Automotive Communication Technology Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

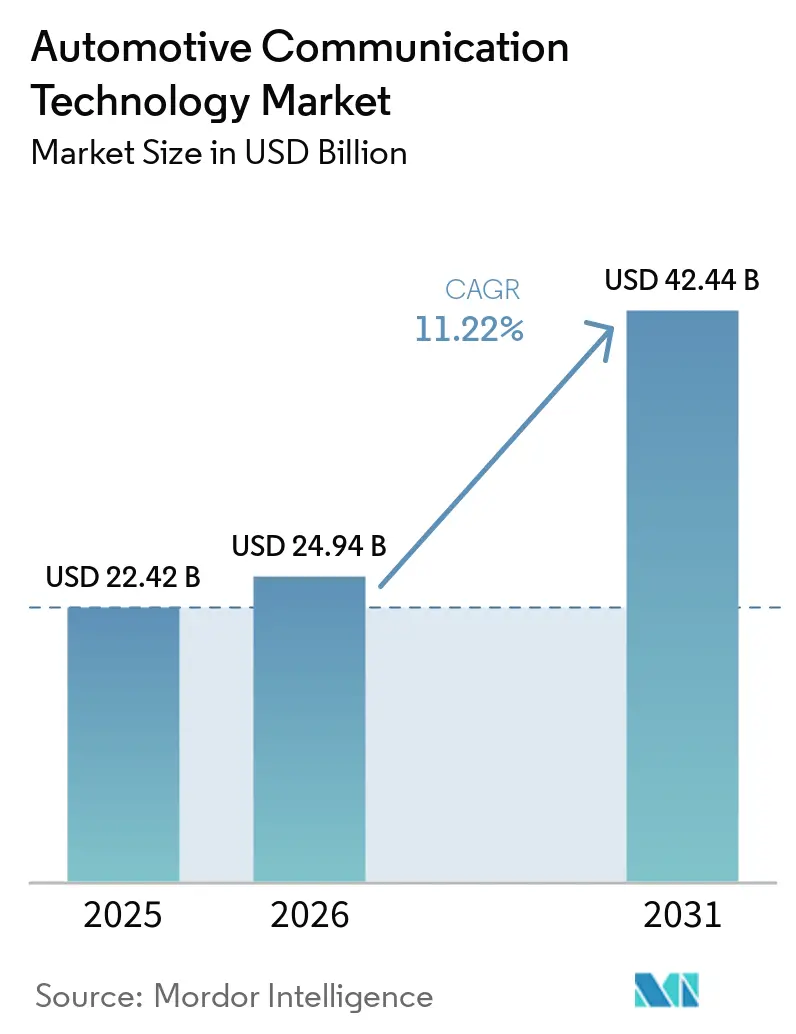

| Market Size (2026) | USD 24.94 Billion |

| Market Size (2031) | USD 42.44 Billion |

| Growth Rate (2026 - 2031) | 11.22% CAGR |

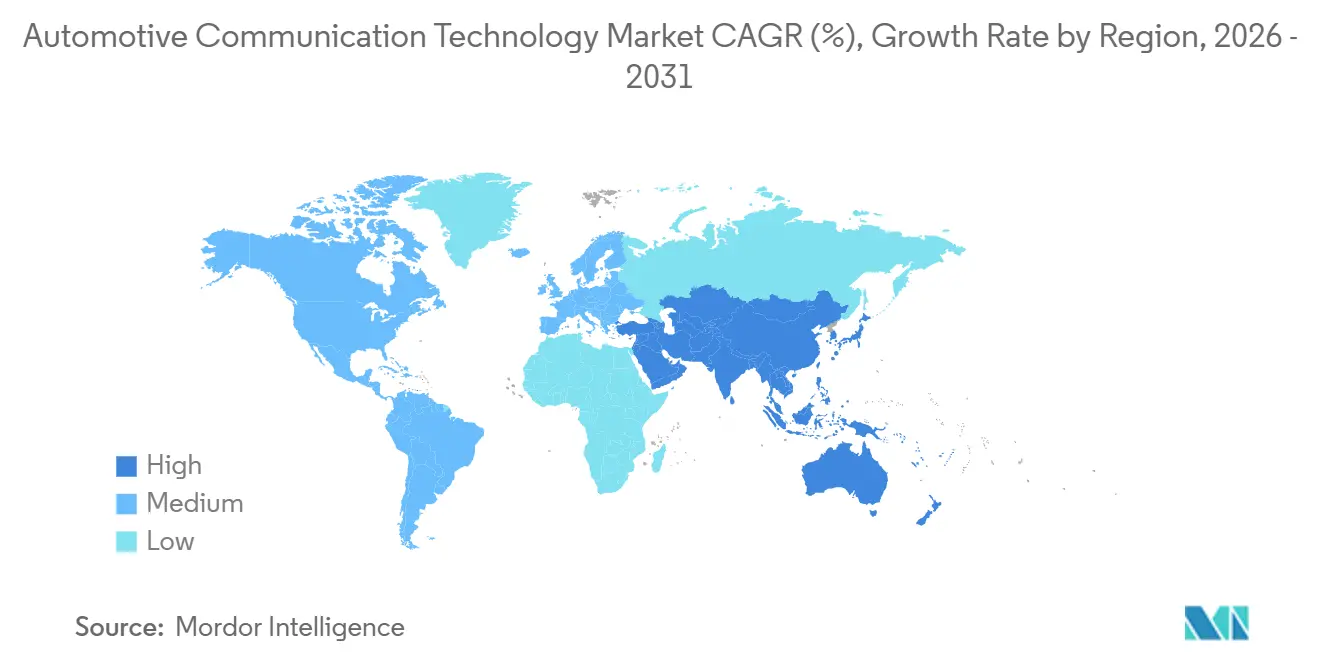

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

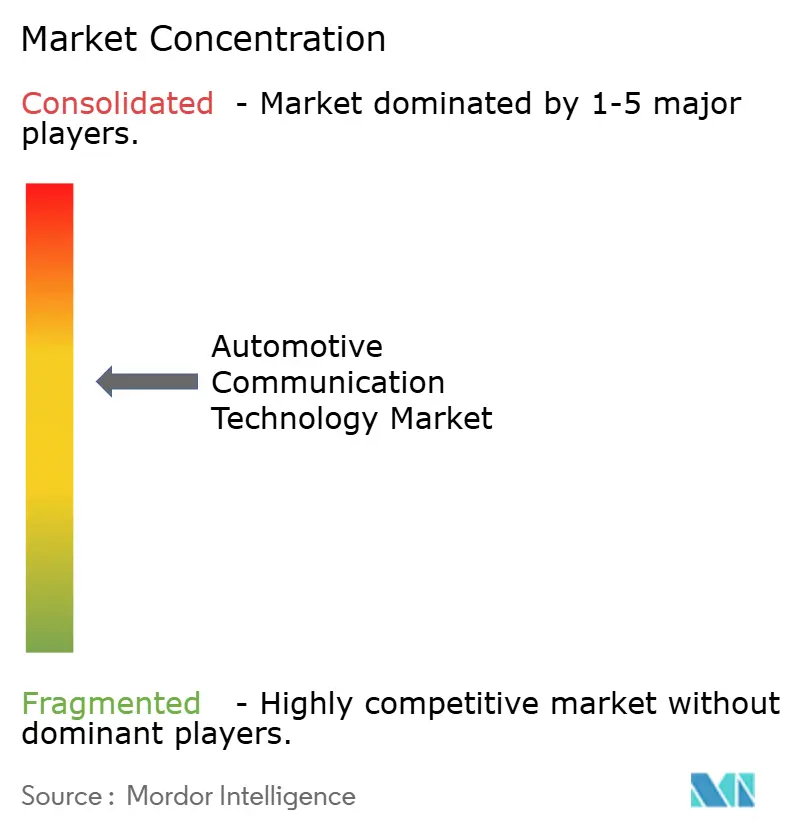

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Communication Technology Market Analysis by Mordor Intelligence

The automotive communication technology market size is expected to grow from USD 22.42 billion in 2025 to USD 24.94 billion in 2026 and is forecast to reach USD 42.44 billion by 2031 at an 11.22% CAGR over 2026-2031. Rising network bandwidth needs, the transition toward software-defined vehicles, and tightening cybersecurity mandates are reshaping the automotive communication technology market. OEMs that once relied on function-specific buses are adopting Ethernet backbones to support camera-rich driver-assistance features, while regulators mandate secure over-the-air updates that legacy protocols struggle to accommodate. China’s GB 44495 cybersecurity rule, which takes effect in January 2026, accelerates the shift to IP-based in-vehicle networks across the automotive communication technology market[1]"GB 44495-2024 English PDF," Field Test Asia Pte. Ltd., www.chinesestandard.net. In parallel, the FCC’s sunset of DSRC strengthens cellular V2X adoption, further broadening the addressable market for automotive communication technology[2]Ariel S. WolfDavid M. BonelliIan R. Williams, Roy Auh, "FCC Adopts Final Rules on C-V2X in 5.9 GHz for Auto Safety," Venable LLP, www.venable.com.

Key Report Takeaways

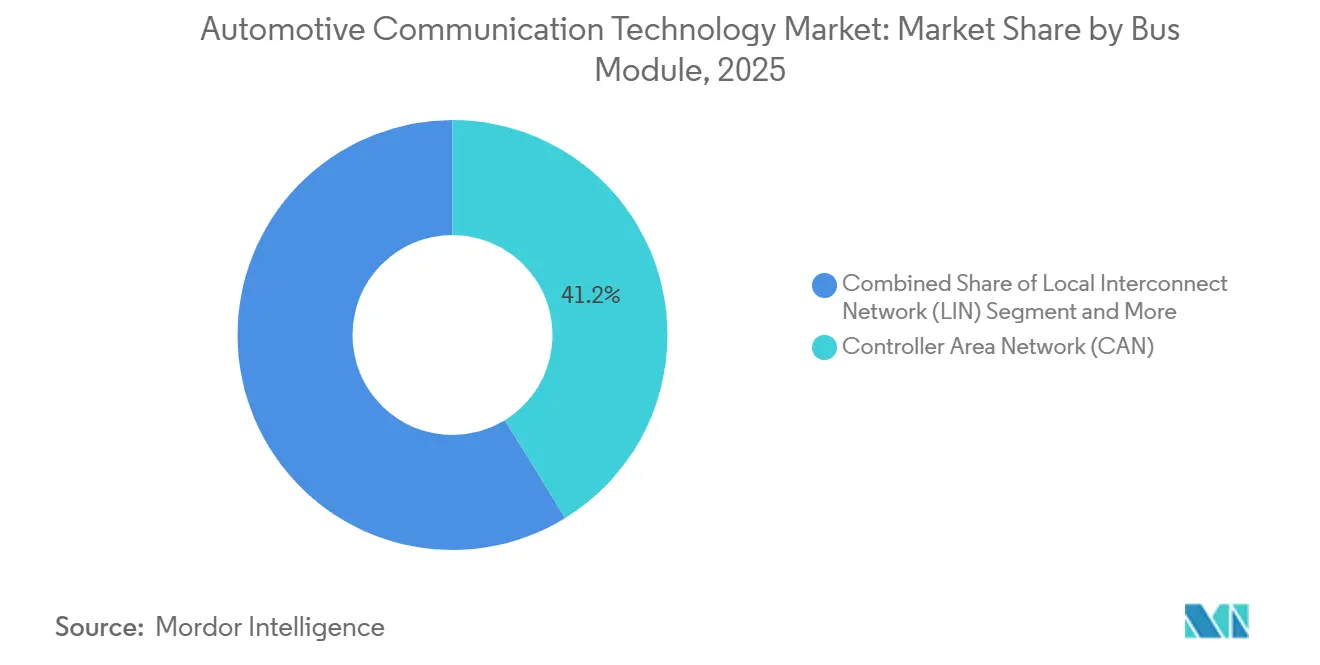

- By bus module, Controller Area Network held 41.22% of the automotive communication technology market share in 2025, while Automotive Ethernet is projected to advance at a 12.84% CAGR through 2031.

- By application, powertrain led the automotive communication technology market with a 36.08% share in 2025, whereas safety and ADAS are poised for the fastest 13.15% CAGR to 2031.

- By communication type, vehicle-to-everything accounted for 58.17% of the automotive communication technology market share in 2025 and remains the fastest-growing sub-segment, with a 11.89% CAGR through 2031.

- By vehicle type, passenger vehicles dominated the automotive communication technology market with a 72.11% share in 2025 and are set to register the fastest 11.58% CAGR through 2031.

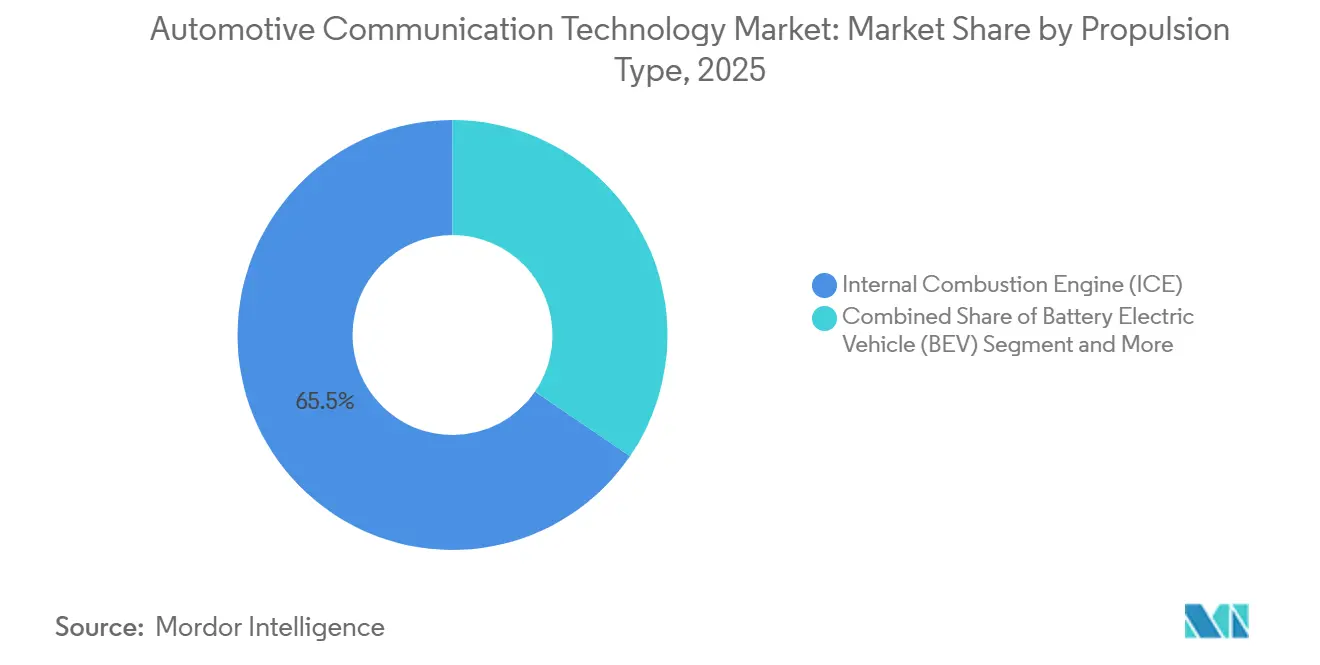

- By propulsion type, internal-combustion platforms commanded a 65.46% share of the automotive communication technology market in 2025, yet battery-electric vehicles will expand at a robust 14.33% CAGR through 2031.

- By distribution channel, OEM-installed systems captured 88.33% share of the automotive communication technology market in 2025, while aftermarket retrofits will accelerate at a 12.44% CAGR to 2031.

- By geography, Asia-Pacific held a 47.14% share of the automotive communication technology market in 2025, and is expected to grow with a 12.06% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Communication Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Integration of ADAS | +2.8% | Global, with early concentration in EU, North America, China | Medium term (2-4 years) |

| Emergence of Zonal E/E Architectures | +2.3% | Global, led by premium OEMs in EU and North America | Medium term (2-4 years) |

| Software-Defined Vehicles and OTA Communication | +2.0% | Global, accelerated in China and EU | Long term (≥ 4 years) |

| Adoption of Time-Sensitive Networking (TSN) | +1.5% | North America, EU, Japan, South Korea | Long term (≥ 4 years) |

| Demand for High-Bandwidth Infotainment | +1.4% | Global, with premium segment leadership in North America and China | Short term (≤ 2 years) |

| Stringent Emission and Safety Regulations | +1.2% | EU (UN R155/R156), China (GB 44495), North America (NHTSA) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Integration of Advanced Driver-Assistance Systems (ADAS)

Cameras, radar, and lidar arrays are scaling rapidly, and the data they generate exceeds what legacy buses can transport within safety-critical latency windows. Centralized domain controllers now fuse perception inputs in real time, pushing the automotive communication technology market toward Ethernet backbones that support time-sensitive networking. Global New Car Assessment protocols increasingly award points for automated steering features that require microsecond-level determinism, embedding communication performance directly into crash-test outcomes. Component makers reply with system-on-chip transceivers that combine CAN-XL, 10BASE-T1S, and hardware security accelerators on a single die. As ADAS becomes standard even in entry-level trims, bandwidth demand expands faster than average vehicle selling prices, making network efficiency pivotal to OEM margins.

Emergence of Zonal E/E Architectures Requiring Ethernet Backbones

Zonal designs collapse dozens of distributed electronic control units into a handful of regionally placed compute nodes. This re-layout shortens harnesses, simplifies power distribution, and concentrates cybersecurity defenses at a few network ingress points. Premium OEMs in Europe and North America have validated early zonal prototypes that reduce wiring mass by roughly one-third, improving energy efficiency in battery-electric vehicles. The architectural shift dovetails with the adoption of multi-gigabit Ethernet, as a single twisted pair can now carry both deterministic control traffic and infotainment streams. Suppliers that deliver switch silicon with built-in functional safety and time-aware shaping win design slots across multiple vehicle lines, catalyzing consolidation inside the automotive communication technology market.

OEM Shift Toward Software-Defined Vehicles and OTA Communication

Separating application logic from hardware lets manufacturers monetize features post-sale, but doing so safely hinges on end-to-end authenticated update chains. UN Regulation 156 mandates auditable update procedures for all new types approved in UN contracting states. The resulting need for large payload transfers favors IP-based networks that can multicast software images without saturating bandwidth. Vendors who offer automotive-grade switches with integrated intrusion-detection logic thus secure long-term recurring revenue streams in the automotive communication technology market.

Adoption of Time-Sensitive Networking (TSN) for Deterministic Automotive Ethernet

Time-sensitive networking extends standard IEEE 802.1 Ethernet with scheduling, preemption, and clock synchronization mechanisms that guarantee bounded latency. Zonal gateways equipped with TSN-capable MACs can now mix fail-operational brake-by-wire messages and high-bit-rate infotainment data on a common backbone without violating functional-safety budgets. Although test-equipment maturity still lags protocol complexity, early production programs prove that TSN can coexist with legacy CAN during transition phases. The automotive communication technology market, therefore, sits at an inflection point. As validation toolchains stabilize, TSN moves from experimental to mainstream, broadening suppliers' addressable revenue while trimming vehicle bill of materials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Network Validation Cost | -1.2% | Global, hits smaller OEMs | Short term (≤ 2 years) |

| Limited Multi-Gig PHY Supply | -0.9% | Worldwide supply chains | Short term (≤ 2 years) |

| V2X Cyber-Security Vulnerabilities | -0.8% | North America and the EU focus | Medium term (2–4 years) |

| CAN/LIN-Ethernet Interoperability Hurdles | -0.7% | Global hybrid platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost and Complexity of Validating High-Speed Networks

Proving that a mixed-protocol vehicle network remains safe under electromagnetic stress and cyberattack involves time-consuming lab campaigns. OEMs must purchase specialized error-injection benches and retrain validation engineers unfamiliar with Ethernet determinism. Regulatory frameworks such as UN Regulation 155 add continuous threat-monitoring requirements, extending test scopes well past those of earlier CAN-centric programs. Smaller automakers face disproportionate cost burdens, which delay feature introductions and temporarily restrain volume growth in the automotive communication technology market. Collaborative validation hubs are emerging to share equipment loads, but best-practice harmonization remains elusive.

Limited Supply of Automotive-Grade Multi-Gig PHY Semiconductors

Multi-gigabit physical-layer chips require niche process nodes and extended-temperature qualification, leaving only a few foundries able to meet automotive reliability targets. Pandemic-era fab expansions focused on consumer silicon, and reallocating capacity has proven slow. Suppliers, therefore, prioritize high-volume passenger-car programs, starving specialty commercial-vehicle lines of the parts they need. While APAC governments fund new fabs, commissioning timelines mean shortages may linger for at least two model cycles. This scarcity tempers the near-term penetration rate of Ethernet backbones across the automotive communication technology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bus Module: Ethernet Takes Pole Position in Zonal Architectures

Controller Area Network retained the largest 41.22% of the automotive communication technology market share in 2025, a testament to its entrenched presence in body and legacy powertrain domains. Automotive Ethernet is forecast to record the fastest CAGR of 12.84% through 2031, underscoring its role as the spine of next-generation zone controllers. Developers now integrate CAN-XL alongside 10BASE-T1S so that gateways can translate critical messages during staged migrations toward full Ethernet. This hybrid approach safeguards platform continuity and lets OEMs roll out advanced features without wholesale rewiring. Hardware vendors that supply mixed-protocol switches are therefore indispensable allies for cost-optimized platform roadmaps.

The coexistence of Ethernet and CAN reshapes supplier ecosystems inside the automotive communication technology market. Tier-1 system integrators must demonstrate determinism by combining time-aware shaping on Ethernet links with gateway buffering for CAN traffic. Test-equipment makers respond by bundling frame-preemption probes and CAN error-injection modules into single consoles, reducing laboratory complexity. Cybersecurity auditors also adjust: a zonal network permits firewalling at fewer ingress points, simplifying compliance with UN Regulation 155 yet raising the stakes for each gateway’s resilience.

By Application: Safety & ADAS Outpace Established Powertrain Dominance

Powertrain communication commanded a 36.08% of the automotive communication technology market share in 2025, but safety and advanced driver-assistance systems are projected to lead growth with a 13.15% CAGR. This inversion springs from mandates for emergency steering and lane-keeping that require deterministic sensor fusion. Ethernet backbones with TSN scheduling ensure that perception data reaches actuation logic within microsecond windows, elevating communication performance to life-critical status. Suppliers race to embed TSN hardware blocks into microcontrollers to secure design wins ahead of regulation-driven cut-over dates. The resulting innovation loop positions ADAS networking as the bellwether for broader electronic-architecture change.

Convergence between external V2X feeds and on-board sensor suites is reshaping software stacks in the automotive communication technology market. Domain controllers once dedicated to camera fusion now parse certificate chains and threat telemetry from roadside units, blending cybersecurity with perception. Local road agencies pilot green-light priority schemes that rely on guaranteed packet-delivery windows, reinforcing demand for deterministic networks. As a corollary, powertrain engineers adopt Ethernet to synchronize regenerative braking and thermal subsystems with ADAS inputs, minimizing energy loss in electric vehicles.

By Communication Type: V2X Sets the Pace for External Connectivity

Vehicle-to-everything services captured a leading 58.17% of the automotive communication technology market share in 2025. They will also post the fastest CAGR of 11.89%, reflecting the regulatory alignment that followed the FCC’s spectrum reallocation decision. Cellular sidelink modes in 3GPP Release 16 now allow direct car-to-car communication without tower coverage, smoothing rural-deployment hurdles [3]"3GPP NR V2X Mode 2: Overview, Models and System-Level Evaluation," National Library of Medicine, pmc.ncbi.nlm.nih.gov. Pilot corridors in China bundle infrastructure subsidies with vehicle incentives, creating reinforcing demand loops. Japan and South Korea standardize test protocols that factor V2X performance into star-rating systems, transforming connectivity from an optional upgrade to a safety prerequisite. This linkage seeds a robust installed base that component makers court with integrated modem-plus-switch solutions.

As infrastructure density grows, V2X data increasingly informs on-board decision-making rather than serving only driver information dashboards. Edge-cloud systems flag blind-intersection hazards and feed alerts to brake-by-wire controllers via Ethernet gateways. The resulting traffic prioritization on in-vehicle networks cements V2X as a cornerstone use case justifying Ethernet migration. Over time, release-over-air firmware updates further blur lines between in-vehicle and external communication realms, embedding continuous security monitoring into telematics control units.

By Vehicle Type: Passenger Cars Lead, Commercial Fleets Catch Up

Passenger vehicles held the dominant 72.11% of the automotive communication technology market share in 2025, yet the commercial segment shows momentum as fleet operators eye telematics efficiencies. Passenger EVs stand out with the fastest 11.58% CAGR, thanks to simplified powertrains and generous government incentives across major economies. Commercial-vehicle electrification lags, but connectivity retrofits bridge functional gaps by overlaying V2X modules on existing CAN backbones. OEMs thus architect gateway designs that scale across duty cycles, boosting volume leverage. The strategy cushions R&D risks while supplying commercial customers with phased upgrade paths.

Consumer expectations for seamless smartphone integration influence wiring budgets, nudging passenger-car OEMs toward Ethernet even in entry models. Automated valet parking pilots showcase how cloud-assisted control can reduce parking-lot footprint, creating value stories that resonate with city planners. In commercial vehicles, predictive-maintenance dashboards powered by high-bandwidth telematics minimize downtime penalties, making connectivity investments straight-line budget items rather than discretionary spend. Consequently, convergence trends close the historical gap between passenger and commercial electrical architectures, elevating the entire automotive communication technology market toward unified design targets.

By Propulsion Type: Battery Electric Vehicles Drive Networking Sophistication

Internal-combustion platforms commanded a 65.46% of the automotive communication technology market share in 2025, yet battery electric vehicles will post the fastest 14.33% CAGR as automakers chase zero-emission targets. Paradoxically, mechanical simplification magnifies communication demands because regenerative braking, thermal loops, and high-voltage safety interlocks all require precise coordination. Ethernet with TSN scheduling guarantees that distributed power electronics exchange timing-critical data even under variable state-of-charge scenarios. As a result, propulsion strategy now dictates network roadmap, intertwining drivetrain and communication procurement.

Fuel-cell prototypes mirror battery electric data-traffic patterns by monitoring hydrogen stack integrity and storage pressure in real time. Hybrid architectures add complexity because control logic must arbitrate torque blending between internal-combustion and electric motors, demanding high-speed gateways that span protocol generations. Standards such as ISO 15118-20 broaden the scope beyond charging to include grid interaction, cybersecurity, and the embedding of payment tokens into energy flows. Suppliers that master these cross-domain hooks gain influence over OEM energy-strategy roadmaps, further entwining propulsion and communication choices across the automotive communication technology market.

By Distribution Channel: Aftermarket Retrofits Unlock Fleet Value

OEM-installed networks retained an 88.33% of the automotive communication technology market share in 2025. Still, aftermarket modules are forecasted to grow at a 12.44% CAGR as municipalities subsidize connectivity upgrades for existing fleets. Plug-and-play dongles that tap on-board diagnostics ports shortcut integration hurdles, making V2X gains accessible without new-vehicle purchases. Fleet managers recoup investments through toll discounts and optimized routing algorithms delivered over cellular links. Retrofit suppliers thus capture a distinct slice of the automotive communication technology market that values deployment speed over deep in-vehicle integration.

OEM channels nevertheless protect their turf by bundling cybersecurity features that aftermarket solutions find difficult to replicate without proprietary key access. Regulators reward factory systems with streamlined type-approval, nudging risk-averse buyers toward factory options. Over time, both channels may converge as OEMs license secure update frameworks to independent module vendors, offering a revenue-sharing model instead of direct competition. This hybrid approach balances speed and security, allowing the automotive communication technology market to expand without exposing drivers to unmanaged cyber risks.

Geography Analysis

Asia-Pacific commanded a 47.14% of the automotive communication technology market share in 2025 and is expected to expand at a 12.06% CAGR through 2031, propelled by China’s large-scale vehicle-road-cloud pilots and South Korea’s integration of cooperative intelligent transport systems into national crash tests. China’s mandatory GB 44495 rule requires certificate-based V2X security and pushes OEMs toward Ethernet backbones, creating a vast domestic pipeline of opportunities. Japan’s ministry-backed pilots feed technical feedback into procurement standards, accelerating supplier readiness. South Korea’s dual-mode V2X platform eases transition pains by bridging cellular and DSRC vehicles. India’s premium models begin to specify 100BASE-T1, foreshadowing gradual mainstream diffusion.

Europe and North America adopt a more coordinated, but slower, rollout under the umbrella of UN Regulations 155 and 156, which embed cybersecurity and software-update management into type-approval checklists. The FCC’s decision to clear the 5.9 GHz band for cellular V2X removed spectrum uncertainty, permitting OEMs to finalize single-mode radio roadmaps. Germany’s supplier base exerts outsized influence on IEEE working groups, injecting European latency and safety perspectives into global Ethernet standards. The United Kingdom follows UN regulations despite regulatory divergence elsewhere, preserving cross-channel parts interchangeability. North American test corridors, such as Michigan’s open-road labs, provide real-world data that shorten validation cycles.

Emerging regions adopt imported electrical architectures rather than crafting bespoke standards, saving validation costs but deferring the implementation of localized feature sets. Brazil’s assembly plants build on EU-spec platforms that already contain Ethernet gateways, while the United Arab Emirates mandates V2X only for premium limousine fleets. South African export hubs are integrating Ethernet to serve European destination markets, even though local buyers still favor basic CAN. Russian carmakers maintain CAN-FD compatibility to ensure eventual reintegration with Western supply chains. Across all non-core geographies, the automotive communication technology market grows via technology trickle-down rather than headline-grabbing pilot programs.

Competitive Landscape

The automotive communication technology market is characterized by moderate concentration, with five semiconductor giants accounting for the majority of transceiver and switch portfolios. Their integrated system-on-chip strategies embed hardware security modules, ASIL-D functional safety, and IEEE 802.1AS time synchronization in a single package, trimming the bill of materials for Tier-1 integrators. Ethernet switch families now offer over 80 Gbps aggregate throughput, reflecting an arms race to consolidate camera, lidar, and telematics traffic in zone gateways. Cellular chipset suppliers diversify into automotive networking by pairing 5G modems with TSN-capable switch cores, leveraging telecom expertise to disrupt incumbents.

Start-ups champion software-defined networking stacks that virtualize gateway functions on general-purpose CPUs, promising OTA-enabled feature rollout without hardware swaps. Standards maturation, notably IEEE 802.1DG’s TSN profile, sets performance baselines and reduces differentiation on pure transport functions. Consequently, cybersecurity resilience and update orchestration emerge as new battlegrounds, where vendors tout intrusion-detection analytics and hardware-anchored root-of-trust blocks as value-add extensions. Price-sensitive mid-tier OEMs gravitate toward one-stop silicon-software bundles that simplify validation under UN Regulation 155.

Consolidation pressures intensify because zonal architectures reduce the number of electronic control units per vehicle, shrinking the sheer number of component slots. Suppliers answer by bundling Ethernet switches, microcontrollers, and power-management ICs into reference designs that cut integration timelines. Aftermarket retrofits create parallel demand streams for plug-and-play V2X boxes, yet those volumes remain a fraction of OEM pipelines. Overall, the automotive communication technology market balances scale efficiencies with specialized niches, rewarding vendors that flex across multiple layers of the communication stack.

Automotive Communication Technology Industry Leaders

-

NXP Semiconductors N.V.

-

Broadcom Inc.

-

Texas Instruments Inc.

-

Infineon Technologies AG

-

Renesas Electronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: LG Innotek agreed to supply a Wi-Fi 7 automotive communication module to a prominent European parts company.

- December 2025: TTTech Auto launched MotionWise Communication middleware to unify in-vehicle data exchange.

- August 2025: Awinic Electronics released automotive-grade RF switch products AW13612PFDR-Q1 and AW12022TQNR-Q1 for connected-vehicle applications.

- August 2025: Infineon Technologies AG completed the takeover of Marvell Technology’s automotive Ethernet unit, expanding its software-defined vehicle capabilities.

Global Automotive Communication Technology Market Report Scope

The Automotive Communication Technology Market is segmented based on bus type, application, communication type, vehicle type, propulsion type, distribution channel, and geography.

By Bus Module, the market is segmented into Local Interconnect Network (LIN), Controller Area Network (CAN), FlexRay, Media-Oriented Systems Transport (MOST), and Automotive Ethernet. By Application, the market is segmented into Powertrain, Body Control and Comfort, Infotainment and Communication, and Safety and ADAS. By Communication Type, the market is segmented into Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), and Vehicle-to-Everything (V2X). By Vehicle Type, the market is segmented into Passenger Vehicles, Light Commercial Vehicles, and Medium and Heavy Commercial Vehicles. By Propulsion Type, the market is segmented into Internal Combustion Engine (ICE), Battery Electric Vehicle (BEV), Hybrid Electric Vehicle (HEV), Plug-in Hybrid Electric Vehicle (PHEV), and Fuel-Cell Electric Vehicle (FCEV). By Distribution Channel, the market is segmented into OEM and Aftermarket. By Geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, and Rest of South America), Europe (United Kingdom, Germany, Spain, Italy, France, Russia, and Rest of Europe), Asia-Pacific (India, China, Japan, South Korea, and Rest of Asia-Pacific), and Middle East and Africa (United Arab Emirates, Saudi Arabia, Turkey, Egypt, South Africa, and Rest of Middle East and Africa).

Market forecasts are provided in terms of Value (USD).

| Local Interconnect Network (LIN) |

| Controller Area Network (CAN) |

| FlexRay |

| Media-Oriented Systems Transport (MOST) |

| Automotive Ethernet |

| Powertrain |

| Body Control and Comfort |

| Infotainment and Communication |

| Safety and ADAS |

| Vehicle-to-Vehicle (V2V) |

| Vehicle-to-Infrastructure (V2I) |

| Vehicle-to-Everything (V2X) |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Bus Module | Local Interconnect Network (LIN) | |

| Controller Area Network (CAN) | ||

| FlexRay | ||

| Media-Oriented Systems Transport (MOST) | ||

| Automotive Ethernet | ||

| By Application | Powertrain | |

| Body Control and Comfort | ||

| Infotainment and Communication | ||

| Safety and ADAS | ||

| By Communication Type | Vehicle-to-Vehicle (V2V) | |

| Vehicle-to-Infrastructure (V2I) | ||

| Vehicle-to-Everything (V2X) | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the automotive communication technology market in 2026?

The automotive communication technology market size reached USD 24.94 billion in 2026 and is projected to climb to USD 42.44 billion by 2031.

Which application segment is expanding the quickest?

Safety and ADAS functions are advancing at a 13.15% CAGR, the fastest among applications, as regulatory bodies embed deterministic networking into automated-driving requirements.

Why is Ethernet adoption accelerating inside vehicles?

Ethernet backbones offer multi-gigabit bandwidth and time-sensitive networking features that CAN and LIN cannot match, making them essential for sensor fusion, OTA updates and compliance with cybersecurity rules such as UN R155.

What drives aftermarket demand for communication upgrades?

Fleet operators retrofit V2X and telematics modules to gain tolling discounts, traffic-signal priority and predictive-maintenance insights without waiting for new-vehicle acquisition cycles.

Page last updated on: