Automotive Aerodynamic Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

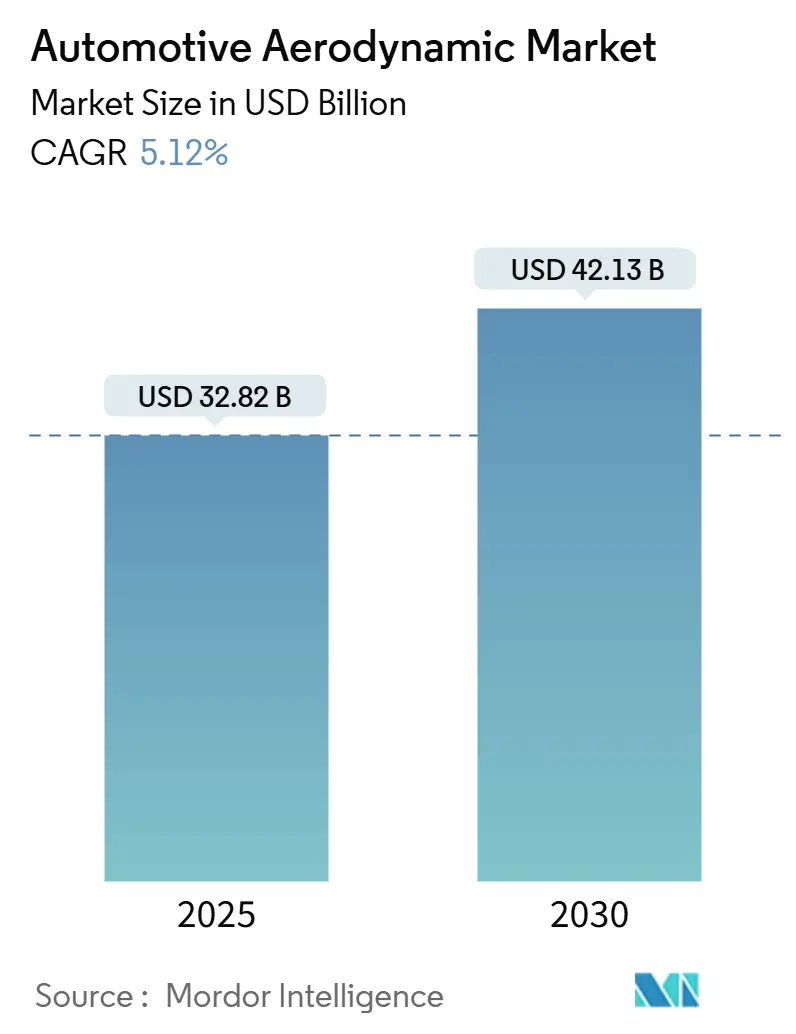

| Market Size (2025) | USD 32.82 Billion |

| Market Size (2030) | USD 42.13 Billion |

| Growth Rate (2025 - 2030) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Aerodynamic Market Analysis by Mordor Intelligence

The automotive aerodynamic market size is USD 32.82 billion in 2025 and is forecast to climb to USD 42.13 billion by 2030, advancing at a 5.12% CAGR. This growth rests on a clear logic, stricter emissions rules continue to tighten worldwide while electric vehicles (EVs) depend on low-drag bodywork to extend driving range. The automotive aerodynamic market, therefore, shifts from optional styling enhancements to core functional systems that help automakers meet fleet-average CO₂ limits and boost battery-only mileage. OEM investment in active airflow devices, lightweight materials, and advanced computational design tools signals a decisive pivot toward efficiency-led vehicle architectures. Suppliers able to integrate aerodynamic functions with lighting, sensing, and thermal-management hardware are now central to competitive strategy in the automotive aerodynamic market.

Key Report Takeaways

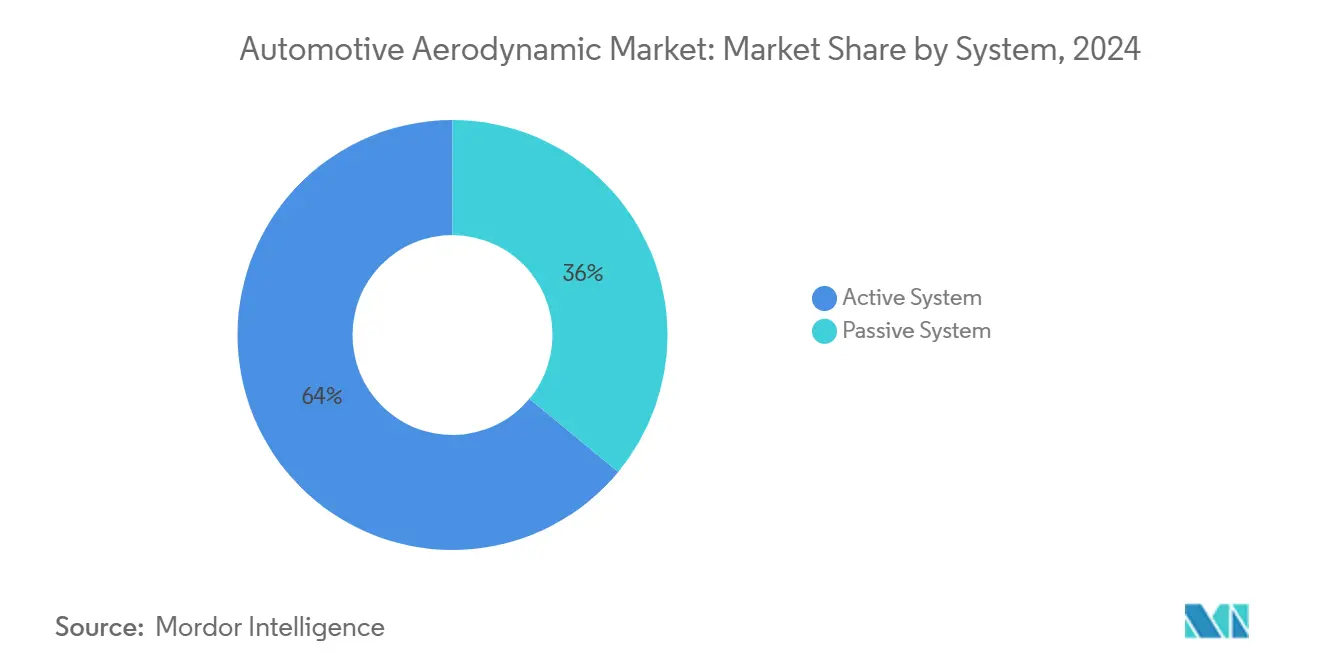

- By system, active aerodynamic solutions held 64.04% of the automotive aerodynamic market share in 2024, and are expected to post the fastest growth at a 6.04% CAGR to 2030.

- By application, spoilers led with 29.11% of the automotive aerodynamic market size in 2024, while grille shutters are projected to grow at a 6.88% CAGR through 2030.

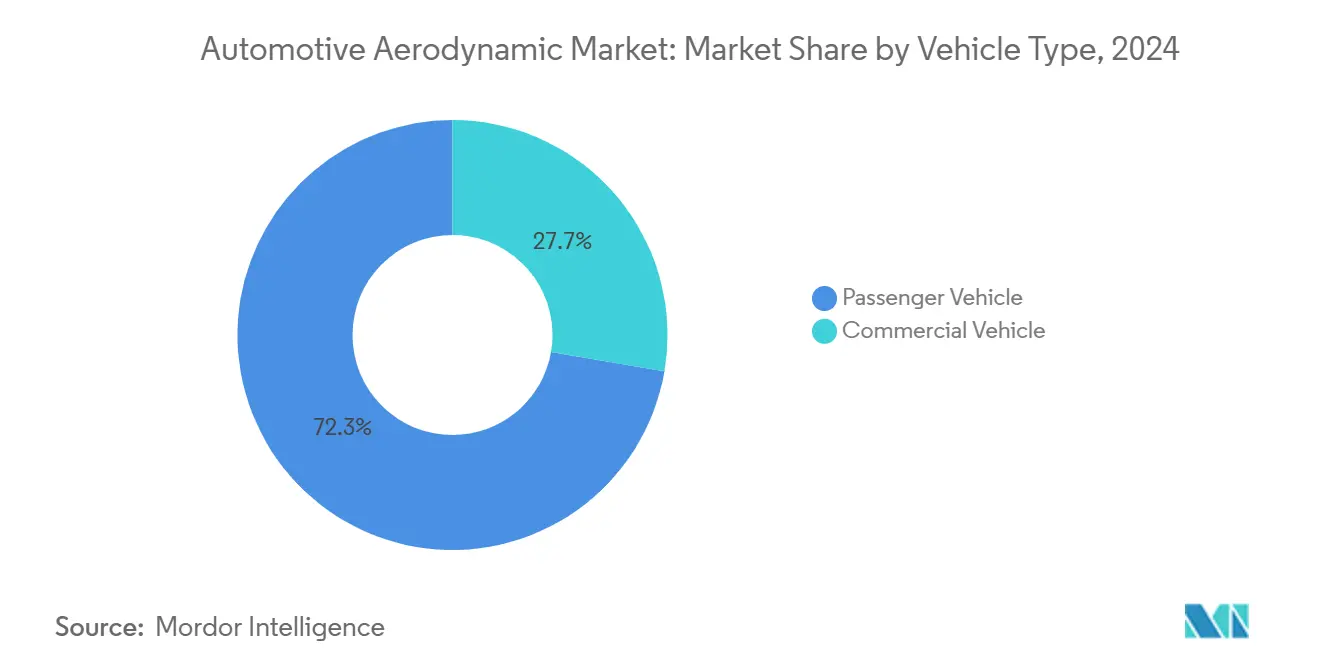

- By vehicle type, passenger vehicles accounted for 72.33% of the automotive aerodynamic market in 2024 and are advancing at a 5.82% CAGR through 2030.

- By material type, polymers retained a 49.06% share of the automotive aerodynamic market size in 2024; composites record the strongest forecast CAGR at 6.35% to 2030.

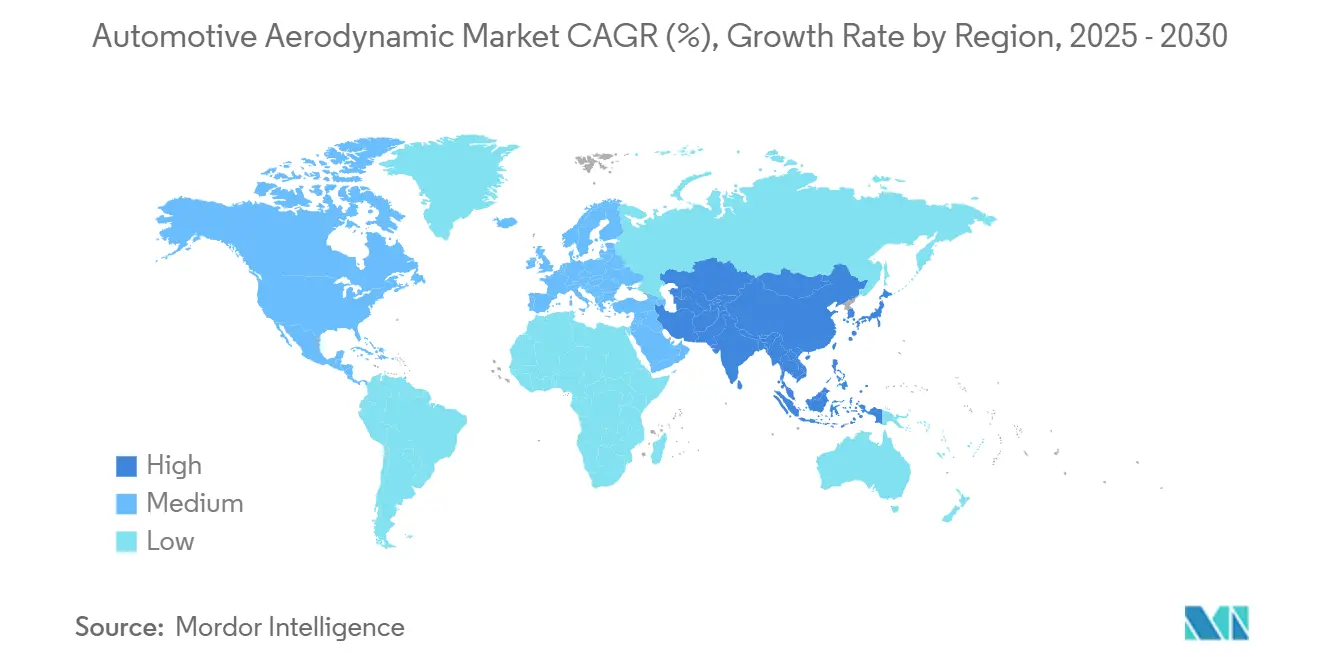

- By geography, Asia-Pacific commanded 46.25% revenue share of the automotive aerodynamic market in 2024, and will continue to advance at a 5.44% CAGR between 2025 and 2030.

Global Automotive Aerodynamic Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Adoption Drives Aero Packages | +1.8% | China, Europe | Short term (≤ 2 years) |

| Stricter Global Emissions Standards | +1.2% | EU, North America | Medium term (2-4 years) |

| OEMs Invest In Active Aero | +0.9% | North America, Europe, Asia-Pacific premium hubs | Medium term (2-4 years) |

| CFD and AI Optimize Aero | +0.7% | Developed markets worldwide | Long term (≥ 4 years) |

| Aero-Battery Integration In BEVs | +0.6% | Global EV hubs | Long term (≥ 4 years) |

| Trucking Demands Fuel-Saving Retrofits | +0.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid EV Adoption Driving Range-Oriented Aero Packages

Range anxiety amplifies the dollar value of every percentage point cut in drag. Tesla’s Model S combines smooth under-body panels with adaptive grille shutters, delivering tangible range boosts that resonate with consumers. Hyundai’s Active Air Skirt trims frontal turbulence around wheels to extend real-world EV mileage, validating adaptive aero even in mid-size platforms [1]“Active Air Skirt Technology Announcement,” Hyundai Motor Company, hyundai.com. Automakers now lock in aero targets as early as the concept phase, demanding supply-ready systems that merge airflow management with battery-thermal channels and radar housings. This urgency positions the automotive aerodynamic market as a linchpin in EV differentiation strategies over the next two years.

Stringent Global CO₂ / Fuel-Economy Standards

Regulators now evaluate real-world aerodynamic drag when certifying new models, closing loopholes that once let stylists prioritize form over airflow. The European Union mandates WLTP-based testing that captures on-road drag, while the United States CAFE updates tie measured drag coefficients to fuel-economy ratings [2]“CO₂ Emission Performance Standards for Cars and Vans,” European Commission, europa.eu. Heavy-duty vehicles in Europe use VECTO simulation, which cross-checks component-level airflow data against whole-vehicle tests, creating a direct compliance pathway for spoilers, diffusers, and grille shutters. These rules elevate the automotive aerodynamic market from a styling niche to a regulatory necessity across segments and price points. As governments widen real-driving emissions (RDE) audits, even small efficiency gains from aero tweaks now swing certification outcomes. That reality anchors sustained demand for both active and passive aerodynamic upgrades well into the next model cycle.

OEM Investments in Active Aero for Premium and Performance Cars

Premium brands recoup higher system costs by bundling dynamic spoilers and shutters with performance or luxury badges. Mercedes-Benz deploys speed-sensitive front splitters and wheel deflectors on the EQS SUV, balancing efficiency and downforce without manual driver input [3]“Aerodynamics of the EQS SUV,” Mercedes-Benz Group AG, mercedes-benz.com. Dodge patent filings outline adjustable rear wings optimized for cooling and drag at different track speeds, signalling continued R&D spend in active aero by muscle-car makers in the United States. These moves prove that active aero unlocks both marketing cachet and measurable fuel savings, helping upscale trims retain profit margins even as battery and software costs rise.

Cost-Effective CFD and AI-Driven Aero Optimization Tools

Cloud-native CFD and machine-learning speed design loops once dependent on expensive wind tunnels. Neural Concept’s GPU-accelerated solver cuts iteration time from weeks to hours, lowering entry barriers for niche suppliers. Ansys SimAI blends ML with traditional solvers so engineers can auto-tune shape parameters for optimum Cd and cooling airflow in the same session. Stellantis reinforces the physical side with a USD 29.5 million moving-ground-plane wind tunnel that mirrors highway wheel rotation for high-fidelity validation. These digital-physical toolchains democratize advanced aero, broadening the automotive aerodynamic market to midsize suppliers worldwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Active Aero Costs | -0.8% | Global cost-sensitive segments | Short term (≤ 2 years) |

| Complex Mechatronic Integration | -0.6% | Worldwide, acute for smaller OEMs | Medium term (2-4 years) |

| Composite Production Bottlenecks | -0.4% | Regions with limited composite capacity | Long term (≥ 4 years) |

| Pedestrian Safety Uncertainty | -0.3% | EU, North America, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Active Aerodynamic Systems

Full-motion shutters, pop-up spoilers, and deployable gap fillers bundle actuators, sensors, and dedicated controllers that add significant costs per vehicle. In price-elastic A- and B-segment cars, those costs outstrip lifetime fuel savings, delaying penetration below premium trims. Even when OEMs absorb hardware spend, redundancy rules for safety-critical motion parts inflate validation and warranty budgets. Until scale economies arrive, sticker-price pressure will cap active adoption and nudge some brands toward refined passive alternatives, limiting near-term lift for the automotive aerodynamic market.

Complex Mechatronic Integration with Vehicle ECUs

Modern cars host 100-plus ECUs competing for bandwidth and thermal budget. Active grille shutters must handshake with cooling, powertrain, and ADAS controllers without latency that risks overheating or sensor misalignment. Cybersecurity rules now treat every connected actuator as a potential attack surface, tacking extra encryption and diagnostics onto aero systems. Smaller automakers lacking deep software teams outsource integration to tier-1 suppliers, raising program costs and stretching launch timelines, which in turn tempers the automotive aerodynamic market expansion rate during the forecast window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Active Systems Drive Premium Integration

Active devices controlled by onboard software captured 64.04% of the automotive aerodynamic market in 2024. Active systems are forecast to outpace passive counterparts at a 6.04% CAGR to 2030 because they let carmakers balance drag, cooling, and downforce on the fly. That capability aligns with multi-mode EV architectures that toggle between eco and sport driving. Hyundai’s Active Air Skirt pivots closed above 50 mph to shield wheels, then retracts in stop-and-go traffic for brake cooling, illustrating the real-time adaptability buyers now expect.

Passive spoilers and diffusers remain staples in cost-sensitive trims where owners favor low maintenance and total simplicity. Commercial fleets also trust fixed aero kits that survive harsh duty cycles. Yet even those segments are beginning to specify actuated gap seals for highway legs. The automotive aerodynamic market, therefore, sees active hardware migrate down the price ladder as economies improve, while passive gear stabilizes as baseline content.

By Application: Spoilers Lead While Grille Shutters Accelerate

Spoilers dominated the automotive aerodynamic market in 2024 with a 29.11% share. It remain popular because they double as styling statements and factory-ready attachment points. Nonetheless, grille shutters post a breakneck 6.88% CAGR through 2030 on the back of EV cooling needs. Modern heat-pump systems allow upper grilles to close for most of a drive cycle, giving shutters sizable drag-cutting leverage. Valeo supplies multiblade modules that integrate noise-damping and snow-ingress defense, shortening OEM validation queues.

Diffusers, side skirts, and air dams grow at steady mid-single-digit rates as package space widens in skateboard EV platforms. An emerging class of active wheel covers that pivot open under hard braking sits in the “others” bucket today, but could graduate to a primary line item later in the decade. Each product family shares a demand driver, quantifiable Cd improvement with minimal compromise to styling or serviceability, which keeps revenue flowing across the automotive aerodynamic market.

By Vehicle Type: Passenger Vehicles Dominate Commercial Growth

Passenger models controlled 72.33% of the automotive aerodynamic market share in 2024 and will expand at a CAGR of 5.82% by 2030. EV crossovers in particular slot aero as a must-have to hit 300-mile range targets without oversized battery packs. CD (Coefficient of Drag) values near 0.20, once frequented only in luxury sedans, now appear in compact SUVs thanks to under-floor shields and hidden wiper pockets.

Commercial trucks add aero upgrades primarily to cut diesel or LNG use on long hauls. The segment’s growth rides on strict California Air Resources Board standards and shipper carbon-audit pressures. Bolt-on fairings that promise sub-18-month payback draw purchase orders even in low-margin logistics fleets. As freight houses pilot battery-electric tractors with limited range, high-efficiency bodies will grow crucial, pulling more suppliers into the commercial slice of the automotive aerodynamic market.

By Material Type: Composites Gain Despite Production Constraints

Polymers such as polypropylene and ABS held 49.06% of the automotive aerodynamic market size in 2024. They remain cost champions with cycle times under a minute for large exterior panels. Metals like aluminum cling to under-hood shield and pickup-bed aero roles where puncture resistance trumps mass.

Composites jump at a 6.35% CAGR toward 2030 because they marry low weight with radar transparency, a vital trait as ADAS sensor counts soar. Hexcel’s woven carbon preforms enable integrated battery-belly pans that both stiffen the chassis and streamline airflow. Still, limited autoclave capacity and high scrap cost mean composites chiefly populate premium trims for now. Breakthroughs in out-of-autoclave curing aim to unlock volume, a pivot that would sharply raise the composite slice of the automotive aerodynamic market later in the decade.

Geography Analysis

Asia-Pacific commanded 46.25% of the automotive aerodynamic market share in 2024 in the automotive aerodynamic market on the strength of China’s massive EV output and subsidy framework favoring extended-range models. the region is projected to witness the fastest growth of 5.44% CAGR through 2030. Chinese plants churn out shutters, wheel deflectors, and molded undertrays at scale, driving regional average costs down and improving supplier margins. Japan and South Korea, though smaller in unit terms, push the technology frontier with active wheel aerodynamics and composite fascia know-how. ASEAN projects see rapid two-wheeler electrification, spawning niche demand for airflow-friendly fairings to stretch modest battery packs.

Europe slots second in value thanks to its policy mix of low fleet CO₂ caps and pedestrian-impact rules that steer designers toward soft-edge aero add-ons. German OEMs pioneer adaptive systems like speed-sensitive spoilers, while French tier-1s provide integrated modules sold across continents. Recycling mandates in the EU also spur R&D into bio-based plastics for aero parts, adding a sustainability twist to purchasing decisions.

North America’s share centers on pickup and heavy-truck platforms where drag-cutting add-ons deliver direct fuel cost relief. CAFE escalators apply pressure on passenger cars, but U.S. suppliers highlight retrofit-ready kits to independent fleets craving fast ROI. Mexico’s export hubs increasingly specify aero sub-assemblies to meet United States requirements, broadening the regional supplier map. Smaller emerging regions like South America and the Middle East follow with slower but steady uptake as local assembly plants adopt global platforms already engineered for low drag.

Competitive Landscape

The automotive aerodynamic market shows moderate concentration. Magna packages active shutter arrays into bumper beams, trimming assembly steps for OEMs. Valeo leverages HVAC expertise to sync grille shutters with heat-pump cycles, cementing pull-through sales of thermal modules. Plastic Omnium taps injection and composite molding to supply bumpers that pass both radar transmission and low-speed crash tests, a dual compliance feat prized by global carmakers.

FORVIA integrates LED light bars inside active rear wings for LYNK & CO, illustrating how form factors merge styling and function in premium segments. Smaller innovators exploit software to challenge hardware incumbents, neural concept licenses AI solvers that help second-tier suppliers propose drag-cutting shapes without owning wind tunnels, nudging competition toward design-intelligence services.

Consolidation pressures intensify as OEM sourcing teams favor single-invoice providers covering aerodynamics, cooling, and sensor packaging. Yet white-space persists in aftermarket trucking kits where fast deployment trumps multi-function integration. This split dynamic keeps the automotive aerodynamic market competitively balanced, letting specialists coexist with giants while startups fill digital tool gaps.

Automotive Aerodynamic Industry Leaders

Magna International Inc.

Valeo SA

Plastic Omnium (OPmobility)

Röchling Automotive

Forvia SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Volvo Trucks adapts aerospace-inspired cab contours to its heavy-duty lineup, reporting drag and CO₂ cuts on production units.

- October 2024: Stellantis completes a USD 29.5 million moving-ground-plane wind tunnel to test tire-related drag, unlocking insights that can slice up to 10% of real-world aero losses.

- January 2024: Hyundai and Kia unveil Active Air Skirt technology that retracts at city speeds and deploys above 50 mph to extend EV range and improve high-speed stability.

Global Automotive Aerodynamic Market Report Scope

| Active System |

| Passive System |

| Diffusers |

| Grille Shutter |

| Side Skirts |

| Air Dam |

| Spoilers |

| Wind Deflectors |

| Others |

| Passenger Vehicle |

| Commercial Vehicle |

| Metals |

| Polymers and Plastics |

| Composites |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By System | Active System | |

| Passive System | ||

| By Application | Diffusers | |

| Grille Shutter | ||

| Side Skirts | ||

| Air Dam | ||

| Spoilers | ||

| Wind Deflectors | ||

| Others | ||

| By Vehicle Type | Passenger Vehicle | |

| Commercial Vehicle | ||

| By Material Type | Metals | |

| Polymers and Plastics | ||

| Composites | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the automotive aerodynamic market?

The market is worth USD 32.82 billion in 2025, rising toward USD 42.13 billion by 2030.

Which application area is growing fastest in automotive aerodynamics?

Grille shutters register the highest forecast growth at a 6.88% CAGR through 2030 as they merge drag reduction with cooling control.

Why are active aerodynamic systems gaining traction?

They dynamically balance drag, cooling, and downforce, which aligns with EV range goals and premium-car performance demands.

Which region leads global demand for vehicle aerodynamics?

Asia-Pacific holds a 46.25% revenue share, powered by China’s large EV production base and supportive regulations.

Page last updated on: