Automotive Air Deflector Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

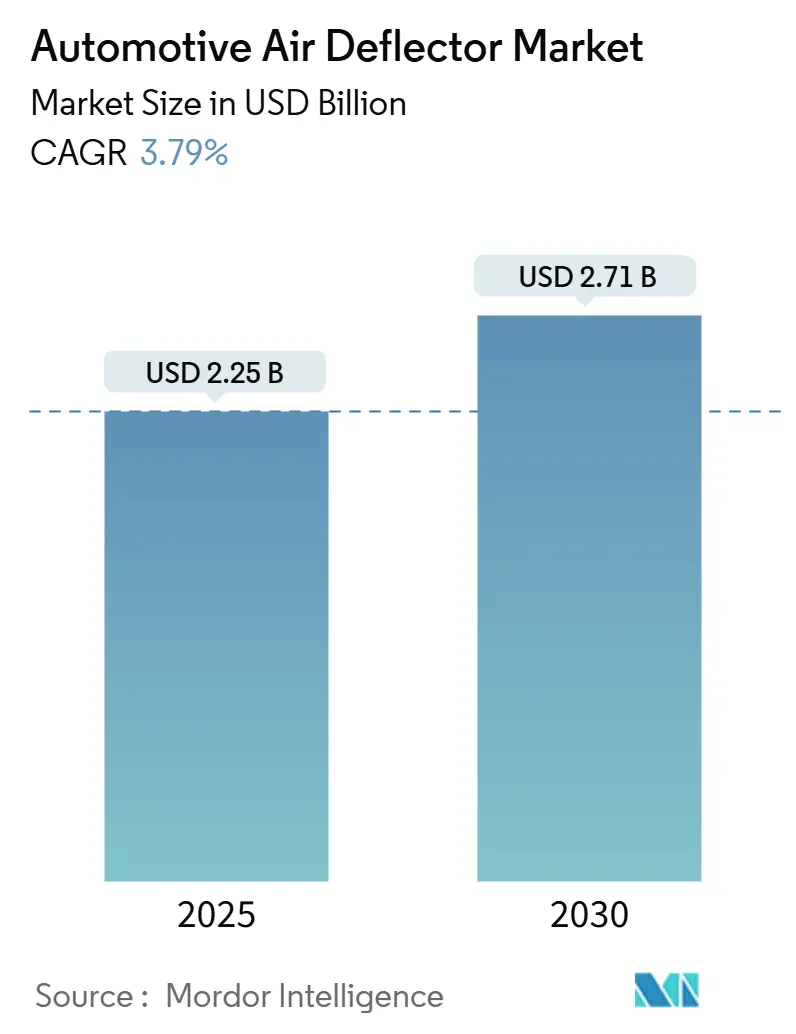

| Market Size (2025) | USD 2.25 Billion |

| Market Size (2030) | USD 2.71 Billion |

| Growth Rate (2025 - 2030) | 3.79% CAGR |

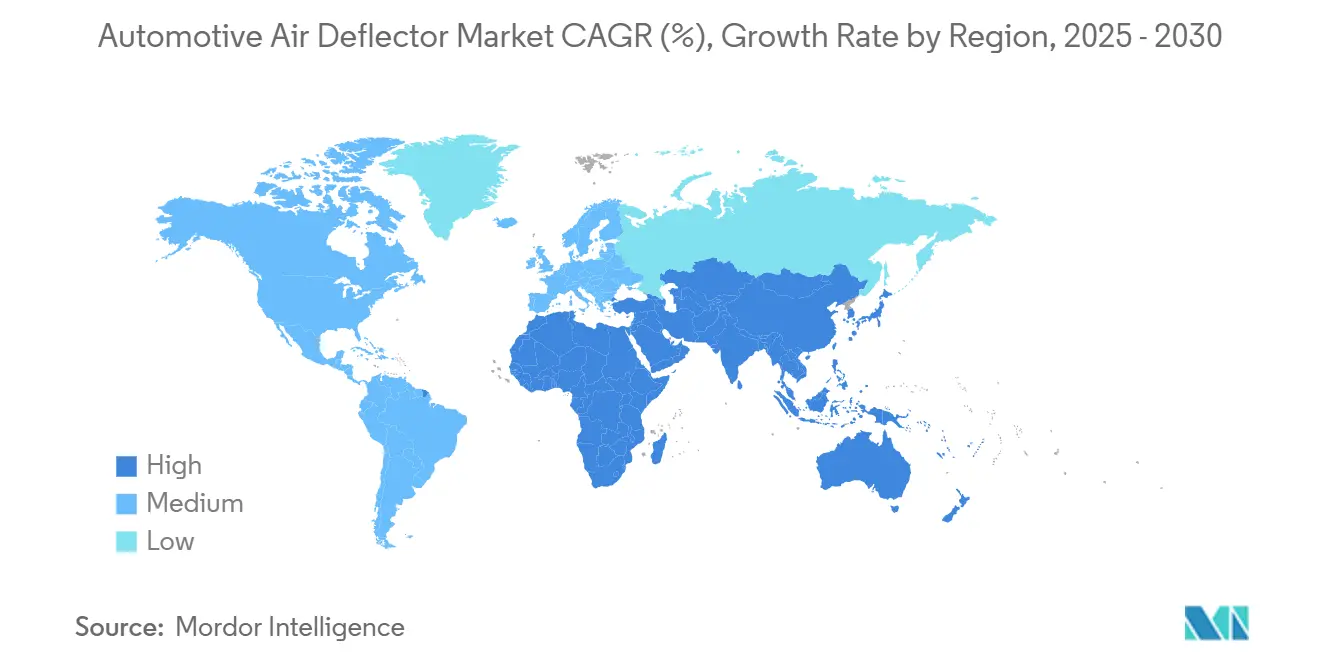

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Air Deflector Market Analysis by Mordor Intelligence

The Automotive Air Deflector Market size is estimated at USD 2.25 billion in 2025, and is expected to reach USD 2.71 billion by 2030, at a CAGR of 3.79% during the forecast period (2025-2030). As regulatory bodies tighten fuel-economy rules and automakers focus on aerodynamic optimization, consumers increasingly lean towards efficiency-driven accessories. This shift underscores the maturation of the market. Current supportive measures include the U.S. EPA's CAFE framework, aiming for 2% annual fuel-efficiency gains through 2031, Europe's cap of 95 g/km for passenger-car CO₂ emissions, and the ongoing range anxiety felt by electric-vehicle owners. In response, suppliers are adopting AI-driven design tools, streamlining prototyping cycles and exploring complex geometries once deemed too costly. Additionally, regionalization spurred by tariffs is pushing composite production closer to home, with value chains now gravitating towards Mexico, Southeast Asia, and Eastern Europe. While price fluctuations in polypropylene, ABS, aluminum, and steel pose challenges to margin expansion, a robust replacement demand in the aftermarket and a surge in OEM integrations buffer against these challenges in the broader automotive air deflector market.

Key Report Takeaways

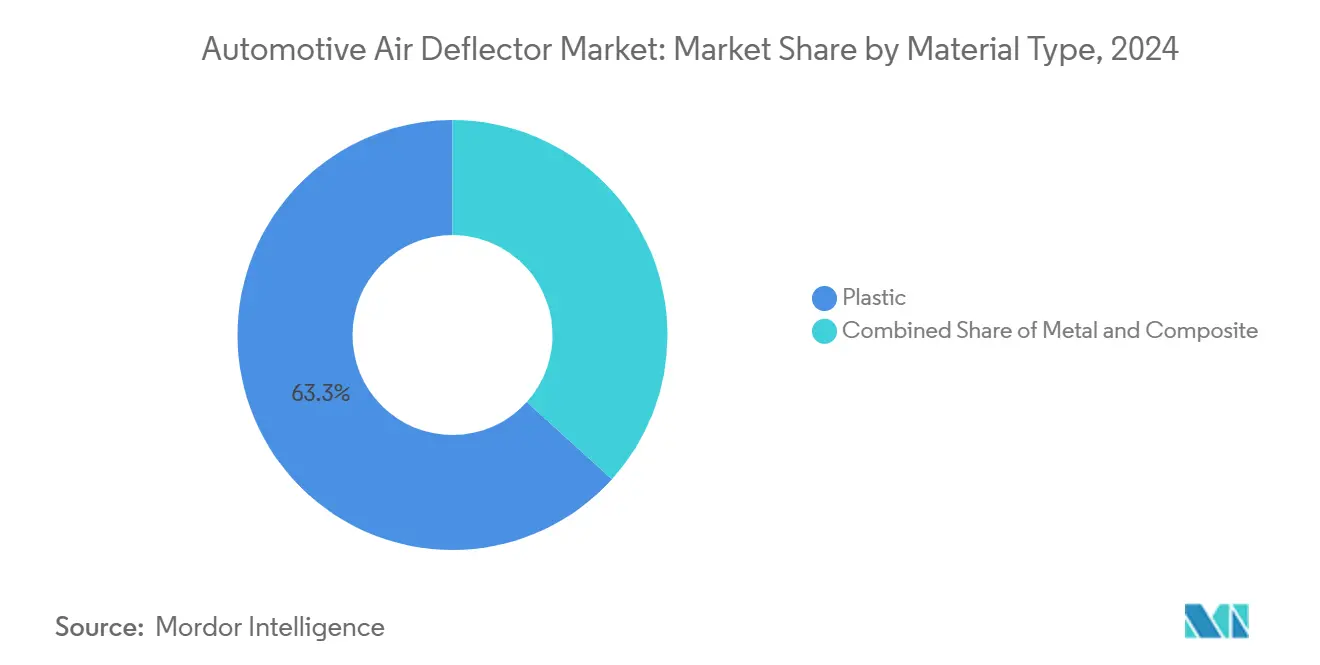

- By material, plastics dominated the automotive air deflector market with a 63.28% share in 2024, whereas the composites segment is expected to grow at a 3.81% CAGR during the forecast period (2025-2030).

- By vehicle type, passenger cars led with a 56.67% share of the automotive air deflector market in 2024; medium and heavy commercial vehicles are expected to expand at a 3.88% CAGR during the forecast period (2025-2030).

- By design, side deflectors commanded a 57.83% share of the automotive air deflector market in 2024, while the roof deflector segment is expected to grow at a 3.85% CAGR during the forecast period (2025-2030).

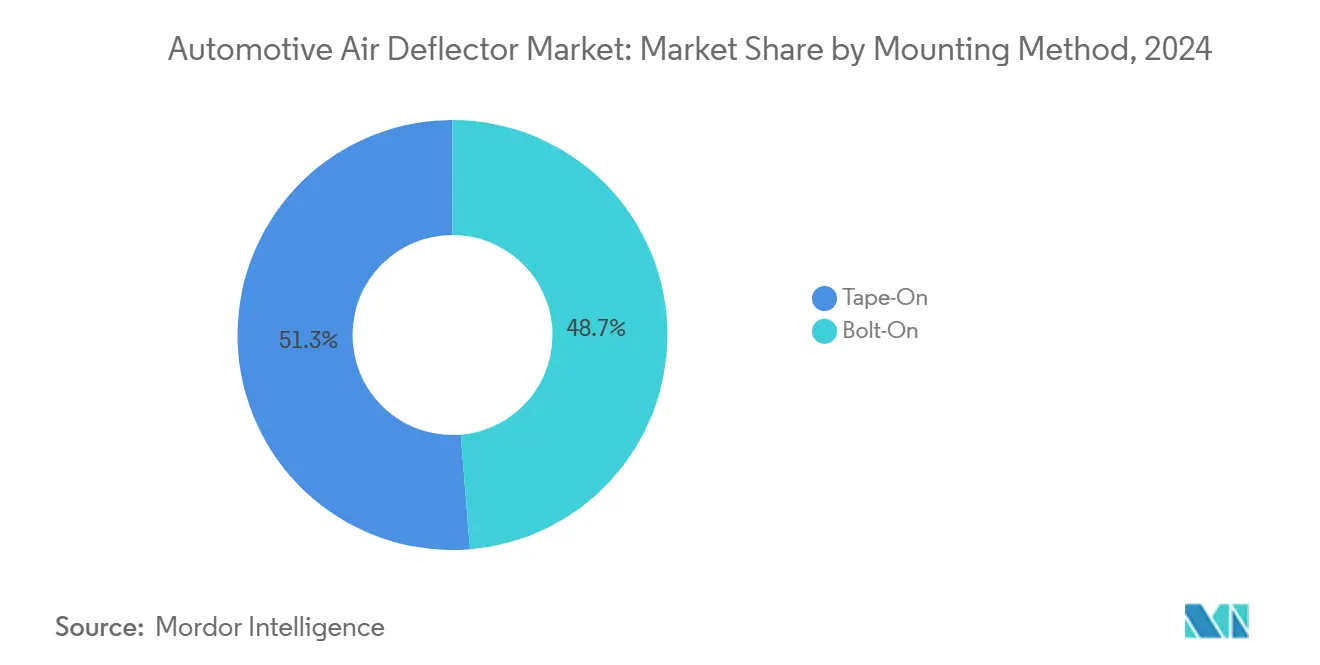

- By mounting, tape-on products held a 51.28% share of the automotive air deflector market in 2024; the bolt-on segment is expected to grow at a 3.83% CAGR during the forecast period (2025-2030).

- By sales channel, the aftermarket accounted for a 54.51% share of the automotive air deflector market in 2024, with OEM fitment forecast to scale at a 3.91% CAGR during the forecast period (2025-2030), on the back of integrated aerodynamic packages.

- By geography, Asia-Pacific controlled 39.81% of global volume in 2024; the Middle East and Africa are positioned for the fastest 3.92% CAGR during the forecast period (2025-2030).

Global Automotive Air Deflector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Global Fuel-Economy / CO₂ Rules | +0.8% | Global, with strongest impact in North America and EU | Long term (≥ 4 years) |

| Rising Global Production | +0.6% | Global, Asia Pacific core with spill-over to Americas | Medium term (2-4 years) |

| Surge In Aftermarket Styling & Comfort Parts | +0.4% | North America and Europe primarily, expanding to Asia Pacific | Short term (≤ 2 years) |

| OEM Focus On EV Range-Gain | +0.5% | Global, led by China and EU EV markets | Medium term (2-4 years) |

| AI-Driven Rapid Prototyping Cuts Design Cycles | +0.3% | Global, concentrated in major automotive hubs | Short term (≤ 2 years) |

| Tariff-Led Near-Shoring Of Composite Deflectors | +0.2% | North America and Mexico, secondary impact in EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Fuel-Economy / CO₂ Rules

Stringent efficiency targets form the most structural growth catalyst for the automotive air deflector market. From 2030 to 2032, fuel efficiency for heavy-duty pickup trucks and vans will rise by 10% annually, followed by an 8% annual increase from 2033 to 2035[1]“USDOT Finalizes New Fuel Economy Standards for Model Years 2027-2031,” National Highway Traffic Safety Administration, nhtsa.gov. Europe enforces its 95 g/km passenger-car cap with further cuts envisioned for commercial vehicles[2]“CO₂ Emission Performance Standards for Cars and Vans,” European Commission, ec.europa.eu . These rules encourage OEMs to embed air deflectors that cut drag coefficients by 0.015–0.030, enough to lower energy consumption by a minimum at highway speed. Automakers now specify deflectors during the clay-model phase rather than as late accessories, channeling reliable volume toward tier-one suppliers. Marketing claims that spotlight verified aerodynamic delta reinforces buyer interest and enables compliance cost pass-through. Successively, long-tail demand visibility justifies supplier outlays on advanced materials and automated production lines.

Rising Global Production of SUVs & Pickups

SUV and pickup assembly hits almost half a billion units worldwide in 2024, a slight jump over 2023, and this body style depicts frontal areas one-fourth larger than sedans[3]“2024 Production Statistics,” International Organization of Motor Vehicle Manufacturers, oica.net . The bulkier silhouette magnifies drag, elevating the relevance of side, roof, and rear deflectors within the automotive air deflector market. Electrified SUVs—once penalized by added battery weight—now rely on aero add-ons to recoup lost range, making deflectors mission-critical rather than cosmetic. Pickup fleets turn to tailgate and bed-cap aerodynamics to slice turbulence that inflates fuel expense. As OEMs bring battery-electric trucks online, each watt-hour saved through improved drag extends real-world range, cementing deflector placement as standard content in higher trims.

Surge in Aftermarket Styling & Comfort Parts

The global automotive aftermarket will grow exponentially by 2030, and styling components will outpace core replacement parts. Tape-on window and hood deflectors escalate because installation takes less than 15 minutes with zero drilling. E-commerce storefronts and social-influencer campaigns propel design-centric variants toward Gen Z car owners in mature markets. Aesthetic differentiation, wind-noise reduction, and venting comfort converge to uphold aftermarket dominance in the automotive air deflector market, even as OEM share creeps upward. During macroeconomic slowdowns, drivers upgrade existing cars rather than purchase new ones, stabilizing deflector sales volumes.

OEM Focus on EV Range-Gain via Aero Add-Ons

Electric-vehicle architectures host smooth underbodies, sealed grilles, and in-wheel aero covers; air deflectors complement these systems by managing localized turbulence. Tesla's Model S, with its state-of-the-art aerodynamic design, leads the industry in efficiency, thanks in part to its adaptive deflectors. Stellantis has strategically invested in advanced testing infrastructure, notably a dedicated aerodynamic tunnel for electric vehicles. This facility aids in validating dynamic deflector systems across different ride-height scenarios. New technologies, like deployable side blades, are setting the standard for the future. They strike a perfect balance between optimal performance at high speeds and the necessary clearance for city driving. Range anxiety drives buyers to prioritize every additional mile, converting aero accessories from nice-to-have to performance differentiators across premium and mass segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Prices Of Plastics & Light Metals | -0.4% | Global, with acute impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Fitment & Warranty Concerns | -0.2% | North America and Europe primarily | Medium term (2-4 years) |

| ADAS-Sensor Interference Risks | -0.3% | Global, concentrated in premium vehicle segments | Medium term (2-4 years) |

| 2025 Micro-Plastic Exterior Regulations | -0.1% | California and EU initially, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Plastics & Light Metals

Due to feedstock shortages and logistics snarls, polypropylene and ABS quotations swung two-fifths during 2024. Aluminum and automotive-grade steel followed similar patterns, raising BOM costs on brackets and fasteners. For suppliers fighting thin margins, quarterly repricing invites pushbacks from catalog distributors and big-box retailers. Larger tier-ones hedge through long-term resin contracts, but small and medium enterprises lack such leverage. Continued raw-material turbulence may delay capex on advanced molds or deter product-line refreshes within the automotive air deflector market.

Fitment & Warranty Concerns in the Crowded Aftermarket

A profusion of off-brand deflectors sold via online marketplaces spawns customer complaints about wind noise, paint damage, and water leakage. OEMs warn that improper installations void corrosion warranties, dampening consumer confidence. Reputable brands now highlight vehicle-specific CAD models and OE-grade adhesives to restore trust, yet the reputational damage curbs impulse purchases. Professional installers benefit, but higher labor fees erode the affordability thesis that fuels aftermarket growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Composites Gain Despite Plastic Dominance

Plastic continued to hold a 63.28% stake in 2024, anchoring the automotive air deflector market size for high-volume trims and cost-sensitive aftermarket kits. Composites are forecast to expand at a 3.81% CAGR, supported by two-fifths weight savings versus plastics and growing OEM appetite for energy-efficient parts. Within composites, glass-fiber reinforced resins balance cost and rigidity, while carbon fiber finds traction in performance badges and premium EVs. Suppliers exploit automated fiber placement to curb scrap rates and pursue repeatable texture finishes that rival painted ABS. This progress invites wider adoption as automakers chase fleet CO₂ credits and range gains.

Adhesive suppliers simultaneously introduce low-VOC bonding agents compatible with composite substrates, ensuring durable adhesion under temperature cycling—a critical milestone for warranty coverage, with raw-material learning curves now plateauing, composite fabrication times edge closer to injection-molded plastics, diminishing earlier cycle-time disadvantages. These advances underpin the expectation that composites will outpace the overall automotive air deflector market through 2030, though plastics remain the volume mainstay thanks to entrenched tooling and distributor familiarity.

By Vehicle Type: Commercial Vehicles Drive Growth

Passenger-car platforms maintained a 56.67% revenue contribution during 2024 as sedans, hatchbacks, and crossovers populate mainstream showrooms. Nevertheless, medium & heavy truck demand spearheads incremental gains with a forecast 3.88% CAGR, reflecting diesel-price sensitivity among logistics operators. EPA SmartWay certifications incentivize fleets to spec roof-fairing and side-skirt deflectors that lower drag slightly, translating to real-world fuel savings of 3–5 mpg on long-haul routes. Fleet ROI calculations deliver payback within 18 months, driving procurement volumes across Class 8 tractors.

Light commercial vans—integral to last-mile ecommerce deliveries—also subscribe to aero packages, particularly because stop-and-go duty cycles amplify the benefit of smoother airflow at sub-highway speeds. Two-wheeler deflectors occupy a niche but profitable pocket, chiefly on touring motorcycles that command premium accessory budgets. Combined, these trends elevate commercial vehicles from supporting role to principal growth engine inside the automotive air deflector market.

By Design Type: Side Deflectors Lead Market

Side deflectors preserved a 57.83% slice of 2024 orders, favored for their high visual impact and straightforward tape-on installation. They redirect rainwater and curb wind buffeting, enhancing cabin comfort without extensive fabrication changes. Though niche last decade, roof deflectors are primed for a 3.85% CAGR as SUVs and crossovers dominate global sales. Wind-tunnel-validated roof blades trim wake turbulence and mitigate roof-rack drag, an attribute particularly valued by EV buyers.

Front-lip deflectors sketched momentum inside performance sub-segments, benefitting from carbon-look composite skins that mirror OEM body-kits. Rear deflectors on pickups and fastback crossovers address low-pressure zones behind the tailgate or hatch glass, smoothing exit airflow and reducing minor lift. Emerging active deflector modules underscore innovation, deploying only at speed to balance aesthetics and functional gains, thereby enriching SKU diversity across the broader automotive air deflector market.

By Mounting Method: Installation Simplicity Drives Adoption

Tape-on adhesives accounted for 51.28% shipment share in 2024, courtesy of 3M VHB tapes that bond firmly yet allow nondestructive removal. Retail consumers appreciate the no-drill reassurance when seeking style upgrades. Adhesive formulations resist UV degradation and car-wash chemicals, pushing warranty terms to five years or longer. While representing a smaller base, bolt-on fixtures register a 3.83% CAGR due to heavy-duty pickup and van customers who desire maintenance-proof attachments that can withstand off-road jolts.

In-channel window deflectors carve a specialized footprint within factory glass channels for OEM-like integration. Though installation demands precision, their flush profile satisfies buyers chasing streamlined looks. Altogether, mounting technologies converge toward faster installation, reversible removal, and OEM finish—all vital features that retain buyer loyalty in the competitive automotive air deflector market.

By Sales Channel: Aftermarket Leads Despite OEM Growth

The aftermarket remained dominant with a 54.51% share in 2024, buoyed by online platforms that bundle free shipping, video tutorials, and loyalty points. Social-media influencers broadcast before-and-after aero gains, amplifying word-of-mouth at minimal cost to suppliers. Nonetheless, OEM take rates log a 3.91% CAGR to 2030 because automakers now integrate aero kits into trim packages and dealer accessories, treating deflectors as a compliance lever rather than décor.

OEM fitment guarantees factory paint match, sensor compliance, and inclusion within vehicle financing—a trifecta attractive to buyers. Suppliers that secure global sourcing agreements escalate volume predictability, unlocking economies of scale absent in long-tail aftermarket SKUs. As a result, the automotive air deflector market splits into mass aftermarket personalization and high-spec OEM functional integration, each with distinct profit pools.

Geography Analysis

Asia-Pacific anchored 39.81% of global deliveries in 2024, underpinned by China’s powerhouse assembly footprint and ASEAN’s cost-competitive component clusters. Shanghai and Guangzhou host tier-one suppliers that feed domestic brands and joint ventures in the United States. Thailand, Vietnam, and Indonesia amplify capacity, benefiting from favorable tariffs and rising regional demand. OEMs localize composite lay-ups to bypass freight and respond swiftly to design tweaks, bolstering the region's automotive air deflector market’s resilience.

North America preserves a sizable slice on the strength of a vibrant aftermarket culture and an outsized pickup mix. The United States enforces sharp fuel-economy improvements, pushing OEMs to include deflectors in aero packages. Using USMCA certainty and lower logistics costs, Mexico emerges as a composite manufacturing hub for the United States truck and SUV programs. Extensive brick-and-mortar installer networks anchor repeat sales for tape-on and in-channel window deflectors.

The Middle East and Africa represent the fastest-rising region at a forecast 3.92% CAGR through 2030. Saudi Arabia’s Vision 2030 auto strategy stimulates downstream component needs, while the United Arab Emirates acts as a re-export hub into North and East Africa. Morocco, South Africa, and Kenya nurture nascent assembly lines, creating greenfield opportunities for pathfinder suppliers. Harsh desert climates elevate demand for durable UV-stable materials, nudging suppliers to develop specialized resin blends, reinforcing brand differentiation in this frontier slice of the automotive air deflector market.

Competitive Landscape

The market remains moderately fragmented; no single actor exceeds a one-fifth global invoice share, leading to a lively mix of regional specialists and multinational tier-ones. Röchling Automotive pioneers active aero modules that deploy automatically above highway speed, a feature now piloted on two German luxury platforms. Inteva Products expanded its Pune site by three-fifths of its capacity in November 2024, targeting APAC OEM contracts for roof and side deflectors. Deflecto Acquisition, absorbed by Acacia Research in October 2024, gains capital to scale HVAC and commercial-truck aero accessories across the United States regions.

Technology rather than price defines competitive edges. AI-enabled simulation locks design rounds to days, not months, while automated composite lay-up presses secure consistent fiber distribution. IP filings surround electromagnetic-transparent materials compatible with radar frequencies, an emerging moat as ADAS penetration accelerates.

Strategic partnerships with adhesive formulators and e-commerce storefronts deliver holistic solutions from virtual design to end-user doorstep, fortifying brand equity in the evolving automotive air deflector market.

Automotive Air Deflector Industry Leaders

Auto Ventshade

Hatcher Components

Piedmont Plastics

ClimAir UK Ltd

FARAD Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Inteva Products invested USD 3.3 million to expand its Pune, India plant, adding five assembly lines for aerodynamic accessories.

- October 2024: Acacia Research Corporation completed the purchase of Deflecto Acquisition, Inc., enhancing distribution breadth inside commercial transport segments.

- October 2024: Stellantis committed USD 29.5 million toward a new wind tunnel dedicated to EV aero optimization, including integrated deflector validation capabilities.

Global Automotive Air Deflector Market Report Scope

| Plastic |

| Metal |

| Composite |

| Two-Wheeler |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Front Air Deflectors |

| Rear Air Deflectors |

| Side Air Deflectors |

| Roof Air Deflectors |

| Tape-On |

| Bolt-On |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Plastic | |

| Metal | ||

| Composite | ||

| By Vehicle Type | Two-Wheeler | |

| Passenger Vehicles | ||

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| By Design Type | Front Air Deflectors | |

| Rear Air Deflectors | ||

| Side Air Deflectors | ||

| Roof Air Deflectors | ||

| By Mounting Method | Tape-On | |

| Bolt-On | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the automotive air deflector market by 2030?

The market is expected to reach USD 2.71 billion, reflecting a 3.79% CAGR from 2025 to 2030.

Which region currently leads in demand?

Asia-Pacific holds 39.81% of global shipments, propelled by China’s output and ASEAN expansion.

Which design type has the highest share?

Side deflectors command 57.83% of 2024 demand due to easy tape-on installation and aesthetic appeal.

Why are OEMs adding deflectors to electric vehicles?

Integrated deflectors help cut drag, improve range, and satisfy efficiency targets, easing range anxiety.

How do tariffs affect supply chains?

A 25% U.S. duty moved composite manufacturing closer to North-American OEMs, mainly into Mexico.

Which material category is growing fastest?

Composites should post a 3.81% CAGR, driven by 40% weight savings and advanced fuel-economy goals.

Page last updated on: