Automotive V2X Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

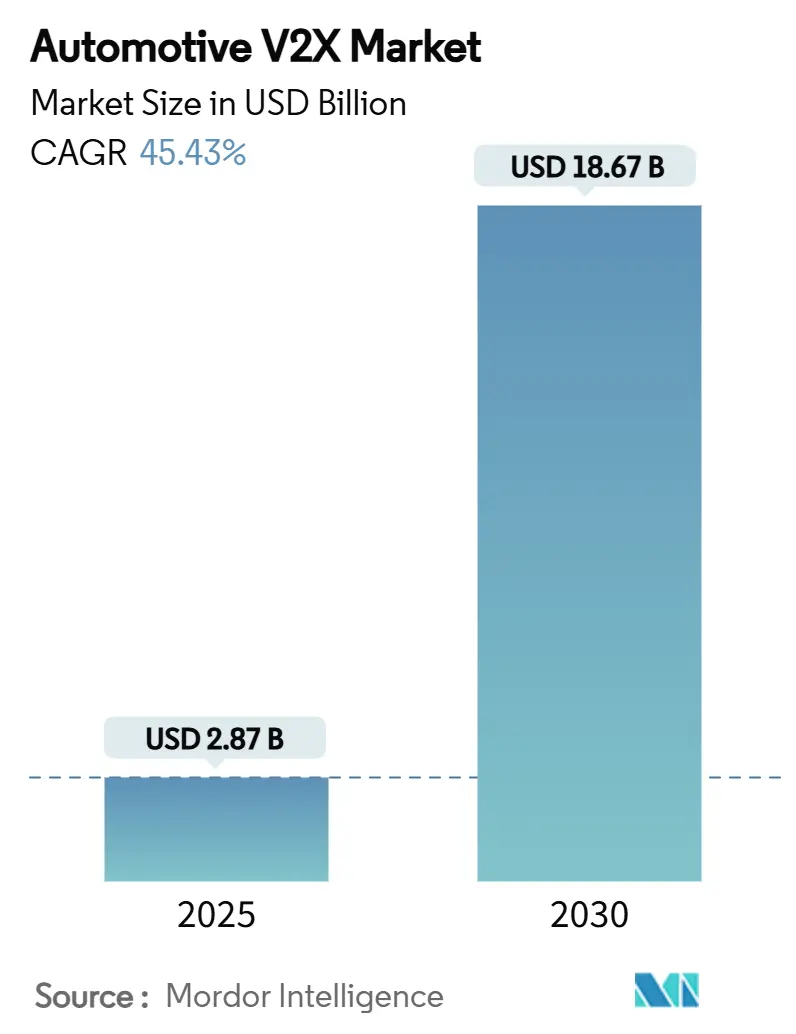

| Market Size (2025) | USD 2.87 Billion |

| Market Size (2030) | USD 18.67 Billion |

| Growth Rate (2025 - 2030) | 45.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive V2X Market Analysis by Mordor Intelligence

The Automotive V2X Market size is estimated at USD 2.87 billion in 2025, and is expected to reach USD 18.67 billion by 2030, at a CAGR of 45.43% during the forecast period (2025-2030). Expedited 5G roll-outs, accelerating autonomous vehicle programs, and binding government safety mandates are combining to create an investment super-cycle for connected-vehicle infrastructure. Real-time data exchange between vehicles, infrastructure, the grid, and vulnerable road users is becoming indispensable as nations confront the 42,514 roadway fatalities reported in the United States during 2024.[1]“National Roadway Safety Strategy,” U.S. Department of Transportation, transportation.gov Asia-Pacific is evolving into the growth engine, propelled by China’s V2X build-out and plans for maximum V2X-equipped vehicles per year by 2034. Across the value chain, chipset consolidation, multi-access edge computing, and spectrum re-allocation toward 5G NR-V2X are accelerating commercial readiness while exposing gaps in cybersecurity governance that could slow near-term adoption.

Key Report Takeaways

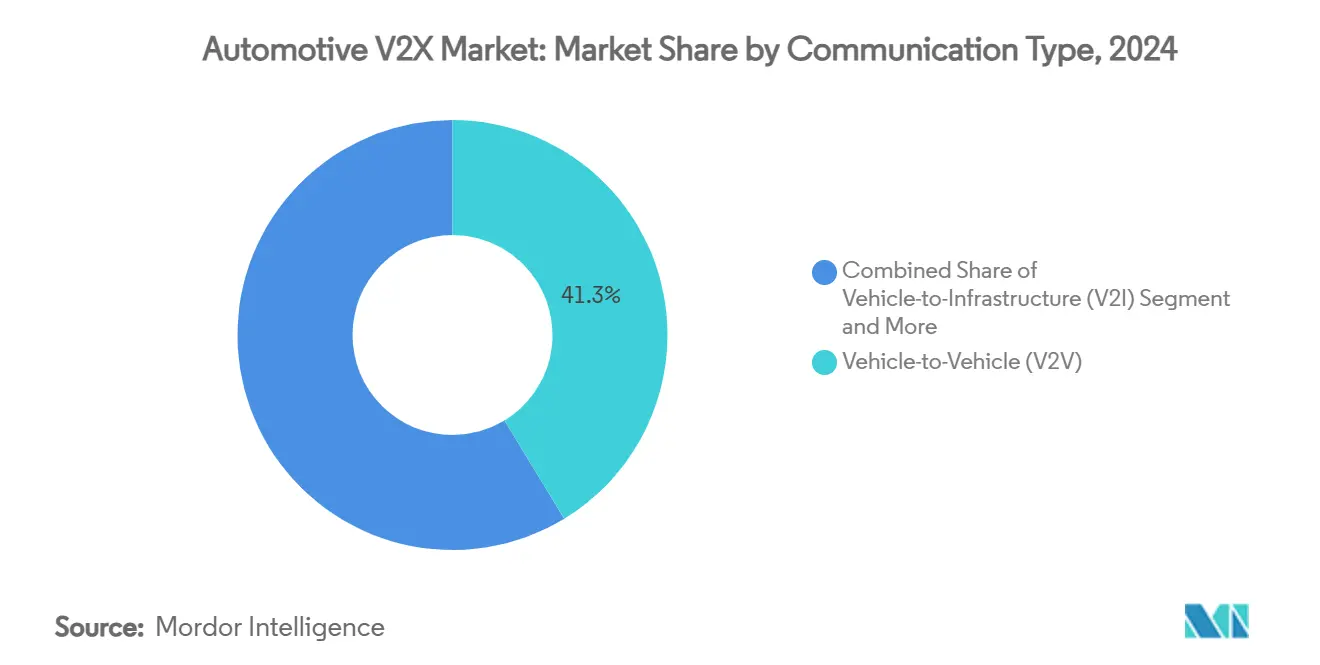

- By communication type, Vehicle-to-Vehicle held 41.28% of automotive V2X market share in 2024, whereas Vehicle-to-Grid is projected to post a 46.13% CAGR through 2030.

- By vehicle type, passenger cars commanded 67.15% share of the automotive V2X market in 2024, while commercial vehicles are expanding at a 45.81% CAGR to 2030.

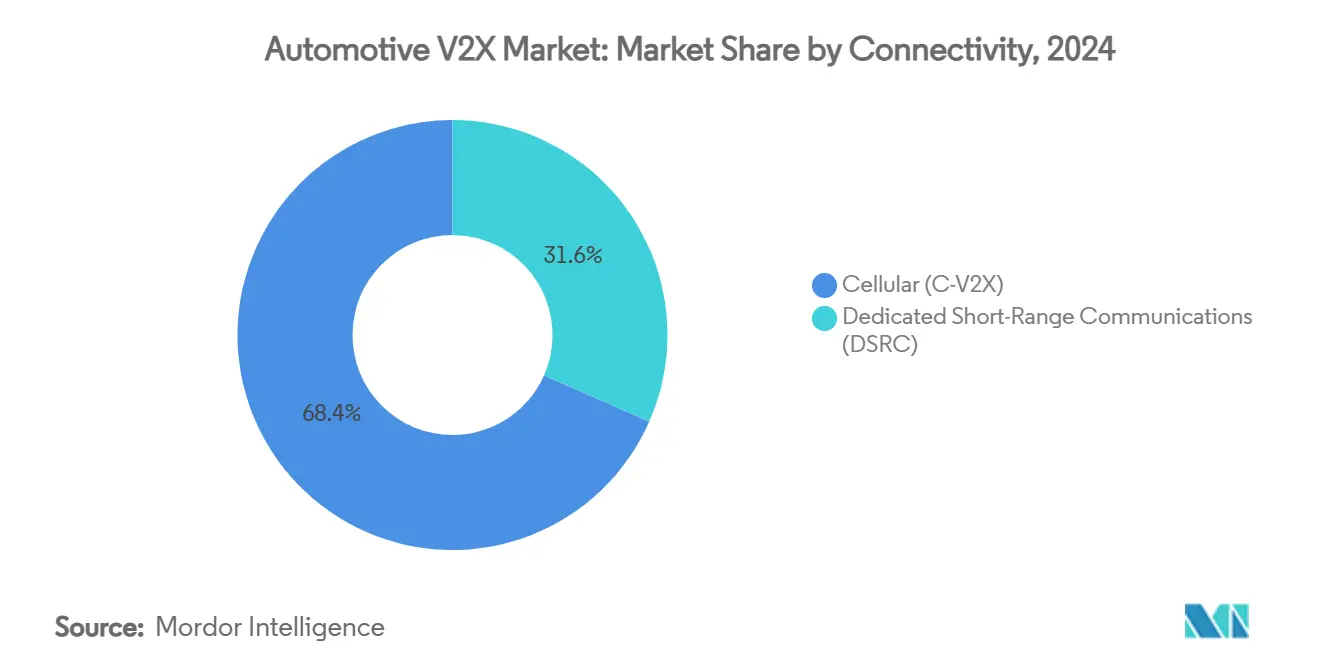

- By connectivity, C-V2X accounted for 68.38% of the automotive V2X market size in 2024 and is set to grow at a 45.57% CAGR during the forecast window.

- By application, safety solutions held 46.53% share of the automotive V2X market size in 2024, whereas EV charging and energy services are on track for a 46.12% CAGR to 2030.

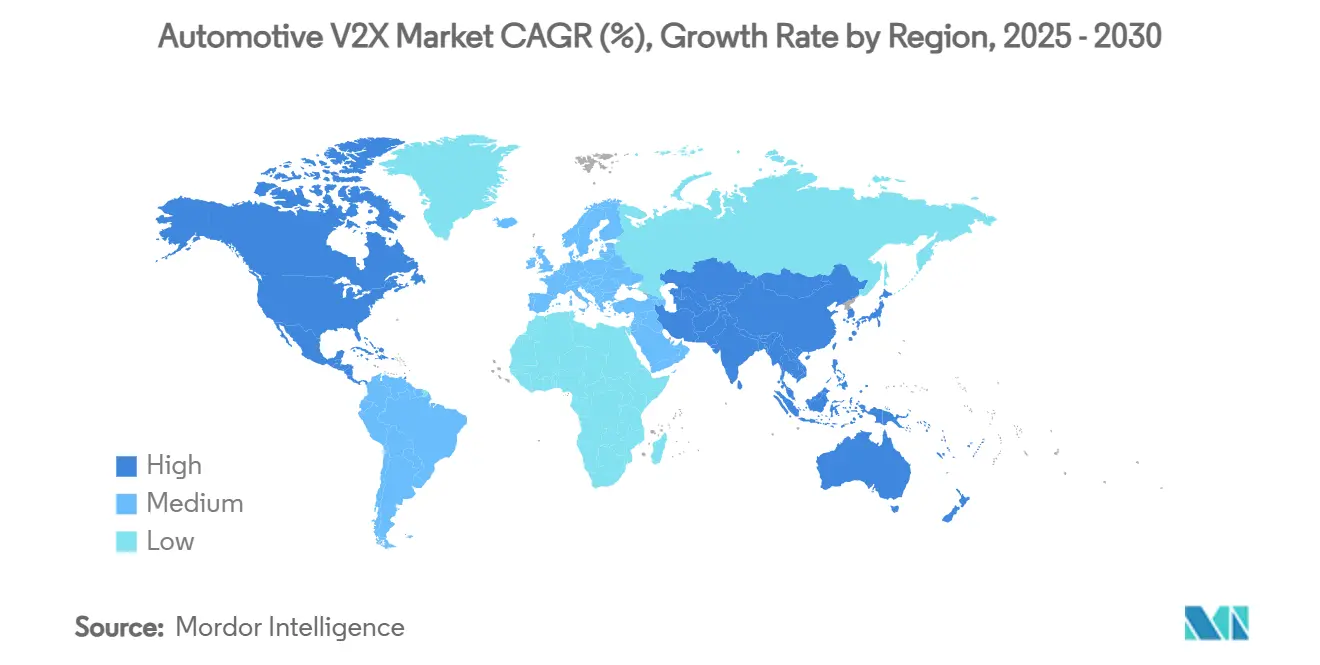

- By geography, North America led with 34.71% revenue share in 2024; Asia-Pacific is forecast to advance at a 45.93% CAGR through 2030.

Market Trends and Insights

Drivers Impact Analysis of Automotive V2X Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Connected & Autonomous Vehicle | +10.3% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Proliferation of 5G URLLC Networks | +8.7% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Government Safety Mandates & Vision-Zero Targets | +8.1% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| OEM Investment in Smart-Mobility | +7.2% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Vehicle-to-Grid Integration | +6.1% | EU leading, North America following | Long term (≥ 4 years) |

| Edge-Compute RSUs | +4.8% | North America and EU early deployment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Connected & Autonomous Vehicle Roll-Outs

Autonomous driving programs offset sensor line-of-sight gaps with cooperative perception delivered by V2X. Hyundai Motor Group announced a significant investment of USD 21 billion in the United States from 2025 to 2028.[2]“2025 Strategy Update,” Hyundai Motor Group, hyundai.com Japan’s Ministry of Internal Affairs validated V2N support for Level 4 trucks on the New Tomei Expressway, underscoring commercial transport as an early beneficiary. As fleets prove that V2X unlocks 360-degree situational awareness, capital spending pivots toward nationwide roadside unit grids. Each additional autonomous vehicle multiplies the value of the infrastructure, forging a self-reinforcing adoption loop that propels the automotive V2X market forward.

Proliferation of 5G URLLC Networks

Fifth-generation ultra-reliable low-latency communications supply the sub-10 millisecond response time demanded by collision-avoidance algorithms. General Motors and AT&T are equipping millions of U.S. vehicles with 5G modules, positioning V2X as a premium telematics tier. In Beijing, more than 7,000 5G-Advanced base stations now support vehicle-road-cloud coordination, demonstrating how densified radio grids correlate with service quality. As operators migrate from LTE-V2X to 5G NR-V2X, the technology shifts from broadcast warnings to coordinated maneuvers, widening the revenue canvas for the automotive V2X market.

Government Safety Mandates & Vision-Zero Targets

Binding regulations are translating road-safety objectives into direct demand for V2X-enabled vehicles. The European Union began enforcing ADAS requirements in July 2024, obliging every new car to support intelligent speed assistance, automated braking, and lane-keeping—features that rely on low-latency V2X data streams. In the United States, the “Saving Lives with Connectivity” plan calls for V2X coverage on 20% of federal highways by 2028 and 50% by 2031, a framework expected to avert 1,300 fatalities annually. Such clarity dismantles the network-effects barrier because OEMs can plan production volumes around known compliance dates. China’s NCAP now rewards V2X readiness, nudging automakers to exceed minimum benchmarks. Together these mandates build a predictable base load for the automotive V2X market, encouraging suppliers to scale production and invest in performance-enhancing innovations.

OEM Investment in Smart-Mobility Ecosystems

Carmakers are pivoting from hardware sales toward mobility subscriptions powered by V2X data. Volkswagen’s partnership with Valeo and Mobileye embeds cooperative perception directly into the MQB platform, signalling that connectivity will be standard, not optional. Hyundai’s Dutch smart-mobility pilot streams real-time traffic data over V2X links, proving that public-private ecosystems scale more rapidly when costs and benefits are shared. Suppliers such as HARMAN introduced “Ready Aware,” a SaaS model delivering infrastructure alerts via cloud APIs, further blurring the boundary between automotive and telecom value chains.[3]“CES 2025 Press Release: Ready Aware,” HARMAN International, harman.com

Restraints Impact Analysis of Automotive V2X Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Infrastructure Cost | -6.8% | Global, particularly acute in developing markets | Medium term (2-4 years) |

| Escalating Cybersecurity Liabilities | -4.2% | Global, with stricter enforcement in EU and North America | Short term (≤ 2 years) |

| Spectrum-Sharing Uncertainty | -3.1% | North America and EU, with regulatory spillover to APAC | Medium term (2-4 years) |

| Weak ROI for Fleet Operators | -2.9% | Emerging markets in APAC, Latin America, and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Infrastructure Cost & Standards Fragmentation

Installing roadside units costs USD 15,000–30,000 per intersection, a burden that falls on agencies managing shrinking budgets. Early DSRC deployments, such as Georgia’s 1,700-unit network, now face upgrade dilemmas after the FCC narrowed DSRC spectrum to 10 MHz and freed 20 MHz for C-V2X. Similar boundary lines divide European C-ITS and Chinese C-V2X profiles, hindering cross-border operability. Dual-mode equipment exists but at a premium, forcing planners into difficult sequencing decisions that slow universal coverage and put a brake on automotive V2X market adoption.

Escalating Cybersecurity Liabilities & Recalls

UN Regulation 155 subjects every new European vehicle sold after July 2024 to rigorous cybersecurity audits, obliging automakers to manage threats through the entire vehicle life cycle. Industry losses linked to automotive cyber-incidents increased in 2024, and V2X’s wireless pathways further enlarge the attack surface. A single breach could paralyze intersection management systems and expose OEMs to coordinated recalls running into billions. LG Electronics secured the first Common Criteria evaluation for a V2X module, illustrating the cost and complexity of compliance. Sustaining over-the-air patching and real-time intrusion detection is now an obligatory line item, nudging smaller suppliers out of the automotive V2X market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive V2X Market Segment Analysis

By Communication Type:

Energy Management Outpaces SafetyVehicle-to-Vehicle services maintained 41.28% share of the automotive V2X market in 2024 because collision-avoidance remained the default deployment priority for regulators. Growth is now shifting toward Vehicle-to-Grid, which is forecast to expand at a 46.13% CAGR as utilities monetize distributed storage. The automotive V2X market size for V2G is projected to quadruple between 2025 and 2030, reflecting rising EV penetration and demand-response incentives. Dual-mode on-board chargers allow bidirectional power flows without hardware swaps, smoothing adoption curves.

In developing economies, V2G roll-outs hinge on grid digitalization and time-of-use pricing reforms. Municipal pilots in India, Brazil, and South Africa illustrate interest but also expose the need for interoperable standards. Platform vendors are crafting API-driven marketplaces where fleet operators can auction battery capacity during peak hours, a model that could compress payback periods to under three years.

By Vehicle Type:

Fleets Lead Practical AdoptionPassenger cars still comprised 67.15% of automotive V2X market share in 2024 because sheer unit volumes dwarf commercial fleet sales. Yet commercial vehicles deliver the higher 45.81% CAGR through 2030, a reflection of quantifiable cost savings in logistics, maintenance, and driver safety. Software-defined trucks under Daimler’s roadmap target Level 4 autonomy by 2027, mandating reliable C-V2X sidelink connectivity for platooning and remote diagnostics. Chinese express-delivery leaders such as ZTO now run autonomous freight convoys able to move 1,000 parcels without human intervention, showcasing immediate ROI. Fleet owners measure paybacks in reduced fuel consumption, lower insurance claims, and stricter regulatory compliance, leading them to pay premium prices for early functionality.

Consumer adoption is catching up. OEMs remove optional-equipment paywalls and instead embed V2X hardware as standard, spreading costs across larger production runs. Subscription services covering hazard warnings, parking payments, and authorization for bidirectional charging transform vehicles into digital wallets. The automotive V2X market therefore benefits from twin adoption curves, with fleets proving business cases upfront and passenger vehicles adding volume later. As chip costs fall and over-the-air updates enable new features post-sale, the ownership gap between commercial and personal segments will narrow, raising baseline connectivity expectations across the board.

By Connectivity:

Cellular V2X Supplants Legacy DSRCC-V2X captured 68.38% of the automotive V2X market in 2024, a lead cemented by carrier-grade reliability and reuse of existing 4G / 5G infrastructure, and is also growing at a robust CAGR of 45.57% through 2030. Automotive OEMs favor the technology’s path toward Release 18 upgrades, which promise improved sidelink throughput for sensor-sharing. Keysight’s Release 16 interoperability demonstration using Ettifos and Autotalks silicon proves multi-vendor readiness, easing supply-chain risk. The FCC’s decision to assign 20 MHz to C-V2X freed manufacturers from spectrum uncertainty, accelerating deployment timetables. Early DSRC installations hold an installed-base advantage in certain U.S. corridors and European C-ITS testbeds, but the cost of maintaining two parallel ecosystems is driving convergence toward dual-mode offerings.

From 2025 onward, the automotive V2X market size tied to DSRC is expected to contract slowly as upgrade cycles favor cellular. However, niche use cases such as rail-crossing alerts and mining operations may keep IEEE 802.11bd devices in service longer because they offer deterministic latency without dependence on operator networks. Hybrid modems handling both standards preserve backward compatibility and safeguard public investments. The long-term trajectory points to software-configurable radios capable of accommodating future waveforms, ensuring resilience against further spectral re-allocations.

By Application:

Safety Dominates, Energy Monetization AcceleratesSafety solutions accounted for 46.53% of the automotive V2X market size in 2024, underpinned by mandates for collision-warning and emergency braking functions. The U.S. requirement for automatic emergency braking in all light vehicles by 2029 intensifies this baseline demand. Yet EV charging and energy services are forecast to post the fastest 46.12% CAGR, driven by utility incentives and carbon-neutral targets. Mobility-management layers leverage AI routing to ease congestion, lowering commute times and tailpipe emissions. Infotainment services round out the mix, transforming cars into rolling media hubs that exploit city-wide Wi-Fi offload and satellite redundancy.

The interplay between safety and energy applications unlocks multi-channel revenue streams. Toshiba’s multi-power conditioner uses V2X data to shift household loads, boosting overall efficiency compared with conventional designs. Municipalities employ intersection analytics to prioritize public transit vehicles, freeing curb space for micro-mobility modes. For OEMs, bundling these services into unified subscription tiers increases lifetime customer value, further amplifying the addressable opportunity in the automotive V2X market.

Geography Analysis

North America Automotive V2X Market

North America retained 34.71% of the automotive V2X market revenue during 2024, driven by coordinated federal investment, a mature telecom backbone, and early regulatory clarity. U.S. DOT grants totaling USD 60 million fast-tracked roadside installations across Arizona, Texas, and Utah, with 20% highway coverage targets by 2028. Proposals for FMVSS 150 and cross-border trials with Canada continue to solidify harmonized standards, enabling economies of scale. Mexico’s export-oriented auto industry is also embedding C-V2X modules into new models for delivery to both domestic and U.S. buyers, closing the regional technology gap.

APAC Automotive V2X Market

Asia-Pacific is forecast to register a 45.93% CAGR through 2030, the fastest rate globally. China’s infrastructure initiative underpins provincial pilots linking 30 million V2X-ready vehicles annually to highway networks. Japan complements this momentum through V2N support for Level 4 freight corridors, and South Korea’s software-defined vehicle program ensures that V2X coding frameworks stay interoperable. These initiatives converge to form the largest contiguous testbed, attracting semiconductor and system-integration suppliers from Europe and North America. Consequently, the automotive V2X market size in Asia-Pacific is poised to eclipse North America before decade-end.

Europe Automotive V2X Market

Europe progresses steadily on the back of binding ADAS mandates and the updated Intelligent Transport Systems Directive. Germany’s Autobahn GmbH collaborates with OEMs to upgrade C-ITS nodes along major corridors, while the Netherlands deploys public-private pilots linking Hyundai and Kia vehicles to smart-traffic platforms. Cybersecurity remains front-and-center, with UN Regulation 155 setting global benchmarks for over-the-air patch governance. Collectively, European best practices funnel into ISO, ETSI, and UNECE workstreams, shaping global rulebooks and anchoring long-term confidence in the automotive V2X market.

Competitive Landscape

The automotive V2X market remains moderately fragmented, with semiconductor leaders, Tier-1 suppliers, telecom operators, and niche software firms jostling for share. Qualcomm and NXP dominate the chipset layer, leveraging economies of scale and reference-design playbooks to lock in OEM sockets. Continental, Bosch, and HARMAN integrate those chipsets into end-to-end stacks that combine sensor fusion, middleware, and cybersecurity. Telecom majors such as AT&T, China Mobile, and Deutsche Telekom supply carrier-edge platforms delivering quality-of-service guarantees, while cloud hyperscalers are positioning low-latency zones for traffic-management analytics.

Strategic responses cluster around vertical integration. Qualcomm’s Autotalks acquisition folds DSRC and C-V2X silicon into the Snapdragon Digital Chassis, ensuring cradle-to-cloud handoffs for over-the-air features. Suppliers intensify software investments; Bosch’s acquisition of Five.ai brings machine-learning talent to cooperative-perception tools, expanding beyond pure hardware. White-space potential exists in cyber-resilience managed services, where companies such as Upstream Security are building cloud-native threat-detection platforms.

Standardization battles are narrowing as IEEE 802.11bd embraces PHY upgrades that can coexist with 5G NR-V2X, creating a runway for dual-mode devices. This harmonization favors scale producers able to amortize R&D across multiple protocols, disadvantaging single-technology specialists. Meanwhile, policy momentum toward open-source stacks, championed by the European Commission, may lower entry barriers for new digital entrants, setting the stage for further fragmentation before eventual consolidation within the automotive V2X market.

Automotive V2X Industry Leaders

Qualcomm Inc.

Continental AG

Aptiv PLC

Robert Bosch GmbH

NXP Semiconductors

- *Disclaimer: Major Players sorted in no particular order

Automotive V2X Market Companies Covered in this Report

- Continental AG

- Aptiv PLC

- NXP Semiconductors

- TomTom International B.V.

- Qualcomm Inc.

- Robert Bosch GmbH

- HARMAN International

- Cisco Systems Inc.

- Mobileye N.V.

- Infineon Technologies AG

- Autotalks Ltd.

- Cohda Wireless

- Savari Inc.

- DENSO Corporation

- Panasonic Corporation

- Huawei Technologies Co. Ltd.

- Ericsson AB

- Nokia Corporation

- Hyundai Mobis

- LG Electronics

Recent Industry Developments in Automotive V2X Market

- June 2025: Qualcomm completed its USD 350 million acquisition of Autotalks, integrating V2X chipsets into the Snapdragon Digital Chassis to support both DSRC and C-V2X protocols.

- April 2024: Hyundai Motor Group partnered with the Dutch government to provide smart-mobility and connectivity services that stream real-time traffic information to Hyundai and Kia vehicles over V2X links.

- February 2024: Cisco and TELUS launched a 5G Mobility Services Platform in North America, enabling automated provisioning of V2X services for 1.5 million vehicles on Cisco’s IoT Control Center.

Global Automotive V2X Market Report Scope

Segmentation Overview

| Vehicle-to-Infrastructure (V2I) |

| Vehicle-to-Grid (V2G) |

| Vehicle-to-Vehicle (V2V) |

| Vehicle-to-Home (V2H) |

| Vehicle-to-Pedestrian (V2P) |

| Vehicle-to-Network (V2N) |

| Passenger Cars |

| Commercial Vehicles |

| Cellular (C-V2X) |

| Dedicated Short-Range Communications (DSRC) |

| Safety |

| Mobility Management |

| Infotainment |

| EV Charging & Energy |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Oceania | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Communication Type | Vehicle-to-Infrastructure (V2I) | |

| Vehicle-to-Grid (V2G) | ||

| Vehicle-to-Vehicle (V2V) | ||

| Vehicle-to-Home (V2H) | ||

| Vehicle-to-Pedestrian (V2P) | ||

| Vehicle-to-Network (V2N) | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Connectivity | Cellular (C-V2X) | |

| Dedicated Short-Range Communications (DSRC) | ||

| By Application | Safety | |

| Mobility Management | ||

| Infotainment | ||

| EV Charging & Energy | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Oceania | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive V2X market?

The automotive V2X market is valued at USD 2.87 billion in 2025 and is projected to climb to USD 18.67 billion by 2030.

How fast is the automotive V2X market expected to grow?

The market is forecast to expand at a 45.43% CAGR between 2025 and 2030, driven by 5G roll-outs, autonomous vehicle programs, and mandatory safety regulations.

Which region holds the largest share of the automotive V2X market?

North America leads with 34.71% revenue share in 2024, supported by U.S. federal funding for connected-vehicle infrastructure.

Which region will grow the quickest through 2030?

Asia-Pacific is projected to register the fastest 45.93% CAGR, propelled by China’s large-scale V2X infrastructure investments and aggressive autonomous-vehicle deployment plans.

What communication type is growing the fastest?

Vehicle-to-Grid (V2G) services are the fastest-growing segment, expected to post a 46.13% CAGR through 2030 as utilities monetize bidirectional charging.

Why is Cellular V2X preferred over DSRC?

C-V2X offers longer range, higher reliability, and smooth integration with existing 4G/5G networks, giving it 68.38% market share in 2024 and a robust 45.57% growth trajectory.

Page last updated on: