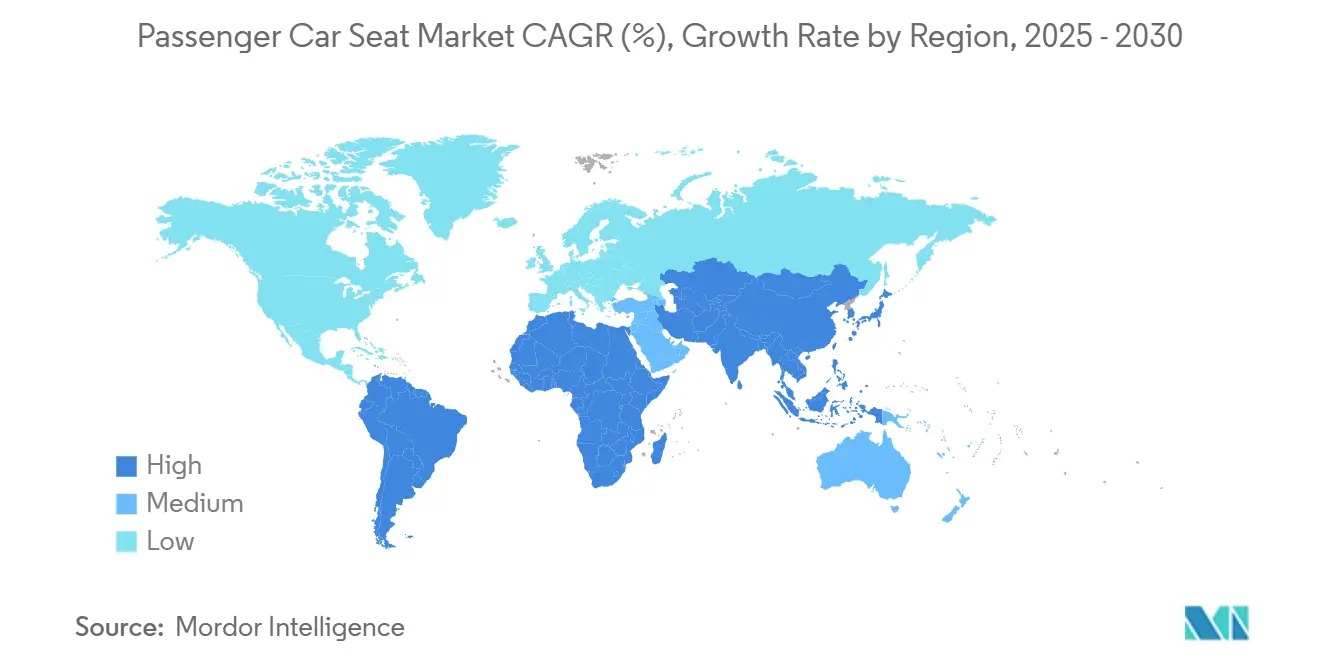

- By geography, Asia-Pacific dominated the passenger car seat market, with 48.42% of the share in 2024, and is forecasted to grow at a 3.37% CAGR during the forecast period (2025-2030).

Global Passenger Car Seat Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Comfort and Powered-Seat Adoption | +1.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| EV-Driven Seat Architecture | +0.8% | APAC core, spill-over to Europe and North America | Long term (≥ 4 years) |

| Health-Monitoring Sensor Seats | +0.6% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Integration of Airbags and Seat-Belts | +0.5% | Global, with regional compliance variations | Short term (≤ 2 years) |

| Sustainable/Vegan Upholstery | +0.4% | Europe-led, expanding globally | Medium term (2-4 years) |

| OTA Feature-on-Demand | +0.3% | North America and Europe early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Comfort & Powered-Seat Adoption

Consumers view cabins as mobile living spaces, so fast-acting heating, lumbar massage, and intuitive adjustment now shape purchase decisions. Lear’s ComfortMax platform launched with a major Detroit OEM in 2025 and shortens warm-up times by 40% while halving part counts, proving that comfort gains can align with manufacturing efficiency[1]“Lear INTU Advanced Seating Innovation,” Lear Corporation, lear.com. As scale improves and unit costs fall, powered features cascade from luxury to mid-range vehicles, lifting average seat content per vehicle and protecting supplier margins.

EV-Driven Seat-Architecture Redesign

Battery-electric platforms eliminate transmission tunnels, open flat floors, and intensify weight-reduction imperatives. FORVIA’s new Thai plant is optimized for lightweight frames and embedded electronics destined for regional EV exports, illustrating how suppliers reposition capacity to meet OEM electrification roadmaps[2]“FORVIA and BYD Open New Seat Assembly Plant in Thailand,” FORVIA, forvia.com. Lightweight alloys, modular power distribution, and swivel mechanisms unlock new interior layouts and revenue opportunities tied to autonomous-ready designs.

Health-Monitoring Sensor Seats

Seat-embedded electrodes now capture heart rhythm and breathing patterns without wearables, turning the chair into a health guardian. A 2025 Nature study showed capacitive ECG accuracy that rivals clinical devices, validating automotive use cases[3]Daowen Zhang et al., “Research on Restraint Strategies for Rearward-Reclined Occupants in a Frontal Rigid Barrier Crash,” Nature, nature.com. Fleet managers see insurance benefits when biometric alerts cut fatigue-related crashes, further pushing adoption. OEMs bundle health dashboards with connected-service plans, opening subscription revenue that extends well past the initial sale. Privacy concerns remain, yet strong encryption and opt-in frameworks reassure regulators and drivers alike.

Safety-Regulation Integration of Airbags & Seat Belts

Governments tighten rules, forcing seats to host advanced restraints and occupant-status sensors. New U.S. standards demand rear-seat belt reminders by 2027, spurring immediate hardware redesign[4]“Federal Motor Vehicle Safety Standards; Occupant Crash Protection, Seat Belt Reminder Systems,” National Highway Traffic Safety Administration, federalregister.gov. Suppliers integrate buckle sensors, weight mats, and side-impact airbags directly into frames, raising electronics content. These mandates add cost but also create a technology moat that favors scale players with deep validation labs. Over time, compliant systems become global norms, harmonizing specifications across regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost and Weight | -0.7% | Global, acute in cost-sensitive segments | Short term (≤ 2 years) |

| Raw-Material Price Volatility | -0.5% | Global, with regional supply chain variations | Medium term (2-4 years) |

| Cyber-Security and Privacy Risks | -0.3% | North America and Europe regulatory focus | Medium term (2-4 years) |

| Longer Replacement Cycles | -0.2% | Global, affecting aftermarket demand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost & Weight of Advanced Systems

Powered adjusters, thermal modules, and massage bladders add 15–25 kg to a vehicle and can boost bill-of-materials significantly. These penalties strain EV range targets, forcing OEMs to trade comfort against efficiency. Suppliers counter with aluminum frames under 10 kg and motor-in-rail designs that cut wiring runs, yet savings only partly offset added features. Procurement teams in cost-sensitive markets still bypass full-power suites, limiting penetration rates. This tension will persist until lightweight actuators and shared-architecture electronics close the cost gap with manual seats.

Raw-Material Price Volatility

Seat frames rely on steel and aluminum whose prices can swing around 20–30% in a single year. Such volatility compresses margins on fixed-price OEM contracts and complicates long-term capacity planning. Larger suppliers hedge exposure through multi-material designs, but smaller firms struggle to absorb spikes. Currency fluctuations add another layer of uncertainty, especially for exporters selling into dollar-denominated contracts. Price instability therefore delays capital projects and slows innovation budgets during peak cost cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology – Standard Seats Maintain Volume Advantage While Powered Features Accelerate

Standard seats commanded 65.18% of the passenger car seat market share in 2024, anchoring the passenger car seat market through affordability and easy repair. Their dominance endures in cost-sensitive regions, public-fleet purchases, and entry-level trims where basic adjustability meets functional need. Manufacturing scale keeps unit costs low, and continual refinement—such as lighter stamped frames and thinner foam pads—preserves margin even as commodity prices fluctuate. Standard architectures also serve as a base for modular add-ons, allowing OEMs to integrate heaters, cushions, or sensors without full redesign.

Powered seats, growing at a 4.54% CAGR during the forecast period (2025-2030), transform cabin experience with memory profiles, lumbar massage, and rapid warming capabilities. Lean motor assemblies and shared electronic control units lower incremental cost, encouraging adoption beyond luxury. As software-defined architectures mature, powered modules ship firmware-ready, enabling future-paid upgrades that bolster lifetime value. This dynamic positions powered variants to close the volume gap beyond 2030, especially in SUVs, where perceived value aligns with higher price points.

By Seat Type – Bucket Seats Propel Ergonomics and Wellness

Bucket seats configurations held 60.21% of the passenger car seat market share in 2024, reflecting their ergonomic contouring, lateral support, and compatibility with integrated airbags. The passenger car seat market benefits from bucket designs because they package ventilated cushions, active bolsters, and biometric sensors with minimal platform intrusion. Sports and performance vehicles champion these features, but mainstream crossovers adopt them to enhance ride quality and brand perception. Integrated air vents reduce cushion humidity, aligning comfort with hygiene expectations.

The bucket seats segment is expected to grow with a 4.79% CAGR during the forecast period (2025-2030), as OEMs monetize wellness narratives, offering fatigue mitigation during commutes. Meanwhile, bench seats remain staples in commercial vans and emerging-market compacts, where passenger capacity and low cost take precedence. Hybrid designs that add sculpted contours to two-thirds of a bench illustrate how manufacturers blend versatility with ergonomics, supporting family-vehicle use cases without abandoning price sensitivities.

By Trim Material – Synthetic Leather Rises on Sustainability Credentials

Fabric retained 49.14% of the passenger car seat market share in 2024 due to cost competitiveness and breathability. Improvements in nano-coated weaves deliver better stain resistance, closing the durability gap with coated surfaces. Fleet buyers favor fabric for easier replacement, while ride-sharing growth elevates hygiene demands that antimicrobial fabrics now meet. Profitable color and pattern customization also sustains the fabric’s appeal in youthful segments.

Synthetic leather is expected to be the fastest riser at a 5.71% CAGR during the forecast period (2025-2030), propelled by vegan consumer preferences and circular-economy targets. Water-borne polyurethane and recycled polyester backings reduce carbon footprints and VOCs, enabling OEMs to publicize ESG gains. Luxury marques experiment with bio-based polymers that emulate grain textures while promising easier recyclability. Genuine leather faces shrinking procurement volumes amid animal-welfare activism, higher tanning costs, and regulatory curbs on chromium discharge, narrowing its scope to ultra-premium niches.

By Component – Armrests Retain Scale, Massage Systems Capture Growth

Armrests represented 22.76% of the passenger car seat market share in 2024, owing to universality across segments. Storage bays, charge ports, and haptic control pads transform them into multi-functional modules that subtly justify incremental pricing. Height adjusters evolve to support biometric optimization, automatically adapting to occupant anthropometry. Suppliers pursue aluminum-reinforced swing-down arms for second-row SUVs that fold to become child-cupholders, showcasing how small innovations extend market relevance.

Pneumatic massage systems are expected to achieve a remarkable 7.29% CAGR during the forecast period (2025-2030), representing the fastest growth among all components as wellness features transition from luxury to mainstream adoption. Compact pneumatic bladders and silent micro-valves deliver shiatsu patterns once exclusive to flagship limousines. As well-being gains quantitative backing through biometric data, insurers may incentivize adoption, positioning massage units as safety devices rather than indulgences.

By Propulsion Type – ICE Volume Persists as BEV Growth Redefines Design Rules

Internal-combustion vehicles still constituted 73.57% of the passenger car seat market share in 2024, anchoring the target market to established manufacturing footprints and financing structures. They will decline gradually rather than collapse, sustaining a vast service and replacement ecosystem. ICE platforms rely on mature supplier tooling, keeping seat variants diverse in size and feature mix. Hybrid electric vehicles bridge the technology transition with moderate growth rates, while fuel cell electric vehicles remain niche applications with specialized requirements.

Battery-electric vehicle seats, surging at a 19.18% CAGR during the forecast period (2025-2030), demand lighter frames, thinner cushions, and recyclable trims to counteract battery mass. The absence of drivetrain vibration prompts emphasis on NVH-damping foams and acoustic membranes. Seats often house high-voltage cabling for rear-HVAC modules, intensifying collaboration between seat makers and e-powertrain engineers. Plug-in hybrid electric vehicles benefit from dual powertrain flexibility but face complexity challenges in seat system integration.

By Vehicle Type – SUVs Cement Leadership Through Premium Content

SUVs generated 42.62% of the passenger car seat market share in 2024 and are expected to post a 6.02% CAGR during the forecast period (2025-2030), as buyers favor higher ride height, interior flexibility, and upscale ambiance. Three-row configurations multiply seat count per vehicle, making this body style pivotal for volume growth. Premium features such as captain's chairs in second rows, ventilated cushions, and phone-based memory settings migrate down the price ladder fastest in SUVs, reinforcing their market hegemony.

Sedans remain validation platforms for advanced comfort tech in mature markets because ride dynamics showcase seat ergonomics and cushioning against chassis feedback. Hatchbacks preserve significance in densely populated regions due to compact footprints and practical rear access, supporting lower-cost seat solutions with simplified recliners. MPVs evolve into customizable lounges for ride-hailing fleets, demanding quick-release seat tracks that enable diverse layouts within shared-mobility business models.

Geography Analysis

Asia-Pacific accounted for 48.42% of the passenger car seat market share in 2024, and is poised for a 3.37% CAGR during the forecast period (2025-2030). China’s deep EV penetration accelerates local demand for lightweight, software-enabled seating, while Southeast Asian governments court foreign investment with tax holidays and zero-tariff export corridors. FORVIA’s Thailand factory exemplifies the region’s dual role as production hub and innovation lab. Japanese tier-ones leverage regional trade pacts to funnel aluminum frames across borders tariff-free, underpinning competitive cost structures even as commodity prices fluctuate.

North America leverages high average transaction prices to mainstream premium features such as seat-based biometric monitoring. However, potential tariff regimes on regional metal flows inject cost uncertainty that propels suppliers to localize content and diversify stamping partners. Stricter U.S. safety regulations, including rear-seat belt reminders, trigger rapid integration of buckle-status sensors and child-presence detection algorithms. These requirements raise electronics content per seat and favor suppliers with embedded-software competencies.

Europe emphasizes sustainability, mandating life-cycle assessments and recycled-material thresholds that boost synthetic-leather uptake. Premium OEMs headquartered in Germany and Sweden commercialize swivel and lounge configurations tested in concept vehicles, carving a path for broader adoption once regulatory clarity on autonomous-ready interiors emerges. EU grants supporting net-zero supply chains fund pilot lines that recycle seat foam into binder-free acoustic pads, advancing circular-economy goals. Meanwhile, emerging markets in Middle East, Africa, and South America scale local assembly plants that demand cost-effective standard seats today but represent latent potential for powered variants as disposable incomes rise.

Competitive Landscape

The Passenger Car Seat market exhibits moderate concentration, creating an oligopolistic structure that enables coordinated technology investments while maintaining competitive dynamics. Adient, Lear, and FORVIA leverage multi-regional footprints and co-located engineering centers within major OEM facilities, enabling early engagement in platform development. Their long-term supply agreements provide volume visibility that justifies sustained R&D outlays in smart textiles and lightweight frames.

Strategic initiatives increasingly blend hardware and software. Lear’s INTU suite packages biometric sensors, machine-learning comfort algorithms, and encrypted cloud connectivity, positioning the seat as a node within the broader vehicle experience. FORVIA partners with Chinese automakers to integrate cockpit electronics, merging seating, displays, and ambient lighting into cohesive modules fabricated under a single quality system. These moves safeguard share as tech-savvy disruptors target niches like sustainable trims or cloud-based subscription features.

Collaborative innovation shapes the mid-tier supplier segment. Joint ventures with material specialists bring bio-based polyurethane and recycled yarns into mainstream production, while alliances with health-tech startups embed medical-grade sensors able to detect early fatigue signs. As seating evolves toward service-enabled revenue, software talent and cloud infrastructure become competitive differentiators. Despite consolidation forces, regional champions retain relevance by offering localized design, faster engineering turnaround, and familiarity with domestic regulations, especially in India, Indonesia, and Brazil.

Passenger Car Seat Industry Leaders

Adient plc

Lear Corporation

Faurecia (FORVIA)

Toyota Boshoku

Magna International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Kia confirmed a six-seat variant of the Clavis EV with second-row captain’s chairs aimed at family buyers prioritizing space and premium comfort.

- April 2025: Lynk & Co, a premium brand under Zeekr Group, began delivering its new Lynk & Co 900, a large six-seater family SUV. The vehicle's spacious interior, advanced technology, and performance capabilities have attracted over 40,000 pre-orders since its launch.

- February 2025: Ceer, Saudi Arabia's first electric vehicle (EV) manufacturer, has established a SAR 543 million (USD 145 million) partnership with Sabelt, an Italian company specializing in automotive seat manufacturing. Sabelt designs and produces high-performance seats, focusing on sports, racing seats, and safety harnesses.

- February 2025: Lear Corporation integrated its engineering capabilities with General Motors to develop the ComfortMax Seat. This seat design incorporates thermal comfort technologies within trim covers to enhance occupant comfort, improve temperature management, and increase manufacturing efficiency.

Global Passenger Car Seat Market Report Scope

| Standard Seats |

| Powered Seats |

| Bucket Seats |

| Bench Seats |

| Fabric |

| Genuine Leather |

| Synthetic Leather |

| Armrest |

| Seat Frame and Structure |

| Recliner |

| Pneumatic System |

| Headrest |

| Seat Track |

| Seat Belt |

| Height Adjuster |

| Side/Curtain Airbag |

| Others |

| Internal Combustion Engine |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-In Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| Hatchbacks |

| Sedans |

| Sport-Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MPVs) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Standard Seats | |

| Powered Seats | ||

| By Seat Type | Bucket Seats | |

| Bench Seats | ||

| By Trim Material | Fabric | |

| Genuine Leather | ||

| Synthetic Leather | ||

| By Component | Armrest | |

| Seat Frame and Structure | ||

| Recliner | ||

| Pneumatic System | ||

| Headrest | ||

| Seat Track | ||

| Seat Belt | ||

| Height Adjuster | ||

| Side/Curtain Airbag | ||

| Others | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery Electric Vehicle (BEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Plug-In Hybrid Electric Vehicle (PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Vehicle Type | Hatchbacks | |

| Sedans | ||

| Sport-Utility Vehicles (SUVs) | ||

| Multi-Purpose Vehicles (MPVs) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the passenger car seat market in 2025?

The passenger car seat market size is USD 47.63 billion in 2025.

What CAGR is forecast for passenger car seat sales through 2030?

Global revenue is projected to advance at a 2.81% CAGR from 2025 to 2030.

Which region leads seat demand today?

Asia-Pacific holds 48.42% of global revenue and remains the fastest-growing geography through 2030.

What segment shows the highest growth rate?

Seats designed for battery-electric vehicles rise at a 19.18% CAGR, far above the market average.

Which material is gaining share fastest?

Synthetic leather posts a 5.71% CAGR thanks to sustainability goals and vegan consumer demand.

Page last updated on: