Automotive Software Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

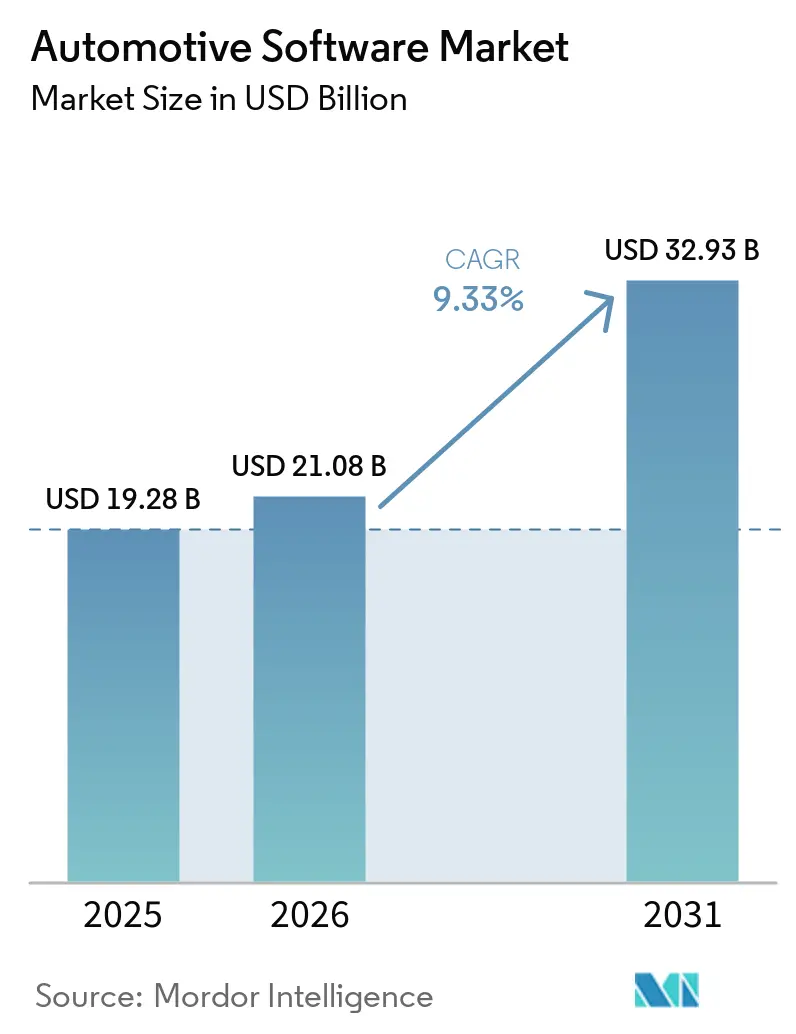

| Market Size (2026) | USD 21.08 Billion |

| Market Size (2031) | USD 32.93 Billion |

| Growth Rate (2026 - 2031) | 9.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Software Market Analysis by Mordor Intelligence

The automotive software market size is expected to grow from USD 19.28 billion in 2025 to USD 21.08 billion in 2026 and is forecast to reach USD 32.93 billion by 2031, advancing at a 9.33% CAGR during the forecast period (2026 to 2031). Centralized compute platforms, continuous over-the-air (OTA) update pipelines, and subscription-based feature monetization are reshaping competitive priorities for vehicle manufacturers and suppliers. Software spend is rising fastest in battery-electric architectures, where energy-management algorithms, thermal strategies, and cloud-linked diagnostics replace legacy mechanical complexity. Regulatory mandates in Europe and North America requiring secure OTA infrastructure are forcing every program to embed hardware security, encryption, and vulnerability-monitoring capabilities. Meanwhile, Chinese original-equipment manufacturers (OEMs) are offering Level-2+ driver-assistance features free of charge, accelerating code volume growth but compressing near-term monetization. Across regions, the automotive software market is evolving from a traditional license model toward recurring revenue streams tied to post-sale digital services, making middleware and operating-system control central to long-term profitability.

Key Report Takeaways

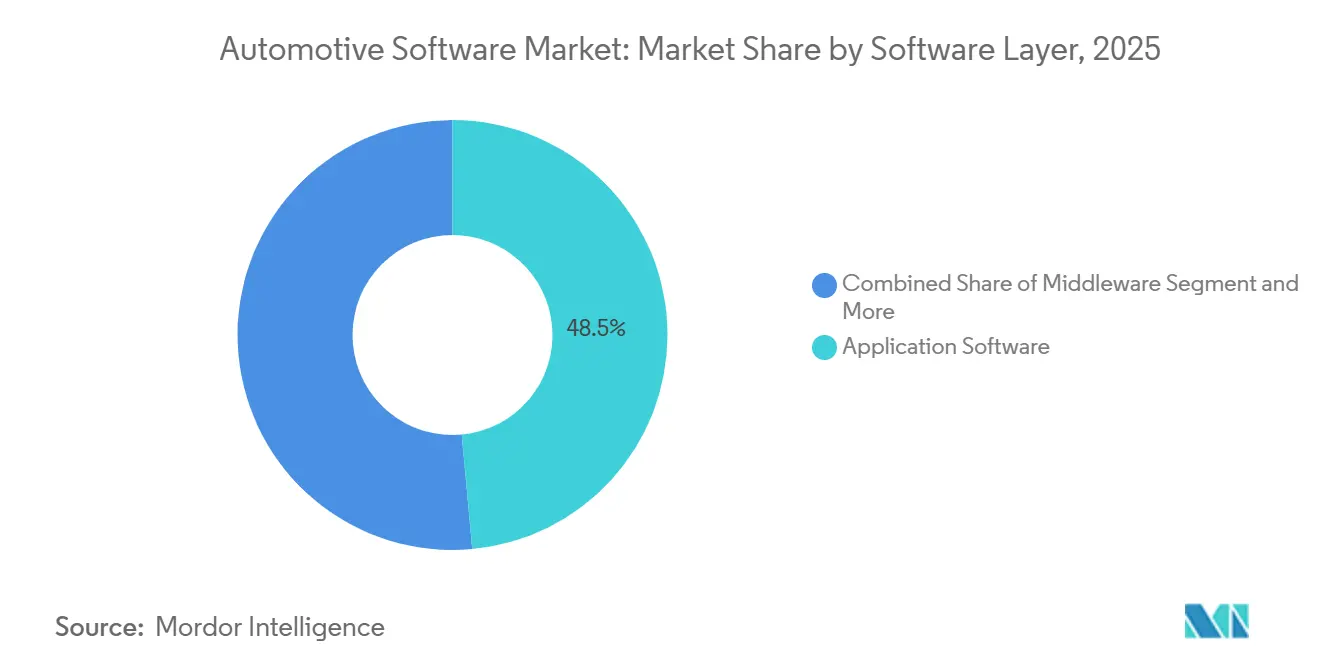

- By software layer, application software accounted for 48.53% of the automotive software market share in 2025, while operating-system platforms are forecast to expand at a 9.82% CAGR through 2031.

- By application, ADAS and safety systems led with 33.76% of the automotive software market share in 2025; powertrain and battery-management software are expected to grow at a 13.35% CAGR through 2031.

- By vehicle type, passenger cars accounted for 74.91% of the automotive software market size in 2025, whereas light commercial vehicles are projected to advance at a 9.77% CAGR over the same period.

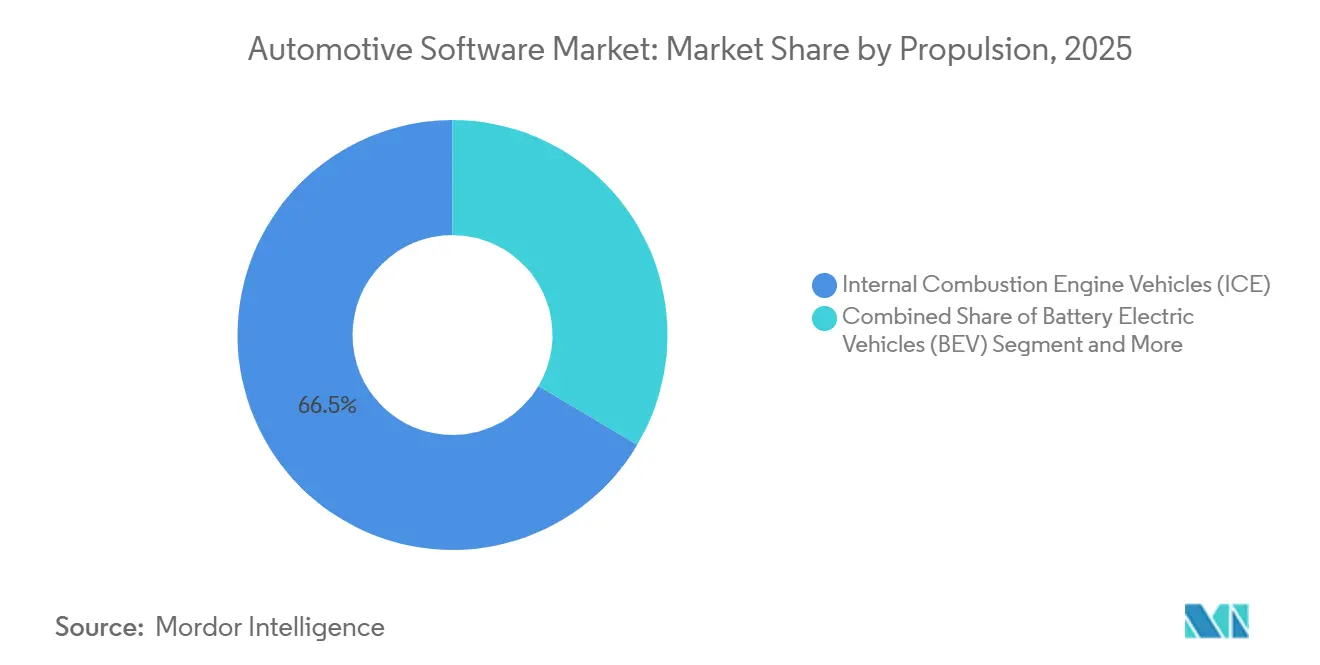

- By propulsion type, internal-combustion vehicles accounted for 66.47% of the automotive software market share in 2025, yet battery-electric vehicles are poised for an 18.94% CAGR through 2031.

- By deployment model, on-board embedded code captured 92.84% of the automotive software market share in 2025, and off-board cloud or edge services are forecasted to climb at a 17.44% CAGR through 2031.

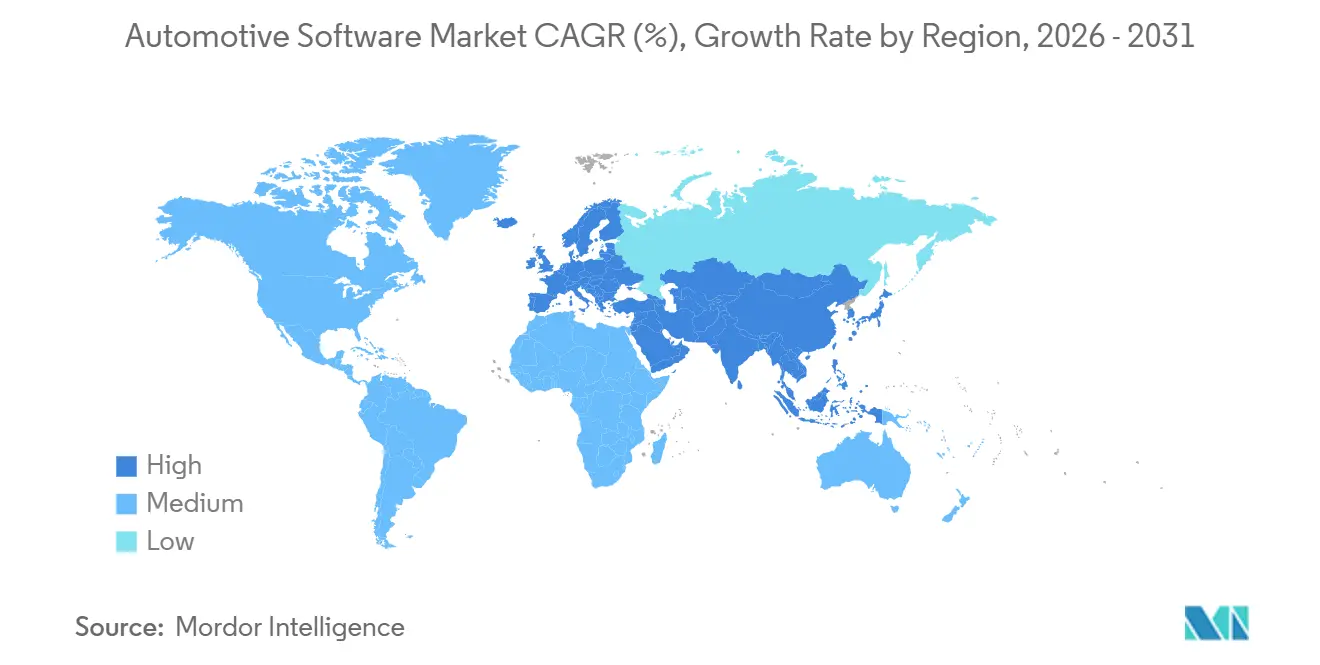

- By geography, Asia-Pacific held 39.04% of the automotive software market share in 2025 and is forecast to expand at a 11.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Automotive Software Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Centralized Zonal E/E Architectures | +1.9% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Level-2+ Autonomous Launches | +2.1% | Asia-Pacific core, particularly China | Short term (≤ 2 years) |

| EU WP.29 OTA-Update Mandate | +1.6% | Europe, with spillover to global platforms | Short term (≤ 2 years) |

| 'Functions-on-Demand' Models | +1.4% | North America, expanding to Europe and Asia-Pacific | Medium term (2-4 years) |

| U.S. IRA EV Incentives | +1.2% | North America, with technology transfer to global BEV platforms | Medium term (2-4 years) |

| 5G-V2X Network Roll-out | +0.9% | South Korea, pilot deployments in Japan and select Chinese cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM Shift to Centralized Zonal E/E Architectures Raising Middleware Spend

Vehicle makers are collapsing dozens of individual electronic control units (ECUs) into a handful of high-performance compute domains that cluster functions by physical zone rather than by discipline. The approach reduces wiring weight, frees cabin space, and allows applications to share processing resources securely. It also elevates middleware from a hidden cost center into a strategic layer that routes high-speed Ethernet traffic, enforces real-time determinism, and delivers OTA partitioning without reflashing entire images. Freedom-from-interference certification at ASIL-B or higher is now a prerequisite for any platform that touches safety-critical workloads, narrowing the supplier field to companies with mature functional-safety histories[1]Abdullah El-Bayoumi, "ISO-26262 Compliant Safety-Critical Autonomous Driving Applications", International Journal of Safety and Security Engineering, iieta.org. As a result, spending once locked in at the application level is migrating toward operating-system and middleware stacks that can promise long-term portability and recurring revenue, reshaping priorities across the automotive software market.

Level-2+ Autonomous Launches by Chinese OEMs Boosting ADAS Code Volume

Chinese automakers have unleashed a price war by bundling high-level ADAS features such as urban navigation and automated lane changes into mass-market models at no additional cost, contrasting sharply with Western pay-per-feature strategies. The free-feature push accelerates code-volume growth, because each brand now competes on the breadth of sensor-fusion pipelines and edge-case handling rather than on hardware alone. While nominal revenue per vehicle falls, the volume of vehicles running advanced perception stacks soars, driving demand for real-time operating systems that can schedule heterogeneous workloads across central compute clusters.

EU WP.29 OTA-Update Mandate Accelerating Secure Software Stacks

Regulations R155 and R156 require cybersecurity management and software update management systems on every new vehicle sold in the European Union as of July 2024[2]"New 2024 cybersecurity regulations for vehicles", INCIBE, incibe.es. OEMs must deploy secure boot chains, certificate-based authentication, and continuous vulnerability tracking from development through end-of-life. The directive forces the adoption of hardware security modules and encrypted update orchestration, standardizing the technical foundation needed for post-sale feature activation and subscription models across the automotive software market. Suppliers capable of demonstrating end-to-end compliance enjoy a defensible advantage, while laggards face delayed product approvals and potential recall exposure.

Subscription-Based “Functions-on-Demand” Models Expanding Post-Sale Revenues

North American brands are decoupling vehicle features from the point of purchase and selling them as time-limited trials, permanent unlocks, or recurring subscriptions. Consumers who accept digital add-ons provide carmakers with an ongoing revenue stream, stabilizing margins that hardware commoditization has eroded. The business model demands robust identity management, secure payment processing, and in-vehicle entitlement verification, layering new middleware complexity on top of existing real-time constraints. Balancing feature pricing with customer tolerance is emerging as a core competency for future profit pools.

Restraints Impact Analysis of Automotive Software Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Middleware Standards | -2.3% | Global, with highest impact in Europe | Medium term (2-4 years) |

| Shortage of AUTOSAR Classic Developers | -1.8% | Europe, with ripple effects globally | Short term (≤ 2 years) |

| Cyber-Homologation Testing Costs | -1.5% | Europe, with global implications for exporters | Short term (≤ 2 years) |

| Legacy CAN Architectures | -1.2% | Asia (excluding China, Japan, South Korea), South America, Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Middleware Standards Hindering Cross-OEM Re-use

Despite two decades of AUTOSAR alignment, proprietary extensions remain the norm, forcing suppliers to rewrite or fork code for every customer. The duplication inflates engineering budgets and slows validation timelines. Smaller platform vendors are especially exposed because each deviation requires new integration and safety recertification. The economic waste delays the universal adoption of service-oriented architectures that could otherwise lower barriers to entry and speed innovation cycles across the automotive software market.

Shortage of AUTOSAR Classic and Adaptive Developers in Europe Inflating Costs

The pivot to software-defined vehicles is colliding with talent scarcity. Engineers fluent in safety-critical C/C++ and model-based design command premium wages, while competition from adjacent sectors, gaming, fintech, and cloud, draws candidates away. OEMs have responded by outsourcing to lower-cost regions, yet time-zone gaps and intellectual-property safeguards add process friction. Program delays cascade through the supply chain, raising inventory costs and jeopardizing launch windows for new nameplates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive Software Market Segment Analysis

By Software Layer:

Consolidation Elevates Operating-System ValueApplication software accounted for 48.53% of revenue in 2025, dominating the automotive software market share, as infotainment, telematics, and basic ADAS have been shipping for years. The trend is now reversing: as zonal architectures replace dozens of discrete ECUs with a handful of domain controllers, operating-system stacks that guarantee time-and-space partitioning become crucial. They are forecast to grow fastest at 9.82% through 2031, a pace linked to OEM demand for safety-certified platforms and cloud-native toolchains. Consolidation also shifts profit pools. When a single hypervisor manages multiple mixed-criticality workloads, middleware that mediates traffic and enforces service isolation commands a premium.

Firmware growth is muted, because silicon bring-up routines are increasingly bundled with system-on-chip reference designs. Together, these forces push the automotive software market toward a layered hierarchy in which control over low-level stacks determines who captures downstream application revenue. In practice, zonal compute nodes must split real-time gateway duties from user-facing tasks without jeopardizing safety certifications. Microkernel designs and deterministic scheduling enable both infotainment and steering-assist processes to coexist on common hardware. The strategy reduces wiring mass, lowers bill-of-materials costs, and shortens validation time by requiring fewer ECUs to undergo independent functional-safety audits.

By Application:

ADAS Gains Regulatory MomentumADAS and safety systems accounted for 33.76% of the automotive software market revenue in 2025, reflecting pervasive adoption of camera-and-radar sensor suites. The fastest expansion, however, is in powertrain and battery-management software, projected to grow at a 13.35% CAGR through 2031. Electrification demands high-resolution estimation of cell temperature, aging, and energy availability, capabilities that internal-combustion controls never required. Advanced batteries are integrated with regenerative braking logic, vehicle-to-grid interfaces, and over-the-air calibration updates.

High-frequency data is sampled and fed into Kalman filters or neural nets to predict degradation, which in turn informs cloud analytics that optimize charging schedules. The complexity rewards suppliers with electrochemistry expertise and scalable validation environments. As battery warranty terms stretch toward a decade, confidence in software-based lifetime prognostics will become a decisive purchase criterion, further enlarging the automotive software market.

By Vehicle Type:

Commercial Fleets Digitise OperationsPassenger cars accounted for 74.91% of the automotive software market revenue in 2025, yet light commercial vehicles will expand at a 9.77% CAGR as fleet operators seek lower total cost of ownership through telematics, remote diagnostics, and automated route planning. Enterprises quantify return on investment in fuel savings, uptime, and insurance premiums, making software adoption straightforward to justify. Fleet managers demand unified dashboards that ingest vehicle health, location, and driver behavior.

Over-the-air updates eliminate downtime associated with service-bay visits, while predictive algorithms schedule maintenance before failures strand shipments. Success stories are poised to return to consumer segments once reliability and payback are proven. Heavy trucks, though lower in unit volume, are exploring platooning and lane-centered autonomy to address driver shortages, reinforcing the theme that commercial requirements often incubate capabilities before they diffuse into the wider automotive software market.

By Propulsion:

Battery-Electric Accelerates Software ValueInternal-combustion vehicles held 66.47% of the automotive software market share in 2025, but battery-electric vehicles will grow at an 18.94% CAGR through 2031, well ahead of the broader automotive software market growth trend. Electric architectures introduce new software domains, charging session coordination, thermal envelope optimization, and real-time range prediction under variable loads, driving up code volume per unit. Regulatory incentives that tie tax credits to battery performance incentivize ever-smarter algorithms.

Cloud-synchronized digital twins track each pack’s health, enabling firmware tweaks that unlock temporary range extensions or power boosts as optional subscriptions. Hybrid powertrains must coordinate two propulsion systems, yet their share is expected to plateau as policy increasingly favors pure electric vehicles. The resulting hierarchy places BEV-centric software stacks at the epicenter of future revenue capture.

By Deployment:

Edge-Cloud Continuum Takes ShapeOn-board embedded code accounted for 92.84% of the automotive software market share in 2025, but off-board cloud and edge services are forecast to grow at a 17.44% CAGR through 2031. BMW’s Azure-backed Mobile Data Recorder illustrates the shift: telemetry reaches cloud data stores within seconds, letting engineers query signals in natural language and cutting analysis cycles from days to hours. The architecture separates latency-critical control loops, which remain in the vehicle, from model training and fleet analytics executed off-board.

Edge gateways pre-process sensor data to limit cellular costs and preserve data sovereignty. Successful partitioning will define future competitiveness by enabling rapid iteration, security patching, and feature experimentation without hardware recalls. As cellular coverage widens and 5G network slicing matures, cloud orchestration layers will convert raw data into recurring service revenue, reinforcing the automotive software market's trajectory toward hybrid compute models.

Geography Analysis

APAC Automotive Software Market

Asia-Pacific commanded a 39.04% share in 2025 and is forecast to grow at a 11.79% CAGR, the fastest regional ascent in the automotive software market. Chinese OEMs offer Level-2+ autonomy at zero price premiums, inflating code bases and accelerating middleware convergence while shrinking per-vehicle licensing revenue. South Korea’s nationwide 5G-V2X deployment pilots are enabling low-latency cooperative services that depend on edge computing. Japan remains deliberate, emphasizing incremental reliability improvements over disruptive architectural shifts, yet its semiconductor leadership positions it for future centralized compute platforms. India, while smaller in vehicle output, is evolving into a global software engineering hub as multinationals tap its talent pool for AUTOSAR integration and cloud tool-chain development.

Europe and North America Automotive Software Market

Europe remains pivotal because UNECE regulations require secure OTA capabilities in every new vehicle. Germany hosts several Tier-One suppliers that specialize in middleware, while the United Kingdom and France focus on cybersecurity testing and digital twin research. The region’s main drag is a scarcity of safety-certified software engineers, which inflates contract rates and stretches launch schedules. Cyber Resilience Act provisions on software bills of materials add compliance overhead but also create defensible barriers for firms with automated vulnerability-scanning pipelines. North America spearheads the commercial rollout of subscription-based functions-on-demand, with the United States' battery incentives fast-tracking the adoption of advanced energy-management software.

MEA and South America Automotive Software Market

South America, the Middle East, and Africa collectively represent a smaller share of the automotive software market. Legacy CAN buses and limited charging infrastructure slow rollout of advanced features, but smart-city pilots in the United Arab Emirates and Saudi Arabia prove out telematics and connected-traffic services under controlled conditions. The cost to include software-defined capabilities is falling as global platforms mature, suggesting that emerging markets could skip incremental steps and adopt centralized architectures more quickly once baseline infrastructure reaches critical mass.

Competitive Landscape

Established players like Robert Bosch, Continental, BlackBerry QNX, NXP Semiconductors, and NVIDIA dominate the automotive software market. These suppliers, with their strong ties to OEMs and expertise in functional safety, effectively safeguard their shares in middleware and operating systems. Cloud hyperscalers, Microsoft, Google, and AWS, provide CI/CD pipelines, digital twins, and managed security services that lower entry barriers for emerging vehicle programs but raise OEM concerns over data sovereignty. Open-source alliances like SOAFEE and Eclipse SDV are gaining momentum as automakers seek to avoid vendor lock-in, pooling non-differentiating development costs in shared repositories.

White-space innovation is emerging around wireless battery-management systems that reduce harness mass, federated-learning frameworks that keep raw data on vehicles while sharing insights across fleets, and mixed-criticality OTA orchestration capable of updating safety-critical ECUs alongside infotainment without downtime. Smaller specialists such as TTTech Auto focus on deterministic middleware, while Airbiquity positions secure update orchestration as a standalone service. Regulatory requirements for continuous vulnerability scanning and secure-boot attestations give incumbents with established DevSecOps tool-chains an advantage. Yet, nimble startups respond with domain-specific point solutions that can be integrated via standardized APIs, intensifying competition for niche profit pools.

Strategic collaborations are becoming common: semiconductor vendors bundle software development kits and hypervisors with hardware reference designs, accelerating time-to-market for OEMs but funneling revenue toward platform owners. Meanwhile, traditional Tier-1 suppliers acquire cybersecurity boutique firms to shore up skills gaps exposed by UNECE mandates. The boundary between hardware and software suppliers continues to blur, with success increasingly measured by the completeness and continuous certification level of the delivered stack rather than by individual product wins. Over the forecast horizon, competitive positioning will hinge on the ability to maintain secure, updatable platforms that bridge the edge and the cloud while unlocking recurring revenue streams central to the growth trajectory of the automotive software market.

Automotive Software Industry Leaders

-

BlackBerry Limited

-

Robert Bosch GmbH

-

Continental AG

-

NXP Semiconductors N.V.

-

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Automotive Software Market Companies Covered in this Report

- Robert Bosch GmbH

- Continental AG

- Elektrobit

- BlackBerry Limited (QNX)

- Google LLC (Alphabet Inc.)

- Microsoft Corporation

- Wind River Systems

- NXP Semiconductors N.V.

- NVIDIA Corporation

- Aptiv PLC

- TTTech Auto AG

- Vector Informatik GmbH

- Infineon Technologies AG

- Intel Corporation

- LG Electronics Vehicle Solutions

- DENSO Corporation

- Panasonic Automotive Systems

- KPIT Technologies Ltd.

- Intellias Ltd.

- Tata Elxsi Ltd.

- Airbiquity Inc.

- MontaVista Software LLC

- Renesas Electronics Corporation

- HARMAN International

- GlobalLogic Inc.

Recent Industry Developments in Automotive Software Market

- January 2026: Visteon Corporation forged a strategic alliance with TomTom, marking the debut of the world's first in-car local AI conversational navigation assistant. This collaboration sees Visteon's cognitoAI platform seamlessly merging with TomTom's Automotive Navigation Application, prioritizing user privacy in navigation.

- January 2026: DXC Technology Company rolled out AMBER, a cutting-edge automotive software platform. With AMBER, automakers can slash development time by half, and its standardized methodology promises an additional 30% in cost savings.

- December 2025: Siemens introduced PAVE360 Automotive technology. This innovative, pre-integrated, off-the-shelf digital twin software aims to address the growing challenges of integrating automotive hardware and software.

- June 2025: NXP closed the USD 625 million acquisition of TTTech Auto, adding MotionWise middleware to its CoreRide platform.

Global Automotive Software Market Report Scope

Automotive software refers to the computer programs, applications, and systems used in the design, manufacturing, operation, and maintenance of automobiles, including software for developing and operating vehicle components and systems.

The Automotive Software market is segmented by software layer, application, vehicle type, propulsion, deployment, and geography. By Software Layer, the market is segmented into Application Software, Middleware, Operating System, and Firmware / Basic Input. By Application, the market is segmented into ADAS and Safety Systems, Infotainment and Telematics, Powertrain and Battery Management, Body Control and Comfort, and Connected Vehicle Services. By Vehicle Type, the market is segmented into Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles. By Propulsion, the market is segmented into Internal Combustion Engine, Battery Electric Vehicle, and Hybrid Electric Vehicle. By Deployment, the market is segmented into On-Board (Embedded) and Off-Board (Cloud / Edge). By Geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, and Rest of South America), Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, and Rest of Asia), and Middle East and Africa (United Arab Emirates, Saudi Arabia, Turkey, and Rest of the Middle East and Africa).

Market forecasts are provided in terms of Value (USD).

Segmentation Overview

| Application Software |

| Middleware |

| Operating System |

| Firmware / Basic Input-Output Software |

| ADAS and Safety Systems |

| Infotainment and Telematics |

| Powertrain and Battery-Management |

| Body Control and Comfort |

| Connected Vehicle Services |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Internal Combustion Engine Vehicles (ICE) |

| Battery Electric Vehicles (BEV) |

| Hybrid Electric Vehicles (HEV/PHEV) |

| On-Board (Embedded) |

| Off-Board (Cloud / Edge) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of the Middle East and Africa |

| By Software Layer | Application Software | |

| Middleware | ||

| Operating System | ||

| Firmware / Basic Input-Output Software | ||

| By Application | ADAS and Safety Systems | |

| Infotainment and Telematics | ||

| Powertrain and Battery-Management | ||

| Body Control and Comfort | ||

| Connected Vehicle Services | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| By Propulsion | Internal Combustion Engine Vehicles (ICE) | |

| Battery Electric Vehicles (BEV) | ||

| Hybrid Electric Vehicles (HEV/PHEV) | ||

| By Deployment | On-Board (Embedded) | |

| Off-Board (Cloud / Edge) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

How large is the automotive software market in 2026, and what is its expected CAGR?

The automotive software market, valued at USD 21.08 billion in 2026, is anticipated to grow at a CAGR of 9.33% through 2031.

How are European regulations influencing automotive software?

UNECE R155 and R156 require secure cyber-security and software-update management on every new vehicle, effectively standardizing encrypted OTA pipelines and raising compliance thresholds.

Why is battery-management software growing faster than other applications?

Electrification introduces complex energy-management tasks such as accurate state-of-health prediction and thermal balancing, which demand advanced algorithms and continuous cloud analytics.

Which region shows the highest growth potential?

Asia-Pacific leads, powered by Chinese OEMs that deploy Level-2+ autonomy at volume and South Korean 5G-V2X roll-outs that enable low-latency edge services.

Page last updated on: