Enterprise Resource Planning Managed Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

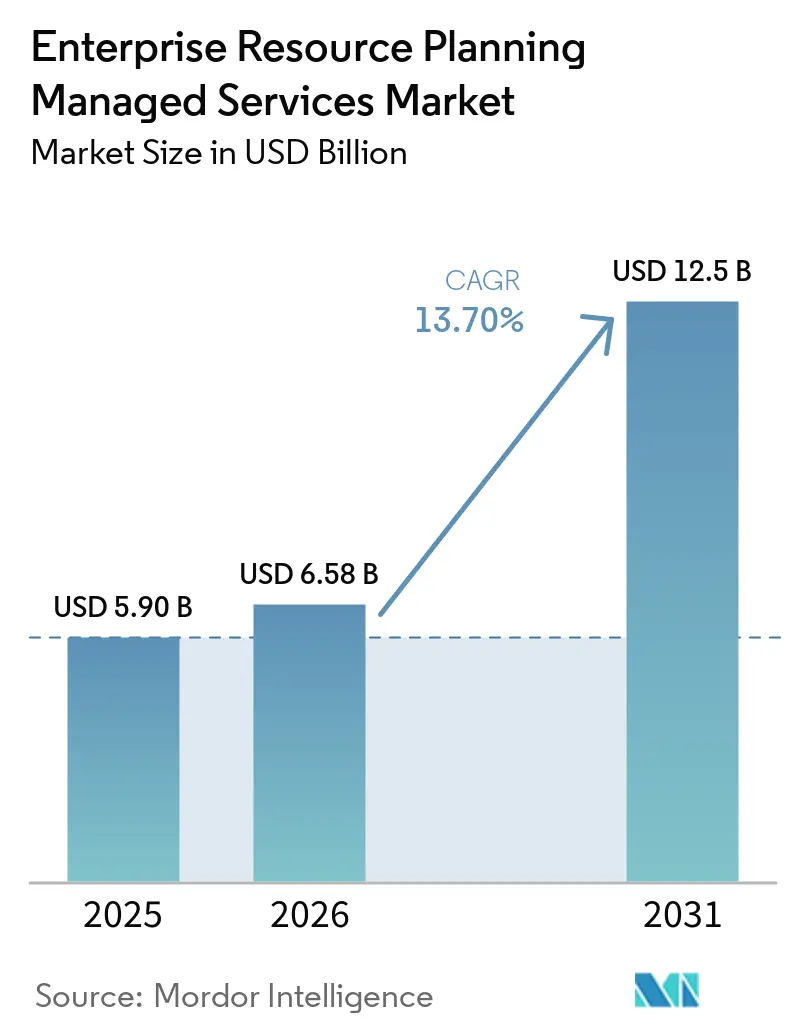

| Market Size (2026) | USD 6.58 Billion |

| Market Size (2031) | USD 12.5 Billion |

| Growth Rate (2026 - 2031) | 13.70% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

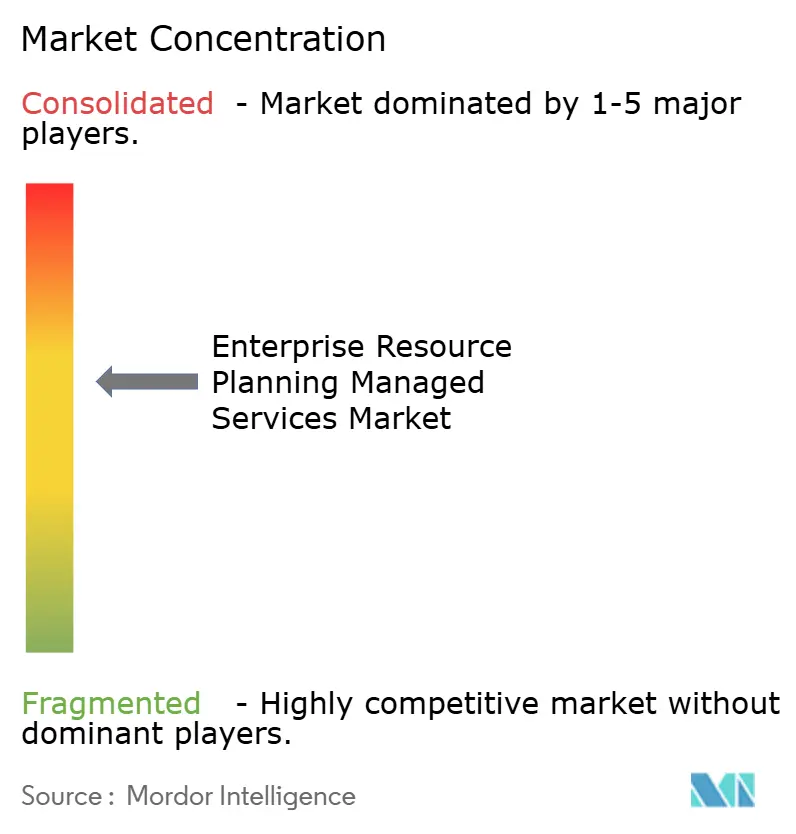

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Resource Planning Managed Services Market Analysis by Mordor Intelligence

The ERP managed services market size is projected to be USD 5.90 billion in 2025, USD 6.58 billion in 2026, and reach USD 12.50 billion by 2031, growing at a CAGR of 13.7% from 2026 to 2031. Surging demand for cloud subscription models, embedded artificial intelligence, and outcome-based contracts is transforming formerly capital-intensive ERP ownership into a predictable operating expense. Strategic alliances among hyperscalers and system integrators are accelerating multi-country ERP rollouts on sovereign clouds, while continuous optimization services that tie fees to measurable business results are redefining buyer expectations. At the same time, real-time analytics, Scope 3 sustainability telemetry, and AI-assisted automation have become table-stakes capabilities, sharpening the competitive contrast between full-service global integrators and niche compliance specialists.

Key Report Takeaways

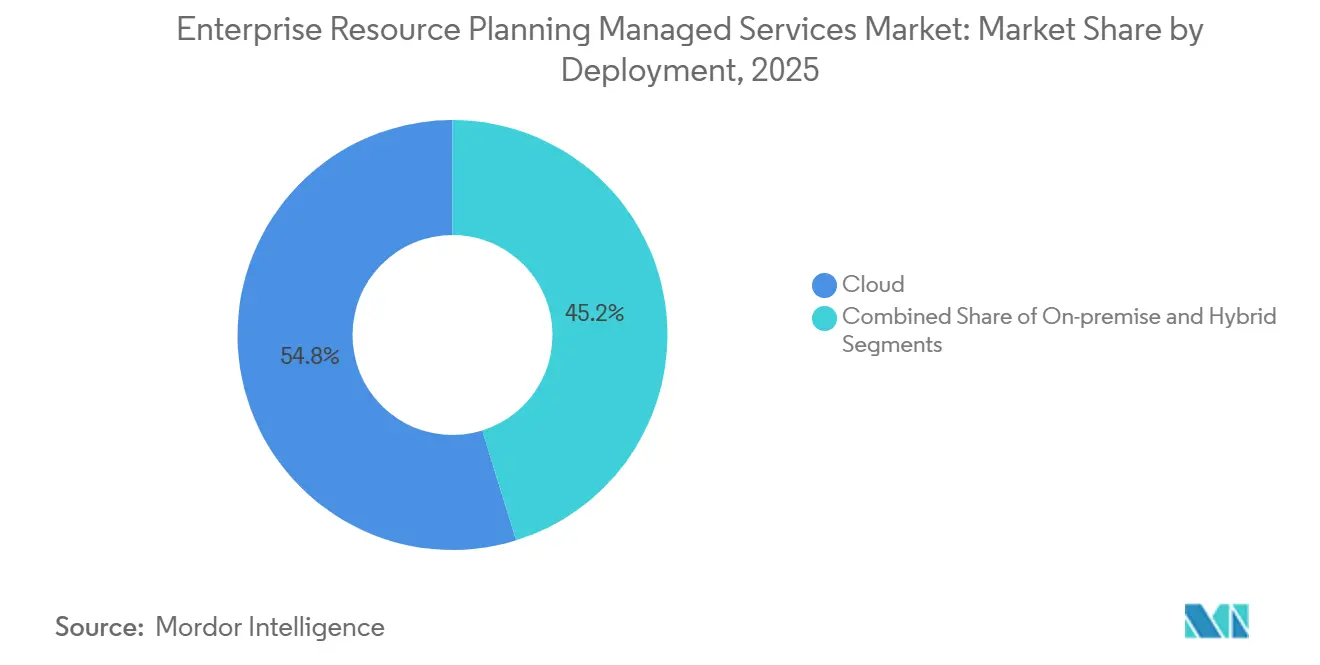

- Cloud deployment captured 54.8% of the ERP managed services market share in 2025, and its 12.9% CAGR keeps it the clear leader through 2031.

- Small and medium enterprises are advancing at a 14.2% CAGR, the fastest of any enterprise-size cohort, even though large enterprises retained 63.5% share in 2025.

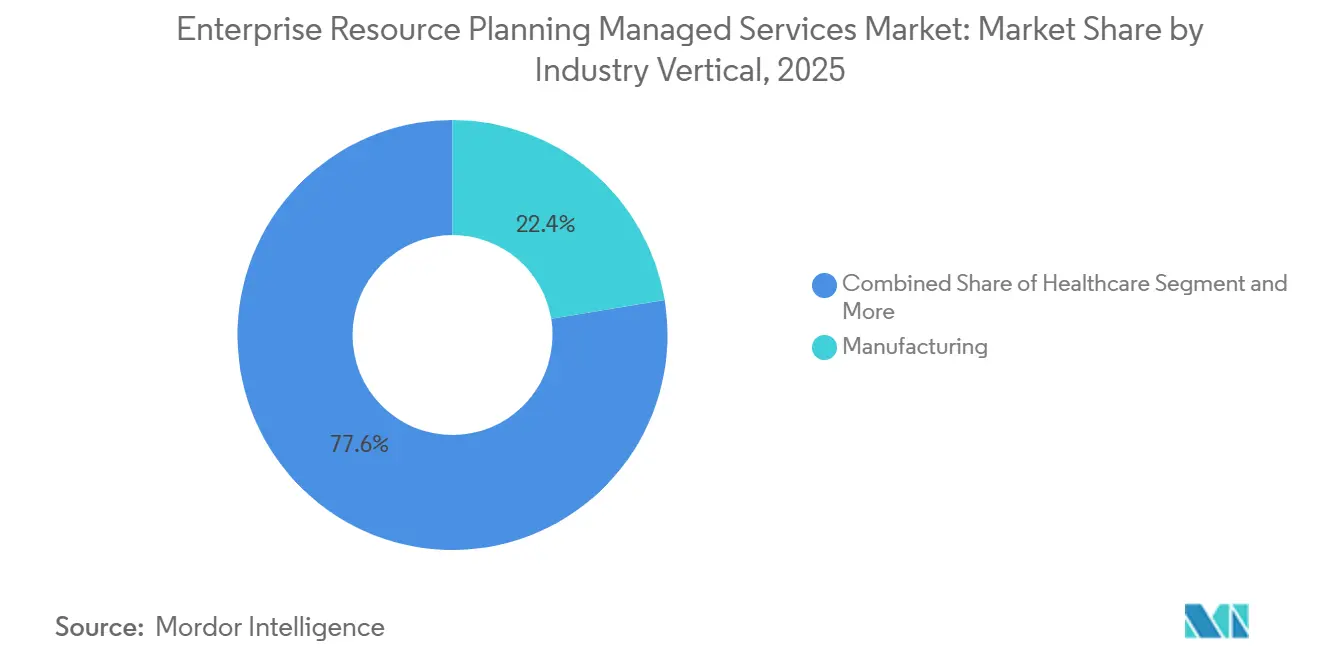

- Manufacturing led all verticals with 22.4% revenue share in 2025, while healthcare is forecast to expand at 12.8% CAGR to 2031.

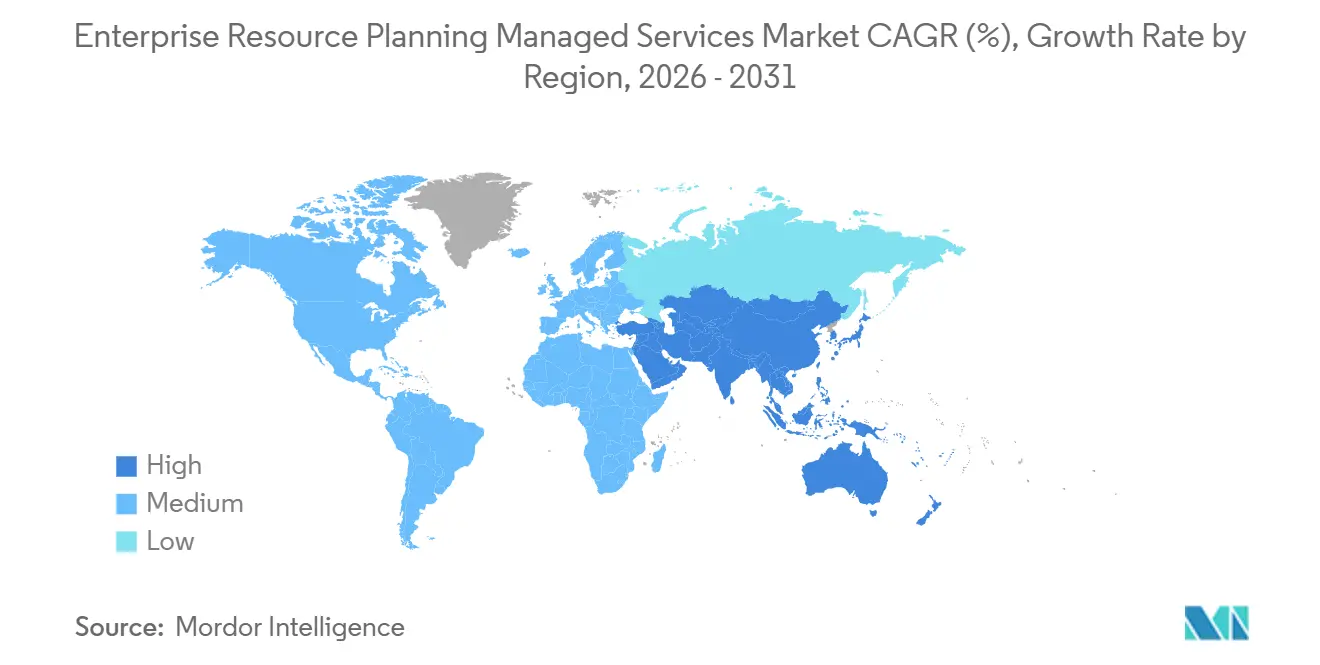

- North America accounted for 34.1% of 2025 revenue, yet Asia-Pacific is projected to grow at 13.6% CAGR, the highest regional pace through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Enterprise Resource Planning Managed Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Cloud-Based ERP Solutions | +3.8% | Global, strongest in Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Increasing Need to Reduce IT Infrastructure Costs | +2.9% | Global, acute among cost-sensitive small and medium enterprises | Short term (≤ 2 years) |

| Rising Demand for Real-Time Data Analytics | +2.4% | North America, Europe, Asia-Pacific manufacturing and BFSI | Medium term (2-4 years) |

| Growing Complexity of ERP Landscapes Due to Multi-Vendor Ecosystems | +1.9% | Global, concentrated in large enterprises with legacy portfolios | Long term (≥ 4 years) |

| Emergence of AI-Driven Autonomous ERP Operations | +1.6% | North America, Europe early adopters; Asia-Pacific following | Medium term (2-4 years) |

| Vendor Push for Outcome-Based Managed Service Contracts | +1.1% | North America, Europe mature markets; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Cloud-Based ERP Solutions

More than 70% of enterprises now operate at least one core ERP module in the cloud, and 75% of new buyers favor cloud-native architectures over on-premises deployments. Hyperscaler partnerships bundle ERP subscriptions with infrastructure credits and AI services, as demonstrated by SAP’s RISE offering on IBM Power Virtual Server, while Oracle Cloud Infrastructure revenue surged 52% in fiscal 2025 on the back of ERP migrations. Sovereign-cloud mandates in China and the European Union drive multi-region, legally isolated ERP instances that still enable cross-border analytics through federated data models. Consumption-based pricing and 90-day deployment frameworks, such as Unit4’s Success4U, are unlocking the mid-market, forcing service providers without deep hyperscaler alliances or compliance-ready delivery models to cede share.[1]Sean Mitchell, “Unit4 Makes Success4U Default Model for ERPx Delivery,” IT Brief US, itbrief.news

Increasing Need to Reduce IT Infrastructure Costs

Subscription-driven managed services are replacing fixed infrastructure outlays, converting data-center depreciation into operating expense and trimming total IT spend by up to 30% in documented cases such as IBM’s 150,000-user internal migration to SAP S/4HANA Cloud.[2]IBM Services, “SAP S/4HANA Migration Case Study,” IBM, ibm.com Government buyers are following suit: the U.S. Defense Logistics Agency issued a USD 903 million, seven-year contract that shifts budget-predictability risk to service providers while mandating 99.9% availability and FedRAMP IL4 compliance.[3]U.S. Defense Logistics Agency, “RFP-ERP Cloud Hosting and Subscription Licenses with Managed Services,” console.sweetspotgov.com Small and medium enterprises alone will direct more than USD 90 billion to managed IT services through 2026, lured by fixed-fee models that eliminate the need for in-house ERP teams. The countertrend is a rising unit cost for multi-cloud-certified ERP specialists, compelling providers to invest in reskilling and AI delivery platforms to protect margins.

Rising Demand for Real-Time Data Analytics

Enterprises now expect sub-second analytics, predictive forecasts, and autonomous workflows from managed ERP environments. AI agents deliver 20%-30% operational efficiency by triaging incidents, predicting capacity bottlenecks, and recommending fixes before service-level breaches.[4]Capgemini Institute, “Future of ADM Services,” Capgemini, capgemini.com The U.S. Air Force’s USD 88 million task order extends Oracle Cloud Infrastructure and AI Database 26ai to classified networks, showing defense-grade ambition for agentic ERP workflows. Manufacturers integrate production telemetry with ERP financials to raise plant utilization by up to 20%, while BFSI firms slash regulatory-reporting cycles from weeks to hours using in-memory analytics. Providers differentiating on business observability, where engineering metrics directly connect to revenue at risk, are poised to secure gain-share contracts linking fees to measurable outcomes.

Growing Complexity of ERP Landscapes Due to Multi-Vendor Ecosystems

The typical large enterprise now juggles 10 or more ERP-adjacent integrations, each costing USD 30,000-USD 100,000 to build and up to USD 200,000 per year to maintain. A February 2026 TCS-ServiceNow alliance promises low-code integration templates that cut time-to-integrate by as much as 40%. China’s dual-ERP architecture, domestic software for administrative compliance, and SAP S/4HANA for global operations, is the legal and technical knot that drives demand for specialized managed services. Providers offering pre-built connectors and composable integration layers have a strategic edge, while clients that fail to negotiate portable integration intellectual property become captive to incumbent partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Security and Privacy Concerns in Outsourced Environments | -1.8% | Global; highest in Europe (GDPR), North America (CCPA), Asia-Pacific (PIPL) | Short term (≤ 2 years) |

| High Switching Costs and Vendor Lock-In | -1.4% | Global, concentrated in large enterprises with legacy customizations | Long term (≥ 4 years) |

| Shortage of Domain-Specific ERP Talent in Service Providers | -1.1% | Europe, North America, spillover to Asia-Pacific | Medium term (2-4 years) |

| Rising Scrutiny of Scope 3 Emissions from Outsourced IT Operations | -0.6% | Europe and North America early movers; expanding to Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Security and Privacy Concerns in Outsourced Environments

The July 2024 Smart ERP Solutions breach exposed 79,000 personal records and triggered EUR 480,000 (USD 540,000) in GDPR fines, plus nearly EUR 840,000 (USD 945,000) in lost business, illustrating how a single incident can erase multiple years of managed-service fees. Zero-day exploits in SAP NetWeaver prompted clients to adopt 24x7 managed security services with continuous penetration testing and zero-trust architectures. Public-sector solicitations now stipulate sovereign-cloud deployment, government-owned encryption keys, and U.S.-citizen staffing, raising the compliance bar for providers. Vendors lacking ISO 27001 certification or cyber-insurance will struggle to pass procurement gates in regulated verticals.

High Switching Costs and Vendor Lock-In

Full replacement of a customized ERP estate can demand USD 10 million-USD 30 million and 18-48 months, locking enterprises into underperforming providers. Oracle ERP Cloud deployments for 1,000 users show a five-year total cost of ownership at USD 40 million-USD 55 million, with integrator services often eclipsing subscription fees. Clean-core remediation, code refactoring, and side-by-side extensions add USD 2 million to USD 5 million in consulting outlays, as seen in China’s legally isolated dual-ERP models. Strategic countermeasures include composable architectures, open-API standards, and exit clauses capping transition costs at 10%-15% of annual contract value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Dominance Reshapes Service Economics

Cloud solutions accounted for 54.8% of the ERP managed services market in 2025 and are on track to expand at a 12.9% CAGR through 2031. Oracle Cloud Infrastructure’s FY 2025 revenue surge, SAP’s RISE migrations, and Alibaba Cloud sovereign deployments in China confirm that subscription pricing, automatic updates, and hyperscaler AI services are now decisive purchase criteria. While on-premises deployments linger in defense and critical-infrastructure sectors that require air-gapped security, even those buyers are layering cloud-based analytics on top of core financial systems. Hybrid configurations blending public cloud for innovation workloads with private or sovereign cloud for regulated data are steadily growing, demanding orchestration skills that only a subset of providers possess.

Margins in legacy on-premises arrangements are pinched as vendors funnel Research and Development to cloud-native functionality, pushing customers toward migration. Meanwhile, managed service practices that combine compliance tooling, modular upgrades, and gain-share economics are capturing wallet share from traditional application management contracts. As a result, the ERP managed services market is tilting decisively toward cloud-centric frameworks, and providers without hyperscaler certifications risk obsolescence.

By Enterprise Size: SMEs Drive Volume Growth

Large enterprises accounted for 63.5% of 2025 revenue and continue to command the highest absolute budgets, yet the small and medium enterprise cohort is accelerating at a 14.2% CAGR, outpacing every other buyer group. Unit4’s 90-day Success4U package, Oracle’s NetSuite for Government contract with 40 U.S. transit agencies, and Microsoft Copilot rollouts in Indian mid-market clients demonstrate how pre-configured templates and AI-assisted setup are shrinking deployment cycles. The ERP managed services market share for SMEs is projected to climb steadily as consumption-based licensing, fixed-fee support, and self-service portals remove historic entry barriers.

In contrast, large enterprises seek multi-module suites, global delivery coverage, and vertical IP that support gain-share contracts tied to business KPIs. They negotiate multi-year deals exceeding USD 100 million in total contract value, creating high switching costs but also imposing stringent service-level and innovation requirements. Providers must therefore operate bifurcated models: productized offerings for volume-driven SME accounts and highly customized, relationship-intensive engagements for Fortune-1000 clients. The ERP managed services industry that masters both motions will capture disproportionate growth.

By Industry Vertical: Healthcare Outpaces Manufacturing

Manufacturing retained a 22.4% revenue lead in 2025, reflecting its need for multi-site planning, quality management, and supply-chain visibility. Yet healthcare is forecast to grow 12.8% CAGR to 2031, propelled by value-based care mandates, interoperability rules, and real-time clinical analytics. Capgemini’s USD 3.3 billion acquisition of WNS aims at integrating financial, supply-chain, and clinical data into a unified managed service, illustrating how domain expertise and AI-powered analytics are now decisive. The ERP managed services market for healthcare applications is expected to double over the forecast horizon as providers replace fragmented, legacy systems.

Other verticals are adding momentum. BFSI buyers demand real-time fraud analytics and regulatory reporting that compresses cycle times from weeks to hours. Retailers emphasize omnichannel inventory and sustainability tracking, while energy utilities adopt composable ERP to manage distributed resources. Government entities such as the City of Atlanta pursue unified platforms that promise USD 17.5 million in ten-year savings. This diversity of domain-specific requirements elevates the value of vertical accelerators and compliance architectures within managed service portfolios.

Geography Analysis

North America generated 34.1% of global revenue in 2025, anchored by federal modernization programs and well-established outcome-based procurement frameworks. The Defense Logistics Agency’s USD 903 million contract and Estée Lauder’s USD 500 million partnership with Accenture typify multi-year deals that integrate AI automation and sovereign-cloud compliance. Strong capital pools and mature vendor ecosystems sustain growth, even as labor shortages drive up the cost of certified ERP talent.

Asia-Pacific is the fastest-growing region, with a 13.6% CAGR, driven by China’s Xinchuang mandates, India’s mass deployment of Microsoft Copilot licenses, and Japan’s shift from legacy ECC systems to S/4HANA. The ERP managed services market in China alone reached USD 3.40 billion in 2025, with domestic vendors Yonyou and Kingdee capturing the bulk of state-owned enterprise spend, while multinational corporations rely on SAP via Alibaba Cloud sovereign instances. India’s tier-1 integrators are exporting low-cost, AI-enabled support tooling worldwide, turning the subcontinent into the labor fulcrum of global delivery.

Europe shows slower topline growth but acute talent scarcity, with S/4HANA specialists now taking 90 days to recruit. Mandatory e-invoicing in France by September 2026 and Digital Product Passport requirements in energy utilities create compliance-driven demand spikes. South America, the Middle East, and Africa remain nascent but opportunity-rich, particularly where localization templates for tax, payroll, and customs are scarce. Providers that can orchestrate multi-country rollouts with continuous compliance updates will unlock first-mover advantages across these emerging regions.

Competitive Landscape

Global system integrators—Accenture, IBM, Deloitte, Capgemini, TCS, Infosys, Cognizant, Wipro, and HCL—collectively hold just above one-third of worldwide revenue, signaling a moderately fragmented arena in which differentiation now turns on vertical IP, AI-enabled automation, and sovereign-cloud certifications. Capgemini’s acquisition of WNS extends its reach into business-process operations, enabling bundled ERP, analytics, and BPO offerings that support gain-share pricing models. Cognizant’s recognition in the ISG Oracle Cloud Ecosystem report, citing 99.99% payroll match and a 40% reduction in manual effort, highlights the competitive power of third-party validation.

Niche providers are carving defensible positions with compliance accelerators, localization-as-a-service offerings, and Workday-native business-process services. OneSource Virtual reduced client billing cycles by 60% through specialized automation, while Syntax Systems leverages SAP-certified private-cloud hosting to win heavily customized workloads. Meanwhile, hyperscalers are deepening co-sell programs that reward partners for ERP migrations, compressing sales cycles and creating virtuous loops of infrastructure and service revenue.

Technology leadership now depends on generative AI integration and end-to-end observability. Microsoft’s December 2025 deployment of 200,000 Copilot licenses across Indian IT firms exemplifies the shift toward AI-assisted service desks that auto-resolve incidents. Providers unable to embed ISO 27001 compliance, cyber-insurance, and audited security into their operating models will struggle to penetrate regulated industries increasingly sensitized by high-profile breaches.

Enterprise Resource Planning Managed Services Industry Leaders

Accenture plc

International Business Machines Corporation

Deloitte Touche Tohmatsu Limited

Capgemini SE

Tata Consultancy Services Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Wipro introduced its AI-DC Solution with NVIDIA hardware to deliver real-time analytics and large-language-model integration for ERP workloads.

- March 2026: Wipro secured a multi-year managed services deal with TruStage to modernize retirement-services operations.

- February 2026: Accenture won a USD 500 million, five-year contract with Estée Lauder to migrate global ERP to cloud platforms and embed AI-driven supply-chain optimization.

- February 2026: TCS and ServiceNow announced a strategic partnership to unify workflows across ERP, CRM, and IT operations with enterprise AI solutions.

Global Enterprise Resource Planning Managed Services Market Report Scope

The ERP Managed Services market refers to the ecosystem of outsourced services that provide ongoing management, monitoring, maintenance, and optimization of Enterprise Resource Planning (ERP) systems on behalf of organizations.

The ERP Managed Services Market Report is Segmented by Deployment Model (On-Premises, Cloud, Hybrid), Enterprise Size (Small and Medium Enterprises, Large Enterprises), Industry Vertical (Manufacturing, Retail and Consumer Goods, Healthcare, BFSI, IT and Telecom, Government and Public Sector, Energy and Utilities, Transportation and Logistics, Other Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| On-Premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Manufacturing |

| Retail and Consumer Goods |

| Healthcare |

| Banking, Financial Services and Insurance (BFSI) |

| Information Technology and Telecom |

| Government and Public Sector |

| Energy and Utilities |

| Transportation and Logistics |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Industry Vertical | Manufacturing | |

| Retail and Consumer Goods | ||

| Healthcare | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Information Technology and Telecom | ||

| Government and Public Sector | ||

| Energy and Utilities | ||

| Transportation and Logistics | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the ERP managed services market in 2031?

The market is forecast to reach USD 12.50 billion by 2031, reflecting a compound annual growth rate of 13.7% from 2026 to 2031.

Which deployment model is growing fastest in managed ERP services?

Cloud deployment is expanding at a 12.9% CAGR, well ahead of on-premises and hybrid models.

Why are small and medium enterprises accelerating adoption?

Consumption-based pricing, AI-assisted configuration, and 90-day deployment frameworks are lowering barriers and driving a 14.2% CAGR among SMEs.

Which vertical will see the highest growth through 2031?

Healthcare is projected to grow at 12.8% CAGR as providers modernize for value-based care and real-time analytics.

What regions promise the most growth?

Asia-Pacific leads with a 13.6% CAGR, buoyed by sovereign-cloud mandates in China and large-scale modernization in India and Japan.

How concentrated is the competitive landscape?

The market scores a 6 on a 1-10 scale, with the top five firms holding about 60% of global revenue.

Page last updated on: