Automotive Air Purifier Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

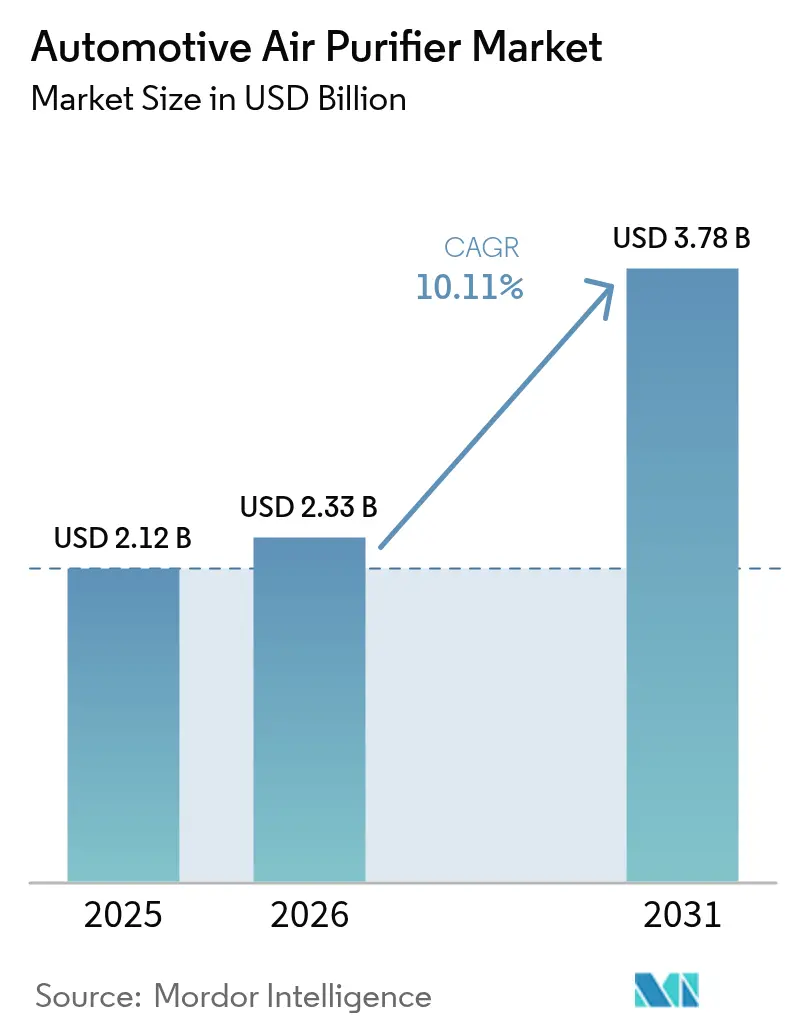

| Market Size (2026) | USD 2.33 Billion |

| Market Size (2031) | USD 3.78 Billion |

| Growth Rate (2026 - 2031) | 10.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Air Purifier Market Analysis by Mordor Intelligence

The automotive air purifier market size in 2026 is estimated at USD 2.33 billion, growing from 2025 value of USD 2.12 billion with 2031 projections showing USD 3.78 billion, growing at 10.11% CAGR over 2026-2031. Rising expectations for interior air quality, tighter vehicle emission rules, and lower filter media costs are propelling demand across model ranges. The Euro 7 framework, published in May 2024, mandates in-cabin emission limits from November 2026, while China VI-B standards that took effect in July 2023 apply similar requirements, prompting automakers to fit advanced purification systems as baseline equipment. Asia-Pacific steers overall growth as megacity pollution heightens consumer health awareness and electric-vehicle (EV) production scales quickly. Passenger cars remain the primary revenue contributor, but battery electric models deliver the highest incremental volume as their ample auxiliary power and wellness positioning accelerate technology uptake. Suppliers have responded with multistage devices that blend HEPA filtration, activated carbon, and ultraviolet (UV-LED) disinfection, allowing automakers to balance performance, cost, and packaging constraints.

Key Report Takeaways

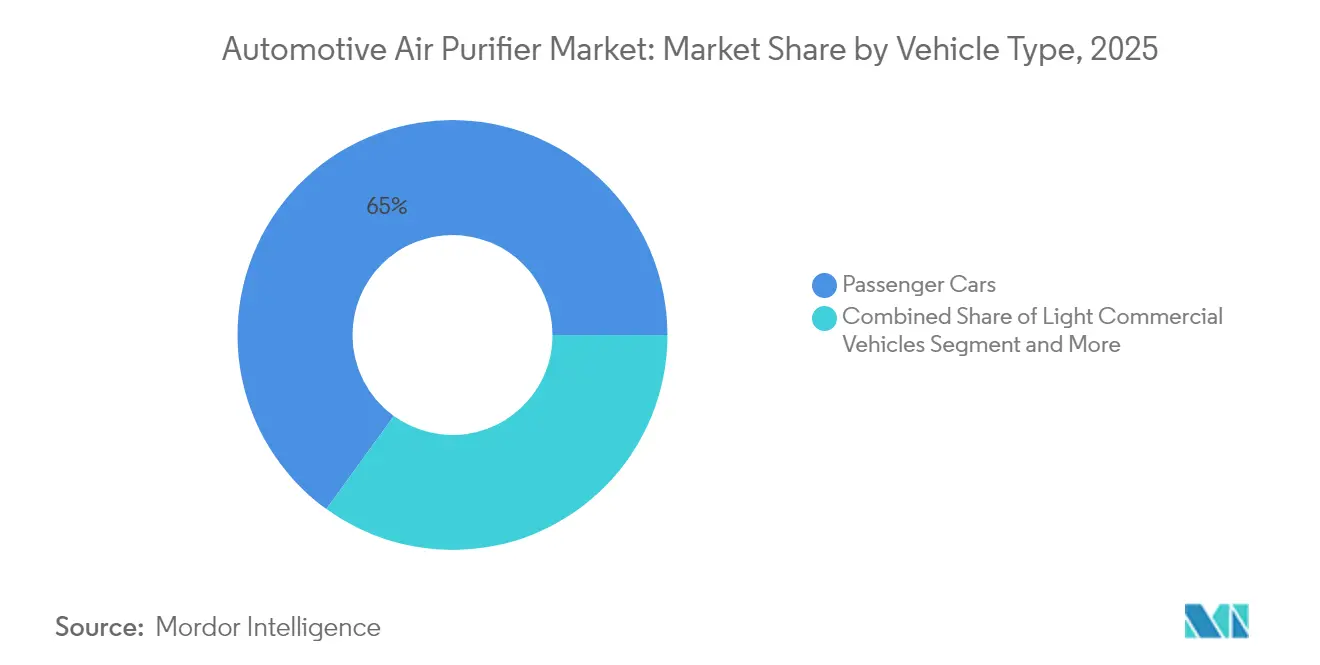

- By vehicle type, passenger cars led with 65.02% revenue contribution in 2025; light commercial vehicles are forecast to advance at an 11.12% CAGR to 2031.

- By technology, HEPA media captured 47.12% of 2025 revenues, while UV-LED units are set to climb at a 11.94% CAGR.

- By installation type, HVAC-integrated factory systems accounted for 57.74% of the automotive air purifier market size in 2025 and will rise at a 10.68% CAGR through 2031.

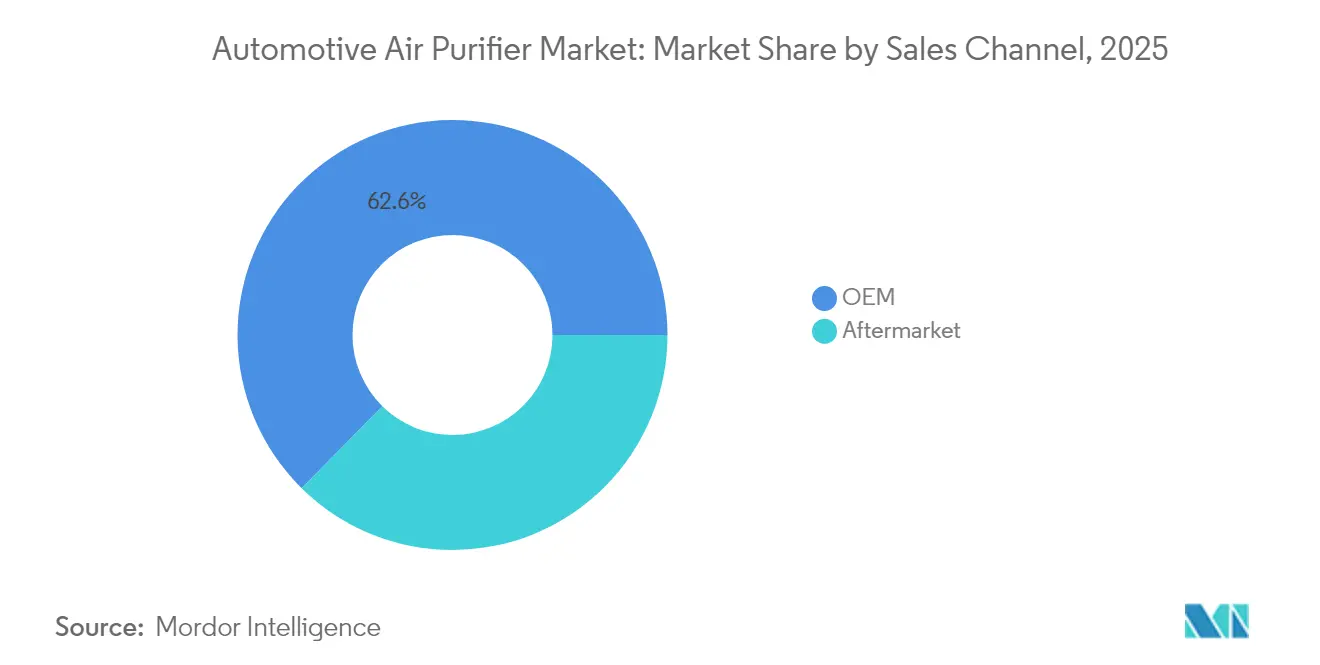

- By sales channel, OEM contributed with 62.62% share in the automotive air purifier market, while the aftermarket channel is set to grow at an 11.03% CAGR.

- By vehicle propulsion, internal-combustion models retained 61.60% of the automotive air purifier market share in 2025,whereas battery electric vehicles posted the swiftest expansion at an 17.66% CAGR through 2031.

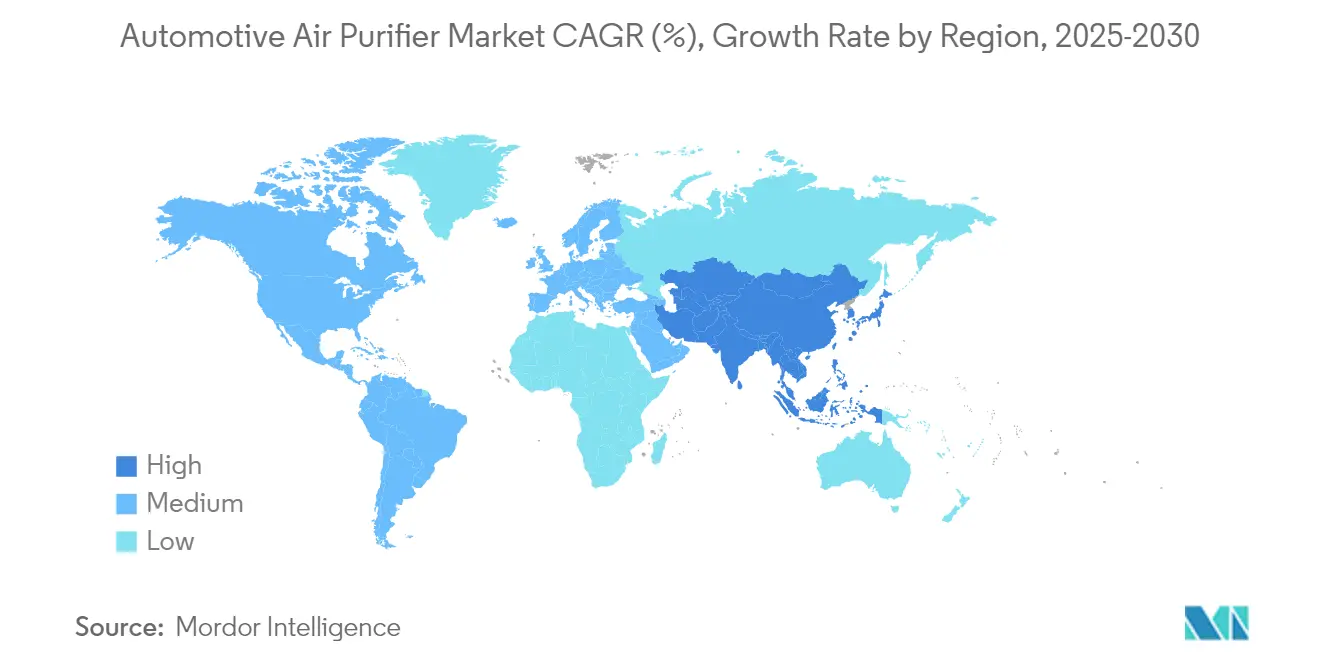

- By geography, Asia-Pacific dominated at 39.04% share in 2025 and will log the highest regional growth at an 10.87% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Air Purifier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising In-cabin PM2.5 Concerns in Megacities | +2.1% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Stricter China VI-B and Euro 7 Interior Air-quality Rules | +1.8% | China and European Union, extending to North America | Short term (≤ 2 years) |

| Automaker Push for Wellness-oriented Cabin Features | +1.4% | Global, premium segments first | Medium term (2-4 years) |

| HEPA Cost Decline from Melt-blown Capacity Additions | +1.2% | Global manufacturing hubs | Long term (≥ 4 years) |

| AI-enabled Smart Scent and Pathogen-sensing Modules | +0.9% | North America and EU premium markets | Long term (≥ 4 years) |

| Mandatory filtration for robotaxis and shared-mobility fleets | +0.7% | Urban centers worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising In-Cabin PM2.5 Concerns in Megacities

Rapid urbanization makes traffic exposure a daily health risk, pushing commuters to treat vehicles as protective bubbles. The 2024 IQAir World Air Quality Report showed only 17% of monitored cities meeting World Health Organization guidelines, underscoring the necessity for onboard filtration. Korea’s national R&D institutes illustrated regulatory urgency by rolling out filter-free electrostatic towers that eliminate over 90% of ultrafine particles in public spaces, a concept soon mirrored inside vehicles [1]Korea Institute of Machinery & Materials, “Filter-Free Electrostatic Air Cleaner,” nst.re.kr. Hyundai therefore embedded After-Blow and Fine-Dust Indicator software that auto-activates recirculation when PM2.5 spikes, turning air cleaning into an invisible safety function. In Asia-Pacific megacities, the automotive air purifier market gains an enduring uplift as households prioritize cabin wellness equal to powertrain efficiency.

Stricter China VI-B and Euro 7 Interior Air-Quality Rules

Regulators now bundle cabin emissions with exhaust limits, erasing the optional status of filtration. Euro 7 compels compliance across passenger cars, vans, and heavy trucks beginning November 2026, while China’s VI-B regime already enforces aldehyde and particulate caps for every new light vehicle. Suppliers such as NGK Insulators have publicly forecast stable revenue despite macro-demand swings because mandated equipment levels create guaranteed purchase volumes [2]NGK Insulators Investor Update 2025, ngk-insulators.com. The standardization effect shortens design cycles: a single purification stack certified for both regulatory blocs can cover most high-volume global platforms, delivering scale economies that widen the automotive air purifier market.

Automaker Push for Wellness-Oriented Cabin Features

With powertrains converging, OEMs differentiate through occupant experience. Yanfeng’s XiM25 concept integrates WAVE vents that mimic gentle breezes while channeling air through a multi-layer filter, framing purification as part of holistic relaxation. Sharp’s LDK+ EV demonstrator adds AI fragrance and circadian lighting control, packaging scent, and pathogen sensing with real-time filtration. Wellness branding lets premium marques charge higher option prices and boosts customer retention, which in turn persuades volume manufacturers to adopt similar functions. This dynamic sustains the automotive air purifier market well beyond compliance volumes.

HEPA Cost Decline from Melt-Blown Capacity Additions

Post-pandemic expansions of melt-blown nonwoven lines lowered HEPA media unit cost and pressure drop. Hollingsworth & Vose’s CabinPro XT maintains 99.97% capture efficiency while extending service intervals, reducing lifecycle cost for fleet operators. Purflux’s CabinHepa+ achieves the same filtration cut-off at 0.3 micron, yet claims 50 times more protection than legacy pollen filters. Lower price points unlock mid-trim vehicle adoption, scaling the automotive air purifier market further and challenging ionizer alternatives that cannot match particle removal rates without ozone risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Global Performance Standards and Test Cycles | -1.3% | Worldwide | Short term (≤ 2 years) |

| Limited Consumer Awareness Outside North Asia | -0.9% | North America, Europe, emerging markets | Medium term (2-4 years) |

| Automaker Cost-down Pressure in Entry-level EVs | -0.8% | Global mass-market segments | Medium term (2-4 years) |

| Micro-ozone Emission Risks from Ionizers | -0.6% | Global, safety-focused markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of Global Performance Standards and Test Cycles

Unlike Euro-NCAP or WLTP, no universally accepted clean-air protocol exists for cars. An Aerosol Science and Technology study logged ionizer clean-air delivery rates between 5 and 10 cfm under varying lab setups, making cross-brand comparisons impossible. OEMs must navigate at least three separate cabin-air test cycles spanning China, the European Union, and Japan, adding cost and delaying launches. Standardization gaps slow the automotive air purifier market as smaller suppliers defer investment until test harmonization materializes.

Limited Consumer Awareness Outside North Asia

North Asian buyers actively compare PM2.5 ratings when selecting vehicles, but surveys in Germany and the United States show most shoppers are unaware of interior air pollutant thresholds. University of Birmingham researchers cut in-cabin nitrogen dioxide by 90% using USD 12–25 activated-carbon filters, yet the findings received scant mainstream coverage. Absent strong marketing, aftermarket uptake lags, limiting volume for replacement cartridges. This knowledge deficit caps the automotive air purifier industry’s growth in mature Western markets until awareness campaigns scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Drive Market Expansion

Passenger cars commanded 65.02% of 2025 revenue, supported by daily commuting patterns that heighten value perceptions for clean interiors. The automotive air purifier market size for passenger cars is forecast to expand to grow at an 11.34% CAGR by 2031, outpacing global light-vehicle production, due to rising installation rates. Manufacturers like Lexus use Panasonic nanoe X generators across UX, RZ, ES, LC, LS, and LX lines, converting what was once an optional extra into brand-wide default hardware.

Commercial-vehicle interest follows as logistics firms evaluate driver health effects on productivity. Medium and heavy trucks log longer daily operating hours, so even marginal filtration benefits translate into reduced absenteeism costs. Fleet pilots in Shanghai show that installing HEPA-plus-carbon cartridges raises driver satisfaction scores on OEM internal indices. Although this segment started from a smaller base, a healthy growth rate through 2030 will lift absolute volume, reinforcing economies of scale for filter suppliers.

By Technology: UV-LED Purification Gains Momentum

HEPA media led 2025 revenue at 47.12%, favored for certified 0.3-micron capture efficiency. Yet UV-LED modules post the fastest rise, with a 11.94% CAGR projected as diode cost curves track the optoelectronics learning curve. Combining UVC LEDs with HEPA, Daikin’s automotive unit validates 99.9% SARS-CoV-2 inactivation in under 10 minutes, answering pathogens that slip through mechanical pores.

Ionizing filters lose share because studies record ozone peaks up to 702 ppb when devices operate at full output, exceeding several national occupational limits. Consequently, manufacturers shift toward hybrid layouts—HEPA for particulates, carbon for gases, and UV-LED for microbes—creating a performance envelope that satisfies Euro 7 interior requirements and builds consumer trust.

By Installation Type: Factory Integration Dominates

HVAC-integrated factory systems held 57.74% of the automotive air purifier market revenue in 2025 and are on track for a 10.68% CAGR. Automakers prefer integration because it safeguards design aesthetics and leverages existing duct paths, lowering additional mass by as much as 300 grams compared with stand-alone consoles. MANN+HUMMEL’s 2024 nanofiber filter launch ships as a direct drop-in for OEM blower housings and aftermarket kits, illustrating dual-channel flexibility.

Stand-alone plug-in purifiers remain vital in used-vehicle markets where owners retrofit protection. Cup-holder units grew steadily in India when Uno Minda introduced a four-layer cartridge, proving that cost isn’t a barrier once awareness spreads. While performance per cubic meter is lower than integrated systems, aftermarket units serve as stepping stones that familiarize first-time buyers with the concept, indirectly fostering later OEM adoption.

By Sales Channel: OEM Integration Accelerates

OEMs generated 62.62% of 2025 shipments, reflecting standard fitment in mid-level trims and mandatory installation for premium brands. The automotive air purifier market size attached to OEM contracts is projected to grow further, translating into secure multi-year volume forecasts for tier-one suppliers. Panasonic’s long-term agreement with Toyota Motor Corporation covers both Lexus and high-volume Toyota models, enabling dedicated filter-media lines and improving cost curves.

Aftermarket demand, though smaller, enjoys an 11.03% CAGR because of filter-replacement cycles and retrofit growth. Eureka Forbes widened its distribution network to 22,000 outlets in 2024, positioning itself to capture rural India’s rising interest in in-cabin hygiene. Replacement cycles average 12–18 months for HEPA elements; with global light-vehicle parc exceeding 1.3 billion units, recurring cartridge revenue puts a stable floor under market forecasts.

By Vehicle Propulsion: Electric Vehicles Lead Innovation

Internal-combustion vehicles remain the majority of users now, leading the automotive air purifier market with 61.60% share in 2025, but electric-drive cars propel the innovation frontier. Battery packs supply consistent 12–16 V accessory power without idle concerns, allowing high-flow blowers and UV-LED arrays to run even when the vehicle is stationary. The automotive air purifier market for BEVs is expected to climb to 17.66% CAGR, aligning with broader electrification curves. Sharp’s LDK+ prototype demonstrates how fragrance diffusion, infrared pathogen sensors, and HEPA-UV modules integrate cleanly when designers are freed from engine-bay packaging limits.

Hybrid and plug-in models capture similar gains, yet their dual powertrains impose stricter energy budgets when the gasoline engine is off. Consequently, filter developers pursue low-resistance nanofiber webs that maintain air exchange rates at reduced blower amperage. The advances made for hybrids trickle back into ICE vehicles, proving that electrification indirectly lifts the entire automotive air purifier industry.

Geography Analysis

Asia-Pacific heads the regional league table with a 39.04% revenue share in 2025 and will compound at 10.87% CAGR through 2031. China accounts for more than half of regional demand thanks to mandatory in-cabin aldehyde limits for new-energy vehicles and consumer readiness to pay USD 100–200 premiums for filtration upgrades. Japanese and South Korean OEMs contribute patented nano-e and plasma-cluster technologies, giving domestic markets early access and reinforcing export competitiveness.

Europe follows, driven by Euro 7 deadlines that oblige both passenger and commercial vehicles to meet unified interior-air benchmarks by late 2026 . German automakers have already committed to dual-stage HEPA-carbon layouts across 80% of new launches in the 2025 model year. Southern European countries, where fleet ages average more than 11 years, offer sizable retrofit potential once awareness climbs through public health campaigns.

North America posts a moderate uptake. United States federal regulations focus on tailpipe emissions, yet Californian legislators plan a 2027 rulemaking agenda for cabin air-quality disclosure stickers, which could mirror tire-pressure-monitoring mandates in their market-catalyst effect. Elsewhere, the Middle East, Africa, and South America remain nascent, but rapid urbanization of Lagos, Cairo, São Paulo, and Riyadh creates high-pollution corridors. Once free-trade zones simplify filter imports, local assemblers are likely to adopt cost-optimized HEPA cartridges originally engineered for Asian mass-market models, fostering long-run convergence.

Competitive Landscape

The automotive air purifier market shows moderate fragmentation. The top five suppliers- Panasonic, 3M, MANN+HUMMEL, Denso, and Bosch, collectively hold dominant share of OEM revenue, leveraging wide product catalogs and global manufacturing footprints. Panasonic’s nanoe X ion-radical generator, now standard on six Lexus nameplates, locks in multi-year cartridge pull-through because only authorized filters maintain design performance. 3M exploits its filtration material heritage to co-develop thin-profile microfibers that fit tight EV dashboards, while MANN+HUMMEL cross-sells new nanofiber blanks to both heavy-duty trucks and passenger vehicles.

Disruptive entrants chase niche performance attributes. UV-LED diode specialists partner with tier-ones to create ultra-compact reactor chambers capable of 99.9% viral deactivation in under five minutes. Sensor start-ups supply AI modules that fuse particulate, gas, and odor measurements, triggering variable fan speeds that cut energy consumption by up to 20%. Tesla’s patent for ride-hailing auto-sanitization shows how software platforms can orchestrate deep-clean cycles between passengers, pointing to a recurring-service business model beyond traditional filter sales.

Strategic activity underscores rising stakes. In August 2024, MANN+HUMMEL unveiled a nanofiber cabin filter that extends service life by 30% and claimed first-to-market status for sub-200 micron thickness. Denso invested in a Chinese melt-blown plant to localize HEPA media, insulating itself from commodity price swings. Bosch launched a cloud-based filter-change predictor integrated with its telematics control unit, securing recurring revenue via subscription alerts sent to vehicle owners.

Automotive Air Purifier Industry Leaders

Honeywell International Inc.

Panasonic Corporation

Denso Corporation

3M

MANN+HUMMEL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Ambrane introduced AeroBliss Auto, a portable 4-layer purifier and aroma diffuser for city commuters.

- June 2024: MANN+HUMMEL launched a nanofiber-based cabin air filter that lifts particle capture while extending lifespan.

- February 2024: SKF released the Smart Air Purification System for aftermarket installers, targeting commercial fleets.

- February 2024: Lumileds rolled out the Philips GoPure GP5611 purifier aimed at reducing airborne viruses in small cabins.

Global Automotive Air Purifier Market Report Scope

The automotive air purifier is designed to filter the air quality inside the vehicle and helps people who have allergies. With an introduction to new technologies, the air purifier can reduce odors, pathogens, and all microscopic pollutants.

The automotive air purifier market is segmented into Vehicle Type, Technology, Sales Channel, and Geography.

Based on the Vehicle Type, the market is segmented into Passenger Cars And Commercial Vehicles.

Based on the Technology, the market is segmented into HEPA, Activated Carbon, And Ionic Filter.

Based on the Sales Channel, the market is segmented into OEM And Aftermarket.

Based on Geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World.

For each segment, the market sizing and forecast have been done on the basis of value (USD Billion).

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| HEPA |

| Activated Carbon |

| Ionic Filter |

| Photo-Catalytic |

| Plasma Cluster |

| Hybrid/Multistage |

| UV-LED Purification |

| HVAC-Integrated Factory-Fit |

| Stand-Alone Plug-in |

| Roof-Mounted Cartridge |

| Cup-Holder/Portable |

| OEM |

| Aftermarket |

| Internal Combustion Engine Vehicles |

| Hybrid and Plug-in Hybrid Vehicles |

| Battery Electric Vehicles |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Technology | HEPA | |

| Activated Carbon | ||

| Ionic Filter | ||

| Photo-Catalytic | ||

| Plasma Cluster | ||

| Hybrid/Multistage | ||

| UV-LED Purification | ||

| By Installation Type | HVAC-Integrated Factory-Fit | |

| Stand-Alone Plug-in | ||

| Roof-Mounted Cartridge | ||

| Cup-Holder/Portable | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Vehicle Propulsion | Internal Combustion Engine Vehicles | |

| Hybrid and Plug-in Hybrid Vehicles | ||

| Battery Electric Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive air purifier market?

The market stands at USD 2.33 billion in 2026 and is forecast to reach USD 3.78 billion by 2031, reflecting a 10.11% CAGR over 2026-2031.

Which region shows the strongest growth for automotive cabin purifiers?

Asia-Pacific leads, holding 39.04% of 2025 revenue and projected to grow at an 10.87% CAGR through 2031 due to megacity pollution concerns and high EV production.

Why are UV-LED systems gaining attention over traditional HEPA filters?

UV-LED modules inactivate pathogens without consumable filter changes and are projected to expand at a 11.94% CAGR, the fastest among all technologies.

How do Euro 7 and China VI-B rules specifically influence automaker purchasing decisions for cabin-air purifiers?

Euro 7 (effective November 2026) and China VI-B (active since July 2023) set binding interior-air contaminant limits, making high-efficiency filtration a compliance item rather than an optional feature, which in turn guarantees baseline demand for purifier modules on every new vehicle sold in those regions.

Page last updated on: