Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 15.81 Billion |

| Market Size (2026) | USD 16.45 Billion |

| Market Size (2031) | USD 20.07 Billion |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Seat Market Analysis by Mordor Intelligence

The Europe Automotive Seat Market size was valued at USD 15.81 billion in 2025 and estimated to grow from USD 16.45 billion in 2026 to reach USD 20.07 billion by 2031, at a CAGR of 4.06% during the forecast period (2026-2031). Vehicle registrations are gradually increasing, with battery-electric vehicles gaining significant market penetration. Stricter EU penalties for carbon dioxide emissions, expected to reach substantial levels in the near future, are influencing procurement choices. These choices lean towards lighter seat frames, advanced thermal features, and architectures rich in sensors. While the European automotive seat market reaps benefits from OEMs' commitments to electrification, it grapples with fluctuating costs of polyurethane and semiconductors. These fluctuations necessitate ongoing revisions in design and sourcing. Sustainability mandates are pushing recycled PET fabrics and bio-based polyurethane foams into mainstream programs, especially as OEMs highlight their circularity targets. Independent aftermarket players are increasing their e-commerce presence for seat refurbishment parts in a notable shift. This move challenges the traditional supply chain, which has predominantly centered around OEMs in the European automotive seat market.

Key Report Takeaways

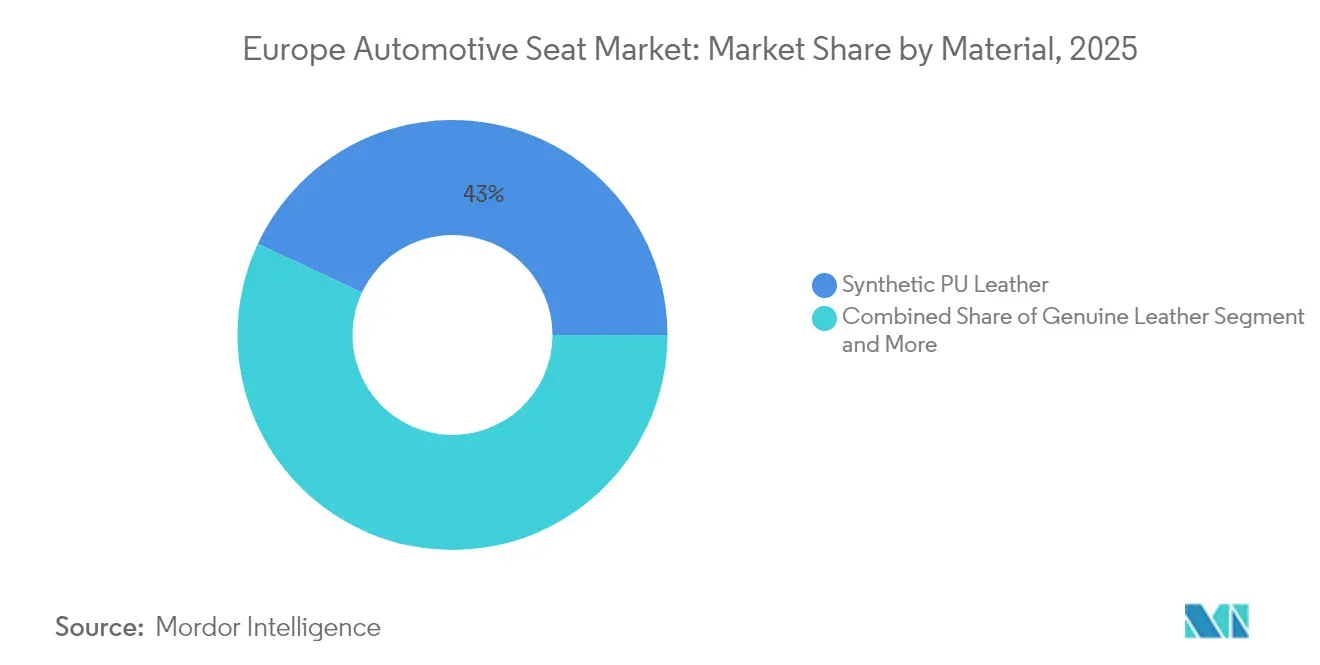

- By material, synthetic PU leather held 43.02% of the European automotive seat market share in 2025, while bio-based PU is projected to expand at a 4.12% CAGR during the forecast period (2026-2031).

- By technology, powered and adjustable seats accounted for 36.20% of the European automotive seat market size in 2025, whereas smart ADAS-integrated seats are tracking a 4.15% CAGR during the forecast period (2026-2031).

- By vehicle type, passenger cars generated 72.85% of the European automotive seat market size in 2025; also, passenger-car seats are set to grow at a 4.08% CAGR during the forecast period (2026-2031).

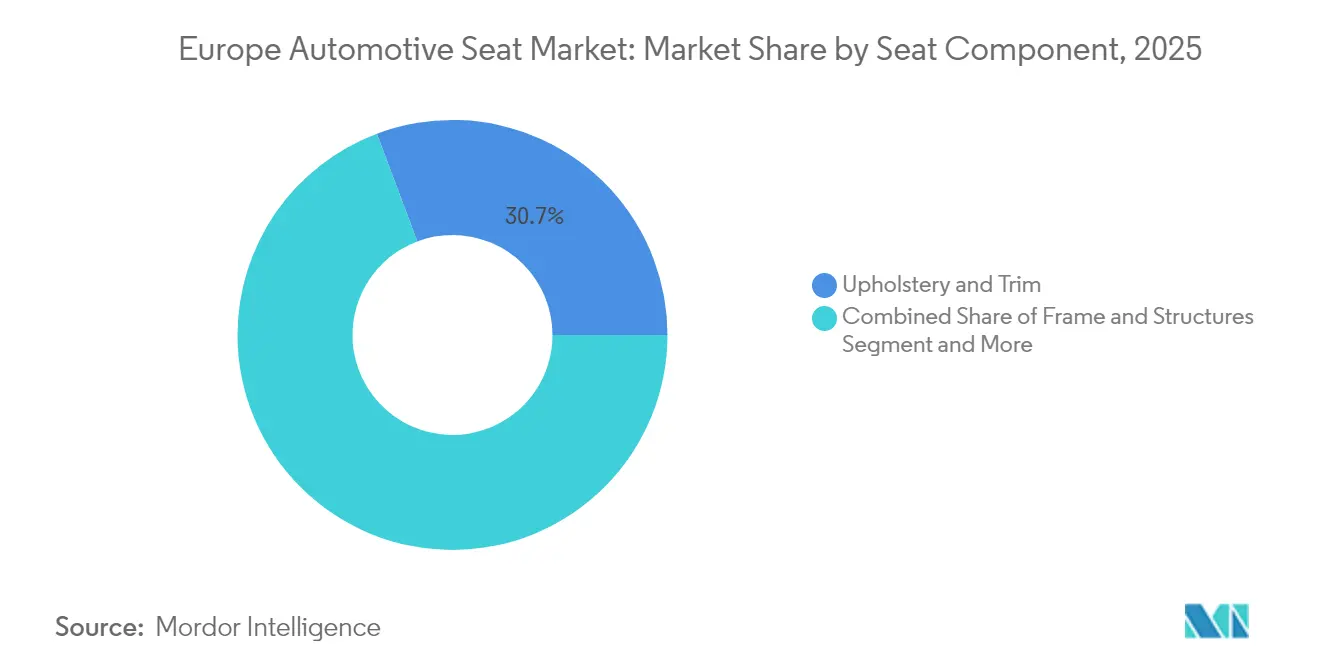

- By seat component, upholstery and trim led the European automotive seat market, with 30.72% of the size in 2025, and sensors plus ECUs are forecast to rise at a 4.13% CAGR during the forecast period (2026-2031).

- By sales channel, OEM programs dominated with 86.95% revenue share in 2025, whereas aftermarket platforms are at a 4.16% CAGR during the forecast period (2026-2031).

- By country, Germany dominated with 36.78% revenue share in 2025, whereas the United Kingdom is on pace for a 4.17% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Automotive Seat Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Electrification | +1.1% | EU-wide, strongest in Nordic countries | Long term (≥ 4 years) |

| EU General Safety Regulation 2019/2144 Mandating | +0.9% | All EU member states | Short term (≤ 2 years) |

| Rise In OEM Demand | +0.8% | Germany, France, Italy core markets | Medium term (2-4 years) |

| Sustainability Push For Circular Upholstery | +0.6% | Western Europe, expanding eastward | Medium term (2-4 years) |

| Aftermarket Customization Boom | +0.4% | Germany, UK, France, Netherlands | Short term (≤ 2 years) |

| Growing Fleet/Ride-Hailing Refurb Cycles | +0.3% | Urban centers across major EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification Creating New Thermal-Management Seat Features

A high BEV share means cabin heating no longer taps engine waste heat. Vitesco data show 48 V seat heaters slash whole-vehicle HVAC load by one-third, raising winter-range credibility—vital in Nordic sub-zero climates [1].“48V Thermal Management for Electric Vehicles,” Vitesco Technologies, vitesco-technologies.com EV-centric seats gain active ventilation, zonal micro-climate control, and self-diagnosing power electronics. Design teams juggle electromagnetic-compatibility constraints next to battery cabling, triggering fresh material stack-ups and conductive-foam trials. Thermal specialists can validate long-cycle vibration and temperature swings and see demand surge, propelling the European automotive seat market toward higher electronic content per unit.

EU General Safety Regulation 2019/2144 Mandating Advanced Seat Sensors

Since July 2024, every new European vehicle must host occupant-status detection and belt reminders rooted in innovative seat electronics. Pressure mats, weight classifiers, and camera-assisted posture tracking now ship standard on mass-market trims. FORVIA and Lear embed redundant CAN nodes to guarantee data integrity for ADAS stacks, turning the seat into a real-time occupant-intelligence hub. Certification labs note a two-fifths increase in seat-related EMC tests, extending program timelines yet assuring compliance. The regulation sparks aftermarket retrofits for fleet vehicles, further stretching the supply of sensor kits across the European automotive seat market.

Rise in OEM Demand for Lightweight, Mixed-Material Seat Frames

European assemblers double down on aluminum-magnesium-composite frames that cut seat mass by one-fourth and help avert looming high CO₂ fines. FORVIA’s multi-material lattice structures illustrate the pathway, pairing carbon-fiber backrests with aluminum rails to uphold crash rigidity. Suppliers now qualify up to five new raw-material sources per program, broadening metallurgical test plans and inflating joining-technology investment budgets. Those mastering hybrid riveting, laser welding, and structural adhesives earn preferred-supplier status in the European automotive seat market. As fleet targets tighten in 2027, lightweight adoption moves from premium models into B-segment platforms, locking in volume gains for innovators.

Sustainability Push for Circular Upholstery (Recycled PET & Bio-PU)

OEM climate pledges elevate recycled textiles and bio-foams. Audi upholsters the A3 with yarn spun from 45 recycled PET bottles per seat set [2]“Recycled PET in A3 Seats,” Audi MediaCenter, audi-mediacenter.com. Huntsman's bio-PU foam reduces cradle-to-gate emissions by one-fourth, and Covestro's water-borne coatings lower process water consumption [3]“ACOUSTIFLEX VEF BIO for Automotive Seating,” Huntsman, huntsman.com . Suppliers invest in closed-loop logistics that back-haul end-of-life fabrics into mechanical recycling lines near German stitching plants. Quality variance in post-consumer feedstock calls for advanced inline optical scanners to protect color consistency at scale. Despite higher material sourcing overhead, momentum keeps bio-content climbing in the European automotive seat market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seat-Electronics Chip Shortages And Price Spikes | -0.9% | All European manufacturing centers | Medium term (2-4 years) |

| Volatile Polyurethane and Leather Input Costs | -0.7% | EU-wide, particularly affecting German production | Short term (≤ 2 years) |

| Under-Utilised European Assembly Capacity | -0.6% | Germany, France, Italy core manufacturing hubs | Medium term (2-4 years) |

| Stricter EU Chemical Rules On Hexavalent-Chrome Tannery Effluents | -0.5% | EU leather processing regions, Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seat-Electronics Chip Shortages and Price Spikes

Smart seats may host up to 15 microcontrollers and power drivers; however, automotive-grade MCU lead times ballooned from 14 to 38 weeks in 2024. Premium SUV lines in Slovakia idled for nine shifts when occupancy-sensor ASICs ran dry. Some suppliers redesign boards to consolidate functions onto readily available processors, cutting chip count by one-eight but raising R&D spend. Firms with dual-sourcing in Taiwan and Europe ride out volatility better, capturing urgently rerouted OEM volumes in the European automotive seat market. Long-term, localized semiconductor fabs could dilute this restraint, yet capacity additions will not ease shortages before 2027.

Volatile Polyurethane & Leather Input Costs

Raw materials consume up to two-fifths of premium-seat build cost, exposing margins to swings in oil-derived polyols and hides. Between 2024 and 2025, spot PU prices oscillated minimally, bankrupting several Tier-2 foam molders clustered around Stuttgart. EU chemical rules banning hexavalent-chrome tanning force tanneries into costlier alternatives, inflating hide procurement by one-fourth. Seat makers hedge with multi-quarter purchase agreements and diversify to bio-based foams, yet contract clauses rarely allow full cost pass-through. Until price curves stabilize, the European automotive seat market endures compressed EBIT for trim-intensive luxury programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Synthetic Dominance Amid Sustainability Push

Synthetic PU leather controlled 43.02% of the European automotive seat market size in 2025, thanks to its uniform surface quality, design latitude, and lower scrap rates than genuine hides. Bio-based PU, although niche, is climbing at a 4.12% CAGR as OEMs publish life-cycle reports quantifying 25% carbon savings. Recycled PET fabric innovations allow manufacturers to meet European end-of-life directives without sacrificing abrasion resistance, a key metric for ride-hailing interiors. Genuine leather persists in flagship trims, but hexavalent-chrome restrictions elevate finishing costs, nudging volume brands toward vegan alternatives. Composite and 3D-knit seat skins shrink mass and uplift breathability, supporting stringent EV range targets.

Europe automotive seat market participants now pair water-borne PU coatings with low-VOC backing adhesives, eliminating most of the process water and cutting curing energy. Supply chains diversify, with Eastern European mills spinning recycled yarns to offset Western labor costs. While raw-material volatility remains, long-term contracts for bio-based feedstocks stabilize input pricing. Sustainable textile labels bolster showroom messaging, reinforcing consumer acceptance and thus accelerating material-mix transition across the European automotive seat market.

By Technology: Smart Seats Propel Safety and Comfort

Smart ADAS-integrated seats will clock a 4.15% CAGR to 2031 as EU GSR 2019/2144 forces occupant-monitoring deployment on every new model. Powered and adjustable mechanisms still own 36.20% of the European automotive seat market share, owing to entrenched consumer expectations for multi-way comfort. Nordic winters sustain elevated demand for heated cushions, whereas Mediterranean climates steer ventilated-perforation take-rates. Premium OEMs bundle massage and posture-correction algorithms that log driver fatigue and then share data with cloud analytics for predictive health services.

Europe's automotive seat industry pioneers now co-package seat ECUs with zonal controllers, trimming wiring weight by 800 g per vehicle. Over-the-air firmware updates allow remote comfort-curve edits, positioning seats as software-defined features. Modular electronics ease compliance updates when safety rules evolve, a competitive lever that underpins recurring revenue models through subscription-based massage sequences. As semiconductor availability normalizes, ADAS seat content will spread into C-segment crossovers, deepening electronic value capture inside the European automotive seat market.

By Vehicle Type: Passenger Car Supremacy as EVs Surge

Passenger cars delivered 72.85% of the European automotive seat market size in 2025. Yet, the BEV passenger-car subsegment is the star, advancing 4.08% CAGR to 2031 as incentive cuts fail to dent consumer interest. Compact SUVs gain momentum, demanding split-fold sliding benches that preserve cargo flexibility. Commercial vehicle seats pivot to high-durability textiles rated for 70,000 cycles, matching logistics operators’ uptime targets. Minibus orders climb in tourist and airport shuttle fleets, widening demand for easily sanitizable vinyl overcovers.

Thermal-neutral foams mitigate battery-pack heat soak in flat-floor EV architectures, while frame engineers wrestle with under-seat pack-mount points that alter load-path modeling. The European automotive seat market thus faces a convergence of comfort, structural, and thermal constraints that vary sharply by vehicle class. Heavy truck cabins integrate pivoting beds and active lumbar systems to meet EU driver-wellness directives, extending seat supplier reach beyond light-duty segments.

By Seat Component: Electronics Lead Value Growth

Sensors and ECUs record a 4.13% CAGR, outpacing the broader European automotive seat market as every seat morphs into a data node. Upholstery and trim still furnish 30.72% revenue share because surface finishes remain the first customer touchpoint. Foam formulators inject micro-vents that raise breathability 22% while shaving density grams—a double win for comfort and mass. Motors have gained brushless architectures, halving noise and extending service life for the past 15 years, which is critical for circular-economy durability pledges.

Lightweight magnesium frames migrate from luxury coupe bolsters into mid-price EVs, trimming 1.8 kg per seat and offsetting battery mass. Airbag suppliers retool side-thorax modules to fit thinner cushion profiles. Integration drives new validation regimes where electronics, pyrotechnics, and composites co-exist, making systems engineering skills a key hiring hotspot in the European automotive seat market.

By Sales Channel: OEM Channels Rule, Aftermarket Goes Digital

OEM assembly plants consumed 86.95% of the European automotive seat market in 2025, cementing tier-one supplier dependence on vehicle production cycles. Nonetheless, online aftermarket value is climbing at a 4.16% CAGR as DIY consumers retrofit heating kits and vegan-leather covers. Multi-language configurators replicate OE stitch patterns, escalating personalization beyond dealer accessories. Fleet refurb contracts award volume certainty to seat rebuilders who can swap cushion cores in under 30 minutes at urban service hubs.

OEM suppliers launch direct-to-consumer storefronts to counter margin dilution, capitalizing on brand equity and reducing wholesaler cuts. Subscription upholstery refresh programs emerge, offering annual seat-skin replacements bundled with detailing visits. The European automotive seat market thus witnesses a hybrid distribution era where traditional just-in-time lines coexist with click-n-ship micro-warehouses serving the continent within 24 hours.

Geography Analysis

Germany anchors the European automotive seat market with 36.78% market share in 2025, a dense supplier ecosystem, and advanced safety regulatory enforcement. Although BEV incentives waned, the country still posted a minimal electric passenger-car share in 2024, sustaining demand for lightweight, thermally efficient seating. FORVIA’s Bavarian plant pilots carbon-fiber backrests trimmed on high-speed water-jet lines. Brose’s Coburg facility rolls out 48 V seat-adjuster drives that integrate seamlessly with zonal body controllers. Yet semiconductor shortages caused nine assembly-line stoppages across German OEMs, pressuring seat suppliers to carry buffer inventories exceeding pre-pandemic norms.

France follows closely, buoyed by a heavy BEV share in January 2025 and PERTE VEC III funds funneling into supplier electrification upgrades. Renault and Stellantis seat programs specify bio-PU foams incorporating one-fifth plant-based polyols, catalyzing domestic chemical suppliers to scale bio-feedstock output. French tier-ones integrate driver-attention sensors into headrests earlier than the demand of EU timelines, earning five-star Euro NCAP ratings that promote export prospects.

The United Kingdom navigates post-Brexit harmonization divergence, posting a robust CAGR of 4.17% through 2031, yet seat safety rules remain harmonized with UNECE frameworks, allowing cross-channel component flows. Nearby, Italian leather-trim specialists in Abruzzo pivot toward water-borne finishing lines to meet EU leather-chem rules, protecting their niche in luxury sports-car segments. Spain’s Zaragoza production clusters supply bench seats for European vans, leveraging competitive labor and proximity to key logistics corridors.

Regulatory Landscape

Europe automotive seats are covered by UNECE type-approval rules that set baseline requirements for seat strength, anchorages, and head restraints (UN R17 for M1/N1), as well as requirements for large-passenger-vehicle seats (UN R80, updated with the 04 series of amendments entering into force on 12 June 2025). Broader UNECE safety regulations for occupant protection in frontal and lateral collisions (UN R94 and UN R95, with supplements entering into force on 12 June 2025) shape seat structures and the integration of restraint systems, while UN R145 (in force 12 June 2025) specifies requirements for ISOFIX anchorages and i-Size seating positions, which influences seat architecture and validation planning.

Materials and cabin health requirements also feed into seat design and sourcing. Under EU chemicals legislation (REACH), Entry 77 sets a formaldehyde emission limit of 0.062 mg/m3 for road-vehicle interior air, increasing testing and documentation demands for foams, textiles, and adhesives. In parallel, EU-wide vehicle-safety requirements under the General Safety Regulation introduced new rules taking effect on 7 July 2026, further reinforcing the need for seats to accommodate advanced safety hardware and robust in-cabin sensing integration aligned with evolving approval and compliance regimes.

Value Chain Analysis

The European automotive seating value chain begins with upstream inputs, including polyurethane chemicals for foam, steel and light alloys for frames and tracks, textiles and synthetic leathers for covers, and semiconductors for sensors, ECUs, and comfort electronics. Tier-2 specialists supply foam molding, cut-and-sew trim, metal stampings, motors and actuators, and sensor modules to Tier-1 integrators such as Adient, Lear, FORVIA, and Magna, which deliver complete seat systems to vehicle OEMs. Industry bodies including CLEPA and Euromoulders support supplier alignment on compliance topics (notably REACH) and competitiveness themes tied to European production footprints.

Downstream, OEM supply dominates, reflecting Europe-based heavy reliance on Just-in-Time and Just-in-Sequence delivery to assembly plants. This delivery model favors supplier proximity and synchronized sequencing. Nearshoring and regionalization show up as responses to logistics risk and program volatility, with Seat and Cupra stating that 75% of part references for the Martorell plant come from within Spain or neighboring European countries. Capacity footprint shifts are also visible across adjacent seating categories, including Sears Seating opening a new manufacturing facility near Madrid, Spain (Sears Manufacturing Iberia, S.L.), reinforcing the role of Iberia and Central and Eastern Europe as manufacturing and logistics nodes for seat and interior supply.

Competitive Landscape

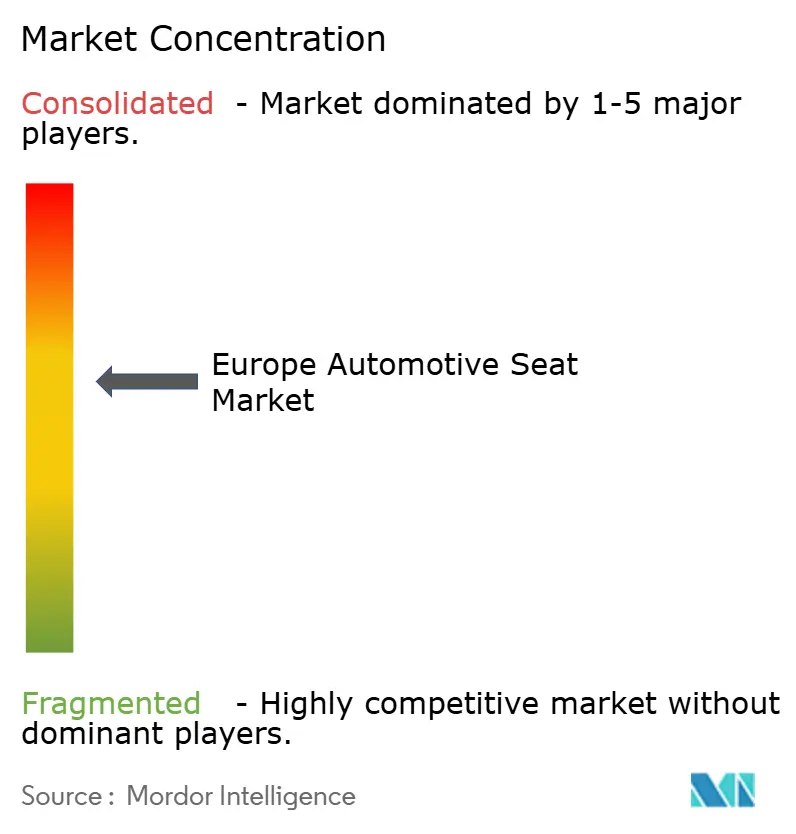

Market concentration remains moderate: Adient, Lear, FORVIA, and Magna dominate a significant portion of tier-one seat volumes. However, they now face fresh competition from electronics-centric entrants and specialist trim houses. FORVIA has restructured, consolidating multiple German facilities into fewer high-automation hubs, reducing logistics miles and cutting Scope 1 emissions. In recent developments, Lear reduced its workforce to optimize fixed costs during semiconductor shortfalls while maintaining R&D investments in innovative seat architectures.

Magna is expanding its Czech plants to produce composite backframes, eyeing mass-market EV contracts with German OEMs. Gentherm, a specialist in thermal comfort, is capitalizing on the Hanon Systems acquisition—finalized by Hankook in early 2025—to ensure a steady supply of thermal-loop components, thus safeguarding its margins in an era of silicon scarcity. Recaro Automotive showcases the potential for niche survival in the European automotive seat market, remaining profitable by concentrating on high-margin segments for premium OEMs and sim-racing enthusiasts.

As the competitive landscape evolves, the focus shifts from cost-per-seat to the functionality delivered per kilogram. Suppliers are pushing data-monetization models, offering occupant analytics subscriptions that OEMs can upsell after purchase. Sustainability disclosures are becoming essential contract components; FORVIA’s ambitious Net Zero by mid-century plan sets a standard that competitors are eager to emulate. The consolidation trend is evident, with smaller foam and sewing shops either carving out niches in local aftermarket refurb fleets or engaging in acquisition discussions with larger entities seeking vertical integration.

Europe Automotive Seat Industry Leaders

Adient PLC

Lear Corporation

Groclin S.A

Forvia SE

RECARO Automotive Italy S.r.l.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulation-driven electronic content and integration work continues to create whitespace for seat suppliers that can industrialize occupant-status detection, belt-reminder sensing, and robust in-seat networks while staying within automotive validation constraints. The EU General Safety Regulation and related UNECE approval requirements keep focus on system-level compliance, supporting opportunities for modular seat electronics, integrated ECUs, and simplified wiring architectures that reduce harness mass and improve manufacturability. In addition, REACH formaldehyde limits for vehicle interior air (0.062 mg/m3 under Entry 77) keep demand anchored for low-emission foams, adhesives, and trim stacks, working alongside OEM circularity efforts that already bring recycled PET fabrics and bio-based polyurethane foams into mainstream seating programs.

Manufacturing and platform investments in Europe also support localized seat sourcing, particularly as new EV and hybrid programs move into industrialization. In June 2026, Stellantis announced a EUR 1 billion investment in its Mulhouse site in France to enable production of three new electric and hybrid Peugeot models on the STLA One platform starting in 2029, creating a qualification window for lightweight structures, thermal comfort features, and compliant interior materials. In commercial vehicles, MAN Truck and Bus started series production of the electric MAN eTGL truck at its Krakow plant in Poland in July 2026, and also signed an MoU with the Polish government tied to investments of about EUR 1.2 billion through 2030, highlighting Central and Eastern Europe as a scaling center where seat makers can expand JIS-ready capacity, electronics integration, and durable trim offerings for electrified fleets.

Recent Industry Developments

- April 2026: Adient introduced its ProForce Massage Flow seating solution for series applications. The launch adds another comfort-electronics content layer to the seat, supporting OEM differentiation through software-controlled massage and actuation features. It also increases the importance of robust electronics sourcing and validation for powered and smart seat programs.

- January 2026: FORVIA announced it won over USD 1 billion in new and extended business with a major European automaker across seating, interiors, and lighting. The award signals ongoing platform-level bundling of interior systems and puts emphasis on Tier-1 suppliers that can integrate seating with broader cockpit and vehicle-electronics architectures. It also strengthens long-term program visibility for European seating operations tied to major OEM production cycles.

- December 2024: Adient partnered with Jaguar Land Rover and Dow to advance closed-loop recycling for polyurethane seat foam recovered from end-of-life vehicles, producing cushions with 20% recycled polyol content. The collaboration shows an early step toward circular foam content in seating, aligning with tightening chemical and sustainability requirements for interior materials. It also pressures competing suppliers to develop scalable recycling and traceability pathways for foams and trim.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers revenues earned from supplying complete automotive seats and key seat systems used in passenger cars and commercial vehicles across Europe, counted at the point of sale through OEM fitment and aftermarket replacement.

Scope exclusions: We exclude non-automotive seating (rail, aviation, marine), general interior trim not tied to seats, and vehicle seating used outside Europe even if produced in Europe.

Segmentation Overview

- By Material

- Genuine Leather

- Synthetic Leather – PU

- Synthetic Leather – PVC

- Fabric

- Composite/3D-knit

- Others

- By Technology

- Standard/Manual

- Powered/Adjustable

- Heated

- Ventilated

- Massage

- Smart ADAS-integrated

- Child Safety Seats

- By Vehicle Type

- Passenger Car

- Hatchback

- Sedan

- SUV/Crossover

- MPV

- Commercial Vehicle

- Light Commercial Vehicle

- Heavy Truck

- Bus/Coach

- Passenger Car

- By Seat Component

- Frame & Structures

- Foam & Padding

- Upholstery & Trim

- Motors & Actuators

- Sensors & ECUs

- Airbags & Restraints

- By Sales Channel

- Original Equipment Manufacturer (OEM)

- Aftermarket

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Poland

- Sweden

- Russia

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure for volumes, price direction, and policy context, and then to cross-check whether the model totals match what the industry is signaling. Public datasets and official sources, such as Eurostat production and trade tables, ACEA vehicle registration statistics, EEA emissions and policy trackers, and UNECE vehicle safety regulations, helped us keep the market tied to real vehicle output and compliance-driven content.

We also reviewed company annual reports, investor decks, and reputable press coverage to understand how seat content per vehicle is changing (comfort, electronics, lightweighting, and recycled materials) and how OEM programs shift between platforms. In a few places, paid subscriptions for company financials and patent databases were used to confirm supplier footprint, technology direction, and timing of platform launches. These examples are not exhaustive, and many other public and paid sources were checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually shipped and paid for in Europe, and on removing assumptions that could not be supported by public data. We spoke with a mix of seat system suppliers, material providers, aftermarket participants, and OEM-aligned experts across major European auto hubs, and used their input to pressure-test volumes, price movement, and content changes by vehicle class.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | |

| Mid tier: 49% | Functional/Unit leaders: 38% | |

| Smaller Players: 14% | Managers: 50% |

Market-Sizing & Forecasting

The core sizing logic starts with a top-down build where Europe vehicle production and registration signals are reconstructed into a seat demand pool, and then translated into value using seat content assumptions and average selling price movement. To keep the totals realistic, we ran selective bottom-up checks using sampled supplier revenue splits, channel checks for aftermarket replacement, and simple volume times ASP calculations for representative seat types.

Inputs that mattered in the model included passenger car versus commercial vehicle mix, OEM build schedules by country, seat technology mix (standard versus powered and ventilated features), upholstery and foam material shifts, and the OEM versus aftermarket share trend, which is affected by vehicle parc aging and e-commerce refurbishment. Where gaps exist, for example when supplier revenue is reported at a broader interior level, allocations were derived using interview-based share ranges and then re-checked against vehicle output and feature penetration.

For forecasting, scenario analysis was used to reflect how vehicle production cycles, electrification program ramp-ups, and material cost pass-through could move the outcome. Assumptions were updated only after they were supported by at least two independent signals, typically one public series and one primary confirmation, and then we moved to year-by-year projections through the stated forecast window.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, and then reviewed for unusual jumps by country, vehicle type, and channel before sign-off. If an implied ASP or penetration rate moved beyond what interviews and public series support, we rechecked the underlying driver and, when needed, went back to sources for clarification.

A second analyst review step was used to confirm arithmetic, scope application, and year alignment, including currency timing and inflation treatment. Reports are refreshed annually, with interim updates triggered by material events such as sharp vehicle production resets, major regulation changes, or sudden input cost shocks. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Europe Automotive Seat Market Size Versus Other Published Estimates

Published market sizes for Europe automotive seats can differ even when the topic name looks the same, because each publisher draws the line around what counts as a seat and what gets counted as a seat-related interior item. Timing also plays a role, since different base years are used and not everyone updates production and pricing assumptions after major vehicle build revisions.

The main gap usually comes from whether aftermarket refurbishment and replacement are counted, and whether value is captured at the full seat system level or diluted into broader interior modules, which changes the implied ASP per vehicle. Some estimates also apply a single Europe-wide price trend, while others adjust by country mix and technology penetration, and then convert currencies using different averaging windows, which can shift the stated USD value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.81 B (2025) | |

| Regional Consultancy A | USD 13.01 B (2022) | Uses an older base year and a narrower value capture that leans on earlier vehicle volumes, with limited normalization for the later shift toward powered and ventilated seat penetration. |

| Trade Journal B | USD 10.00 B (2024) | Reported as an approximate value and often treated as seating materials and assemblies, which can exclude full seat system content and understate OEM program driven ASP increases. |

The table shows that year selection and what is counted inside the seat system are the biggest drivers of spread, followed by how technology mix is priced into the model. By tying volumes to Europe vehicle output and then updating penetration and ASP assumptions through validation checks and recent refreshes, a clearer seat system-only view is maintained, which is a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the European automotive seat market?

The European automotive seat market size is USD 16.45 billion in 2026, projected to reach USD 20.07 billion by 2031.

How fast is the market growing?

The market is expanding at a 4.06% CAGR from 2026 to 2031, driven by electrification, safety regulations, and sustainability initiatives.

Which material segment leads revenue?

Synthetic PU leather commands 43.02% revenue share, benefiting from cost efficiency and design flexibility.

Which seat technology is growing the fastest?

Due to EU safety mandates, smart ADAS-integrated seats hold the highest growth outlook at a 4.15% CAGR.

How dominant are OEM channels versus the aftermarket?

OEM programs account for 86.95% of sales, but online aftermarket platforms are the fastest-growing channel at a 4.16% CAGR.

What is the primary restraint affecting suppliers?

Volatile polyurethane and leather input costs and semiconductor shortages compress margins and stretch lead times.

Page last updated on: