Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 27.13 Billion |

| Market Size (2031) | USD 37.54 Billion |

| Growth Rate (2026 - 2031) | 6.71% CAGR |

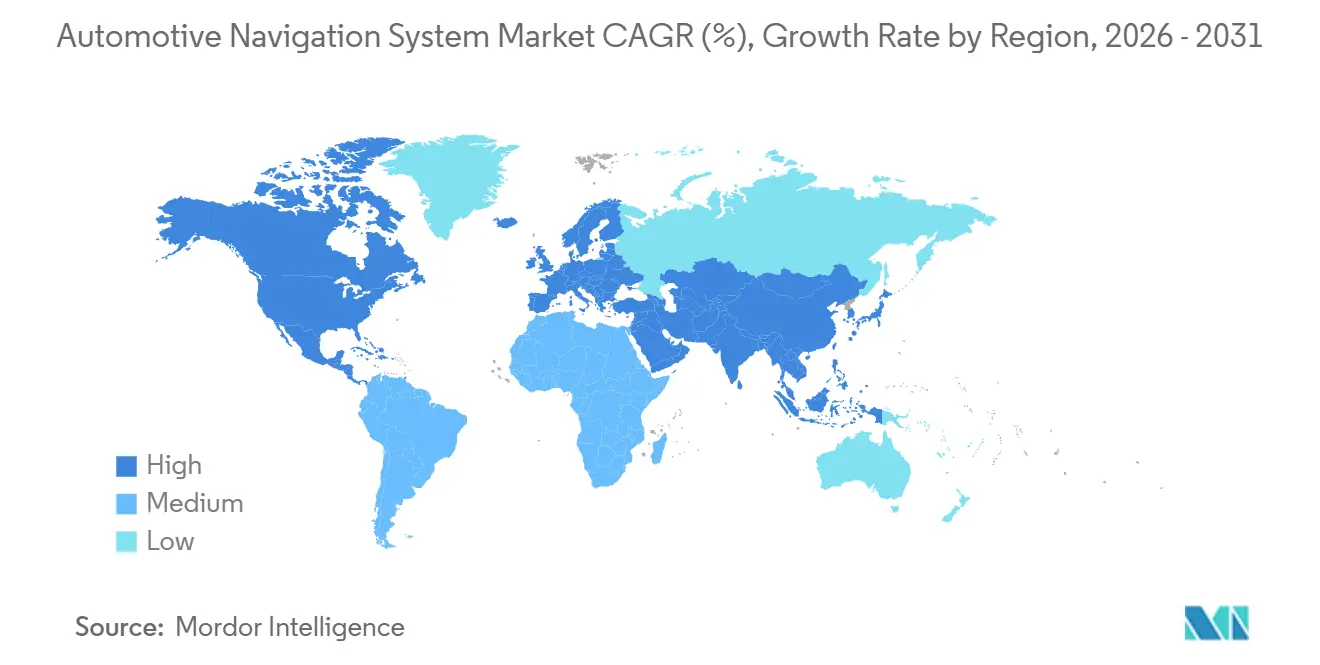

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

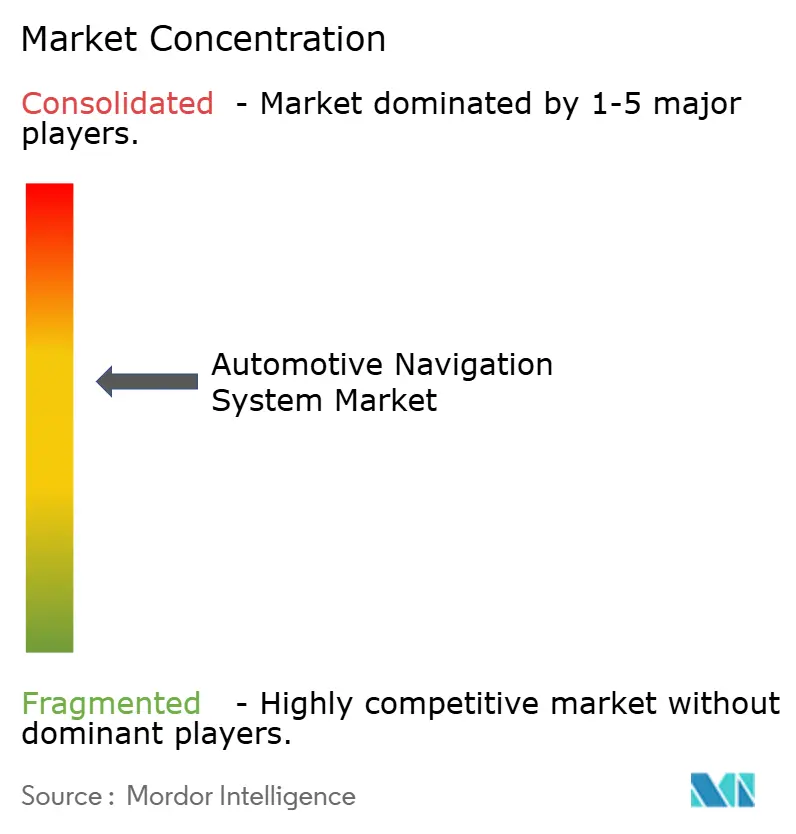

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Navigation System Market Analysis by Mordor Intelligence

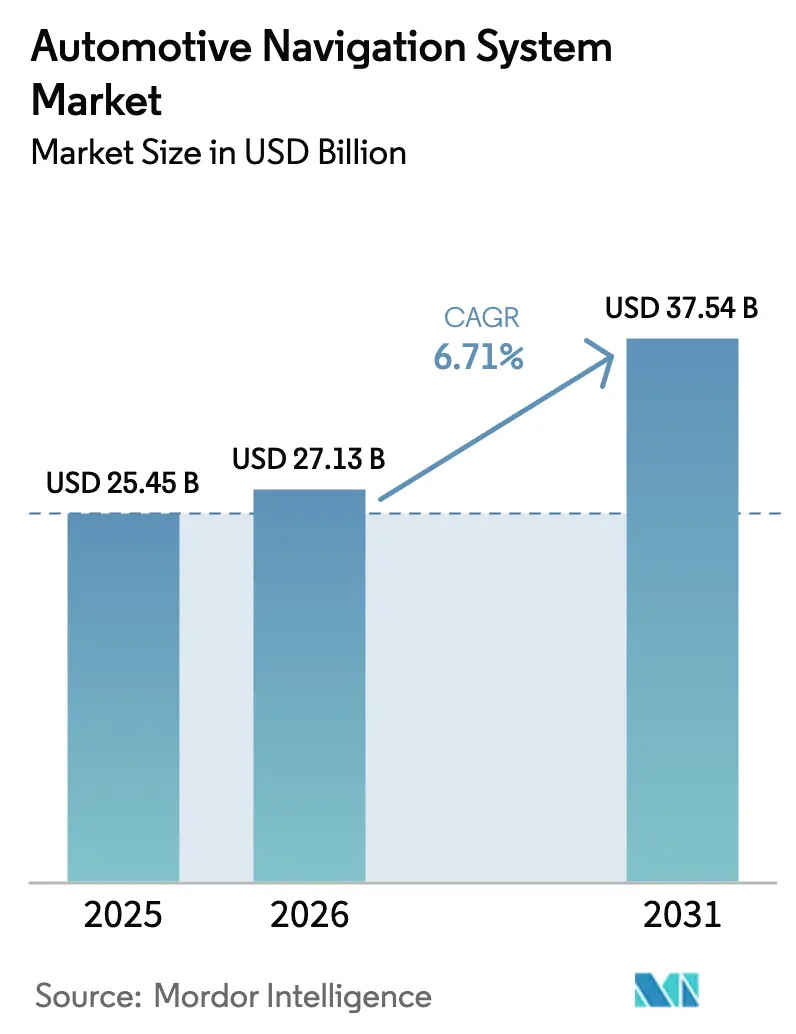

The automotive navigation system market is expected to grow from USD 25.45 billion in 2025 to USD 27.13 billion in 2026 and is forecast to reach USD 37.54 billion by 2031, growing at a 6.71% CAGR over the forecast period (2026-2031). The market's growth reflects three structural shifts: mandated e-Call and similar emergency regulations, mainstream adoption of factory-fitted infotainment units, and the rise of electric-vehicle-specific routing algorithms. The penetration of embedded connectivity modules continues to rise, enabling lane-level positioning that supports Level 2+ driver-assistance features. Meanwhile, subscription-based over-the-air (OTA) map updates are pivoting revenue toward services. Strategic dilemmas emerge because smartphone mirroring still captures almost half of user preference, forcing automakers to choose between proprietary stacks and tech-giant interfaces. Finally, accuracy gains from dual-frequency GNSS improve safety and automation potential, yet they heighten exposure to spoofing attacks.

Key Report Takeaways

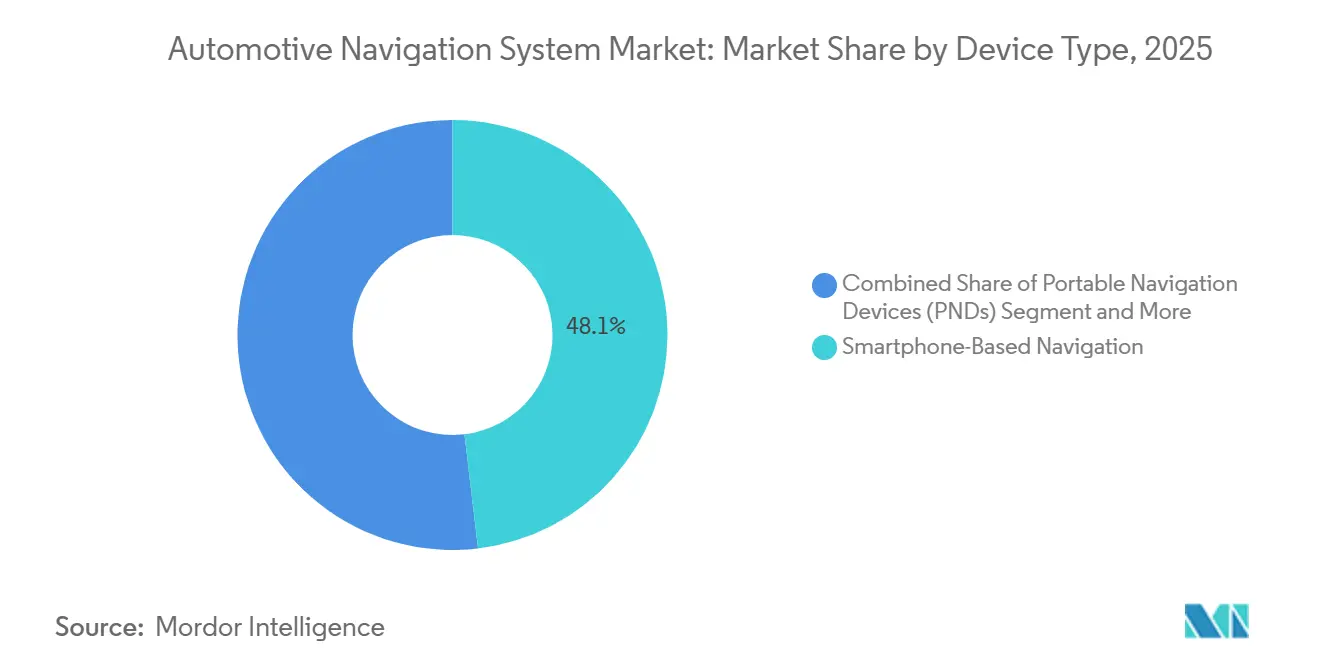

- By device type, smartphone-based navigation commanded 48.11% of the automotive navigation system market share in 2025, while in-dash systems are projected to grow at a 12.84% CAGR through 2031.

- By 2025, 2D maps led the automotive navigation system market with a 51.63% share; augmented-reality navigation is forecasted to expand at a 24.72% CAGR through 2031.

- By vehicle type, passenger cars accounted for 77.58% of the automotive navigation system market size in 2025, while commercial vehicles are projected to advance at a 10.12% CAGR through 2031.

- By component, software held a 45.37% share of the automotive navigation system market in 2025, whereas services are projected to post the fastest 14.92% CAGR over 2026-2031.

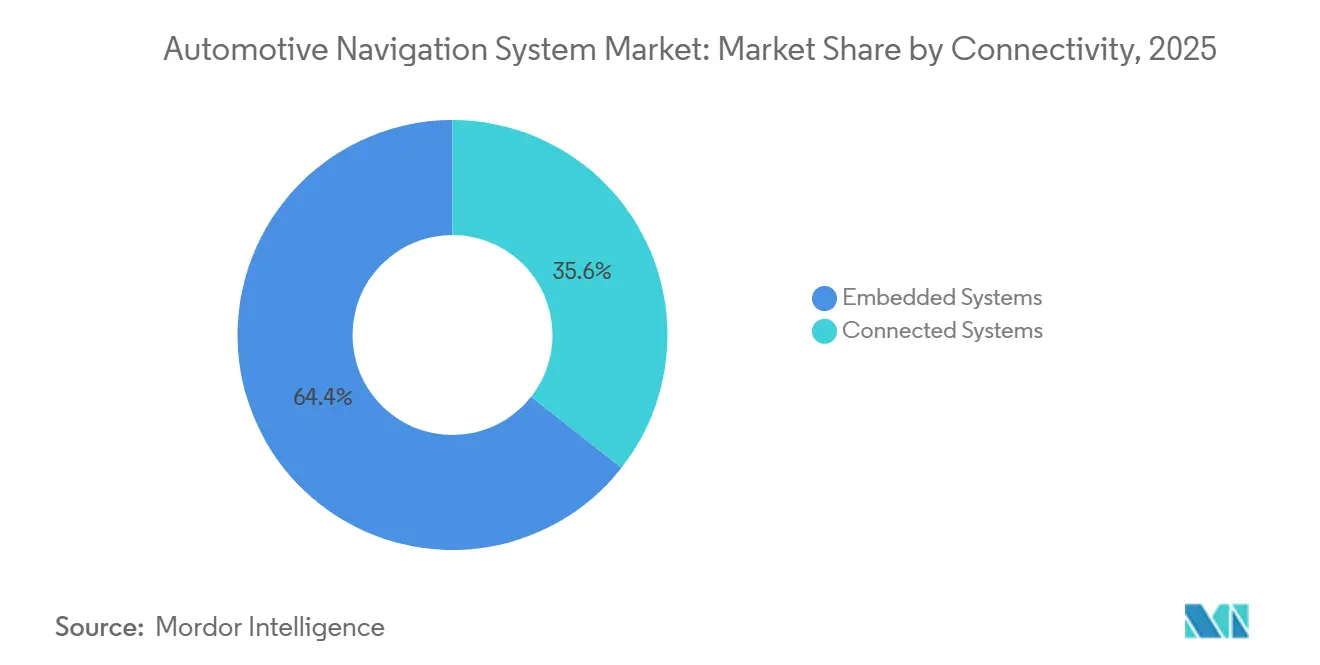

- By connectivity, embedded systems dominated the automotive navigation system market with a 64.41% share in 2025, while connected systems are projected to grow at an 11.68% CAGR to 2031.

- By distribution channel, OEM-installed units captured 69.22% of the automotive navigation system market share in 2025; aftermarket solutions are expected to grow at a 10.76% CAGR through 2031.

- By geography, the Asia-Pacific region held a 33.48% share of the automotive navigation system market in 2025 and is projected to grow at a CAGR of 6.93% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Automotive Navigation System Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Connected Vehicles | +1.8 | Global, led by North America, Europe, China | Medium term (2–4 years) |

| Penetration of Factory-Fitted Infotainment Units | +1.5 | Global, strongest in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Regulatory Push for e-Call and Advanced Safety Compliance | +1.2 | Europe, Russia, India | Short term (≤ 2 years) |

| EV-Specific Range-Aware Routing Algorithms | +0.9 | North America, Europe, China | Medium term (2–4 years) |

| Subscription-Based OTA Map-Update Revenue Streams | +0.7 | Global, premium OEMs | Long term (≥ 4 years) |

| Low-Cost Dual-Frequency GNSS + IMU Accuracy Gains | +0.6 | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Connected and Autonomous-Ready Vehicles

The majority of vehicles in Europe and North America shipped with embedded connectivity modules in 2025, creating a larger installed base for navigation-centric driver-assistance functions. High-definition maps with centimeter-level lane geometry now underpin adaptive cruise, lane keeping, and automated parking, shifting navigation from simple routing to a localization backbone. Tesla’s software loads the road topology before sensors, improving urban energy efficiency by 8–12%. Automakers favor suppliers that can integrate mapping, localization, and path-planning into a single stack, thereby accelerating vertical integration across the automotive navigation system market. Predictive capabilities that anticipate road conditions rather than reacting to them are becoming a differentiator, supporting Level 2+ and future Level 3 autonomy programs.

Penetration of Factory-Fitted Infotainment/Navigation Units

Factory-fit navigation penetration in Japan, Europe, and North America surged in 2025, driven by bundled infotainment strategies that lower incremental hardware cost to under USD 50 per vehicle. The EU’s General Safety Regulation[1]"Intelligent speed assistance (ISA) set to become mandatory across Europe," European Road Safety Charter, road-safety-charter.ec.europa.eu mandates speed limit recognition based on map data, further solidifying the role of embedded units. Platforms such as Harman Ignite integrate voice assistants and e-commerce, locking users into OEM ecosystems and generating recurring revenue from apps. Lower price premiums and tighter ADAS coupling mean that embedded systems are increasingly recapturing share from smartphones within the automotive navigation system market.

Regulatory Push for e-Call and Advanced Safety Compliance

Since 2018, Europe has required new light vehicles to include an e-Call module that automatically transmits crash location, cutting rural emergency response times by 40%. Russia’s ERA-GLONASS and India’s planned 2027 pedestrian alert system [2]Junaid Shah, "India to Mandate Pedestrian Alert Systems (AVAS) in Electric Vehicles from 2026," Saur Energy, saurenergy.com ensure every new vehicle must incorporate reliable, power-independent navigation. Draft Chinese rules would make vehicle-to-everything broadcasts mandatory, again tethering compliance to navigation accuracy. These regulations establish a captive, non-discretionary foundation for embedded navigation hardware, thereby reinforcing the growth momentum in the automotive navigation system market.

EV-Specific Range-Aware Routing Algorithms

Electric-vehicle drivers value route planning that integrates battery state of charge, weather, elevation, and charger availability. Tesla’s navigation reroutes to Superchargers before depletion, resulting in 89% satisfaction scores by 2025. HERE and Mercedes-Benz model battery degradation over time, advising charge patterns that extend pack life by up to 20%. Chinese OEMs embed the locations of swap stations, enabling five-minute battery exchanges. As EV adoption increases, such algorithms evolve from a premium perk into a core purchasing criterion, expanding the addressable revenue within the automotive navigation system market.

Restraints Impact Analysis of Automotive Navigation System Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Free Substitutes | -1.4 | Global, especially North America, Western Europe | Short term (≤ 2 years) |

| High Costs | -0.9 | Global | Long term (≥ 4 years) |

| GNSS Spoofing and Cyber-Attack Liability | -0.5 | Global | Medium term (2–4 years) |

| Data-Sovereignty Laws | -0.4 | China, Russia, EU, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Free Smartphone-Navigation Substitutes

Google Maps and Apple Maps offer free routing, frequent updates, and calendar integration, leading the United States drivers to prefer phones over embedded systems in 2025. Their dominance in the portable navigation device segment collapsed, pushing Garmin’s revenue down 42% between 2020 and 2025. Automakers respond by integrating CarPlay and Android Auto, yet doing so surrenders control of the interface and data monetization. The convenience and perceived parity of smartphones continue to be a headwind for the automotive navigation system market, particularly in price-sensitive segments.

High Hardware and Software Development Costs

A competitive navigation stack demands USD 50–100 million in R&D, spanning GNSS receivers, HD maps, routing, UI, and cybersecurity. Bosch allocated EUR 2.3 billion to software in 2025, with navigation absorbing 18%. Smaller OEMs resort to white-label solutions, trading differentiation for cost containment. Visteon’s 2024 exit from navigation hardware underscores consolidation pressures. Capital intensity slows entrant turnover and tempers the speed of innovation in the automotive navigation system industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive Navigation System Market Segment Analysis

By Device Type:

Smartphone Mirroring Dominates, Yet Embedded Systems Gain GroundSmartphone-based solutions retained 48.11% of the automotive navigation system market share in 2025, benefitting from familiar interfaces and zero incremental cost. In-dash systems, however, are forecast to grow at a 12.84% CAGR through 2031 as automakers integrate navigation with ADAS that demands vehicle-calibrated positioning. The automotive navigation system market size for in-dash units is projected to reach USD 18.9 billion by 2031, reflecting the rising penetration of factory-fit units. Portables have shrunk to niche commercial use but persist where device mobility matters.

Reliability and deeper sensor integration give embedded platforms a unique value proposition. Alpine’s Halo11 continues to provide guidance even when smartphones are disconnected, satisfying professional drivers. Pioneer’s integration of Alexa voice control demonstrates convergence between consumer IoT ecosystems and vehicle functions. Over-the-air updates narrow the map freshness gap with phones, supporting the gradual reclaiming of share inside the automotive navigation system market.

By Technology:

2D Maps Persist, AR Navigation Emerges as Premium DifferentiatorTraditional 2D maps held a 51.63% market share in the automotive navigation system market in 2025, driven by their low data requirements and broad hardware compatibility. Augmented-reality navigation will expand at a 24.72% CAGR, unlocking new revenue pockets in premium segments. The automotive navigation system market size for AR-enabled solutions is expected to surpass USD 5 billion by 2031 as head-up displays proliferate.

Continental’s AR-HUD projects full-color graphics onto the real road view in a 130 cm (51 in) wide by 60 cm (23 in) high segment of the driver's field of vision, simulating an optical distance of 7.5 m (24 ft 9 in).[3]Colin Jeffrey, "Continental's Augmented Reality HUD puts information on the road," New Atlas, newatlas.com distance, reducing driver distraction. WayRay’s holographic projector delivers full-color images visible in sunlight and is currently implemented in Mercedes-Benz EQS models. Panasonic adds eye-tracking to maintain alignment, highlighting the rapid evolution of this feature. While 3D maps and voice guidance remain important, AR’s immersive overlay positions it as the next competitive frontier.

By Vehicle Type:

Passenger Cars Lead, Commercial Vehicles AcceleratePassenger cars accounted for 77.58% of the automotive navigation system market share in 2025, driven by higher volumes and consumer infotainment demand. Commercial vehicles, buoyed by telematics integration and electronic-logging regulations, are expected to post a 10.12% CAGR through 2031. Automotive navigation system market share for passenger cars remains dominant, yet fleets increasingly view navigation as an operational efficiency tool.

Platforms such as Geotab’s MyGeotab with TomTom routing cut empty miles by 14%. Daimler Truck’s Detroit Connect aligns maintenance alerts with navigation, reducing breakdowns. Fleet-oriented navigation emphasizes durability, subscription economics, and compliance features, differentiating it from consumer-focused systems.

By Component:

Software Leads, Services Surge on Subscription ModelsSoftware contributed 45.37% of the automotive navigation system market share in 2025; however, services are expected to grow with a 14.92% CAGR through 2031, as subscriptions for traffic updates, parking, and hazard warnings increase. Hardware margins continue to narrow, shifting profit pools toward cloud services. The automotive navigation system services market is forecast to double between 2026 and 2031.

HERE Plus+ generated USD 143 million annual recurring revenue in 2025. TomTom’s MyDrive converts hardware buyers into long-term subscribers, smoothing cash flow. Professional B2B licensing to ride-hailing, delivery, and AV developers diversifies supplier income, underscoring a pivot from product to platform economics.

By Connectivity:

Embedded Systems Dominate, Connected Systems RiseEmbedded systems captured 64.41% of the automotive navigation system market share in 2025, thanks to the integration of e-Call and sensors. Connected systems leveraging 4G/5G modems are expected to grow at a 11.68% CAGR through 2031, introducing cloud-based routing and cooperative driving features. The automotive navigation system market size for connected architectures is expected to surpass USD 26 billion by 2031.

Sony-Honda’s Afeela streams HD tiles on demand, slashing onboard storage. Qualcomm’s Snapdragon Cockpit combines a 5G modem with navigation capabilities, enabling cooperative lane-change assistance. Nonetheless, rising cybersecurity scrutiny may temper adoption speed unless robust data-protection frameworks emerge.

By Distribution Channel:

OEM Dominance, Aftermarket Niche PersistsOEM installations held a 69.22% of the automotive navigation system market share in 2025, reflecting the shift toward integrated cockpits. Aftermarket solutions are expected to continue growing at a 10.76% CAGR through 2031. The automotive navigation system market size for aftermarket devices could approach USD 7 billion by 2031, provided installers address the integration complexity.

Garmin’s Overlander serves off-road niches with topographic maps. Alpine’s partnership with Best Buy simplifies same-day fitment, lowering adoption barriers. Success depends on offering features that smartphones cannot, such as rugged housings, sensor inputs, or fleet management APIs.

Geography Analysis

APAC Automotive Navigation System Market

The Asia-Pacific region held a 33.48% share of the automotive navigation system market in 2025 and is projected to outpace all other areas with a 6.93% CAGR through 2031. India’s subsidies for NavIC-compatible receivers stimulate domestic supplier growth. These dynamics boost local innovation, although foreign vendors must navigate data-sovereignty rules to capture share inside the automotive navigation system market.

North America Automotive Navigation System Market

North America commanded the second-highest share in 2025. General Motors plans to phase out CarPlay in favor of its Ultifi stack, signaling a strategic pivot. Ford’s BlueCruise relies on embedded maps to designate hands-free zones, illustrating the role of navigation in ADAS branding. Canada pilots weather-overlay features that reduce winter accidents, demonstrating how regional conditions influence product priorities.

Europe Automotive Navigation System Market

E-call mandates and a high density of premium vehicles underpin the European market. Continental generated EUR 3.8 billion from navigation and infotainment in 2025, reflecting robust demand from Tier 1. The U.K.’s impending 2030 ICE ban is expected to accelerate the uptake of EV-specific navigation systems, with JLR’s Pivi Pro emphasizing range prediction. France’s Michelin acquired a 30% stake in Sygic, illustrating cross-segment convergence.

Regulatory Landscape

Regulation is tightening around cyber security, software updates, and connected-vehicle supply chains, which is directly shaping embedded navigation architectures and OTA map-update operations. In Great Britain, the UK Government implemented mandatory application of UNECE WP.29 UN Regulation No. 155 (Cyber Security) and UN Regulation No. 156 (Software Updates) for new GB vehicle types from 1 February 2026. This raises the compliance bar for in-vehicle navigation stacks that rely on connectivity, cloud services, and frequent software releases.

In the United States, the Department of Commerce final rule restricting connected vehicle systems (VCS) hardware and software with a nexus to foreign adversaries took effect on 17 March 2025, with additional phase-in tied to Model Year 2027 (software) and Model Year 2030 (hardware). These policies increase supplier-provenance scrutiny for telematics modules, GNSS-related components, and software supply chains that support navigation, while also reinforcing convergence toward UNECE-aligned cyber security and software update management processes.

Value Chain Analysis

The navigation system value chain is software-led, starting with geospatial content creation and aggregation (base maps, HD/lane-level attributes, traffic, and POI). It then moves through platform layers such as navigation engines and SDKs, with automotive-grade integration by Tier 1 suppliers into head units and digital cockpits, and ends with OEM validation, deployment, and lifecycle services (OTA map and software updates, subscriptions, and data operations). An upstream map-provider layer (for example, HERE Technologies and TomTom) and large platform ecosystems (for example, Google Maps Platform and Mapbox) feed routing, search, and real-time data that OEMs increasingly embed into software-defined vehicle programs.

Downstream, Tier 1 integrators and cockpit compute platforms translate mapping and routing into production systems with functional safety and cyber security controls, then distribute through OEM-fitted channels (dominant) and a smaller aftermarket. Partnerships show how value is captured across layers: HERE partnered with ECARX (April 2025) to launch next-generation in-car navigation for brands including Lotus, Lynk & Co, Smart, and Hongqi, while Rivian began rolling out Rivian Navigation with Google Maps using the Google Maps Auto SDK (July 2025). Key bottlenecks include long OEM validation cycles, limited availability of automotive software engineers skilled in ISO 26262/ASPICE, and regional data-localization constraints that force separate data and software variants.

Competitive Landscape

The top five suppliers accounted for a significant share of the 2025 revenue. OEMs increasingly develop proprietary stacks to protect data and branding, placing pressure on traditional map vendors. Competition now hinges on software quality, update cadence, and ADAS integration rather than screen hardware. Augmented-reality navigation and EV-specific routing represent white-space arenas where newcomers such as WayRay gain footholds by licensing holographic patents.

OEMs are increasingly developing proprietary navigation software to differentiate their brands and capture user data, thereby reducing their reliance on third-party suppliers and compressing margins for traditional map providers. The competitive dynamic has shifted from hardware differentiation—where screen size, resolution, and processing power were key—to software and services differentiation, where map accuracy, update frequency, and integration with ADAS and e-commerce platforms determine market share.

White-space opportunities exist in augmented-reality navigation, where WayRay and Continental are pioneering holographic head-up displays that project lane-level guidance onto windshields, and in EV-specific routing, where Tesla's proprietary algorithms set the benchmark for range prediction and charging-station optimization.

Automotive Navigation System Industry Leaders

-

Robert Bosch GmbH

-

Denso Corporation

-

Harman International

-

LG Electronics Inc.

-

Panasonic Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Automotive Navigation System Market Companies Covered in this Report

- TomTom International BV

- HERE Technologies

- Garmin Ltd.

- Continental AG

- Denso Corporation

- Robert Bosch GmbH

- Alpine Electronics

- Pioneer Corporation

- Mitsubishi Electric Corp.

- Aisin AW Co.

- Harman International

- JVCKENWOOD Corp.

- Panasonic Holdings Corporation

- Sony Group Corp.

- Visteon Corp.

- Faurecia Clarion

- LG Electronics Inc.

- Apple Inc. (CarPlay)

- Google LLC (Android Auto / Maps)

- WayRay AG

Market Opportunities and Future Outlook

Opportunities center on navigation becoming a software-defined cockpit function, supported by AI-driven interaction, lane-level content for ADAS/ISA, and service monetization through OTA updates. A concrete whitespace area is privacy-preserving, offline-capable conversational navigation that runs on vehicle compute rather than the cloud, aligning with cyber security and data-sovereignty constraints. Visteon and TomTom (January 2026) announced an in-car local AI conversational navigation assistant built on Visteon cognitoAI and TomTom Automotive Navigation Application, which points to on-device inference while keeping automotive-grade user experience and resilience.

Another opportunity involves scaling streaming navigation and regional partnerships to support global vehicle platforms where map content, regulations, and data handling differ by market. HERE expanded its online navigation partnership with Hyundai AutoEver to North America and Australia (January 2026), and HERE signed an MoU with Baidu Maps (April 2026) to combine HERE live maps with Baidu navigation capabilities for advanced in-vehicle navigation and driver-assistance use cases, including Intelligent Speed Assistance. These moves highlight demand for multi-region deployment toolchains, standardized SDK integrations, and subscription-ready service layers that connect navigation to ADAS, EV routing, and connected-cockpit ecosystems.

Recent Industry Developments in Automotive Navigation System Market

- July 2026: DENSO TEN launched two new ECLIPSE car navigation system models in Japan (RS-series AVN-RS01 and RBS-series AVN-RBS01) featuring 2025 autumn map data. The release reinforces the importance of frequent map refresh cycles and OEM-grade update pipelines as embedded navigation competes with smartphone update cadence.

- November 2025: HERE Technologies and Amap formed a strategic alliance to deliver next-generation, AI-driven navigation solutions for Chinese automakers. The collaboration supports cross-border product strategies by combining a global mapping provider with a major China navigation platform, addressing localization and compliance needs tied to connected navigation services.

- January 2024: Hyundai Motor Group and Google announced a collaboration on software capability for future mobility, spanning connected vehicle and infotainment foundations that enable navigation-centric services. The tie-up reflects how cockpit software ecosystems and third-party platforms influence navigation feature velocity, real-time data access, and developer tooling across vehicle programs.

Automotive Navigation System Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the automotive navigation system market covers navigation functions used in vehicles to guide drivers, whether built into the dashboard or added as an external device, and measured in revenue terms.

Scope exclusions: We exclude general smartphone-only navigation apps that are not sold as part of an automotive navigation device, embedded head unit, or vehicle-fitted navigation offering.

Segments Covered in This Report

-

By Device Type

- In-Dash Navigation Systems

- Portable Navigation Devices (PNDs)

- Smartphone-Based Navigation

-

By Technology

- 2D Maps

- 3D Maps

- Voice-Guided Navigation

- Augmented Reality Navigation

-

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

-

By Component

- Hardware

- Software

- Services

-

By Connectivity

- Embedded Systems

- Connected Systems

-

By Distribution Channel

- OEM-Installed Systems

- Aftermarket Systems

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Turkey

- Rest of Middle-East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the market context and to anchor assumptions that are hard to validate from interviews alone. We reviewed public sources such as road safety and transport agencies, vehicle registration and parc statistics, customs import-export summaries for in-vehicle electronics, and standards and regulatory publications that shape in-vehicle safety and connectivity requirements.

To keep the model grounded, we also used company annual reports, investor decks, product brochures, and credible press coverage to track feature shifts, for example embedded connectivity, OTA map updates, and screen-size trends. In a few places, we referenced paid subscriptions for company financials and news, patent tracking for navigation and positioning features, and shipment-level trade data to sanity-check directionally. These desk sources are illustrative only, and other public references were used to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work focused on confirming what gets counted as a paid navigation system in real vehicle programs and in the aftermarket, and then pressure-testing adoption and pricing assumptions. We spoke with a mix of OEM-facing stakeholders, aftermarket channel participants, and component and software ecosystem experts across major auto-producing and high-vehicle-parc regions, and then reconciled the inputs back to the desk-built model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 50% |

| Mid tier: 44% | Functional/Unit leaders: 37% | EMEA: 30% |

| Smaller Players: 20% | Managers: 51% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the demand pool from vehicle production and sales by region, then applies fitment and take-rate assumptions for navigation by vehicle category and channel (OEM vs aftermarket). After forming the ceiling, we corroborate the totals with selective bottom-up checks, such as sampled price points by screen size and device type, and revenue reasonableness checks against a short list of suppliers and channel signals.

A few variables that consistently shaped the model were new vehicle output, in-dash infotainment penetration, the split between embedded and tethered connectivity, average selling prices by device type (in-dash vs portable), and the share of navigation offered as bundled vs optional content. Where direct inputs were missing, gaps were handled using proxy indicators like regional vehicle parc growth, regulation-led adoption of connected features, and expert ranges for take rates, then narrowed through follow-up calls.

For forecasting, scenario analysis was used because adoption and pricing are shaped by both feature bundling and smartphone substitution trends. The forward view is driven by consensus ranges from interviews on take-rate movement, expected pricing steps, and connectivity mix changes, followed by annualized smoothing to avoid unrealistic jumps.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals like vehicle production trajectories, regional mix shifts, and the plausibility of implied revenue per equipped vehicle. When a region or channel produced outlier results, assumptions were re-reviewed, and in many cases respondents were re-contacted to confirm whether the change came from take rates, pricing, or scope interpretation.

Before sign-off, the model goes through multi-step analyst review where calculations, units, and currency timing are checked, and the story is validated against recent market events. Reports are refreshed annually, and interim updates are made when material events affect demand or pricing. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Automotive Navigation System Market Size Compared With Other Published Estimates

Published market sizes for automotive navigation systems often do not match because firms group products differently and also pick different timing for currency conversion and price updates. We also see differences when one estimate follows vehicle shipments more closely, while another leans more on broader consumer navigation spending trends.

Some external estimates fold smartphone-only navigation and wider connected infotainment revenues into the same bucket, and then apply a single ASP curve across regions. For Mordor Intelligence, revenue is counted only when navigation is sold as an in-vehicle system or add-on device through OEM or aftermarket channels, and app-only usage is left out, which keeps the total tied to fitment and take-rate signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 27.13 B (2026) | |

| Industry Research House A | USD 19.78 B (2025) | Uses a 2024 base and a longer horizon, and the scope appears to be narrower on paid in-vehicle systems, which can undercount OEM-bundled navigation value and higher screen-size mixes. |

| Market Tracker B | USD 34.74 B (2031) | Reported year is a later endpoint and the approach emphasizes shipments and revenue together, which can shift results if unit assumptions or regional ASP timing are not aligned to the same currency and pricing year. |

The spread in the table is mainly explained by timing and scope choices, not just math. By keeping inputs traceable to vehicle output, fitment, channel mix, and realistic pricing steps, the final number stays repeatable and easier to reconcile with how navigation revenue is actually realized in the auto market.

Key Questions Answered in the Report

How big is the Automotive Navigation System Market?

The automotive navigation system market is expected to grow from USD 25.45 billion in 2025 to USD 27.13 billion in 2026 and is forecast to reach USD 37.54 billion by 2031, growing at a 6.71% CAGR during the forecast period.

What is the current Automotive Navigation System Market size?

In 2026, the Automotive Navigation System Market size is expected to reach USD 27.13 billion.

Who are the key players in Automotive Navigation System Market?

Panasonic Holdings Corporation, Robert Bosch GmbH, Harman International Industries, LG Electronics Inc. and Denso Corporation are the major companies operating in the Automotive Navigation System Market.

Which is the fastest growing region in Automotive Navigation System Market?

Which is the fastest growing region in Automotive Navigation System Market?

Which region has the biggest share in Automotive Navigation System Market?

In 2025, Asia Pacific accounts for the largest market share in Automotive Navigation System Market.

Page last updated on: