Automotive Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

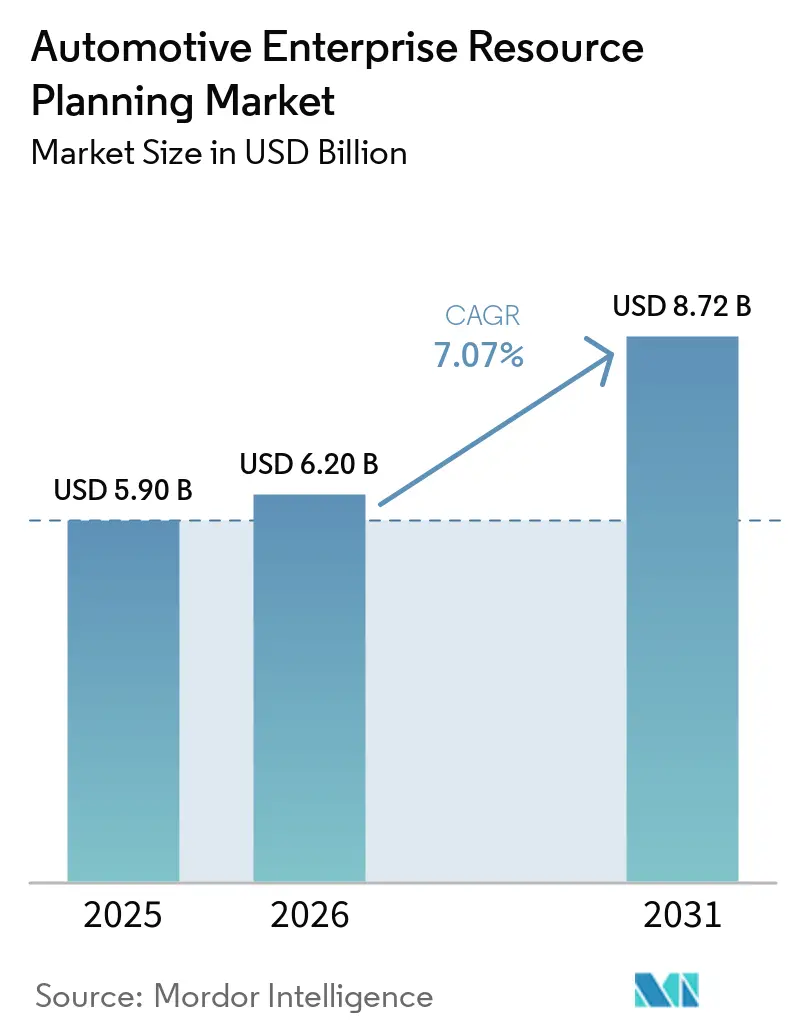

| Market Size (2026) | USD 6.20 Billion |

| Market Size (2031) | USD 8.72 Billion |

| Growth Rate (2026 - 2031) | 7.07% CAGR |

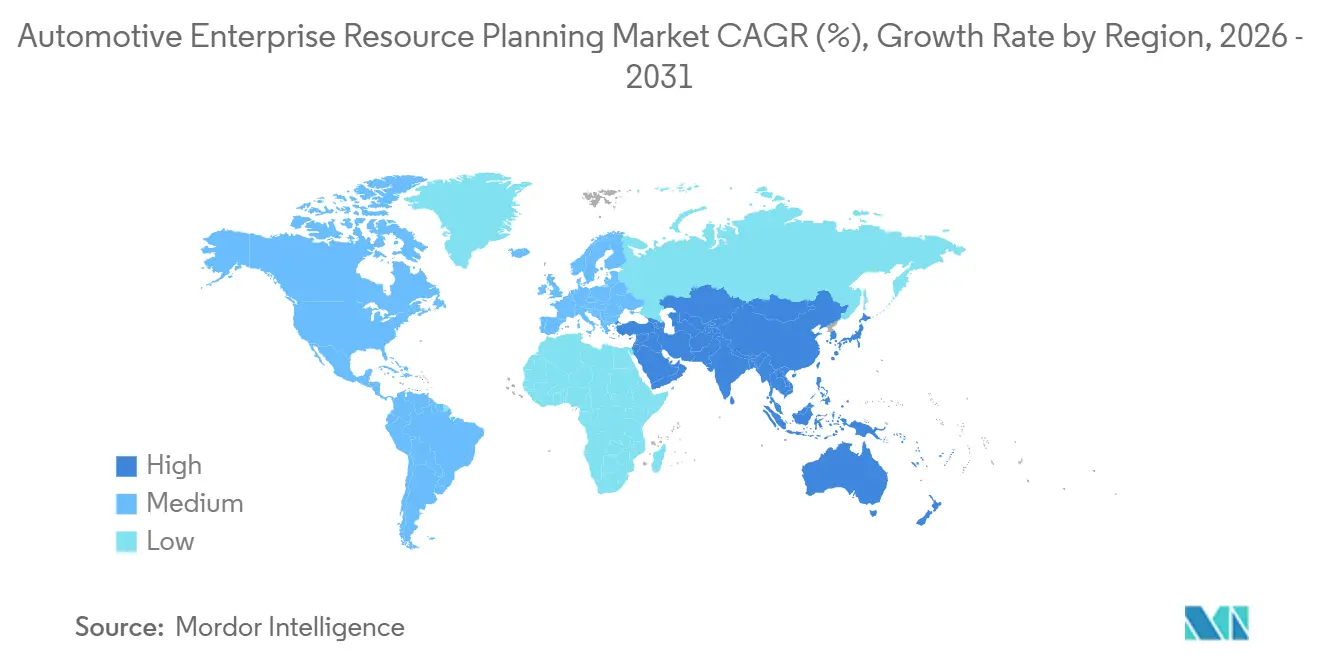

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Enterprise Resource Planning Market Analysis by Mordor Intelligence

The automotive ERP market size is projected to expand from USD 5.90 billion in 2025 and USD 6.20 billion in 2026 to USD 8.72 billion by 2031, registering a CAGR of 7.07% between 2026 and 2031. Cloud-native deployments that embed artificial intelligence and Internet of Things functions inside production planning, quality control, and supply chain modules dominate current demand and set the competitive tone for new contracts. Large original equipment manufacturers are accelerating cloud migration to support software-defined vehicle programs, while Tier-2 suppliers view modular, subscription-priced suites as a pathway to meet electronic data interchange and IATF 16949 mandates without owning data centers. Vendors now differentiate through embedded analytics that cut month-end close cycles from weeks to days and through industry cloud portfolios that shorten implementation by pre-configuring automotive workflows. Yet recent ransomware attacks on dealer management systems spotlight cybersecurity and data residency as gating factors that steer some customers toward hybrid architectures where shop-floor execution remains local and synchronizes with the cloud in scheduled windows.

Key Report Takeaways

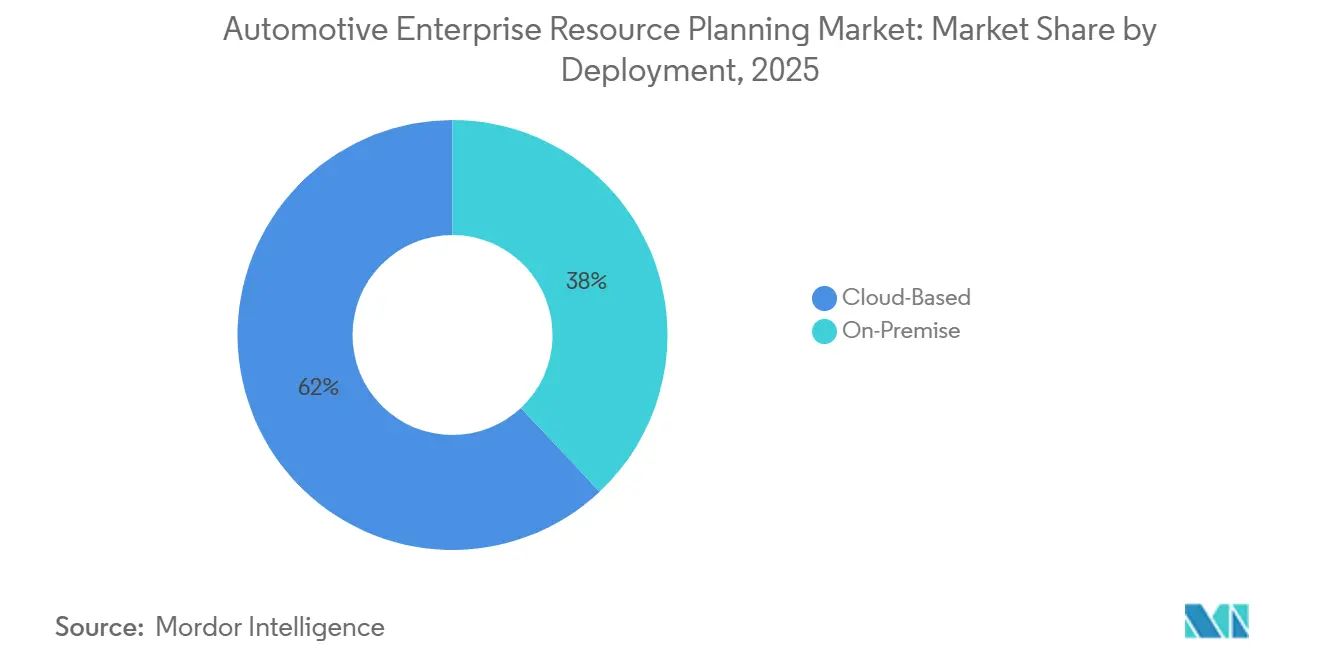

- By deployment model, cloud platforms captured 62% of the automotive ERP market share in 2025, while on-premises solutions are advancing at a 13.40% CAGR through 2031.

- By organization size, large enterprises accounted for 54% of revenue in 2025; small and medium enterprises are forecast to expand at a 12.10% CAGR through 2031.

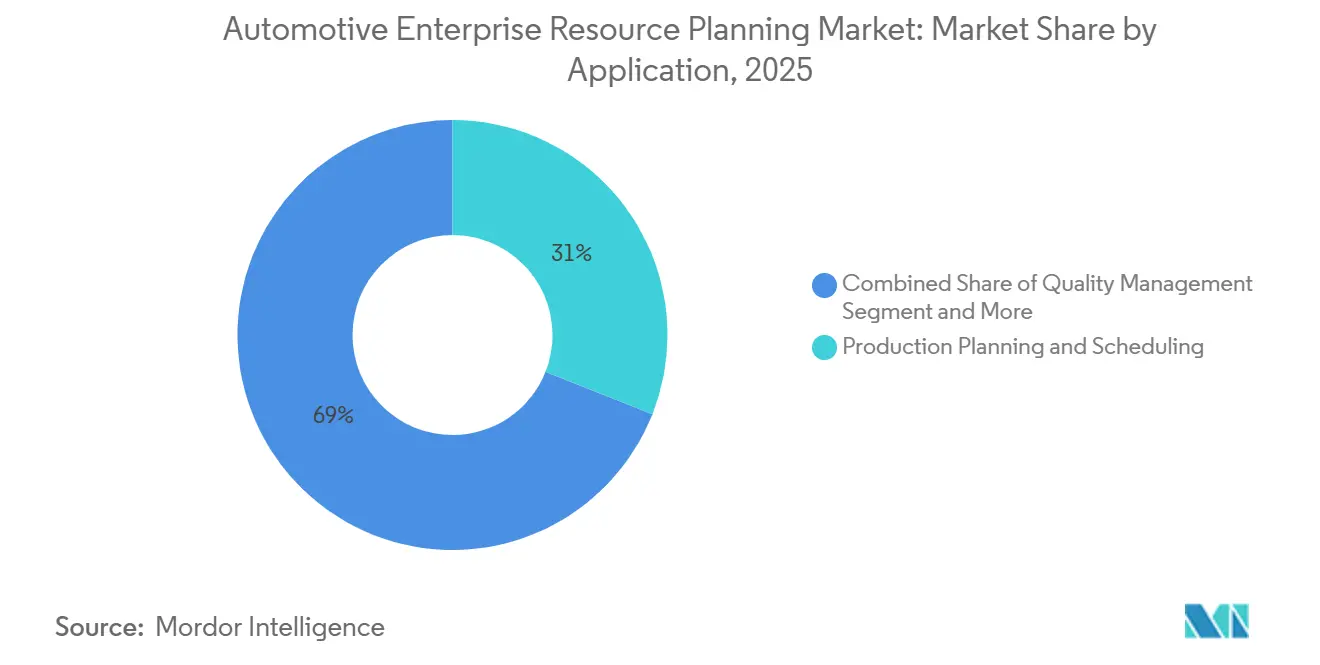

- By application, production planning and scheduling accounted for 31% of the automotive ERP market in 2025, whereas quality management is poised to grow at a 14.20% CAGR through 2031.

- By end user, fleet operators are projected to record the fastest 15.00% CAGR to 2031, outpacing original equipment manufacturers, suppliers, and dealerships.

- By geography, North America led with a 33% revenue share in 2025, and Asia-Pacific is set to grow at a 11.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Cloud-Based ERP in Automotive Manufacturing | +2.1% | Global, especially North America and Western Europe | Short term (≤ 2 years) |

| Integration of AI and IoT for Predictive Maintenance and Quality Control | +1.8% | Germany, Japan, United States | Medium term (2-4 years) |

| Shift Toward Modular Architectures to Support Software-Defined Vehicles | +1.5% | North America, Europe, China | Medium term (2-4 years) |

| Compliance with Stringent Emissions and Traceability Regulations | +1.2% | Europe, China, North America | Long term (≥ 4 years) |

| Consolidation of Global Supply Chains Post Semiconductor Shortages | +0.9% | Asia-Pacific and Europe | Short term (≤ 2 years) |

| Growing Demand for Real-Time Analytics in EV Battery Lifecycle Management | +0.8% | China, Europe, United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Cloud-Based ERP in Automotive Manufacturing

Cloud adoption in automotive plants rose between 2024 and 2025 as subscription economics converted capital expenses into operating expenses, reducing the burden of on-site infrastructure. Original equipment manufacturers now unify regional instances on single-tenant clouds to gain real-time inventory visibility across dozens of factories, cutting close-cycle times by more than one week and enabling faster responses to part shortages. Early adopters, however, discovered that uninterrupted connectivity is essential, prompting hybrid topologies in which execution data is cached locally and synchronized at scheduled intervals. This compromise preserves shop-floor reliability while still tapping cloud analytics, although it introduces middleware complexity that requires new integration skills inside information technology teams. Consequently, consulting partners that can blueprint zero-downtime cutovers and edge-to-cloud synchronization patterns are winning high-margin service work.

Integration of AI and IoT for Predictive Maintenance and Quality Control

Modern automotive ERP suites ingest vibration, temperature, and acoustic telemetry from programmable logic controllers and robot cells, generating machine-learning forecasts that warn maintenance teams of failures three to four days ahead of time. Suppliers deploying these capabilities have reported double-digit reductions in unplanned downtime and a boost in first-pass yield after embedding computer-vision defect detection into quality workflows. As ERP morphs from a transactional ledger into a prescriptive decision engine, workforce skills must evolve to focus on interpreting algorithmic recommendations rather than manual inspections. Vendors that supply no-code model-training environments and pre-trained defect libraries lower the barrier for Tier-2 suppliers that lack data-science talent, accelerating diffusion across the production network.

Shift Toward Modular Architectures to Support Software-Defined Vehicles

Software-defined vehicles require ERP to handle software bills of material alongside mechanical parts, track firmware versions by vehicle identification number, and launch recall campaigns triggered by security vulnerabilities rather than hardware faults. Microservices-based ERP enables manufacturers to replace modules without disruptive core upgrades, speeding time-to-market for new over-the-air features. This flexibility is vital for joint ventures between automakers and technology firms, where distinct legacy systems need to coexist while sharing production data. Early movers demonstrate that modular architectures cut new feature release cycles by as much as half compared with monolithic suites, strengthening competitive positions in the race to deliver continuous vehicle updates.

Compliance with Stringent Emissions and Traceability Regulations

Euro 7, the Carbon Border Adjustment Mechanism, and China’s dual-carbon policy collectively push the automotive ERP market toward traceability features that capture Scope 1, 2, and 3 emissions and provide digital product passports for batteries. [1]European Commission, “Euro 7 Emissions Standards for Light and Heavy-Duty Vehicles,” ec.europa.eu Failure to supply certified data threatens exclusion from lucrative markets, so even small stamping plants now view modern ERP as a ticket to participate in global supply chains. Systems capable of linking material provenance with carbon intensity at a part-number level transform compliance from a reporting afterthought into a strategic differentiator that secures preferred-supplier status and de-risked revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Costs and Lengthy Implementation Cycles for Tier-2 Suppliers | -1.4% | South America, Southeast Asia, Eastern Europe | Short term (≤ 2 years) |

| Data Security and IP Protection Concerns in Cloud Deployments | -1.1% | Germany, Japan, South Korea | Medium term (2-4 years) |

| Shortage of Skilled ERP Professionals in Emerging Markets | -0.9% | India, Mexico, Brazil, Vietnam, Thailand | Long term (≥ 4 years) |

| Legacy System Integration Complexities in Large OEM Environments | -0.7% | North America, Europe, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Costs and Lengthy Implementation Cycles for Tier-2 Suppliers

Tier-2 machining and molding firms often operate on thin net margins, making six-figure software investments and year-long deployment projects financially daunting. Academic research highlights cost overruns rooted in data-cleansing surprises, customization creep, and reliance on external consultants. Seasonal production peaks compound the challenge, as subject-matter experts cannot be spared for workshops and user acceptance testing during order surges. Cloud subscriptions ease capital expenditure yet introduce permanent operating charges that shrink profitability unless suppliers renegotiate prices with customers. Consequently, many Tier-2 firms defer full-scale ERP adoption or choose narrow functional rollouts, delaying the network effects that original equipment manufacturers expect from end-to-end digital integration.

Data Security and IP Protection Concerns in Cloud Deployments

Automotive executives fear that cloud platforms hosting proprietary process recipes and costed bills of material will become high-value targets for cyber criminals or nation-state espionage. A high-profile ransomware attack on a dealer management system in 2024 underscored operational risks, freezing vehicle sales for nearly two weeks. Regulators in Germany and Japan enforce strict data-residency mandates, forcing providers to stand up regional data centers at premium cost, which erodes the economies of scale normally associated with hyperscale infrastructure. Some manufacturers respond with hybrid strategies that keep sensitive intellectual property on-premises while pushing transactional workloads to the cloud, but this split model creates architectural complexity and latency that blunt real-time analytics benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Growth Accelerates Despite Hybrid Complexities

Cloud platforms represented 62% of spending in 2025 and are projected to outpace the overall automotive ERP market at a 13.40% CAGR through 2031. This momentum reflects vendor roadmaps that prioritize cloud-only innovation, such as artificial intelligence-driven demand sensing and zero-touch upgrades. The automotive ERP market size for on-premises solutions continues to shrink among Tier-1 suppliers, yet pockets of resistance remain in plants with unreliable broadband or stringent sovereignty mandates. Hybrid configurations, where manufacturing execution workloads remain local and synchronize periodically, balance latency and resilience but add middleware overhead and monitoring burden. Over time, the widening functionality gap pushes even reluctant customers toward cloud adoption as they seek predictive maintenance and supply chain control tower features unavailable in legacy releases.

The June 2024 cyber incident that crippled thousands of dealerships stimulated rigorous third-party security audits and multimillion-dollar cyber-insurance requirements in new procurement cycles. Providers responded with ISO 27001 certifications, zero-trust frameworks, and recovery point objectives of 15 minutes or less, restoring buyer confidence. Subscription pricing that spreads expenses over time appeals to small suppliers, yet total lifetime costs must still compete with depreciated on-premises assets. Consequently, buyers now issue requests for proposal that demand clear five-year total cost of ownership models, transparent exit clauses, and regionally partitioned data-storage options, shaping a maturing procurement discipline inside the automotive ERP market.

By Organization Size: Small and Medium Enterprises Narrow the Digitization Gap

Large enterprises accounted for 54% of revenue in 2025, reflecting multibillion-dollar original equipment manufacturer rollouts across finance, logistics, and engineering change control. The automotive ERP market share among small and medium enterprises is expanding rapidly as electronic data interchange mandates make spreadsheet-based workflows untenable. Vendors court this segment with pre-configured templates and rapid deployment accelerators that promise go-live in under 120 days, though such speed often limits customization and later triggers rework. Successful adopters report reduced line-stop incidents because material call-offs now synchronize directly from customer production schedules, eliminating phone-call firefighting.

Implementation success still hinges on executive sponsorship and change management skills that many small firms lack, resulting in projects missing timelines or budgets. To mitigate the gap, ecosystem partners bundle managed services that provide remote application management and periodic process audits, turning ERP into an operational subscription rather than a one-time technology purchase. As cloud maturity rises, collective learning reduces configuration errors, and templates embed industry best practices such as failure mode and effects analysis out of the box, lowering risk and encouraging broader SME participation in the automotive ERP market.

By Application: Quality Management Surges Under Regulatory Pressure

Production planning and scheduling retained the largest slice of the automotive ERP market size at 31% in 2025, reflecting its centrality to just-in-sequence assembly and global build-to-order models. Quality management, however, is advancing at a robust 14.20% CAGR as IATF 16949 audits intensify and digital product passport rules loom for batteries. [2]IATF, “IATF 16949:2016 Automotive Quality Management System Standard,” iatfglobaloversight.org Modern modules integrate statistical process control charts and computer vision inspection, automatically opening rework orders and adjusting takt time to minimize scrap and warranty exposure.

Supply chain and inventory applications climbed sharply after semiconductor shortages exposed blind spots beyond Tier-1 suppliers, driving demand for multi-tier control towers that predict disruptions weeks in advance. Finance, human resources, and customer relationship management round out the suite, with embedded analytics that correlate order intake, overtime costs, and material inflation to inform pricing and capacity decisions. The composability trend means customers mix enterprise core finance with specialty-quality or battery-traceability apps, selecting the optimal blend of breadth and depth for their unique footprint.

By End User: Fleet Operators Propel the Next Wave of Demand

Original equipment manufacturers accounted for 38% of revenue in 2025, leveraging global ERP backbones to manage complex bills of material and coordinate simultaneous launches across continents. Fleet operators form the fastest-growing slice, clocking a 15.00% CAGR as electric vehicle adoption accelerates and real-time battery health feeds directly into enterprise maintenance planners. Integrated telematics and ERP reduce unscheduled downtime and extend asset life, making the business case compelling for logistics firms and ride-hailing platforms.

Tier-1 and Tier-2 suppliers remain the numerically largest customer group, with more than 50,000 component makers worldwide needing ERP for electronic data interchange compliance. Dealerships are migrating from legacy dealer management systems to cloud-native alternatives that embed digital retail journeys, transforming back-office accounting and customer experience in parallel. Each end-user cohort demands tailored functionality, forcing vendors to build vertical add-ons or partner with specialists, thereby widening the ecosystem and adding cross-selling opportunities inside the automotive ERP market.

Geography Analysis

North America led with 33% revenue share in 2025, buoyed by entrenched ERP estates at Detroit original equipment manufacturers and a wave of dealer management system replacements. Cloud adoption accelerates as automotive ERP vendors capitalize on scalable infrastructure and artificial intelligence features that North American buyers quickly monetize. Data-localization rules are comparatively lenient, enabling faster rollout of multi-region tenants that consolidate operations across Canada, Mexico, and the United States.

Asia-Pacific is on track to post an 11.90% CAGR through 2031, driven by China’s vast vehicle production base and government policies favoring domestic ERP champions that already hold nearly three-quarters of the local manufacturing segment.[3]China Automotive Industry Association, “2024 China Automotive Production Statistics,” caam.org.cn India’s component export growth fuels rapid cloud uptake among Tier-2 suppliers aiming to meet global electronic data interchange and sustainability requirements. [4]Automotive Component Manufacturers Association of India, “Auto Component Export Data 2024,” acma.in Japan faces the 2025 cliff for legacy infrastructure, prompting urgent modernization projects, even as cultural caution continues to favor hybrid or private-cloud deployments under domestic control.

Europe’s stringent environmental directives reshape buying criteria toward carbon-accounting capabilities, cementing ERP’s role in compliance workflows. South America and the Middle East and Africa expand more modestly as capital constraints and limited connectivity slow migrations, but burgeoning assembly plants attract SaaS vendors that bundle connectivity hardware alongside software subscriptions. Overall, regional dynamics underscore that the automotive ERP market is governed as much by policy and data sovereignty as by pure technology considerations.

Competitive Landscape

The top five vendors account for a significant share of collective revenue, signaling a moderately consolidated field where scale advantages in research and development and cybersecurity investments matter. Incumbents leverage their installed bases to sell industry clouds that promise zero-defect migration to modern architectures, while cloud-native entrants win greenfield projects by cutting deployment from 18 months to three. Artificial intelligence copilots that automate journal entries, suggest master-data corrections, and forecast demand have become baseline differentiators rather than future features.

Strategic acquisitions shape product breadth, such as the absorption of supply chain analytics and asset-management firms that instantly enhance multi-tier visibility and predictive maintenance capabilities. Security posture now carries equal weight with functionality, following highly publicized cyber incidents. Buyers routinely demand SOC 2 Type II reports, regional data center options, and recovery point objectives of 15 minutes or less, screening out vendors without robust operational discipline.

White-space opportunities cluster around battery lifecycle management, multi-tier semiconductor supply chain control, and composable microservices that let customers hot-swap modules without risking plant downtime. Vendors capable of demonstrating under-four-hour recovery from simulated outages and providing open application programming interfaces capture premium pricing and longer contract terms. Consequently, the competitive bar has risen from transactional breadth toward measurable operational resilience, positioning security investments and uptime guarantees as decisive levers inside the automotive ERP market.

Automotive Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor, Inc.

Epicor Software Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Microsoft signed a USD 150 million, five-year agreement with Stellantis to deploy Dynamics 365 Finance and Operations across 130 plants in 30 countries, targeting a 20% inventory reduction and higher on-time delivery performance.

- January 2026: SAP introduced Industry Cloud for Automotive, embedding more than 200 sector-specific processes including battery passport workflows and electronic data interchange adapters, with promises of 40% faster deployment versus bespoke projects.

- November 2025: Tekion secured USD 200 million in Series D funding at a USD 3.5 billion valuation to fuel European and Asia-Pacific expansion targeting 2,000 dealership go-lives by 2027.

- September 2025: Oracle purchased Cerner’s automotive supply chain analytics arm for USD 850 million, weaving multi-tier risk prediction into Fusion Cloud Supply Chain Management.

Global Automotive Enterprise Resource Planning Market Report Scope

The Automotive ERP market refers to the ecosystem of specialized enterprise software solutions and associated services designed to manage, integrate, and optimize end-to-end business processes across the automotive value chain, including manufacturing, supply networks, distribution, and aftersales operations.

The Automotive ERP Report is Segmented by Deployment Model (Cloud-Based, On-Premises), Organization Size (Small and Medium Enterprises, Large Enterprises), Application (Production Planning and Scheduling, Supply Chain and Inventory Management, Finance and Accounting, Human Resources and Payroll, Quality Management, Customer Relationship Management, Other Applications), End User (Original Equipment Manufacturers, Tier 1 and Tier 2 Suppliers, Dealerships and Distributors, Fleet Operators), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premises |

| Small and Medium Enterprises |

| Large Enterprises |

| Production Planning and Scheduling |

| Supply Chain and Inventory Management |

| Finance and Accounting |

| Human Resources and Payroll |

| Quality Management |

| Customer Relationship Management |

| Other Applications |

| Original Equipment Manufacturers |

| Tier 1 and Tier 2 Suppliers |

| Dealerships and Distributors |

| Fleet Operators |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Application | Production Planning and Scheduling | |

| Supply Chain and Inventory Management | ||

| Finance and Accounting | ||

| Human Resources and Payroll | ||

| Quality Management | ||

| Customer Relationship Management | ||

| Other Applications | ||

| By End User | Original Equipment Manufacturers | |

| Tier 1 and Tier 2 Suppliers | ||

| Dealerships and Distributors | ||

| Fleet Operators | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is cloud adoption progressing among automotive ERP buyers?

Cloud deployments already represent 62% of spending in 2025 and are forecast to advance at a 13.40% CAGR through 2031 as buyers pursue artificial intelligence and Internet of Things capabilities.

Which region is growing the quickest in automotive ERP demand?

Asia-Pacific is projected to register an 11.90% CAGR through 2031, driven by China's vast production scale and domestic vendor support, along with Indias rapidly digitizing supplier base.

Why are fleet operators investing in ERP solutions?

Electric vehicle fleets need real-time battery state-of-health data and predictive maintenance scheduling, leading to a 15.00% CAGR for fleet operator ERP spending to 2031.

What application area inside ERP is expanding the fastest?

Quality management modules are growing at a 14.20% CAGR through 2031 due to stricter certification and digital product passport requirements.

How are cybersecurity concerns influencing ERP procurement?

Buyers now insist on ISO 27001 and SOC 2 Type II certifications plus rapid recovery objectives, shifting vendor selection criteria toward operational resilience as much as feature depth.

Which deployment model provides the lowest total cost of ownership for small suppliers?

Subscription-based cloud suites reduce upfront license fees and eliminate data-center capital outlays, though suppliers must weigh lifetime subscription charges against depreciated on-premises assets.

Page last updated on: