Vehicle Fleet Maintenance And Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 314.32 Billion |

| Market Size (2030) | USD 413.15 Billion |

| Growth Rate (2025 - 2030) | 5.62% CAGR |

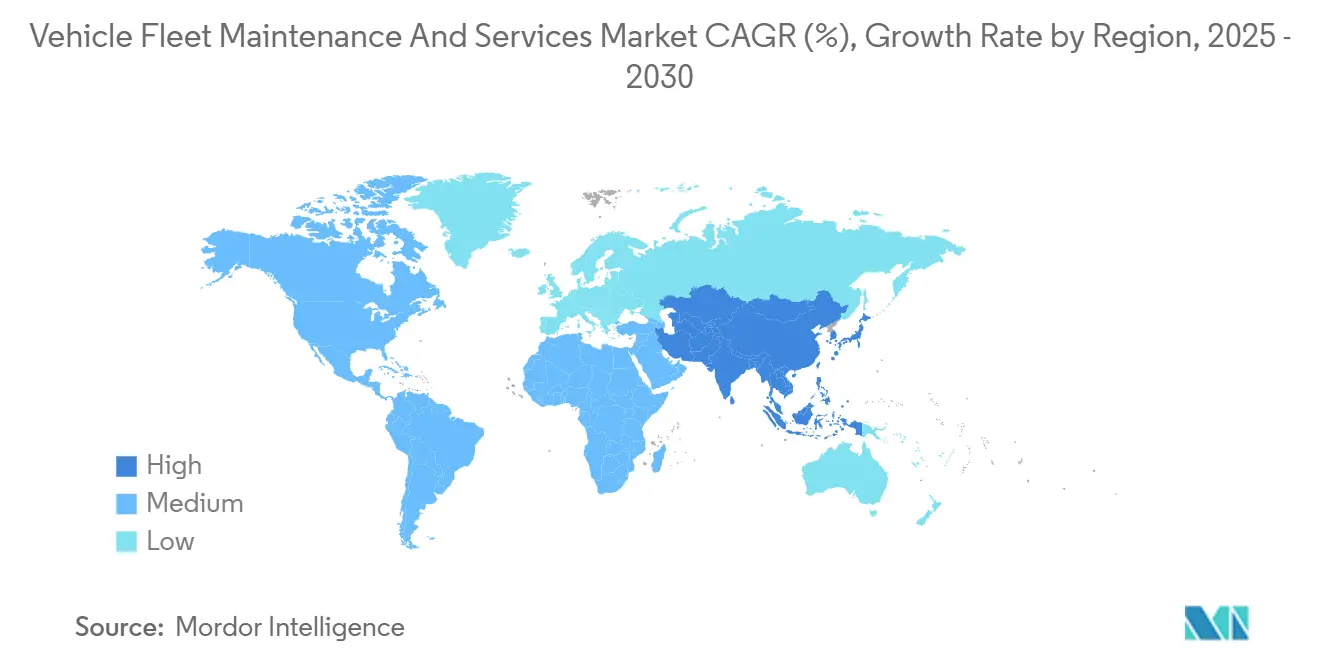

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

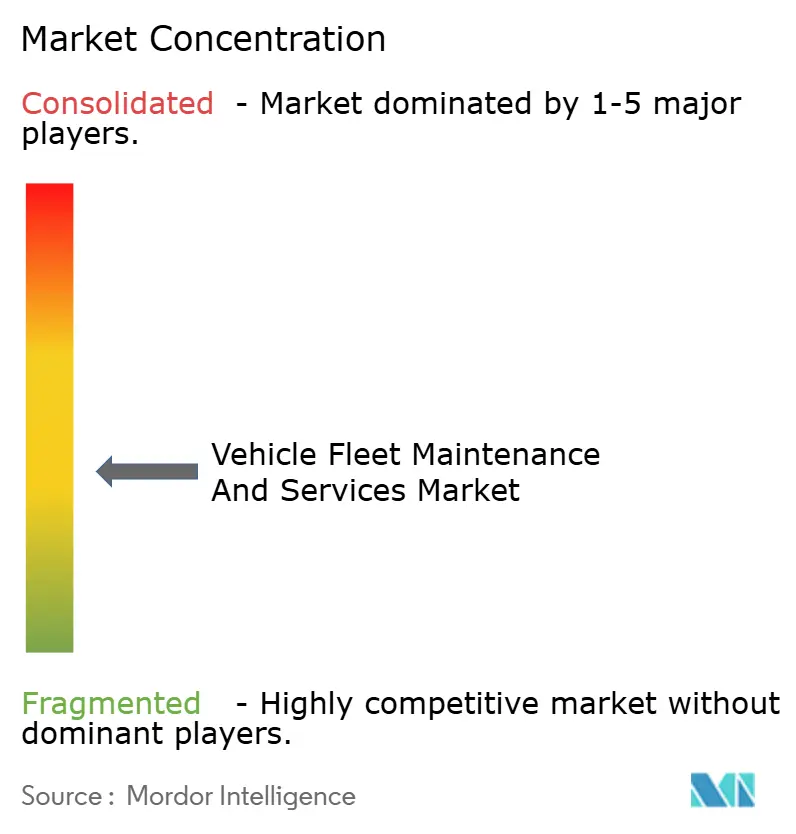

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vehicle Fleet Maintenance And Services Market Analysis by Mordor Intelligence

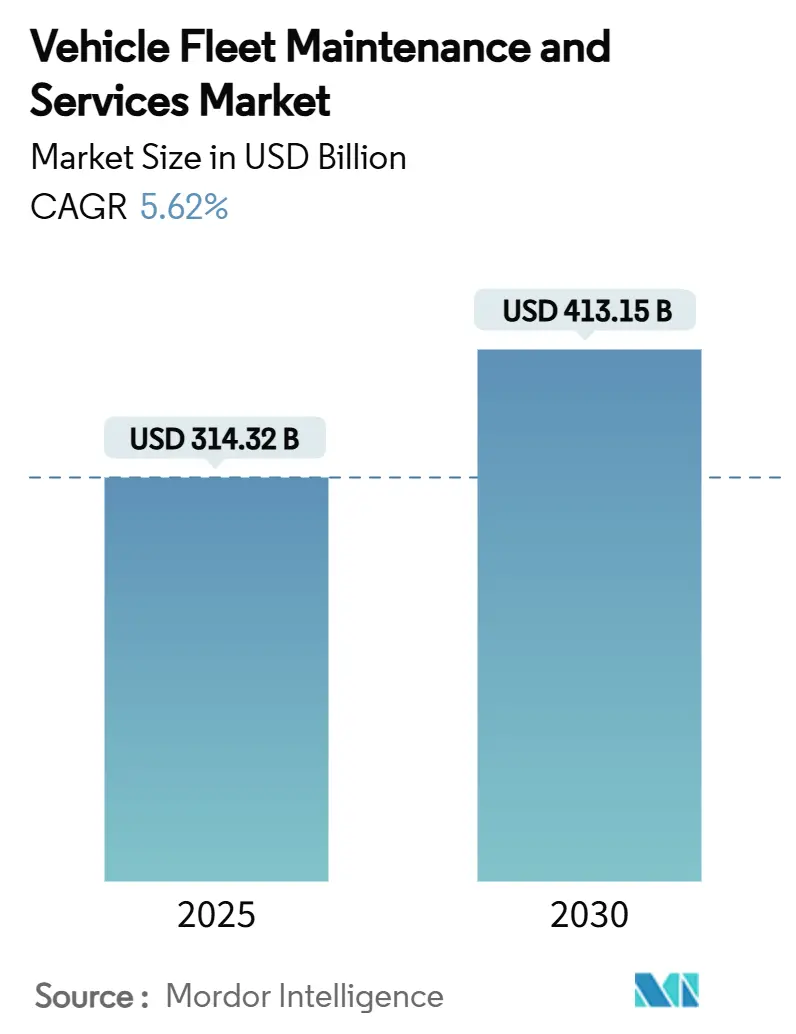

The vehicle fleet maintenance and services market was valued at USD 314.32 billion in 2025 and is forecast to reach USD 413.15 billion by 2030, translating into a 5.62% CAGR. This expansion is underpinned by stricter Federal Motor Carrier Safety Administration (FMCSA) inspection mandates, the rapid scaling of e-commerce logistics networks, and the mainstreaming of telematics-enabled predictive maintenance strategies that lower downtime and repair costs. Passenger cars still generate the largest revenue pool, yet light commercial vehicles (LCVs) are now the chief growth engine as retailers race to shorten last-mile delivery times. High vehicle utilization intensifies wear-and-tear, lifting demand for outsourced preventive maintenance packages and mobile on-site repair. Meanwhile, artificial-intelligence parts-demand forecasting and over-the-air (OTA) software updates are emerging revenue streams as fleets look beyond conventional service contracts. Consolidation is accelerating: tire majors, telematics vendors, and full-service leasing companies are acquiring midsize repair networks to build end-to-end service ecosystems that guarantee uptime and lock in parts sales.

Key Report Takeaways

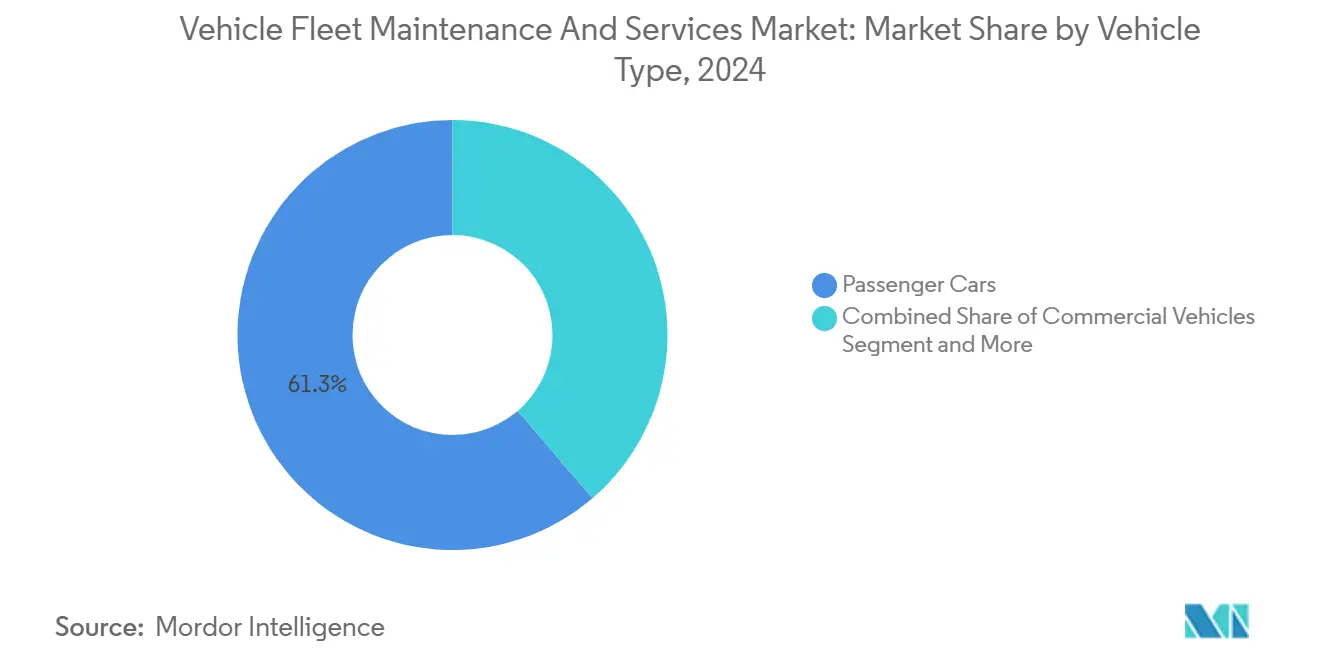

- By vehicle type, passenger cars led 61.29% of the vehicle fleet maintenance and services market share in 2024, while light commercial vehicles are projected to advance at a 9.42% CAGR through 2030.

- By service type, preventive maintenance captured 32.51% of the vehicle fleet maintenance and services market share in 2024; telematics-driven diagnostics is expected to expand at an 8.39% CAGR to 2030.

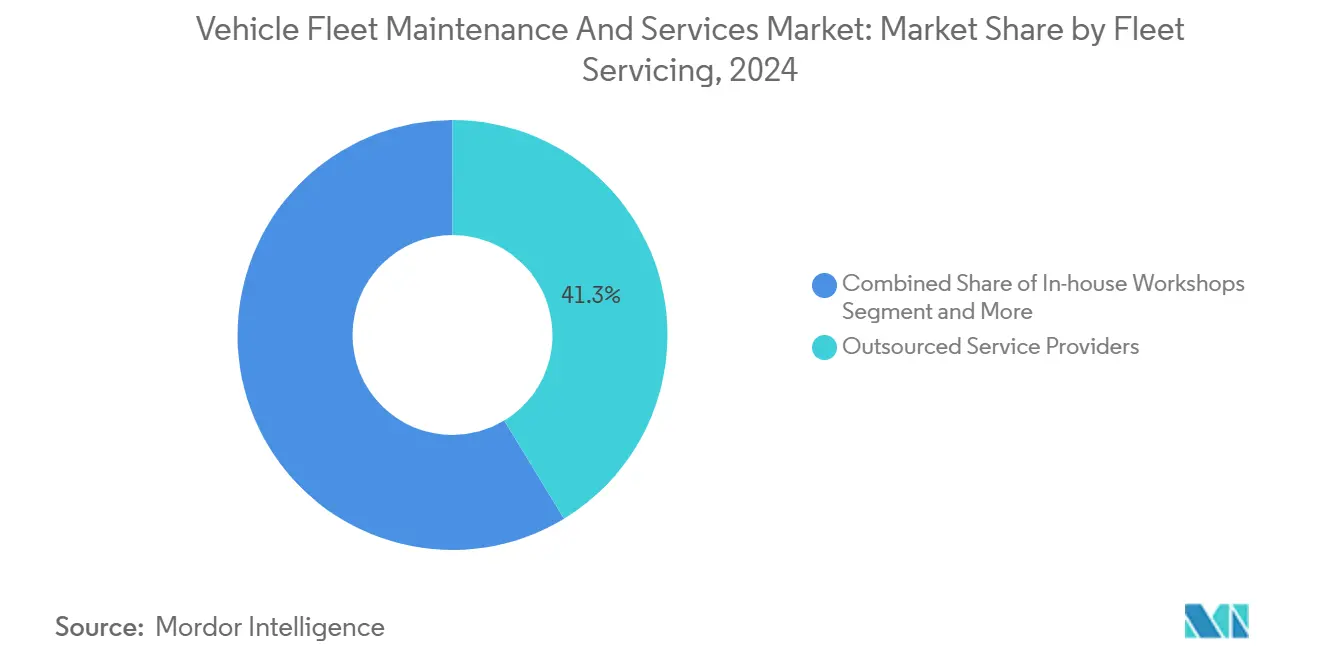

- By fleet servicing model, outsourced service providers controlled 41.32% of the vehicle fleet maintenance and services market size 2024. In contrast, mobile repair services hold the fastest growth outlook at an 8.31% CAGR to 2030.

- By ownership, private corporate fleets accounted for 42.14% of the vehicle fleet maintenance and services market share in 2024, while logistics and freight companies exhibited the highest forecast CAGR at 9.71% to 2030.

- By geography, North America commanded 37.28% of the vehicle fleet maintenance and services market share in 2024; Asia-Pacific is on track for the quickest regional expansion at an 8.63% CAGR to 2030.

Global Vehicle Fleet Maintenance And Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce-Driven Commercial Fleet Growth | +1.8% | Urban delivery corridors worldwide | Short term (≤ 2 years) |

| Telematics-Enabled Predictive Maintenance | +1.2% | North America, Europe, progressing globally | Medium term (2-4 years) |

| Rising Average Vehicle Age | +0.9% | Mature markets in North America and Europe | Long term (≥ 4 years) |

| Mandatory Safety and Emissions Inspections | +0.7% | Developed markets worldwide | Long term (≥ 4 years) |

| AI-Based Spare-Parts Forecasting | +0.7% | Asia-Pacific first movers, spreading to all regions | Medium term (2-4 years) |

| OTA Software-Enabled Service Revenues | +0.5% | Premium vehicle segments worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of E-Commerce-Driven Commercial Fleets

Last-mile parcel volumes keep climbing and are projected to push the global last-mile delivery sector. Amazon’s Delivery Service Partner hubs illustrate how concentrated driver bases create localized maintenance demand, with independent repair shops reporting higher counts of routine mirror and door-handle fixes from these vans. Same-day shipping offerings, now provided by logistics operators, compress service windows and elevate the appeal of mobile repair units that restore vehicles on the dock apron. Early pilots involving battery-electric delivery trucks—such as Uber Freight’s collaboration with WattEV—are layering high-voltage diagnostics and charging-system upkeep onto the standard service roster.

Growing Telematics-Enabled Predictive Maintenance

Most fleet managers now deploy telematics, and connected devices are fitted to a smaller number of commercial vehicles worldwide. Penske’s Catalyst AI platform sifts through 100 billion points annually, averting roughly 90,000 breakdowns annually and trimming repair times by up to 60 minutes[1]“Catalyst AI Preventive Maintenance Results,”, Penske Transportation Solutions, penske.com. Such data-driven scheduling cuts maintenance expense by 10-40% while halving unplanned downtime when benchmarked against reactive models. The resulting digital audit trail also simplifies compliance with FMCSA record-keeping rules, giving fleets tangible regulatory and economic incentives to expand deployments.

Rising Average Vehicle Age and Post-Warranty Volumes

Although replacement cycles shortened temporarily after pandemic-era shortages, most commercial vehicles now sit in the 1-4-year band, and fleets retain older units longer to defer new-vehicle expenditures. Maintenance can absorb the fleet’s operating budget, and the line item rises sharply as mechanical complexity mounts with age. FMCSA’s 49 CFR Part 396 still obliges systematic maintenance regardless of odometer readings, locking in repair demand throughout prolonged asset lifecycles.

AI-Based Parts-Demand Forecasting for Uptime Gains

Machine-learning applications in parts logistics now combine survival analysis with environmental data to pinpoint failure windows, letting distributors stage inventory closer to job sites and save carriers hours of idle time. Automotive OEMs that embedded these algorithms report 30% process-automation gains in warehouses and materially faster order-picking. In shipping fleets, similar models delivered cost relief over two-year horizons by right-sizing bulk orders and rationalizing vendor rosters[2]“Machine-Learning Optimization in Shipping Fleets,”, Journal of Industrial Engineering and Management, journaloieam.com. As semiconductor and ABS sensor shortages linger, the predictive lens has become indispensable for keeping high-utilization assets rolling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Certified Technicians | -0.8% | Acute in North America and Europe | Long term (≥ 4 years) |

| Supply-Chain Volatility for Critical Spares | -0.6% | Global, most visible in high-tech components | Short term (≤ 2 years) |

| EV Power-Train Complexity Barriers | -0.5% | Developed markets with rising EV penetration | Medium term (2-4 years) |

| Data-Ownership Conflicts | -0.4% | North America and Europe regulatory focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Technicians Inflating Labor Cost

Service centers have raised labor rates in response to intensifying wage competition. With retirements on the rise and regulatory requirements like FMCSA inspector certification narrowing the available talent pool, fleets are turning to signing bonuses and on-the-job apprenticeships. However, these strategies have led to increased maintenance costs and squeezed profit margins.

EV Power-Train Complexity Limiting Independent Shops

Independent garages struggle to justify the capital required for high-voltage tooling, insulated work bays, and OEM software subscriptions. Hertz’s experience shows EV repairs can be twice as expensive as internal-combustion fixes, driven by scarce parts and specialist labor[3]“Investor Update Q2 2025,”, Hertz Global Holdings, hertz.com. Battery replacements climb, and repair cycles run longer, eroding fleet availability at scale. While training initiatives from the National Institute for Automotive Service Excellence (ASE) are underway, uptake remains modest, leaving OEM dealer networks as the default repair channel and constraining competitive price discovery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Integration Lifts LCV Share

Passenger cars dominated revenue, contributing 61.29% of the vehicle fleet maintenance and services market share 2024. Their strength is mature dealer networks and standardized service schedules that simplify outsourcing contracts. However, the vehicle fleet maintenance and services market is witnessing a rapid pivot toward LCVs, which are forecast to post a 9.42% CAGR through 2030 as omnichannel retailers scale last-mile operations. Telematics hardware is increasingly bundled into factory specifications for vans, accelerating predictive maintenance adoption and boosting contract value per vehicle.

Higher-gross-weight trucks also gain attention as federal infrastructure spending revives freight volumes. Medium-duty units benefit from urban emission regulations that push fleets to spec cleaner powertrains. At the same time, heavy-duty tractors ride the corridor freight rebound between major ports and inland hubs. Due to harsh operating environments and specialized parts demand, off-highway machinery—mining trucks, construction loaders, and agricultural tractors—remains a niche but lucrative pocket of the vehicle fleet maintenance and services industry. Digital tire pressure monitoring and remote diagnostics now feed actionable data to centralized control towers, further linking these vehicles into mainstream service ecosystems

By Maintenance and Repair Service Type: Data-Driven Routines Redefine Value

Preventive packages held 32.51% of 2024 revenue, reinforcing their role as the foundation of every fleet’s compliance program. The segment’s growth remains steady as FMCSA rules mandate periodic inspections, yet the maturity of oil-change and brake-pad schedules caps upside. Remote fault detection allows downtime slotted into low-demand windows, raising asset availability and justifying premium service rates.

Collision repair holds stable volumes, supported by road-traffic density and insurance mandates. Emergency corrective work is gradually receding as predictive analytics redirect service into pre-failure windows. Tires, batteries, and lubricants are high-frequency items, underpinning repetitive revenue streams for national chains. Mobile repair solutions, projected to grow 8.31% annually, capitalize on driver-in-yard time to deliver repairs without towing, an efficiency that resonates with fleet uptime. OTA updates supply an emerging subscription revenue layer, particularly for electric vans whose drive-unit software can be revised without shop visits.

By Fleet Servicing Model: Outsourcing Mix Shifts Toward On-Site Support

Outsourced service providers captured 41.32% of 2024 revenue as operators doubled down on core transport activities and offloaded wrench-turning to specialists. Large conglomerates bundle parts procurement, mobile repair, and warranty administration into single invoices, shrinking back-office complexity for shippers. Hybrid models are proliferating: fleets retain in-house quick-service bays for inspections while outsourcing heavy repairs to multi-brand centers. The mobile sub-segment, expanding at an 8.31% CAGR, exemplifies this convergence; Ryder’s acquisition of Pit Stop Fleet Service grew its national mobile footprint and embedded diagnostic tech that dispatches trucks directly to downed units.

Municipal and defense fleets keep sizable in-house shops for security and mission-critical uptime. Yet even these entities trial vendor-managed inventory programs that shift parts planning to suppliers, a tactic first adopted in private trucking. Data-sharing agreements underpin such arrangements, yielding transparency but also sparking debates over intellectual-property boundaries, a restraint noted earlier.

By Fleet Ownership Type: Logistics Operators Drive Volume, Corporates Retain Scale

Private corporate fleets generated 42.14% of 2024 revenue, anchored by diversified retail and energy sectors. Their purchasing power secures bulk parts discounts, and their stable asset replacement plans give service providers predictable volumes. Logistics and freight carriers, however, will deliver the highest unit growth, adding vehicles at a 9.71% CAGR through 2030. Same-day, point-to-point delivery demands high utilization and tolerant maintenance models that absorb night-shift repairs and proactive part swaps to avoid delivery window breaches.

Rental and leasing companies present unique churn dynamics: high usage hours compress service intervals, while resale values hinge on documented maintenance history. Government fleets, governed by public tenders, favor long-term, fixed-price contracts that form a risk-mitigation anchor for providers amid market volatility.

Geography Analysis

North America retained leadership with 37.28% of revenue in 2024. FMCSA’s well-defined maintenance regulations, deep telematics penetration, and a dense network of national chains guarantee a steady stream of outsourced contracts. Yet chronic technician shortages and wage inflation are elevating cost bases, pressuring fleets to adopt mobile units that maximize billable wrench hours. Canada’s CAD 575 million modernization of Goodyear’s Napanee plant underscores continued investment in localized tire supply to support EV rollout.

Asia-Pacific will advance the fastest at an 8.63% CAGR through 2030 as China, India, and Southeast Asia modernize commercial fleets. China’s heavy-duty truck rebounded to 900,000 units in 2023, and the growing preference for gas and electric drivetrains has multiplied specialized service requirements. India’s wider adoption of preventive maintenance contracts, now bundled with financing packages, is accelerating after supply-chain shocks nudged carriers toward uptime guarantees. However, fragmented service coverage and varying national regulations temper near-term profitability.

Europe maintains solid, regulation-driven growth. Euro VI emission standards and the EU Data Act’s owner-data access provisions encourage predictive maintenance investment while creating legal clarity over telematics streams. Bridgestone’s strategic pullback from China to refocus on premium European passenger markets indicates sharpening regional specializations. Elsewhere, Gulf Cooperation Council states and Latin America represent emerging plays, combining growing construction activity with relatively young service infrastructures that invite foreign joint ventures.

Competitive Landscape

The competitive field scores as moderately concentrated. Ryder System’s USD 302 million purchase of Cardinal Logistics enhanced its route-based maintenance volumes. Cox Automotive’s fleet division scaled beyond 1,500 technicians by blending acquisitions with its FleeTec Academy pipeline to neutralize the labor shortage.

Tire manufacturers use connected-tire data to cross-sell maintenance packages. Goodyear’s tires-as-a-service subscription reduced emergency breakdowns by 80% for pilot fleets, proving that data-enabled models can syndicate rubber and repair labor. Bridgestone’s collaboration with Geotab merges tire and vehicle telematics, offering fleets a dashboard that flags pressure anomalies and automatically schedules service calls. Telematics vendors are equally acquisitive, integrating mobile repair firms to monetize diagnostic alerts within minutes of a fault code surfacing. Independent repair networks, while fragmented, are clustering via franchising to defend local relationships

Vehicle Fleet Maintenance And Services Industry Leaders

Bridgestone Fleet Solutions

The Goodyear Tire & Rubber Company

Continental AG

Bosch Mobility Services

Penske Truck Leasing

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Amerit Fleet Solutions aligned with New Mountain Capital to accelerate geographic expansion, adding field technicians and mobile units.

- July 2024: Ryder acquired Pit Stop Fleet Service, integrating its proprietary mobile-repair software and technicians into Ryder’s service matrix.

Global Vehicle Fleet Maintenance And Services Market Report Scope

| Passenger Cars | |

| Commercial Vehicles | Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches | |

| Tractors | |

| Off-Highway Vehicles |

| Preventive Maintenance |

| Telematics-driven Diagnostics |

| Body-shop Collision Repairs |

| Emergency/Corrective Repairs |

| Tires, Brakes, Batteries & Lubricants |

| Others |

| In-house Workshops |

| Outsourced Service Providers |

| Mobile Repair Services |

| Others (Hybrid Models) |

| Private Corporate Fleets |

| Government Fleets |

| Rental and Leasing Companies |

| Logistics and Freight Companies |

| Others (Agriculture, Energy, etc.) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Spain | |

| Italy | |

| France | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East & Africa |

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| Tractors | ||

| Off-Highway Vehicles | ||

| By Maintenance and Repair Service Type | Preventive Maintenance | |

| Telematics-driven Diagnostics | ||

| Body-shop Collision Repairs | ||

| Emergency/Corrective Repairs | ||

| Tires, Brakes, Batteries & Lubricants | ||

| Others | ||

| By Fleet Servicing | In-house Workshops | |

| Outsourced Service Providers | ||

| Mobile Repair Services | ||

| Others (Hybrid Models) | ||

| By Fleet Ownership Type | Private Corporate Fleets | |

| Government Fleets | ||

| Rental and Leasing Companies | ||

| Logistics and Freight Companies | ||

| Others (Agriculture, Energy, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Spain | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How big is the vehicle fleet maintenance and services market in 2025?

The sector generated USD 314.32 billion in revenue during 2025 and is set to grow to USD 413.15 billion by 2030.

What is the expected CAGR for fleet maintenance services through 2030?

The market is projected to expand at a 5.62% CAGR over the 2025-2030 period.

Which vehicle category will grow fastest in service demand?

Light commercial vehicles are forecast to post a 9.42% CAGR, driven by e-commerce delivery fleets.

Why is predictive maintenance becoming mainstream?

Telematics and AI analytics reduce total maintenance spend by up to 40% and cut downtime by half while supporting FMCSA compliance.

How are mobile repair services changing fleet upkeep?

Mobile technicians eliminate the need for vehicle shuttles, supporting uptime targets and are projected to grow 8.31% annually.

Page last updated on: