Automotive Over-the-Air Updates Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 4.78 Billion |

| Market Size (2030) | USD 11.23 Billion |

| Growth Rate (2025 - 2030) | 18.63% CAGR |

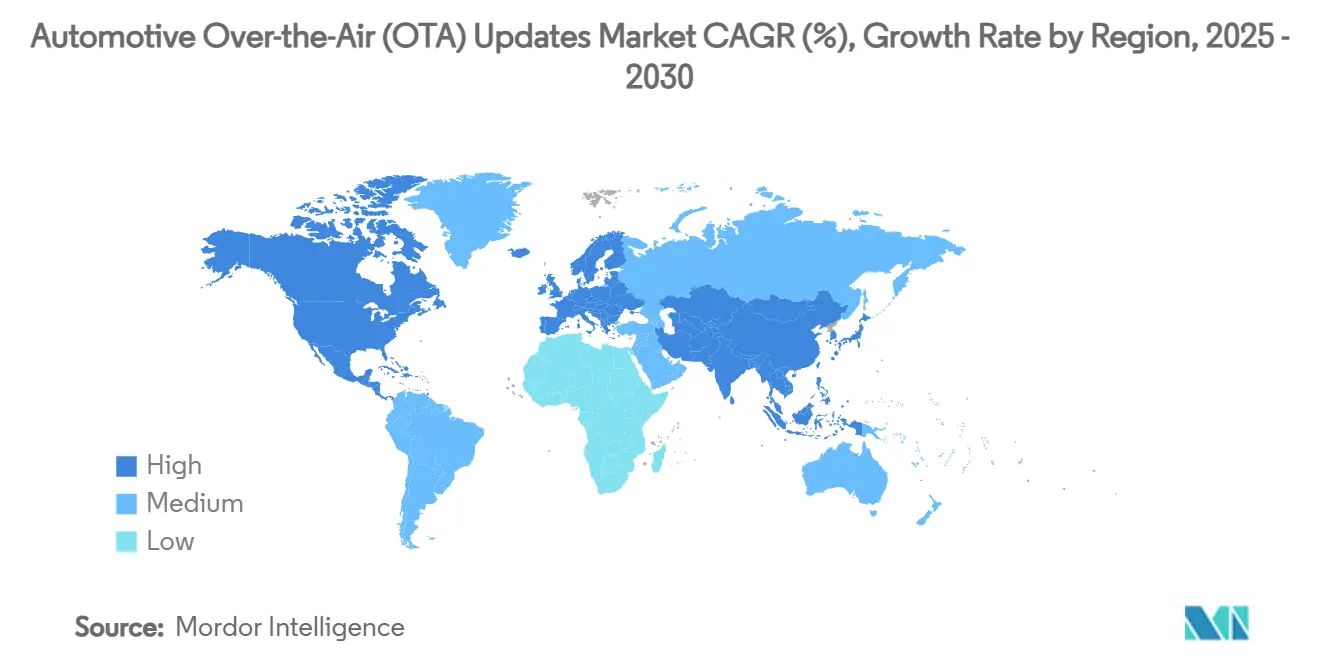

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

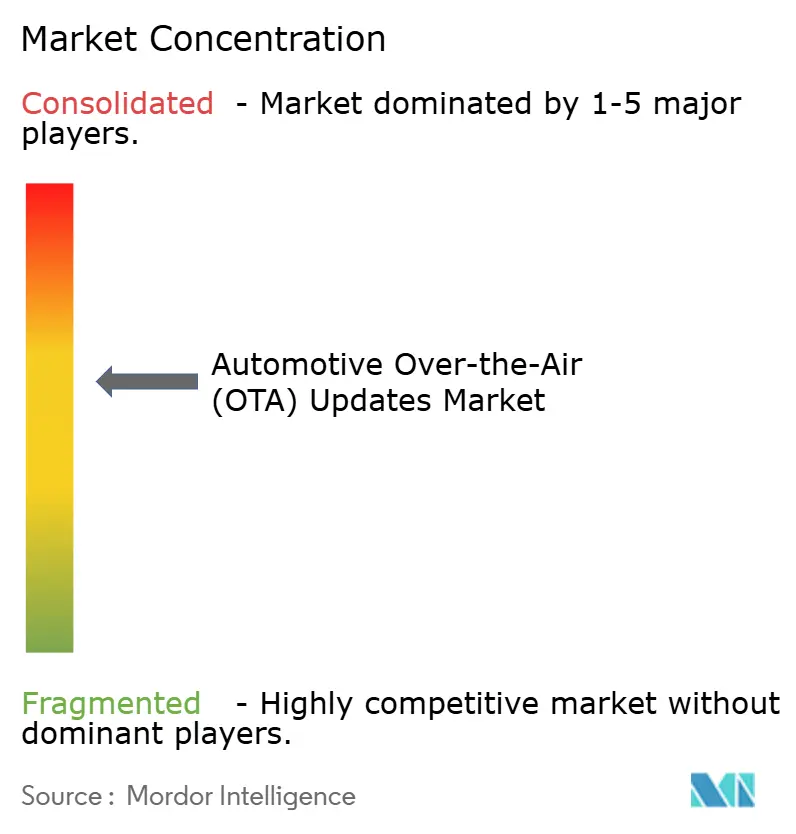

| Market Concentration | Medium |

Major Players-updates-market/automotive-over-the-air-(ota)-updates-market-1753246043456-major-players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

-updates-market/automotive-over-the-air-ota-updates-market-size-image-1753246111780.webp)

Automotive Over-the-Air Updates Market Analysis by Mordor Intelligence

The Automotive Over-the-Air Updates market size stands at USD 4.78 billion in 2025 and is projected to reach USD 11.23 billion by 2030 at a 18.63% CAGR. This expansion mirrors the sector’s pivot toward software-defined vehicle architectures that demand frequent remote updates for safety, performance, and feature optimisation [UL.COM]. Increased regulatory scrutiny, mounting cybersecurity requirements, and consumer demand for connected experiences combine to fuel rapid platform rollouts. Original equipment manufacturers invest in secure update pipelines to curb physical recall costs and to accelerate feature deployment. Telecom operators strengthen 5G coverage, while satellite players address remote gaps, ensuring reliable update delivery. Convergence of electric propulsion, cloud-native diagnostics, and subscription revenue models opens new revenue pools across the value chain.

Key Report Takeaways

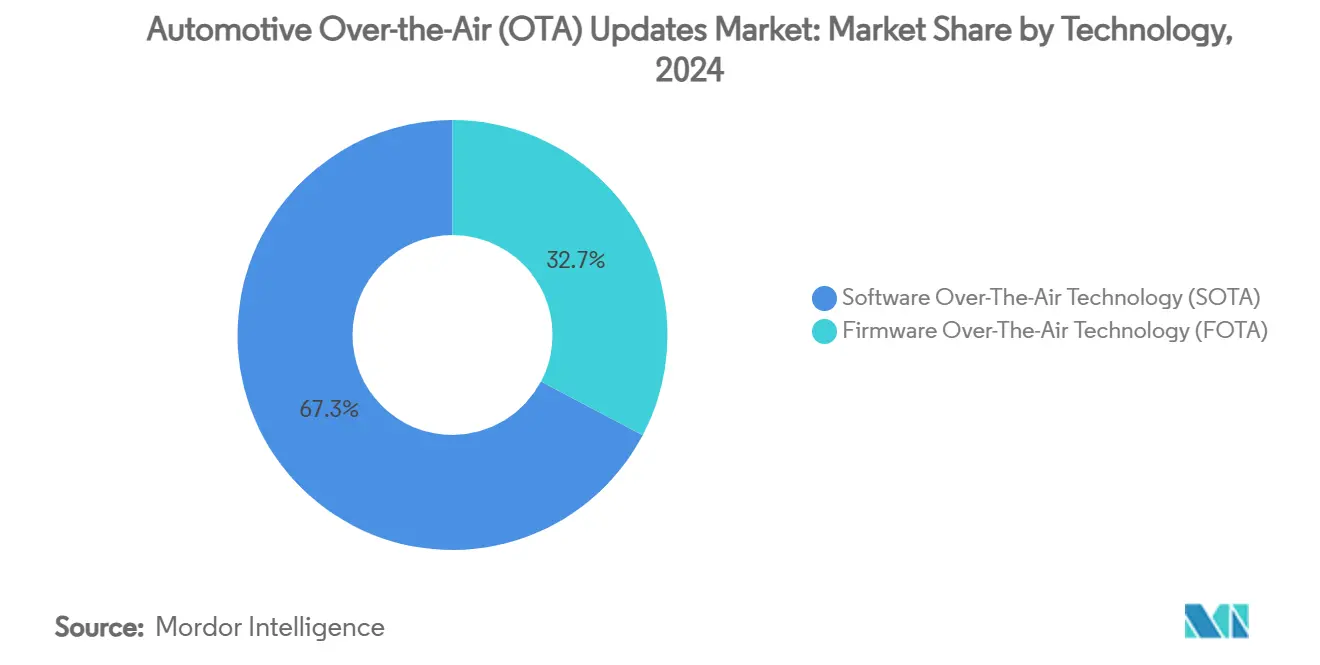

- By technology, Software Over-the-Air commanded 67.29% revenue share in 2024; Firmware Over-the-Air is advancing at a 24.87% CAGR to 2030.

- By application, telematics control units held 34.17% of the Automotive Over-the-Air Updates market share in 2024, while safety and security software is growing at a 22.32% CAGR through 2030.

- By propulsion, internal combustion vehicles accounted for 74.65% of the Automotive Over-the-Air Updates market size in 2024; battery electric vehicles are set to expand at a 29.42% CAGR between 2025 and 2030.

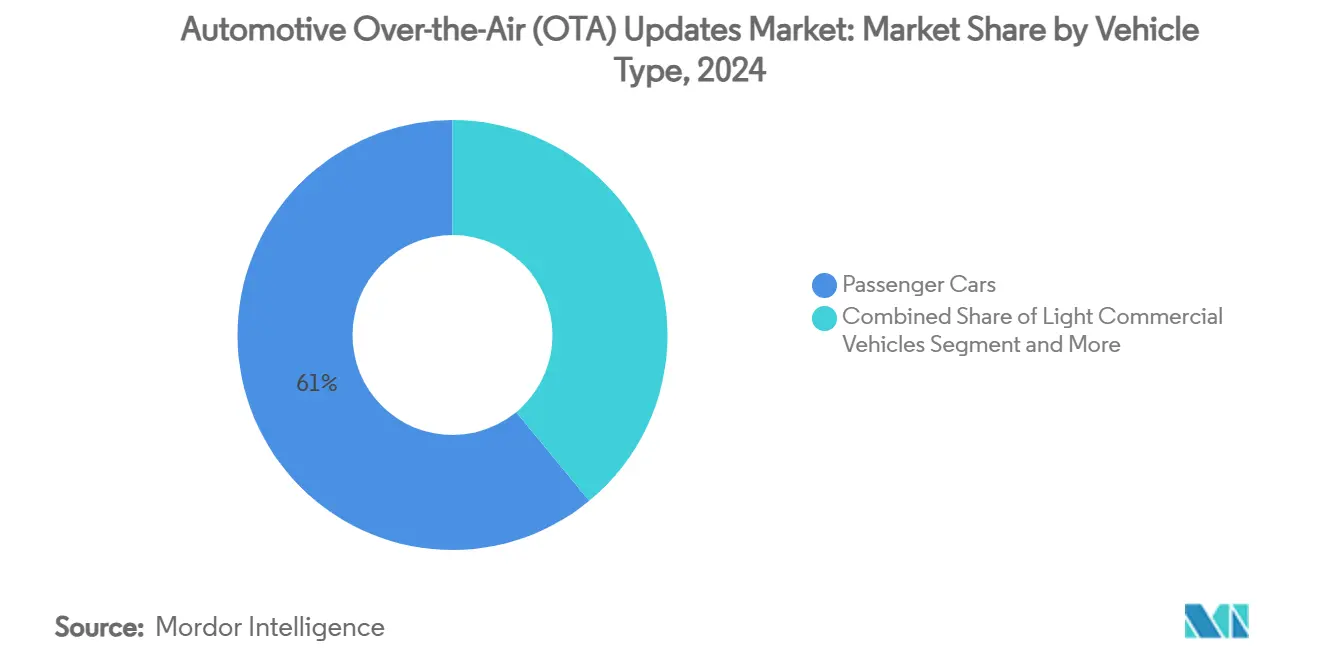

- By vehicle type, passenger cars led with 60.98% revenue share in 2024 and are progressing at a 20.31% CAGR to 2030.

- By communication type, cellular connectivity captured 69.35% of the Automotive Over-the-Air Updates market size in 2024; satellite communication is registering the fastest 26.39% CAGR to 2030.

- By geography, north America led with a 43.11% market share in 2024, while Asia-Pacific is expected to register the fastest CAGR of 18.92% through 2030.

Global Automotive Over-the-Air Updates Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification And SDV Updates | +4.3% | Global, with early gains in China, Europe, North America | Long term (≥ 4 years) |

| Safety-Recall and Cyber-Security Compliance | +3.2% | Europe, North America, Japan, South Korea | Medium term (2-4 years) |

| Connected-Car and Telematics Penetration | +2.8% | Global | Short term (≤ 2 years) |

| Feature-As-A-Service Monetization | +2.1% | North America, Europe, spill-over to APAC | Medium term (2-4 years) |

| OTA Off-Load Via EV-Charging Hubs | +1.9% | North America, Europe, China | Long term (≥ 4 years) |

| Satellite-based Remote OTA Delivery | +1.4% | Global, with early gains in rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification and SDV Architectures Demanding Frequent Updates

Electric and software-centric vehicles rely on centralised electronic and electrical architectures that simplify over-the-air delivery. Centralisation cuts physical recall costs and supports rapid feature rollouts, turning vehicles into upgradeable digital platforms. Code lines in a modern vehicle now exceed 100 million, and remote patching ensures resilience, performance, and regulatory compliance throughout the lifecycle. Continuous integration models let manufacturers iterate navigation, battery management, and autonomous modules without dealer visits, reinforcing brand differentiation at every software release[1]HARMAN Automotive, “HARMAN Automotive Over-The-Air Solutions,” HARMAN, car.harman.com.

Regulatory Push on Safety-Recall and Cyber-Security Compliance

Since July 2024, UNECE regulations require every newly approved vehicle in regulated markets to feature a certified software update management system. Automakers must document secure pipelines, audit risk mitigation, and maintain incident response mechanisms for the full product life. Compliance accelerates investment in cryptographic signing, secure boot, and rollback capabilities, rewarding firms with mature security frameworks and penalising those with fragmented legacy stacks.

Widespread Connected-Car and Telematics Penetration

Global connected-car shipments continue to climb as embedded 4G and 5G modules transition from premium to mainstream trims. Expanded bandwidth empowers high-resolution infotainment, situational awareness, and cloud analytics. Commercial fleets integrate predictive diagnostics to trim downtime and fuel bills, anchoring update infrastructure as a revenue-generating asset for telecommunications partners.

Feature-as-a-Service Monetization Models for OEMs

Manufacturers increasingly embed dormant hardware and unlock functions via paid software keys. Subscriptions for advanced lighting, ride-control, and driver-assist modules create dependable cash flows beyond initial sale. Success hinges on intuitive pricing, transparent value propositions, and friction-less in-vehicle commerce. Over-the-air activation shortens time-to-market and avoids hardware retrofit, enhancing return on investment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Security and Data-Privacy | -1.8% | Global | Short term (≤ 2 years) |

| Fragmented Software Stacks | -1.2% | North America, Europe, established OEMs globally | Medium term (2-4 years) |

| High Cloud Bandwidth Cost | -0.9% | APAC emerging markets, South America, Africa | Medium term (2-4 years) |

| Slow Multi-Brand Certification | -0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security and Data-Privacy Vulnerabilities

As vehicular connectivity rises, malicious actors target update channels. Secure signing, end-to-end encryption, and multi-layer validation are vital to prevent firmware tampering or man-in-the-middle attacks. Adoption of frameworks such as Uptane bolsters resilience but requires investment in secure hardware modules, raising short-term costs[2]Mohamed A. et al., “Threat Classification and Vulnerability Analysis on 5G Firmware Over-the-Air Updates for Mobile and Automotive Platforms,” Electronics, mdpi.com. Consumer resistance to data collection practices, exemplified by FTC scrutiny over General Motors' data monetization strategies, creates additional compliance burdens that slow OTA adoption rates.

Legacy ECU Architectures and Fragmented Software Stacks

Older distributed architectures with more than 100 microcontrollers complicate holistic patch management. Integration of secure gateways and domain controllers mitigates fragmentation but demands capital outlays and expertise. Many incumbent manufacturers maintain dual pipelines, one for older variants and another for next-generation platforms, diluting scale benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: SOTA Dominance Drives Current Revenue

Software Over-the-Air updates hold 67.29% share, anchored by infotainment and app-layer patches that influence user experience. Continuous refinement of navigation, voice assistants, and energy-management algorithms keeps vehicles relevant after sale. Firmware Over-the-Air accelerates at a 24.87% CAGR as regulation compels secure updates to powertrain, braking, and driver-assist controllers. Feature-rich electronics and rising electric vehicle penetration broaden the firmware opportunity window.

Automotive Over-the-Air Updates market size for Firmware Over-the-Air is set to expand steadily, closing the gap with Software Over-the-Air through 2030. Manufacturers standardise update packages across global regions, cutting engineering workload and enhancing compliance. As the industry shifts towards software-defined vehicles, the technology segmentation underscores the growing importance of continuous software updates.

By Application: TCU Leadership Faces Safety Disruption

Telematics control units integrate cellular modems, GNSS, and secure elements, giving them a 34.17% slice of 2024 revenue. Predictive maintenance, remote diagnostics, and fleet analytics underpin their appeal. Safety and security software rises at a 22.32% CAGR as over-the-air patches address vulnerabilities and refine driver-assist algorithms.

The Automotive Over-the-Air Updates market share of safety software is forecast to widen, with automakers embedding intrusion detection and response logic that updates autonomously. Infotainment applications benefit from consumer demand for enhanced in-vehicle experiences and smartphone integration capabilities, yet face commoditisation as smartphone mirroring frameworks gain ubiquity.

By Propulsion: ICE Dominance Yields to EV Innovation

Internal combustion vehicles remain the largest installed base, commanding 74.65% share, but electric models lead growth due to software-centric architectures. Automotive Over-the-Air Updates market size for electric platforms is poised for a 29.42% CAGR. Software governs battery conditioning, regenerative braking, and rapid charging protocols, making remote optimisation indispensable.

Hybrid and plug-in hybrid systems represent transitional segments that leverage dual control pathways, benefitting from both combustion and electric powertrain optimization through software updates.. Centralised controllers reduce complexity and trim wiring, easing mass-update execution. In 2025, smarter ICE vehicles with OTA updates are set to capture a larger market share.

By Vehicle Type: Passenger Cars Lead Across Metrics

Passenger cars represent 60.98% slice and log the strongest 20.31% CAGR as consumers embrace connected experiences. Personalisation, gaming, and driver-assist upgrades spur repeat revenue. Light commercial fleets adopt telematics-driven updates to cut fuel usage and maximise uptime, while heavy trucks integrate predictive powertrain updates tailored to duty cycles.

The passenger car dominance reflects consumer willingness to pay for software-enhanced features, as evidenced by BMW's subscription model success for adaptive headlights and suspension systems. Automotive Over-the-Air Updates market size for commercial vehicles rises steadily as logistics operators align with zero-emission mandates and demand predictive diagnostics.

By Communication Type: Cellular Supremacy Faces Satellite Challenge

Cellular communication (3G/4G LTE/5G) remains dominant at 69.35% because of ubiquitous coverage and low module costs. eSIM adoption eases global roaming and update scheduling. Satellite connectivity grows 26.39% annually, filling coverage gaps along shipping routes, deserts, and rural highways. Kymeta aggressively targets civilian armored vehicles, collaborating with Toyota to provide satellite-based updates in areas beyond cellular coverage.

While Wi-Fi, Dedicated Short-Range Communication, and Vehicle-to-Everything technologies cater to niche applications, they occupy relatively modest market segments. Wi-Fi complements high-bandwidth, low-mobility updates in residential garages and public chargers, while vehicle-to-everything protocols handle localised micro-patches for cooperative safety.

Geography Analysis

North America retains 43.11% share owing to early electric vehicle uptake, robust telecom infrastructure, and well-defined cybersecurity frameworks. Regional CAGR of 17.2% reflects transition from standalone features to integrated digital ecosystems. Government investments in charging corridors extend automated update channels beyond city clusters.

Asia-Pacific records the fastest 18.92% CAGR through 2030. China’s electric vehicle boom and domestic software expertise propel large-scale update deployments. Indian manufacturers accelerate born-electric programmes with bundled update platforms. Japan and South Korea enforce stringent security rules that encourage adoption among local automakers.

Europe grows at 16.01% CAGR on the back of regulatory mandates and supplier innovation. Scalable update frameworks allow premium brands to introduce prototype-to-production cycles within months, raising competitive stakes. South America and the Middle East & Africa trail but see rising investments in connected infrastructure and green mobility that boost update demand.

Competitive Landscape

Industry concentration is moderate. Several multinational groups follow with double-digit positions powered by internal software platforms and strategic alliances. Tier-1 suppliers supply modular stacks that integrate cyber-security, campaign management, and delta-compression, accelerating time-to-market for legacy brands.

To close capability gaps, incumbent manufacturers forge high-value alliances with technology specialists. Volkswagen and Rivian established a multi-billion-dollar joint venture that pools intellectual property for next-generation electric platforms featuring native update support. Continental created the Aumovio brand to separate its software-defined vehicle assets, giving automakers an integrated stack that spans vehicle operating systems, update orchestration, and cyber-security compliance.

Start-ups specialise in lightweight, hardware-agnostic update clients that meet stringent safety norms, offering cost-effective entry points for mid-tier manufacturers. Cross-industry consortia define interoperable protocols, reducing vendor lock-in and supporting multi-brand service centres. Telecom providers and cloud hyperscalers bundle connectivity, edge processing, and analytics to capture recurring platform fees.

Automotive Over-the-Air Updates Industry Leaders

Tesla, Inc.

Volkswagen AG

General Motors Co.

Hyundai Motor Group

Toyota Motor Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hyundai enabled Plug-and-Charge authentication via over-the-air update for the 2025 Ioniq 5 lineup.

- January 2025: Rivian and Volkswagen launched a USD 5.8 billion joint venture to co-develop electric platforms with native over-the-air capabilities, aiming for first models in 2027.

- September 2024: Volvo issued a remote update to 2.5 million vehicles, expanding infotainment functionality and energy-management algorithms.

- June 2024: HARMAN released OTA 12.0, adding distributed onboard orchestration and larger image support for more than 40 global automakers.

Global Automotive Over-the-Air Updates Market Report Scope

| Software Over-The-Air Technology (SOTA) |

| Firmware Over-The-Air Technology (FOTA) |

| Electronic Control Unit (ECU) |

| Infotainment |

| Safety and Security |

| Telematics Control Unit (TCU) |

| Others |

| Internal Combustion Engine (ICE) | |

| Electric Vehicle | Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) | |

| Plug-In Hybrid Electric Vehicle (PHEV) |

| Passenger Car |

| Light Commercial Vehicle |

| Heavy Commercial Vehicle |

| Cellular (3G, 4G LTE, 5G) |

| Wi-Fi |

| Satellite |

| Dedicated Short-Range Communication (DSRC) |

| Vehicle-to-Everything (V2X) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Software Over-The-Air Technology (SOTA) | |

| Firmware Over-The-Air Technology (FOTA) | ||

| By Application | Electronic Control Unit (ECU) | |

| Infotainment | ||

| Safety and Security | ||

| Telematics Control Unit (TCU) | ||

| Others | ||

| By Propulsion | Internal Combustion Engine (ICE) | |

| Electric Vehicle | Battery Electric Vehicle (BEV) | |

| Hybrid Electric Vehicle (HEV) | ||

| Plug-In Hybrid Electric Vehicle (PHEV) | ||

| By Vehicle Type | Passenger Car | |

| Light Commercial Vehicle | ||

| Heavy Commercial Vehicle | ||

| By Communication Type | Cellular (3G, 4G LTE, 5G) | |

| Wi-Fi | ||

| Satellite | ||

| Dedicated Short-Range Communication (DSRC) | ||

| Vehicle-to-Everything (V2X) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Automotive Over-the-Air Updates market?

The market stands at USD 4.78 billion in 2025 and is forecast to hit USD 11.23 billion by 2030.

Which technology segment leads the market?

Software Over-the-Air holds 67.29% revenue share, reflecting its critical role in user-facing updates.

Why are battery electric vehicles important for over-the-air updates?

Battery electric vehicles use centralised architectures that rely on frequent software refinements, driving a 29.42% CAGR for OTA revenue in this propulsion class.

How does regulation influence market growth?

UNECE cybersecurity and software-update rules oblige automakers to implement robust remote update systems, adding 3.2% to forecast CAGR.

What communication method is growing fastest for OTA delivery?

Satellite connectivity is expanding at 26.39% CAGR, complementing cellular networks in remote regions.

Which region shows the highest growth potential?

Asia-Pacific leads with an 18.92% CAGR as electric vehicle adoption and domestic software capabilities surge.

Page last updated on: