Automotive E-Compressor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

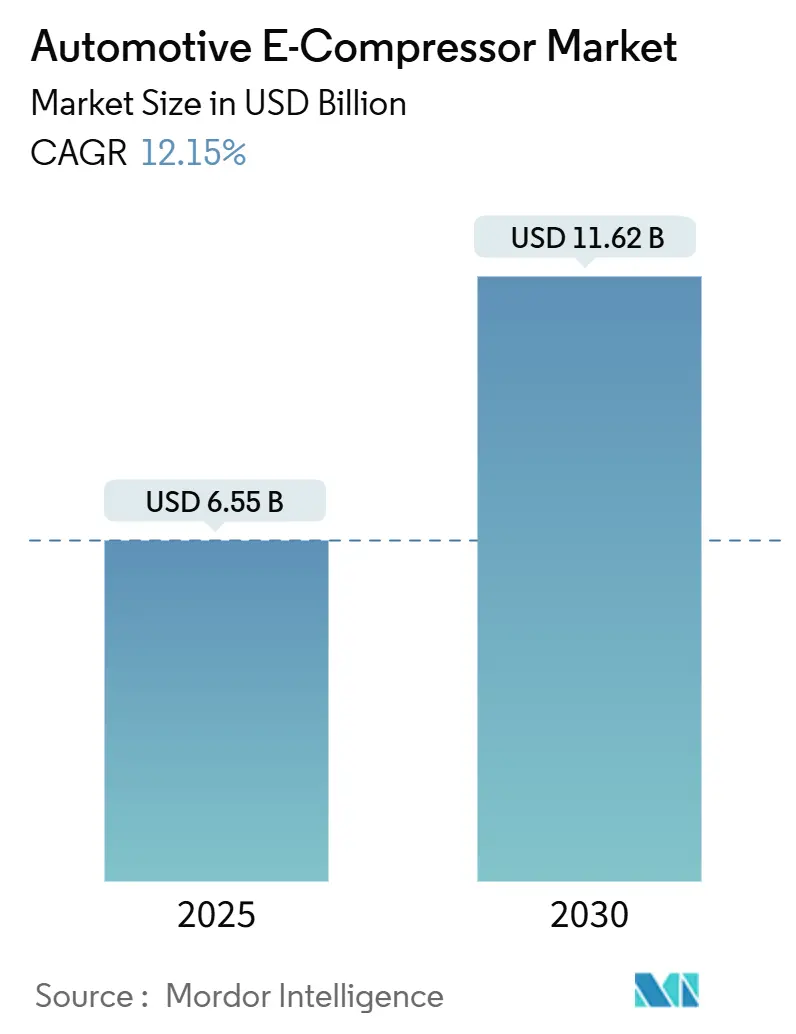

| Market Size (2025) | USD 6.55 Billion |

| Market Size (2030) | USD 11.62 Billion |

| Growth Rate (2025 - 2030) | 12.15% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive E-Compressor Market Analysis by Mordor Intelligence

The Automotive E-Compressor Market size is estimated at USD 6.55 billion in 2025, and is expected to reach USD 11.62 billion by 2030, at a CAGR of 12.15% during the forecast period (2025-2030). Accelerated electrification, rapid heat-pump adoption, and stricter refrigerant rules are expanding the automotive e-compressor market across battery electric, plug-in hybrid, and hybrid platforms. Scroll technology efficiency gains, 800 V vehicle architectures, and rising demand for quiet NVH profiles further strengthen growth prospects. Suppliers are localizing manufacturing outside East Asia to hedge geopolitical risk, while OEM cost-reduction mandates continue to squeeze margins. Government incentives, such as the U.S. Inflation Reduction Act, reinforce investment in regional production, improving supply resilience and shortening lead times.

Key Report Takeaways

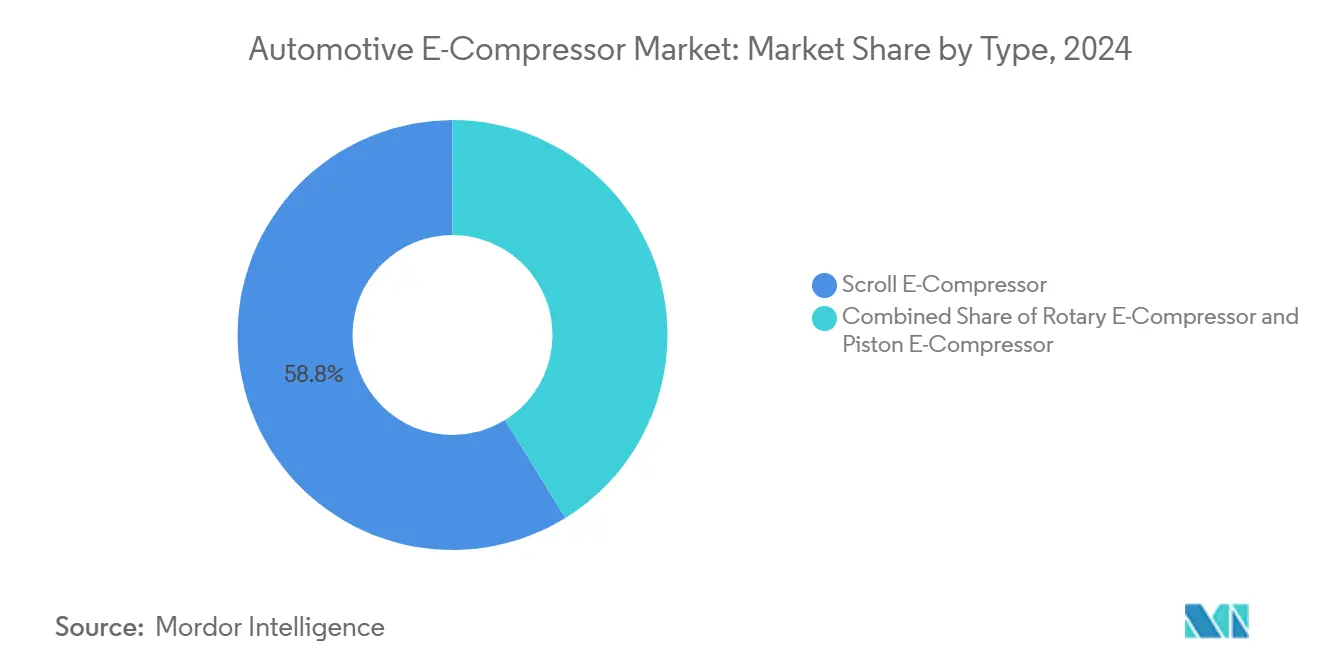

- By type, scroll compressors captured 58.81% of the automotive e-compressor market share in 2024, whereas rotary compressors are projected to expand at a 12.17% CAGR during the forecast period (2025-2030).

- By application, air-conditioning accounted for 46.73% of the automotive e-compressor market size in 2024, while the thermal management systems segment is projected to grow at a 12.27% CAGR during the forecast period (2025-2030).

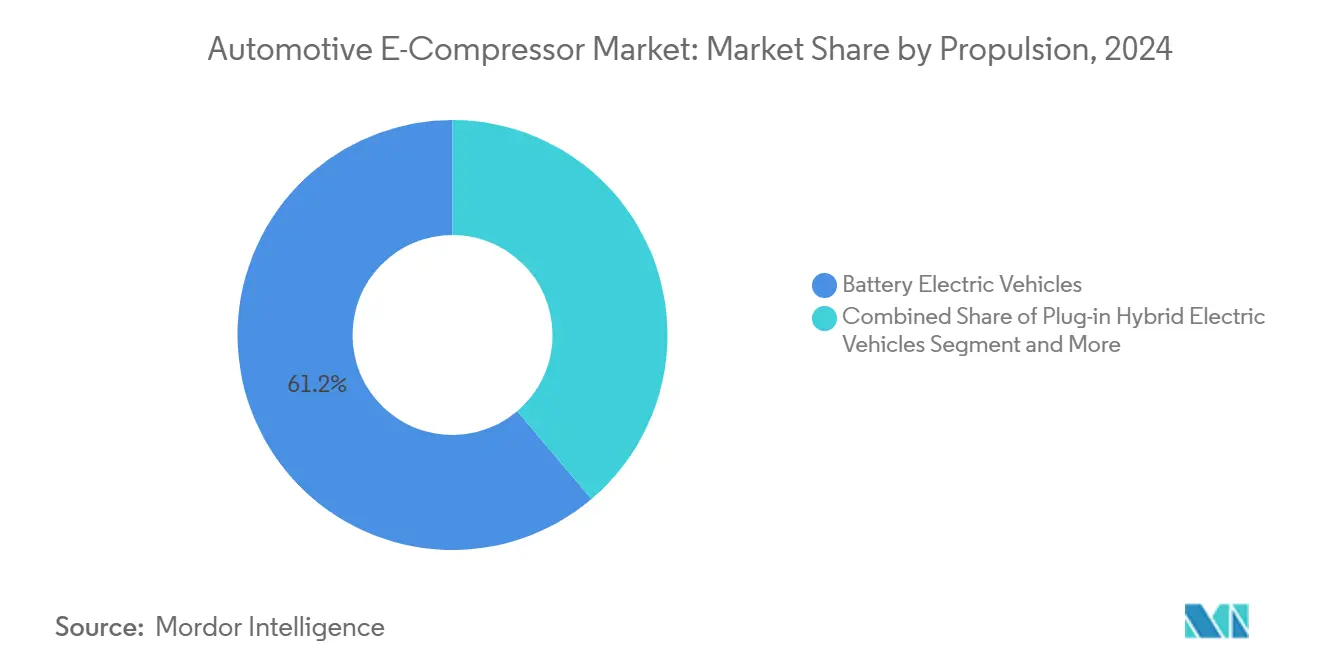

- By propulsion, battery electric vehicles held 61.22% of the automotive e-compressor market size in 2024, and the same segment is projected to grow at a 12.19% CAGR during the forecast period (2025-2030).

- By vehicle type, passenger cars dominated with 58.74% revenue share in 2024; the medium and heavy commercial vehicles segment is projected to grow at a CAGR of 12.25% during the forecast period (2025-2030).

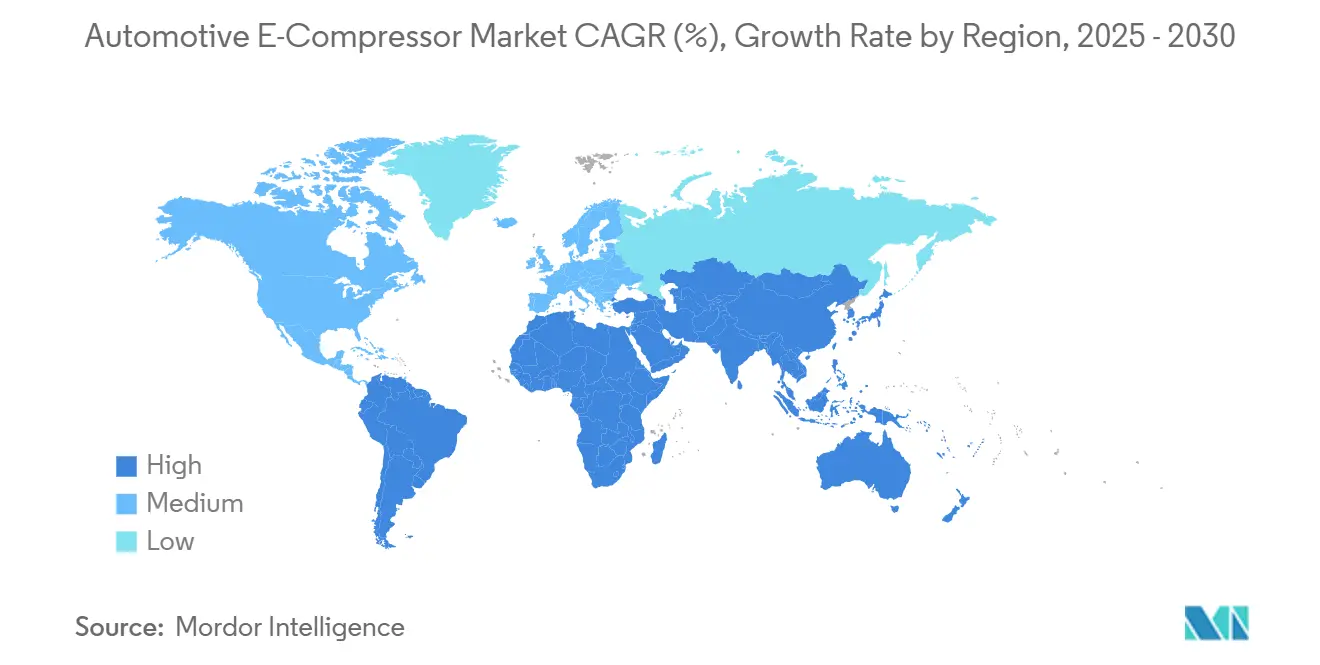

- By region, Asia-Pacific led with 38.73% revenue share in 2024, while Middle East and Africa is forecast to expand at 12.22% CAGR during the forecast period (2025-2030).

Global Automotive E-Compressor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising BEV & PHEV Production Volumes | +3.2% | Global, with Asia Pacific leading | Medium term (2-4 years) |

| Shift To Heat-Pump HVAC Architectures In EVs | +2.8% | North America and EU primarily | Long term (≥ 4 years) |

| Stricter GWP and PFAS Refrigerant Regulations | +2.1% | Global, EU and North America leading | Short term (≤ 2 years) |

| 800V Vehicle Platforms Needing High-Speed E-Compressors | +1.8% | Global, early adoption in premium segments | Long term (≥ 4 years) |

| Demand For Quieter NVH Profiles In Premium EVs | +1.4% | North America, EU, premium Asia Pacific markets | Medium term (2-4 years) |

| Fleet Electrification Of Buses and Off-Highway Machinery | +1.2% | Asia Pacific core, spill-over to North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising BEV & PHEV Production Volumes

Battery electric and plug-in hybrid output is scaling quickly, and every new electrified platform requires an electric compressor because engine-driven units are no longer viable. The U.S. Department of Energy projects a high domestic fleet of plug-in vehicles by 2032, placing sustained volume pressure on e-compressor suppliers. Economies of scale are lowering unit costs, yet OEMs now seek closer collaboration to optimize integration, shifting revenue toward upfront development contracts. Commercial vehicles deepen the opportunity by demanding larger capacity units with longer duty cycles. Fleet operators focus on total cost of ownership, rewarding suppliers that balance efficiency with long-life reliability. As production widens, aftermarket sales give way to direct OEM fitment, reshaping distribution channels and strengthening tier-1 relationships.

Shift to Heat-Pump HVAC Architectures in EVs

Heat pumps offer reversible cooling and heating, boosting winter range but raising compressor complexity. Ford’s 2024 patent filing for propane R290 heat-pump systems underscores the move toward flammable refrigerants that require sealed, variable-speed scroll or rotary technology [1]“Ford Applies for Propane Refrigerant Patent,” Ford Motor Company, ford.com. New designs must handle bidirectional flow, wide pressure ratios, and advanced software that syncs cabin, battery, and powertrain loops. European OEMs lead adoption, driven by cold-climate efficiency mandates. Suppliers who co-develop integrated thermal modules gain a defensive moat, as validation cycles are lengthy and platform specific. As heat pumps become standard on high-volume models from 2027 onward, the automotive e-compressor market will see a pivot toward multi-loop control capability and more expansive operating windows.

Stricter GWP & PFAS Refrigerant Regulations

EU Directive 2006/40/EC and updated EPA rules cap mobile refrigerant GWP at 150, forcing a shift to R1234yf, CO2, or natural options [2]“Directive 2006/40/EC relating to emissions from air-conditioning systems in motor vehicles,” European Parliament, europa.eu. Compressor internals, lubrication chemistry, and sealing strategies need redesign to accommodate these fluids’ thermodynamic and chemical traits. Dual-refrigerant compatibility helps OEMs transition fleets during model-year overlaps, creating a premium for suppliers with broad test data. Certification complexity favors incumbents with accredited labs. As phase-out deadlines approach, OEMs lock procurement earlier, further consolidating demand among compliant manufacturers.

Demand for Quieter NVH Profiles in Premium EVs

Electric cars expose HVAC sounds without combustion noise, prompting luxury brands to specify near-silent compressors. Scroll designs meet this with continuous compression and fewer moving parts. TÜV SÜD’s high-voltage component certification programs reinforce the need for tightly balanced rotors and advanced damping mounts. Superior NVH allows automakers to promote cabin serenity, justifying a price premium. Segmentation emerges: high-end EVs choose quiet, high-efficiency scrolls, while cost-sensitive trims accept simpler rotary units. NVH leadership, thus, becomes a marketing differentiator and a margin lever for suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Unit Cost Versus Belt-Driven Compressors | -2.4% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Reliability Concerns Over Inverter Failures | -1.8% | Global, with higher impact in commercial applications | Medium term (2-4 years) |

| Supply-Chain Concentration In East Asia | -1.6% | Global, particularly affecting Western OEMs | Medium term (2-4 years) |

| Shortage Of Certified HVAC Technicians | -1.2% | Global, with higher impact in rapid EV adoption markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Unit Cost Versus Belt-Driven Compressors

Electric compressors, equipped with an inverter and a high-precision motor, command notably higher average street prices than their traditional belt-driven counterparts. In a 2025 EV price war, Chinese automakers demanded one-tenth supplier cost cuts, pressuring margins across the automotive e-compressor market. Manufacturers respond by automating scroll machining and vertically integrating electronics to absorb price erosion. Yet value arguments resonate where range gains translate into more miniature battery packs, offsetting upfront cost. Emerging economies remain sensitive, slowing penetration in entry-level hybrids despite long-term efficiency payback.

Reliability Concerns Over HV Inverter Failures

A failed inverter turns off HVAC entirely, and service centers often replace the whole assembly at significant expense. Light technician coverage for 400 V and 800 V systems magnifies downtime for fleet operators. Commercial duty cycles heighten stress, pushing suppliers to extend validation cycles, adopt redundant logic, and lengthen warranties. Training initiatives like Standard Motor Products’ 2025 high-voltage curriculum are slowly expanding repair capacity. Until perception catches up with real-world reliability, some buyers hesitate, trimming near-term adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Scroll Technology Leads Efficiency Drive

Scroll compressors controlled 58.81% of the automotive e-compressor market in 2024, owing to smooth, valve-less operation that lifts isentropic efficiency and reduces vibration. This dominance is expected to persist even as rotary designs post a 12.17% CAGR through 2030, attracted by compact footprints and lower tooling costs. Rotary units, meanwhile, will benefit from scaled production in China and capture new mini-EV platforms.

Manufacturing advances, such as MAPAL’s tighter tolerance boring solutions, further push scroll performance, ensuring continued preference in heat-pump applications where bidirectional flow and wide load modulation are critical. Rotary growth thrives where OEMs prioritize price over peak efficiency, particularly in sub-USD 25,000 EVs for emerging markets. Piston compressors keep a niche presence for high-pressure CO2 systems serving buses and refrigerated trucks. Dual-strategy sourcing is thus common: scroll for flagship trims, rotary for entry models, and piston for specialized commercial fleets.

By Application: Thermal Management Systems Gain Momentum

Air-conditioning represented 46.73% of the automotive e-compressor market in 2024, driven by universal cabin-cooling demand. Thermal management systems, integrating battery, inverter, and motor loops, are forecast to grow at 12.27% annually.

OEMs now pursue one-module solutions that house the e-compressor, chiller, and expansion valve, shrinking packaging and lowering refrigerant charge. Suppliers that co-design control software with vehicle ECUs gain stickiness because calibration is labor-intensive to replicate. Commercial refrigeration, although smaller, keeps steady revenue as grocers electrify delivery vans needing continuous cooling. As battery chemistries evolve, cell temperature windows tighten, further cementing compressor demand beyond simple occupant comfort.

By Propulsion: BEV Dominance Drives Market Growth

Battery electric vehicles accounted for 61.22% of the automotive e-compressor market in 2024, and the segment is projected to expand at a 12.19% CAGR. Pure EVs mandate electric compressors for every climate zone, unlike hybrids that sometimes retain mechanical backups. Plug-in hybrids still provide stable volume where charging infrastructure lags, but their share gradually tapers past 2028.

The automotive e-compressor market share for BEVs grows as zero-emission regulations tighten in Europe and China. North America sees a slower pivot, yet IRA tax credits accelerate domestic BEV output. PHEV designs, by contrast, push suppliers to develop dual-mode compressors tolerant of engine bay heat. As 800 V platforms proliferate, high-speed scrolls up to 14,000 rpm become standard, enabling smaller conductor sizes and faster DC fast-charge cycles.

By Vehicle Type: Commercial Vehicles Accelerate Adoption

Passenger cars led revenue with a 58.74% share in 2024, reflecting sheer volume. Medium and heavy trucks, however, are projected to post a 12.25% CAGR, the fastest within the automotive e-compressor market, as fleets electrify for urban delivery mandates. Class 7-8 tractors demand 10 kW-plus cooling loads and 24/7 duty, prompting suppliers to stress-test bearings and improve inverter thermal pads.

Regulatory tailwinds, such as California’s Advanced Clean Fleets rule, catalyze orders for high-capacity compressors. Light commercial vehicles bridge consumer and fleet requirements, adopting passenger-car hardware with upgraded duty cycles. Specialty off-highway machines and e-buses adopt dedicated CO2 compressors to meet extreme ambient temperature and safety requirements.

Geography Analysis

Asia-Pacific held 38.73% of the automotive e-compressor market in 2024, anchored by China’s EV leadership and dense supplier networks. Japanese makers like Denso and Mitsubishi Electric export high-precision scroll units worldwide, while Korean firms integrate strong power-electronics know-how. Despite cost advantages, geopolitical tensions cause Western OEMs to localize.

Europe sustains demand through tight CO₂ targets and early adoption of natural refrigerants, especially in Germany, France, and the Nordics. The region’s premium segment values low-noise scrolls, supporting higher ASPs. North America benefits from IRA incentives that spur factory groundbreakings in Tennessee and Michigan, while Mexico’s maquiladora corridor gains compressor sub-assembly work.

Middle East and Africa, though small, is the fastest-growing market at 12.22% CAGR, led by assembling plants in Morocco and South Africa that now import compressors but look to eventual local build. Latin America records steady expansion as Brazil’s bus electrification drives large-capacity CO₂ compressor uptake. Across regions, supply-chain resilience ranks high, driving multi-continental footprints despite cost premiums.

Competitive Landscape

The automotive e-compressor market is moderately fragmented, with the top five players estimated to hold nearly three-fifths collective revenue. Denso, Hanon Systems, Valeo, Mahle, and Sanden leverage legacy HVAC portfolios to supply integrated modules, while Garrett Motion, Sanhua, and Guchen carve niches through speed leadership and regional proximity. Consolidation is underway: Hankook & Company Group’s November 2024 bid for Hanon Systems illustrates tier-1 convergence, seeking scale in electrified thermal management [3]“Hankook Announces Plan to Acquire Hanon Systems Stake,” Hankook & Company Group, hankook.com.

Technology roadmaps revolve around higher-voltage readiness, natural-refrigerant compatibility, and software-defined control. Partnerships with automakers increasingly include joint labs to co-calibrate heat-pump logic, locking in multiyear supply contracts.

Chinese challengers offer cost-aggressive rotary units, especially for micro-EVs, pressuring incumbents on price. Western suppliers respond with North American or European factories that cut freight and mitigate tariff exposure, offsetting labor premiums via automation. Competitive intensity is expected to heighten through 2028 as volume surges and platform counts shrink, making design wins at leading OEMs pivotal.

Automotive E-Compressor Industry Leaders

Denso Corporation

Hanon Systems

Valeo S.A.

Mahle GmbH

Sanden International USA Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: At Auto Shanghai 2025, Garrett Motion showcased its E-Cooling Compressor, highlighting its 800 V capability tailored for next-generation EVs. This advanced compressor is designed to enhance thermal management systems, ensuring improved efficiency and performance in electric vehicles.

- March 2025: To enhance its precision compressor offerings for automotive clients, Atlas Copco has acquired Kyungwon, a compressor manufacturer based in Korea. This acquisition is expected to strengthen Atlas Copco's position in the automotive market by expanding its product portfolio and catering to the growing demand for advanced compressor solutions.

- December 2024: Mitsubishi Electric has established a factory in the United States for heat-pump compressors, bolstering its localized production for EV thermal management. This move aims to meet the growing demand for electric vehicle components in the region and ensure a more efficient and reliable supply chain. The facility will focus on producing advanced heat-pump compressors, critical in maintaining optimal thermal conditions in electric vehicles.

Global Automotive E-Compressor Market Report Scope

| Scroll E-Compressor |

| Rotary E-Compressor |

| Piston E-Compressor |

| Air-Conditioning Systems |

| Refrigeration Systems |

| Thermal Management Systems |

| Electric-Vehicle Heating Systems |

| Battery Electric Vehicles (BEVs) |

| Plug-in Hybrid Electric Vehicles (PHEVs) |

| Hybrid Electric Vehicles (HEVs) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Scroll E-Compressor | |

| Rotary E-Compressor | ||

| Piston E-Compressor | ||

| By Application | Air-Conditioning Systems | |

| Refrigeration Systems | ||

| Thermal Management Systems | ||

| Electric-Vehicle Heating Systems | ||

| By Propulsion | Battery Electric Vehicles (BEVs) | |

| Plug-in Hybrid Electric Vehicles (PHEVs) | ||

| Hybrid Electric Vehicles (HEVs) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size and projected growth rate of the automotive e-compressor space?

Global revenue reached USD 6.55 billion in 2025 and is slated to climb to USD 11.62 billion by 2030, equal to a 12.15% CAGR.

Which compressor technology holds the largest share today?

Scroll units lead with 58.81% share in 2024, due to high efficiency and low NVH, while rotary designs are expanding quickest at a 12.17% CAGR.

Which geographic region commands the highest sales?

Asia-Pacific accounted for 38.73% of worldwide revenue in 2024 because of dense manufacturing clusters in China, Japan, and South Korea.

Why are heat-pump HVAC systems boosting demand?

Heat pumps require reversible, high-efficiency electric compressors that can cool and heat, driving higher unit volumes and technical complexity for upcoming EV platforms.

How do 800 V vehicle architectures influence compressor design?

Higher bus voltages demand high-speed motors and inverters, prompting suppliers to engineer compressors that run efficiently at up to 14,000 rpm while trimming conductor weight.

Which companies are shaping competitive dynamics?

Denso, Hanon Systems, Valeo, Mahle, and Sanden anchor the field, while Garrett Motion and emerging Chinese makers intensify price and technology competition.

Page last updated on: